Market Movers: Reshuffling

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 7 minutes

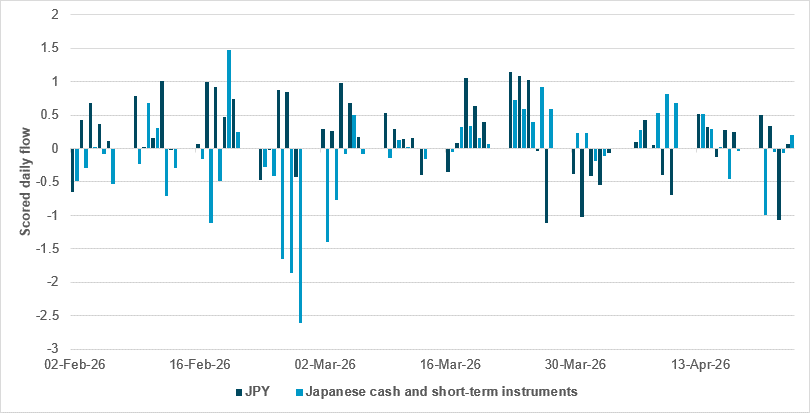

Liquidity preference in JPY and Japanese cash and short-term securities softens pre-BoJ meeting

Source: BNY

The BoJ is once again caught between a rock and a hard place. As at most central banks, there is a strong aversion to hiking at a very difficult point in the cycle, even as balance-of-payments stress is growing.

For most of the past two months, JPY has been well-bid on our figures. For large parts of the first few weeks of the war, it enjoyed a strong liquidity preference and saw significant surge flows. Indeed, several days of purchases with flow scores above 1.0 score helped push holdings into a rare situation for a low-yielder of being strongly overheld. This is not intrinsically different to JPY’s holdings situation before the war began, when the market was already partial to the currency on valuation grounds; risk aversion then helped to sustain additional inflows, even though the nature of the shock would not typically favor funders.

More recently, these concerns have come to the forefront. JPY performance has weakened since the end of March, as strong outflow days have emerged and inflows have softened in magnitude. Another sign of JPY’s safe haven status is that throughout the second half of March and until recently, cash and short-term JPY instruments (CAST) continued to see consistent inflows – albeit modest and insufficient to offset the heavy selling during the first week of the war. This likely reflects some liquidity management, as investors take advantage of front-end JPY yields and cheap valuations, alongside rotation out of equities or long-dated bonds into cash rather than outright outflows. Overall, better liquidity preference should help the currency avoid significant downside risk, but based on current flow averages, the lack of strong inflows also means there is little flow support to drive JPY higher.

Record-high equity markets are holding despite higher oil prices. U.S. futures are mixed, the dollar is softer and bonds are weaker, with the focus on central bank decisions, big tech earnings and the stalled U.S.-Iran peace talks. Today starts significant front-end bond supply tests for the U.S. markets as we head into month-end. The reshuffling of risks in month-end portfolio allocations highlights the ongoing tensions between safe haven demand and the desire to put money to work as energy shortage fears rise.

Bottom line: Trading today is dominated by the lack of big news over the weekend and the wait for central bank decisions, starting with the BoJ tomorrow. The focus on geopolitical risks remains front and center, but today’s earnings releases and bond sales will be important events to watch. The view that the Fed chair nominee Kevin Warsh will be able to move through the confirmation process has not provided any new relief, so front-end rates will be watching the inflation and growth data. USD and oil continue to lead as the key cards in the deck, which looks ready for a fresh reshuffle once the Fed and others provide their guidance on how to look through the global energy supply shock.

U.S. Senator Thom Tillis has backed Kevin Warsh for Federal Reserve chair, removing the final obstacle to confirming President Trump’s nominee before Jerome Powell’s term expires on May 15. Tillis had delayed support for months due to a Department of Justice investigation into Powell but reversed his position after receiving assurances that the probe had been fully closed and would not be reopened without a formal referral. This shift clears the path for a Senate Banking Committee vote, likely to be closely followed by confirmation. The development reduces uncertainty around the Fed’s leadership succession and underscores how legal and political dynamics have influenced the timing of the appointment process. S&P Mini -0.07% to 7190, DXY -0.061% to 98.473, 10y UST +1.9bp to 4.32%.

