Market Movers: Vigilance

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Geoffrey Yu

Time to Read: 8 minutes

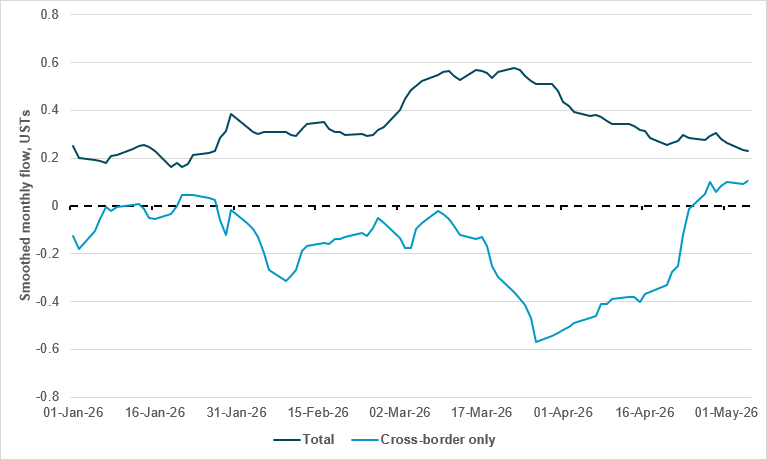

Cross-border investors can return to U.S. Treasury markets on a far greater scale

Source: BNY

A true end to the Iran conflict may still be some way off, but the market is increasingly confident that this is the broader direction. Yesterday’s news of a potential memo to this effect has driven a strong move in bond markets. As oil prices decline and fears over inflation ease, we would naturally expect a decent move in bonds as real rates reprice globally, almost without exception.

However, the flow performance of individual markets has been highly uneven over the last month, and the risk-reward payoff in chasing the bond rally differs widely. For example, on a regional basis we would be wary of aggressively chasing developed market European bonds, even though yields have moved quite aggressively of late, e.g., with U.K. very long-dated borrowing costs reaching a 28-year high. Conversely, although nominal yields in APAC are low, the selling has been just as strong in magnitude, and this is where risk-reward could be much more favorable. Composition of client flows also matters, and this will have FX implications as well in due course.

The U.S. Treasury market has also reacted strongly to hopes of an end to the conflict, just as the foreign vs. domestic gap is starting to close. On the real rates side, we stress that the sales seen through the last six weeks are still a function of liquidity needs rather than worries over U.S fiscal conditions or inflation-driven steepening, even though those factors will need to feature more heavily over the medium term. By default, if oil prices ease, exporter surpluses could rise from here and normal service will resume in reserve management trends, which will continue to heavily favor the dollar’s performance.

Risk sentiment continues to grind higher as all indications point to progress toward peace in the form of the one-page memorandum reported yesterday. Japan’s return to markets after the holiday period also produced another strong session in Asia. Japan saw a 5.6% catch-up gain, shrugging off any worries about an earnings translation hit from a stronger JPY, as intervention risk continues. Nonetheless, we expect questions to linger over the ability of markets to defy more prolonged supply shocks and the potential policy response. Yesterday’s moves in fixed income globally have helped pushed out inflation premiums, but a swift return to the pre-conflict status quo in energy is unrealistic. Even with secular investment themes such as data centers and semiconductor fabrication, direct cost increases and indirect cost transmission into the wider economy will create earnings headwinds.

The cost of AI infrastructure comes in all shapes and forms: As companies directly tied to the semiconductor industry continue to deliver upside earnings surprises, the demand angle is not in question. However, warnings about supply crunches continue to be interspersed across earnings reports. Some factors were existent before the war, but the cost pressures will only intensify in the near term due to input disruptions. Rapid reopening of the Strait of Hormuz is only the first step, as bringing facilities back on line and delivering raw, intermediate and finished goods will involve a time lag. Meanwhile, regulatory pressures regarding data centers are also growing: Denmark’s state-owned grid operator has paused new data center grid connections due to high demand. The Nordic region has been a key destination for data center investment for structural reasons but any sign of infringement on normal usage, especially amid the current global energy shock, will understandably lead to a political pushback.

Hawkish surprises still possible: Norges Bank confounded expectations in delivering its first rate hike since 2023, pushing the deposit rate to 4.25%. The central bank was blunt in stating that “inflation is too high,” but Governor Ida Wolden Bache also stressed that the rate rise was “not only due to war impacts” and that the central bank had to react to the strong wage growth seen in recent years. Bank Negara Malaysia and the Riksbank remained on hold, preferring a “wait-and-see” approach but maintaining maximum vigilance over inflation pressures as the war continues to keep energy costs elevated. Despite very different economic structures and exposures, Sweden and Malaysia both face downside growth risks, which their central banks hope will be sufficient to anchor inflation expectations for now.

