Market Movers: Changing the Story

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 7 minutes

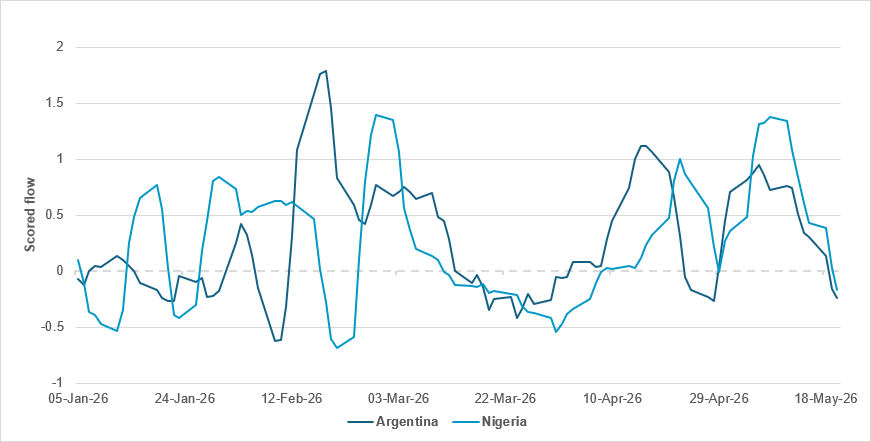

Strong fixed income flows into Argentina and Nigeria point to geography and commodity premium

Source: BNY

Frontier markets are generally in a better position than at the start of the conflict. Last month’s ceasefire has generally held, helping to avert additional hedging or liquidation in frontier assets.

However, it is becoming increasingly clear that the supply challenges will likely remain in place. This is starting to pressure global curves, not least in the U.S., where higher yields will have material ramifications for global high-yielding assets. Within frontier market sovereigns, for example, although only six markets were clearly sold, the magnitudes were relatively high. This already indicates sensitivity to any potential U.S. rate shock.

The well-bought markets were mostly in Latin America, and Nigeria was the top performer. None these markets has to contend with geographical proximity to the conflict, while in part they are benefiting from improvements in terms of trade (realized or not) from higher energy and soft commodity prices.

Nigeria and Argentina are large frontier markets where flows should track global trends. Consequently, the alignment between the two should not come as a surprise. Flows peaked in early May, but there are some signs of stress now that the oil rally appears to have run its course (affecting Nigeria), while higher dollar yields could hurt relative interest in hard-currency FM debt in place such as Argentina. However, overall performance remains strong, indicating there is a good real yield buffer in place. More progress on real rates will be needed though, as USD may raise the bar on such investments.

The U.S. stock market is set for another weekly gain, making the run-up in risk the best since 2023. However, correlations for risk are mixed. On the day, oil is higher, as is USD. Both of these usually mean lower global equities, but shares are buoyant, led by technology, while bonds are bid. The news headlines also provide mixed signals on the prospect of a quick resolution to the U.S./Iran conflict, while the economic focus does not fit the narrative either: Japan’s April core CPI was the lowest in four years, while German sentiment rose in the May ifo survey.

Japan: Today’s CPI release is for April, putting the focus on May Tokyo CPI next week, which will be more significant for BoJ policy expectations. Adding to the support for stocks, the Japanese government is planning to release a $19bn extra budget to offset the energy shock. The Nikkei rallied on this mix of news, while JPY remains stuck at 159 to the USD and JGBs have rallied with bull flattening. The risk for investors is in FX again.

Oil: Despite gains of 3% for Brent today, oil is set to end the week down 4%, with Brent well below $110 and WTI below $100. Hopes of a resolution to the supply disruptions dominate. The weekend watch for some form of memorandum of understanding between the U.S. and Iran on opening the strait and a path to discussing uranium clashes with the NYT report on Iranian plans to codify its toll system for vessels through the chokepoint.

IPOs: The SpaceX IPO is set for June, and listing plans for OpenAI and potentially for Anthropic are expected to follow in Q3. The key question for many is in how making room for the new market capitalization will affect the balance for markets. Fast tracking into the Nasdaq will mean more passive money flows into the new shares, likely forcing a rotation trade to make room for it all. Asset allocation into the end of the next month will be a key factor to watch for trading risk.

