Policy crossroads

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 8 minutes

Despite a historic oil supply shock, financial markets have shown resilience, with contained volatility outside of energy and no broad-based panic. However, rising oil prices are fueling inflation concerns, lifting global rates and complicating the Fed’s policy outlook as markets scale back expectations for rate cuts.

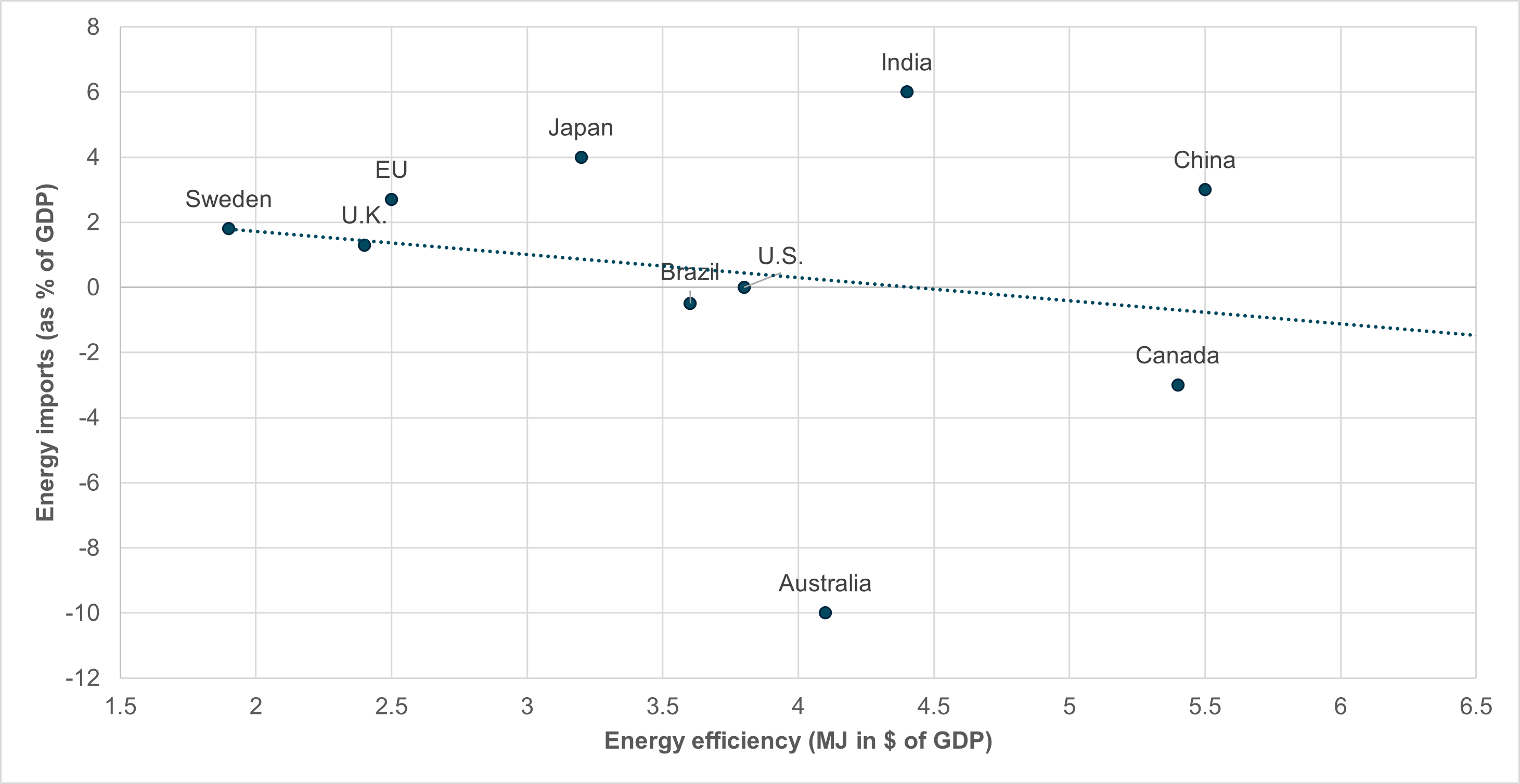

EXHIBIT #1: ENERGY EFFICIENCY AND ENERGY IMPORTS

Source: BNY, Bloomberg, International Energy Agency

