Market Movers: Almost There

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 7 minutes

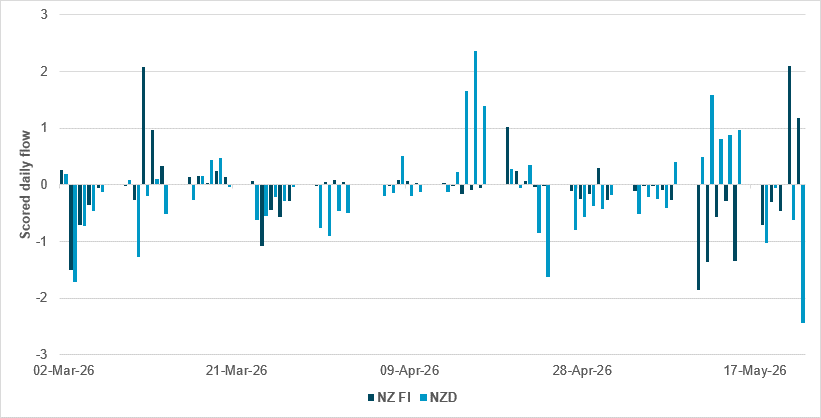

NZD underperforms NZ fixed income ahead of RBNZ decision

Source: BNY

NZD heads into tomorrow’s RBNZ decision on a very soft footing. To make matters worse, there were barely any flows last week; Friday’s outflow was then exceptional at close to -2.5 scored flow. This was the biggest outflow since April 2018, due to a large net long position (in swap) which was not rolled over. While it did not produce a clear FX impact, the size of the flow is significant and points to a large net exposure reduction. If such positions purely follow developments in rate differentials, it should not come as a surprise if the market is continuing to harbor doubts over the current trajectory of rates. Although three more are in the price for the rest of the year, increasing hesitation on the RBNZ’s part could lead to gradual reductions in any existing long positions, especially if underlying assets are not expected to perform well given the current risks to growth.

The RBNZ itself has warned that while it would “act decisively” on core inflation, additional hikes also risk “unnecessarily stifling an economic recovery,” meaning that a balancing act is needed. Given the overall flow trends since early March, NZD has broadly held on despite global risk aversion, but two attempts to put together a good purchase run in late April and mid-May have both faltered. If the U.S. now starts to shift gears on rates, it will be hard to see high-beta G10 names perform well, especially as NZD’s carry is far weaker than historical norms.

The holiday weekend in the U.S. and U.K. is over, but despite ongoing talks and defensive escalation, the war with Iran continues. The “almost there” mood regarding a path toward peace continues to roil risk taking. The oil market is down vs. Friday but up from yesterday, with WTI at $93 from $99 and Brent at $99 from $104. Global equity markets also made gains on Monday, still led by AI optimism, with U.S. futures up. Bonds are mixed, with the ECB and BoJ signaling higher rates to come, while USD is down 0.25% since Friday.

Bottom line: The last week of May brings more reallocation pressures for risk across portfolios. Looking through oil and inflation has become the mantra for many, with AI optimism and technology the driving forces. The risk premium between bonds and stocks has narrowed sharply given May’s surge in yields around the world. How that leads to rebalancing and what it means for the dollar will be crucial in setting the tone for June. The markets’ price action over the weekend will be tested by the facts of the day ahead, with jobs and inflation worries still the goal posts for higher returns. Expect the best barometer today to be in places where the Iranian conflict has left the largest moves: EM FX and G10 long-end rates.

Iran’s Supreme Leader Ayatollah Mojtaba Khamenei has warned that Gulf states will no longer provide safe protection for U.S. military bases. He declared that Washington would no longer have a secure haven in the region, as Iran and the U.S. continued negotiations aimed at ending their three-month conflict. The comments, issued through Khamenei’s Telegram channel, came shortly after U.S. forces struck missile sites in southern Iran and targeted vessels allegedly attempting to lay naval mines, actions that threatened a fragile ceasefire established on April 8. The statement also drew attention because Khamenei has not appeared publicly since becoming supreme leader in March, fueling speculation about his health following injuries sustained during earlier strikes. Markets remain sensitive to developments, given that the conflict has severely disrupted energy flows in the region and driven up risks to the global economic outlook. Brent +2.882% to 98.91, WTI -4.348% to 92.4, Omani crude -5.657% to 95.9, Dubai crude +0.424% to 103.355.

