Conflict behavior shows up in flows

iFlow > Investor Trends

Investor Trends provides a deep dive into patterns and behaviors in equity, bond and currency markets around the globe, underpinned with deeper macro insights.

iFlow > Investor Trends

Investor Trends provides a deep dive into patterns and behaviors in equity, bond and currency markets around the globe, underpinned with deeper macro insights.

Geoff Yu

Time to Read: 5 minutes

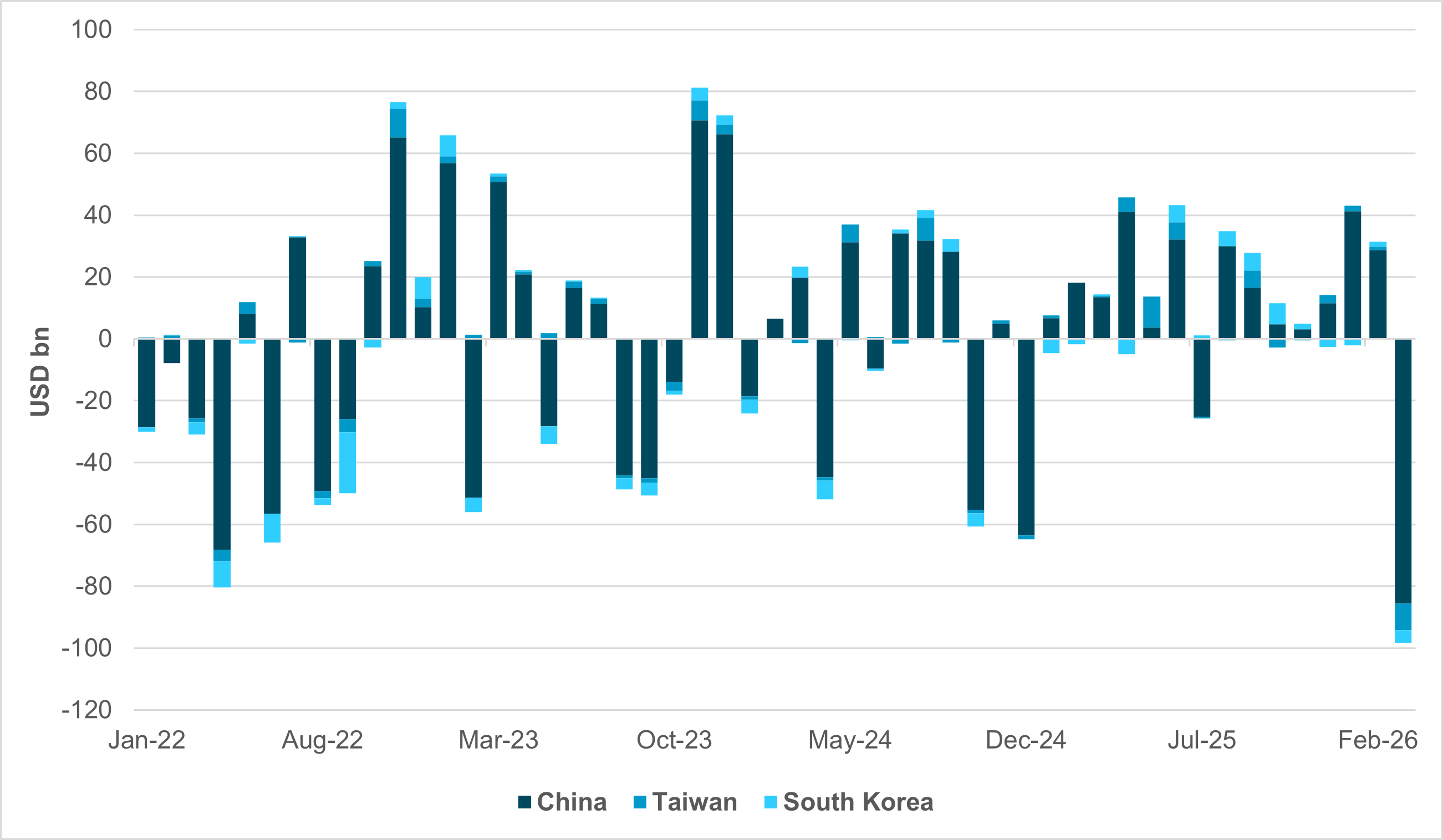

EXHIBIT #1: COMBINED RESERVE CHANGE – CHINA, TAIWAN AND SOUTH KOREA CENTRAL BANKS

Source: BNY, Bloomberg

Our take

Emerging market central banks are starting to release their March reserve holdings figures, and the balance-of-payments damage is becoming clear. On a combined basis, China, Taiwan and South Korea have seen FX reserves drop by nearly $100bn. Valuation effects will be in place, and the scale of intervention will differ between individual central banks, but the scale is material.

