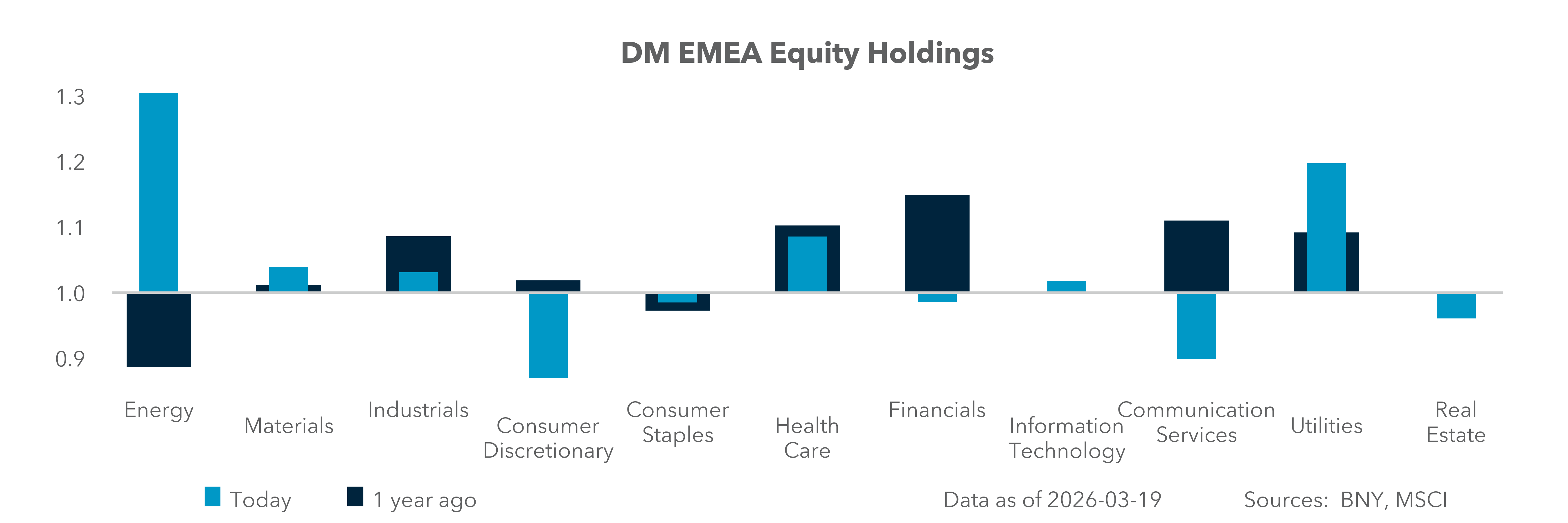

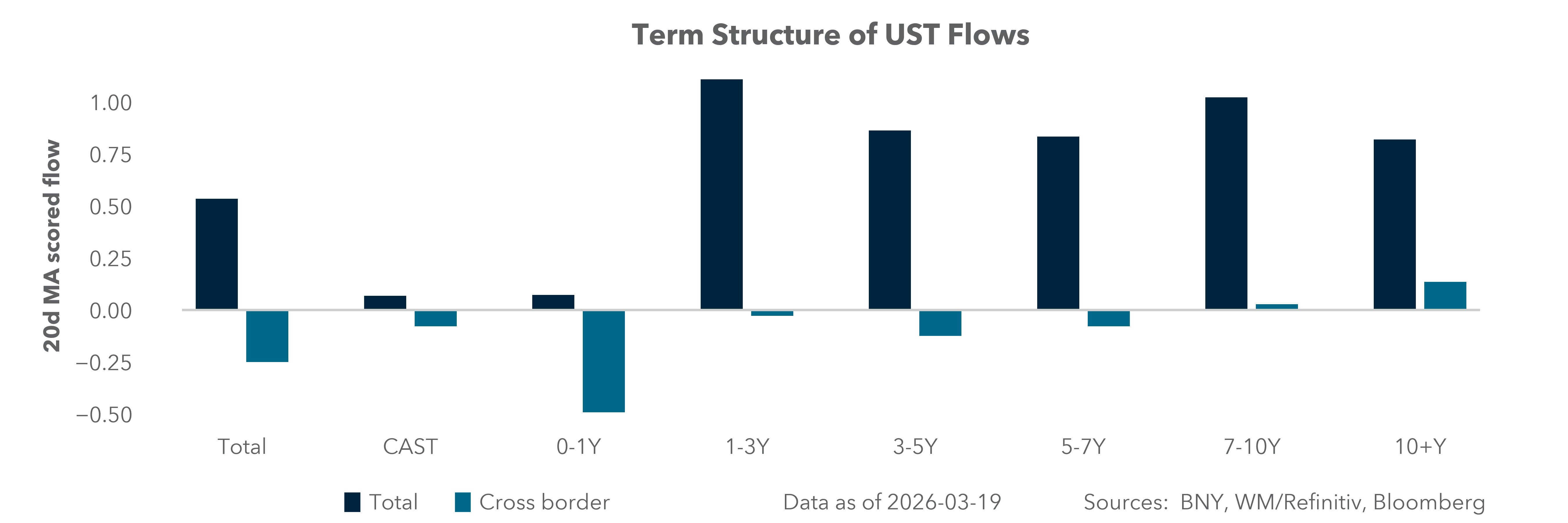

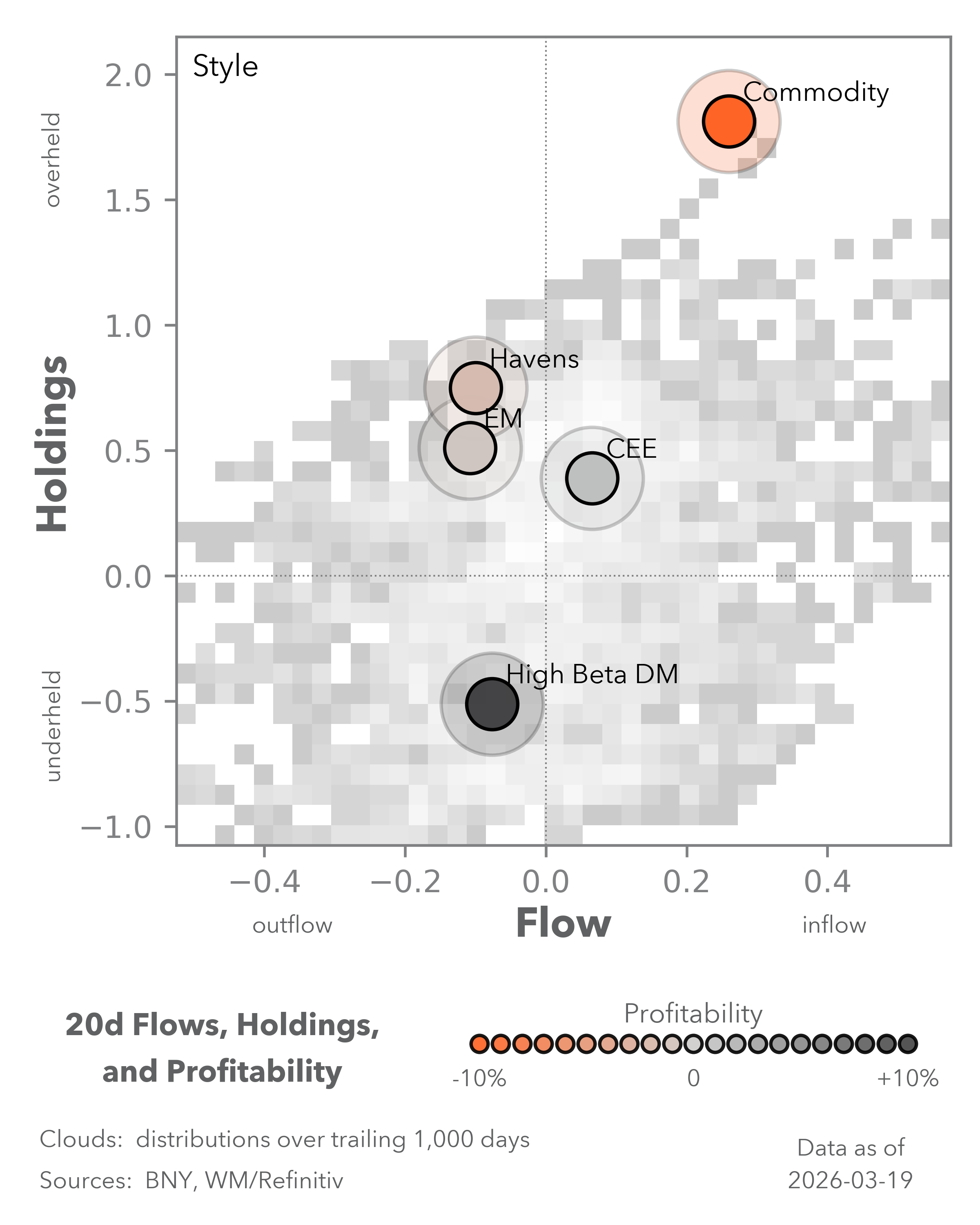

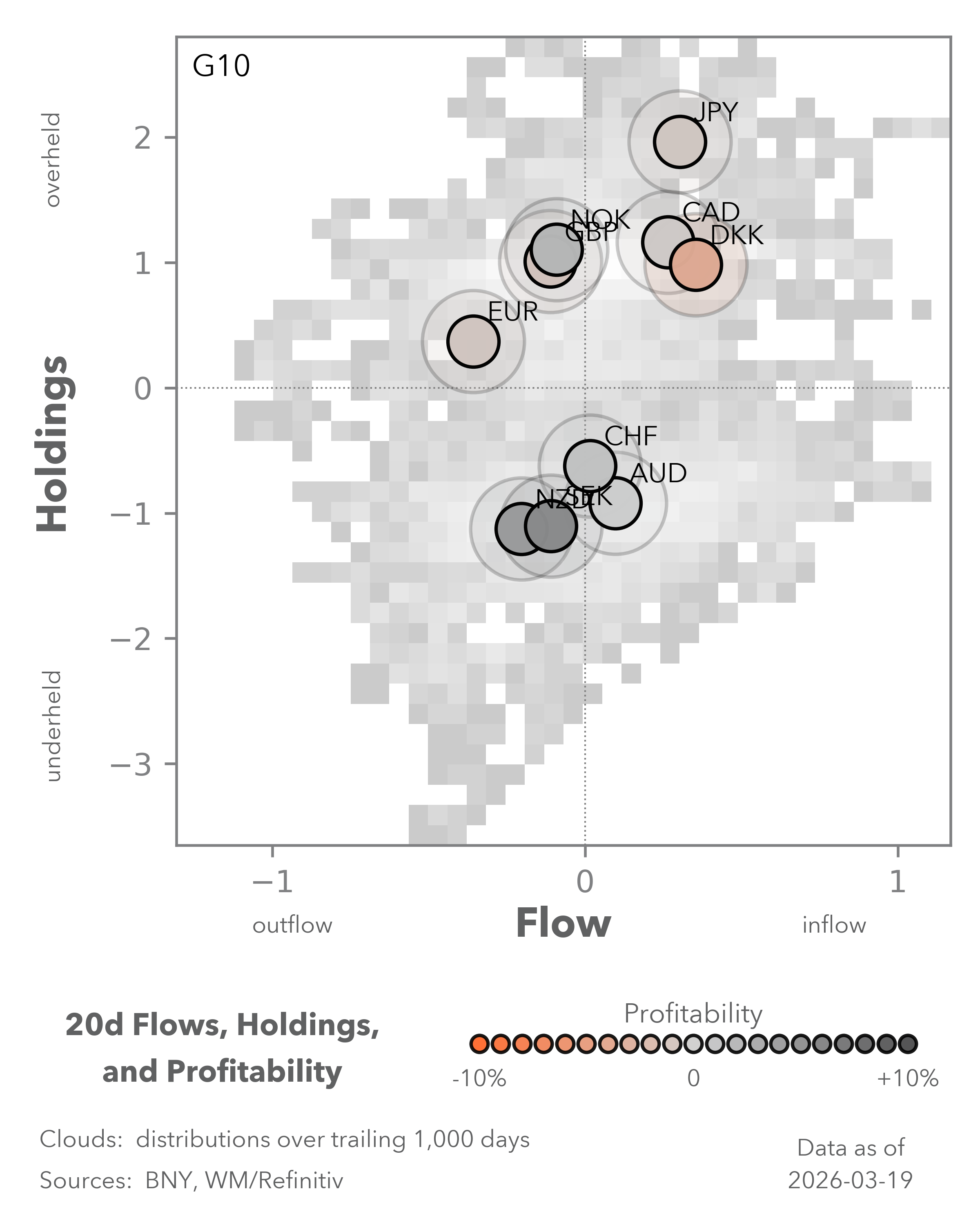

No loose ends

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 8 minutes

Spring begins, but the transition into the next quarter remains unfinished. The coming week will focus on rebalancing and reassessing risks.

After three weeks of conflict in Iran, investors are increasingly fatigued by the lack of resolution. Market reactions have been contained in FX and equities but far more pronounced in commodities and, more recently, rates. The energy shock has triggered a sharp monetary policy reassessment, with the European Central Bank (ECB), Bank of England (BoE), and FOMC all signaling a more hawkish stance than expected. Breakeven inflation rates have surged, while yield curves have flattened, repricing rate hike expectations sharply higher. The risk of further market adjustments is rising, not fading.

Do higher rates mean a rising recession risk?