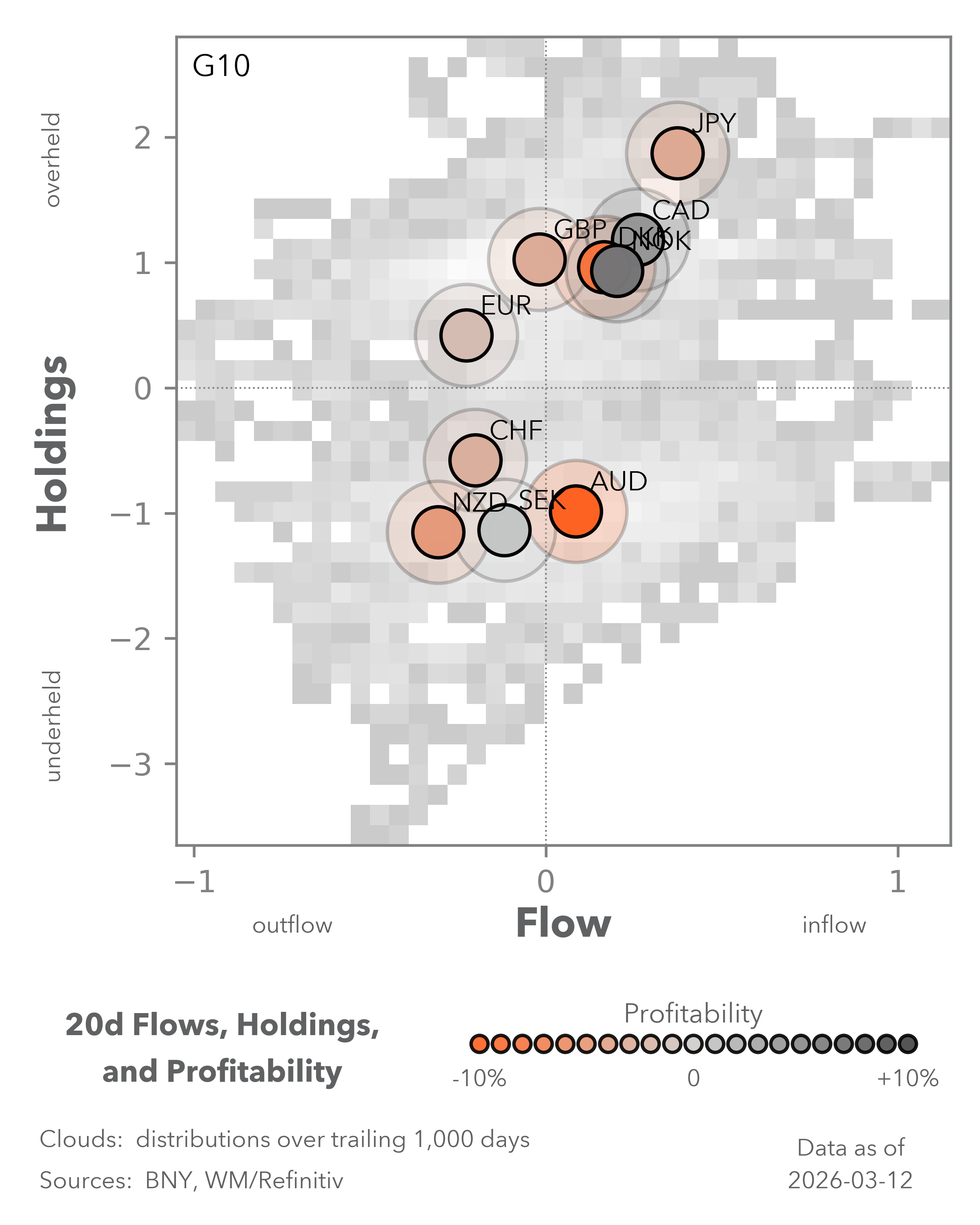

Our take: The energy shock across stocks, bonds and FX has been linked most to the rise of the USD. At the same time BRL, AUD and CAD have fared better than other currencies.

The role of energy imports and efficiency in differentiating nations becomes clear when examining the dispersion between G10 and BRIC economies and how energy affects growth. The biggest outliers are Australia and India. Canada and China are at one end of the spectrum, while Sweden, the EU and the U.K. are on the other.