Acting via Pakistani mediators, Iran has proposed a deal to the U.S. that prioritizes reopening the Strait of Hormuz and ending the war, postponing nuclear talks to a later stage. This aims to bypass internal Iranian disagreements on nuclear concessions. The U.S. blockade would be lifted first, but that could reduce U.S. leverage over Iran’s uranium stockpile and enrichment suspension, which are key objectives for the Trump administration. President Trump is planning a situation room meeting to discuss the stalled negotiations and next steps. Iranian Foreign Minister Abbas Araghchi has held talks in Pakistan and Oman, with further discussions expected in Moscow. The U.S. has yet to respond to the proposal. Brent +2.08% to 107.52, WTI +1.844% to 96.14, Omani crude -1.644% to 105.32, Dubai crude -0.057% to 105.992.

U.S. sanctions against a large private refiner in China have escalated pressure on the country’s petrochemical sector. Washington blacklisted the firm over alleged ties to Iran, marking a significant broadening of enforcement beyond smaller operators. The move is seen as strategically timed ahead of high-level U.S.-China engagement and reflects efforts to curb Iranian oil revenues, with potential geopolitical signaling. The targeted refiner, a major supplier of petrochemicals and key inputs such as purified terephthalic acid, plays a central role in regional supply chains, meaning disruptions are expected to ripple across East Asia. Early signs include canceled orders and concerns over supply shortages, which could drive input costs and inflation up, while also creating opportunities for competing producers in the region.

China’s commerce ministry has criticized the EU for its proposed Industrial Accelerator Act. It formally submitted comments on April 24 outlining strong concerns over what it views as discriminatory provisions against foreign investors. The ministry argues that the legislation imposes restrictive requirements in key sectors such as batteries, electric vehicles, photovoltaics and critical raw materials, while embedding exclusionary “EU origin” clauses in public procurement and support policies. It contends that these measures violate core World Trade Organization principles, including most favored nation and national treatment rules, and could undermine fair competition and investor confidence. Beijing also warned that the act could hinder the EU’s green transition and disrupt multilateral trade norms, urging revisions and signaling potential countermeasures if Chinese firms are adversely affected. Euro Stoxx 50 -0.19% to 5883, EURUSD +0.06% to 1.1729, BBG AGG Euro Government High Grade EUR 0bp to 3.258%.

Bangko Sentral ng Pilipinas governor Eli Remolona has been named in a legal complaint filed by the spouse of Vice President Sara Duterte. This intensifies existing political and institutional tensions over the disclosure of bank records during a congressional impeachment probe. The complaint alleges violations of banking secrecy, anti-money laundering and data privacy laws, arguing that confidential financial information was released publicly without consent during a televised hearing. Authorities maintain that the disclosures were made under subpoena as part of legislative scrutiny into the vice president’s finances, reflecting a deepening rift within the political leadership. The case underscores escalating legal risks for institutions and could raise concerns over governance standards, regulatory independence and the handling of sensitive financial data in the Philippines. PSEi -0.71% to 5901, USDPHP +0.051% to 60.76, 10y PHGB +0.7bp to 6.706%.

U.S. April Dallas Fed manufacturing activity forecast to rise to 0.4 vs. -0.2.

Canada April Bloomberg Nanos Confidence is expected at 47 vs. 47.2.

Central bank speakers: Fed enters external communications blackout; ECB in pre-rate decision quiet period.

U.S. Treasury sells $77bn in 26-week bills, $89bn in 13-week bills, $69bn in 2y notes and $70bn in 5y notes.

Mood: iFlow Mood has eased to 0.179 from recent highs, driven by renewed demand for core sovereign bonds, while equity inflows remain intact.