Bottom line: The story is changing for monitoring risk across markets, as factors and correlations deliver mixed signals. The barometer of oil and USD is not working like it did in March and April. The need for a change of narrative shows up most clearly in the current risk parity programs, which are driving stocks and bonds to rally or fall together. The unofficial start of summer this Memorial Day weekend in the U.S. will be a time to rethink the war and 2026 investment mixes. The waiting game for clarity rests on markets’ resilience, i.e., how able they are to hold despite the volatility in rates and oil. The U.S. session looks set to test the new storyline, with the focus on consumer sentiment and the swearing-in of the new FOMC chairman.

NATO Secretary General Mark Rutte has welcomed President Trump’s surprise decision to deploy an additional 5,000 U.S. troops to Poland, reversing an earlier plan to suspend a brigade deployment and catching several allies off guard. The abrupt policy shift added to uncertainty within NATO, as European governments attempt to assess Washington’s longer-term military commitment to the region amid tensions linked to the Iran conflict. Rutte said the alliance remained focused on boosting defense spending, arguing that European members were moving toward NATO’s 5% of GDP target under increasing U.S. pressure to shoulder more of their own security burden. Swedish Foreign Minister Maria Malmer Stenergard acknowledged confusion inside the alliance, while Polish officials were reportedly surprised after previously being informed the deployment would be halted. MSCI World 0.48% to 1107, DXY -0.011% to 99.247, BBG Global Aggregate 0bp to 3.882%.

European Commissioner for Economy and Productivity Valdis Dombrovskis has said the ECB will need to respond to rising inflation pressures stemming from the Iran conflict, as surging energy costs are increasingly weighing on the euro area economy. Speaking ahead of a meeting of EU finance ministers, Dombrovskis pointed to the European Commission’s updated forecasts showing weaker growth and the highest inflation since 2023 for 2026, reinforcing expectations of an ECB rate hike in June. While officials stressed the resilience of the European economy, ministers broadly agreed that any government support measures should remain temporary despite mounting pressure from countries such as Italy and Spain for greater fiscal flexibility. Several ministers also argued that the crisis highlights the urgent need to reduce Europe’s dependence on fossil fuels and accelerate investment in the green transition. Euro Stoxx 50 +0.87% to 6012, EURUSD +0.009% to 1.1608, BBG AGG Euro Government High Grade EUR -7.8bp to 3.351%.

China’s National Team, a group of state-backed investors, is set to reduce its holdings in domestic equity ETFs by about 90% in H1, having already sold approximately $170bn, including $30bn since April. This move aims to temper market froth and has placed the CSI 300 Index under pressure. Despite these sales, increased purchases by retail and overseas investors are supporting the broader market. The reduction takes the group’s holdings below the disclosure threshold and may signal an end to heavy selling. The CSI 300 remains the main index with significant National Team holdings, while tech-focused indexes like ChiNext have performed strongly this year. CSI 300 +1.3% to 4845, USDCNY +0.092% to 6.7952, 10y CGB 0bp to 1.752%.

The South Korean government is considering raising the National Pension Service’s domestic stock holding limit by five percentage points from 14.9% to 19.9% of its total portfolio to prevent forced sales amid a rising KOSPI and averted Samsung Electronics strike. Without this increase, the pension fund may need to sell about ₩150tn won in shares, potentially destabilizing the market. The plan is expected to be finalized at the National Pension Fund Management Committee meeting on the May 28, alongside the mid-term asset allocation plan for 2027-31. The new limit could allow holdings of up to 24.9%, including strategic and tactical allocations. KOSPI +0.41% to 7848, USDKRW -0.571% to 1517.15, 10y KTB -1.3bp to 4.182%.

U.S. May final University of Michigan consumer sentiment is forecast to hold at 48.2 vs. 48.2. 1-year inflation expectations are expected at 4.6% vs. a flash estimate of 4.5% and 4.7% in April. 5-10-year inflation expectations are expected at 3.4% vs. a flash estimate of 3.4% and 3.5% in April.

U.S. May Kansas City Fed Services Activity is expected to rise to 5 points vs. 3.0.