European fiscal risk to test the bond rally: The main political event of the day is local elections in the U.K. A loss of more than 2,000 council seats for the Labour Party is generally seen as a worse-than-expected result for the ruling party, and the market fears that whatever the ramifications for individuals, there will be a push for greater fiscal spending to help alleviate the cost of living crisis. There will be similar calls elsewhere, and we are already seeing repeated upward revisions to fiscal deficit projections in Central and Eastern Europe. For now, the impact on currencies has been surprisingly muted as yields remain firm, but any extension of yesterday’s moves in bonds will likely hinge on fiscal outcomes up ahead.

Bottom line: The market’s risk-positive framework will continue if tech and AI-related earnings deliver, but selectivity will likely come through as cost pressures are brought to bear. Either this will come through via cost pressures directly, or central banks will start to react more aggressively, although this is not our base case. Ultimately, we doubt markets will react to hawkish surprises unless there is a material shift in Fed expectations – which seems unlikely given the need for labor market caution. Today will bring more commentary from Fed members to help investors gauge whether there will be a shift in the direction of travel, or whether maximum vigilance while current policy is in a “good place” is adequate. The latter appears to be the default position in developed markets, but there is high skepticism regarding the sustainability of this approach. Nonetheless, the burden of proof for bears remains tilted toward disappointments in the technology and U.S. growth themes, be it from earnings reports, infrastructure investment levels or even trade data from key semiconductor fabrication economies.

U.S. Treasury Secretary Scott Bessent will visit Japan for three days next week, meeting Prime Minister Sanae Takaichi, Finance Minister Satsuki Katayama and BoJ Japan Governor Kazuo Ueda. Discussions are expected to focus on recent currency market volatility, including Japan’s recent intervention to support the yen, alongside rare earths minerals and the Iran conflict. This visit precedes the U.S.-China summit in Beijing on May 14-15, where Bessent and President Trump will meet Chinese President Xi Jinping. Japan reportedly spent around $34.5bn to curb speculative trading in its first yen intervention since July 2024. S&P Mini +0.16% to 7401, DXY -0.116% to 97.91, 10y UST -2.3bp to 4.326%.

China’s financial regulator has advised major banks to temporarily halt new yuan-denominated loans to five refineries recently sanctioned by the U.S. for ties to Iranian oil, including Hengli Petrochemical. Banks were instructed to review their exposure but not to call in existing loans. This directive contrasts with China’s Ministry of Commerce urging companies to ignore U.S. sanctions, reflecting Beijing’s efforts to balance defiance toward Washington with protecting state-owned banks against secondary sanctions. The U.S. has warned Chinese banks of sanctions risks linked to Iranian oil transactions ahead of the upcoming Trump-Xi summit in mid-May. CSI 300 +0.48% to 4901, USDCNY +0.147% to 6.8025, 10y CGB -0.5bp to 1.758%.

South Korea will extend its ban on hoarding petroleum products for two more months to July amid ongoing supply concerns from the Middle East conflict, Finance Minister Koo Yun-cheol has announced. The original ban, which took effect in March, aims to prevent unfair practices such as sales refusal under the price ceiling. Additional measures include a reward program to deter hoarding and stricter enforcement of the tariff-rate quota system on essential imports. The mandatory release period for imported sugar under this system will be shortened from six to four months. The government is closely monitoring potential U.S.-Iran ceasefire talks. KOSPI +1.43% to 7490, USDKRW -0.063% to 1448.7, 10y KTB +0.2bp to 3.935%.

Norges Bank has raised its policy rate by 25bp to 4.25%, defying market expectations of a hold, citing persistently elevated inflation and ongoing upside risks to price growth. The decision reflects concerns that inflation, which has been above target for several years, could remain elevated due to higher wage growth and stronger external price pressures linked to the Middle East conflict, particularly through energy markets. While domestic economic conditions, including employment and capacity utilization, remain broadly stable, policymakers emphasized that there is significant uncertainty around the outlook. The bank indicated that rate projections are largely unchanged, with the policy rate expected to rise further this year if needed to ensure inflation returns to target within a reasonable timeframe. OSE -0.78% to 1986, EURNOK -0.527% to 10.8689, 10y NGB -0.4bp to 4.408%.

