Market Movers: Old Worries, New Hopes

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 7 minutes

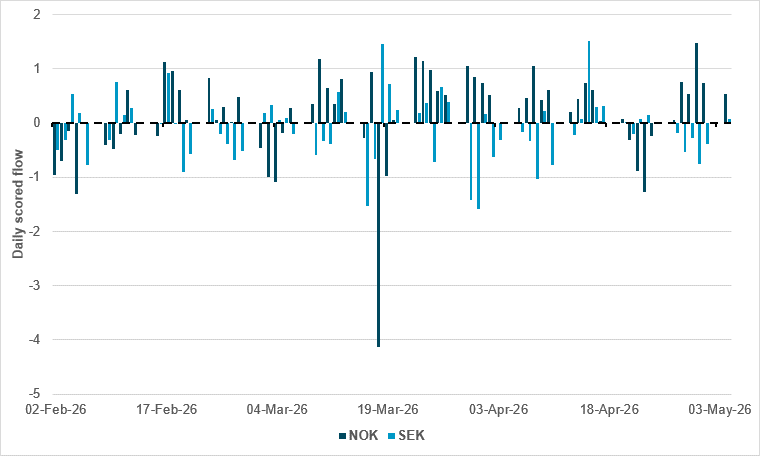

NOK and SEK flows largely divergent

Source: BNY

A hike by either Norges Bank or the Riksbank tomorrow would come as a major surprise. For now, the ECB is the only Western European central bank clearly on course to tighten, and the market appears to believe that policy gaps between the ECB and peers cannot widen significantly. We disagree with this stance, and Norges Bank is probably the best example of applying idiosyncratic risk first by focusing on the path of domestic wages.

NOK is currently one of the best-bought currencies in iFlow, and the rolling three-month average since the beginning of February is running at 0.10. The country is widely expected to benefit from the conflict, and the interest shows. The strength of flow and easing in financial conditions associated with such interest may have even bought Norges Bank some time, even though it has already affirmed a need for a hike. If markets take the view that inhibiting hikes due to softer demand is the right way forward, the EUR may weaken on a relative-value basis against peers and greatly reduce pass-through risk. This was probably going to happen anyway if an early ECB move exacerbated demand weakness and helped regional peers – especially those with fiscal resources in the Nordics – outperform in growth.

However, none of this is new news, and it could prove more challenging for NOK to maintain its current flow momentum. In contrast, SEK has been lackluster. Sweden may have much more diversified primary energy exposure, but the growth risks were always going to be high. Meanwhile, the inflation response to the current supply shock has not materially pushed up CPI or CPI-F figures, as borne out by the CPI release overnight. There is perhaps a stronger balance of payments or even growth premium for Sweden due to sticky exports and fiscal strength, but there is clearly no energy-related “re-rating” as seen in NOK. Current flow momentum is close to flat, but this means that the path is clear for a large move in the event of a policy surprise.

Investors have embraced the new hopes from AI and a path toward a U.S./Iran deal. They are also clinging to the old worries about zero-sum games in AI and employment, and ongoing supply shocks leave inflation and deficits a problem for bonds. Technology shares have extended the global rally in equities, with AI investments seen as driving the growth. Risk sentiment is further supported by a muted market response to renewed Iran tensions alongside diplomatic efforts, as Axios reports that the U.S. and Iran are closing in on a 14-point memorandum of understanding. USD is lower on another apparent round of Japanese intervention, and oil is down 5% on hopes that the Strait of Hormuz will open to traffic again.

AI chip normalization, stock rotations: Nvidia may continue to lead within AI semiconductors, but Samsung and AMD shares reflect the ongoing universal demand for chips. One driver is the ongoing push for AI productivity, and that leads to further watching of jobs and companies on the front lines of replacement fear. Anthropic has announced a new model for financial work providing pitch books, valuation models and more, adding to the pressure on S&P, FactSet and Morningstar. Expect ongoing rotation pressures in AI baskets against companies vulnerable to software. Jobs losses are seen as a key barometer for sector pressures.

Oil supply and volatility: WTI is down 6.2%, trading back at $95/barrel, while the end-of-year December contract is trading 4% lower at $78.45. The API weekly US crude inventory showed a 8.0mb draw in oil, a 6.1mb drop in gasoline and a 4.6mb fall in distillates. Gasoline is now 2% below the five-year average supply, while distillates are 11% below. This is despite the SPR draw, which put reserves at November 2024 lows of 392.7mb. There is 320mb of storage capacity for the SPR. Overnight, Australia’s government committed to a new fuel SPR providing 50 days of supply for future shocks. Key measures to watch for oil as a risk barometer will be the forward curve and normalization back to $65/barrel.

