Market Movers: Shifting Leadership

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 7 minutes

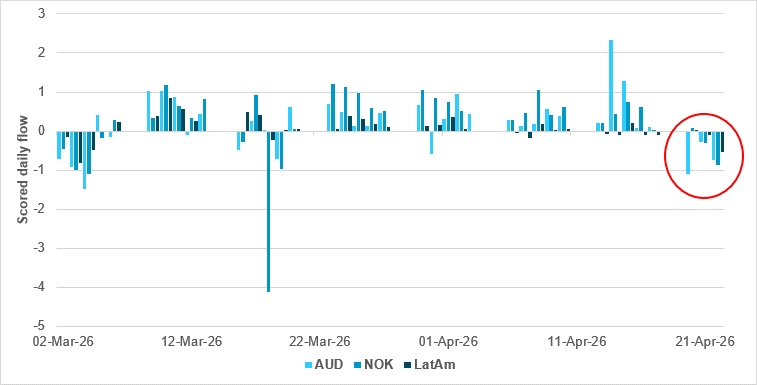

Softening in commodity FX flows emerging

Source: BNY

Markets remain uneasy, but recent trends still point toward gradual de-escalation, suggesting recovery flows could build while conflict hedges lose support. Commodity FX has led, especially in LatAm, along with NOK and AUD in the G10, which are benefiting from energy and hawkish policy, reinforcing carry dynamics.

However, momentum is turning, as flows soften across commodity currencies. LatAm has seen the sharpest reversal – the first five days of selling since the conflict began. Meanwhile AUD has recorded its biggest three-day outflows and NOK has seen two days of outflows as policy expectations peak and hedge demand unwinds, though conviction remains low. Even while the energy backdrop remains supportive, we believe NOK has largely completed its re-rating, particularly as Norges Bank has signaled a commitment to one further hike while pushing back against the prospect of additional tightening.

There is a shifting focus today across markets despite the usual weekend worries and next week’s heavy month-end news agenda, with central bank decisions and more economic data on growth and inflation. Market leadership returned to technology over energy overnight. Earnings reports and outlooks are driving global equities higher on the week, but unevenly. Risk sentiment suggests less effect from the ongoing geopolitical backdrop with Iran, even as oil prices ratchet higher. There are some clear exceptions, mostly in emerging markets. Indonesia saw its stock market drop for the fifth day in a row, its worst run since February 2025; bank shares are sagging, with IDR seeing ongoing intervention but still 3% weaker since the start of the war. The main difference today lies in that break of correlation, with USD higher, stocks higher, oil higher and bond yields higher – not the usual mix. The economic data continue to lag as a driver, although in Japan CPI was higher and in the U.K. retail sales surged. The host of central bank decisions next week are producing shifts in swap markets, with rolling risks of June action.

Bottom line: USD is up 0.6% on the week – the first gain in a month. This is something to watch today, given that equity futures point to a higher open, led by technology. Dollar intervention risks are rising, with JPY 160 clearly in play overnight and the country’s higher inflation putting the BoJ in a tougher position next week. Risk sentiment is not robust, but right now that matters less than the earnings releases that are beating expectations. Oil remains the barometer, but fears of any U.S./Iran weekend escalation are looked through as the narrative continues to see a deal in the making. Trading markets on the price of oil is not working today or this week, suggesting investors are looking for new leadership as they climb the wall of worry into month-end next week.

The global natural gas market is expected to remain tight for at least two more years as the Iran war continues to disrupt supply and delay the anticipated LNG expansion, says the International Energy Agency. The conflict has effectively removed around one-fifth of global oil and LNG supply, while damage to Qatari facilities has reduced liquefaction capacity and could take years to repair, pushing back the impact of new supply growth led by the U.S. The IEA estimates a cumulative shortfall of around 120 billion cubic meters between 2026 and 2030, reinforcing a prolonged period of tight market conditions. In response, gas demand has softened in key importing regions, particularly in Asia, as higher prices and policy measures drive fuel switching and reductions in consumption. HH natural gas -1.531% to 2.574, Dutch TTF natural gas +1.673% to 45.24.

