Market Movers: Limbo

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 6 minutes

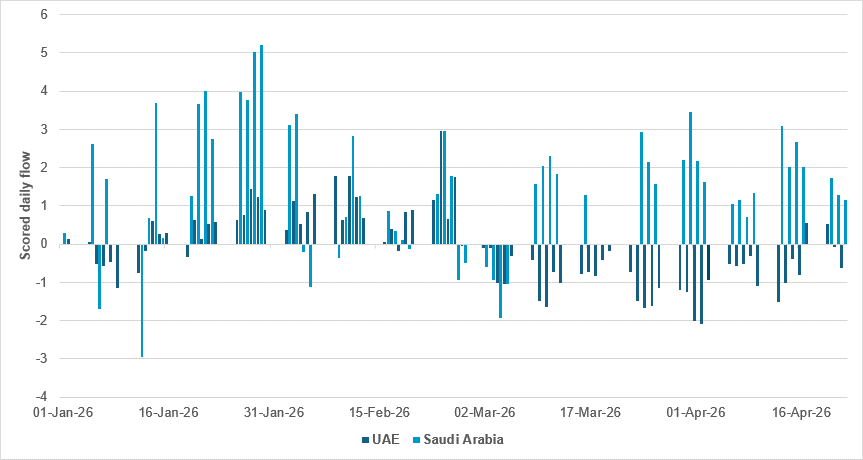

Core MENA equity markets diverge strongly in March

Source: BNY

Frontier markets have had a tough six weeks, sitting at the sharp end of the conflict’s impact. MENA has seen heavy fixed income and equity outflows, while other frontier economies have been hit by balance-of-payments and terms-of-trade shocks. A tentative recovery is emerging as the ceasefire holds, but it remains uneven: MENA FI is continuing to see outflows, while LatAm, Central America and parts of EMEA are attracting inflows, led by oil beneficiaries such as Nigeria.

In equities, divergence within MENA is clear. Saudi Arabia has shown strong resilience, with consistent inflows supporting market stability. Meanwhile the UAE has only recently seen modest buying after sustained outflows, reflecting a more cautious rebound tied closely to conflict developments rather than signs of distress.

The Iran talks are in limbo. The Strait of Hormuz remains mostly shut. The duration of the conflict continues to be the key risk factor for markets as they watch commodity prices and economic data for clues about growth and inflation. Market reactions continue to be led by the conflict, with oil up, stocks down, bond yields higher and USD bid. The flash April global PMI reports are compounding stagflation concerns, while the rate hike by the Philippines’ central bank and ongoing intervention by Indonesia have added to concerns about the effects of the war.

Bottom line: The U.S. session will again focus on earnings and economic growth, with weekly jobless claims and flash PMI important but unlikely to move markets out of limbo. The uncertainty over the duration of the conflict and the implications to supply chains continue to nag at investors. Higher equities and higher bond yields are slowing in play as correlations shift, reflecting the current state of unknowable positioning. In FX, USD is holding onto its gains and showing momentum in EM risk again, with IDR, ZAR and HUF all unwinding. USD is clearly back as a tool for trade, with Swift data showing a 51% jump in March. The implications for risk watchers are that any productive shifts to ending the conflict could drive unwinding not just in oil prices, but also in the dollar.

The head of the International Energy Agency has warned that the world is facing the biggest energy security threat in history, citing severe supply disruptions caused by the Iran conflict and the closure of the Strait of Hormuz. Fatih Birol said around 13 million barrels/day of oil supply have been lost, with the key shipping route effectively under a double blockade, halting flows that previously averaged 20 million barrels daily. The disruption is expected to hit global growth, push up inflation and risk fuel shortages, particularly in Europe where jet fuel supplies could run short within weeks. While emergency stock releases are providing temporary relief, Birol stressed that reopening the strait is essential, urging governments to diversify energy sources and consider demand reduction measures if shortages persist. Brent +1.58% to 103.52, WTI +1.625% to 94.47, Omani crude +2.665% to 104.79, Dubai crude +2.158% to 105.095, HH natural gas -0.441% to 2.71, Dutch TTF natural gas +4.026% to 45.305.