Bonds and global imbalances: The worst fears concerning energy shocks are over, and bonds from the U.K. to Japan and the U.S. reflect that. The pressure of volatility and intervention in JPY leave some doubt about Japanese Prime Minister Sanae Takaichi’s plans for a “responsible extra budget.” Meanwhile the U.K. awaits tomorrow’s local elections, as the fate of the government hangs in the balance. In the U.S., the Trump/Xi talks will highlight the pressure of trade and global imbalances. The U.S. Treasury’s quarterly funding plans will highlight the deficit spending and the 7.5% of GDP budget gap pressure on rates.

Bottom line: Expectations of a path toward peace are high, meaning any headline disproving that will be taken badly. Markets are focused on the AI vs. energy story, but the return of putting money to work has left correlations in bonds and stock positive. This will not last, as risk parity programs require diverse correlations to work in the long run. Investors have been content to look through the current geopolitical risks, and seeing rewards, earnings and stronger data have helped that narrative. Nevertheless, the day ahead may still be about the conflict, volatility and rates.

The Japanese yen surged to a two-month high overnight, strengthening by as much as 1.8% to 155.04 per dollar before partially reversing, prompting market speculation about renewed official intervention by Japanese authorities. The move follows a late April episode in which authorities reportedly entered the market for the first time since 2024, with estimates suggesting around $34.5bn was deployed to support the currency. Although officials have not confirmed any action, the price dynamics are widely interpreted as consistent with intervention, aimed at preventing a move toward 160 per dollar and discouraging speculative positioning against the yen. This highlights ongoing sensitivity around exchange rate stability. Nikkei +0.38% to 59513, USDJPY +0.761% to 156.43, 10y JGB 0bp to 2.518%.

The U.S. and Iran are nearing a potential preliminary agreement to end hostilities and establish a framework for nuclear negotiations. Discussions are focused on a one-page memorandum of understanding that could mark the closest progress since the conflict began. The proposed deal would include a temporary halt to Iran’s uranium enrichment, phased U.S. sanctions relief and a gradual reopening of the Strait of Hormuz, alongside a 30-day window for negotiating a more detailed agreement. Key sticking points remain, particularly over the duration of enrichment limits and verification measures, while uncertainty persists given divisions within Iran’s leadership and skepticism among U.S. officials about whether a final agreement can be secured. Brent -3.405% to 106.13, WTI -3.736% to 98.45, Omani crude -2.687% to 103.25, Dubai crude -2.237% to 104.537.

China has hosted Iran’s Foreign Minister Abbas Araghchi for the first time since the U.S.-Israel war on Tehran, just days before President Trump’s visit to Beijing. Chinese diplomat Wang Yi met Araghchi to discuss bilateral relations and regional issues. The visit signals Tehran and Beijing aligning interests ahead of the Trump-Xi summit. China is seeking stability in the Persian Gulf to protect trade and energy flows, urging free passage through the Strait of Hormuz. Iran is aiming to secure assurances on oil, finance and diplomatic support, while China may push Iran to ease threats to Gulf shipping. CSI 300 +1.44% to 4876, USDCNY +0.159% to 6.8173, 10y CGB +0.9bp to 1.761%.

French President Emmanuel Macron has nominated his former chief of staff Emmanuel Moulin as governor of the Bank of France. The move underscores efforts to secure influence over key institutions ahead of the 2027 presidential election amid rising support for opposition parties. Moulin, an experienced civil servant who has led the Treasury and held senior finance ministry roles, would also sit on the European Central Bank governing council, giving him influence over euro area monetary policy. The nomination has sparked criticism from opposition figures over risks to institutional independence given his close ties to the executive, although parliamentary rejection remains unlikely given the high threshold required. CAC 40 +1.61% to 8192, EURUSD +0.488% to 1.175, 10y OAT -5.8bp to 3.654%.

Polish central bank base rate announcement: expected to hold at 3.8%.

U.S. April ADP employment change forecast to rise to 120k vs. 62k.

U.S. Treasury quarterly refunding announcement – focus on coupon issuance.

