Ceasefire relief, energy reality

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 11 minutes

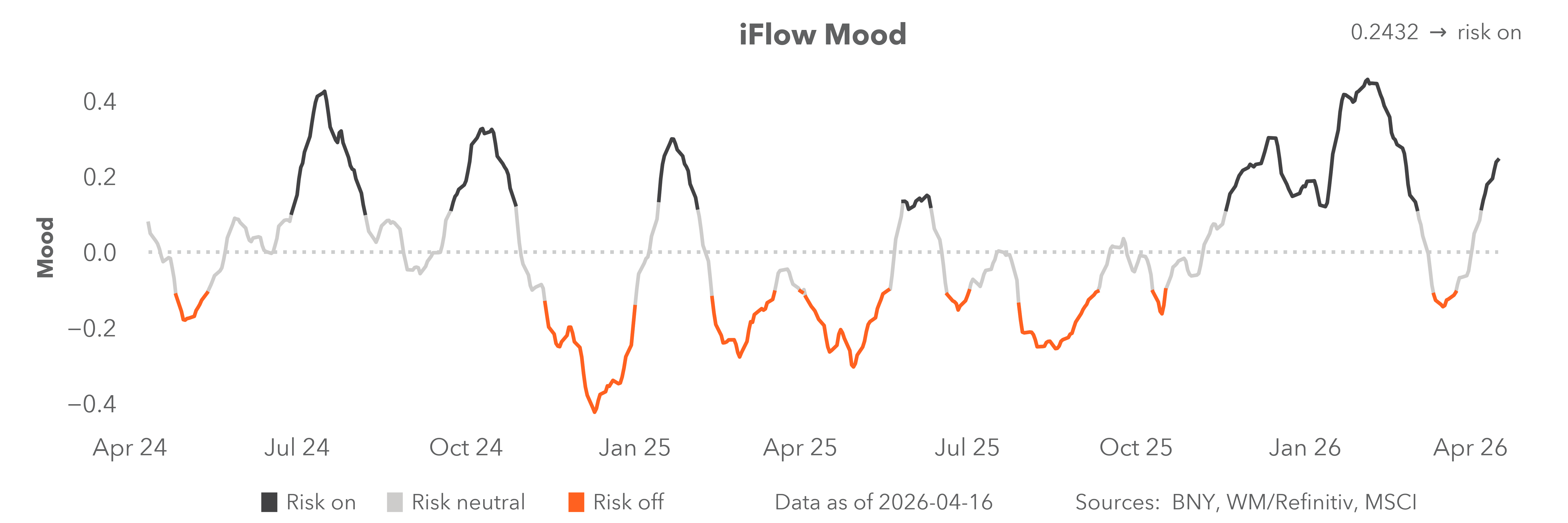

The ceasefire changed market sentiment last week and remains the most critical driver for risk this week, though the subsequent rise in global asset prices has reset some war-related fears. The sentiment cost of the conflict has been fully recovered, but the economic cost is another matter. IMF meetings highlighted concerns over energy supply shocks and the risk that AI agentic models are moving from disruption to destruction. That focus shift will be shaped by the economic data this week, alongside ongoing headlines about a path to a sustainable truce in the Middle East.

What will matter next?

The critical barometer of geopolitical risk has been distilled into one datapoint: the number of ships transiting the Strait of Hormuz. Last week saw a peak of 15 ships pass through the chokepoint. In order for energy and other materials to normalize, this number will need to quadruple. Peace talks matter, but the immediate focus is on oil and other supply shortages driving inflation. The oil-to-inflation-to-front-end-yield transmission channel is the critical mechanism for sizing the conflict’s economic impact.