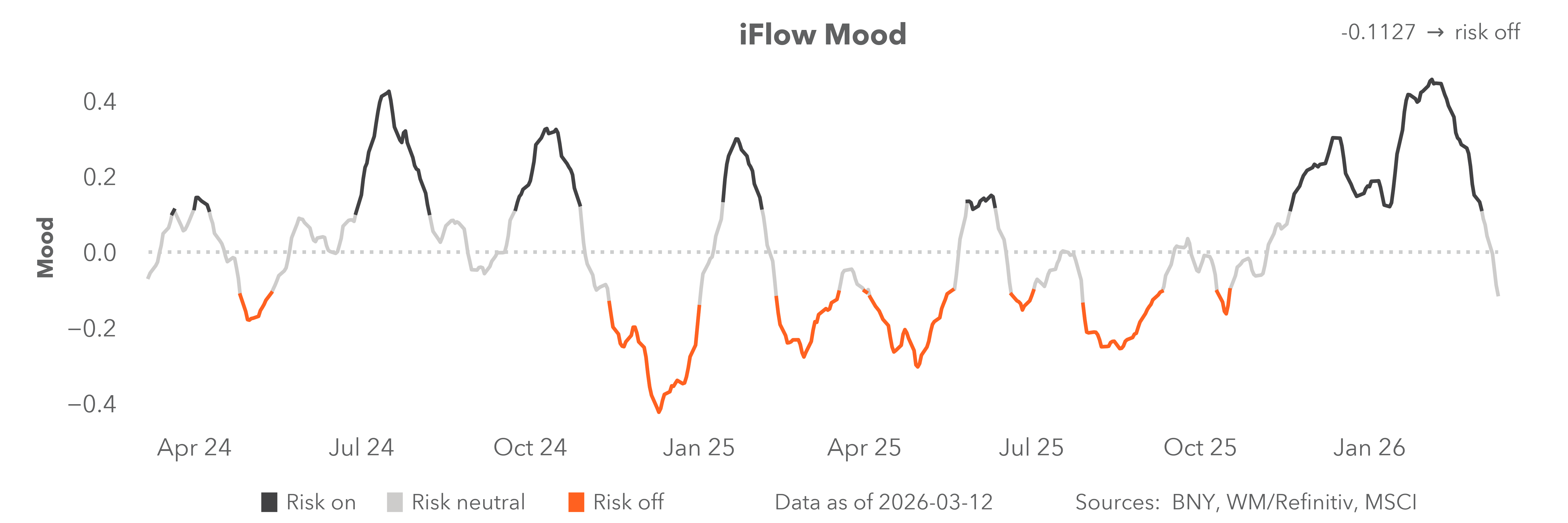

Forward look: Looking at the world through an energy lens is useful only in ordering risks for the weeks ahead. But other factors, like policy responses and ongoing financial conditions, will also be critical. Investors have already been shifting their holdings in bonds, stocks and currencies on the back of the energy shock. India has been sold while Australia has been bought, but this could change with shifts in oil prices or policies. Energy’s role in supporting the USD and BRL may also be overstated. Carry, politics and growth all matter. The role of risk sentiment shifting sharply lower seems underpriced, yet we start the week with iFlow Mood in extreme negative territory for the first time this year. Positions could flip from oil shocks to demand-destruction bias, where safe havens are in cash, not energy.

North America: Fed and BoC to guide on war and stagflation risks

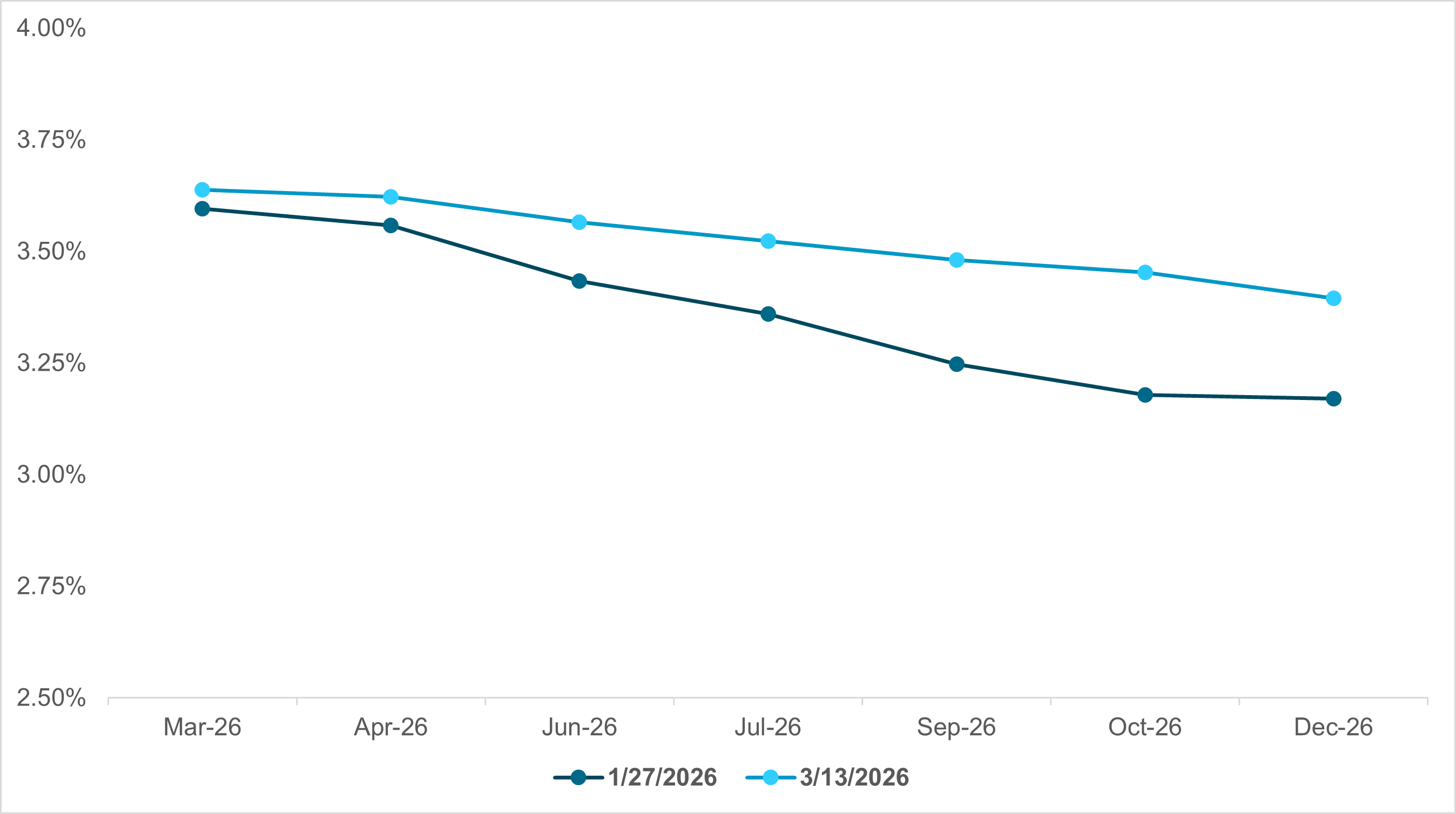

EXHIBIT #2: U.S. MARKET-IMPLIED FED FUNDS RATE EXPECTATIONS

Source: BNY, Bloomberg

Our take: While this won’t be a heavy data week, Wednesday brings FOMC and Bank of Canada (BoC) meetings, which will give the market plenty of things to watch. We don’t expect rate moves from either, but against the backdrop of the conflict in the Middle East, it will be worth digesting how each central bank addresses the fallout (so far) of the hostilities.