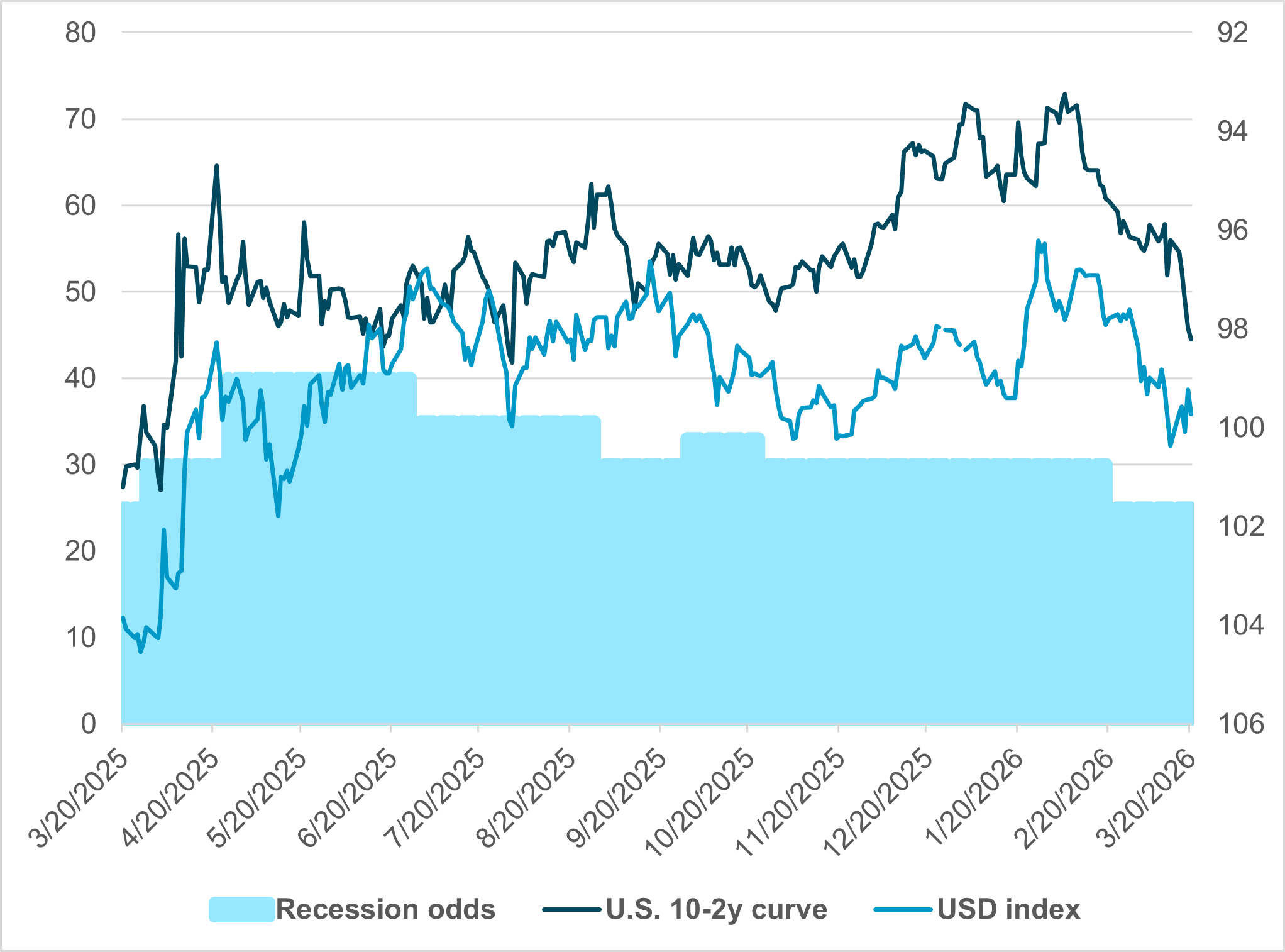

EXHIBIT #1: U.S. 10-2Y BOND YIELD CURVE AND USD INDEX

Source: BNY, Bloomberg

Our take: The front-end of the U.S. rate market matters for how USD and growth views shift. The war and the ensuing energy shock have made rate hike risks real – a dynamic the ECB and others’ actions after “liberation day” 2025 highlight in reverse, showing how FX and front-end rate correlations break down. The role of the curve – and how investors see it reflecting the odds of a recession from outside shocks – is clearly different today. iFlow’s equity inflation factor has flattened out even as breakeven inflation rates are rising. The cyclical vs. defensive equity flows are pointing to a downturn, and this is where the price action of the curve and USD are likely to matter. Financial conditions are tightening fast.

Forward look: Traders are unwinding yield-curve steepening positions and USD hedges, effectively tightening financial conditions for the U.S. and EU markets. This will either lead to further policy concerns or questions about when “demand destruction” emerges instead of “inflation” in markets. The current iFlow Mood index is in the 25th percentile – negative territory – indicating more trouble for market sentiment ahead. The next logical part of the equation for investors is how higher yields everywhere translate to lower growth expectations. Any upside U.S. economic data surprises could be confusing given the balance of inflation fears vs. demand destruction expectations.

