Can AI overtake oil again?

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 9 minutes

Last week was notable: the USD rose, oil gained and U.S. equities advanced. Concern about the ongoing conflict and Strait of Hormuz headlines faded as a market volatility driver, while earnings and AI returned to the fore. In the week ahead, oil and the war remain center stage, but rate decisions, earnings and key economic data – along with the usual month-end rebalancing flows – will compete for attention.

Can AI beat oil for leadership in markets this week?

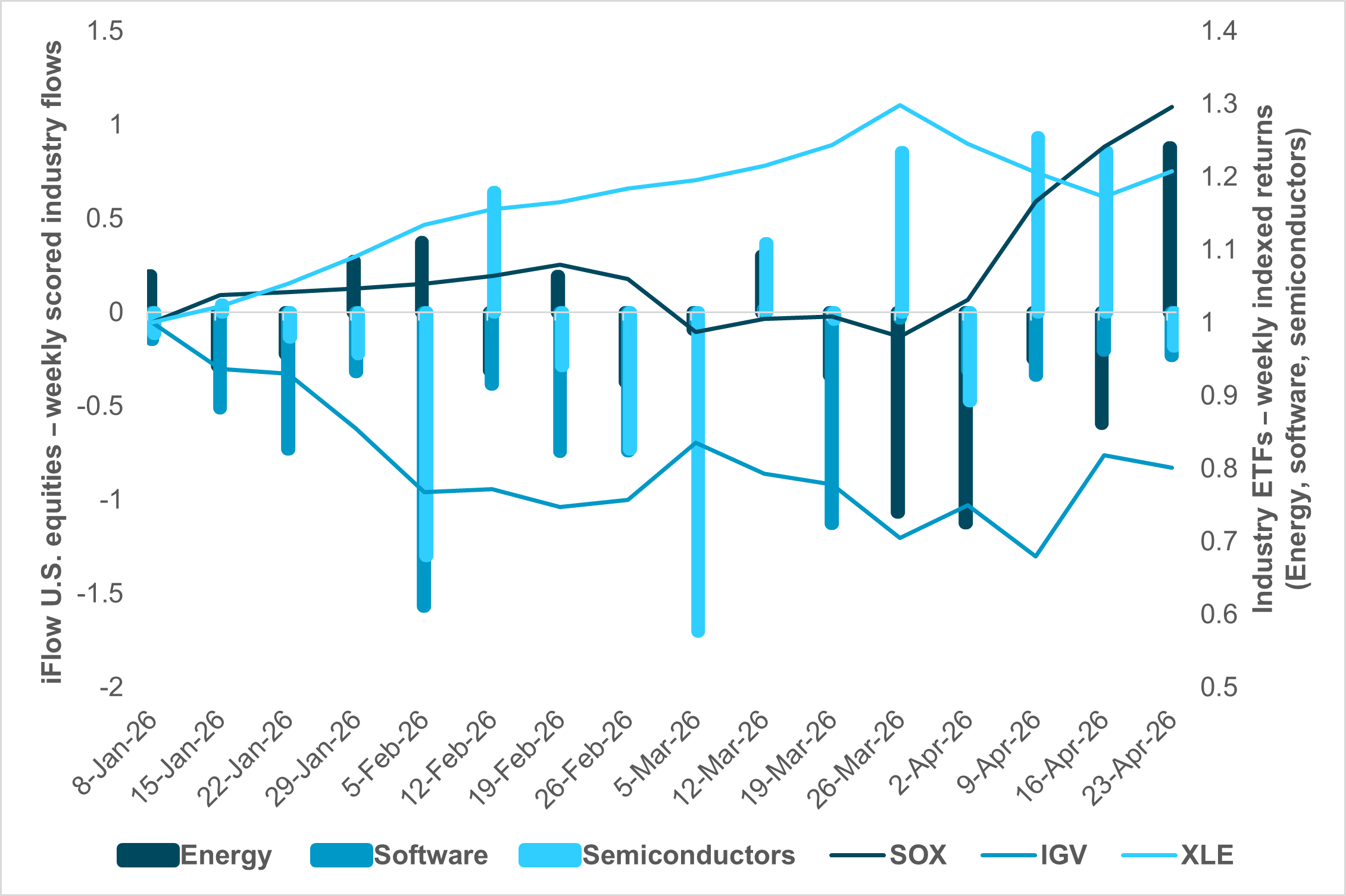

EXHIBIT #1: U.S. EQUITY FLOWS – ENERGY, SOFTWARE AND SEMICONDUCTORS VS. ETFS

Source: BNY, Bloomberg

Our take: Last week saw semiconductor flows hit record highs. Oil prices rose and energy sector shares recovered off their March war highs, while software shares were mixed but off their pre-ceasefire lows in early April. Our flows mostly match the ETFs, but there are some exceptions. The risk for a larger move in software and semiconductors stands out, with U.S. holdings of both near historic averages while flows have been mixed.