Canada March retail sales forecast to hold at 0.6% m/m vs. 0.7% m/m. Retail sales ex auto are expected to rise to 0.9% m/m vs. 0.5% m/m.

Canada April industrial product prices are expected at 1.3% m/m vs. 2.4% m/m.

Canada April raw materials price index is expected at 2.6% m/m vs. 12.0% m/m.

Central bank speakers: Fed Governor Christopher Waller gives a guest lecture on the economic outlook, ECB Governing Council members Boris Vujčić, Peter Kažimír and Madis Müller speak at a roundtable on financial literacy in Ljubljana.

Mood: Risk-off momentum has accelerated, with iFlow Mood falling to its weakest level since the “Liberation Day” volatility episode in April 2025. Equity outflows have intensified, while flows into core government bonds have remained resilient.

FX: Strong USD demand persisted, alongside substantial inflows into ZAR, while EUR, JPY, CAD and SGD continued to face outflows.

FI: Demand remained firm for Eurozone and Colombian government bonds, U.K. gilts and U.S. Treasurys, while Brazilian, Peruvian, Hungarian and Turkish government bonds saw continued selling pressure.

Equities: Outflows were concentrated in South Korea and Japan, while Singapore, Thailand, China and South Africa attracted inflows. Within DM Americas, the energy sector recorded the strongest inflows, while materials was the most sold sector.

“I have come to believe that while the past is unchangeable, our perceptions of it are malleable." – Nicholas Sparks

“The world changes according to the way people see it, and if you alter [...] the way people look at reality, then you can change it.” – James Baldwin

Germany’s Ifo business climate index unexpectedly improved in May, rising to 84.9 points from a revised 84.5 in April and defying expectations of a decline to 84.2. The modest rebound suggested that business sentiment stabilized somewhat after sharp deterioration in March and April, although conditions remained fragile amid continued economic uncertainty and elevated energy costs linked to the Iran conflict. Firms reported slightly better assessments of current conditions, with the current situation index increasing to 86.1 from 85.4, while expectations for the coming months also became marginally less pessimistic as the expectations index edged up to 83.8 from 83.5. Ifo President Clemens Fuest said the German economy was stabilizing for the time being but warned that the recovery remained vulnerable. Germany’s export-oriented economy continues to face structural pressure from higher energy costs and stronger competition from China, limiting the pace of any broader rebound. DAX +0.55% to 24743, EURUSD -0.087% to 1.1609, 10y Bund -4.1bp to 3.057%.

German GDP increased by 0.3% q/q in Q1, confirming preliminary estimates and marking a modest recovery after weak growth at the end of 2025. The improvement was driven primarily by a strong resurgence in exports, which rose 3.3% as foreign demand for chemical products, metals and machinery strengthened. Household and government consumption also increased, although private consumption remained weaker than earlier estimates. By contrast, investment activity deteriorated sharply, with gross fixed capital formation falling 1.5% q/q. Construction investment was down 2.5% because of unusually poor winter weather, while machinery and equipment investment also weakened. Industrial production and manufacturing value added improved modestly, particularly in the automotive sector, while services activity was mixed across sectors. Compared with the same quarter a year earlier, GDP rose 0.5% in price-adjusted terms. Germany’s quarterly growth nevertheless remained below that of the broader EU, where economic output increased by 0.2% q/q and 1.0% y/y. DAX +0.67% to 24771, EURUSD +0.009% to 1.1608, 10y Bund -3.8bp to 3.06%.

Germany’s construction sector orders declined in March, with real new orders in the main construction industry falling 1.6% m/m on a seasonally adjusted, calendar-adjusted basis. The decline was driven by weakness in both residential and civil engineering activity, although m/m results remained volatile. Compared with March 2025, real construction orders were down 7.7%, with residential construction orders rising 9.9% but civil engineering orders falling sharply by 20.1%. Over the January to March period, incoming orders were 1.6% lower than in the previous three months, reflecting weaker underlying momentum across the sector. Despite softer order activity, real construction turnover increased by 2.5% y/y in March, while nominal turnover rose 5.3% to €9.2bn. Employment in the construction sector also remained resilient, with the number of workers up 1.6% from a year earlier to around 545,000.