North America: Q1 end and Fed speakers drive reactions to energy shock

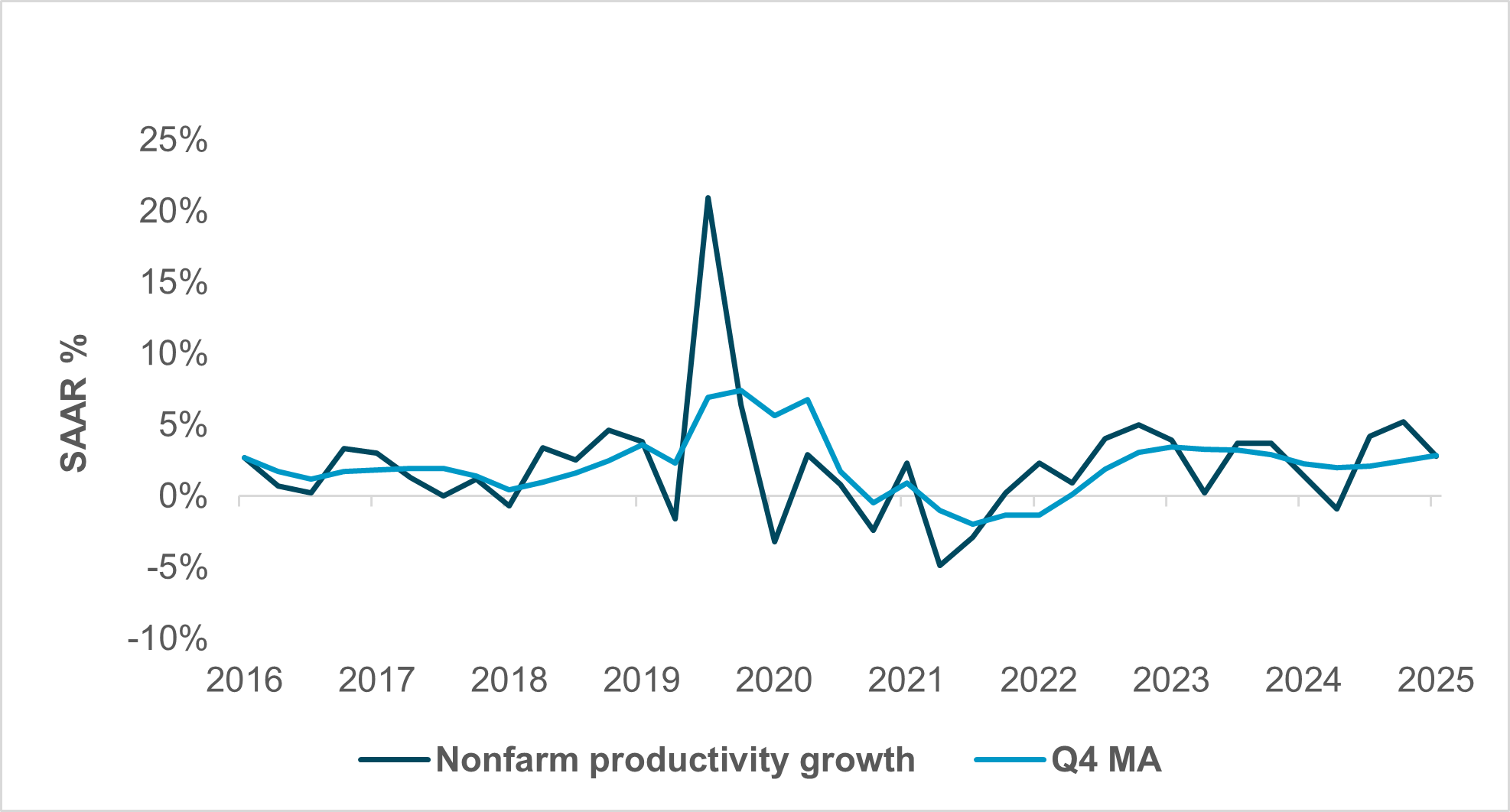

EXHIBIT #2: U.S. PRODUCTIVITY IS A KEY PART OF ECONOMIC RESILIENCE TO ENERGY PRICES

Source: BNY, Bloomberg

Our take: This week is light on U.S. data, but news flow will not be. We’ll hear from Fed speakers now that the pre-FOMC blackout has lifted, and the conflict in the Middle East will spark plenty of headlines and market reaction. It’s also the last week before quarter end, so investor positioning is likely to shift in preparation.

Forward look: Regional PMIs from the Richmond, Philadelphia and Kansas City Feds, the S&P Global U.S. PMI, the final Q4 productivity, and the usual weekly ADP employment change report are all expected Tuesday, with weekly jobless claims following on Thursday – the latter of which has been quite benign lately. The final University of Michigan Consumer Sentiment print is expected on Friday.