ECB Executive Board member Isabel Schnabel has said the European Central Bank should raise interest rates at its June meeting, arguing that the energy shock linked to the Middle East conflict is too large and persistent for policymakers to ignore. Speaking to Reuters, Schnabel stated that even if the war were to end immediately, damage to energy infrastructure and supply chains had already created lasting inflationary pressures that would require a monetary policy response. She warned that the euro area has effectively moved beyond the ECB’s previous adverse energy scenario and highlighted growing evidence of second-round inflation effects spreading beyond energy into broader consumer prices and non-energy industrial goods. While acknowledging downside risks to economic growth from weaker confidence and higher energy costs, Schnabel stressed that maintaining the ECB’s anti-inflation credibility required a timely policy response. Euro Stoxx 50 -0.45% to 6109, EURUSD -0.069% to 1.1636, BBG AGG Euro Government High Grade EUR 0bp to 3.211%.

BoJ Deputy Governor Ryozo Himino has said the central bank would continue considering further interest rate increases, but stressed that the timing and pace of tightening would depend heavily on how the Middle East conflict affects Japan’s economy and inflation outlook. Speaking in parliament, Himino warned that the BoJ’s baseline forecasts could shift sharply due to higher energy prices and global inflation risks stemming from the conflict. He emphasized that the BoJ must adjust monetary easing at an appropriate pace to maintain market confidence in its commitment to controlling inflation, particularly as Japanese government bond yields have climbed to their highest levels since 1996. His remarks reinforced increasingly hawkish communication from BoJ officials, with markets now assigning a high probability to a June rate hike as policymakers grow more concerned about persistent inflationary pressures and the risk of inflation overshooting forecasts. Nikkei -0.25% to 64996, USDJPY +0.164% to 159.17, 10y JGB +2.5bp to 2.728%.

China’s central bank has allowed the interest rate on 1y medium-term lending facility loans to banks to fall to a record low of 1.45% in May from 1.50% previously, signaling Beijing’s growing concern over slowing economic momentum and willingness to provide additional monetary support. The move follows weaker April activity data, with industrial production and retail sales recording some of their softest growth rates in years, increasing pressure for stronger policy easing. Although the PBoC has shifted its operational focus toward the seven-day reverse repo rate, the lower MLF funding rate still points to easier liquidity conditions and reduced bank funding costs that could feed through to broader financing conditions. The PBoC also injected a net ¥100bn into the banking system through the facility in May and reiterated its commitment to maintaining a moderately loose monetary policy stance while monitoring imported inflation risks. CSI 300 +0.53% to 4948, USDCNY +0.056% to 6.787, 10y CGB -0.1bp to 1.75%.

Hungarian central bank rate decision: forecast to remain on hold at 6.25%.

U.S. ADP Weekly Employment Change is due; the most recent print was 42.3k.

U.S. April Chicago Fed National Activity Index is expected at 0 vs. -0.2.

U.S. May Philly Fed Non-Manufacturing Activity forecast at -13.0 vs. -16.5.

U.S. March FHFA House Price Index is expected to rise to 0.1% m/m vs. 0.0% m/m.

U.S. March S&P Cotality Case-Shiller 20-City Index is expected at -0.06%% m/m, 0.9% y/y vs. -0.05% m/m, 0.9% y/y in February.

U.S. May Conference Board Consumer Confidence forecast to ease to 92.0 vs. 92.8.

U.S. May Dallas Fed Manufacturing Activity is expected at 0 vs. -2.3.

U.S. Treasury sells $89bn in 13-week bills, $77bn in 26-week bills, $85bn in 6-week bills and $69bn in 2y notes.

Central bank speakers: Nicolas Vincent, External Deputy Governor at the Bank of Canada, delivers a speech in Montreal on labor market trends and structural changes in the Canadian economy. The ECB’s Olaf Sleijpen speaks in Amsterdam.

Mood: Risk sentiment has stabilized but remained firmly in risk-off territory, with iFlow Mood at -0.265. Equities have continued to face selling pressure, while inflows into core government bonds held steady.

FX: Strong USD demand persisted, against broad-based selling across the rest of the iFlow universe, led by CAD, DKK, NZD and SGD. ZAR also recorded substantial inflows.

FI: Buying was concentrated in U.S. Treasurys and Eurozone and Chinese government bonds, while Brazilian, Peruvian, Hungarian and Turkish government bonds saw heavy selling pressure.

Equities: Broad-based selling continued, led by South Korea, Indonesia and Japan, while selective inflows were seen in Singapore, China, New Zealand and South Africa.