An internal Pentagon email has outlined potential measures to penalize NATO allies, particularly Spain, following divisions over support for U.S. operations in the Iran war, highlighting deepening strains within the alliance. The proposals include suspending Spain from NATO roles and reconsidering U.S. backing for U.K. sovereignty over the Falkland Islands. This reflects frustration over allies’ refusal to grant access, basing and overflight rights during the conflict. The Trump administration views European partners as insufficiently supportive and aims to reduce what it sees as their sense of entitlement. While no formal policy decisions have been made, the discussion is a sign of escalating tensions and raises broader concerns about NATO cohesion and the future of transatlantic security cooperation. Euro Stoxx 50 -0.29% to 5878, EURUSD +0.069% to 1.1691, BBG AGG Euro Government High Grade EUR +1.1bp to 3.239%.

China’s Ministry of Commerce has announced that it has added seven EU entities to its export control list, citing their involvement in military-related activities linked to Taiwan. The measures prohibit Chinese exporters from supplying dual-use items to these entities and ban third parties from transferring such goods originating from China to them, with all ongoing related activities required to cease immediately. The authorities emphasized that the action targets only a limited number of EU entities and applies specifically to dual-use goods, stating it will not affect normal China-EU trade relations. Beijing also noted that it had informed the EU through bilateral dialogue mechanisms in advance and reiterated its commitment to maintaining global supply chain stability.

BoE Deputy Governor Sarah Breeden has warned that global equity markets may be underpricing risks despite record high share prices, highlighting a growing disconnect between asset valuations and underlying economic pressures. She pointed to elevated geopolitical uncertainty linked to the Iran conflict and cautioned that markets appear insufficiently priced for potential shocks. Breeden emphasized the risk of multiple stress events occurring simultaneously, including a macroeconomic downturn, a correction in AI related valuations and instability in private credit markets. Her comments come as global equities continue to rally on strong earnings and improved sentiment, raising concerns that a sharp adjustment could occur if these risks materialize. MSCI World -0.37% to 1067, DXY -0.004% to 98.767, BBG Global Aggregate 0bp to 3.733%.

Japan’s Finance Minister Satsuki Katayama has indicated that policymakers are taking a cautious wait-and-see approach to the economic outlook amid heightened global uncertainty from the Middle East conflict. She noted that Japan has so far avoided a significant impact on growth or inflation but risks remain fluid. Katayama highlighted that the yen remains vulnerable to volatility driven not only by strong U.S. economic performance, but also by speculation linked to movements in oil markets, with recent swings in crude prices amplifying currency fluctuations. Authorities are in close coordination with the U.S. and retain full flexibility to intervene in foreign exchange markets if needed, with past interventions proving effective. While the yen’s weakness is partly dollar-driven, Katayama stressed that speculative activity is contributing to instability, and officials are prepared to take decisive action to stabilize markets if volatility intensifies. Nikkei +0.97% to 59716, USDJPY +0.019% to 159.74, 10y JGB +1bp to 2.439%.

U.S. April Final University of Michigan consumer sentiment is forecast to rise to 48.5 vs. 47.6, while 1y inflation expectations are expected at 4.8% vs. a flash estimate of 4.80% and 3.8% in March and 5-10y inflation expectations are expected at 3.4% vs. a 3.40% flash estimate and 3.2% in March.

U.S. April Kansas City Fed services activity is expected at 10 points vs. 15.

Canada February retail sales are expected to ease to 0.9% m/m vs. 1.1% m/m.

Canada February retail sales ex auto are expected to hold at 0.8% m/m vs. 0.8% m/m.