Given the lack of scheduled events, we expect another week dominated by conflict headlines, oil price developments, and the fallout from last week’s central bank meetings.

EMEA: Pulling back inflation and rate expectations; Meloni faces key vote

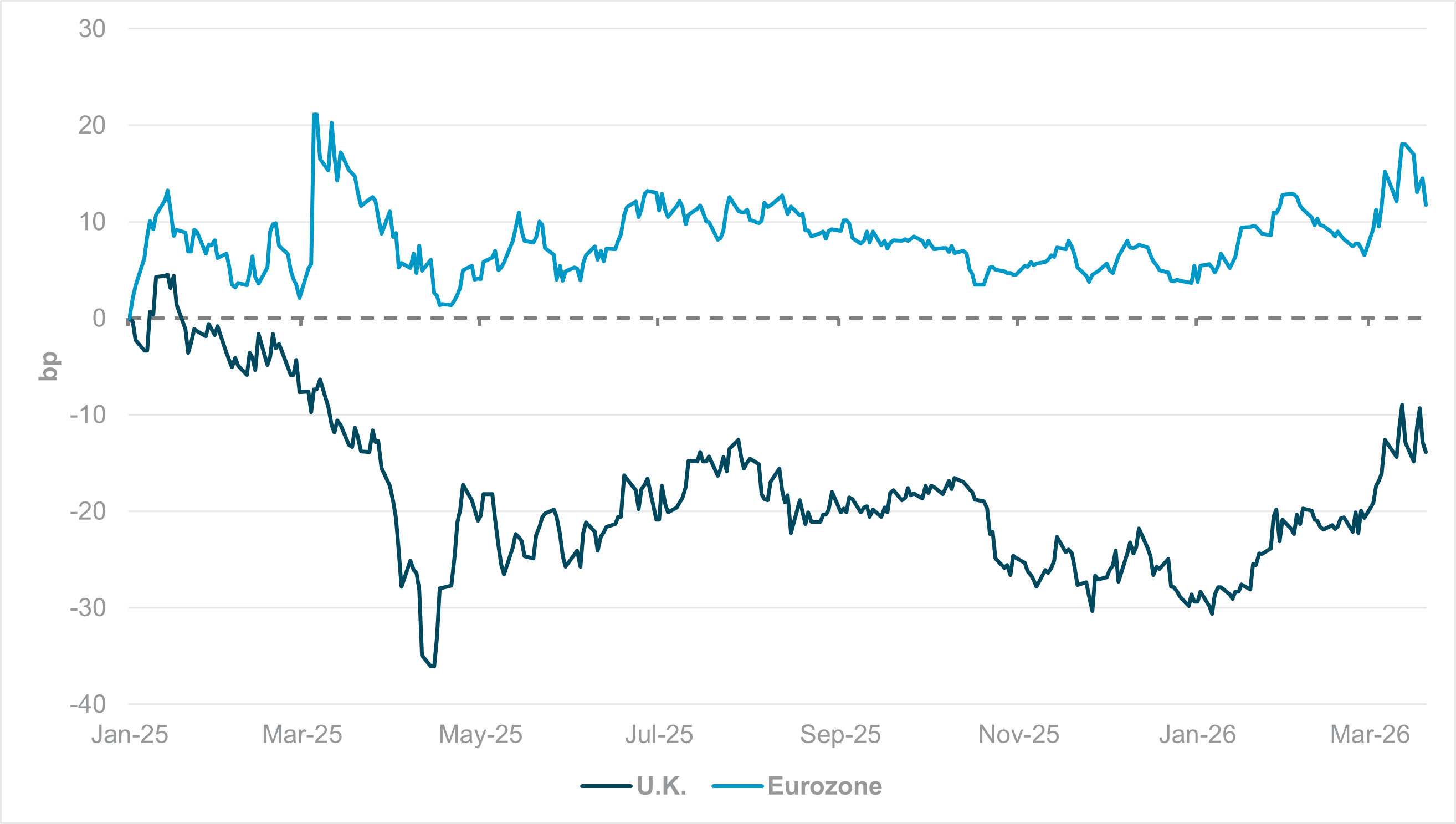

EXHIBIT #3: CHANGE IN 5Y5Y INFLATION SWAPS – U.K. AND EUROZONE

Source: BNY

Our take: We believe the moves in European rates markets in response to rising inflation are beginning to look detached from fundamentals. The biggest moves were in the U.K., rekindling memories of the 2022 mini-budget crisis, despite no evidence that the current government’s reaction function will be anything close to what materialized in 2022. We acknowledge that the 9-0 vote by the BoE’s monetary policy committee was a surprise. However, household behavior and the labor market outlook both support the prior assessment that the U.K. economy is approaching late-cycle. If rate expectations rise, we believe households will likely retrench further.