“We’re almost there and nowhere near it. All that matters is that we’re going.” — Lorelei Gilmore

“Good things don’t wait until you’re ready. Sometimes they come right before, when you’re almost there.” – Taylor Jenkins Reid

France’s retail trade turnover increased by a modest 0.4% m/m in April after a 0.3% rise in March, marking a second consecutive monthly gain and suggesting slightly firmer consumer demand. Growth was driven by manufactured goods sales, which rose 0.8%, while food sales edged down 0.2%. Within manufactured goods, the strongest increases were recorded in sports equipment, textiles and clothing, and consumer electronics, while sales weakened in press and stationery, automotive equipment, and watches and jewelry. By distribution channel, supermarket and hypermarket sales increased by 0.7% and 0.4%, respectively, whereas small retail stores saw a 1.9% decline and department store sales were flat. Over the latest three-month period, retail sales rose only 0.2%, reflecting still subdued consumption momentum overall. CAC 40 -0.38% to 8227, EURUSD -0.069% to 1.1636, 10y OAT +3.9bp to 3.598%.

Spain’s industrial producer prices accelerated sharply in April, with the Industrial Price Index rising 8.3% y/y from 3.1% in March, while producer prices increased by 1.7% m/m. The surge was driven primarily by energy prices, where y/y inflation jumped to 22.3% from 7.1% previously, reflecting higher petroleum refining prices and a smaller decline in electricity generation and distribution prices than a year earlier. Intermediate goods inflation also strengthened to 3.8% from 0.8%, supported by sharp increases in basic chemicals, fertilizers, plastics and synthetic rubber prices. Excluding energy, industrial producer inflation rose to 2.6% y/y, remaining well below the headline rate. By region, the strongest y/y price increases were recorded in Andalusia, Murcia and the Basque Country, while Aragon and Navarra saw the smallest gains. IBEX 35 -0.06% to 18407, EURUSD -0.069% to 1.1636, 10y Bono +4.3bp to 3.41%.

U.K. shop price inflation for May was 1.2% y/y, up from 1.0% in April and above the three-month average of 1.1%. Food prices increased by 2.7% y/y, down from 3.1% in April, with fresh food inflation at 3.4% y/y and ambient food at 1.6% y/y. Non-food prices rose 0.5% y/y, reversing a slight decline in April (-0.1% y/y). M/m, overall shop prices increased by 0.5% in May, driven by a 0.8% rise in non-food prices, while food prices decreased marginally (-0.1%). Retailers are striving to keep prices low amid rising costs. FTSE 100 +0.71% to 10541, GBPUSD -0.237% to 1.3472, 10y gilt -4.4bp to 4.853%

Sweden’s producer and import prices accelerated sharply in April, with the Producer Price Index rising 1.1% m/m and 4.7% y/y, up from 2.0% y/y in March, as higher crude oil prices drove broad energy-related cost pressures across export and import markets. Export prices increased by 2.5% m/m and import prices rose 3.3% m/m, while domestic producer prices slipped 0.1% m/m due to lower electricity and district heating costs. Energy-related products rose 27.0% y/y in the PPI and 33.5% y/y in the domestic supply index, while producer prices excluding energy-related goods increased by 1.4% y/y. By sector, refined petroleum products, chemicals, metals, plastics, pulp and motor vehicles contributed positively, while electricity prices weighed on domestic and export markets. Import price gains were led by crude oil, chemicals and computers. OMX -0.67% to 3171, EURSEK +0.202% to 10.826, 10y Swedish GB +3.3bp to 2.748%.

Sweden’s Q1 economic statistics showed stronger private sector profitability, investment activity and inventory accumulation, pointing to improved business conditions despite global trade and energy market uncertainty. Total value added increased by 5.9% y/y in current prices and 6.7% in constant prices as production volumes rose faster than intermediate consumption, reducing the input share from 66.7% to 65.3%. The profit share of value added increased to 27.8%, up 1.9 percentage points from a year earlier, while gross operating surplus rose 13.6% and operating profit was up 11.4%, lifting the operating margin to 7.3%. Gross fixed capital formation rose 7.4%, driven mainly by machinery and equipment investment, while inventories increased by SEK 29.7bn q/q, led by goods for resale.

