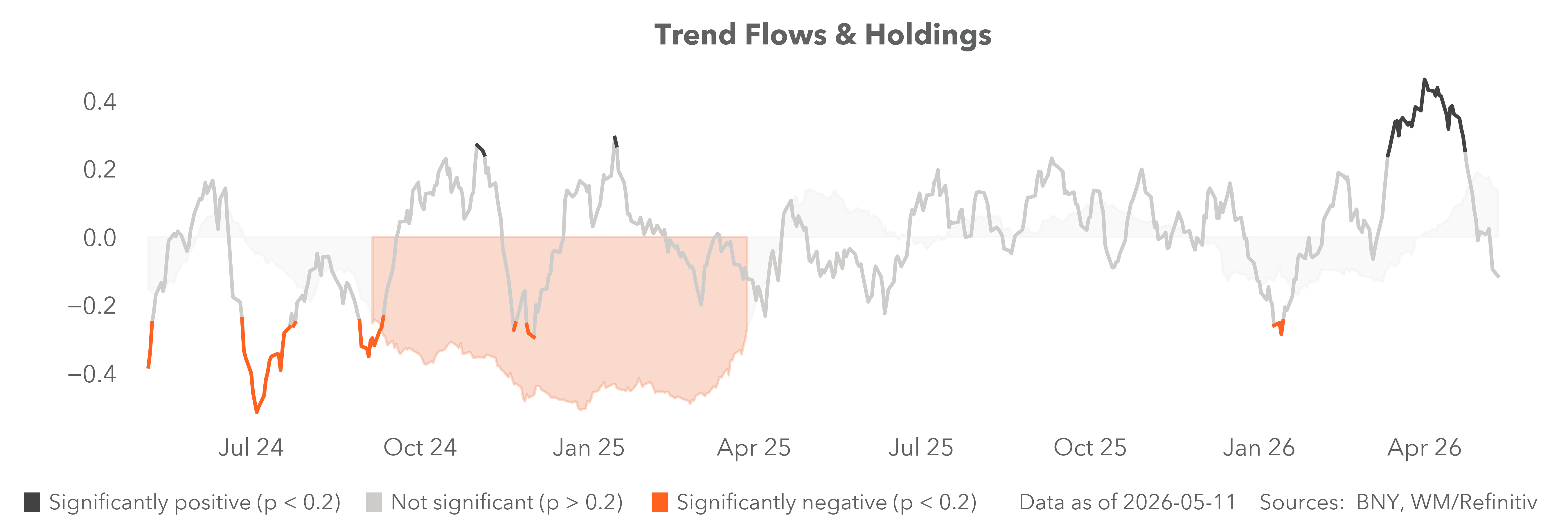

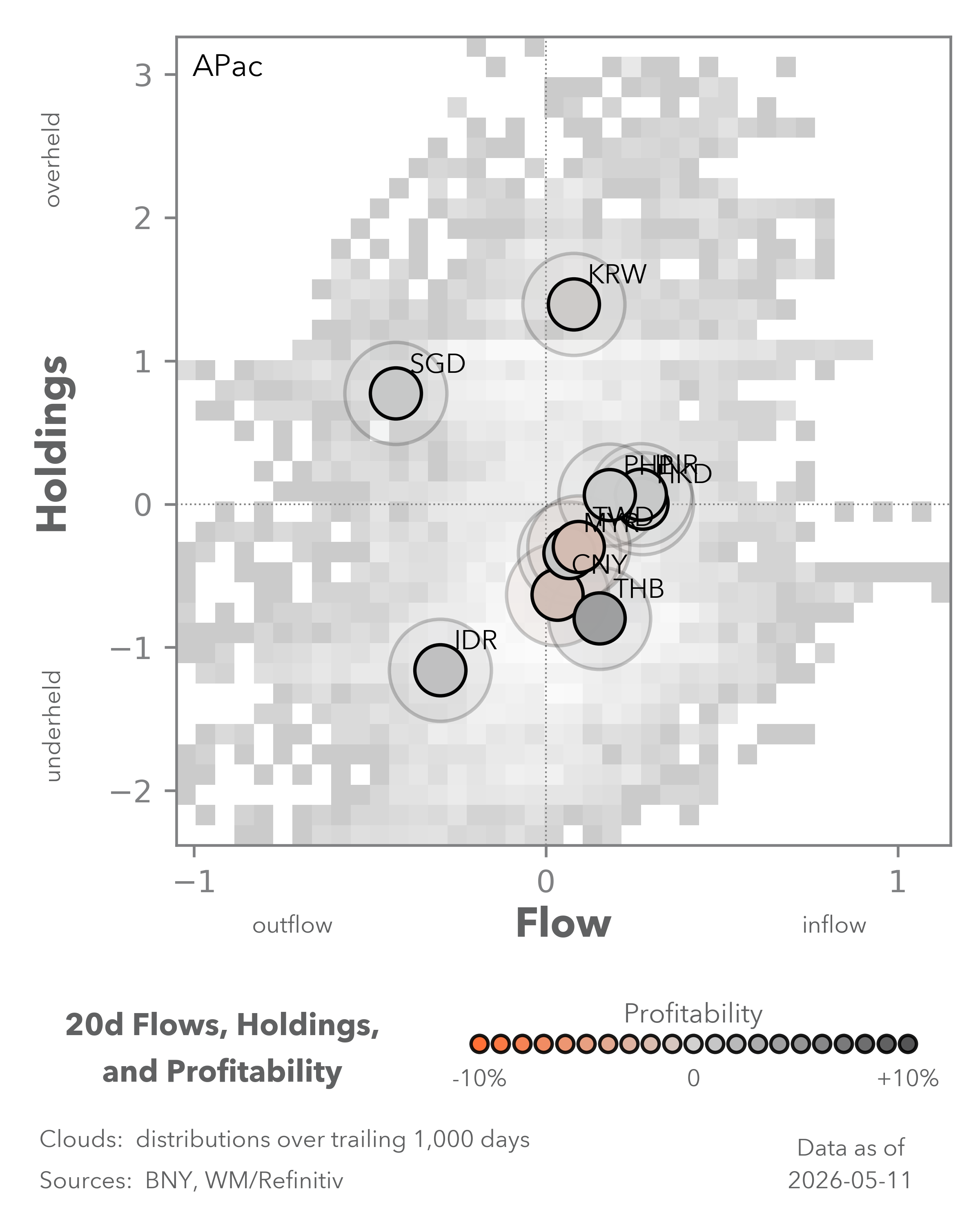

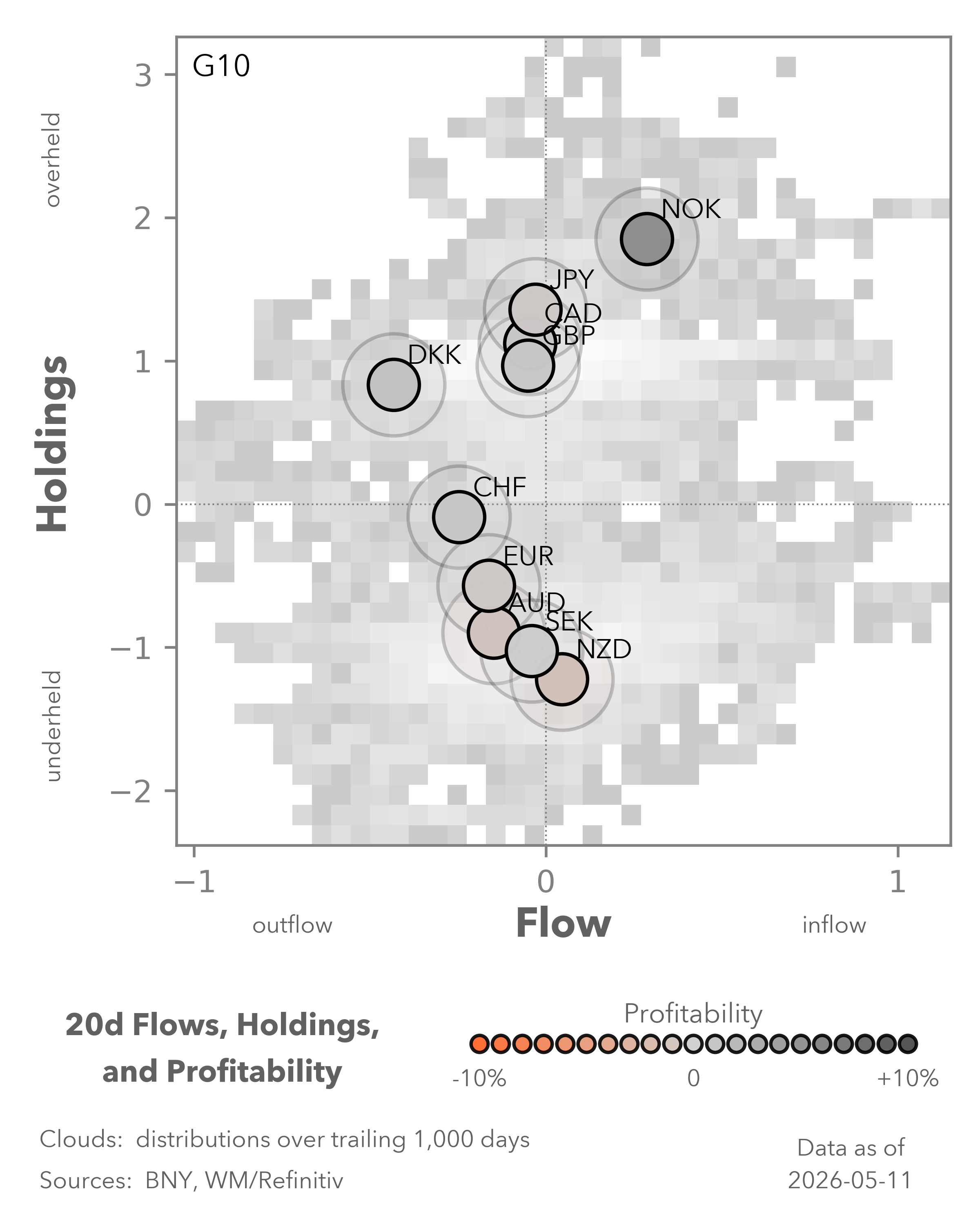

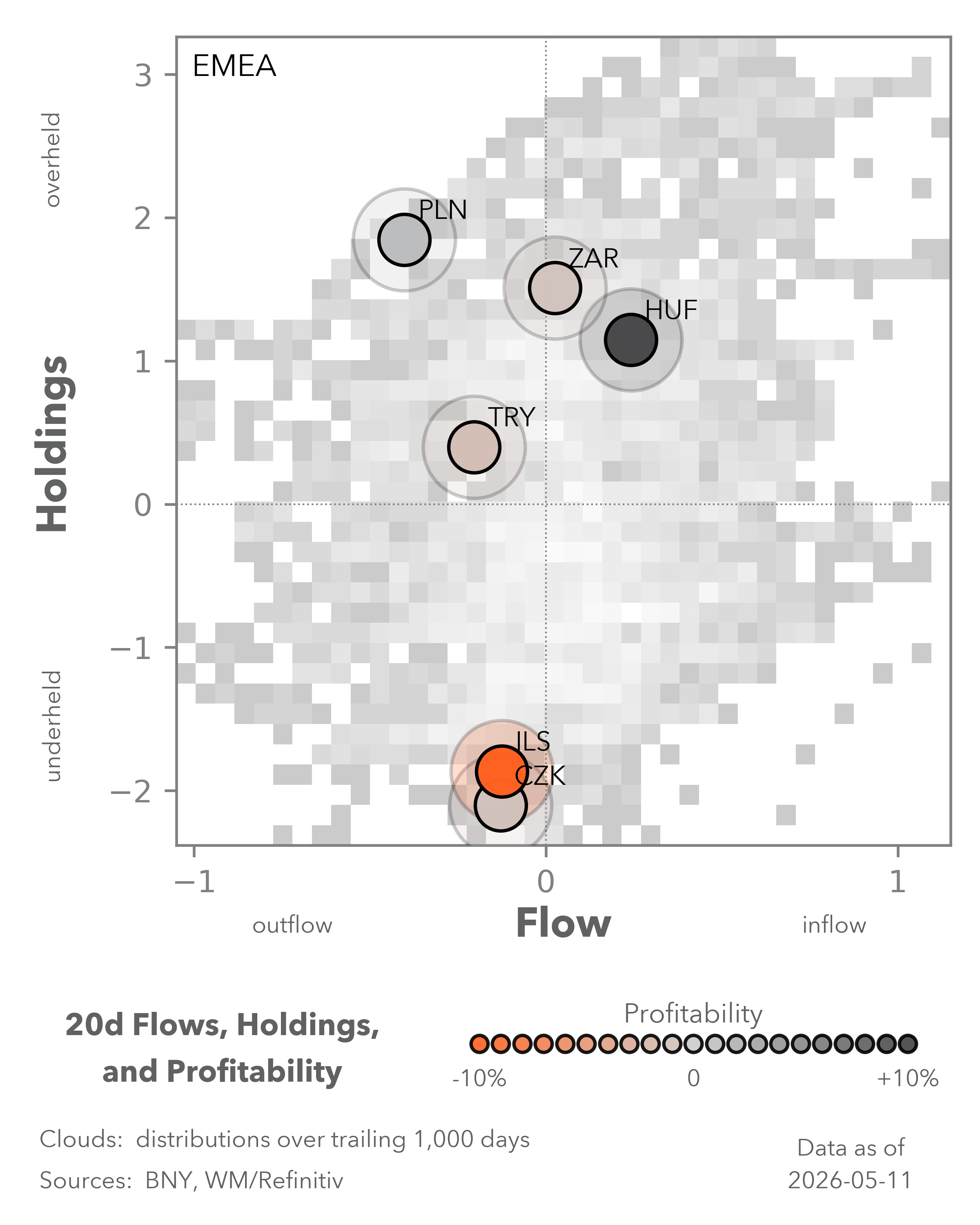

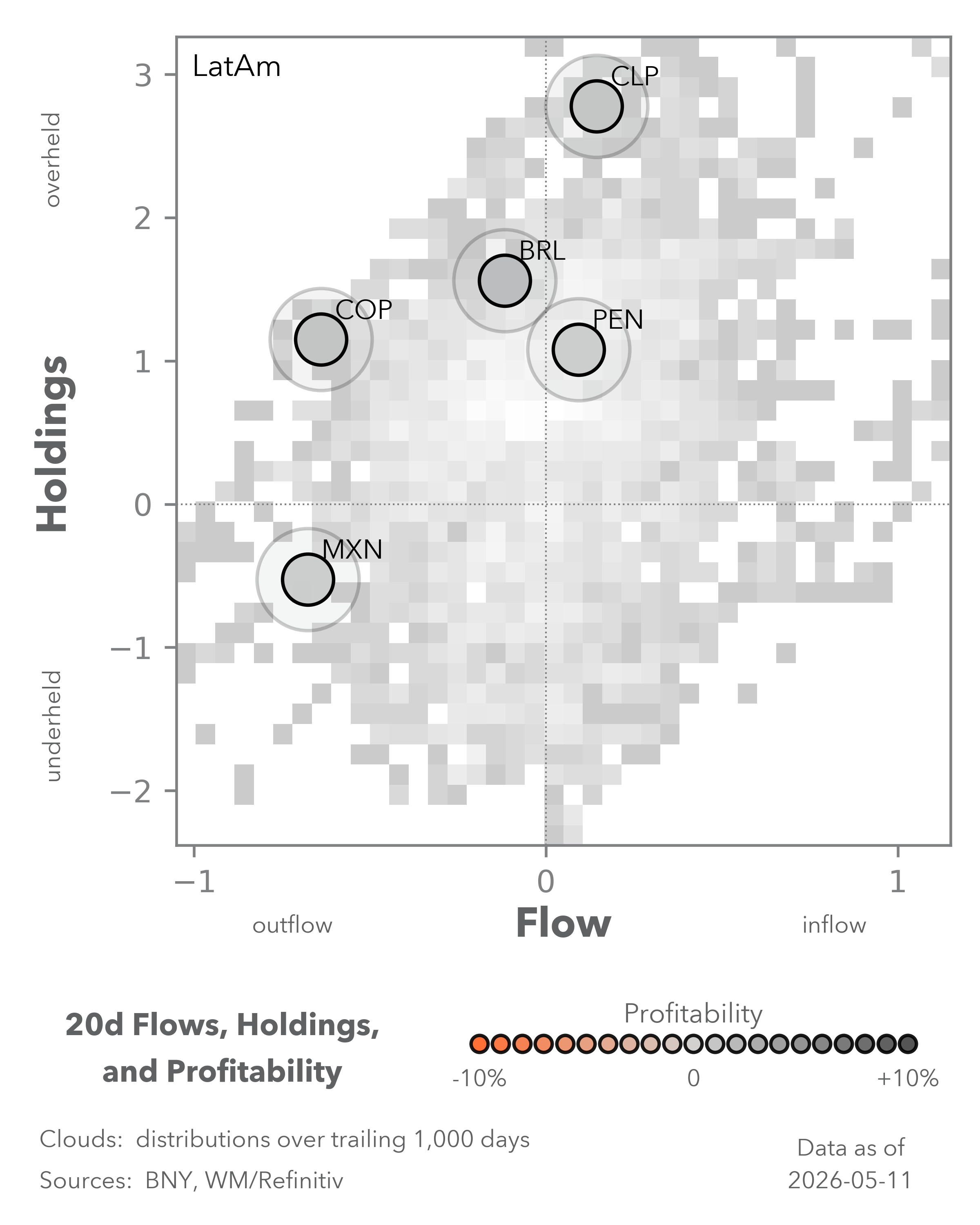

Valuations still drive the flow picture

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 4 minutes

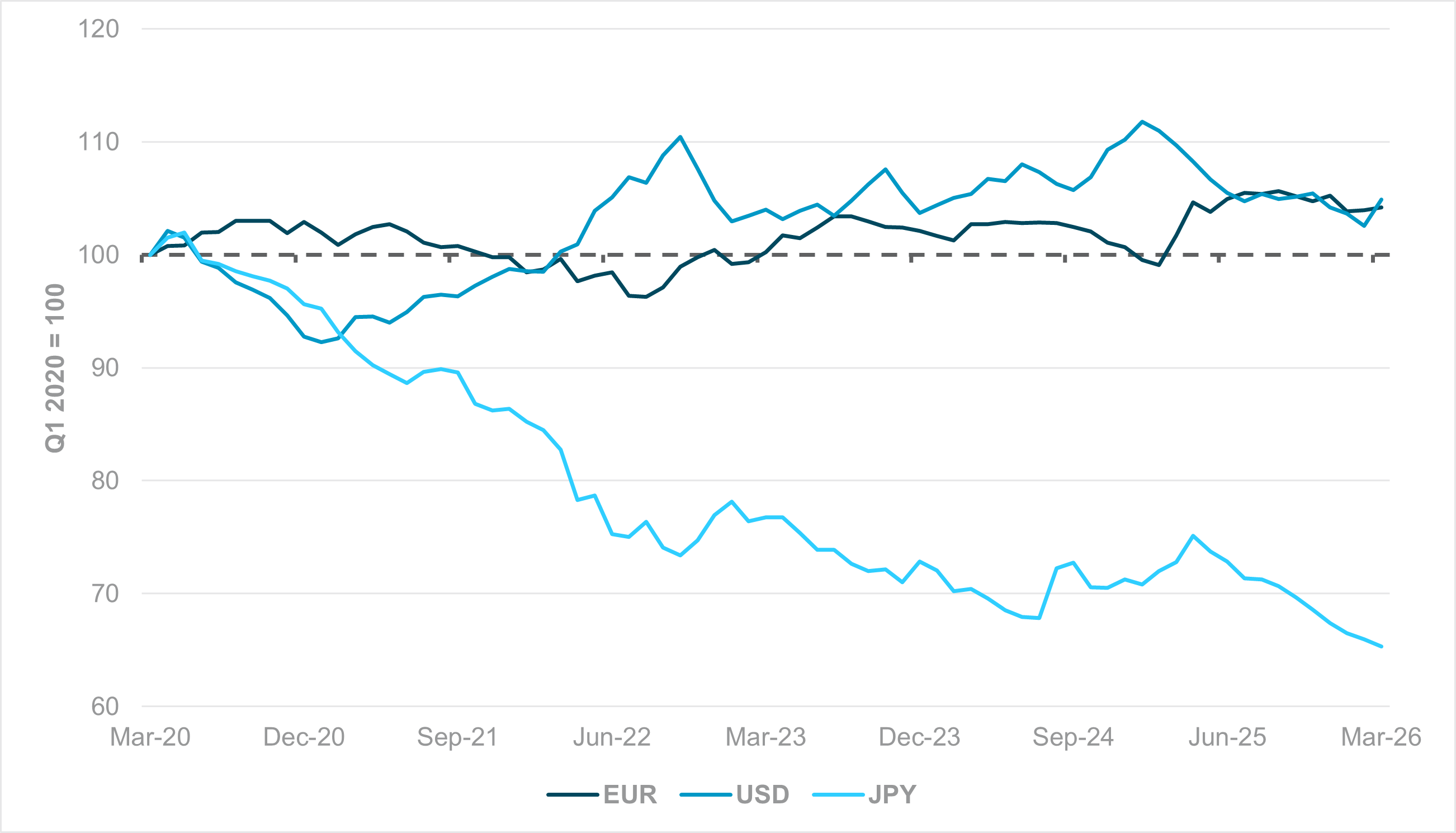

EXHIBIT #1: EUR, USD AND JPY REERS, Q1 2020 = 100

Source: BNY

Our take

U.S. Treasury Secretary Scott Bessent’s trip to Tokyo was accompanied by another sharp, brief drop in USDJPY. The