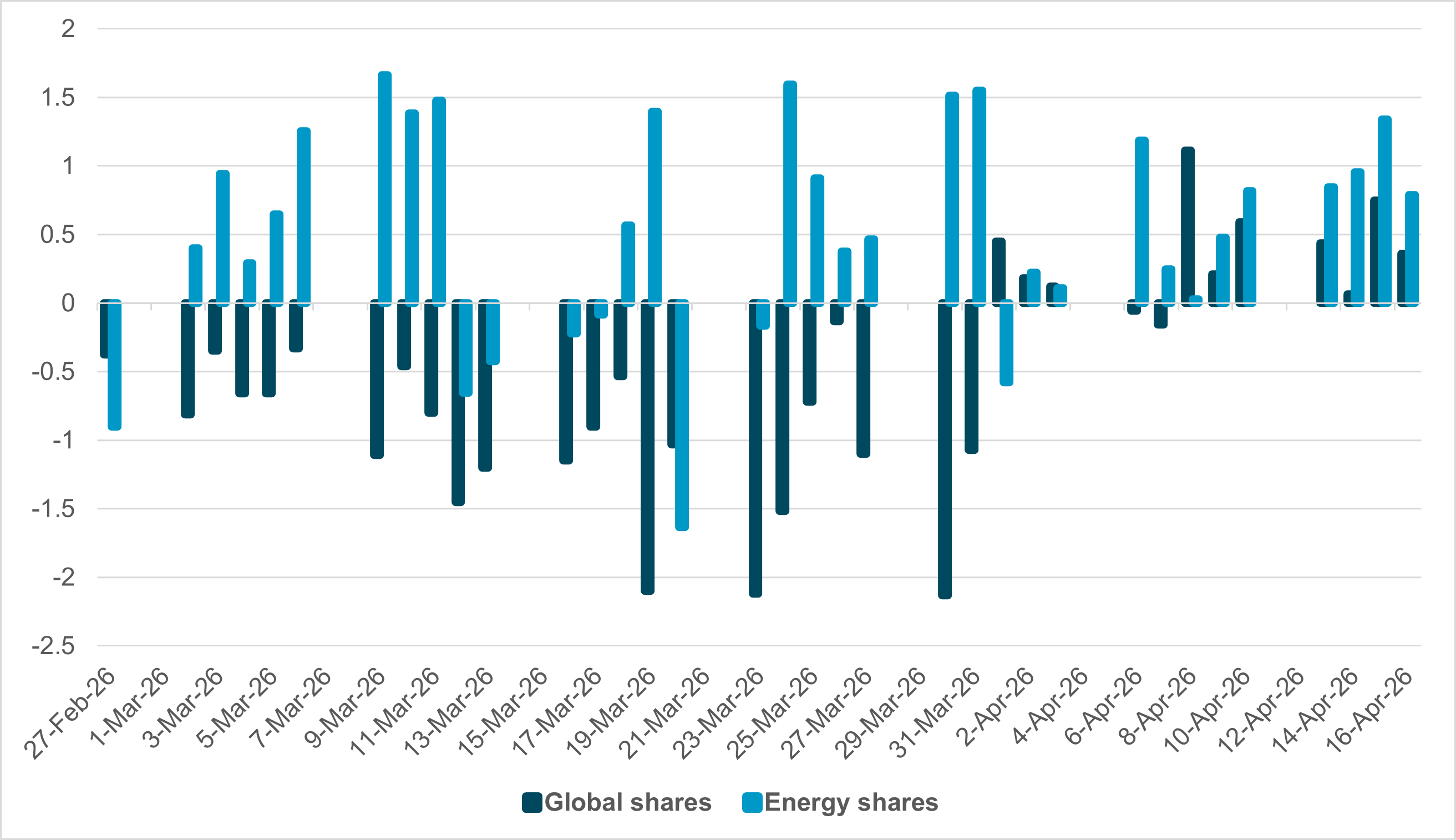

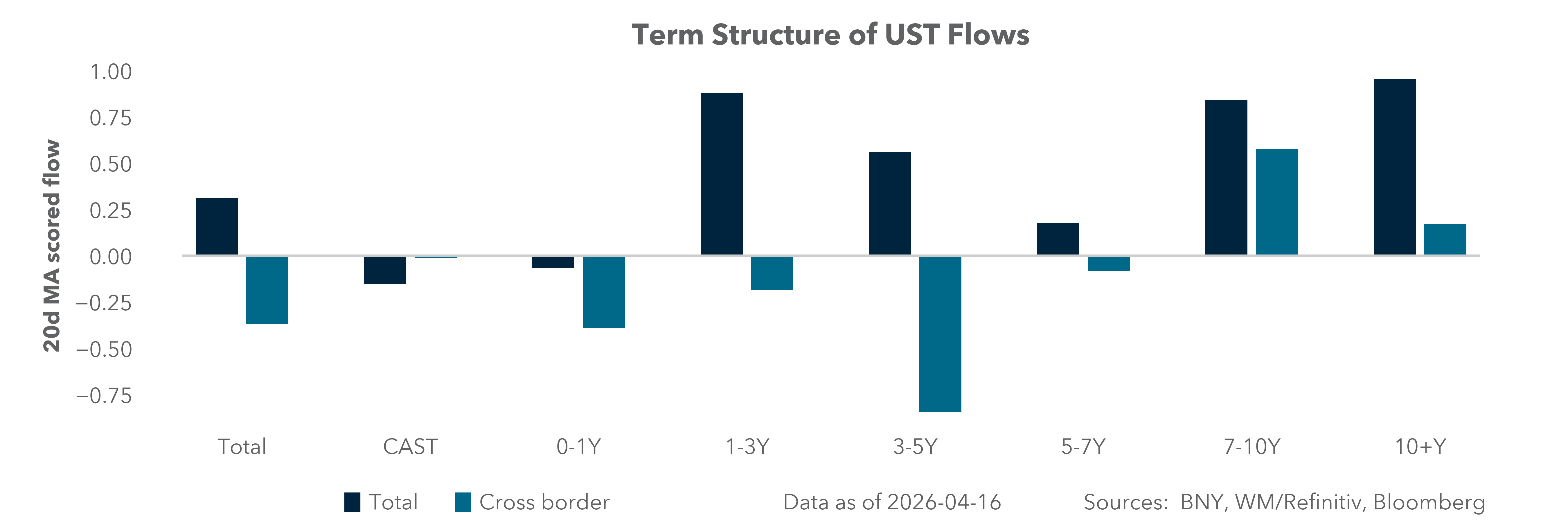

EXHIBIT #1: ENERGY VS. GLOBAL EQUITY FLOWS

Source: BNY, Bloomberg

Our take: Global shares buying has stood out since the ceasefire, while energy sector buying was clearly seen as a safe haven – a trend that appears to persist regardless of the oil price. Overall, flows in both categories look modest but steady: not outsized, but trending.