Norway’s unemployment rate for April was unchanged at 4.8% of the labor force, equivalent to 147,000 people, though this was 0.2 percentage points higher than in January, signaling some softening in labor market conditions during early 2026. Statistics Norway noted that unemployment had stabilized during H2 2025, but increases this year have mainly occurred among workers aged 25 and older, while youth unemployment around 14% has broadly plateaued. Preliminary seasonally adjusted figures showed employment declined by just under 3,000 jobs m/m in April following a gain of more than 7,000 in March, leaving total jobs down nearly 6,500 so far this year. Education contributed most to April’s decline, while healthcare and social services remained the strongest support in final March figures. OSE -0.38% to 2036, EURNOK +0.134% to 10.7762, 10y NGB -5.1bp to 4.409%.

Norwegian household credit growth remained stable at 4.7% y/y in April, unchanged from earlier in the year, with households’ domestic debt reaching NOK 4.709tn. Total domestic debt growth for the public sector slowed slightly to 4.4% from 4.5% in March, mainly due to weaker municipal borrowing. Municipal debt growth fell to 4.7% from 5.2%, marking the first time in more than two years that municipal debt growth was not higher than the other major sectors. Municipal debt outstanding reached NOK 829bn, around 10% of total public domestic debt. Non-financial corporations were the only sector to record faster debt growth, with a rise to 3.8% from 3.7% in March. Statistics Norway noted that corporate credit growth has gradually recovered over the past six months after stabilizing at low levels following the 2022-23 policy tightening cycle.

Poland’s labor market data for April showed continued weakness in enterprise employment alongside rising registered unemployment pressures. Average employment in the enterprise sector fell 0.9% y/y to 6.39 million, with the sharpest declines recorded in mining, manufacturing, utilities and administrative services, while employment growth remained limited to sectors such as water management and hospitality. Registered unemployment stood at 934,300 people at the end of April, up 16.4% y/y, although down 1.6% from March, with the unemployment rate easing to 6.0% from 6.1% in the previous month but remaining 0.8 percentage points above year-earlier levels. Long-term unemployment and the share of unemployed people without professional qualifications both increased. Job offers remained subdued at 40,900 vacancies, while planned group layoffs rose sharply, with firms intending to cut 21,500 jobs by end-April. WIG -0.01% to 137847, EURPLN +0.112% to 4.235, 10y PGB +3.5bp to 5.807%.

Poland’s labor market remained relatively stable in Q1, although activity and employment softened slightly from the previous quarter. The labor force participation rate for people aged 15-89 fell to 58.7% from 59.0% in Q4 2025, while the employment rate declined to 56.8%, though both indicators remained above year-earlier levels. Total employment stood at 17.24 million people, down 109,000 q/q but up 177,000 y/y, with manufacturing, wholesale and retail trade, education, construction and transport remaining the largest employment sectors. The unemployment rate edged up to 3.3% from 3.2% in the previous quarter but was slightly below Q1 2025 levels, with youth unemployment remaining elevated at 12.5%. The average job search duration increased to 8.5 months, and 41.3% of the population aged 15-89 were classed as economically inactive.

South Africa’s composite leading business cycle indicator strengthened further in March, rising 2.4% m/m and 7.5% y/y. This signaled improving forward-looking economic momentum despite weaker conditions among major trading partners. The South African Reserve Bank said six of the seven available component series contributed positively, led by faster growth in real M1 money supply and a wider spread between long-term and short-term interest rates. Additional support came from stronger export commodity prices, higher building plan approvals, increased vehicle sales and firmer job advertisements. In contrast, the coincident indicator edged down 0.1% in February due to lower manufacturing capacity utilization and weaker industrial production, while the lagging indicator climbed 0.6%. The data suggest near-term domestic activity remains mixed, although forward indicators point to improving conditions ahead. JSE TOP 40 -0.64% to 107479, USDZAR +0.347% to 16.3454, 10y SAGB +9.7bp to 8.774%.

Japan’s Economic Trend Index for March revealed continued improvement. The leading index rose to 114.0 (up from 113.2 in February), indicating positive future economic activity. The coincident index edged up slightly to 116.4 (from 116.2), reflecting current economic conditions. The lagging index declined marginally to 112.4 (from 112.6), suggesting some delayed economic effects. Key contributors to the leading index included inventory rate indices and new job openings, while consumer sentiment weakened. Industrial production and shipments showed mixed results. Overall, the coincident index signals an upward phase in the economy, supported by steady manufacturing and retail sales trends. Nikkei -0.25% to 64996, USDJPY +0.164% to 159.17, 10y JGB +2.5bp to 2.728%.