France’s wholesale trade business climate improved slightly in May, with the indicator rising to 96 points from 95 in March, although it remained below its long-term average of 100. The improvement was driven mainly by a sharp rebound in assessments of past sales, including export sales, particularly in household goods and industrial equipment wholesaling. However, the broader outlook deteriorated significantly, with the general business outlook balance falling to its weakest level since 2013 outside of the pandemic period. Order intentions weakened across most subsectors, and treasury conditions deteriorated further to their weakest non-pandemic level since 2009. Employment expectations also remained subdued. At the same time, selling price expectations rose sharply again, reaching their highest level since March 2023, especially in food, beverages and industrial equipment wholesaling, signaling renewed inflationary pressures despite fragile demand conditions. CAC 40 +0.48% to 8125, EURUSD +0.009% to 1.1608, 10y OAT -4.4bp to 3.683%.

France’s manufacturing business climate improved further in May, with the headline indicator rising to 102 from 100 in April, moving back above its long-term average. The improvement was mainly driven by a strong resurgence in reported past production, while order books (both domestic and foreign) also improved modestly. However, manufacturers remained cautious about the outlook, with production expectations weakening for a fourth consecutive month and broader production expectations staying well below average. Perceived economic uncertainty remained elevated, while supply-side pressures intensified again as more firms reported labor shortages and supply difficulties. Selling price expectations increased for a fifth straight month to their highest level since March 2023, particularly in pharmaceuticals, chemicals, plastics and textiles. By sector, confidence improved most strongly in food processing and other manufacturing industries, while transport equipment remained broadly stable and investment goods softened slightly.

France’s overall business climate remained subdued in May, with the composite indicator unchanged at 94 points, still well below its long-term average. Conditions deteriorated sharply in retail trade, where the indicator fell to 89, driven by a steep decline in order intentions. Meanwhile, the services sector weakened further to its lowest level since 2015 outside of the pandemic period, particularly in accommodation and food services. By contrast, confidence improved modestly in construction and wholesale trade and rose more solidly in manufacturing. Across sectors, firms continued to report rising selling price expectations, while general business outlook indicators weakened almost everywhere outside industry. Labor market sentiment also deteriorated significantly, with the employment climate indicator falling three points to 92, its weakest level since the pandemic, largely because of worsening hiring expectations in services. The data suggest that weak domestic demand and softer labor market conditions continue to weigh on the broader French economy despite some resilience in industrial activity.

France’s services sector business climate deteriorated again in May, as the headline indicator fell to 93 points from 94 in April, its weakest level since 2015 outside of the pandemic period. Firms became markedly more pessimistic about future activity, with the balance on expected activity dropping to its lowest level since June 2025, while assessments of past activity also weakened below historical norms. Employment conditions remained fragile, particularly outside temporary staffing, where both past and expected employment balances deteriorated sharply. Weakness was broad-based across sectors, with accommodation and food services collapsing to their weakest non-pandemic level since 2013, while real estate and information-communication also weakened materially. Although transport services improved modestly, sentiment remained below average. Price expectations stayed elevated and uncertainty remained high, suggesting ongoing pressure from weak demand alongside persistent cost concerns across the French services economy.

France’s retail trade business climate deteriorated sharply again in May, with the indicator for retail and automobile trade falling to 89 points from 94 in April, its weakest level since 2014 not including the pandemic period. The decline was driven primarily by a steep drop in order intentions, which reached their lowest non-pandemic level since 2013, while broader business outlook expectations also deteriorated significantly. Although retailers reported a modest bounce in past sales, expected sales remained weak and inventories increased above normal levels, pointing to softer underlying demand conditions. Selling price expectations continued to rise strongly and reached their highest level since mid-2023, while treasury conditions worsened substantially. Both the non-automotive retail sector and automobile trade weakened further, with particularly severe deterioration in business outlook indicators. Employment expectations remained subdued overall, despite some stabilization in current staffing conditions.