China’s Ministry of Commerce has declared that recent U.S. tariff refunds represent a constructive step toward correcting earlier tariff policies, while reiterating its firm opposition to unilateral tariff actions such as reciprocal and fentanyl-related duties imposed by the U.S. Officials argued that these measures violate international trade rules and U.S. domestic law, while undermining global trade order and broader economic interests. The spokesperson also noted that such tariffs are collected by U.S. customs from importers and ultimately borne by American consumers. Against this backdrop, Chinese authorities urged domestic exporters to actively engage with relevant stakeholders to safeguard their legitimate interests amid ongoing trade tensions. CSI 300 -0.28% to 4786, USDCNY +0.097% to 6.8355, 10y CGB +2.8bp to 1.757%.

Japan’s Prime Minister Sanae Takaichi has sought support from Saudi Arabia to secure additional energy supplies amid concerns over oil disruptions linked to the Iran conflict. She held a call with Crown Prince Mohammed bin Salman, who responded positively to the request. The discussion focused on maintaining crude flows, including via Yanbu Port, and broader risks to supply routes such as the Strait of Hormuz. This is a critical passage for Japan, which sources over 90% of its oil from the Middle East. Takaichi has intensified diplomatic outreach, engaging multiple global leaders to mitigate supply risks, while Mexico has agreed to provide 1 million barrels of crude by July, highlighting Japan’s efforts to diversify its energy sources under tightening geopolitical conditions. Nikkei -0.75% to 59140, USDJPY +0.132% to 159.69, 10y JGB +2.5bp to 2.429%.

The Philippines central bank, BSP, has delivered a 25bp rate hike to 4.50% and retained a clear hawkish bias. The move was primarily driven by a deteriorating inflation outlook. While the BSP framed the hike as pre-emptive policy action to safeguard price stability, it also signaled readiness to take all necessary monetary actions to ensure the CPI target is met, pointing to further tightening that could take place as early as the June policy meeting. The vote was not unanimous. The BSP revised its 2026 and 2027 CPI forecasts up from February’s 3.6% and 3.2%, with average inflation for both years now set to breach the upper end of the 2-4% inflation target range. In March, the BSP had forecast 2026 and 2027 inflation of 5.1% and 3.8%, respectively; in other words, upward inflationary pressure is seen as being higher for longer. PSEi -0.1% to 5984, USDPHP -0.53% to 60.46, 10y PHGB -1.9bp to 6.578%.

U.S. March Chicago Fed National Activity Index forecast at -0.13 vs. -0.11.

U.S. weekly initial jobless claims are expected to rise to 210k vs. 207k.

U.S. April preliminary S&P Global Manufacturing PMI forecast to rise to 52.5 vs. 52.3, while the services PMI is expected to rise to 50.5 vs. 49.8 and the composite PMI is expected to reach 50.6 vs. 50.3.

U.S. April Kansas City Fed manufacturing activity is forecast to ease to 10 points vs. 11.

Canada March industrial product prices are expected to rise to 1.9% m/m vs. 0.4% m/m.

Canada March raw materials price index is expected to rise to 9.4% m/m vs. 0.6% m/m.

Central bank speakers: ECB Governing Council member Joachim Nagel gives a speech on central bank independence.

U.S. Treasury sells $80bn in 4-week bills, $75bn in 8-week bills and $26bn in 5y TIPS.

Mood: Equity demand continues to be firm, while selling in core sovereign bonds has stabilized. iFlow Mood remains in risk-on territory at 0.243.

FX: G10 FX has continued to see strong inflows, with only light outflows in USD and DKK. Flows across LatAm, EMEA and APAC were moderate and mixed, with notable demand for HKD and CLP, offset by outflows in PLN, MXN and CZK.

FI: Demand for Eurozone and Turkish government bonds remains strong, contrasting with substantial selling in Australia and Indonesia. LatAm government bond flows turned to outflows, while EMEA saw a pick-up in demand.

Equities: Broad-based equity buying across LatAm, EMEA and APAC, led by China, Malaysia, Chile and Peru. In the G10, Sweden and Norway saw inflows, while the U.S., Canada and the U.K. experienced light selling. Within EM APAC, industrials and healthcare attracted the strongest inflows, while energy and communication services saw outflows.

“Sometimes limbo is a tolerable place to be stuck.” – William Boyd

“To be in a long-term state of limbo, not knowing the outcome or length of time waiting, is utterly, shatteringly exhausting.” – Tanya Marlow

The Eurozone flash composite PMI for April fell to 48.6 from 50.7 in March, marking a 17-month low and signaling a return to contraction in private sector activity. The downturn was driven primarily by the services sector, where activity declined to a 62-month low. Meanwhile manufacturing output continued to expand, partly supported by inventory building amid supply concerns. New orders contracted for a second consecutive month, reflecting weaker demand conditions. At the same time, inflationary pressures intensified sharply, with both input costs and output prices rising at the fastest pace in over three years, linked to higher energy costs and supply chain disruptions. Business confidence weakened and employment edged lower, pointing to a more fragile outlook. Euro Stoxx 50 -0.48% to 5878, EURUSD -0.06% to 1.1698, BBG AGG Euro Government High Grade EUR +2.7bp to 3.229%.