Forward look: In the U.S., there will be a new set of dots via the quarterly Summary of Economic Projections. It will be interesting to see if the committee changes its outlook for the upcoming year or two. We expect “uncertainty” to be cited in reference to the effects of the war, and frankly, like the Fed, we’re unable to be more prescriptive than that. In many ways, although it is scheduled to be Chair Jerome Powell’s penultimate FOMC meeting, we expect few fireworks.

The same goes for Canada, where we expect the BoC to be similarly noncommittal, while emphasizing trade- and war-related uncertainty.

U.S. macro data are limited, but there are a few regional PMIs (New York and Philadelphia), along with the February PPI released Wednesday before the FOMC. The PPI has been indicating continuing pricing pressures from tariffs. Although it won’t cover the period after the war began, it remains at risk of further rises.

EMEA: Justification needed to avoid hikes across Europe

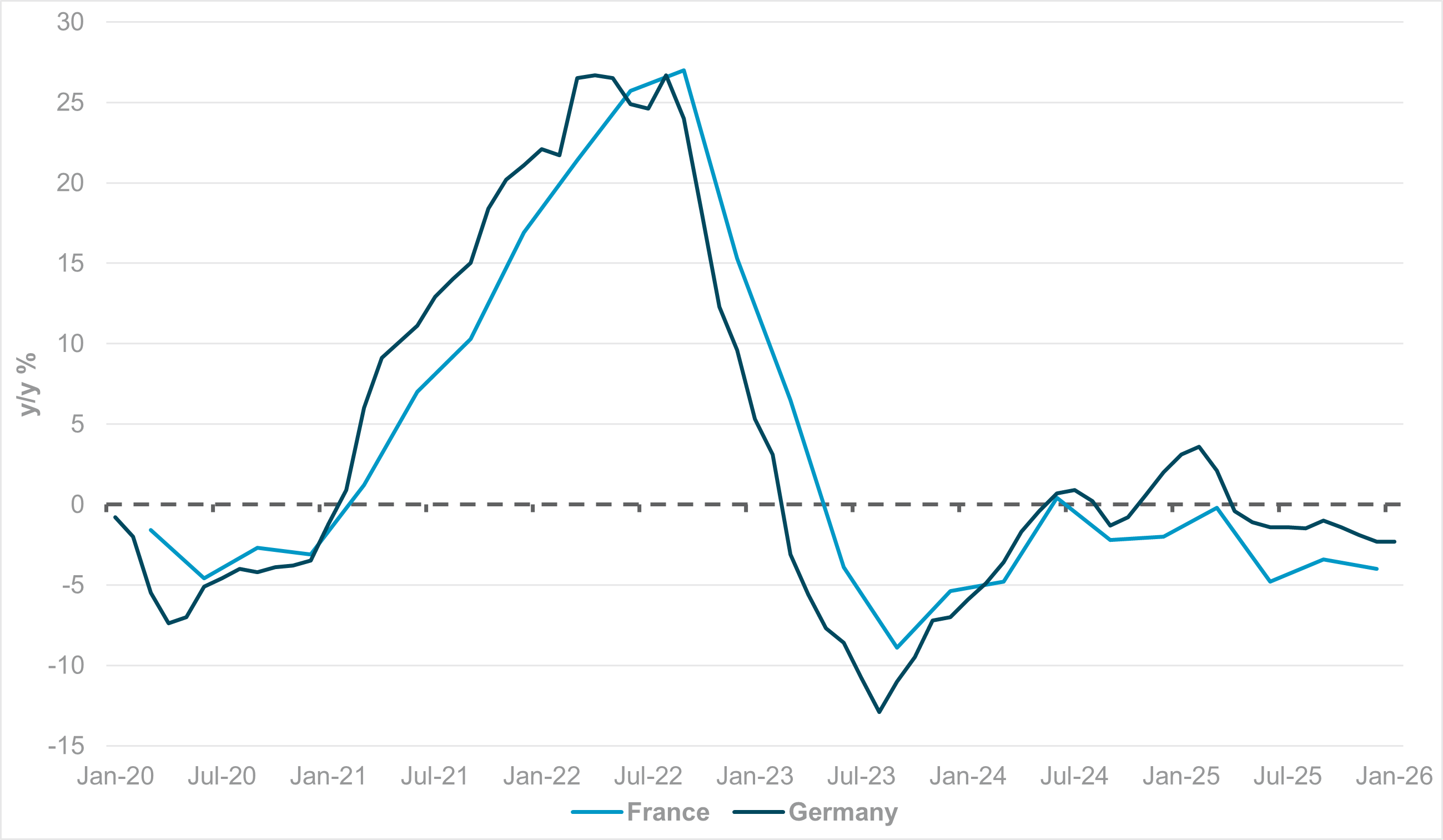

EXHIBIT #3: FRENCH AND GERMAN IMPORT PRICE INDICES

Source: BNY

Our take: The European Central Bank (ECB), Swiss National Bank (SNB), Riksbank, Bank of England (BoE), and Czech National Bank (CNB) decisions in the week ahead will all have one item on the agenda. To paraphrase BoE Governor Andrew Bailey’s pre-conflict view of the U.K.’s rate path, the swing voter on the Monetary Policy Committee was looking for “justification to hike.” In other words, the burden of proof was on the dovish argument amid sticky wage growth in the U.K. The same can be said across the continent. The conflict has now turned the outlook on its head, and most policymakers will need to look for reasons not to hike.

Decision-makers in the region may err on the side of acting early to anchor inflation expectations, having been scarred by the experience of 2022 to 2023. During that period, almost all central banks in the region were accused of being “behind the curve” in viewing the energy and post-pandemic supply shock as driving “transitory” inflation. We saw this clearly in various ECB commentaries before the blackout period. Within a week, the strict line of not acting “in haste” shifted toward inflation “vigilance” and even the prospect of hikes arriving earlier than expected. ECB policy has now shifted toward a June hike, and most officials have probably realized that even if de-escalation comes soon, normalization of energy supplies will take time and occur at a significant cost that may yet be passed on to consumers and households.

