Market Movers: Citizen Dividends

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 8 minutes

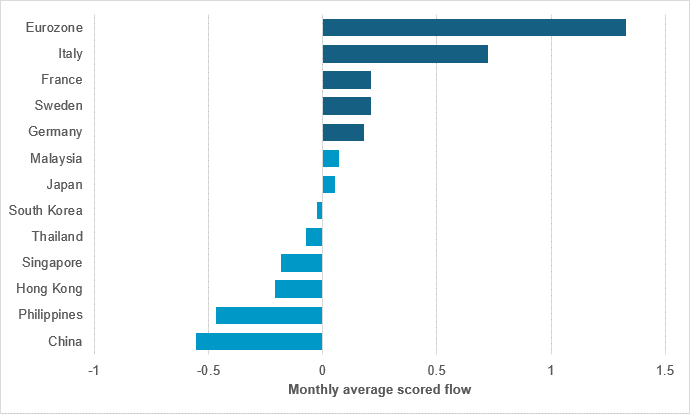

Sharp falls in real rates undermining APAC fixed income flow

Source: BNY

Chinese inflation data are starting to materially surprise to the upside, and a U.S./AI-centric market is looking for potential opportunities to diversify exposure, especially with Europe still stuck in stagflation fears. In fairness, on a base effect and cyclical basis markets were expecting China to help drive some reflation in the region at the beginning of the year. This would have allowed some real effective exchange rate gains and driven steepening across the region if Beijing were to start exporting inflation. The conflict has just accelerated that process. Normally, higher yields tend to encourage international flows, especially given the strong savings positions across APAC. However, the current fear is that the combined shock (supply and Chinese exports becoming more expensive) is so sudden such that balances of payments in the region are unable to adjust. In other words, the steepening is more pernicious in terms of asset allocation and will materially drive down real rates.

Flows in sovereign bonds of “funders” without any form of commodity backing show the preference for Europe vs. APAC. Every single core European funder was net bought over the past month, while Malaysia and Japan were the only APAC names with some purchases, and those were marginal at best. Clearly, the balance of payments story remains highly potent and the market is opting for further steepening risk rather than trying to capture “value” in high yields.

U.K. Prime Minister Sir Keir Starmer faced his cabinet overnight and pledged to stay in office, as more members of the ruling Labour Party called upon him to set a timeline for an orderly exit as leader. A junior minister also resigned, and his spokesperson refused to rule out a resignation when speaking to the press before the cabinet meeting. It is clear that Starmer’s speech yesterday failed to inspire the Parliamentary Labour Party (PLP) to rally around his leadership following very poor results in the local elections. At the latest count, over 70 MPs are calling for a timeline, not far off the figure needed to trigger an outright leadership challenge. For now, it appears a managed exit is the preferred option for the PLP. U.K. borrowing costs have continued to rise in this uncertain political context, as the market prices in a shift to the left and higher government spending under a future administration. FTSE 100 -0.87% to 10180, GBPUSD -0.457% to 1.3527, 10y gilt +10.2bp to 5.1%.

Japanese Finance Minister Satsuki Katayama has confirmed close coordination with U.S. Treasury Secretary Scott Bessent on currency policy. She reaffirmed adherence to last September’s joint statement, which allows currency intervention to address excessive FX volatility. This follows suspected large-scale yen intervention by Japan in late April, estimated at around $24.7bn plus $30bn in follow-up operations. The two officials also discussed broader issues including China’s unfair restrictions on critical minerals exports to Japan, AI technology risks, and ongoing trade and investment cooperation. Bessent’s visit underscores strong U.S.-Japanese collaboration amid regional economic and geopolitical challenges. Nikkei +0.52% to 62743, USDJPY -0.21% to 157.47, 10y JGB +3.5bp to 2.558%.