Forward look: Energy’s role of in pushing up CPI headlines will not fade as quickly as the worst-case scenario war risk premium in markets. The asset allocation question over the next few weeks rests on how much energy exposure remains in portfolios relative to other sectors. Earnings and the oil price will both be central to this story. The greater challenge for investors is the anticipated divergence in the bond-equity correlation – something seen since the war started.

North America: U.S. data takes a back seat to earnings and geopolitics

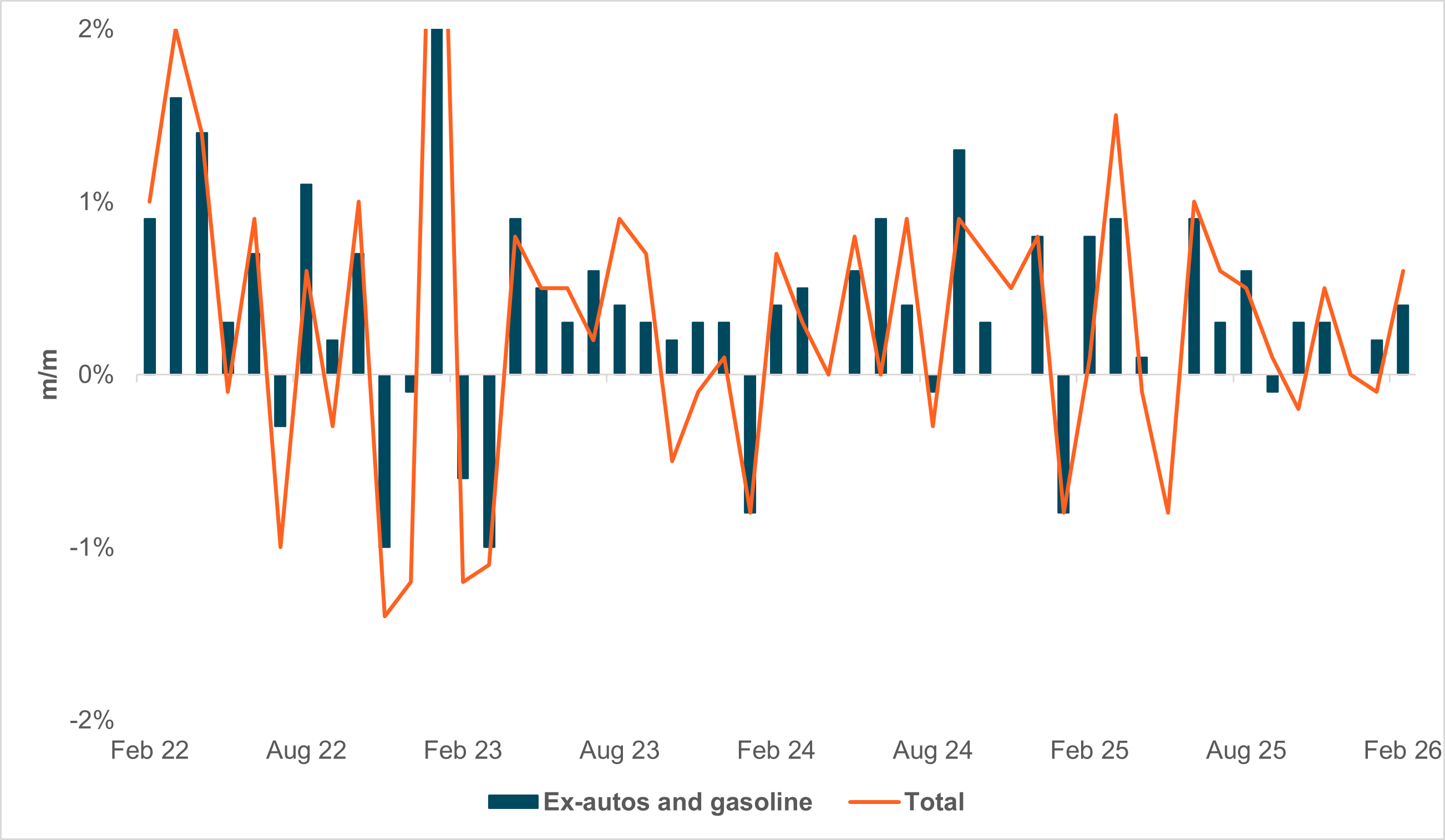

EXHIBIT #2: U.S. RETAIL SALES AND THE GASOLINE EFFECT

Source: BNY Bloomberg

Our take: War (or peace?) headlines will likely dominate the news flow this week, which features precious little data and no Fed speakers given the pre-FOMC meeting blackout is in effect. Monday could see the markets reprice any new developments depending on the outcome of this weekend’s discussions around extending the ceasefire. The slim data docket includes retail sales, pending home sales (Tuesday), and the S&P Global PMIs (Thursday).