U.S. Treasury sells $69bn in 17-week bills.

Central bank speakers: The Fed’s Alberto Musalem speaks at the Mississippi Bankers Association. The Fed’s Austan Goolsbee speaks at a panel event. The Governor of the Bank of Canada, Tiff Macklem, will appear before the Standing Senate Committee on Banking, Commerce and the Economy.

Mood: iFlow is close to neutral (0.007), with broadly balanced buying across global equities and core government bonds.

FX: Modest selling pressure overall. Outflows were most notable in COP, MXN and AUD, while HUF, NOK, GBP and INR saw the strongest inflows.

FI: Moderate demand for government bonds, led by U.K. gilts and Eurozone and Canadian sovereigns. Light selling was observed in Chilean and Colombian government bonds.

Equities: U.S. equities attracted inflows, contrasting with broad outflows across G10 markets. Elsewhere, selling was concentrated in Hungary, South Korea, Hong Kong and Taiwan. In EM APAC, the IT and industrials sectors led outflows, while consumer staples, healthcare and energy saw buying.

“Worry does not empty tomorrow of its sorrow; it empties today of its strength.” – Corrie ten Boom

“Although no one can go back and make a brand new start, anyone can start from now and make a brand new ending.” – Carl Bard

Eurozone composite PMI for April fell to 48.8 points from 50.7 in March, marking a 17-month low and signaling a return to contraction for the first time in almost one-and-a-half years, while the services PMI declined to 47.6, its weakest level in 62 months. The downturn was driven by a sharp deterioration in services activity, which more than offset continued resilience in manufacturing output. Demand weakened further, with new orders falling at the fastest pace since late 2024, while business confidence dropped to multi-year lows amid geopolitical uncertainty. At the same time, inflation pressures intensified, with input costs rising to a 40-month high and output prices increasing at the fastest rate in three years, reinforcing stagflation risks. Euro Stoxx 50 +1.46% to 5956, EURUSD +0.488% to 1.175, BBG AGG Euro Government High Grade EUR -0.4bp to 3.35%.

The ECB wage tracker shows broadly stable dynamics for Eurozone negotiated wage growth data in 2026, with forward-looking growth around 2.6% by year-end and largely unrevised from the previous release. The headline tracker with smoothed one-off payments shows wage growth easing from 3.2% in 2025 to 2.3% in 2026, while measures excluding one-off payments point to moderation from 3.8% to 2.6%. Quarterly profiles suggest a gradual rise throughout 2026 as base effects from earlier one-off payments fade, though overall volatility remains lower than in prior years. The data indicate a normalization in wage pressures, with negotiated pay growth stabilizing at more moderate levels despite ongoing economic uncertainty.

Eurozone industrial producer prices rose sharply in March (+3.4% m/m), reversing a 0.6% decline in February, while annual growth reached 2.1%, indicating a renewed pickup in pipeline inflation pressures. The increase was driven predominantly by energy prices, which surged 11.1% on the month, while other components such as intermediate goods, capital goods and consumer goods recorded more modest gains. Excluding energy, producer prices rose by 0.5%, suggesting underlying price pressures remain contained. Across member states, price dynamics were uneven, with strong increases in countries such as Lithuania, Spain and Italy, while others including Estonia and Finland recorded declines, highlighting significant regional divergence.

Germany’s services PMI fell into contraction territory in April: the business activity index declined to 46.9 from 50.9 in March, in the first contraction in eight months and the sharpest decline since November 2022. The downturn was driven by a pronounced weakening in demand, with new business falling at the fastest pace since January 2024, partly reflecting reduced export orders and heightened uncertainty linked to geopolitical tensions. Firms also reduced headcounts for a fourth consecutive month amid falling backlogs and weaker capacity utilization. At the same time, cost pressures intensified, as input price inflation rose to a three-year high and firms increasingly passed these costs on, lifting output price inflation to a multi-year high, while confidence deteriorated sharply. DAX +1.5% to 24768, EURUSD +0.488% to 1.175, 10y Bund -4.4bp to 3.019%.

France’s manufacturing output increased by 1.2% m/m in March, rebounding from a marginal 0.1% decline in February, while total industrial production rose 1.0% after a sharp prior contraction. The expansion was broad-based across sectors, with sizable gains in transport equipment, and electrical and electronic goods, along with a strong surge in refined petroleum products, indicating a cyclical recovery in industrial activity. On a q/q basis, manufacturing output was 1.5% higher y/y, driven by strength in transport equipment, although the food production and energy-related sectors remained weak. In contrast, construction output continued to contract, highlighting uneven momentum across the broader economy. CAC 40 +1.61% to 8192, EURUSD +0.488% to 1.175, 10y OAT -5.8bp to 3.654%.