Japanese Prime Minister Sanae Takaichi has announced a supplementary budget worth around ¥3tn, or roughly $19bn, to replenish contingency reserves and expand subsidies aimed at limiting fuel and utility costs as higher energy prices and yen-driven import inflation pressure households. The move reverses her earlier stance against additional fiscal spending and reflects concern that the Iran conflict and elevated oil prices could undermine public support. Takaichi sought to reassure financial markets by stating that overall government bond issuance would remain unchanged, with stronger tax revenues, non-tax income and underspending expected to offset the need for additional borrowing. The announcement follows a sharp rise in Japanese government bond yields after reports of possible new debt issuance, while investors remain focused on broader fiscal risks including potential consumption tax cuts and rising debt-servicing costs.

Singapore’s manufacturing output rose 17.6% y/y in April (March: 9.2%), excluding biomedical manufacturing it increased by 21.5% (March: 12.4%). On a seasonally adjusted m/m basis, output grew 5.8%, including biomedical. Electronics led with 44.0% y/y growth, driven by infocomms, consumer electronics and semiconductors amid strong AI demand. General manufacturing and precision engineering expanded by 16.9% and 15.1%, respectively. Transport engineering grew 10.1%, supported by aerospace and marine activities. Biomedical manufacturing declined by 16.1%, and chemicals fell 17.6% due to feedstock supply disruptions. The data reflect robust manufacturing momentum outside of the biomedical and chemicals sectors. STI -0.59% to 5040, USDSGD +0.071% to 1.2779, 10y SGB -5.2bp to 2.073%.

Singapore’s household sector balance sheet for Q1 showed that household net worth growing by 6.7% y/y, slower the 7.3% recorded in Q4 2025. Asset growth softened to 6.8% y/y, driven by slower increases in financial and residential property assets. Liabilities growth accelerated to 8.2% y/y, surpassing the previous peak of 7.4% in Q4 2021, mainly due to faster growth in mortgage loans (5.8% y/y) and personal loans (14.6% y/y). Household net worth and assets stood at 868.3% and 976.2% of personal disposable income (PDI), respectively, while liabilities reached 107.9% of PDI.

Taiwan’s industrial production increased by 14.2% y/y in April, with manufacturing output rising 15.1%, supported by sustained demand for artificial intelligence, high-performance computing and cloud infrastructure applications. Manufacturing production remained heavily driven by the information and electronics sector, where electronic components output rose 11.5% y/y and computer, electronic and optical products surged 85.4%, reflecting strong demand for servers, semiconductor testing equipment, switches and advanced semiconductor production capacity. Machinery and equipment output also increased by 9.7% as semiconductor firms continued to expand advanced process and packaging capacity. In contrast, traditional industries remained weaker, with chemical materials and fertilizers falling 10.0% and automotive production down 2.9% on soft demand and cautious customer orders. The Ministry of Economic Affairs said continued global investment in AI infrastructure and cloud services should support further growth in semiconductor and server-related production. TAIEX -0.27% to 43525, USDTWD -0.074% to 31.436, 10y TGB -0.5bp to 1.61%.

Taiwan’s wholesale, retail and restaurant sales all expanded in April, supported by continued AI demand, holiday spending and seasonal promotions. Wholesale sales increased 25.2% y/y to TW$1.54tn, led by machinery and equipment wholesalers, which surged 44.3% on strong server, memory and electronic component shipments linked to AI and cloud computing demand. Retail sales rose 5.2% y/y, or 7.3% excluding vehicle sales, driven by department store Mother’s Day promotions, stronger apparel demand, e-commerce growth and new consumer electronics launches, although motor vehicle sales fell 4.6% amid cautious demand for imported cars. Restaurant sales increased by 4.5% y/y as holiday dining demand, store expansion and beverage sales supported activity. The Ministry of Economic Affairs said AI infrastructure investment and seasonal consumption trends should continue supporting wholesale, retail and catering sales in May.

The Central Bank of Sri Lanka has raised its overnight policy rate by 100bp to 8.75%, exceeding expectations of a 50bp hike. This decision reflects concerns over elevated global commodity prices, especially petroleum, driven by Middle East tensions, which have pushed domestic energy prices higher. These factors contributed to a 5.4% y/y inflation in April 2026, largely supply-driven but supported by strengthening demand, credit expansion and import growth. Headline inflation is expected to stay above the 5% target in the near term before stabilizing, with short-term inflation expectations rising but remaining anchored over the medium term. Colombo All Share -0.85% to 22175, USDLKR -0.347% to 322.45, 10y SLGB -4bp to 11.23%