Mood: Cash is being redeployed, with sustained equity buying and a return of demand for core sovereign bonds for the first time in April. iFlow Mood has eased slightly to 0.219.

FX: Flows were mixed and moderate, with no strong directional bias. G10 FX remained bid overall, except for light USD and AUD outflows. EMEA and LatAm saw net outflows, while HKD inflows stood out in APAC.

FI: Divergence across regions. Australia saw substantial selling, while Eurozone government bonds and U.K. gilts attracted solid demand. LatAm and EMEA bonds were better bid, whereas APAC flows remained skewed toward selling.

Equities: Strong demand in LatAm, China and Sweden, with no notable outflows. In contrast, equities in Europe, the U.K. and the U.S. saw light selling.

“Leadership is not the power to command but the courage to serve.” – Plato

“The first step toward getting somewhere is to decide you are not going to stay where you are.” – John Pierpont Morgan

Germany’s Ifo business climate index fell to 84.4 points in April, from 86.4. This marks its lowest level since May 2020 and signals a sharp deterioration in economic sentiment. The decline was driven by significantly more pessimistic expectations and weaker assessments of current conditions, with the Iran conflict cited as a key drag on the economy. Weakness was broad-based across sectors, with manufacturing hit by worsening outlooks and supply bottlenecks, particularly in chemicals, while services saw a sharp drop led by logistics pressures. Retail sentiment deteriorated amid concerns over inflation-induced weakening in consumer demand, and construction experienced a pronounced collapse in confidence, with expectations falling sharply and hopes of a near-term recovery fading. DAX +0.08% to 24175, EURUSD +0.069% to 1.1691, 10y Bund +3bp to 3.039%.

France’s consumer confidence fell sharply in April, with the headline indicator declining to 84. This 5-point m/m fall is the largest drop since early 2022, taking the measure further below its long-term average. The deterioration was broad-based, with households reporting significantly weaker views on both past and future personal financial conditions, alongside a reduced willingness to make major purchases. While savings capacity also fell, it remained above historical norms, suggesting some residual financial buffers. Perceptions of the national economic outlook worsened further, with sharp declines in views on living standards and a rise in unemployment concerns. Inflation perceptions surged significantly, with households reporting a strong increase in past price growth and higher expectations for future inflation. CAC 40 -0.79% to 8162, EURUSD +0.069% to 1.1691, 10y OAT +3.6bp to 3.7%.

Spain’s industrial producer prices rose by 3.4% y/y in March, a sharp increase of 10.3 percentage points from the previous month, while surging 6.5% on a m/m basis, indicating a strong resurgence in pipeline inflation. The acceleration was driven primarily by the energy sector, where prices rose significantly due to higher electricity generation and petroleum refining costs, alongside rises in gas production. Intermediate goods also contributed modestly, reflecting rising chemical input prices. Excluding energy, producer price growth was more subdued at 1.2%, highlighting the dominant role of energy in the overall increase. M/m dynamics were led by a sharp jump in refining activity, while food-related components exerted slight downward pressure. IBEX 35 -0.95% to 17676, EURUSD +0.069% to 1.1691, 10y Bono +3.7bp to 3.508%.

Spanish mortgage approvals rose by 16.3% y/y in March, with 45,563 new residential mortgages registered, while the average loan size increased by 11.0% to €173,280, indicating continued strength in housing credit demand. Total capital lent for residential mortgages also expanded strongly, reflecting both higher volumes and larger loan sizes. The average interest rate on new mortgages stood at 2.88%, with a majority of loans issued at fixed rates, highlighting relatively stable financing conditions. Meanwhile, the number of mortgage modifications fell y/y, suggesting reduced refinancing activity despite rising borrowing volumes. By region, growth was strongest in Madrid, Castilla La Mancha and Andalusia, pointing to uneven geographic dynamics in housing market activity.

