After April's rally, what does May hold?

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 9 minutes

This week features less data and more signals, as investors turn to May and watch how financial conditions, credit and political concerns drive growth and returns into the seasonal lull. Historically, golden-week equity returns have been modest – up 0.3% – driven more by earnings and other geopolitical headlines than seasonal momentum. Markets are likely to spend this week digesting last week’s moves than positioning for the month ahead. Investors are rethinking rates, the April rally, the balance of growth and inflation, and the political fallout from the current energy price shock.

Key themes

Will investors put cash to work in May?

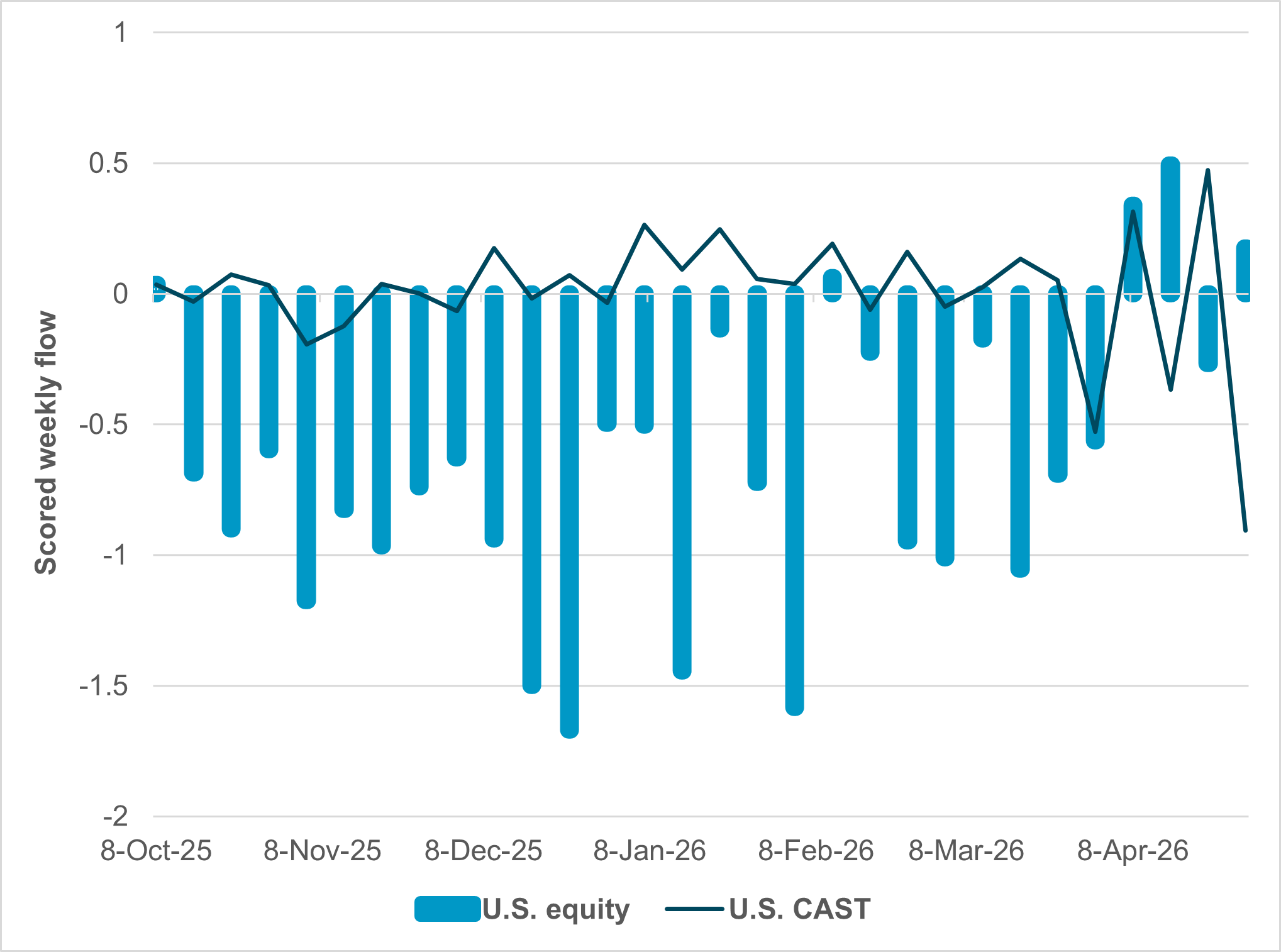

EXHIBIT #1: IFLOW CAST VS. WEEKLY U.S. EQUITY FLOWS

Source: BNY

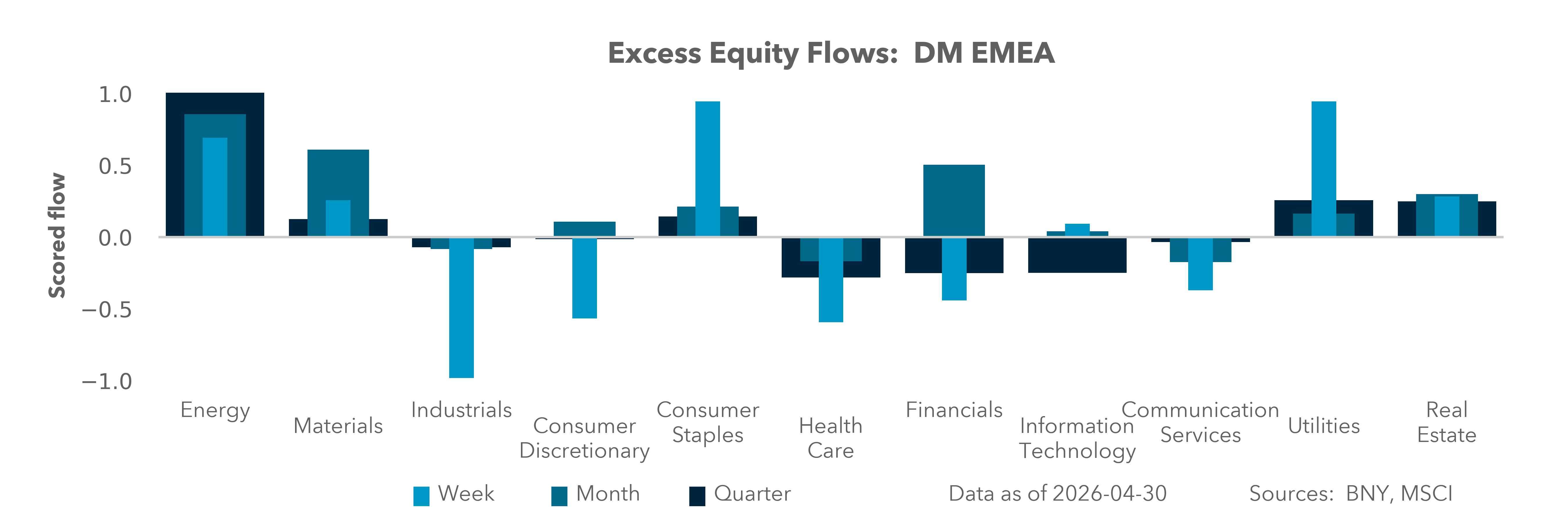

Our take: The last six months of U.S. equity trading have seen a significant sector rotation out of big tech into Energy, Materials and Industrials. The shift to cash (measured by our CAST index) was also notable. Investors were defensive in this barbelled approach. This all changed in April with the U.S.–Iran ceasefire, and the reversal into month-end was significant. The S&P 500 returned 10% in April, the best result since the peak COVID-era rush back to risk. The cash-and-leverage dynamic will test the bond-equity correlation going into May.

Forward look: April’s best monthly S&P 500 gain in 33 years has sent a strong “putting money to work” signal, one that will complicate views about the Fed. Financial conditions have become a significant part of how consumer sentiment and demand work in the U.S. The K-shaped economy arguments fall apart if stocks fall sharply. The tension between gasoline prices driving voter sentiment and stock prices driving domestic demand will be an important divide through the summer trading lull.

Clarity on the war’s end, confidence that AI investment will sustain growth, and a coherent read on energy-driven inflation are the key conditions for investors to put money to work in Q2. The subtle difference between April and May is about “buying the dip” vs. “chasing the tape.” Value and momentum factors will be clashing across global asset classes.