Forward look: With Fed speakers off the airwaves and limited macroeconomic data, we expect a full earnings week to add key market-moving information to geopolitical headlines. Some 130 companies listed on the S&P 500 report earnings, ranging from railroads and large industrial conglomerates to aerospace and technology.

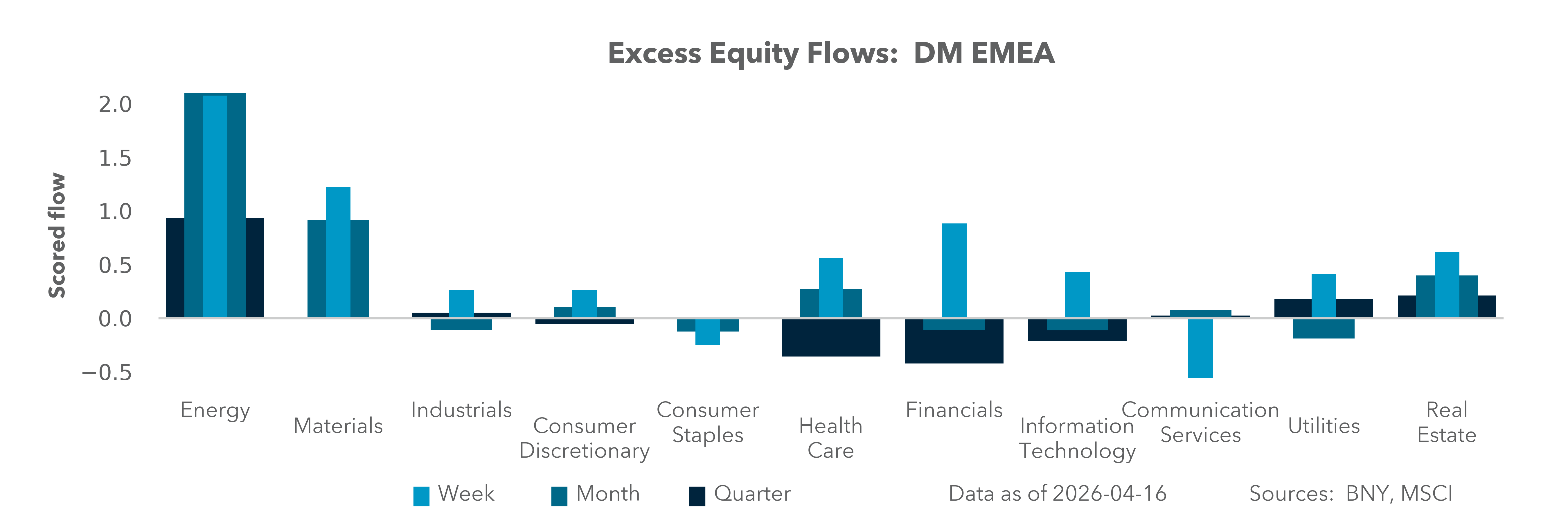

EMEA: Activity levels may need to take precedence over prices in leading indicators