FX: LatAm FX has shifted to outflows after a prolonged inflow period but remains the most overheld region. The G10 and APAC FX saw broad inflows, with light selling in USD, NOK, AUD, CNY and SGD. EMEA FX was generally sold.

FI: Australian government bonds saw substantial outflows, contrasting with strong demand for Eurozone sovereigns and U.K. gilts. Elsewhere, flows were mixed, with modest inflows into Chinese and Mexican government bonds.

Equities: Inflows were concentrated in Chinese and LatAm equities, while flows elsewhere were mixed and generally light. U.S., Eurozone, U.K., South Korean and Taiwanese equities saw outflows.

“If the cards are stacked against you, reshuffle the deck.” – John D. MacDonald

“Shuffling is the only thing which Nature cannot undo.” – Arthur Eddington

Euro area firms reported tighter financing conditions in Q1 2026, as the ECB SAFE survey showed rising bank loan interest rates and higher non-interest costs alongside slightly weaker credit availability. Financing demand remained broadly stable, leaving the loan financing gap still positive but marginally narrower. Firms continued to cite the economic outlook as the main constraint, although banks’ willingness to lend improved slightly. Corporate performance was mixed, with flat turnover and weaker profits, but future turnover and investment expectations strengthened. Price pressures intensified, with firms expecting higher selling prices and input costs, partly linked to the Middle East conflict, while wage expectations moderated. Short-term inflation expectations rose substantially, while medium-term expectations remained stable.

Germany’s consumer climate for May deteriorated sharply, with the GfK headline indicator falling to -33.3 from -28.1 in April. This marks a 5.2-point decline and the weakest reading since February 2023. The downturn was driven primarily by income expectations tumbling 18.1 points to -24.4 amid rising inflation concerns linked to higher energy prices. Willingness to buy also weakened to a two-year low of -14.4, while the savings indicator eased slightly but remained elevated at 16.1, signaling continued precautionary behavior. Economic expectations deteriorated further to -13.7, reflecting concerns that geopolitical tensions, particularly the Iran conflict, could derail Germany’s fragile recovery outlook. DAX -0.11% to 24129, EURUSD +0.06% to 1.1729, 10y Bund +2bp to 3.014%.

Norway’s household and corporate credit growth softened in March. Total domestic debt rose 4.4% y/y, down 0.2 percentage points from February, bringing outstanding debt to NOK 7,898bn. The slowdown was primarily driven by non-financial corporations, where debt growth eased to 3.7% from 4.1%, remaining below other sectors. Household debt growth held steady at 4.7%, while municipal debt growth edged up to 5.1% from 4.9%, still relatively high by the standards of recent years. Net borrowing data suggest loan demand has been influenced by factors beyond interest rates alone, with recent increases in borrowing occurring despite limited changes in policy rates, indicating broader drivers of credit dynamics. OSE -0.48% to 1994, EURNOK -0.084% to 10.9044, 10y NGB +1.5bp to 4.396%.

Japan’s Economic Trend Index (CI) for February shows the leading index at 113.3 (up from 112.0 in January), indicating continued economic momentum. The coincident index declined to 116.3 from 118.1, suggesting a pause in current economic activity. The lagging index rose slightly to 113.1 from 112.2. Key contributors to the leading index included a strong rally in real machinery orders (+30.3% m/m) and improved consumer sentiment (+2.1 points). However, new job offers fell by 5.8% m/m, weighing on the index. The overall assessment indicates that the coincident index has stabilized, signaling a halt in the economic decline. A y/y rise in the leading indicator suggests upside for GDP growth. Nikkei +1.38% to 60537, USDJPY -0.069% to 159.27, 10y JGB +3.5bp to 2.474%.

Japanese Prime Minister Sanae Takaichi has ruled out an immediate supplementary budget despite mounting calls for one, given the impact of the Middle East conflict on oil prices and supply. She stressed that the government would act flexibly depending on the degree of economic damage but rejected measures to curb economic activity. The government is currently deploying about ¥2tn ($12.55bn) in fuel subsidies but may exhaust funds by July if the crisis persists. Takaichi is supportive of including all spending in annual budgets, avoiding extra budgets.