North America: Jobs and Fed speakers

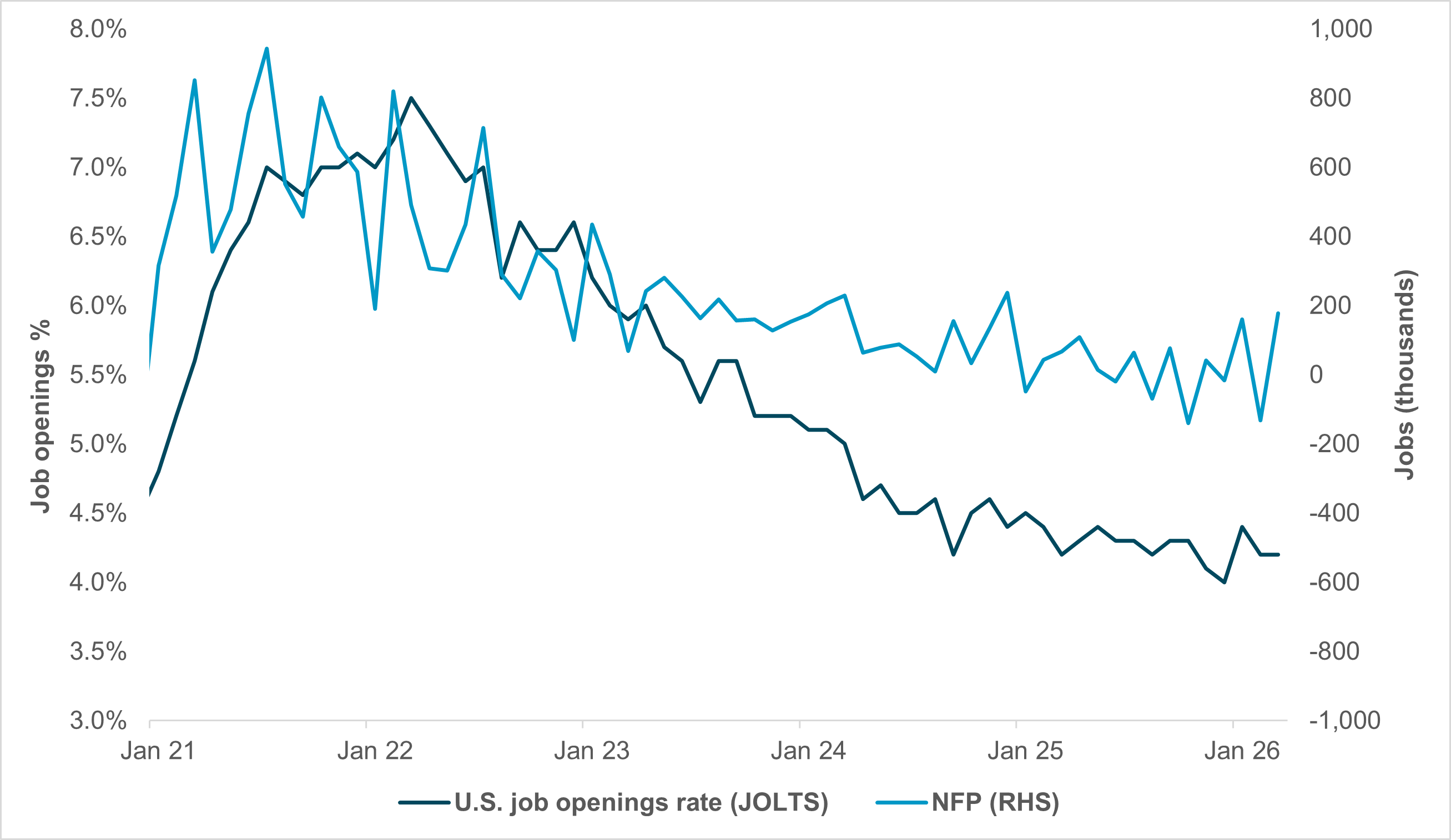

EXHIBIT #2: JOLTS VS. NFP, M/M CHANGE

Source: BNY Bloomberg

Our take: The usual post-FOMC wave of Fed communications kicks off Thursday with Cleveland’s Beth Hammack and Neel Kashkari of Minneapolis. Dallas’s Lorie Logan is not yet on the docket but is expected to appear. Hammack and Kashkari have already released statements explaining their dissents from last week’s meeting. Thursday’s appearances should offer greater insight into the committee dynamics that incoming Chair Kevin Warsh will inherit.

Speaking of the presumptive Fed Chair, Warsh’s appointment appears to be a done deal following his clearance by the Senate Banking Committee last week, though the formal vote awaits the Senate’s return this week.

Following a blockbuster week of data, this week will be quieter in the U.S., with S&P PMI and JOLTS the highlights. Canada’s employment data will be available at the end of the week.