U.K. public sector borrowing rose sharply in April, with the deficit reaching £24.3bn, up £4.9bn from the same month a year earlier and significantly above the Office for Budget Responsibility’s forecast of £20.9bn. The increase reflected higher spending pressures and pushed the current budget deficit, which excludes investment spending, to £17.4bn – also above expectations. Despite the weak start to the new fiscal year, borrowing for the financial year ending March 2026 was revised lower to £129.0bn, down £22.8bn from the previous year and below the OBR’s forecast, helped by updated central government data. Public sector net debt stood at 94.2% of GDP at end-April, remaining near levels last seen in the early 1960s, while broader public sector net financial liabilities rose to 83.6% of GDP. Meanwhile, the central government net cash requirement eased slightly y/y to £15.5bn, indicating only modest improvement in immediate financing pressures. FTSE 100 +0.43% to 10489, GBPUSD +0.038% to 1.3429, 10y gilt -4.9bp to 4.916%.

U.K. retail sales volumes fell 1.3% in April following a revised 0.6% increase in March, as weaker fuel demand and softer discretionary spending weighed on activity. Automotive fuel sales dropped sharply after strong March growth, with retailers reporting that consumers had previously stocked up ahead of rising fuel prices but later cut back on driving and fuel purchases. Excluding automotive fuel, retail sales volumes fell 0.4% m/m, with clothing retailers and online sellers citing variable weather conditions and weaker demand. Despite the m/m decline, retail sales volumes over the three months to April still rose 0.5% q/q, supported by continued strength in non-food stores and non-store retailers. Cosmetics and toiletries retailers recorded a fourth consecutive m/m increase, while computer and telecommunications retailers benefited from sustained demand following new product launches earlier in the year, indicating that underlying consumer spending remained uneven rather than collapsing outright.

U.K. May GfK consumer confidence slightly improved to -23 from -25 in April (its lowest reading since October 2023). However, willingness to make major purchases fell to -20, the lowest since January 2025, especially among lower-income groups. Savings intentions dropped 10 points, indicating consumers are using savings for daily expenses. Inflation easing in April has not boosted optimism in light of expected price pressures and interest rate uncertainty. Recent government measures aim to mitigate the energy price shock from the Iran war, while political uncertainty around the prime minister is also dampening economic sentiment.

Türkiye’s labor input indices for Q1 showed continued strength in wage growth despite softer labor utilization trends. Employment across industry, construction and trade services sectors increased by 1.2% y/y, supported by gains in construction and services, although industrial employment declined by 3.2%. Hours worked fell 1.7% y/y, reflecting broad weakness in industrial and construction activity, while trade services hours rose modestly. Gross wages and salaries surged 37.0% from a year earlier, highlighting persistent inflationary pressures and strong nominal compensation growth. Labor cost indicators accelerated even more sharply, with hourly labor costs rising 41.4% y/y and hourly labor costs excluding earnings increasing by 51.4%. On a quarterly basis, employment edged up only 0.2% while hours worked declined by 0.7%, indicating weaker underlying labor demand. Meanwhile, gross wages and salaries rose 10.3% q/q, underlining continued pressure from elevated wage adjustments and labor costs across the Turkish economy. BI 100 +1.54% to 13367, USDTRY -0.278% to 45.7421, 10y TGB +54bp to 36.41%.

Türkiye’s foreign trade data for April showed export growth significantly outpacing imports, helping to narrow the trade deficit despite continued strong domestic demand. Under the general trade system, exports increased by 22.3% y/y to $25.4bn, while imports rose 3.1% to $33.9bn. As a result, the trade deficit narrowed by 29.8% to $8.5bn and the export-import coverage ratio improved to 74.9% from 63.2% a year earlier. Excluding energy and non-monetary gold, exports rose 23.6% and imports increased by 3.3%, further highlighting strong external demand conditions. Manufacturing products accounted for 94.2% of total exports, while intermediate goods represented 71.1% of imports, reflecting Türkiye’s continued dependence on imported production inputs. Germany remained the largest export market, while China was the main origin of imports. Seasonally adjusted exports rose 11.6% m/m, whereas imports declined by 3.5%, suggesting improving external momentum entering Q2.