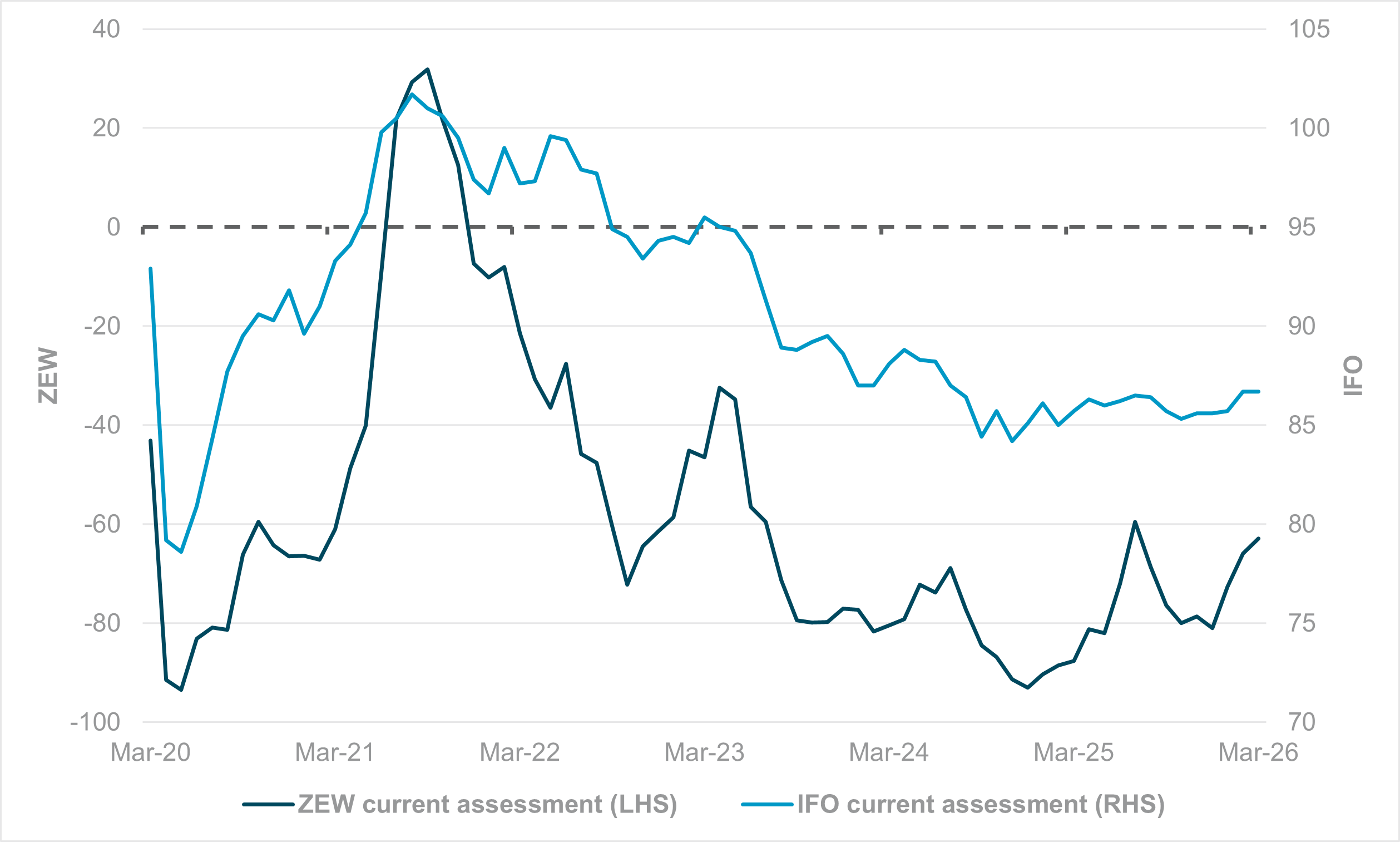

EXHIBIT #3: CURRENT ASSESSMENTS SURPRISINGLY RESILIENT IN MARCH, BUT DETERIORATION LIKELY

Source: BNY

Our take: Germany’s three key leading indicators – IFO, ZEW and PMIs – are all due this week, as the ECB heads into the blackout period ahead of its month-end policy decision. By all accounts, the April meeting is “live,” with some Governing Council members stressing that it may be appropriate to act even before the entire picture on second-round price effects becomes clear. This will set it apart from its global peers, but strict adherence to price stability is to be fully expected.

Most central banks in Europe and globally do not have a strict growth or Fed/Reserve Bank of Australia-style full employment mandate, but it would be remiss of monetary authorities to discount underlying demand conditions when setting policy. While unlikely to be the base case for the ECB at present, there is a strong chance that households and corporates have retrenched enough in recent weeks to open a demand gap sufficient to offset any upside price risks from supply. Policymakers’ poor assessment of a large mismatch in 2022–2023 does not mean the scenario does not exist. Consequently, it will be essential to look at the upcoming surveys holistically: input prices and their expectations are fully expected to maintain elevated levels, but if current conditions drop sharply, the case for an early hike may not be as clear-cut.

The current assessment figures for ZEW, IFO (Exhibit #3) and PMIs were surprisingly resilient for March. Sampling was likely carried out during the weeks of material uncertainty. While the forward outlook was already deteriorating and input costs registered clear gains, there were no signs of orderbooks collapsing or sudden stops in production due to shortages of raw materials or intermediate goods. ECB hawks should note that in absolute terms, current conditions remain toward the low end of multi-year ranges – a far cry from the post-COVID demand explosion, which was still working its way through the global economy in 2022. Either way, the ECB should fully acknowledge the risk of asymmetry: “resilience” at a low level does not indicate sustained economic strength that could exacerbate the price shock, while clear deterioration would point to further retrenchment – one that a rate hike would only aggravate.

Forward look: Leading indicators aside, there will be a final round of ECB speeches encompassing the entire hawk-dove spectrum, and President Christine Lagarde may provide some final guidance to the market before the quiet period. The establishment of a durable ceasefire over the intervening period may also weigh on the decision, as could escalation – though risk sentiment appears to be framing that as a tail scenario.

Outside the Eurozone, the U.K.’s March inflation figures are due, and we expect a continuation of the European tendency to register a sharp divergence between headline and core inflation. Subdued household demand is well-established in the U.K., and BoE hawks show no inclination to hike, particularly if wage figures continue to cool. That said, this week’s data likely lack sufficient information value to reflect developments since the conflict began.