While not particularly in focus, Bank of Canada Governor Tiff Macklem and Senior Deputy Governor Carolyn Rogers are scheduled to appear before the House of Commons.

Forward look: Fed speakers will offer plenty of material to speculate about palace intrigue, though we find it unlikely that either Fedspeak or data releases will give much cause to change the rates outlook.

Canada should be similarly static, though as we know by now, developments in Iran could quickly shift the outlook.

EMEA: ECB has a direction but not everyone may follow

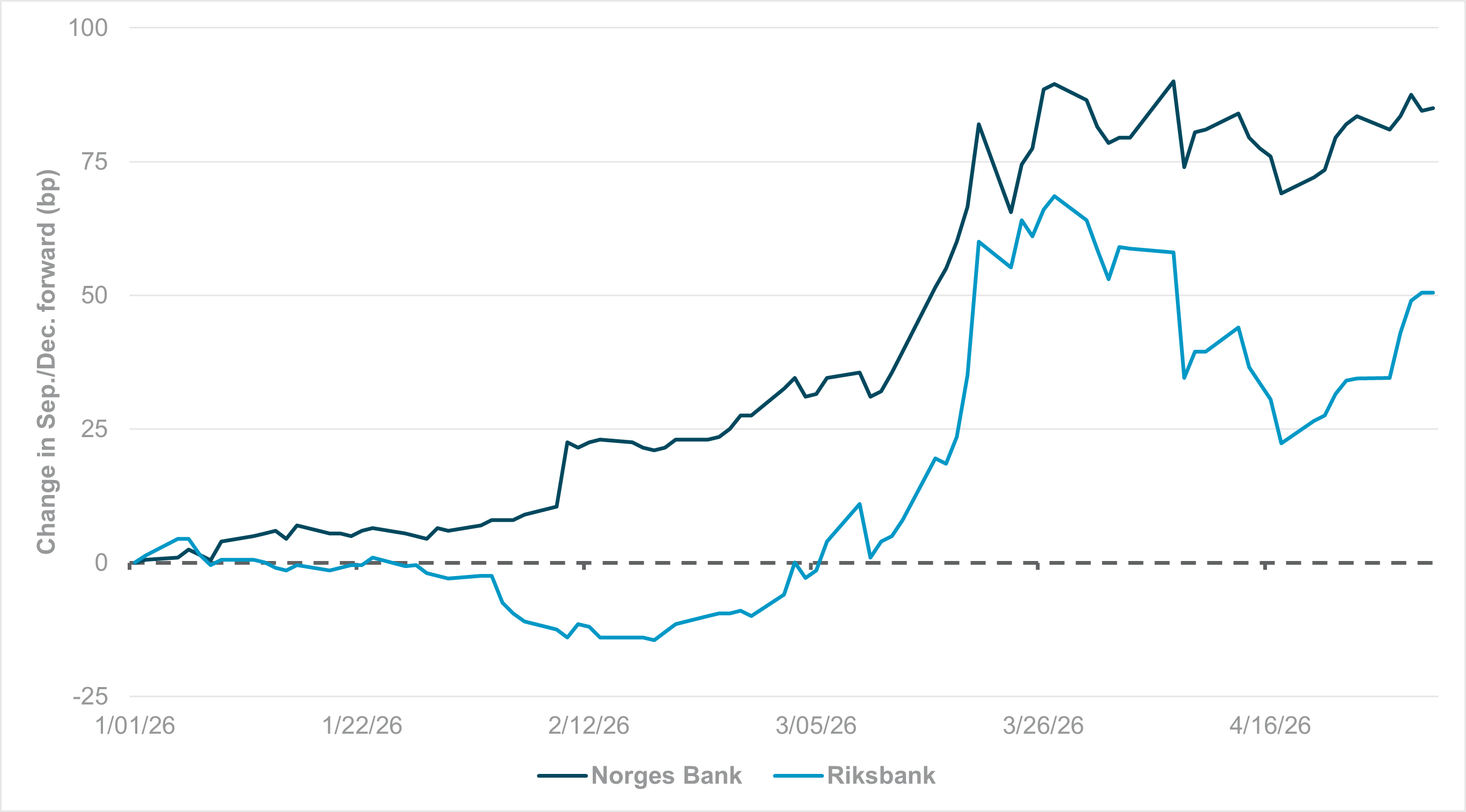

EXHIBIT #3: NORGES BANK AND RIKSBANK YEAR-END RATE EXPECTATION CHANGES

Source: BNY, Macrobond

Our take: The ECB and BOE decisions for April have largely set the tone for the rest of the continent. The ECB is clearly leaning toward a June move at this point, with President Christine Lagarde stating at the post-decision press conference that while the economy was not seen as facing second-round effects, she knew “where the ECB is headed on interest rates.” The fact that there is even a direction in place moves squarely against the notion of the “policy in a good place” designation before the conflict. This also stands in contrast to BOE Governor Andrew Bailey’s notion that unchanged rates were “a reasonable place” for the BOE. The latter’s scenario analysis is quite clear and maps where inflation could head under extreme scenarios, but it appears most policymakers would prefer to have full confirmation of any scenario before reacting. Even the lone dissenter on the MPC, Huw Pill, recognized that “second-round effects may be more modest with a looser labor market” and only saw a need for a “prompt and modest” hike as mitigation, not the full multi-hike cycle that markets are currently pricing.

Transposing such views onto Norges Bank and the Riksbank, which decide in the coming days, we believe a similar approach is needed as markets continue to expect multiple hikes toward year end at both. As we have stressed, domestic conditions already justified aggressive moves from Norges. With energy-related output adding upside risk to the labor market, a more assertive stance is perhaps warranted – though much of this is already in the price. Norges will continue to sell FX to purchase NOK for May, but at NOK 100mn a day, the pace sits toward the lower end of historical transaction records. We expect a move to neutral soon.