France’s services PMI for April signaled a deeper contraction, with the business activity index falling to 46.5 points from 48.8 in March. This is the lowest level since February 2025, extending the downturn to four consecutive months. The decline was driven by a sharp deterioration in demand, with new orders falling at the fastest pace in nearly two-and-a-half years amid client caution, cost pressures and geopolitical uncertainty. Despite a surge in input cost inflation to a 29-month high, firms enjoyed only a limited ability to raise output prices due to weak demand conditions. Employment increased only marginally, while business confidence weakened. The composite PMI also fell to 47.6, indicating the fastest decline in overall private sector activity in over a year.

Italy’s services PMI for April 2026 indicated near-stabilization, with the business activity index rising to 49.8 points from 48.8 in March, remaining just below the 50-point threshold and signaling marginal contraction. The sector saw only slight growth in new business, constrained by a sharp decline in export demand and broader uncertainty linked to geopolitical tensions, which weighed on client confidence and spending. Cost pressures intensified further, driven by higher energy, fuel and wage inputs, while firms were less able to pass these onto customers, leading to softer charge inflation and margin compression. The composite PMI edged up to 50.5, reflecting modest overall output growth led by manufacturing rather than services. FTSE MIB +1.31% to 49192, EURUSD +0.488% to 1.175, 10y BTP -7.7bp to 3.785%.

Spain’s services PMI for April 2026 fell into contraction territory, with the business activity index declining to 47.9 from 53.3 in March, marking the first sub-50 reading since August 2023 and the weakest since early 2022. The downturn was driven by a sharp fall in new business amid weakened demand and confidence linked to geopolitical uncertainty, particularly the Middle East conflict. Cost pressures remained elevated due to higher energy, supplier and wage costs, although firms continued to pass these on to customers. The composite PMI also dropped to 48.7 points from 52.4, signaling a broader slowdown, even as manufacturing activity remained relatively resilient. IBEX 35 +1.62% to 17931, EURUSD +0.488% to 1.175, 10y Bono -6bp to 3.454%.

Dutch household consumption rose by 0.9% y/y in March, following declines in the previous two months. Spending on durable goods increased by 4.7%, driven by passenger cars, home furnishings and electrical appliances. Service expenditure grew by 0.4%, supported by transport, communication, medical and housing services, while accommodation, food services and recreation declined. Food, beverage and tobacco spending fell by 0.5%, and other goods, including energy and motor fuels, decreased by 1.4%. Despite this growth, consumption conditions worsened in April due to negative consumer financial outlooks and slower share price gains than in March. AEX +0.83% to 1023, EURUSD +0.488% to 1.175, 10y NGB -4.5bp to 3.14%.

The U.K. services PMI rose to 52.7 points in April from 50.5 in March, signaling a modest rebound in activity but still indicating slower growth compared with earlier in the year. The improvement came despite subdued demand conditions, with new business broadly flat and export sales weakening amid geopolitical tensions and disruption linked to the Middle East conflict. Cost pressures intensified sharply, with input price inflation reaching its highest level since November 2022, driven by fuel and wage increases, which in turn pushed output price inflation to a multi-year high. Employment continued to decline, albeit at a slower pace, while business confidence remained subdued despite a slight uptick. FTSE 100 +1.73% to 10395, GBPUSD +0.54% to 1.3614, 10y gilt -6.5bp to 4.996%.

U.K. labor market data for March showed tentative stabilization, with vacancies rising 3.74% m/m to 752,711. While this was a second consecutive increase, the measure is still down 13.60% y/y and near post-2021 lows. Wage dynamics remained firm, as average advertised salaries increased by 0.55% m/m and 4.93% y/y to £44,031, outpacing inflation, while London salaries surpassed £50,000 for the first time. Labor market slack persisted, with jobseeker competition at 2.29 per vacancy and unemployment at 4.9%. Sector divergence was notable, with strong hiring in teaching but sharp y/y declines in healthcare and logistics, alongside continued weakness in graduate vacancies.