U.S. Q1 preliminary non-farm productivity is expected to ease to 0.6% q/q vs. 1.8% q/q.

U.S. Q1 preliminary unit labor costs are expected to ease to 2.5% q/q vs. 4.4% q/q.

U.S. initial jobless claims are expected to rise to 205k vs. 189k.

U.S. March construction spending is expected to rise to 0.2% m/m vs. -0.3% m/m.

U.S. NY Fed 1-year inflation expectations are expected at 3.5% vs. 3.42%.

U.S. March consumer credit is expected to rise to $13.25bn vs. $9.484bn.

U.S. Treasury sells $90bn in 4-week bills and $85bn in 8-week bills.

Central bank speakers:

Cleveland Fed President Beth Hammack speaks on WOSU public radio in Columbus, Ohio at 10 ET.

San Francisco Fed President Mary Daly appears on Bloomberg TV at 12:30 ET.

Minneapolis Fed President Neel Kashkari participates in a fireside chat in Michigan at 13:00 ET.

Cleveland Fed President Beth Hammack speaks in a fireside chat in Columbus at 14:05 ET.

New York Fed President John Williams participates in a moderated discussion on regional economic insights at 15:30 ET.

Mood: iFlow Mood turned negative (-0.007) for the first time since early April, as demand for core government bonds outpaced buying of global equities.

FX: Flows were moderate and mixed. There were notable outflows for COP and MXN, against strong buying in USD, HUF and NOK. Elsewhere, CNY and INR saw inflows, while EUR, JPY and KRW were sold.

FI: Demand for Eurozone and Canadian government bonds and U.K. gilts was firm. Selling was concentrated in Chinese and Malaysian government bonds.

Equities: Flows were broadly weak across G10 and EMEA, with exceptions in U.S. and South African equities, which saw buying. LatAm and APAC flows were mixed: strong inflows into Chinese and Malaysian equities were offset by significant outflows from Hong Kong, South Korea and Taiwan.

“Never believe any war will be smooth and easy.” – Winston Churchill

“No nation could preserve its freedom in the midst of continual warfare.” – James Madison

U.S. Challenger job cuts data for April show layoffs rose sharply to 83,387, up 38% m/m but down 21% y/y, highlighting continued volatility in labor market adjustments. YTD, announced job cuts totaled 300,749, representing a 50% reduction compared with the same period in 2025, indicating a significantly lower cumulative pace of layoffs. The technology sector remained the primary driver of cuts, with AI cited as a leading factor behind restructuring decisions, accounting for a growing share of layoffs. Other sectors such as pharmaceuticals, chemicals and industrial goods also saw sizable increases in job reductions. Meanwhile, hiring plans weakened materially, falling both m/m and y/y, suggesting softer forward labor demand despite lower cumulative layoffs overall. S&P Mini +0.19% to 7403, DXY -0.142% to 97.884, 10y UST -2.2bp to 4.327%.

Euro area retail trade edged down by 0.1% m/m in March, while EU retail sales increased by 0.3%, indicating mixed short-term momentum across the region. On a y/y basis, retail volumes rose by 1.2% in the euro area and 1.9% in the EU, pointing to modest underlying growth. Sector data show that m/m weakness in the euro area was driven by declines in food and automotive fuel sales, partly offset by gains in non-food retailing. Across member states, performance was uneven, with strong increases in countries such as Slovenia and Luxembourg, while Germany recorded a substantial contraction. Overall, the data suggest subdued but still-positive consumer demand trends amid divergent national developments. Euro Stoxx 50 +0.33% to 6047, EURUSD +0.154% to 1.1766, BBG AGG Euro Government High Grade EUR -0.4bp to 3.35%.

Eurozone construction activity deteriorated further in April, with the construction PMI falling to 41.7 points from 44.6 in March, signaling the sharpest contraction since August 2024 and extending a prolonged period of decline. The downturn was broad-based across countries and sectors, with commercial and residential activity weakening significantly, while civil engineering also declined. New orders fell at the fastest pace in 17 months, reflecting subdued demand amid rising uncertainty and elevated costs. Input price inflation accelerated to its highest level since late 2022, driven by higher material costs linked to geopolitical tensions, which further weighed on activity. Employment declined for a third consecutive month, and business sentiment weakened to a 16-month low, pointing to continued fragility in the sector outlook.