For the Riksbank, considering their low policy starting point, matching the ECB would have been understandable, but the surprisingly soft inflation prints for March (sequential decline in both CPI and CPI-F) and lackluster growth expectations forced out almost 50bp in tightening through mid-April, though expectations are ticking up again due to ceasefire uncertainty (Exhibit #3). We don’t see the Riksbank moving this year either, and NOK–SEK divergence will likely become more apparent in the coming cycles.

Forward look: While policy comments will dominate European markets, the week is also fraught with political risk. The U.K. will hold local elections on May 7, and the days after the result – likely to be very damaging for the ruling Labour Party – could represent the moment of maximum jeopardy for Prime Minister Starmer. A bad result, broadly seen as a loss of 2,000 council seats or more, could lead to open calls by senior party members for his removal. An outright leadership challenge is also possible, but the process for Labour to replace its leaders is relatively more difficult than that of the main opposition Conservative Party, and we suspect that most within Labour and the country would prefer a cleaner “exit.” On the other hand, with the King’s Speech scheduled for May 13, less than a week later – where he sets out the priorities of the next Parliament – timing is of the essence and any internal changes would have to take place very quickly, lest the country find itself in legislative limbo at a very fraught moment.

Our data continue to track relatively decent domestic demand for gilts due to higher real yields, and the latest BOE decision is broadly consistent with the lack of inflation premia reflected in gilts. However, markets could shift to fiscal concerns very soon depending on the next Labour leader and chancellor, and that would represent a new challenge amid a highly uncertain economic backdrop.