U.K. firms reported higher inflation expectations in the Bank of England’s Decision Maker Panel survey for April. Year-ahead own price growth increased to 3.8% from 3.5% previously, while realized price growth remained steady at 3.7%, indicating renewed upward pressure linked to higher energy costs. Consumer price inflation expectations also increased to 3.5% over the next year, with shorter-term indicators showing a sharper rise, while longer-term expectations edged up to 2.8%. Wage dynamics were more stable, with realized wage growth holding at 4.3% and expected growth easing slightly to 3.4%. Labor market conditions softened, with employment contracting by 0.4% and expectations weakening to zero growth, while firms expect higher prices and lower margins from the energy shock. FTSE 100 -0.49% to 10406, GBPUSD +0.104% to 1.3481, 10y gilt +5bp to 4.989%.

The BoE’s agents’ summary of business conditions for April 2026 indicates weak economic activity. It shows subdued annual output growth, dragged down by declines in construction and manufacturing, while demand remains soft across business services, exports and household consumption. Confidence has deteriorated since the Middle East conflict began, reversing earlier optimism about a modest recovery, although direct impacts on activity remain limited so far. Employment intentions are broadly flat, with pay settlements averaging around 3.5%, and little immediate effect from the conflict. Input cost pressures have risen due to higher oil and transport costs, but price inflation remains contained overall. The outlook suggests that higher energy costs may offset disinflation elsewhere, with uncertainty around the balance between rising costs and weak demand.

U.K. retail sales volumes rose by 0.7% m/m in March, contributing to a 1.6% q/q increase in Q1, indicating a modest recovery in consumer spending. The m/m rise followed a revised decline in February and reflected strong fuel sales, as consumers brought forward purchases amid rising prices, alongside gains in clothing driven by improved weather conditions. Excluding fuel, retail sales increased by 0.2% m/m, supported by growth in non-food categories such as cosmetics, telecommunications and online retail, with new product launches boosting demand. Overall, the data point to a gradual strengthening in retail activity, led by discretionary spending and non-store channels.

Sweden’s producer price index rose by 2.0% y/y in March, rebounding from a decline in February, and climbed 0.6% m/m, driven by strong gains in export and import prices despite a contraction in domestic prices. Export prices were up 3.5% and import prices surged 6.5% m/m, supported by a sharp rise in crude oil costs and higher prices for refined petroleum products, chemicals and metals; prices in the domestic market fell 2.0%, due mainly to lower electricity-related prices. The Swedish krona’s weakness against major currencies added upward pressure on import prices, while producer prices excluding energy edged down slightly y/y, indicating more subdued underlying inflation dynamics. OMX -1.3% to 3091, EURSEK +0.044% to 10.8276, 10y Swedish GB +2.5bp to 2.878%.

Norway’s consumer confidence index remained deeply negative in April at -19.1, little changed from March and highlighting persistently weak sentiment following the geopolitical shock from the Iran conflict. The index has remained well below recent averages, reflecting continued pessimism driven by high energy and commodity prices, ongoing trade uncertainty and expectations of further interest rate increases by Norges Bank. More than half of respondents expect the national economy to worsen over the next year, while household-level expectations have also deteriorated, with significantly more consumers anticipating weaker personal finances than improvements. The data suggest that negative sentiment has become entrenched, with economic uncertainty and global risks increasingly shaping Norwegian consumer behavior. OSE +0.2% to 2008, EURNOK +0.037% to 10.9261, 10y NGB +2bp to 4.425%.

Poland’s April business climate indicators pointed to broadly stable or improving economic conditions, with the strongest gains in accommodation and food services and continued strength in financial activities, while transport and storage experienced a sizable deterioration. Manufacturing and construction remained in negative territory but showed modest m/m improvement, while retail trade was broadly stable. The overall synthetic indicator rose to 99.0, approaching its long-term average, supported by stronger current conditions despite weaker forward-looking expectations. Firms reported easing constraints from weak demand and labor costs y/y, but increasing concerns about economic uncertainty and rising energy-related costs, with price expectations generally pointing to slower increases ahead. WIG -0.64% to 130576, EURPLN -0.012% to 4.2423, 10y PGB +3.4bp to 5.627%.