market will look to intervention figures at month end to gauge the Japanese Ministry of Finance’s resolve in intervening in FX markets, but so far it has very little to show for it. Bessent stressed that while he made no specific fiscal policy requests, FX volatility was not desirable, and that “the strength of the Japanese economy will be reflected in the exchange rate.” Given that strong economies – export-driven or otherwise – are not supposed to have weak currencies, the message was clear: he still views the JPY as too weak. We fully agree with this view, but given where G3 currency valuations currently stand, it is surprising that the EU has not been more vocal, especially relative to previous cycles. Bessent has made his view on several Asia-Pacific currencies known in recent months, especially in the context of cheap valuations, but neither German Finance Minister Lars Klingbeil nor EU Economy Commissioner Valdis Dombrovskis have offered their views.

Based on the Bank for International Settlements’ (BIS) Real Effective Exchange Rate (REER) indices, measured by their change over the last five years, the dollar and euro have fully converged in valuation over the past six months. A range breakout would require a significant structural catalyst – the technology drivers behind “U.S. exceptionalism” or the “European strategic autonomy” theme on defense. The common theme there is large-scale investments, public and/or private, which were expected to drive productive growth and lift REERs.

Japan has had no such lift, but there is a difference between “lack of appreciation” and the kind of secular depreciation currently witnessed.

Forward Look

The risks of sustained and significant JPY undervaluation are much more of an issue for Europe than the U.S. due to greater export competition, though that has been eroded over time, especially in the automotive sector, where China has significantly disrupted global markets. While the U.S. tariffs issue has faded somewhat, it remains a long-term concern and could yet force REER appreciation. Japan’s ability to offset this more effectively through the exchange rate than the EU can is a separate competitiveness challenge. Granted, the ECB has far lower tolerance for inflation relative to the Bank of Japan, but as major exchange rate misalignments have escalated into the diplomatic sphere in the past, Europe should take a proactive approach.

Unless Europe now sees inflation differentials on a structural basis due to higher wage growth but without commensurate productivity gains, the exchange rate emphasis alone is secondary. U.S.–Japan coordination on exchange rates is already in play, and we see EU and U.S. interests aligning here as well.