This marks the biggest combined drop in FX reserve holdings in four years, surpassing the April 2022 figure of around $80bn. The 2022 print is a good reference point, as it was also driven by a supply shock. These economies are a good case in point for measuring the impact of a sudden shift in import costs, as domestic demand is generally soft compared to developed markets. There isn’t as strong a non-commodity import surge distorting figures. Evidently, the rise in energy costs will continue to make its way through the system.

Managed intervention is the best way to avoid pro-cyclical flows, whereby further currency weakness will widen balance-of-payments gaps and feed into an even more adverse currency narrative. However, we doubt markets will look for severe volatility in CNY, TWD and KRW. Thanks to strong export prowess and very high domestic savings, these economies are seen as having credible levels of reserve coverage compared to the rest of Asia, where governments and central banks do not have the resources to be as active. In these countries, having a weaker currency to drive up import costs is a painful but necessary channel to tighten domestic financial conditions.

Forward look

Rather than assess performance of APAC names, these reserve numbers will probably have a bigger impact on traditional reserve currencies. Although reserve management is much more dynamic and diversified at present, liquidity buffers are still dollar heavy. During periods of higher dollar preference, such as the present, other reserve assets will need to be sold to help fund dollar needs. We explored the impact of UST selling for the same purposes this week.

The need to front-load dollar funding is even more pressing, as much of the balance-of-payments stress revolves around paying much higher prices for necessary commodity imports, the vast majority of which remain dollar-denominated. Consequently, after each dollar sale, additional liquidation of the likes of the EUR, JPY and GBP will be needed to ‘top-up’ dollar levels, and this process is self-fulfilling until underlying import bills drop.

The bottom line is that reserve managers have fundamentally shifted their flows over the past month and in extremely large volumes. The impact on price action will remain until goods export-driven surpluses provide a sufficiently large offset – a reversion that we do not see materializing soon.