Poland’s March 2026 industrial production numbers were a mixed bag, with output declining in a majority of product categories over Q1, highlighting ongoing weakness in industrial activity. Production fell across sectors including energy, metals, machinery and consumer goods such as clothing and furniture, indicating broad-based contraction trends. However, selected areas recorded strong gains, particularly food products, chemicals, plastics and transport equipment, demonstrating pockets of resilience. Overall, despite increases in some product groups, the balance of evidence points to a fragmented industrial environment, where widespread declines are outweighing gains, suggesting uneven momentum across Poland’s manufacturing sector.

The Polish labor market continued to soften in March. Average employment in the enterprise sector declined by 0.9% y/y to 6.389 million, while registered unemployment rose y/y and remained broadly stable m/m. The number of people registered unemployed reached 949.8k at the end of March, with the unemployment rate at 6.1%, unchanged from February but 0.7 percentage points higher than a year earlier. Inflows to unemployment shrank y/y, while outflows also fell, although more people exited due to finding jobs. By region, unemployment rates varied widely; structurally, the majority of unemployed people lacked benefit entitlement, highlighting persistent labor market imbalances despite modest hiring resilience.

The Hungarian labor market weakened slightly in March, with employment at 4.646 million and the unemployment rate at 4.5%, while broader quarterly data indicated a softening trend. In the January-March period, average employment fell 65k y/y, reflecting reductions across both men and women, alongside a fall in the working-age population. The employment rate eased to 74.8%, while domestic primary labor market employment also decreased. Unemployment averaged around 226k with a rate near 4.7%, and job search duration remained elevated at over one year on average. Despite this, the number of registered jobseekers declined slightly, suggesting some administrative improvement even as underlying labor conditions softened. Budapest SI -0.36% to 134307, EURHUF -0.039% to 366.73, 10y HGB +18bp to 6.1%.

Czechia’s economic sentiment indicator edged down to 101.3 in April, a m/m fall of 0.8 points, reflecting a divergence between stable business sentiment and weaker consumer confidence. Business confidence remained broadly unchanged at 100.4, with gains in services and construction offset by declines in trade and industry, indicating mixed dynamics across sectors. In contrast, consumer confidence fell sharply by 4.4 points to 106.0, driven by a rising share of households expecting a deterioration in the economic outlook over the next 12 months. Expectations for improvements in personal financial conditions also weakened, while views on current financial situations and intentions to make major purchases showed little change, pointing to cautious household behavior. Prague SE -0.83% to 2609, EURCZK +0.037% to 24.372, 10y CZGB +7.1bp to 4.801%.

Japan’s national Consumer Price Index (CPI) for March rose 1.5% y/y, up from 1.3% in February, with a 0.4% m/m increase (seasonally adjusted) vs. -0.2% m/m in February. CPI excluding fresh food rose 1.8% y/y (February: 1.6%) and 0.6% m/m, while CPI excluding fresh food and energy was up 2.4% y/y (February: 2.5%) and 0.2% m/m (February: 0.1% m/m). Food prices increased by 3.6% y/y but decreased by 0.3% m/m, while fresh food prices fell 4.8% y/y and 3.2% m/m. Energy prices dropped 5.7% y/y but rose 3.9% m/m, with gasoline down 14.9% y/y. Transportation and communication costs increased by 2.1% y/y. Overall, inflation showed moderate y/y growth with mixed monthly movements across key components. The 2025 fiscal year average CPI rose 2.6% y/y. Nikkei +0.97% to 59716, USDJPY +0.019% to 159.74, 10y JGB +1bp to 2.439%.