Forward look: This week will be focused on the large tech earnings reports. Our flows and holdings suggest upside surprise risk if energy prices stay rangebound and the Iran conflict holds its current equilibrium or moves toward a truce. The key for all is energy supply shock not deteriorating further, and the continued flow of oil from producers to users. The question of whether AI is driving semiconductor demand while hurting software will be the main story in a benign geopolitical scenario. We see this week’s four large tech reports as likely to extend the nascent shift back toward technology leadership over energy.

North America: Fed and BoC on hold in fog of war

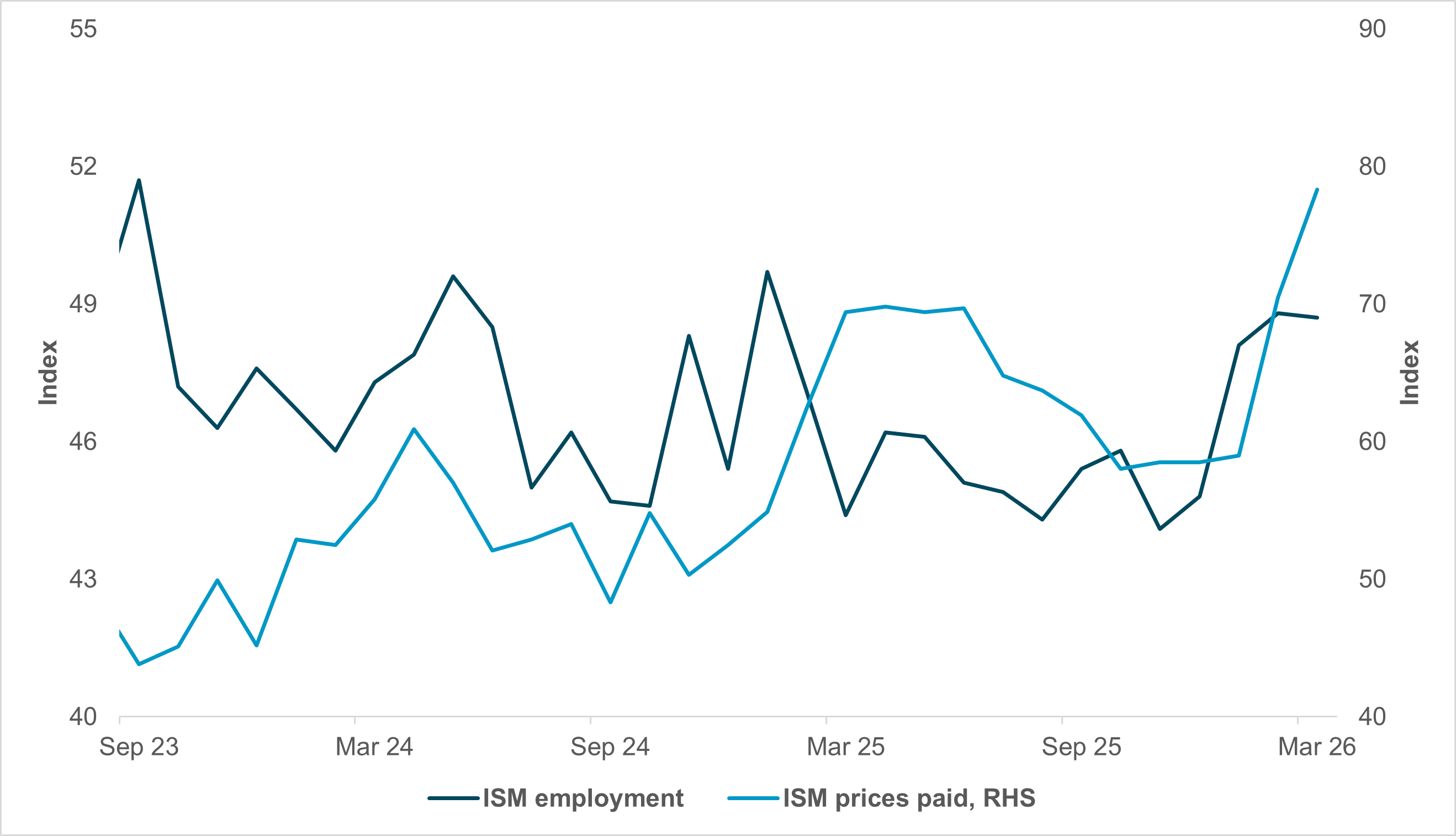

EXHIBIT #2: U.S. ISM JOBS VS. PRICES

Source: BNY Bloomberg

Our take: North America is not to be excluded from the parade of global central bank meetings this week, as both the Fed and the BoC hold rate-setting meetings on Wednesday. Truth be told, very little action is expected from either Washington or Ottawa. With new Fed Chair designee Kevin Warsh still in confirmation limbo, this week could bring us Chair Jerome Powell’s last press conference.

While the two central bank meetings are unlikely to provide much to chew on, the data docket is considerably heavier than last week’s. After the Dallas Fed PMI on Monday, we’ll see house prices on Tuesday, along with the Conference Board’s consumer confidence release. Durable goods orders for March come on Wednesday, and the March PCE deflator and the advanced Q1 GDP print hit the tape on Thursday. We round the week out with the widely watched ISM manufacturing PMI.

Canada will provide less data, though some important numbers nonetheless, including the Government’s Spring Economic Update (Tuesday), the SEPH payroll employment report on Tuesday and February pre-conflict GDP on Thursday.

Forward look: While the central bank meetings will probably leave us unmoved, the data releases should paint a comprehensive picture of the two countries’ economic reactions to the war. We’re watching the U.S. inflation and capex data, while Canada’s release will add color on the labor market and could test the case for rate hikes later this year.

EMEA: ECB and BoE likely to avoid rate hike but signal “live” meetings in the near term