Sweden’s inflation data for April showed a sharp cooling in price pressures, with headline CPI falling to -0.1% y/y from 0.5% in March, while monthly prices declined by 0.6%. Core measures also weakened substantially, as CPIF eased to 0.8% from 1.6% and CPIF excluding energy dropped to 0.0% from 1.1%, both recording m/m contractions of 0.6 percentage points. The decline was driven in part by a significant 5.5% fall in food prices over the month, highlighting volatile components behind the disinflation. Overall, the data point to rapidly softening underlying inflation momentum, reinforcing the view that price pressures are now well-contained. OMX +1.88% to 3130, EURSEK +0.125% to 10.8518, 10y Swedish GB -8.4bp to 2.814%.

Sweden’s services PMI slowed to 52.5 points in April from 55.9 in March, signaling a loss of momentum in the sector, with the three-month average also declining to 52.4 and remaining below the historical norm of 55.6. The moderation was driven primarily by weaker new orders, alongside softer business activity and employment components, indicating a broad-based easing in demand. Composite PMI similarly declined to 53.8 from 56.0, pointing to slower overall private sector growth. Cost pressures intensified, with input price indices rising to 72.1, well above historical averages, partly reflecting supply disruptions. Overall, the data suggest a more fragile recovery, with services facing growing headwinds even as manufacturing continues to expand.

Norwegian house price data for April showed continued strength, with prices rising 1.0% m/m and 0.6% on a seasonally adjusted basis, bringing YTD growth to 5.6%. The average dwelling price reached NOK 5.07mn, with momentum driven by regional markets such as Stavanger, Kristiansand and Bergen, while Oslo lagged with only 2.5% growth so far this year. Transaction activity remained solid but softened slightly, with sales down 2.3% y/y and listings up 8.7%, indicating improving supply conditions. Time to sell decreased marginally to 49 days, suggesting still healthy demand, though regional divergences persist and higher interest rate risks could weigh on future price dynamics. OSE -0.53% to 2023, EURNOK +0.571% to 10.8848, 10y NGB -4.4bp to 4.421%.

Hungary’s industrial production rallied strongly in March, with output rising 6.7% y/y and 3.1% m/m on a seasonally adjusted, working-day-adjusted basis. Working-day-adjusted growth stood at 3.7% y/y, indicating broad-based improvement across the sector. Expansion was driven by key manufacturing segments, notably computer, electronic and optical products, electrical equipment, and food, beverages and tobacco, while transport equipment recorded more modest gains. Despite the robust March performance, Q1 growth was remained relatively subdued at 1.0% compared with the same period in 2025, suggesting the recovery is still uneven but gaining traction. Budapest SI +0.23% to 136252, EURHUF -0.507% to 359.72, 10y HGB +3bp to 6.02%.

Czech preliminary inflation for April showed consumer prices rising by 2.5% y/y, with prices also increasing by 0.5% m/m. The release indicates a moderate inflation pace, suggesting price pressures remain contained but stable relative to recent trends. The figures are based on early data collection methods including field price surveys and administrative sources, with final confirmed data scheduled for mid-May. Overall, the preliminary reading points to a steady inflation environment, with no significant acceleration, consistent with a broadly balanced demand and cost backdrop in the economy. Prague SE +2.32% to 2516, EURCZK -0.132% to 24.355, 10y CZGB -5.4bp to 4.869%

South Africa’s PMI data for April showed business conditions improving modestly, with the headline index rising to 51.6 from 50.8 in March, marking the strongest reading since August 2022. The expansion was driven by a rebound in output and new orders, partly supported by precautionary stock building amid concerns over supply disruptions linked to the Middle East conflict. However, inflationary pressures intensified significantly, with input costs rising at a 30 month high due to higher fuel prices and supplier charges, prompting firms to hike selling prices. Supplier delivery times also lengthened, while employment growth strengthened, indicating firms were responding to improved demand despite elevated cost pressures. JSE TOP 40 +2.22% to 109403, USDZAR -1.46% to 16.4279, 10y SAGB -13bp to 8.845%.