There is also an argument that demand may be dampened by households’ experience of the last energy shock, which could mitigate any further supply shock. Even so, we believe that in the near term, all European central banks deciding next week will likely lean toward maximum hawkishness, but without resorting to a hike yet. At the very least, it should help prevent further declines in the euro due to stagflation risk and help limit import price gains. Between 2022 and 2023, import prices in France and Germany (Exhibit #3) moved above 25% y/y and took around a year to settle – a timeline and scale of move that policymakers will want to resist where policy tools allow.

Forward look: Within individual decisions, we believe it is also important for the central banks to spell out the underlying criteria for hikes and their purpose. We expect any future move (most likely in Q2) to be precautionary, and only if full-year energy prices are expected to materially deviate from the baseline. The ECB has already confirmed that the upcoming staff projections will incorporate the moves since the beginning of the conflict. Normally, the alternative scenarios set out moves in energy and FX prices at the 75% interval based on options-implied densities (likely from the first week of March), and a significant overshoot of that “upper bound” would trigger a response.

Otherwise, we see a risk of one or two votes for a hike by the ECB, one or two BoE doves moving back toward a hold rather than a cut, and the risk of a hawkish turn by the CNB. The Riksbank will likely re-introduce language encouraging SEK strength. The SNB has the most challenging job – expressing support for CHF strength in a pass-through inflation context while discouraging extremely large safe-haven flows that could prove problematic for inflation targets over the medium term.

Finally, we also expect more fiscal announcements to come through to limit any gains in energy prices. France has already announced cuts to fuel prices, though Banque de France Governor François Villeroy de Galhau warned at the beginning of the conflict that France “doesn’t have money to subsidize fuel.” Larger fiscal commitments akin to the energy price cap that directly contributed to the 2022 mini-budget crisis in the U.K. could introduce a new layer of market volatility through the fiscal channel. iFlow has already identified a significant pullback in Eastern European bond markets for this reason, and the larger Western European markets should not assume they are immune to market challenges to fiscal credibility.

APAC: China activity and investment, regional exports; RBA, BoJ, BI and CBC to meet