German services turnover rose modestly in February, with real revenue increasing by 0.3% m/m and 2.4% y/y, while nominal turnover grew by 0.5% m/m and 4.0% y/y, indicating continued but moderate expansion in the sector. The release highlights that growth was uneven across subsectors, with professional, scientific and technical services leading monthly gains at 0.9%, followed by transport and storage at 0.4%, while information and communication recorded a 0.3% increase. Other business services and real estate activities posted smaller gains of 0.2%. Overall, the data suggest stable underlying momentum in Germany’s services sector, supported by broad-based but relatively subdued increases across key industries. DAX +0.29% to 24991, EURUSD -0.187% to 1.1767, 10y Bund -2.3bp to 2.976%.

German manufacturing orders increased strongly in March, rising 5.0% m/m and 6.3% y/y in real terms, following an upwardly revised 1.4% m/m gain in February. The report indicates that the expansion was broad-based across sectors, with particularly strong contributions from electrical equipment, machinery and electronics, while orders excluding large contracts also rose 5.1% to reach their highest level since February 2023. By demand category, intermediate goods orders led gains, followed by consumer and capital goods, while geographically both domestic and foreign demand contributed, with euro area orders substantially stronger. Despite the m/m rally, Q1 orders were still below the previous quarter due to prior large order volatility, pointing to uneven underlying momentum.

France’s trade balance deteriorated further in March, with the deficit widening by €1.4bn m/m to -€6.9bn, primarily driven by a strong increase in imports that outpaced export growth. Imports rose by €1.8bn, largely due to higher energy purchases amid rising prices linked to geopolitical tensions, while exports increased by a more modest €0.5bn, also supported by energy products. The data show that the energy balance was the main drag, alongside weaker balances in transport equipment and machinery. Geographically, there were wider deficits with Europe, the Americas and the Middle East, partly offset by improvements with Asia and Africa. Overall, the release highlights energy-driven import pressures as the key factor behind the worsening external position. CAC 40 +0.53% to 8343, EURUSD -0.187% to 1.1767, 10y OAT -3bp to 3.593%.

French Q1 wage growth data show the basic monthly salary index increased by 0.7% q/q and around 1.6-1.7% y/y, broadly unchanged from the previous quarter. Meanwhile, the hourly wage index for workers and employees also rose 0.7% q/q and 1.6% y/y. By sector, wage growth was slightly stronger in construction and industry than in services, with similar modest gains across occupational groups. However, with consumer price inflation running at 1.7% y/y, real wage dynamics remained weak, as the hourly wage index fell 0.1% in real terms and the monthly salary index was broadly flat. Overall, the data indicate nominal wage stability but limited real income growth amid persistent inflation pressures.

U.K. construction activity contracted sharply in April, with the construction PMI falling to 39.7 points from 45.6 in March. This was the weakest reading in five months, signaling a deepening downturn in the sector. The decline was broad-based across subsectors, led by civil engineering and housebuilding, while commercial construction also weakened. New business fell at the fastest pace since November 2025, reflecting subdued demand and heightened uncertainty, particularly linked to the Middle East conflict. At the same time, input cost inflation surged to its strongest level since mid-2022, driven by higher fuel and material costs, while supply chain delays intensified. Employment declined further, and business confidence weakened, pointing to ongoing pressures on activity. FTSE 100 -0.58% to 10378, GBPUSD +0.214% to 1.3622, 10y gilt -2.6bp to 4.913%.

Swiss unemployment data for April show the jobless rate dipping to 3.0%, down 0.1 percentage points from March. It was unchanged on a seasonally adjusted basis, indicating broadly stable labor market conditions. The number of registered unemployed fell by 3,353 to 142,902, while total jobseekers also declined by 4,206 to 230,609, suggesting some improvement in labor demand. However, leading indicators were mixed, as reported vacancies decreased by 408 to 48,435, pointing to softer hiring momentum. In addition, earlier data on short-time working showed a deterioration, with the number of affected workers rising by around 14% in January, highlighting pockets of weakness despite the overall stable unemployment rate. SMI +0.39% to 13335, EURCHF +0.18% to 0.91502, 10y Swiss GB -1.6bp to 0.372%.

Sweden’s Riksbank has decided to keep its policy rate unchanged at 1.75%, citing heightened uncertainty linked to the ongoing Middle East conflict and its global economic spillovers. The policy board warned that the conflict has pushed up oil and commodity prices, raising cost pressures and increasing the risks of higher inflation, although current inflation remains below target and recent readings have undershot forecasts. At the same time, economic activity in Sweden has been weaker than expected at the start of the year, prompting a cautious policy stance. The Riksbank emphasized that while the current rate provides flexibility, it is ready to tighten policy if inflation pressures become broad and persistent, while continuing to monitor risks to growth and inflation closely. OMX +0.05% to 3161, EURSEK -0.226% to 10.8427, 10y Swedish GB -2.4bp to 2.763%.