Japanese CPI rose 0.3% m/m, 1.4% y/y in April, slightly down from 0.4% m/m, 1.5% y/y in March. Excluding fresh food, CPI rose 1.4% y/y, unchanged m/m (March: 1.8% y/y); excluding fresh food and energy, it rose 1.9% y/y but declined by 0.2% m/m (March: 2.4% y/y). Key inflation contributors included food (+3.5% y/y), especially confectionery and beverages, and communication services (+7.4% y/y). Energy prices fell (-5.7% y/y), driven by declines in electricity and gasoline costs. Education fees decreased significantly, notably private high school tuition (-10.6% y/y), exerting downward pressure on inflation. Nikkei +2.68% to 63339, USDJPY 0% to 159.13, 10y JGB -1.1bp to 2.763%.

New Zealand’s Q1 retail sales volume rose 0.9% q/q to NZ$26bn, matching the pace of the quarter ending December 2025. Key contributors included supermarket and grocery stores (+1.7%), hardware and garden supplies (+2.7%), accommodation (+6.1%) and pharmaceutical retailing (+2.8%). Clothing and footwear declined by 4.8%. The fuel sales volume edged up 0.2% q/q, with stock values surging 42% to NZ$290mn. The value of retail sales increased by 2.2% q/q to NZ$32bn, led by fuel (+5.9%) and accommodation (+6.8%). 13 out of 16 regions saw higher sales, notably Auckland (+2.1%) and Otago (+4.5%). Total stock value rose 2.5% y/y to NZ$9.3bn. NZX 50 +0.88% to 12991, NZDUSD +0.137% to 0.5862, 10y NZGB -2.3bp to 4.688%.

South Korea’s May 2026 Consumer Tendency Survey showed a rise in the Composite Consumer Sentiment Index to 106.1 points, up 6.9 from April. Sentiment improved across current living standards (93, +2), future outlook (97, +5), household income (100, +2) and spending (110, +2). Confidence in current and future domestic economic conditions increased significantly to 83 (+15) and 93 (+14), respectively. Expected inflation rates were 2.8% for one year ahead and 2.6% for both three and five years ahead. KOSPI +0.41% to 7848, USDKRW -0.571% to 1517.15, 10y KTB -1.3bp to 4.182%.

In South Korea, new mortgage loans per borrower rose to a record high in Q1 despite the government tightening regulations to cool the overheated housing market. South Korea’s Q1 borrower-level household debt data show newly issued household loans per borrower rose to ₩35.42mn, up ₩0.99mn from Q4 2025. Mortgage loans per borrower increased by ₩16.53mn to ₩229.39mn. Sizable rises were recorded among borrowers in their 30s (+₩6.35mn), Seoul metropolitan area (+₩2.46mn), non-bank financial institutions (+₩3.17mn) and mortgage loans. Outstanding household loan balance per borrower was ₩97.40mn, nearly unchanged, while mortgage loan balances increased by ₩1.79mn q/q to ₩160.06mn.

Taiwan’s unemployment rate dropped 0.04 percentage points to 3.30% in April, with the seasonally adjusted rate at 3.34%. Labor force participation edged down to 59.52% but increased by 0.25 percentage points y/y. Total employment in the country decreased by 6,000 (-0.05%) to 11,632,000 but rose by 27,000 (+0.23%) y/y. Agriculture employment increased by 1,000 (+0.16%), while industry and services sectors declined by 5,000 (-0.13%) and 2,000 (-0.03%), respectively. Compared with April 2025, agriculture and industry employment fell by 13,000 (-2.68%) and 5,000 (-0.13%), whereas services grew by 45,000 (+0.63%). TAIEX +2.18% to 42268, USDTWD +0.086% to 31.568, 10y TGB -0.8bp to 1.622%.

Taiwan’s central bank has set a principle that foreign investors choosing to receive dividends in U.S. dollars should maintain the same currency choice throughout the year, avoiding frequent switches between TWD and foreign currencies each quarter. This aims to reduce operational burdens for listed companies, especially large exporters like TSMC, and to prevent excessive market speculation on exchange rate movements. The Financial Supervisory Commission has allowed listed companies to pay foreign currency dividends to foreign shareholders, with custodian banks handling direct foreign currency transfers. Implementation is expected by 2027 at the earliest after system upgrades. The core message is that frequent dividend currency changes should be avoided to stabilize market expectations.