Türkiye’s TCMB decision is the only key central bank meeting of the week. We expect it to continue anchoring high nominal rates to stave off any additional balance of payments pressure. Even with double-digit inflation and strong fiscal impulse in place, a rate hike is not in the cards for the same reasons it shouldn’t be seriously considered in developed economies.

On the political side, markets will continue to assess the speed at which Hungary’s Prime Minister-elect Péter Magyar can assume office (his target is early May) as pressing matters at the national and EU-level – on the economy and Ukraine – may require his presence to resolve urgently.

APAC: Regional Inflation and trade, India and Australia PMI, BI and BSP policy meeting

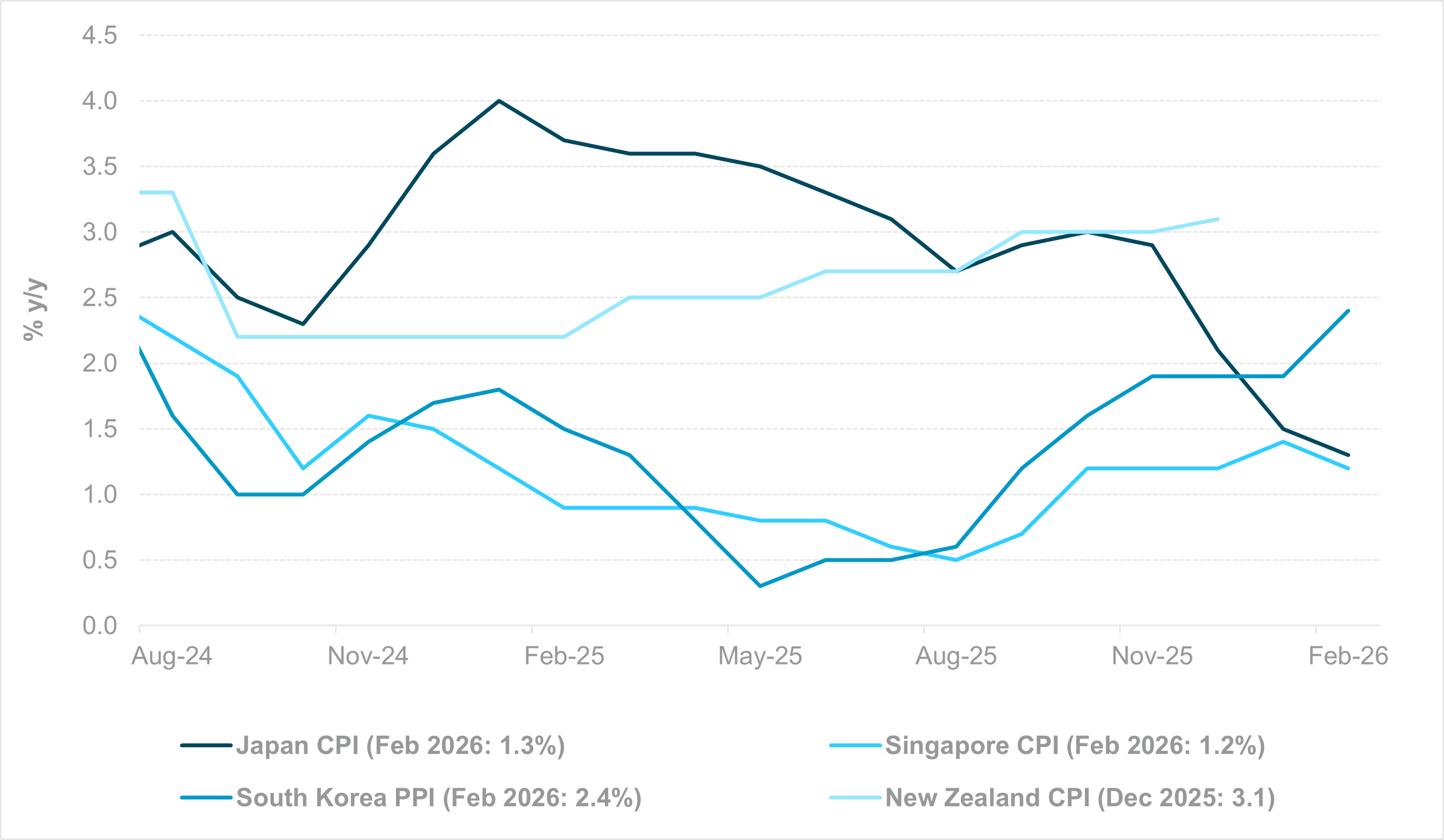

EXHIBIT #4: INFLATION TREND: JAPAN, SOUTH KOREA, SINGAPORE AND NEW ZEALAND

Source: BNY, Bloomberg

Our take: The week ahead is anchored by a dense slate of trade and inflation data across Asia, alongside key central bank meetings. In North Asia, South Korea’s Q1 GDP is the primary focus, while early-April export data (1–20 days), along with Taiwan’s export orders and industrial production, will be closely watched for signs of tech cycle traction. Trade releases from Japan, New Zealand, Malaysia, and Thailand will help gauge regional export recovery and the impact of higher oil prices on imports and trade balances.