Japan is planning to tighten the rules on shareholder proposals amid rising corporate pushback against activist investors. Lawmakers and business groups argue that current thresholds are too low, enabling what they see as abusive proposals that distract companies from long-term growth. Proposed changes include raising the minimum shareholding required to submit proposals from 300 units to at least 1% of voting rights, with further increases under discussion. Activist proposals affected a record 52 companies in June 2025, from 46 the previous year. The justice ministry will seek public input before submitting legislation next year. Some investors warn this may hinder corporate reform efforts.

Chinese industrial enterprises above designated size saw profits rise 15.5% y/y in Q1, accelerating from January-February. Equipment manufacturing profits grew 21.0%, driven by electronics (+124.5%) and rail/ship/aerospace (+16.7%). High-tech manufacturing profits surged 47.4%, led by AI, semiconductors and green manufacturing sectors. Raw materials manufacturing profits increased by 77.9%, with large gains in non-ferrous metals (+116.7%) and chemical industries (+54.5%). Operating revenue rose 5.0% y/y, with profit margins at 5.11% – the highest since 2023. Despite these improvements, challenges from external uncertainties and domestic supply/demand imbalances persist. CSI 300 0% to 4769, USDCNY -0.053% to 6.8284, 10y CGB +1.2bp to 1.77%.

The People’s Bank of China (PBoC) is set to withdraw a net ¥200bn via its one-year medium-term lending facility (MLF) in April, in the first net withdrawal since February 2025. This move aims to rebalance liquidity by reducing medium to long-term funds while maintaining short-term funding through open-market operations. The net drain follows similar withdrawals in three-month and six-month reverse repos, with outright reverse repo withdrawals rising to ¥400bn in April from ¥300bn in March. Despite these actions, low interbank funding costs reflect weak credit demand rather than proactive tightening.

Singapore’s manufacturing output expanded strongly in March, rising 10.1% y/y, or 13.5% excluding biomedical manufacturing. Seasonally adjusted output increased by 4.7% m/m. Growth was broad-based across most clusters, led by electronics, which surged 30.0% on robust semiconductor and AI-related demand, alongside solid gains in precision engineering at 14.0% and general manufacturing at 7.6%. Transport engineering posted modest growth of 2.0%, supported by aerospace activity. However, biomedical manufacturing contracted by 14.3% due to weaker medical device demand, while chemicals declined by 16.0% on feedstock disruptions, highlighting divergence across sectors despite the strong overall industrial performance. STI -0.61% to 4893, USDSGD -0.071% to 1.2744, 10y SGB +1.7bp to 2.117%.

Taipei City’s residential price index declined for the fourth consecutive quarter in Q4 2025, falling 0.02% q/q to 126.88 and 2.93% y/y (Q4 2024: 130.71). The average pre-sale housing price edged down by 0.28% q/q to NT$1.2560mn per ping, with the transaction volume up 65.42% q/q to 1,196 units. The rental market strengthened, with the rent index rising 1.42% q/q and 5.28% y/y. Despite strong economic fundamentals, credit controls are continuing to suppress investment momentum. The market shows signs of stabilization with price stability and reduced transaction volume, while policy easing may support a gradual recovery. TAIEX +1.76% to 39617, USDTWD -0.327% to 31.401, 10y TGB +1.2bp to 1.491%.

Taiwan’s overall business monitoring indicator fell by 2 points to 39 in March, remaining in the “red” alert or “boom” zone. The trend-adjusted leading index fell 0.14% to 102.58, in a second consecutive month of decline. Meanwhile, the coincident index rose 1.77% to 109.26, continuing a seven-month upward trend. The lagging index decreased by 0.12% to 98.18, in a fifth successive fall. The government will maintain close surveillance of the economic situation amid these mixed signals.