Norway’s Q1 unemployment rate stood at 4.7% of the labor force, equivalent to around 144,000 people, indicating a stabilization following earlier increases in 2025. The report notes that while unemployment has leveled off over the past four quarters, it remains above the long-term average of roughly 4.0%, reflecting a structurally higher level of slack. The recent rise in unemployment has been driven more by an expansion in the labor force than by a decline in employment, suggesting stronger participation dynamics. Additional breakdowns show that a significant share of unemployed individuals are young and seeking part-time work, while broader measures indicate substantial underutilized labor capacity beyond headline unemployment, pointing to lingering slack in the labor market. OSE -0.78% to 1986, EURNOK -0.527% to 10.8689, 10y NGB -0.4bp to 4.408%.

Norwegian employment data for Q1 show job growth remained subdued, with total employment rising by 0.5% y/y. This is equivalent to an increase of around 14,300 jobs and represents the weakest growth in recent years. The report highlights declining labor market dynamism, as both hiring and separations continued to fall, with hiring dropping more sharply, dampening net job creation. Sector trends were mixed, with the strongest gains in accommodation and food services, and transport, while education and construction recorded significant job losses. Public sector employment, particularly in education, continued to contract, driven largely by reductions in temporary roles. Meanwhile, wage growth remained relatively firm at 4.3% y/y, suggesting continued earnings resilience despite weakening employment momentum.

Hungarian retail sales grew strongly in March, with volumes up 1.9% m/m and 8.2% y/y on a calendar-adjusted basis, indicating solid momentum in consumer demand. Growth was broad-based but led by non-food retailing, which expanded by 8.4% y/y. Food sales rose a more modest 2.6% and automotive fuel sales surged by 20.6%, reflecting both volume and price effects. Online and mail order sales also recorded double-digit growth, reinforcing structural shifts in consumption patterns. Over Q1 as a whole, retail volumes increased by 5.3% y/y, suggesting a sustained recovery in household spending supported by strong gains across key retail segments. Budapest SI +0.03% to 135940, EURHUF +0.233% to 357.25, 10y HGB -12bp to 5.9%.

Czechia’s trade balance for March came in at a surplus of CZK 31.9bn, widening by CZK 3.8bn y/y, as export growth outpaced imports. Exports increased by 6.5% y/y to CZK 459.1bn, while imports rose 6.0% to CZK 427.2bn, with the balance supported by stronger surpluses in transport equipment and motor vehicles and a narrower deficit in electronics. However, gains were partly offset by a deeper deficit in petroleum products, metals and pharmaceuticals. By region, the surplus with EU countries expanded, while the deficit with non-EU partners widened. On a q/q basis, the surplus narrowed to CZK 73.0bn, and on a m/m basis exports rose modestly while imports declined, indicating mixed underlying momentum. Prague SE +0.72% to 2545, EURCZK +0.029% to 24.32, 10y CZGB -4.8bp to 4.775%.

Czech industrial production increased by 0.9% y/y but fell 0.2% m/m in March, as growth momentum softened. The expansion was supported mainly by fabricated metal products and transport equipment, alongside gains in chemicals and food production, although some sectors declined due to base effects. New industrial orders rose by 1.2% y/y, driven by stronger foreign demand, which increased by 2.5%. Meanwhile, domestic orders fell by 1.1%, pointing to external demand resilience but weaker internal conditions. On a m/m basis, new orders rose 0.9%. Industrial employment continued to contract, with the average number of employees falling by 1.1% y/y, highlighting ongoing labor market adjustment within the sector.

Australia’s international trade in goods for March 2026 showed a seasonally adjusted deficit of AU$1.841bn, the first deficit since December 2017, down AU$6.867bn from February’s surplus of AU$5.026bn. Exports fell by 2.7% m/m and 2.1% y/y to AU$43.929mn, mainly due to a 11.6% m/m decline in rural goods, while non-rural goods were stable. Imports rose 14.1% m/m, 20.3% y/y to AU$45.770bn, driven by a 36.8% m/m increase in capital goods, particularly automatic data processing equipment (204.4% m/m). Key export commodities such as iron ore and coal saw mixed m/m volume changes, with some increases after prior declines. ASX -0.34% to 5583, AUDUSD -0.097% to 0.7262, 10y ACGB -3.1bp to 4.922%.