Germany’s flash composite PMI fell to 48.3 in April from 51.9 in March, which represents a 16-month low and signals a return to contraction in private sector activity. The downturn was driven primarily by a sharp decline in services activity, which dropped to a 41-month low amid weaker demand and heightened uncertainty linked to geopolitical tensions. Manufacturing output remained in expansion but slowed significantly. New business fell at the fastest pace since late 2024, and business confidence turned negative. At the same time, cost pressures intensified, with input price inflation reaching its highest since 2022 and firms raising selling prices at the fastest pace in over three years, highlighting rising inflationary pressures. DAX -0.25% to 24135, EURUSD -0.06% to 1.1698, 10y Bund +2.2bp to 3.03%.

France’s flash composite PMI for April fell to 47.6 from 48.8, marking a 14-month low and indicating a deeper contraction in private sector activity at the start of the second quarter. The decline was driven primarily by the services sector, where activity dropped to a 14-month low amid weaker demand and increased customer caution. Manufacturing provided a partial offset, with output rising to a 50-month high due to advance orders ahead of expected shortages and price increases. Input cost inflation accelerated sharply to a three-year high, particularly in manufacturing, although passthrough to selling prices remained relatively contained. Business confidence weakened further, reflecting elevated uncertainty and concerns over demand. CAC 40 +0.45% to 8193, EURUSD -0.06% to 1.1698, 10y OAT +3bp to 3.688%.

France’s industrial business survey for April indicates that demand conditions weakened in outlook terms despite stronger recent activity. Firms reported improved domestic and foreign demand over the past three months but expect a deterioration in the next quarter. Production constraints intensified, as the share of firms facing capacity bottlenecks rose sharply to 43%, the highest since 2023, while capacity utilization edged up to 81%. Price pressures strengthened, with firms reporting a 0.4% increase in selling prices and anticipating a faster 0.8% rise ahead. Recruitment difficulties eased further, and investment expectations rebounded modestly but remained below average, pointing to cautious sentiment despite ongoing supply constraints.

France’s business climate deteriorated substantially in April, with the headline indicator falling three points to 94, back to its July 2024 level and clearly below its long-run average. The weakening was broad-based across market sectors, with general business expectations worsening everywhere and expected selling prices rising. Retail saw the sharpest drop, services also softened, construction was unchanged at a subdued level and industry improved only slightly. The employment climate was stable at 95, still below normal, suggesting labor market conditions remain soft rather than collapsing. Overall, the survey points to a more fragile growth backdrop, weaker confidence across sectors and persistent pricing pressure despite subdued activity momentum.

France’s industrial business survey for April showed a modest improvement in headline sentiment, with the manufacturing climate indicator rising one point to 100, back at its long-run average. The gain was driven mainly by a rebound in past output and total order books, while foreign order books were steady and finished goods inventories remained elevated. Beneath the headline, however, forward-looking signals were less encouraging, as general production expectations fell sharply to their weakest level since late 2024 and perceived economic uncertainty rose strongly. Firms also reported a marked increase in expected selling prices, the highest since March 2023, while supply-related constraints remained high. The picture is therefore one of slightly firmer current conditions but weaker forward momentum.

France’s construction business climate was stable in April at 96, remaining below its long-term average and indicating continued weakness in the sector. Builders reported a small rally in recent activity, but expectations for future activity deteriorated sharply and order books worsened again, remaining far below normal levels. Broader sector expectations also became more pessimistic, even though perceived economic uncertainty fell to its lowest level in two years. Capacity utilization edged up to 89.2% and remained slightly above average, while 36% of firms said they were at full capacity. At the same time, expected selling prices surged to their highest level since January 2024 and views on cash flow deteriorated, pointing to renewed margin and financing strain.