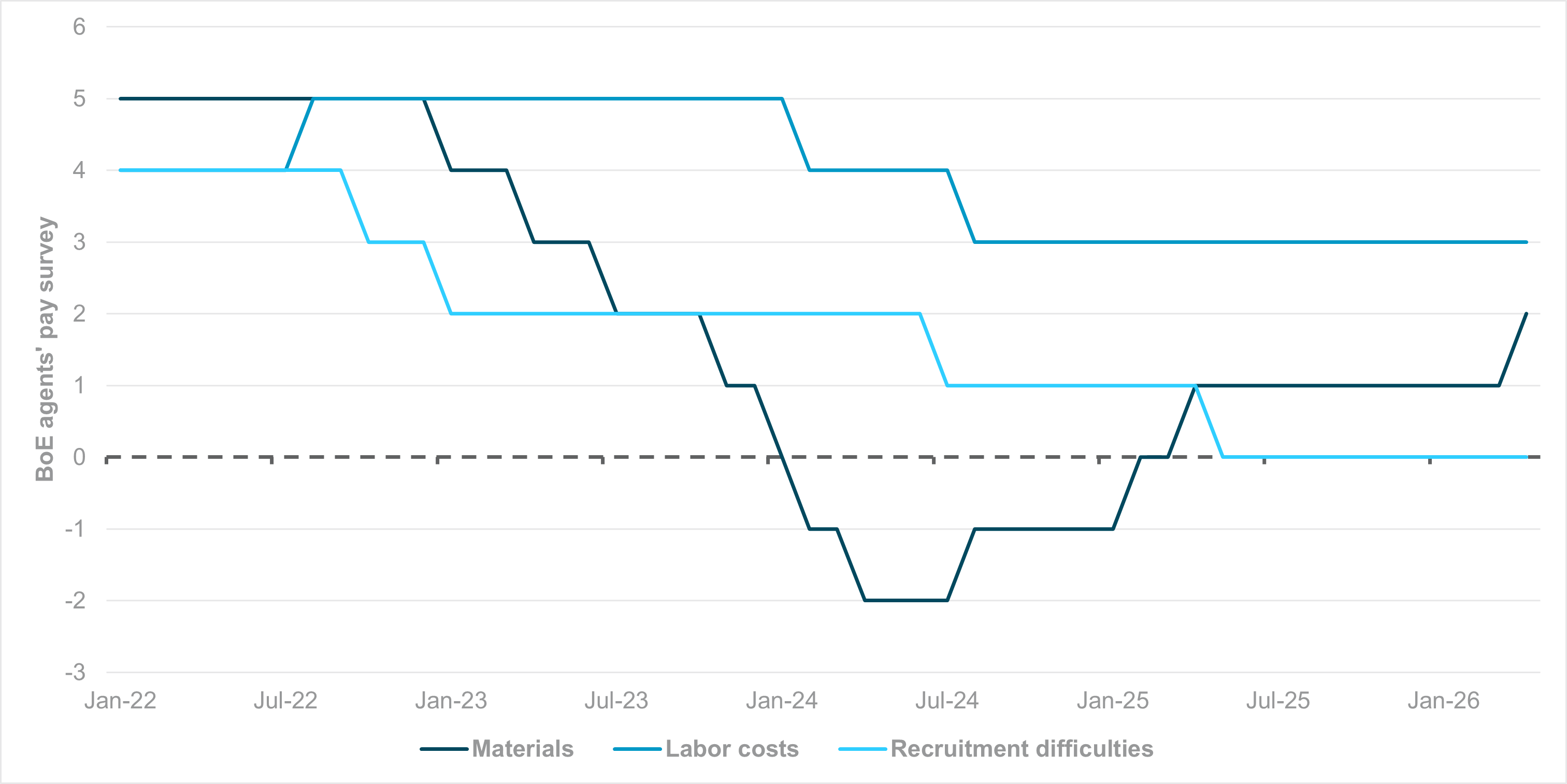

EXHIBIT #3: BOE AGENTS SURVEY DOES NOT POINT TO WAGE PRESSURES FROM CONFLICT

Source: BNY, Macrobond

Our take: The BoE and ECB decisions this week will be critical tests of rate-hike market pricing, which in our view is excessive and inconsistent with fundamentals. No changes are expected, but there will likely be votes for a hike and robust discussions around addressing second-round effects. In this context, the BoE’s approach is closely tied to household conditions and wage pricing power. This is also what Norges Bank stated in its last monetary policy meeting, even after it affirmed a hike.

In contrast, the ECB’s view (or at least among the more hawkish members) leans much more toward pre-emptive or “insurance” tightening. Given where the economy stands in the cycle, we don’t see a case to characterize any tightening as “insurance” – the resulting tightening in financial conditions would only exacerbate the demand drag. Even in “fiscally dominant” economies such as France, there is a recognition that government spending needs to be materially curtailed if energy-related subsidies are set to rise – removing any argument for monetary “insurance” or offset. If we look at the BoE’s latest agents’ survey (Exhibit #3), released on Friday, the “materials” cost element has clearly increased due to supply issues, but the labor market-related components, both in costs and recruitment difficulties, remain consistent. For context, all three price-push factors (materials, wages and labor availability) were at elevated levels in 2022. In short, no central bank should be tightening right now simply to prove t isn’t behind