Japan’s Services Producer Price Index (SPPI) for March was up 3.1% y/y (February: 2.7%) and 1.2% m/m (February: 0.1% m/m). Excluding international transportation, the SPPI increased by 1.0% m/m, 2.8% y/y (February: 0.1% m/m, 2.7% y/y). Key contributors to the y/y increase included ocean freight transportation (+42.1% y/y), hotels (+10.5% y/y) and leasing services (+3.3% y/y). Subtractors were civil engineering and architectural services (5.2% y/y) and television and radio advertising (5.4% y/y). The rise reflects broad-based price pressures across the transportation, leasing and service sectors, signaling ongoing inflationary trends in Japan’s service industry.

Japan’s national department store sales rose 3.2% y/y in March, up from 1.6% in February. Key segment increases included sundries and cosmetics (+6.9% y/y), accessories (+4.8% y/y) and household goods (+2.6% y/y). Clothing sales grew modestly (+1.4% y/y), while food sales edged up 0.7% y/y. In Tokyo, department store sales rose 4.7% y/y in March, accelerating from 3.0% in February, with substantial gains in clothing (+4.4% y/y) and sundries/cosmetics (+7.4% y/y).

Singapore’s Q1 real estate data showed a 0.9% rise in private residential property prices (0.6% in Q4 2025), with non-landed properties up 1.3% and landed properties down 0.4%. Rents edged up 0.3%, after falling previously. Developers launched 1,844 units and sold 2,013, both down from the previous quarter. Resale transactions accounted for 59.6% of sales. About 55,800 private residential units are expected to be completed in the coming years, with a 6.2% vacancy rate. Office prices rose by 0.2% and retail prices by 2.2%, while office and retail rents dipped slightly. STI -0.24% to 4932, USDSGD -0.055% to 1.2777, 10y SGB +2.7bp to 2.101%.

Thai exports, measured in USD, reached a record $35.2bn in March, up 18.7% y/y in a 21st consecutive month of growth. This was driven primarily by strong demand for electronics and electrical goods linked to AI and data center expansion. In Q1, exports rose by 17.6%, although imports remained higher, resulting in a trade deficit of $3.3bn in March and $9.5bn over the quarter. Industrial exports grew robustly, by more than 21%, led by computers, telecommunications equipment and machinery, while agricultural exports showed mixed performance, with strong gains in fruits and processed foods offset by falls for rubber and seafood. Export growth was broad-based across major markets, particularly the U.S., the EU and ASEAN, though contractions were seen in China and the Middle East amid geopolitical disruptions. SET -0.32% to 1457, USDTHB +0.037% to 32.45, 10y TGN +3.8bp to 2.137%.

The Taiwan Institute of Economic Research has revised its 2026 economic growth forecast up to 7.56%, a 3.51-percentage-point increase from January, driven by strong AI demand boosting semiconductor and ICT capital expenditure and private investment. Rising raw material prices and early stockpiling also lifted exports and orders. Despite ongoing Middle East tensions and uncertain energy supplies, Taiwan’s manufacturing exports, production and orders grew significantly in March. The service sector remains stable, supported by finance and tourism, while construction and real estate face challenges. Global growth risks and geopolitical issues may impact Taiwan’s export and domestic demand outlook, warranting cautious monitoring. TAIEX +3.23% to 38932, USDTWD -0.219% to 31.504, 10y TGB +0.1bp to 1.485%.

Taiwanese central bank member Zhang Jianyi has stated that Taiwan will consider tightening monetary policy only if the Middle East conflict lasts over 150 days, causing oil prices to surge beyond the state oil company’s absorption capacity and government subsidies. This would lead to higher consumer prices being reflected in the CPI. Currently, Taiwan’s CPI impact from oil prices remains manageable thanks to subsidies, and with economic growth ongoing, no rate changes are planned. The Taiwan Institute of Economic Research estimates that with subsidies, 2026 inflation will stay below 2%, but a prolonged conflict risks 1970s-style stagflation.