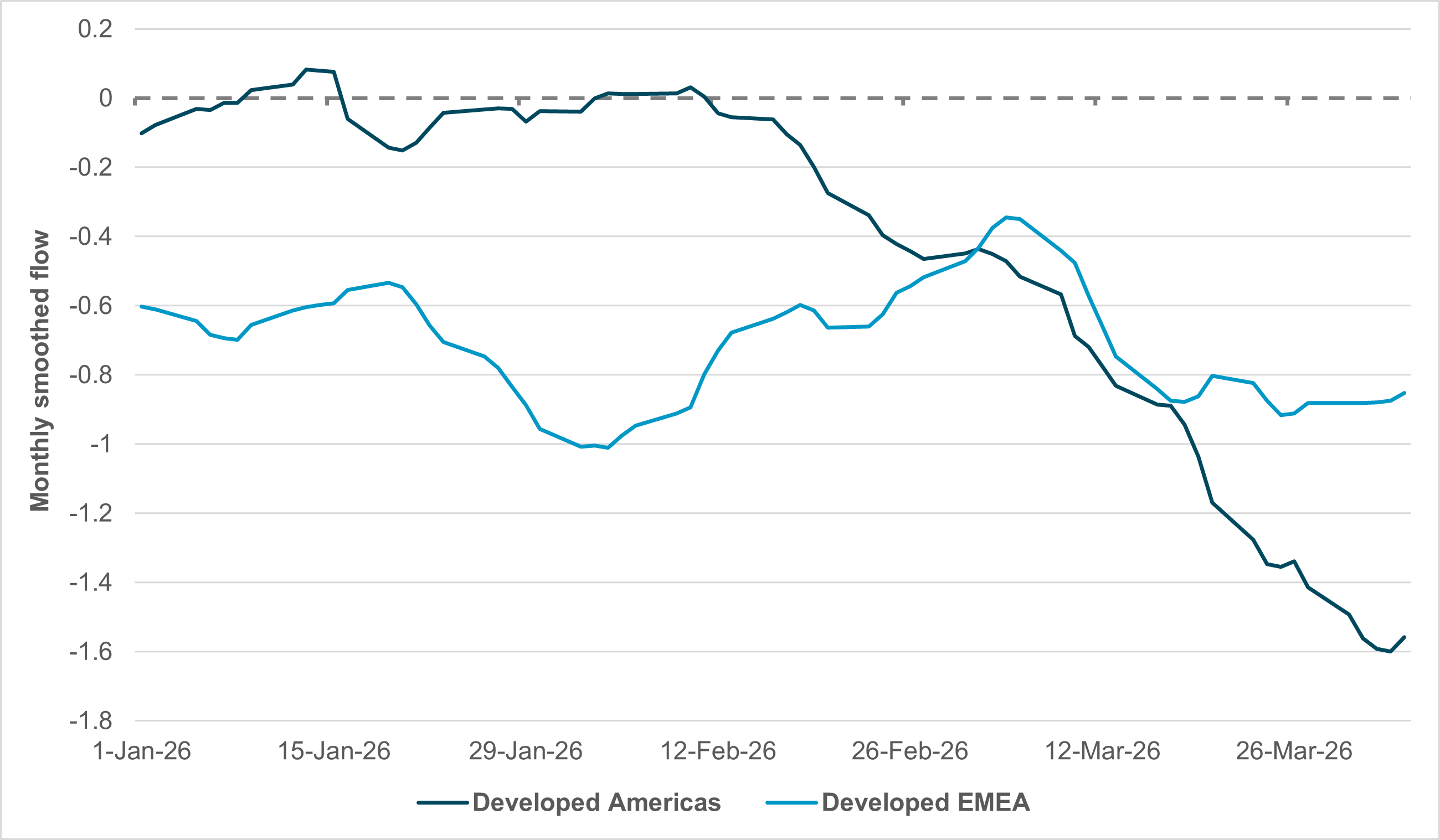

EXHIBIT #2: MONTHLY SMOOTHED FLOWS – CONSUMER DISCRETIONARY IN AMERICAS AND EMEA

Source: BNY, Bloomberg

Our take

As higher energy prices continue to affect household cash flow, we believe the growth impact will become increasingly clear. If anything, central banks are counting on a household pullback to limit the need to hike rates aggressively. Apart from some very vocal hawks in the European Central Bank, most policymakers are choosing to be reactive. A different reaction function by households and governments – who are simply too fiscally constrained to act – will continue to push against the pricing of rate hikes. However, this also means that corporate profitability will continue to struggle, especially in the consumer discretionary segment. This is currently the worst performing sector in developed markets and one of the worst in developing markets. However, on a trend basis, there are clear regional differences. We note that developed Americas – reflecting U.S. household demand – has recently shifted strongly toward heavy consumer discretionary stock liquidation.

In contrast, developed Europe, while continuing to face outflows, is not showing any marginal deterioration. This underscores a key valuation difference: European households were never expected to drive strong earnings, but American households had started the year robustly, helped by a tight labor market. Friday’s payrolls figure indicates that prospects in the U.S. remain favorable, but households will remain cautious.

Forward look

Given the differing “steady state” of U.S. and European household demand, the marginal impact on earnings from an energy supply shock for the U.S. consumer is understandably much stronger compared to European counterparts. Furthermore, as the shock is mostly being felt through gas prices, the marginal impact on U.S. household disposable income is also higher due to differences in driving preferences. This has pushed U.S. consumer discretionary stocks from a leadership position toward severe weakness very quickly. On the other hand, given the scale of the flow and holdings discount, if there is a path toward swift de-escalation of the conflict and normalization of energy prices (simply put, prices at the pump), a recovery for U.S. consumer discretionary stocks can be just as strong, provided the labor market holds.