Notably, import prices surged in March in Taiwan (+4.8% y/y, Feb: -1.0%) and South Korea (+18.4% y/y, Feb: +1.6%). Inflation indicators, including South Korea’s March PPI, Singapore’s March CPI, New Zealand’s Q1 CPI, and Japan’s March national CPI, will be key to assessing price pressures.

On sentiment, India and Australia PMIs are likely to confirm a deterioration in outlook amid the prolonged Iran conflict; both consumer and business confidence in Australia plunged in March by a magnitude comparable to the GFC and COVID periods. Japan’s heavy data slate (CPI, PMI, services) will provide a comprehensive read on domestic demand and inflation ahead of the Bank of Japan meeting next week.

Elsewhere, the Philippines’ BSP and Bank Indonesia are expected to hold rates, as monetary policy remains a blunt instrument against supply-driven inflation shocks. Overall, the week’s data should offer an early read on the pass-through of elevated oil prices to trade balances and inflation.

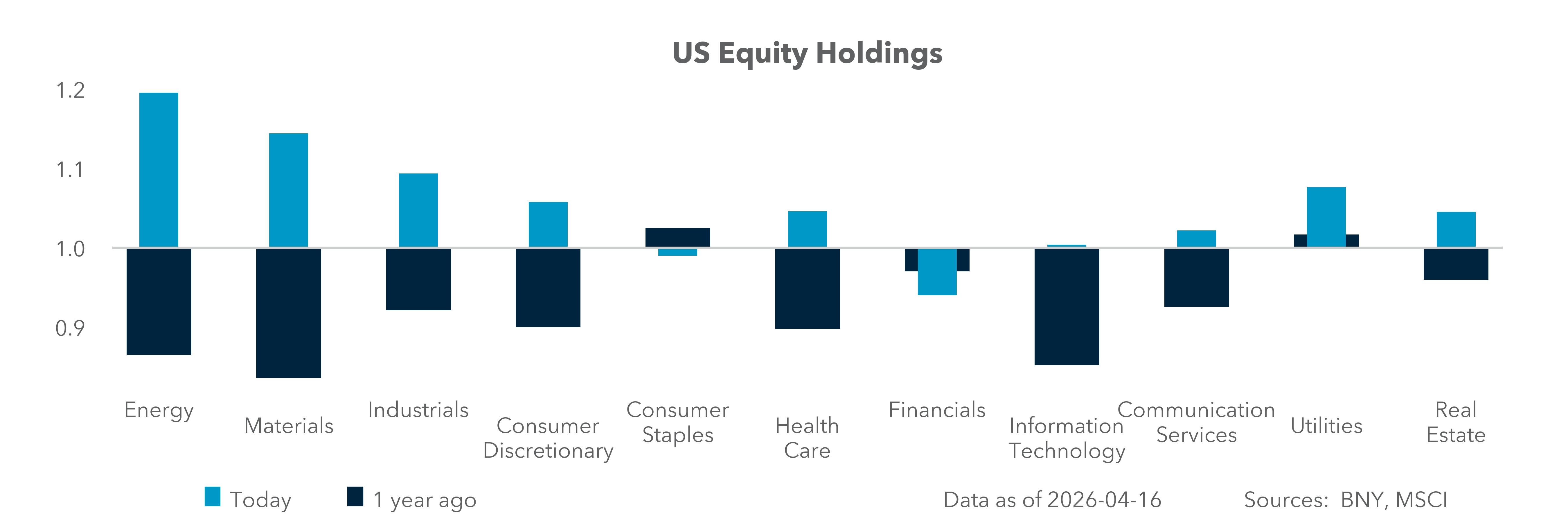

Forward look: We remain constructive on equities, supported by accelerating investor demand (BNY iFlow), but the outlook for APAC FX is less straightforward. We stay cautious on net oil-importer currencies as crude remains elevated in absolute terms, lagging the broader normalization in other asset classes and continuing to pressure terms of trade via higher import costs. CNY has remained resilient through recent geopolitical stress and is among the best-performing APAC currencies YTD (around 2.5%), alongside MYR. Ongoing foreign inflows into Chinese equities should continue to support CNY, while reduced short positioning (lower scored holdings) signals improving investor confidence. Recent regulatory measures to curb depreciation may offer near-term support, but effects are likely transient as long as elevated oil prices and capital outflows persist. For example, South Korea’s National Pension Service (NPS) scrapping the 15% FX hedge cap, and India’s import controls and NOP limits, have not delivered sustained KRW and INR rallies.

In APAC FX, we are overweight CNY, SGD and MYR, underweight INR, PHP and THB, and see upside in KRW and TWD on anticipated renewed foreign equity inflows.

The near-term market regime is shifting from acute geopolitical risk repricing toward a more complex macro-financial balancing act. While the ceasefire has restored risk appetite, the transmission channel from energy prices to inflation and front-end yields remains the dominant constraint on asset allocation. Investors should expect markets to show heightened sensitivity to oil dynamics, particularly via inflation expectations and central bank credibility.