Mortgage fixes are already higher due to the sharp moves in swap rates to which they are benchmarked. Precautionary savings (already at 9.5% as of Q3 2025) will likely rise further to pay higher utility bills, as U.K. households are highly exposed to indexation. Crucially, the BoE perhaps should have elaborated – unlike their peers on the Continent – on the point that inflation expectations remain under control.

This was Governor Andrew Bailey’s message after the decision, where he warned markets against “strong conclusions” on rate hikes and stressed that the context compared to 2022–2023 was also different. Some ECB members, including Banque de France’s governor François Villeroy de Galhau, have stated the same. The Swiss National Bank’s own conditional inflation forecasts pointed to marginal changes in their headline CPI outlook over the forecast horizon. Even after the large moves in natural gas prices in Europe, inflation swaps (Exhibit #3) have not moved aggressively: compared to the beginning of 2025, U.K. inflation expectations are only back to levels seen in the immediate aftermath of “liberation day” tariffs, while Eurozone inflation expectations remain lower. We would not rule out hikes in the near term, but any moves need justification in shifting expectations, and nothing points to more than precautionary moves rather than a new cycle. That said, new information is needed. Next week’s release of the ECB’s February 1y and 3y CPI expectations has more limited information value.

Forward look: Otherwise, it will be a quiet data week, but the ECB will be very attentive to the preliminary March PMI and ifo releases out of Germany, which will provide the first indications of the impact on the conflict for industry and exporters, especially in terms of input costs. Supply manager surveys are critical in the current environment, as fiscal, regulatory, or even diplomatic measures to mitigate the energy shock can be adopted more quickly than transmission through EU-wide adjustments or monetary policy. The best base-case scenario would be for limited change in the demand and output figures, but short-term increases in expectations for input costs are unavoidable. The February print of 50.9 was the first recovery into expansion territory this cycle, but the ECB and governments are resigned to the fact that positive momentum has probably vanished for now.

On the political side, we expect ongoing EU negotiations on emergency energy mechanisms, while the Hungary veto of a Ukraine loan remains a key point of contention. The constitutional referendum in Italy will also be a key test of Prime Minister Giorgia Meloni’s domestic standing. Meloni is often seen as President Trump’s strongest ally in Western Europe and an anchor of current EU policy, so any erosion of her domestic standing will have material implications for the bloc’s decision-making at a critical juncture, given her strong working relationships with France and Germany. The outcome currently remains highly uncertain. From a market perspective, anything that could lead to a questioning of Italy’s fiscal outlook – a European financial success story in recent years – will only add to volatility in eurozone government bond markets, which are already struggling with an inflation shock.