Australia’s 2026-27 budget projects an underlying cash deficit of AU$31.5bn (1% of GDP), above the median estimate of AU$25bn, with a similar shortfall of AU$31bn in 2027-28 (from AU$28.3bn in 2025-26). The budget aims to return to balance by 2034-35. Net debt is expected to rise to 19.9% of GDP by June 2027 (from 18.8% currently) and reach 21.9% by 2029-30. GDP growth is forecast at 2.25% in 2025-26, slowing to 1.75% in 2026-27 then rebounding to 2.25% in 2027-28. CPI inflation is expected to ease to 2.5% in 2026-27 (from 5% in 2025-26). The unemployment rate is projected at 4.5%, with wages rising 3.5% p.a. over the next three years. ASX -0.89% to 5472, AUDUSD -0.318% to 0.722, 10y ACGB +4bp to 5.032%.

South Korea’s KOSPI plunged over 5% intraday and closed 2.3% lower following remarks by Kim Yong-beom, presidential chief of staff for policy, proposing an “AI national dividend” that would redistribute excess tax revenue from the AI industry to citizens. The initial statement sparked investor concerns over potential windfall taxes on AI profits, causing significant market volatility. Kim later clarified that no new tax would be imposed, and the proposal referred only to using naturally increased tax revenue. The episode highlighted the public debate over the economic impact of AI and income inequality in South Korea. Market sentiment partially recovered after the clarification, and the South Korean president noted that Kim’s comments represented his “personal views.” KOSPI -2.29% to 7643, USDKRW -1.128% to 1489.3, 10y KTB +4.6bp to 3.95%.

India is considering emergency measures to protect foreign exchange reserves amid rising oil prices and a widening current account deficit. Proposed steps include hiking fuel prices for the first time since the Iran conflict began, restricting non-essential imports such as gold and electronic goods, and encouraging public fuel conservation. Prime Minister Narendra Modi has urged citizens to avoid gold purchases for a year and to limit overseas travel. The Reserve Bank of India (RBI) has intervened to stabilize the rupee, which hit a record low, and may tighten currency hedging rules for importers. Foreign exchange reserves stood at $690.7bn as of May 1. SENSEX -1.36% to 74980, USDINR -0.448% to 95.74, 10y INGB +1.3bp to 7.045%.

U.S. April NFIB Small Business Optimism is expected to rise to 96.1 vs. 95.8.

U.S. April CPI is expected at 0.6% m/m, 3.7% y/y vs. 0.9% m/m, 3.3% y/y in March. April Core CPI is expected at 0.3% m/m, 2.7% y/y vs. 0.2% m/m, 2.6% y/y in March.

U.S. real average hourly and weekly earnings may soften from 0.2% y/y and 0.1% y/y, respectively, in March.

NY Fed Quarterly Report on Household Debt and Credit

U.S. Treasury sells $80bn in 6-week bills, $50bn in 52-week bills and $42bn in 10y notes.

Central bank speakers: The Fed’s Austan Goolsbee speaks at the Greater Rockford Chamber of Commerce.

Mood: iFlow mood deteriorated further to -0.05, reflecting a defensive tilt, with rising demand for core government bonds alongside reduced global equity flows.

FX: Broad-based, moderate outflows from other currencies into USD. GBP, EUR and SGD saw the heaviest selling, with EUR positioning moving deeper into underheld territory.

FI: Mixed, moderate flows. Selling pressure in Australian government bonds contrasted with buying in Eurozone, Swedish and Hungarian government bonds and U.K. gilts.

Equities: Strong inflows into U.S., Chinese and Thai equities, offset by outflows from Europe, the U.K. and South Korea. Within DM, buying was concentrated in industrials, IT, healthcare and energy, while materials, consumer discretionary and real estate saw light selling.

“Never doubt that a small group of thoughtful, committed citizens can change the world; indeed, it’s the only thing that ever has.” – Margaret Mead

“The world is my country, all mankind are my brethren, and to do good is my religion.” – Thomas Paine

German inflation for April was confirmed at 2.9% y/y, accelerating from 2.7% in March and 1.9% in February, while prices rose 0.6% m/m. The pickup was primarily driven by energy, with prices up 10.1% y/y, reflecting higher fuel costs linked to geopolitical tensions in the Middle East. Food inflation remained subdued at 1.2%, while core inflation was 2.3%, indicating more moderate underlying price pressures. Services inflation was 2.8%, supported by rises for transport and social services. Despite sharp increases in fuel and heating oil, some household energy components saw falls, partially offsetting the overall impact. DAX -0.86% to 24140, EURUSD -0.162% to 1.175, 10y Bund +4.5bp to 3.085%.