the curve or treating current pressures as transitory. If that message lands, rate markets – which remain extremely aggressive relative to baseline and pre-conflict levels – face significant front-end repricing, with two to three cuts needing to come out.

Forward look: The EU formally approved a €90bn loan to Ukraine last week, ahead of an informal summit this weekend – the first significant gathering of EU leaders in the post-Orban era. Our flow figures indicate that the re-rating for Central and Eastern Europe through unblocked funding (both current and future) appears to have run its course, and markets will revert to growth and policy paths driving assets. Hungary faces one of the heaviest fiscal burdens in the EU (along with Poland). Markets acknowledge that positive real rates support currencies in the region, but would also like to see fiscal restraint. The MNB decision is also the first since the Hungarian election; observers will look for subtle shifts pointing to a stronger institutional independence, which typically translates into a hawkish lean.

Otherwise, preliminary inflation numbers will be due in core Western European nations. German sequential inflation is expected to show a 0.7% m/m gain after a 1.1% m/m gain in March, pushing the annualized headline figure close to 3%. Similar results are expected in Spain (consensus 0.9% m/m) and France (consensus 1.0% m/m). These figures will land before the ECB decision, and any upside surprise could support Governing Council members’ pushing for an early move. We would also watch core divergence, which should confirm that second-round effects or a sudden demand push are far from guaranteed.