Japanese office market data for April show Tokyo business district vacancy rates declined to 2.20%, down 0.02 percentage points m/m and 1.53 percentage points y/y, marking the first drop in three months. Average rents rose for a 27th consecutive month to ¥22,454 per tsubo, up 0.68% m/m and 8.19% y/y. The report highlights that vacancy reductions were driven by strong leasing in newly completed buildings and expansion-related demand, offsetting some new supply and downsizing moves. The new building vacancy rate fell to 12.11%, while existing stock remained tight at 2.02%. District-level data indicate mixed vacancy movements but broadly rising rents across all five central wards, reinforcing a continued tightening and upward pricing trend.

Japan’s monetary base shrank by 11.3% y/y to ¥590.9tn in April. This follows a 11.6% y/y decrease in March. Key components contributing to the decline include current account balances, down 13.5% y/y, and reserve balances, down 12.0% y/y. Banknotes and coins in circulation also fell slightly by 1.8% and 1.1% y/y, respectively. The seasonally adjusted annual rate showed a smaller decline of 5.6% in April, improving from a 22.8% drop in March. Overall, the monetary base contraction continues, but at a gentler pace.

The BoJ released the minutes of its March 18-19 monetary policy meeting. These show that it discussed maintaining the uncollateralized overnight call rate at around 0.75%, amid concerns over inflation risks from rising crude oil prices due to Middle East tensions. While some members favored a rate hike to about 1.0% to address upside price risks and real interest rate differentials, most agreed to hold rates for now, monitoring economic and price developments. The impact of prior rate hikes on firms and households remains limited, with labor shortages and material costs affecting investment more than rates. The bank is planning gradual rate increases aligned with the economic and inflation outlooks, emphasizing careful assessment of risks and enhanced communication on underlying inflation.

Bank Negara Malaysia’s Monetary Policy Committee decided to keep its Overnight Policy Rate unchanged at 2.75%, highlighting a cautious stance amid rising external uncertainties. The decision reflects resilient global and domestic growth conditions in early 2026, supported by domestic demand and strong exports, particularly in electronics, although escalating energy prices and supply disruptions linked to the Middle East conflict are beginning to weigh on momentum. The central bank noted that Malaysia’s growth outlook remains supported by investment projects, household spending and tourism, but faces downside risks from a prolonged conflict. Inflation, which averaged 1.6% (headline) and 2.1% (core) in Q1, is expected to edge higher but remain contained, with policy deemed appropriate to balance price stability and growth risks. KLCI +0.3% to 1762, USDMYR +0.341% to 3.9097, 10y MGB +0.2bp to 3.574%.

The Philippines’ GDP grew by 0.9% q/q, 2.8% y/y in Q1 vs. 0.6% q/q, 3.0% y/y in Q4 2025. This is the slowest GDP growth since Q4 2009 outside of the COVID period. Key contributors were wholesale and retail trade (4.6% y/y), financial and insurance activities (3.4% y/y) and public administration and defense (8.6% y/y). By sector, services expanded by 4.5% y/y, while agriculture (-0.2% y/y) and industry (-0.1% y/y) contracted. On the demand side, household consumption rose by 3.0% y/y, government consumption by 4.8%, exports by 7.8% and imports by 6.1%. Gross capital formation declined by 3.3%. Gross national income rose 3.0% y/y, with net primary income from abroad up 4.5%. PSEi +1.12% to 6034, USDPHP +1.54% to 60.416, 10y PHGB -15.3bp to 6.99%.

Taiwan’s April CPI was up 0.79% m/m and 1.74% y/y (March: +1.20% y/y), driven by higher prices for spring/summer clothing, fuel, vegetables, dining out and travel costs during holidays. Core CPI increased by 1.91% y/y (March: 1.94% y/y). Food prices rose 0.39% m/m, led by a 5.52% increase in vegetables, while fruits were down. Fuel costs rose 10.54% m/m due to deferred March adjustments. PPI increased by 3.04% m/m and 8.54% y/y, supported by higher prices for petroleum, chemicals, electronics and pharmaceuticals. Import and export prices rose significantly, with export prices up 2.78% m/m and 18.00% y/y in USD terms. TAIEX +1.93% to 41934, USDTWD +0.303% to 31.393, 10y TGB +2.1bp to 1.522%.