Germany’s ZEW investor expectations index for May improved to -10.2 from -17.2 in April, significantly outperforming expectations of a decline. Meanwhile, the current conditions index weakened further to -77.8, highlighting continued divergence between sentiment and actual activity. The bounce-back in expectations rebound reflects fewer respondents anticipating a deterioration, while current assessments remain overwhelmingly negative. The sector breakdown shows a mixed outlook: strong optimism in information technology, with a balance of 56.6, and solid sentiment in utilities and construction contrast with deep pessimism in cyclicals such as automobiles at -57.2, chemicals at -42.7 and retail at -41.6. Financials remain relatively resilient, with positive balances for banks and insurers. Overall, forward-looking sentiment is stabilizing, but sector dispersion and weak current conditions signal fragile recovery dynamics.

Italy’s industrial production rose by 0.7% m/m in March, marking a second consecutive increase, while output declined by 0.2% q/q in Q1. The m/m gain was driven by capital goods (+2.1%) and intermediate goods (+0.3%), while consumer goods and energy fell by 0.4% and 1.2%, respectively. On a calendar-adjusted y/y basis, production increased by 1.5%, supported by strong growth in capital goods at 5.8% and partly offset by declines in consumer goods and energy. By sector, transport equipment and electronics led gains, while chemicals and energy recorded the largest contractions, indicating uneven industrial momentum. FTSE MIB -1.07% to 49132, EURUSD -0.314% to 1.1746, 10y BTP +9bp to 3.865%.

U.K. BRC same-store sales fell 3.4% y/y in April, with food down 3.1% and non-food down 3.6%. This was attributable to the timing of Easter, with food sales most affected. Weak consumer confidence amid concerns over cost-of-living increases caused by the Middle East also restrained spending. Big-ticket items, including furniture, saw reduced demand, while uncertainty around summer holidays dampened discretionary purchases. Non-food sales fell 3.3% y/y, with online sales outperforming physical stores, pushing online penetration to its highest level this year. Retailers anticipate a boost from the upcoming World Cup, with early signs of increased demand for TVs and sound systems. FTSE 100 -0.87% to 10180, GBPUSD -0.457% to 1.3527, 10y gilt +10.2bp to 5.1%.

Switzerland’s producer and import price index rose by 0.8% m/m in April to 100.5 points, but was still down 2.0% y/y, as annual deflation persisted despite the recent momentum. The m/m increase was driven by higher prices for petroleum products, crude oil and gas, alongside gains for metals and intermediate goods, with import prices rising more sharply at 2.3% m/m. In contrast, some categories such as raw milk, medical goods and machinery recorded lower prices. The producer price index increased by a modest 0.2% m/m, while import prices showed stronger volatility. Overall, energy-related components were the dominant driver of short-term price dynamics, while broader price pressures remained subdued. SMI -0.58% to 13026, EURCHF -0.052% to 0.91678, 10y Swiss GB +1.3bp to 0.422%.

Norway’s household expectations indicator deteriorated sharply in Q2: the seasonally adjusted main index fell to -20.0 points from -12.4 in Q1 and -4.1 three quarters earlier, signaling a broad-based return of pessimism. The decline reflects widespread concern over geopolitical tensions and rising prices, with sentiment weakening across income groups, ages and regions. Subcomponents show particularly negative views on the national economy, with assessments of the past year at around -47 and expectations for the next year near -35, both close to historical lows. Households also turned slightly negative on their own financial outlook. Despite weak sentiment, underlying conditions remain relatively resilient, supported by low unemployment and solid wage growth, limiting immediate financial stress. OSE +0.55% to 1988, EURNOK +0.331% to 10.7899, 10y NGB +5.4bp to 4.492%.