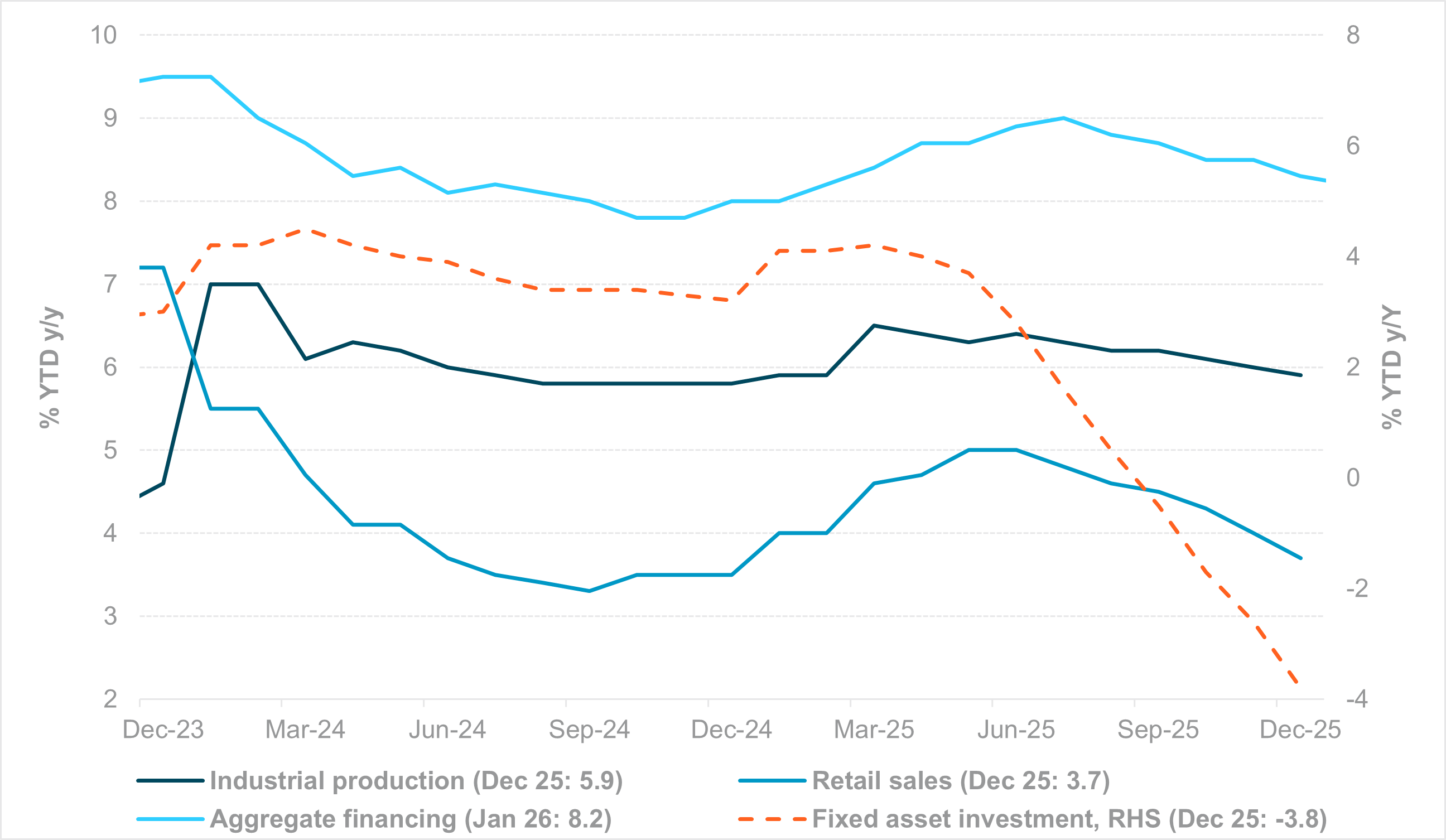

EXHIBIT #4: CHINA DATA INDICATE SLOWING ACTIVITY AND INVESTMENT TRENDS

Source: BNY

Our take: The APAC calendar this week is led by China’s February activity data – retail sales, industrial production, fixed-asset investment, unemployment, and property investment and sales – which will set the tone for regional FX and rates. Markets will look for signs of post-Lunar New Year demand stabilization and whether infrastructure and manufacturing capex can offset the ongoing property-sector drag. A downside surprise may have limited spillover following last week’s lower 2026 GDP target of 4.5% to 5.0%, announced at the NPC. Property price data (new and existing homes) will be closely watched for signs of stabilization; persistent weakness would reinforce expectations of further policy easing.

Elsewhere, February export data from Taiwan, Malaysia, India, Singapore, and Japan will provide a pulse check on regional demand and the electronics upcycle. Central banks will also be in focus. The Bank of Japan (BoJ), Bank Indonesia (BI), and Taiwan’s Central Bank of the Republic of China (CBC) are widely expected to hold rates steady. The Reserve Bank of Australia (RBA) is a closer call, with market pricing influenced by Deputy Governor Andrew Hauser’s hawkish remarks, tight labor conditions, and lingering upside inflation risks.