The French retail and auto trade business climate weakened sharply in April, with the composite indicator dropping six points to 94, well below its long-run average. The deterioration was led by a steep fall in order intentions and another marked decline in general business expectations, which fell to their weakest non-pandemic level since 2014. Past and expected sales also fell further, confirming softer demand conditions. Expected selling prices rose strongly for a third straight month, suggesting firms still see pricing pressure despite weaker activity. Employment indicators improved modestly, and uncertainty was broadly stable. Both core retail and auto-related trade deteriorated materially, with the auto segment especially weak as its business climate reading fell to 92.

France’s services business climate darkened further in April, with the headline indicator falling two points to 94, its lowest non-pandemic level since 2015 and the eighteenth consecutive month below average. Firms became more pessimistic about expected demand, expected activity and sector-wide prospects, while the balance for expected employment fell sharply to its weakest reading since May 2025. Past activity improved slightly but remained soft, and perceived economic uncertainty rose to its highest level since April 2023. The survey also showed weaker cash flow and subdued investment intentions, while recruitment difficulties remained below average. Sector details were mixed, with information and communication improving but administrative support services and road freight transport deteriorating significantly.

U.K. public sector borrowing in March came in at £12.6bn, which was £1.4bn lower than a year earlier and the lowest March level since 2022. Meanwhile borrowing for the financial year ending March 2026 was estimated at £132.0bn, down 13.1% y/y and slightly below official forecasts. This equated to 4.3% of GDP, marking an improvement from the prior year and the lowest ratio since 2020. The current budget deficit narrowed sharply to £50.9bn, or 1.7% of GDP. However, public sector net debt rose to 93.8% of GDP, with broader liabilities also increasing, even as the annual net cash requirement shrank significantly. FTSE 100 -0.52% to 10422, GBPUSD -0.008% to 1.3501, 10y gilt +3.6bp to 4.945%.

U.K. flash composite PMI rose to 52.0 in April from 50.3 in March, indicating a modest pickup in private sector activity and marking a two-month high. The improvement was driven by stronger output in both services and manufacturing, with factory activity returning to growth and services expanding at a faster pace. However, the rally was partly attributed to advance purchasing ahead of expected price increases and supply disruptions. Cost pressures intensified sharply, with input price inflation reaching its highest level since late 2022, driven by higher raw material, fuel and transportation costs. Firms passed on some of these increases, pushing output price inflation higher, while business confidence weakened and employment continued to decline, pointing to risks to the sustainability of growth.

Norway’s unemployment rate for March 2026 was 4.7%, unchanged from February and January, indicating a stabilization in labor market conditions following earlier increases in 2025. While the unemployment rate has plateaued, employment dynamics remain positive, with preliminary data showing an increase of around 8,100 jobs in March after a modest decline in February. Job growth was concentrated in education, and health and social services, suggesting sector-specific strength. Over recent months, employment levels have fluctuated but remained broadly stable within a narrow range. Overall, the data point to a resilient labor market with steady job creation offsetting earlier weakness, even as unemployment remains elevated relative to prior periods. OSE +0.52% to 2008, EURNOK -0.112% to 10.879, 10y NGB +3.3bp to 4.425%.

Norway’s industrial survey for the first quarter of 2026 showed flat production compared with the previous quarter, while export demand weakened, resulting in a decline in overall order intake. Domestic orders were broadly unchanged, but total order backlogs fell, particularly among producers of investment and consumer goods. Employment growth stalled, and capacity utilization remained below its historical average at around 77.9%. At the same time, input prices continued to rise faster than output prices, contributing to declining profitability. Despite these softer current conditions, firms remained cautiously optimistic regarding the second quarter: they expect higher production, improved order intake from both domestic and export markets and a modest recovery in order backlogs, although investment plans remained unchanged and financing costs were cited as a constraint.

Poland’s consumer confidence deteriorated further in April, with the current consumer confidence indicator falling to -14.1 from -12.2 in March, reflecting weaker sentiment around both current and future conditions. The decline was driven mainly by a sharp worsening in assessments of the country’s economic situation, alongside weaker views on household financial conditions, although willingness to make major purchases improved slightly. The leading consumer confidence indicator also fell to -11.2, pointing to softer consumption prospects, with rising concerns about unemployment and future finances. Despite the m/m deterioration, both indicators remained slightly higher than a year earlier, suggesting some underlying improvement in sentiment relative to 2025. WIG -0.9% to 131540, EURPLN +0.175% to 4.2521, 10y PGB +7.8bp to 5.6%.