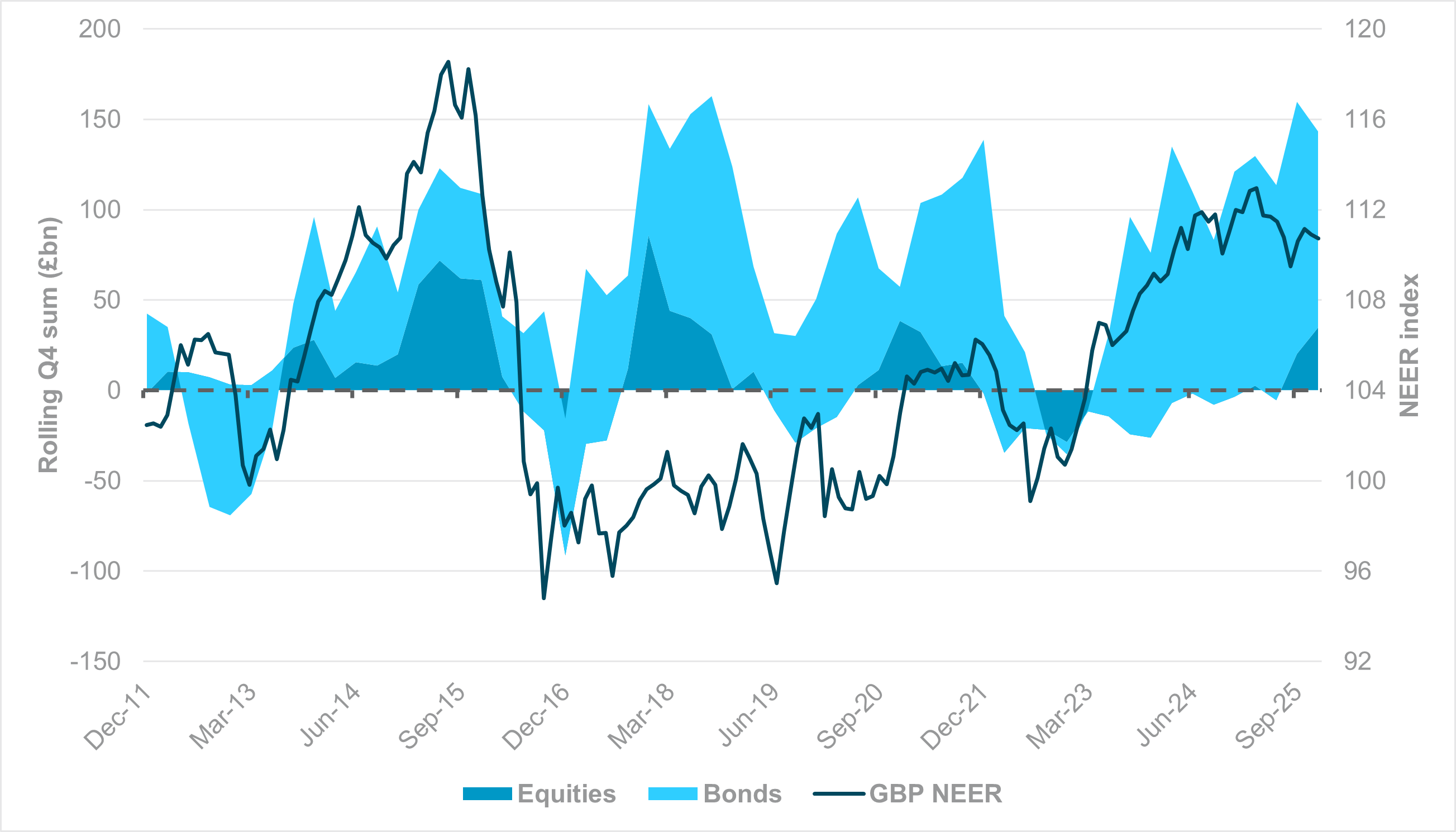

EXHIBIT #2: U.K. EXTERNAL LIABILITIES (Q4 ROLLING SUM) VS. GBP NEER

Source: BNY, Macrobond, BIS

Our take

We expect U.K. political theater to continue as Labour Party backbenchers tally the numbers ahead of a leadership challenge. The political environment remains febrile and, irrespective of the outcome, the gilt market is choosing to stay on the defensive for now.

GBP has held up better, but we are not enthused by current pricing, which has shifted back to three rate hikes for the rest of the year, this time driven by domestic factors rather than global supply pressures. The market clearly believes that, whatever the political denouement, fiscal loosening is inevitable, which would force a different Bank of England reaction function.

Forward Look

GBP cannot rely on rate expectations alone for resilience. We maintain that tightening anywhere in Western Europe could exacerbate demand stress, and policymakers do have the capacity to lean more on domestic restraint and a high savings rate. Much of the residual funding from domestic asset allocators is moving into gilts, but we note that official balance-of-payments data suggest that cross-border interest in U.K. bonds ended 2025 on a strong note (Exhibit 2), notwithstanding fiscal concerns surrounding the autumn budget.

The data show that such strong inflows have historically benefited the currency, but toward Q4 last year, some of the support was already starting to wear off. Consequently, GBP now faces flow asymmetry: yield-driven inflows merely support valuations, while fiscal premium-driven outflows could trigger a sharper downside. GBP’s NEER remains above long-term averages, and fiscal authorities – current and future – will need to watch currency reactions as closely as gilts through the next parliament.