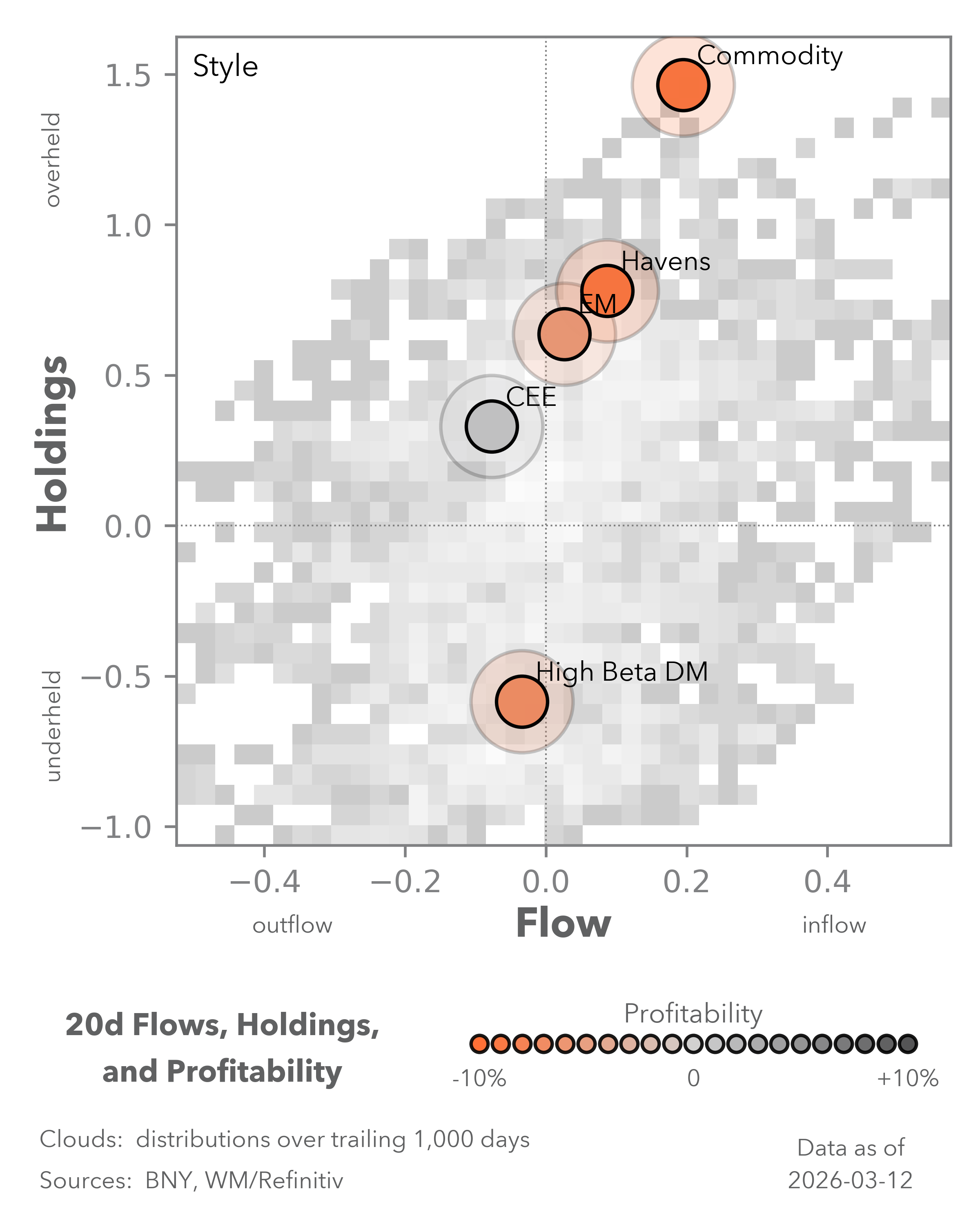

Forward look: Geopolitical uncertainty and heightened cross-asset volatility are likely to persist in the near term until markets gain confidence in a stabilization of the Iran conflict. As a result, caution prevails, and de-risking remains the dominant regional theme. This is clearly observed in iFlow, where EM – including EM APAC equities and sovereign bonds – posted accelerated outflows last week after a relatively muted prior week.

Although oil prices have retreated from near $120 highs to below $100, offering some relief to net oil importers, levels remain uncomfortably elevated in absolute terms. In response, regional governments have acted swiftly, introducing temporary increases in gasoline and diesel subsidies, extending fuel tax cuts, and – in South Korea’s case – launching an emergency support package comparable to the program initiated during COVID in 2020.

We maintain the view that currencies of net oil-importing economies – KRW, THB, INR, PHP and JPY – are likely to remain under pressure. In contrast, CNY and SGD should continue to serve as relative anchors of regional FX stability. Risks to Asia remain skewed to the downside. That said, we expect regional central banks to step up currency management efforts, particularly in economies where exchange rates are approaching historically weak levels, including India, the Philippines, South Korea and Indonesia.

As we begin the week, resilience remains the defining feature of global markets – but it is a conditional resilience. Energy has become the organizing force across FX, rates, and equities, yet broader contagion has so far been contained. The next phase will hinge less on the initial oil shock and more on policy credibility and demand dynamics. Central banks face a narrow path: acknowledge stagflation risks without triggering financial tightening that accelerates demand destruction. The Fed’s updated projections, Europe’s hawkish bias, and Asia’s growth pulse will help determine whether this remains an energy-led repricing or evolves into a broader growth scare. Positioning is already defensive, sentiment is stretched, and safe-haven flows may increasingly favor liquidity over commodities. For financial professionals, the focus should remain on cross-asset correlations, fiscal credibility, and whether inflation persistence or growth erosion becomes the dominant narrative into 2026.

Central bank decisions

Australia, Reserve Bank of Australia (Tuesday, March 17): The RBA is expected to hike rates by 25bp to 4.10%, and considering recent events, the market is now pricing in a far more aggressive trajectory with consecutive moves in play. The prospect of 4% inflation is now in play, and domestic inflation expectations continue to rise. Endorsing a hawkish trajectory to alleviate tradables inflation in the current supply environment will also be welcome: liquefied natural gas price gains are positive for Australian terms of trade, but petrol prices are already showing strains amid global events.

Indonesia, Bank Indonesia (Tuesday, March 17): We expect BI to keep the policy rate unchanged at 4.75%, while retaining an easing bias. However, the bar for further cuts is high, given currency and market stability concerns. BI has stepped up its rhetoric – from “bold intervention” to “very large FX interventions” (January), and most recently “increasing intensity of IDR stabilization measures” (February). Policy focus remains on safeguarding stability and improving credit transmission. Although average lending rates eased in February, they remain elevated at 14.2% in March 2026.