APAC: China PMI, South Korea BSI, Australia, Tokyo CPI, BoJ, BoT policy meetings

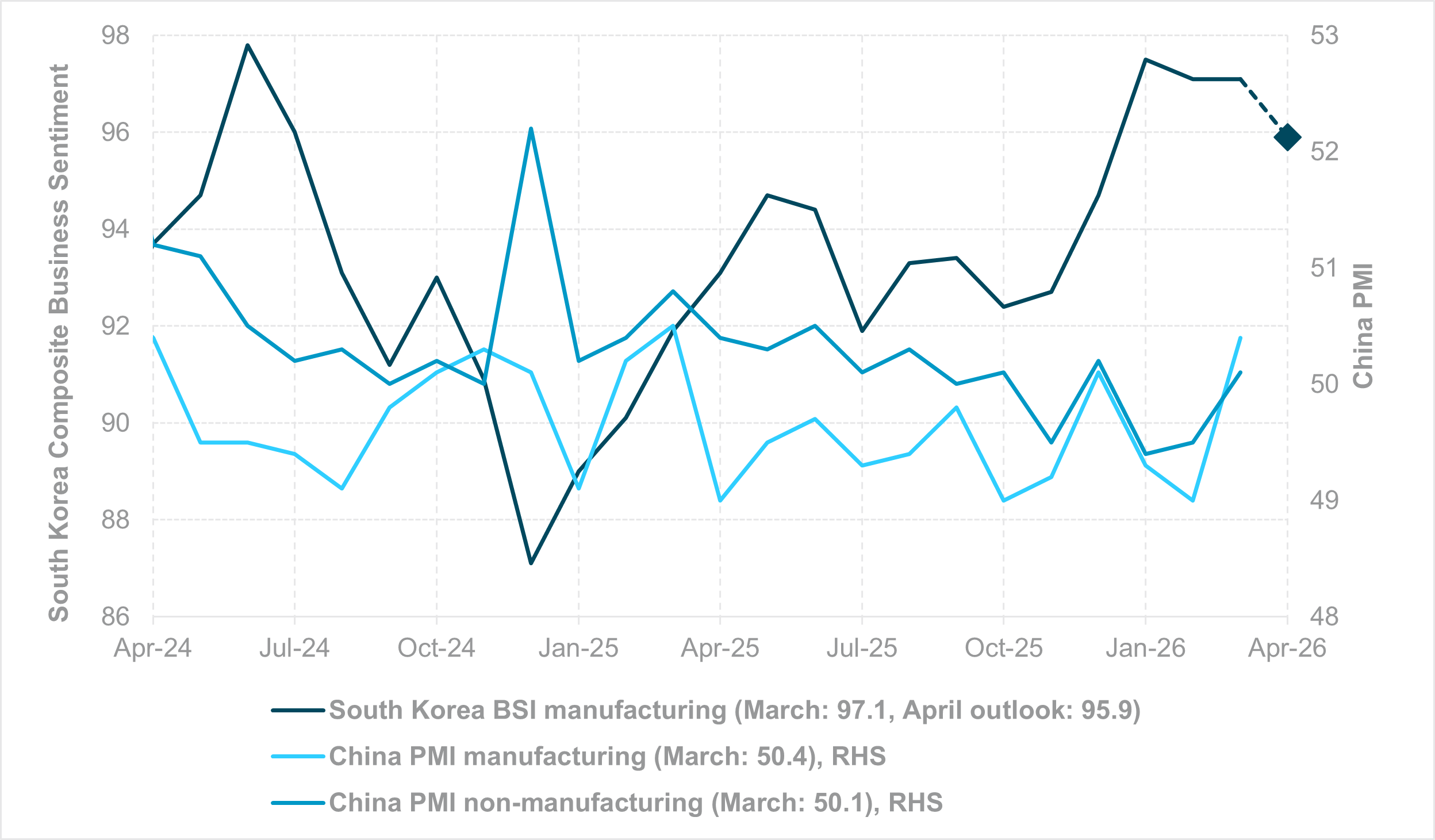

EXHIBIT #4: CHINA AND SOUTH KOREA BUSINESS SENTIMENT

Source: BNY, Bloomberg

Our take: This week’s APAC calendar centers on business sentiment across China, South Korea, Australia, New Zealand, and Japan, alongside key inflation prints in Australia and Japan.

In Japan, the BoJ meeting is set to overshadow a heavy data slate, including April Tokyo CPI, March retail sales, industrial production, and housing starts. China’s April PMI and March industrial profits will shape regional growth sentiment, with markets looking for signs of stabilization amid still-soft demand. South Korea’s April exports and Composite Business Sentiment Index will serve as key high-frequency gauges of global trade and tech cycle momentum.