APAC: CPI, trade data, and business sentiment in focus

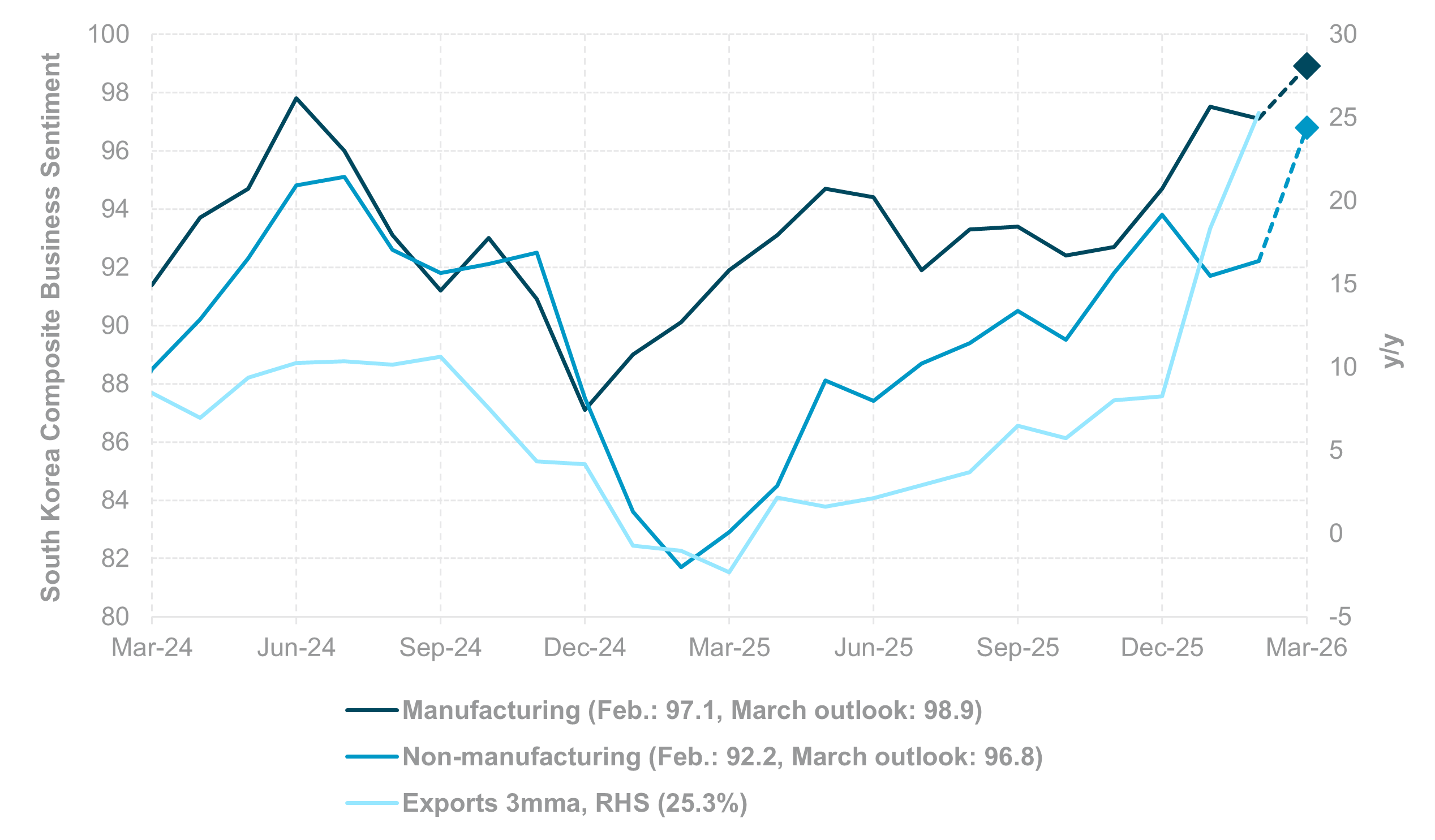

EXHIBIT #4: SOUTH KOREA COMPOSITE BUSINESS SENTIMENT INDEX

Source: BNY

Our take: APAC’s data calendar this week is dominated by inflation prints and early trade indicators, with Japan’s February national CPI the key focus – though near-term inflation trends may be distorted by the surge in oil prices and currency weakness. January headline and core (ex-fresh food and energy) CPI slowed to 1.5% and 2.6% y/y, respectively, from ~3.3% in June 2025. Attention will also turn to the upcoming wage negotiations, with Rengo set to report next week after demanding a 5.94% wage increase for 2026 (vs. 6.09% in 2025).

In Australia, the February monthly CPI indicator will be critical in validating current rate hike expectations and the bullish AUD outlook, after the Reserve Bank of Australia (RBA) raised rates by 25bp last week to 4.1% with an emphasis on upside inflation risks. Singapore’s February CPI will guide domestic price pressures ahead of the MAS policy decision in mid-April. Activity indicators – including March PMIs for Australia, Japan and India, and South Korea’s March Composite BSI – will provide insight into regional manufacturing momentum amid the Iran conflict. South Korea’s 1–20-day export data will be closely watched for signals on semiconductor shipments and global tech demand. Additional releases include Taiwan industrial production, Thailand exports and manufacturing output, and trade data from the Philippines. Overall, inflation dynamics and business sentiment remain the key themes.

No central bank meetings are scheduled this week. The next decisions (RBNZ, RBI, BoK) are due in early April.

Forward look: Extreme market volatility and geopolitical uncertainty remain the primary drivers of APAC risk, and any further reduction in risk appetite would amplify cross-asset moves. Last week’s marginal hawkish tilt from Taiwan and the Philippines’ central banks – flagging potential tightening if oil prices remain elevated – is notable but unlikely to become the regional baseline. Instead, central banks and governments are expected to shift further into defensive mode: intensifying FX intervention to smooth volatility and deploying macroprudential measures to cushion living costs. This, however, may add to fiscal pressures. INR, IDR, KRW, and PHP remain the most vulnerable, hovering near key psychological levels. Overall, we stay cautious with risks skewed to the downside.

In contrast, we expect the Chinese yuan to remain relatively supported and outperform within the region.

The interplay between energy supply disruptions, monetary policy recalibration, and evolving growth expectations will define market direction into the next quarter. The sharp repricing of front-end rates and flattening yield curves signal tightening financial conditions that are increasingly inconsistent with resilient growth narratives. Investors should be prepared for a transition from inflation-driven concerns to demand destruction risks, particularly if higher energy costs persist and begin to erode consumption and industrial activity. Central bank communication will be pivotal, as policymakers balance credibility on inflation with emerging downside risks to growth.

In FX and rates, cross-asset correlations are likely to remain unstable, requiring more dynamic hedging and positioning strategies. Portfolio resilience will depend on navigating elevated volatility, reassessing exposure to cyclicals, and identifying relative value across regions where policy responses and energy sensitivities diverge. The risk environment remains asymmetric, with downside growth surprises likely to dominate.