Poland’s retail sales rose by 8.7% y/y in real terms in March, rallying strongly from a small decline a year earlier, and were up 18.1% m/m. On a seasonally adjusted basis, sales grew 7.0% y/y and 3.3% from February, indicating solid underlying momentum. Growth was broad-based across categories, with particularly strong increases in fuels, clothing and discretionary goods, while food sales rose more moderately. Online sales also expanded, with their share of total retail increasing. Overall, retail activity in the first quarter rose 4.8% y/y, supported in part by calendar effects such as the earlier timing of Easter.

Australia’s April Flash PMI data showed the Composite Output Index rising to 50.1 (March: 46.6), indicating stabilizing business activity. Services activity improved to 50.3 (March: 46.3), while the manufacturing index rose to 51.0 from 49.8. Manufacturing output declined further to 48.2 (March: 49.4), in a third consecutive monthly contraction. Total new business fell for the second month in a row, though export orders to North America, Asia and New Zealand increased slightly. Business sentiment weakened to a 2.5-year low amid cost and demand concerns. Input cost inflation accelerated to the highest figure since August 2022, driven by rising fuel and shipping costs, with charge inflation at a 3.5-year peak. ASX -0.55% to 5592, AUDUSD -0.126% to 0.7153, 10y ACGB +4.4bp to 5.001%.

New Zealand’s housing market saw sales volumes fall for a third consecutive month in March (-2.4% y/y), rounding off a subdued Q1 (January: -7.6%, February: -3.1%). Nationwide property values remained stable, rising 0.2% in March and 0.3% in Q1, with regional divergence: Auckland values fell by 0.2% in Q1 (-3.4% y/y), while Christchurch prices rose 1.1% (2.4% y/y). First home buyers accounted for 27% of Q1 sales, above the 22% average, supported by improved affordability and credit access. Rents fell by 0.4% y/y, though gross yields reached 3.9%, the highest since 2015. The market outlook remains constrained by inflation, geopolitical risks and muted confidence. NZX 50 -0.47% to 12885, NZDUSD -0.406% to 0.5888, 10y NZGB +4.3bp to 4.716%.

South Korea’s consumer sentiment index fell sharply in April, with the composite consumer sentiment index declining to 99.2 from 107.0 in March, in a 7.8-point drop. The deterioration was broad-based, with current and prospective living standards weakening, alongside falls in expectations for household income and spending. Sentiment toward domestic economic conditions saw the steepest fall, particularly for current conditions, highlighting growing pessimism about the macro outlook. Employment expectations also softened, while interest rate expectations increased further. Inflation expectations edged higher in the near term, with one-year-ahead expectations rising to 2.9%, while medium-term expectations remained relatively stable, suggesting persistent but contained price pressures. KOSPI +0.9% to 6476, USDKRW -0.223% to 1481.65, 10y KTB +4.1bp to 3.697%.

South Korean GDP grew strongly in Q1, beating expectations at +1.7% q/q, from -0.2% in Q4 2025. Real gross domestic income (GDI) surged 7.5% q/q. Private consumption grew 0.5% q/q, while government consumption edged up 0.1%. Construction and facilities investment increased by 2.8% and 4.8% q/q, respectively. Exports rose 5.1% q/q, driven by IT items such as semiconductors, with imports up 3.0% q/q. On a y/y basis, real GDP expanded by 3.6% (Q4 2025: 1.6% y/y), supported by manufacturing (+6.4% y/y) and services (+3.3% y/y). Agriculture, electricity and construction saw mixed performances.

Singapore’s MAS core inflation measure rose to 1.7% y/y in March (from 1.4% y/y in February), driven by higher inflation in retail and other goods and in services, with a 0.1% m/m increase (February: 0.5% m/m). CPI-All Items inflation increased to 1.8% y/y (from 1.2%), supported by rises in private transport, retail goods and services; its m/m rise was 0.5% (February: 0.6%). Food inflation remained stable, while electricity and gas prices decreased steadily. Imported cost pressures are expected to rise due to Middle East developments, with MAS projecting 2026 inflation at 1.5-2.5%. Inflation risks are skewed upward amid potential energy supply disruptions but face downside risks from an economic slowdown. The higher March CPI numbers affirmed expectations of MAS policy tightening in April. There is a high chance of further tightening at the July policy meeting if inflation goes up again. STI -1.06% to 4950, USDSGD -0.251% to 1.2763, 10y SGB +0.7bp to 2.074%.