In ASEAN, the Bank of Thailand meeting is the main policy event; rates are expected to remain unchanged. Taiwan’s Q1 GDP will provide insight into semiconductor-driven growth, while Singapore’s industrial production offers a timely read on electronics demand. In India and the Philippines, credit and money supply data will help assess domestic liquidity conditions, though market impact should be limited. Overall, the week reinforces the divergence theme – upside inflation risks in Australia and Japan versus uneven growth momentum across Asia – keeping FX and rates markets sensitive to both inflation surprises and growth downside.

Forward look: Geopolitical uncertainty remains elevated, with commodity prices volatile despite the announced indefinite U.S.–Iran ceasefire and ongoing risks around the Strait of Hormuz. Investor sentiment toward APAC equities, however, remains resilient, led by Chinese and tech-heavy South Korean and Taiwanese equities.

Net oil-importing currencies (KRW, THB, PHP, INR) continue to underperform relative to the region, reflecting deteriorating terms of trade, rising inflationary pressures from higher commodity prices, and widening external deficits. Central bank FX intervention and smoothing operations are likely to be measured and calibrated amid the risk of prolonged elevated oil prices. This follows significant FX reserve drawdowns in March across APAC, including India (-$40bn, -6% m/m), Thailand (-$13bn, -5% m/m), the Philippines (-$6.6bn, -6% m/m), China (-$85bn, -2.5% m/m), Indonesia (-$4bn, -2% m/m), and Taiwan (-$8.6bn, -1% m/m). Policy tightening risks are rising at the margin following MAS’s S$NEER slope adjustment and BSP’s pre-emptive 25bp hike. Reserve Bank of India and Bank Indonesia are also potentially under scrutiny given accelerating inflation – 3.4% y/y in India (mid-target ~4%) and 3.48% y/y in Indonesia (mid-target ~3%). That said, this is not our base case. We maintain that rate hikes are unlikely to effectively address supply-driven inflation or arrest currency depreciation. FX volatility is set to persist, with net oil importers remaining under pressure. We continue to prefer CNY, SGD, and MYR within the region, while IDR stands out as the weakest link amid deficit and confidence concerns.

Looking ahead, markets are likely to stay caught between two competing leadership themes: geopolitics and AI. If the conflict around Iran and the Strait of Hormuz remains contained, investor attention should rotate further toward earnings, capex, and the durability of the AI-led technology cycle. The concentration of hyperscaler results this week gives equities a clear near-term catalyst, particularly for semiconductors and selected software names, where positioning still leaves room for upside surprise. At the same time, oil remains the key macro swing factor. Any renewed disruption to physical energy flows would quickly revive inflation concerns, pressure rate expectations, and challenge the recent rebound in risk assets. Central bank guidance, month-end flows, and major U.S. and global data releases add further event risk. Our base case is that, absent a material worsening in energy supply conditions, technology can reassert leadership over energy, but conviction will depend on earnings delivery, the credibility of AI spending plans, and stable macro expectations.

Central bank decisions

Japan, Bank of Japan (Tuesday, April 28): The BoJ is expected to keep rates on hold at 0.75% as it struggles to balance inflation expectations management against serious growth risks from the supply shock. USDJPY continues to hold around 160, and language from the Ministry of Finance remains firm on intervention risk. However, the market will likely look for opportunities to test resolve, depending on data evolution. The long end of the JGB curve continues to factor in higher inflation and fiscal risk, and we see real rates rising to compensate over time.

Hungary, Magyar Nemzeti Bank (Tuesday, April 28): The MNB decision is not expected to yield any policy changes, and we believe the central bank is generally comfortable with its current real rates position. Of greater interest to markets is whether the seismic shift in Hungarian politics produces subtle changes in the MNB’s outlook. EU fund unlocking will have clear spending implications, but the more important question is how the central bank’s relationship with the new government resets – which markets may interpret as a marginally more hawkish stance if conditions warrant.

Chile, Banco Central de Chile (Tuesday, April 28): The BCC should be relatively comfortable with the TPM profile for now, but 4.5% is still low by LatAm standards, and the global inflation outlook has shifted to some extent. Nonetheless, we note that CLP has been one of the strongest performing names throughout the conflict, and if there is an acceleration toward renewables, Chile is well placed to benefit from positive terms-of-trade adjustments. However, the economy is somewhat soft while inflation has picked up, so policy requires careful calibration.

Thailand, Bank of Thailand (Wednesday, April 29): We expect the BoT to keep the policy rate unchanged at 1.00%, maintaining a wait-and-see stance. While higher oil prices pose upside risks to inflation, ongoing disinflationary pressures should keep concerns contained. Near-term focus will remain on financial stability and potential fiscal stimulus measures. Markets will closely watch updated BoT macro forecasts: as of December 2025, the BoT projected GDP growth at 1.5% in 2026 and 2.3% in 2027, with headline CPI at 0.3% and 1.0%, respectively.