APAC: Regional PMI, CPI, Exports and FX reserves, BNM and RBA policy meeting

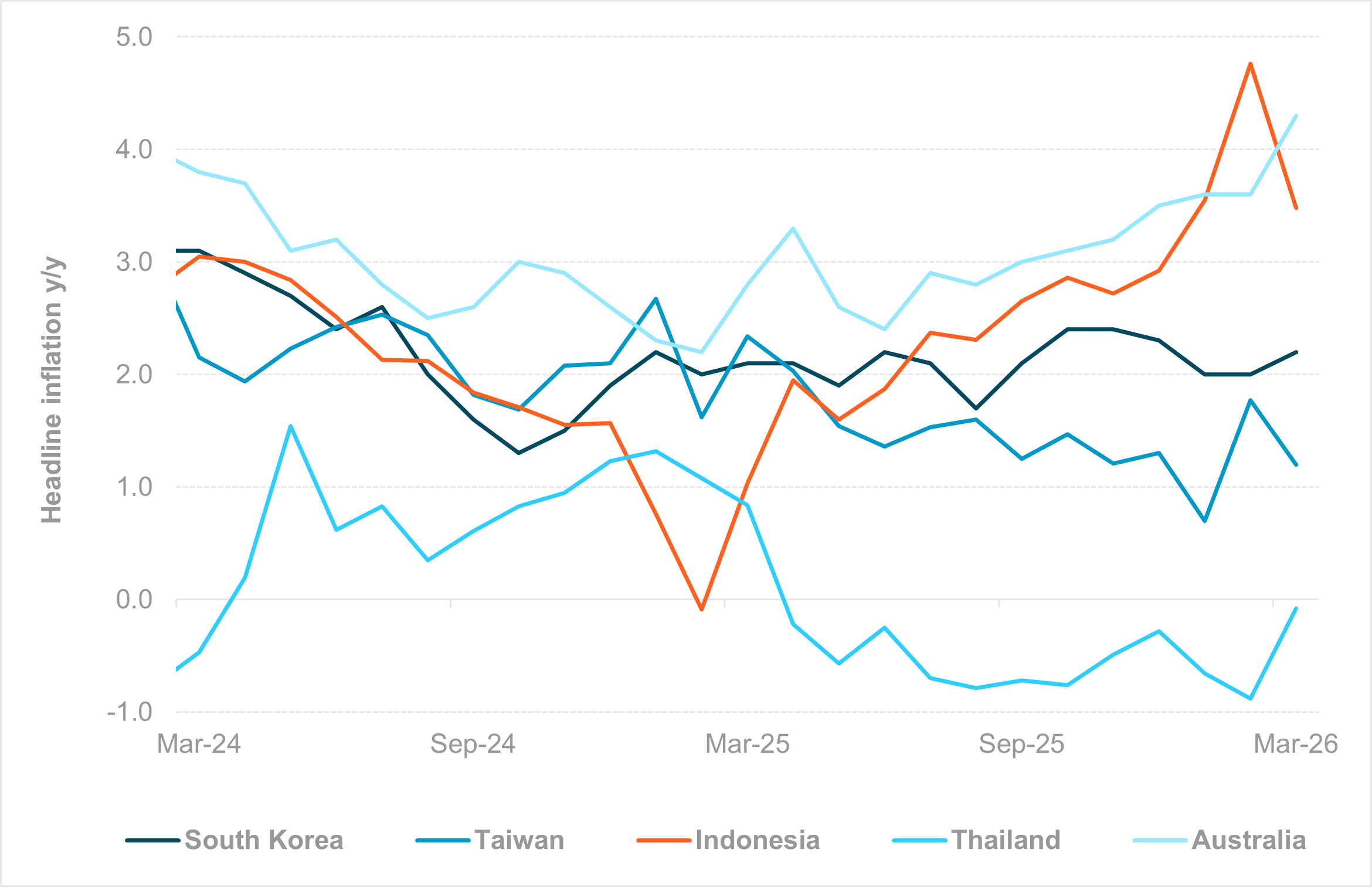

EXHIBIT #4: REGIONAL INFLATION TREND

Source: BNY, Bloomberg

Our take: Asia’s data calendar this week is heavy, with a dense run of inflation and growth releases across the region. China and broader regional April PMI prints, alongside FX reserves data, will be closely watched for signs of domestic demand stabilization and evidence of intervention activity. In North Asia, South Korea’s April CPI and balance of payments data are key for KRW – both for gauging inflation momentum and implications for Bank of Korea policy expectations, as well as monitoring the pace of domestic equity outflows that have weighed on KRW since Q4 2025. Taiwan’s CPI and export data remain pivotal for TWD, given Taiwan’s high beta to the global tech cycle. Meanwhile, FX reserves across China, South Korea, Taiwan, the Philippines, Indonesia, Singapore, and India will be scrutinized for signals of intervention intensity amid ongoing USD volatility.

In ASEAN, Bank Negara Malaysia is expected to keep rates unchanged. Indonesia stands out with a full set of releases – Q1 GDP, CPI, and trade – which should drive both IDR and local rates via the growth-inflation mix and external balance dynamics. In the Philippines, Q1 GDP and April CPI are likely to reinforce expectations of further BSP tightening, while Thailand’s CPI and sentiment indicators will guide THB through domestic demand signals. In DM, the Reserve Bank of Australia decision anchors the week, with AUD likely to react more to policy guidance than data. New Zealand will release Q1 labor market data, including unemployment and wages. In Japan, real cash earnings remain central to BOJ normalization expectations and JPY, particularly through the wage-inflation transmission channel. Overall, the week is skewed toward inflation and policy signals, with FX likely driven by relative policy expectations and evidence of FX intervention across the region.