New Zealand’s labor market saw a slight improvement in Q1. The unemployment rate was 5.3% (down from 5.4% in Q4 2025), while the underutilization rate held steady at 12.9%. The seasonally adjusted labor force participation rate was 70.4% (vs. 70.5% in Q4 2025). The employment rate remained at 66.7%. In the year ended March 2026, the Labor Cost Index (LCI) for all salary and wage rates rose 2.0% y/y, with private sector wages up 2.0% and public sector wages up 1.7%. Annual CPI inflation was 3.1% y/y for the same period. Average ordinary time hourly earnings grew 3.1% y/y to $44.12, with private sector earnings up 3.5% to $41.89 and public sector pay 1.5% higher at NZ$52.45. Average weekly earnings for full-time employees rose 3.0% y/y to NZ$1,716. NZX 50 +0.84% to 13145, NZDUSD +1.123% to 0.5947, 10y NZGB +0.9bp to 4.658%.

New Zealand’s Financial Stability Report was released, assessing risks to the country’s financial system from the Middle East conflict. Key impacts include higher oil prices affecting transport, primary sectors and chemical manufacturing, increased global market volatility raising equity and borrowing risks, and heightened cyberattack threats linked to geopolitical tensions and AI adoption. Economic growth recovery is slowing, potentially increasing debt servicing stress. The banking sector remains resilient, with strong capital and funding buffers, while general insurers are maintaining their profitability despite limited direct conflict exposure. Challenges include rising health insurance costs and credit access issues for small businesses. Global fiscal sustainability risks from rising government debt also pose potential financial stability concerns.

China’s general services PMI rose to 52.6 points in April (from 52.1 in March), indicating faster expansion in service sector activity and new business. The 12-month outlook improved, reflecting optimism driven by new projects and market development. Domestic demand remained strong, while new export orders declined slightly for the second month in a row. Employment fell marginally for a third consecutive month amid cost-saving measures. Input prices increased due to higher oil and fuel costs linked to the Middle East conflict, reaching the highest inflation in 2026, although the figure was still modest overall. Average selling prices declined slightly. The composite output index rose to 53.1 (51.5 in March), signaling broad-based growth. CSI 300 +1.44% to 4876, USDCNY +0.159% to 6.8173, 10y CGB +0.9bp to 1.761%.

South Korea’s Consumer Price Index (CPI) rose by 0.5% m/m, 2.6% y/y in April vs. 0.3% m/m, 2.2% y/y in March, the highest y/y headline CPI figure since July 2024. Core inflation, excluding food and energy, increased by 0.3% m/m but steady at 2.2% y/y. Key contributors to the rise included transport (+3.4% m/m, 9.7% y/y), recreation and culture (+1.5% m/m, 3.4% y/y) and furnishings (+0.2% m/m, 1.9% y/y). Food and non-alcoholic beverages declined by -0.8% m/m. Other categories such as housing (+0.2% m/m, 1.7% y/y) and restaurants and hotels (+0.4% m/m, 2.6% y/y) also saw moderate increases, while communication remained unchanged. KOSPI +6.45% to 7385, USDKRW +1.289% to 1455.25, 10y KTB +1.8bp to 3.933%.

Singapore’s private sector PMI rose to 57.9 points in April (56.7 in March), signaling strong economic growth driven by a record surge in new business, mainly from domestic demand. Output growth accelerated, though job cuts occurred for the first time in 2026, increasing backlogs. Input costs remained elevated due to higher fuel prices, with firms passing most costs on to customers, resulting in near-record output price inflation. Purchasing activity hit its highest level since 2012, supported by improved supply chains and inventory buildup. Business confidence reached an all-time high, underpinned by robust new orders and planned marketing efforts. STI +0.08% to 4924, USDSGD +0.37% to 1.2721, 10y SGB +2.4bp to 2.119%.

Hong Kong SAR’s private sector experienced its strongest deterioration in business conditions in ten months in April, with the S&P Global PMI falling to 48.6 from 49.3 in March. Output and new orders fell for a second consecutive month, with output contracting at the fastest pace since June 2025. Rising input costs, driven by raw material price surges linked to the Middle East conflict, pushed input price inflation to its highest level since October 2011. Firms raised selling prices at the fastest rate since August 2023. Employment fell for the first time in three months amid weak demand. Business sentiment remained substantially negative despite slight easing. Hang Seng +1% to 26157, USDHKD +0.008% to 7.8359, 10y HKGB -1.2bp to 1.417%.