Canada, Bank of Canada (Wednesday, April 29): The BoC meets with little expectation of a rate change or much forward guidance, given geopolitical uncertainty. A Monetary Policy Report will also be produced, but we don’t expect the Report or Governor Macklem to be very prescriptive – more likely, both will outline the two-sided risks to the inflation/employment trade-off.

United States, Federal Open Market Committee (Wednesday, April 29): We expect little from the Fed this week, and policy expectations are flat for the remainder of the year thanks to the war and the Fed’s impending transition. While it could be Chair Powell’s last meeting as Chair of the FOMC, prediction markets are skeptical that he’ll leave the Fed by the end of this month.

Brazil, O Comitê de Política Monetária (Wednesday, April 29): Brazil is emerging as one of the biggest LatAm beneficiaries of the conflict, as its prowess in energy, soft commodities and other core inputs supports terms of trade. BRL’s resilience is also complemented by very high nominal rates, which shouldn’t face too much downside pressure in the near term due to the need to maintain policy vigilance. Inflation’s current run-rate remains manageable, but COPOM would also be mindful of the need for restraint if a sustained commodity rally materializes.

United Kingdom, Bank of England (Thursday, April 30): The Monetary Policy Committee is unlikely to move on rates as data and underlying conditions have not changed materially from March. Sequential price changes have been weaker than in Eurozone peers, and corporates appear to be absorbing rather than passing on higher input costs for now. Nonetheless, the labor market is resilient, and the surprisingly strong April PMI report suggests that the household offset in services (and wages, by extension), may not be as strong as anticipated.

Eurozone, European Central Bank (Thursday, April 30): The ECB decision is clearly “live,” but we don’t think there will be enough votes to get a hike over the line. Several Governing Council members, while affirming the need to use monetary policy to address inflation risks on a pre-emptive basis, are not yet fully in support of a move in April. We do not see a hike as necessary given the weak domestic household and industrial outlook, but some Governing Council members may push for early action while keeping their options open.

Colombia, Banco de la República (Thursday, April 30): BDRL is expected to continue its easing cycle with a 50bp cut to 11.75%, extending the adjustment after the 100bp hike at the previous meeting. At close to 12%, there will be a meaningful real rate gap: March sequential inflation fell below 1% on both the headline and core measures. However, domestic activity remains robust as retail sales surged by close to 11% in February, and we continue to see terms-of-trade gains for the economy from current global supply constraints.