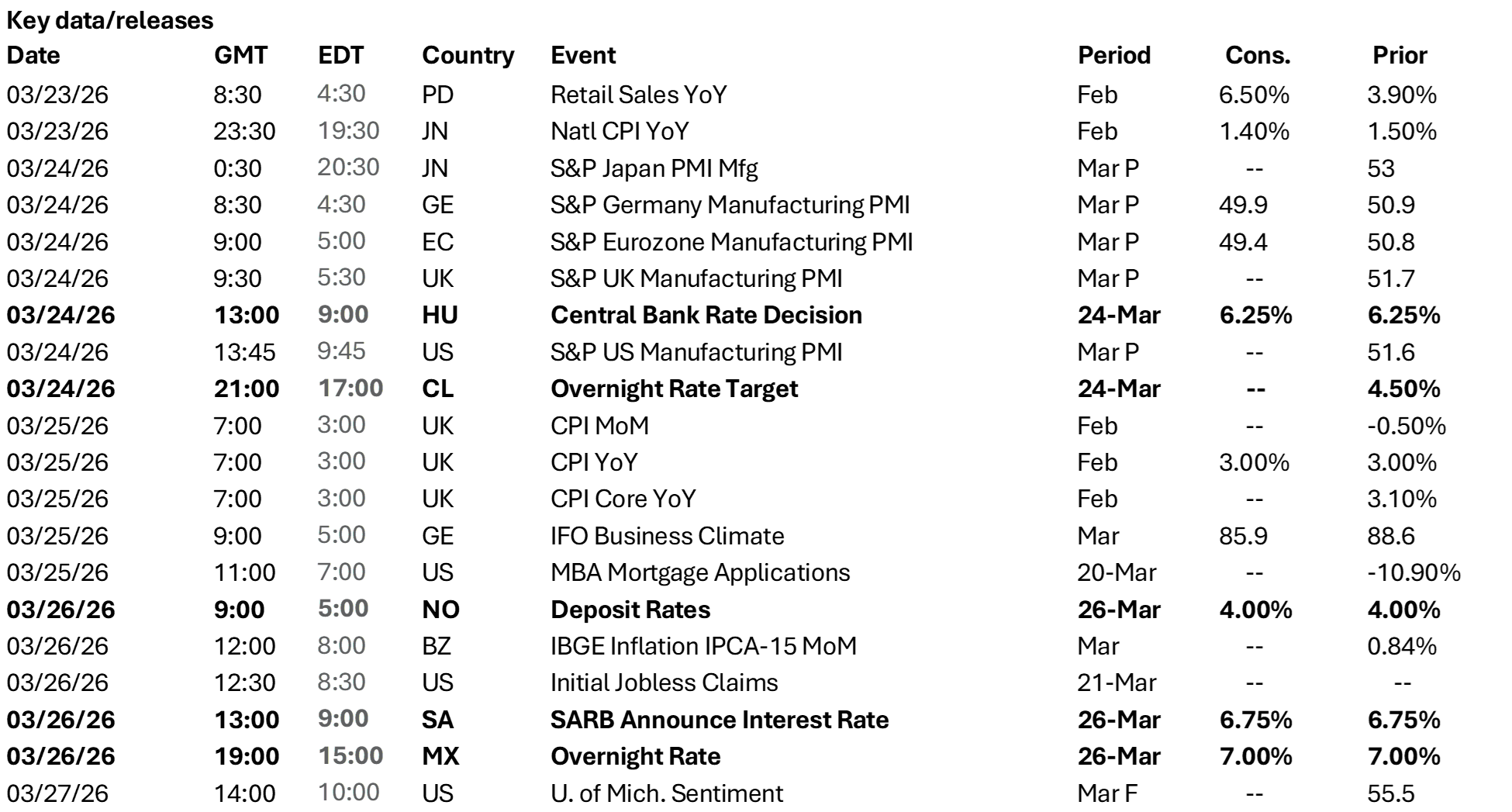

Central bank decisions

Hungary, Magyar Nemzeti Bank (Tuesday, March 24): The MNB is expected to keep rates on hold at 6.25%, and we doubt there is any scope for easing soon. Across Europe, inflation looks set to pick up, and Hungary faces its own set of energy distribution issues that are already leading to difficult conversations with the rest of the EU. Crucially, the country has imposed caps on energy prices, but this will have the effect of artificially depressing real rates through the fiscal channel as headline inflation will begin gaining in other areas. For now, the rate buffer is sufficient, but circumstances have changed and expectations can shift very quickly.

Chile, Banco Central de Chile (Tuesday, March 24): The BCC is expected to keep rates on hold at 4.50%. LatAm is not seen as exposed to the current conflict as EMEA and Asia. Strong inflows into LatAm debt markets reflect that, even as the rest of the emerging markets space is struggles with outflows. However, commodity producers outside of energy are also struggling right now with prices and are not immune to broader supply risks.

Norway, Norges Bank (Thursday, March 26): Whatever remaining hope Norges held for cuts has been swept away by the conflict in the Middle East, but Norway is in a unique position to lean against inflation risk through its positive terms of trade outlook. Energy-related receipts will rise sharply from current levels, and the initial stages will generate a stronger NOK to keep tradables inflation low. At some point, there will be a sufficient shift in balances for NOK sales but until then, policy will remain vigilant and there is no need to signal hikes yet – though it cannot be ruled out either.

South Africa, South African Reserve Bank (Thursday, March 26): Expectations for South Africa have shifted rapidly since the beginning of the conflict. What seemed to be autopilot toward additional easing and even stronger fiscal consolidation is now at risk due to the energy price and supply outlook. Wage settlements are also erring to the high side, and the real rate outlook has deteriorated accordingly. SARB will need to signal an end to its easing cycle and put hikes fully back on the table, lest the market bring through balance of payments concerns.

Mexico, Banco de México (Thursday, March 26): Banxico will be looking for a balanced approach, but there is little room for easing right now as global financial conditions have shifted materially. The current conflict could well prove supportive for Mexico’s terms of trade on the margins, but other input costs will need close monitoring as well given global prices for energy and raw goods remain a factor. There is sufficient space in nominal and real terms for rates to support the MXN – reflected in our holdings and flow data – but additional vigilance is necessary.

Source: BNY

Source: BNY