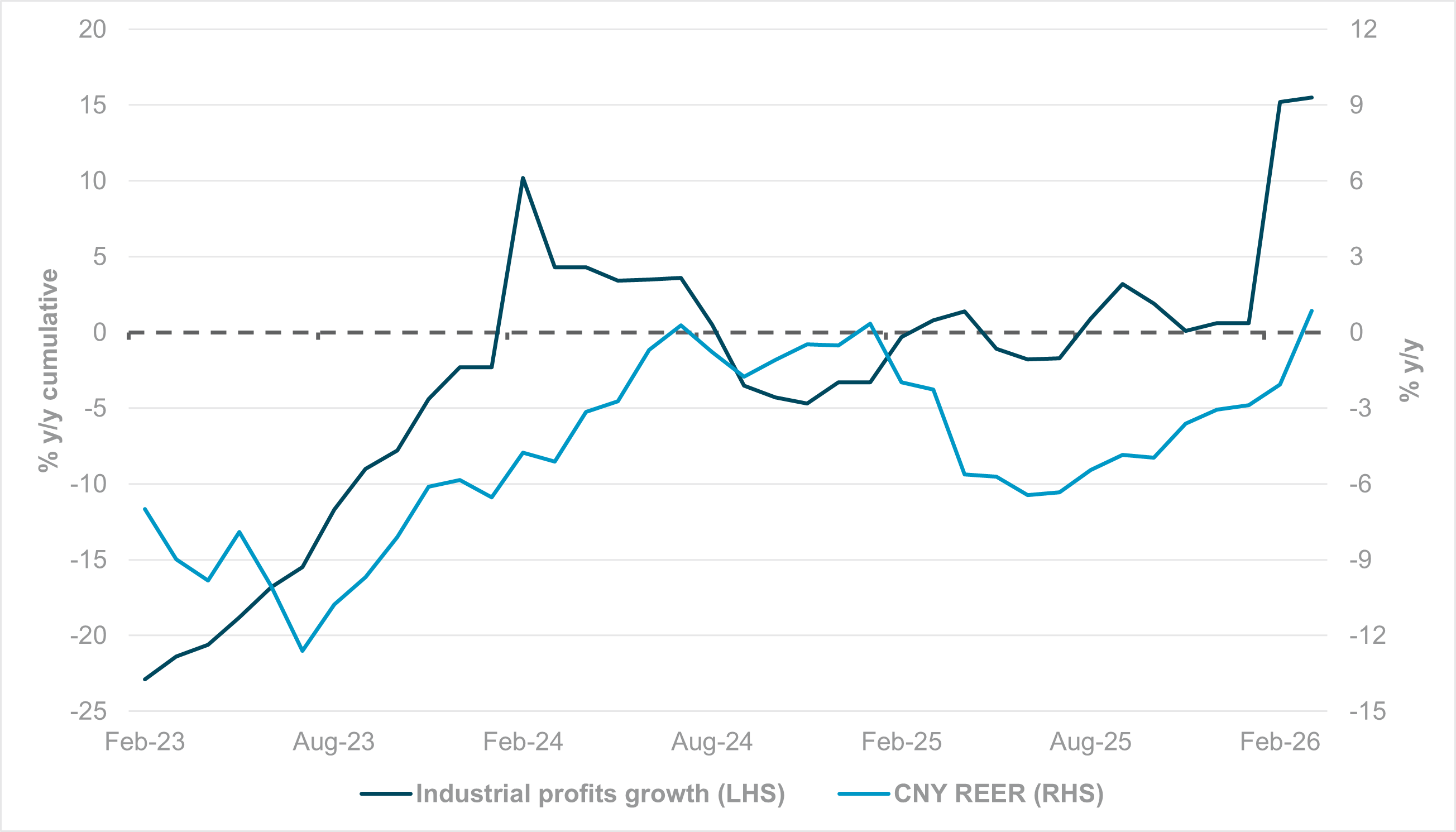

EXHIBIT #3: CHINESE INDUSTRIAL PROFITS VS. CNY REER

Source: BNY, Bloomberg LP

Our take

The bulk of the “action” in Asian equities remains in South Korean and Taiwanese markets, and, to a lesser extent, Japan, due to AI-related investments, though Chinese equities are starting to beef up their performance as well. Heading into the Trump–Xi summit, the CSI 300 is up 10% year to date. The latest data suggest it is more than a simple asset allocation or passive positioning story: cumulative annualized industrial profit growth has surged to a post-pandemic high.

Base effects and long-awaited reflation are coming into play. Chinese companies onshore can benefit from stronger fiscal and household demand, while exporters are also looking to take advantage of broader market share to improve margins. Markets often expect Beijing to slow CNY appreciation in a soft-growth environment to protect exporters, but we see that risk as low for now.

Forward look

First, we stress that CNY appreciation for now is minimal. Its REER is only modestly positive on an annualized basis, even though this is the highest growth figure in three years.

Second, last year’s large trade surplus was achieved despite a substantial implicit REER appreciation through tariffs, even after the truce that followed “liberation day” by several weeks. The cost was likely borne through extreme – and unsustainable – margin compression. Prices are likely to move higher anyway given current supply stress, and a stronger CNY helps reduce pass-through on dollar-priced inputs.

Most importantly, China needs to drive growth through the domestic channel, and the focus this year, from both government and households, looks sharper. These earnings are FX-neutral, and the income and wealth effects that follow could materially lift growth expectations.