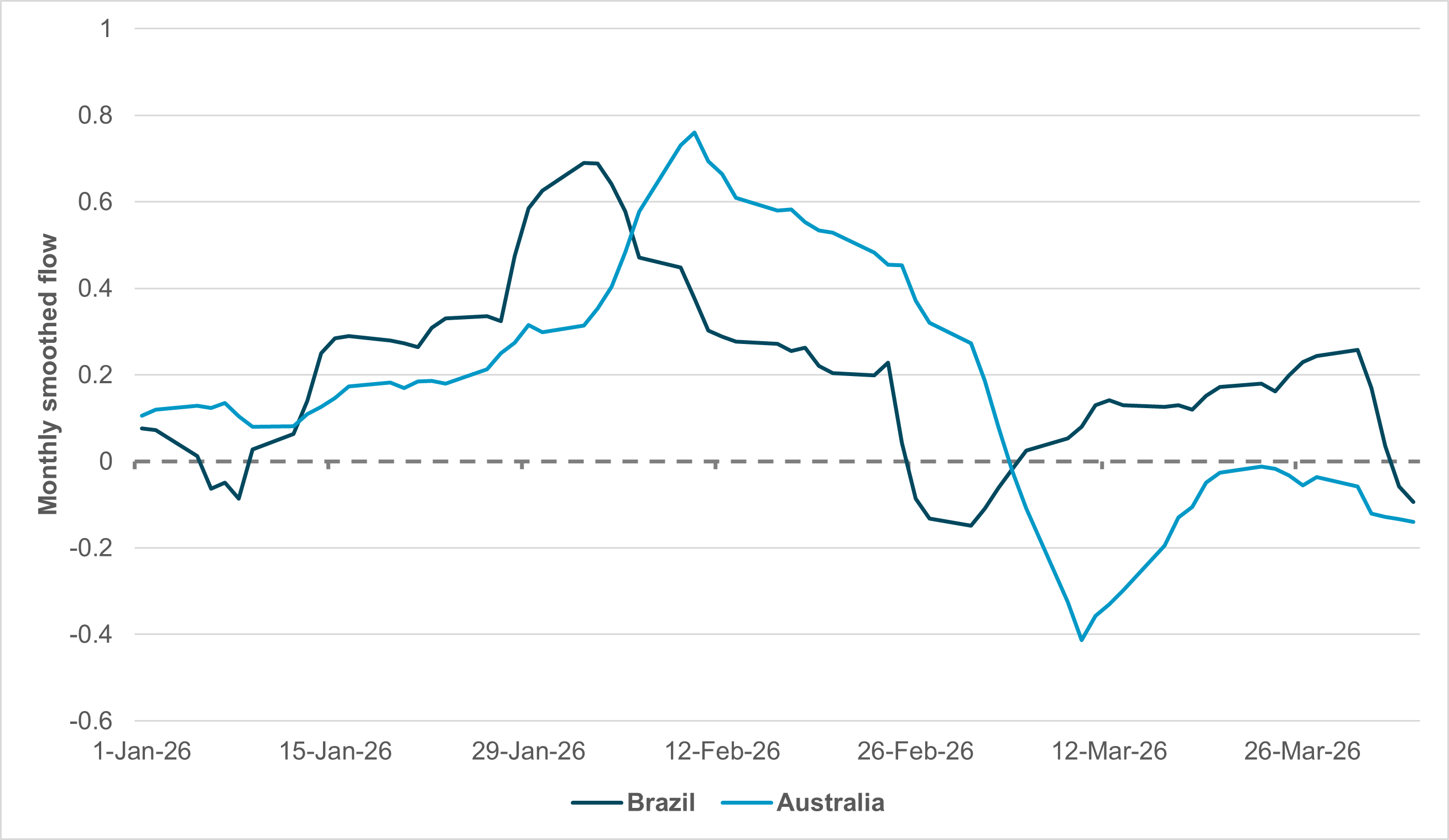

EXHIBIT #3: MONTHLY SMOOTHED FLOW – BRAZILIAN AND AUSTRALIAN GOVERNMENT BONDS

Source: BNY

Our take

Last week, we noted that Brazilian equities were performing strongly because of diversified commodity exposure, from industrial to soft commodities, helping drive positive terms-of-trade adjustment. In developed markets, Australia is the best equivalent and currently the strongest-performing market in all iFlow. In theory, a positive terms-of-trade shock should also be positive for local fixed income: import prices fall relative to export prices, and this should result in lower tradables inflation, which would contribute to higher real rates. However, our flows indicate that the opposite is taking place, with sovereign debt in Brazil and Australian government bonds ending the month net sold (Exhibit #3).

Forward look

The “Dutch Disease” holds that resource booms often hurt productivity for the rest of the economy, and evidently markets believe that this time will be no different. Even before the conflict, Australia was a G10 economy pivoting back toward rate hikes. At the time, we felt that Norway wasn’t far behind. The Reserve Bank of Australia has even acknowledged that there were structural reasons behind high inflation in the country.

A sudden boost to terms of trade will likely generate additional demand impulse, though household cashflow may suffer slightly this time, more due to higher energy costs.

For Brazil, nominal rates are already sufficiently high to act as a restraining factor, but progress has been slow due to fiscal impulse. The risk is that any resource-based windfall will push fiscal spending further without commensurate productivity gains and not generate any sufficient risk reward to materially add to fixed income exposures.