The Taiwanese labor market weakened slightly in March, with total employment falling by 6,000 to 11.64 million, although it remained 28,000 higher than a year earlier. The unemployment rate edged up to 3.34%, with the seasonally adjusted rate also rising to 3.35%, while broader labor underutilization measures increased modestly, indicating some softening in labor conditions. The unemployment count rose slightly to 402,000, though it was broadly stable compared with both the previous month and a year earlier. Meanwhile, the labor force participation rate dipped marginally to 59.57% but remained higher on a y/y basis, suggesting underlying resilience despite short term fluctuations. TAIEX -0.43% to 37714, USDTWD +0.127% to 31.573, 10y TGB +2.3bp to 1.485%.

Taiwanese monetary aggregates showed moderate growth in March, with M1B rising by 0.23% m/m and 7.83% y/y, while M2 increased by 0.46% m/m and 5.79% y/y, reflecting stronger loan and investment activity. Over Q1, average growth rates were 6.84% for M1B and 5.44% for M2. Credit conditions also strengthened, with monetary institutions’ loans and investments expanding by 0.85% m/m and 7.64% y/y, driven by increased lending to the private sector and public enterprises. Broader financial sector lending growth remained solid after adjustments, indicating continued credit expansion in the economy.

India’s private sector activity expanded sharply in April, with the HSBC Flash Composite PMI Output Index rising to 58.3 from 57.0 in March. Manufacturing led growth, with output and new orders increasing significantly (Manufacturing PMI Output Index: 59.1 vs. 55.7 in March). Services activity also grew but at a slower pace due to the Middle East war. Input cost inflation remained elevated, driven by fuel, gas, raw materials and transportation, though it was below March’s peak. Output price inflation rose but lagged input costs. Employment growth hit a ten-month high, supported by strong demand and expansion plans. Business confidence remained high despite a slight dip. SENSEX -1.08% to 77667, USDINR -0.298% to 94.0788, 10y INGB +2.5bp to 6.948%.

Philippine local-currency government bonds will be included in a widely tracked emerging market index starting January 2027, marking a significant milestone for the country’s financial markets. The bonds will be phased into the Government Bond Index Emerging Markets with a final weighting of 1.78%, a move expected to attract foreign inflows from funds tracking the index, where over $200bn is managed. Officials have framed the inclusion as a strong endorsement of the Philippines’ macroeconomic fundamentals and recent market reforms, with potential inflows estimated at around $3bn. The development is expected to broaden the investor base, improve liquidity and reduce borrowing costs, while supporting a shift toward greater issuance in local-currency debt. PSEi -0.1% to 5984, USDPHP -0.53% to 60.46, 10y PHGB -1.9bp to 6.578%.

The Philippines’ fiscal position for March showed a monthly budget deficit of PHP 349.7bn, up slightly y/y. However, the cumulative deficit for the first quarter narrowed significantly to PHP 355.5bn, down 20.3% from a year earlier on strong revenue growth. Revenues rose by 9.25% y/y in March and by 13.74% in the first quarter, supported by gains in both tax and non-tax collections, including higher dividend remittances. Meanwhile, government spending increased by 5.23% in March and 3.22% YTD, reflecting higher transfers to local governments, energy-related outlay and support to state firms. Overall, improved revenue performance helped offset rising expenditure and reduced the fiscal deficit.

Hong Kong’s consumer price index rose by 1.7% y/y in March, from an average of 1.5% in January and February, while underlying inflation increased to 1.6%, indicating a modest acceleration in price pressures. On a m/m basis, inflation remained stable, with both headline and underlying rates unchanged from February, and seasonally adjusted momentum was steady at 0.2%. Price increases were led by services, transport and utilities, while durable goods and clothing continued to see falls. Q1 inflation averaged 1.6% y/y. The uptick in inflation was mainly driven by higher fuel-related costs linked to rising global oil prices, although broader price pressures remained contained. Hang Seng -0.95% to 25915, USDHKD -0.007% to 7.8327, 10y HKGB -1.2bp to 1.417%.

Hong Kong’s unemployment rate for January-March 2026 fell to 3.7% from 3.8% in the previous quarter. The underemployment rate also eased to 1.6%, indicating a modest improvement in labor market conditions. Despite the lower headline rates, total employment fell by around 7,300 and the labor force shrank by about 5,300, suggesting some underlying softness. The number of unemployed people rose slightly to 136,600, while underemployment decreased. Developments were mixed by sector, with substantial improvements in accommodation services and construction-related activities. Overall, authorities expect continued economic growth to support the labor market, though geopolitical risks remain a key uncertainty.