Hong Kong retail sales rose 12.8% y/y in March to $33.9bn, with Q1 sales up 12.1% y/y (January-February revised: +11.8%). Online sales surged 35.1% y/y in March, accounting for 9.7% of total sales, with Q1 online sales up 30.1% y/y. The volume of total retail sales increased by 9.8% y/y in March and Q1. Strong growth was seen in motor vehicles (+80.8%), jewelry (+27.2%) and electrical goods (+30.1%), while fuels (-14.2%) and footwear (-10.2%) recorded falls. Seasonally adjusted Q1 retail sales rose 7.8% q/q by value and 5.4% q/q by volume. Growth is supported by recovering demand, inbound tourism and a favorable macro environment.

The Philippine unemployment rate eased to 5.0% in March from 5.1% in February, although this is still above March 2025’s 3.9%. Labor force participation was 63.3%, slightly down from 63.8% in February 2026 but higher than 62.9% a year earlier. The employment rate stood at 95.0%, down from 96.1% in March 2025. The services sector led employment at 63.0%. The underemployment rate was 12.3%, higher than February’s 11.8% but lower than March 2025’s 13.4%. The youth employment rate rose to 87.4%, with a youth underemployment rate of 13.1%. PSEi +1.17% to 5967, USDPHP +0.323% to 61.365, 10y PHGB +10.2bp to 7.141%.

In Q1, the value of production in Philippine agriculture and fisheries declined by 0.3% y/y to PHP 437.52bn. Crop production fell 2.4% y/y to PHP 243.62bn, mainly due to a 6.3% drop in the value of palay. Livestock production rose 5.1% y/y to PHP 60.74bn, supported by a 6.4% increase in hog production. Poultry value expanded 7.1% y/y to PHP 80.83bn, with all poultry commodities increasing. Fisheries production decreased by 6.1% y/y to PHP 52.34bn.

Thailand’s CPI was up 2.89% y/y in April, rebounding from -0.08% in March, driven by a core CPI rate of 0.83% (up from 0.57% in March). Key contributors included food and non-alcoholic beverages (+0.98% y/y), with sizable rises in eggs and milk (+3.18%) and vegetables and fruits (+1.29%). Energy prices surged 18.87% y/y, while transport and communication costs increased by 11.38%. On a m/m basis, CPI jumped 2.75%, led by energy (+17.90%) and transport (+10.13%). Food inflation rose 1.13% m/m. The data reflect broad-based inflationary pressures after several months of subdued or negative inflation. SET +1.2% to 1508, USDTHB +0.879% to 32.43, 10y TGN +4.8bp to 2.229%.

In April, Indian services activity expanded at its fastest pace since November, with the HSBC India Services PMI rising to 58.8 (March: 57.5). Growth was driven by stronger domestic demand, e-commerce and a shift from international to domestic suppliers amid the Middle East conflict, boosting transport services. New export business growth slowed to its weakest reading in over a year due to the war and subdued tourism. Input costs rose at a softer but still high rate, led by food, gas and labor, while output price inflation eased to a three-month low. Employment increased across all service sectors, supported by rising new business. SENSEX -0.09% to 76948, USDINR +0.22% to 95.0825, 10y INGB -3.8bp to 6.98%.

President Prabowo Subianto has endorsed Bank Indonesia’s seven-step plan to stabilize the rupiah amid recent weakness. Key measures include intensified onshore and offshore foreign exchange interventions supported by ample reserves, strengthening capital inflows via rupiah securities and enhanced fiscal and monetary coordination with government bond purchases totaling IDR 123.1tn ($7.6bn) YTD. The central bank has ample liquidity with 14.1% base money growth and is tightening U.S. dollar purchase limits to curb speculation, expanding offshore interventions and strengthening regulatory oversight with the Financial Services Authority to ensure financial stability. JCI +0.37% to 7083, USDIDR +0.069% to 17413, 10y IDGB -5.2bp to 6.765%.

Fitch Ratings has upgraded Argentina’s Long-Term Foreign and Local Currency Issuer Default Rating to “B-” from “CCC+” with a stable outlook, citing improved fiscal and external balances, economic reforms and better FX reserve prospects. Key reforms include labor and environmental law changes and a 2026 budget that maintains fiscal discipline. Argentina’s external position strengthened as a net energy exporter, with a Q1 trade surplus of $5.5bn (up from $1.1bn a year earlier). Inflation remains elevated but is expected to ease to below 2% m/m by year-end. Economic growth is uneven, projected at 3.2% in 2026, with election-related risks ahead in 2027. IBG -0.5% to 115315600, USDARS -0.634% to 1392.8737, 10Y AGB -0.7bp to 8.857%.