The Czech unemployment rate declined to 4.9% in April, down 0.1 percentage points from March, reflecting seasonal hiring and continued labor market resilience. The number of registered jobseekers reached 364,472, higher than a year earlier, while vacancies increased to 94,483, indicating sustained labor demand. Around 42,774 individuals were newly registered during the month, and nearly 39,500 found employment, with hiring concentrated in the manufacturing, trade and services sectors. By region, unemployment remained highest in industrial areas, while most districts recorded m/m falls. Despite the modest improvement, the ratio of jobseekers to vacancies remains high, pointing to persistent mismatches in the labor market. Prague SE -0.39% to 2518, EURCZK +0.029% to 24.331, 10y CZGB +6.6bp to 4.953%.

South Africa’s unemployment rate rose to 32.7% in Q1, up from 31.4% in Q4 2025, reflecting a deterioration in labor market conditions. Employment declined by 345,000 to 16.8 million, while the unemployment count increased by 301,000 to 8.1 million, resulting in a slight contraction in the labor force. Broader measures also weakened, with the combined unemployment and underemployment rate rising to 35.9% and the expanded unemployment measure reaching 43.7%. The potential labor force increased to 4.9 million, driven by a rise in discouraged jobseekers, highlighting growing labor market detachment. Overall, the data indicate worsening employment dynamics and persistent structural slack in the economy. JSE TOP 40 -1.54% to 109034, USDZAR +0.661% to 16.5403, 10y SAGB +9.2bp to 8.939%.

Japan’s March Household Survey shows that real consumption expenditure per household (two or more people) fell 2.9% y/y (-1.3% m/m, seasonally adjusted) to ¥334,701. Nominal consumption also fell 1.3% y/y. Real income for worker households rose 4.7% y/y after adjusting for CPI excluding imputed rent, and 4.8% y/y using overall CPI, with nominal income up 6.4% y/y to ¥557,663 per household. Key declines were seen in transport and communication (-16.8% y/y), food (-2.9% y/y), fuel, light and water (-3.2% y/y) and clothing and footwear (-2.6% y/y). Conversely, medical care spending rose 20.1% y/y and housing increased by 15.3% y/y. Nikkei +0.52% to 62743, USDJPY -0.21% to 157.47, 10y JGB +3.5bp to 2.558%.

Japan’s coincident index rose by 0.3 points m/m to 116.5 in March. The leading index was up 1.3 points m/m to 114.5, continuing a 10-month rise, while the lagging index posted a third successive m/m rise (+0.5 points to 113.4). Positive contributions came from the export quantity index and shipments of industrial production goods. The overall assessment indicates an upward phase shift in the economic cycle, reflecting improving economic conditions after recent fluctuations.

The BoJ’s Summary of Opinion for its April policy meeting heralds the prospect of rate increases in upcoming meetings. The BoJ acknowledges that underlying CPI inflation is nearing 2% and real interest rates are very low, supporting continued policy rate hikes to adjust monetary accommodation based on economic and price developments. Despite stable economic growth at close to potential, risks of upward price deviations persist. Inflation expectations remain adaptive, and a strong wage-price spiral is unlikely. The BoJ emphasized its role in price stability, aiming to normalize rates gradually while monitoring risks to economic activity and inflation.

Australia’s NAB Monthly Business Survey for April showed purchase cost growth surging to 4.5% q/q, outpacing product price growth at 1.8% q/q and squeezing margins. Business conditions were down 3 points to +3, while confidence improved by 5 points to -24. Forward orders dropped 4 points in April, down 11 since February. Capex fell 8 points in the largest m/m decline since COVID. The manufacturing and construction sectors face extreme margin pressure, with purchase costs exceeding price growth by 3.4 percentage points and 3.8 percentage points, respectively. Capacity utilization eased to 82.5%, the lowest since July 2025 but still above average. Rising costs and weakening demand signal a tougher operating environment amid energy price shocks. ASX -0.89% to 5472, AUDUSD -0.318% to 0.722, 10y ACGB +4bp to 5.032%.

Thai consumer confidence fell to 50.6 points in April from 51.8 in March. The present conditions index fell to 34.7 (35.9 in March), while future expectations dropped to 58.3 (59.7 in March). The economic conditions, employment and future income indices also decreased m/m. All sub-indices remain below the neutral level of 100, indicating negative consumer sentiment. This marks a continued downward trend in confidence since February (53.7). SET -0.17% to 1487, USDTHB +0.047% to 32.408, 10y TGN -0.9bp to 2.15%.