Forward look: A shortened trading week lies ahead, with extended holidays in Japan and China. APAC FX is expected to remain driven by terms-of-trade dynamics. Net oil importers – INR, THB, KRW, PHP – and deficit-exposed IDR are likely to underperform, while CNY, SGD and MYR should be more resilient. TWD remains supported by sustained inflow momentum. Singapore recorded a sharp S$33.2bn rise in non-resident deposits in March (to S$659.1bn), pointing to flight-to-quality inflows and underpinning SGD.

In contrast, PHP and IDR hit fresh all-time lows last week, with risks skewed toward further downside in IDR and INR amid persistent foreign equity outflows and external vulnerabilities. A more hawkish global central bank backdrop adds to the softening APAC outlook. Tightening by the Philippines’ central bank is unlikely to materially support PHP, as markets are shifting focus to rising growth risks rather than rate differentials. FX intervention across the region is likely to remain measured and calibrated, particularly given the risk of persistently elevated oil prices. Overall, APAC currencies remain vulnerable to further downside.

As markets transition into May, the key challenge will be reconciling easy financial conditions with still-elevated risk appetite following April’s sharp rally. Investors are increasingly focused on whether higher rates and sustained energy shocks will begin to meaningfully erode growth, particularly as central banks shift toward data dependency and offer less forward guidance. The durability of equity gains will depend on further confirmation that earnings, especially in technology and AI-linked sectors, can offset rising input costs and weaker real incomes. At the same time, geopolitical developments – particularly around Iran and energy supply – remain the dominant macro variable, with the potential to quickly alter inflation expectations and policy paths. Liquidity conditions, thinned by global holidays, could amplify market reactions to both data surprises and political events. Ultimately, May may mark a transition from momentum-driven gains to more selective positioning, where valuation discipline, policy signals, and macro resilience determine whether investors deploy cash or turn more defensive.