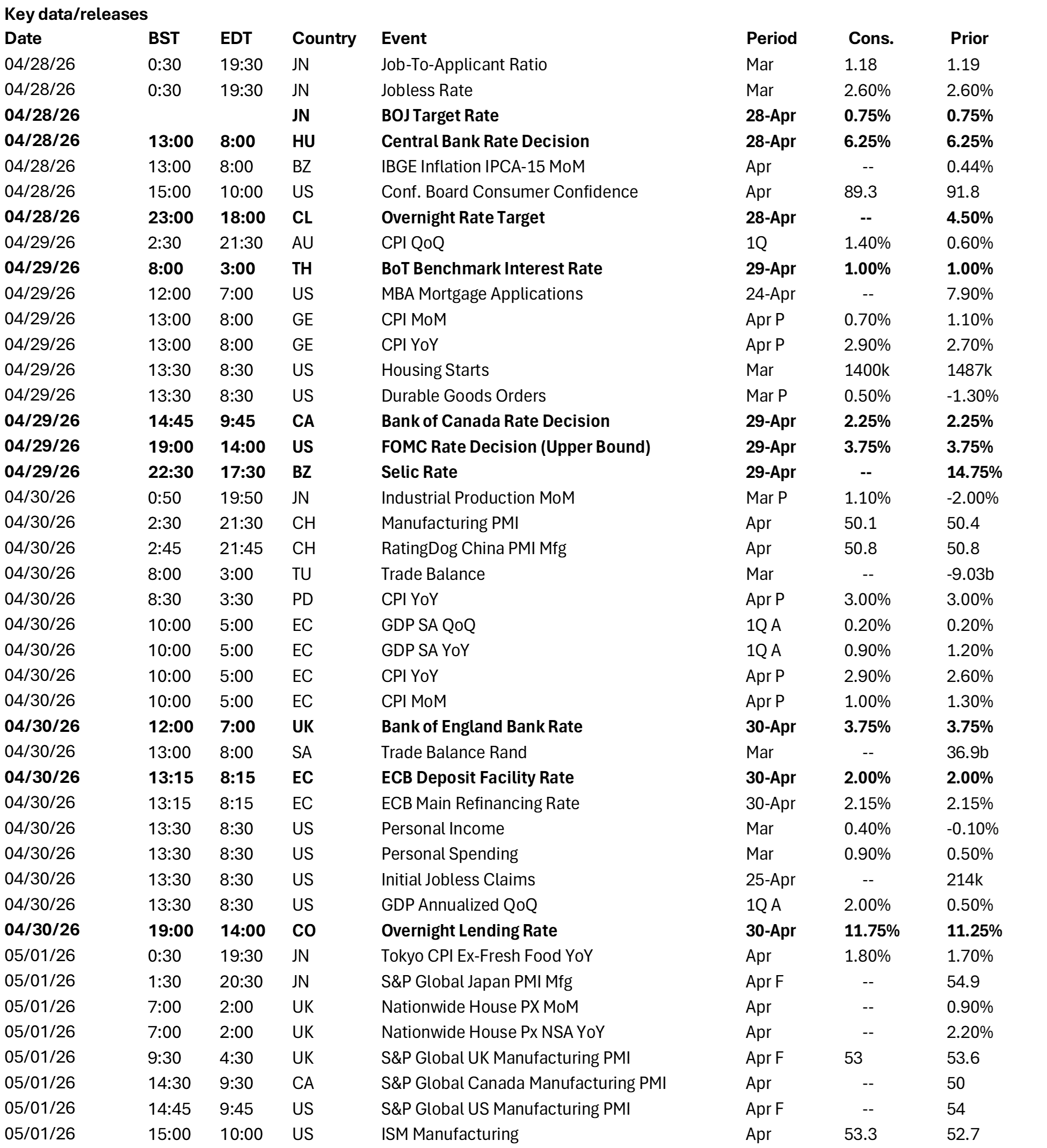

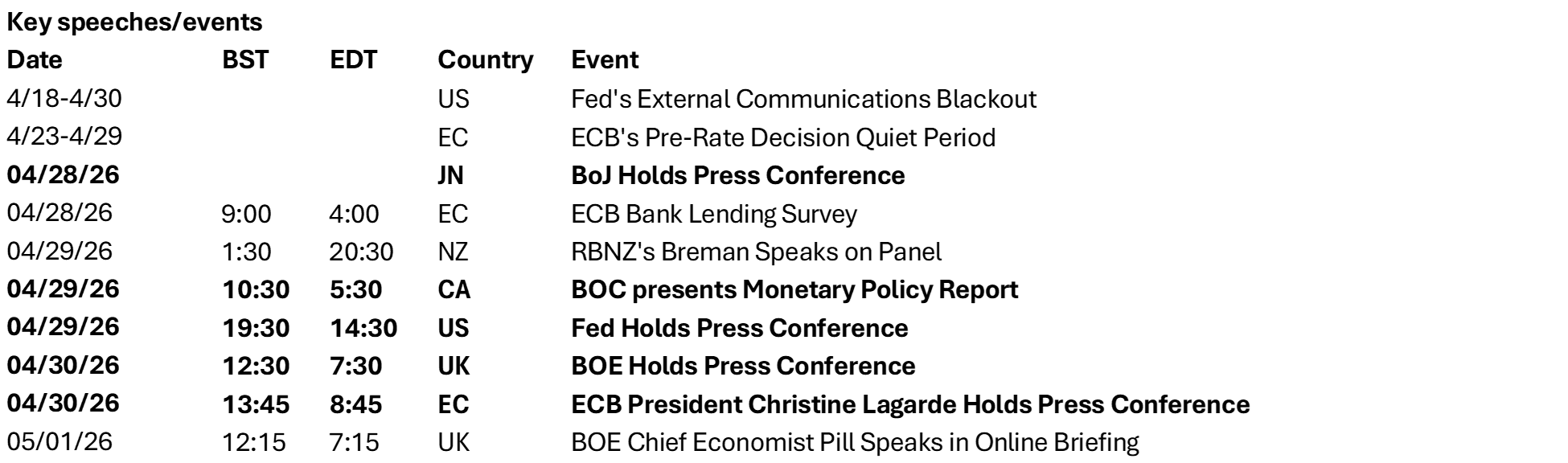

Source: BNY

Source: BNY