The upcoming data cycle – spanning U.S. activity, U.K. inflation, China policy, and European PMIs – will be critical in determining whether growth can absorb elevated input costs without reaccelerating inflation, shaping both the durability of the equity rebound and the direction of global yields.

Portfolio construction should prepare for a potential return of negative stock-bond correlation, alongside persistent strength in energy-linked exposures. Selectivity across regions and sectors – particularly in balancing cyclicals against inflation hedges – will be essential as earnings and macro signals increasingly diverge.

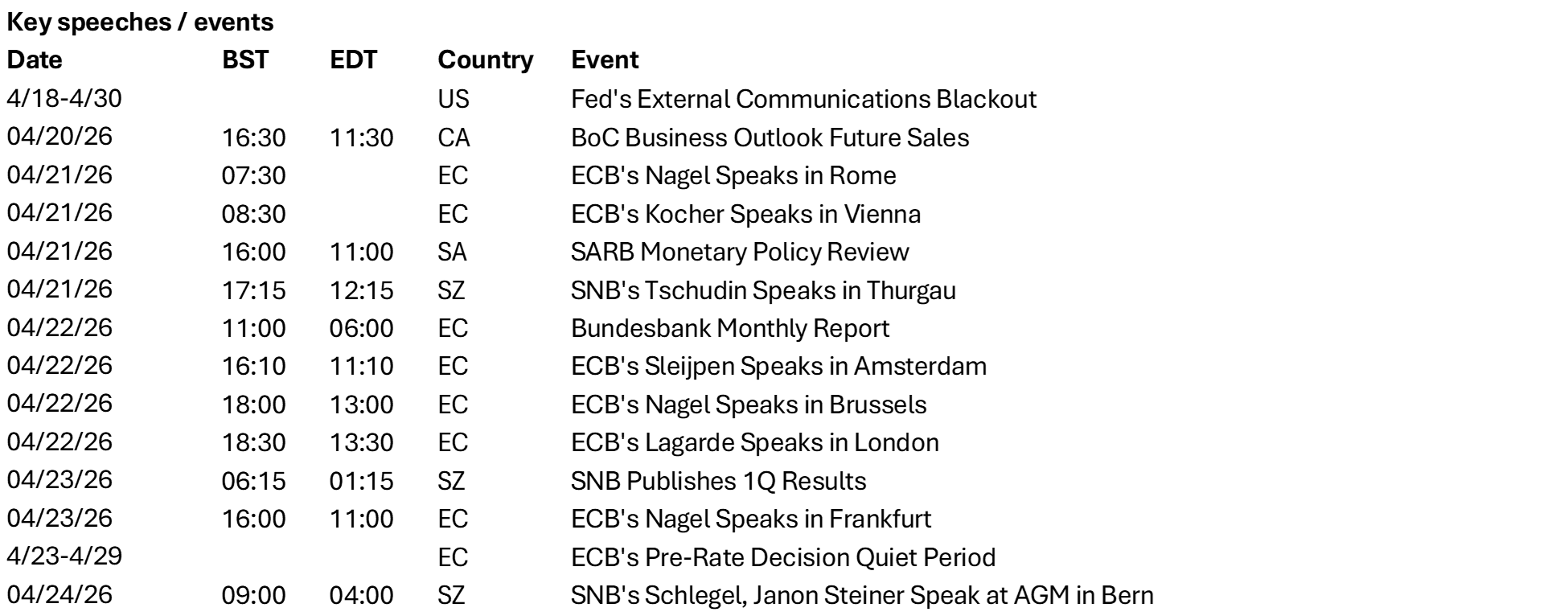

Central bank decisions

Indonesia, Bank Indonesia (Wednesday, April 22): We expect BI to remain on hold at 4.75%, maintaining a neutral bias and reiterating its commitment to the intensity of its market intervention. Focus will be on updated macro forecasts and implications for the fiscal and external balances. As of March, BI projects 2026 GDP growth at 4.9–5.7% and the current account at -0.9% to -0.1% of GDP.

Türkiye, Türkiye Cumhuriyet Merkez Bankası (Wednesday, April 22): The TCMB is expected to remain committed to tight financial conditions, but fiscal policy will do most of the work in offsetting higher energy costs and other supply constraints. Like regional peers, the central bank is unlikely to hike rates due to fears of prolonging or even triggering a post-conflict growth shock, but much will depend on whether inflation expectations show any sign of sudden reversal. Sequential inflation numbers are manageable for now.

The Philippines, Bangko Sentral ng Pilipinas (Thursday, April 23): We expect BSP to keep rates unchanged at 4.25% and adopt a wait-and-see stance. The prior easing cycle has effectively paused as renewed inflation pressures emerge. While rhetoric may turn more hawkish, a rate hike is unlikely given the supply-driven nature of price pressures and risks to growth – with near-term priority likely to remain financial stability.

Source: BNY

Source: BNY