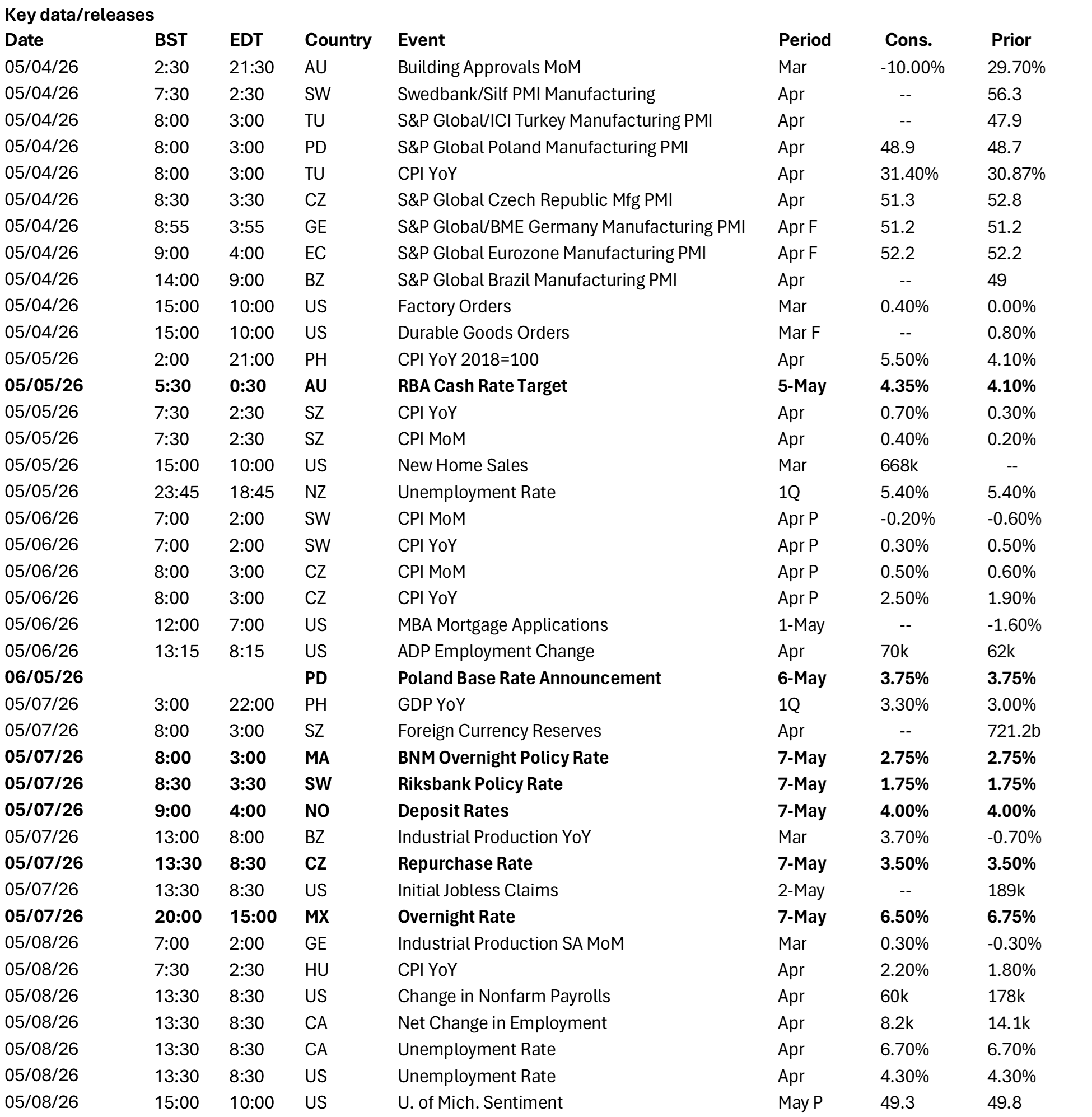

Central bank decisions

Australia, Reserve Bank of Australia (Tuesday, May 5): The market is near-unanimous in expecting an RBA rate hike to 4.35%. According to multiple surveys, Inflation expectations driven by the conflict have shifted notably, and the Q2 price print will likely push headline figures well above the Q1 trimmed mean of 0.8% q/q. Crucially, the labor market is strong and demand may also benefit from the terms-of-trade gains from the conflict, though import exposures on the refined products side could push headline prices higher. Based on current pricing, the RBA is likely to end the year with the highest rates among the G10.

Poland, Narodowy Bank Polski (Wednesday, May 6): The NBP is expected to hold rates at 3.75%, but debate is building over the need to tighten financial conditions to offset fiscal impulse. The debt-to-GDP ratio faces clear upside risk from energy-related costs – comparisons with prior fiscal stress episodes are unfavorable – reinforcing the view that real rates remain too low. As much of Europe remains on hold, we expect the NBP to have sufficient capacity to also hold for now, but upside surprises to inflation will require a response, as much as Poland’s growth and productivity profile are power anchors.

Malaysia, Bank Negara Malaysia (Thursday, May 7): We expect BNM to keep its policy rate unchanged at 2.75%, maintaining a neutral stance. The central bank is likely to reiterate that the current policy setting remains appropriate and supports growth while preserving price stability. Our base case is for BNM to remain on hold through 2026. Focus will be on any commentary regarding the currency, with MYR the best-performing currency in the region year to date. Notably, BNM has avoided explicit references to the ringgit since September 2025.

Sweden, Sveriges Riksbank (Thursday, May 7): The Riksbank is unlikely to hike rates, and the surprisingly soft March inflation figures – relative to peers – negated the need for an early move. Preliminary April inflation due this week is expected to show some contraction and keep headline figures low. The Riksbank will have noted the approaches of the BOE and ECB in April and is likely to frame its own decision within similar scenario analysis.

Norway, Norges Bank (Thursday, May 7): Norges Bank is expected to keep rates unchanged at 4.0%, though it is so far the only Western European central bank that has all but confirmed the need to raise them. Norges had already been leaning in this direction due to domestic conditions ahead of the conflict; at the margin, the shift toward tightening should not be considered aggressive. If anything, we believe commodities and energy exposures are overextended, and Norges Bank’s policy stance is unlikely to provide sufficient support to extend NOK gains.

Czechia, Česká národní banka (Thursday, May 7): No change is expected from the CNB, and the country’s inflation outlook is broadly well-contained – March CPI came in below 2% on a headline basis, though from a very low base, given that prices were deeply contractionary at both the consumer and producer level. Business confidence is holding well, so a “wait and see” approach is apt, though the ECB’s signaled direction makes future tightening a live possibility.

Mexico, Banco de México (Thursday, May 7): Banxico still has capacity to cut rates, and a further 25bp reduction is possible. That said, holding rates is a scenario worth considering given emerging domestic inflation risks, even with Mexico’s relatively limited exposure to the Iran conflict. MXN is currently performing poorly in iFlow, which points to concerns over real rates, especially relative to LatAm peers, which have stronger profiles and greater crude exposure. However, the general overheld position for regional currencies should remain intact.

Source: BNY

Source: BNY