Canada, Bank of Canada (Wednesday, March 18): The BoC meets on Wednesday, and we don’t expect any change in rates. In its policy statements in subsequent public appearances, BoC officials have emphasized uncertainty and the risks to the economy from trade shocks but have been approving of inflation developments. The Middle East crisis could upend how the Bank characterizes the outcome, but we don’t expect much concrete guidance.

U.S., Federal Open Market Committee (Wednesday, March 18): What was once expected to be a relatively straightforward FOMC meeting has become more interesting. Not that we expect any moves in policy rates, but we are curious to hear how the Fed views the impact of the Middle East crisis on the economy, inflation, and the potential rate path going forward. The Summary of Economic Projections is due, and we’ll be carefully interpreting it to get a clue on policy. Rate expectations for year-end have become much less dovish since the conflict began.

Brazil, Comitê de Política Monetária (Wednesday, March 18): We believe no central bank should be in a position to cut rates at present, as global inflation expectations are rising sharply due to the conflict. Even economies with very high nominal rates are turning cautious – the Turkish Central Bank was very clear in warning this week that tightening is possible if the outlook deteriorates. The Selic rate, at 15%, offers sufficient room for COPOM to act, but expectations for a 50bp move could prove over-optimistic, even if the real rate buffer remains large. Sequential inflation is already accelerating in Brazil (0.7 m/m IBGE basis in February), and with the coming months likely to show even higher prints, a hold or a 25bp move would be more appropriate.

Japan, Bank of Japan (Thursday, March 19): The BoJ will need to tread extremely carefully while establishing as much vigilance as possible due to the country’s very high exposure to imported mineral fuels. The very large release of strategic reserves by the government already points to high levels of concern over domestic prices. An oil shock is exactly the kind of risk-off move that damages Japan’s balance of payments, placing even greater strain on the JPY. We believe intervention risk – on a unilateral or bilateral basis – is non-zero as USDJPY approaches 160, and any pass-through to imported goods would warrant a stronger response, while still balancing fiscal needs.

Taiwan, Central Bank of the Republic of China (Taiwan) (Thursday, March 19): We expect the CBC to keep its policy rate unchanged at 2.0% at the March meeting. The focus will be on its updated 2026 macro forecasts. The CBC currently projects 2026 GDP growth at 7.71% and CPI at 1.68% (as of February 13), broadly in line with DGBAS forecasts of 1.63% to 1.66% for headline CPI. Despite strong growth and the recent inflation uptick, we expect the CBC to retain a neutral stance, leaving the reserve requirement ratio and real estate-related measures unchanged.

Switzerland, Schweizerische National Bank (Thursday, March 19): The SNB has already given a stern warning to markets that sharp appreciation in the franc under current conditions will face intervention. Nonetheless, over the past two weeks, there has been general acceptance of a stronger franc, especially through the EURCHF channel, which continues to generate the bulk of franc nominal effective exchange rate appreciation. As import prices may rise in the near term, allowing franc strength – within a reasonable pace – is a strong enough expression of vigilance, but all options will likely remain on the table.

Sweden, Sveriges Riksbank (Thursday, March 19): The Riksbank had been one of the top candidates in Europe for a resumption of easing after having signaled the end of the cycle, but current conditions perhaps require a more balanced approach. Current demand-dampening features in the Swedish economy are clear and should limit the need for over-reaction but considering easing while ECB pricing is moving in the opposite direction is suboptimal. A low starting point for inflation should limit the need for a strong offset, while language highlighting the need for SEK to realize better valuations could return to the agenda to help prevent pass-through.

U.K., Bank of England (Thursday, March 19): The BoE will likely stay on hold for this decision and hope that the current conflict does not cause a longer-term shift in inflation expectations. Beforehand, Governor Bailey – the main swing voter – had demanded “justification for cuts” in a firm indication that the burden of proof lay with an inflation surprise to the downside, especially through the wage channel. A new supply shock will muddle the situation, though, due to regulatory reasons, energy prices will likely remain low for the next quarter. Cuts have been priced out for now but will likely return if there is de-escalation in the Middle East.

Eurozone, European Central Bank (Thursday, March 19): The language of ECB Governing Council members has clearly shifted in recent days, with some going as far as warning a hike may come “sooner than expected.” A March hike would seem hasty. The rates market now anticipates a full hike by the June meeting, and we would not rule out one or two votes for a move at the upcoming March meeting. Crucially, the new set of staff projections will incorporate moves in energy prices since the conflict began, which could provide some indication of the inflation impact from current levels and where the ECB would deem stronger monetary restraint necessary.

Czechia, Czech National Bank (Thursday, March 19): We expect the CNB to stay on hold at 3.50% at the upcoming meeting. Even though the Czech economy is in a much better position to withstand a supply shock due to fiscal restraint and a lower inflation base, import pass-through can be swift, so vigilance is also necessary. A prolonged rise in energy prices may also generate some government pushback out of necessity, but we expect the CNB will not overreact and will instead monitor the data alongside Eurozone conditions. The prospect of demand-dampening price pressure is much stronger for CEE at present than in 2022 to 2023.

Source: BNY

Source: BNY