Silver linings amid the conflict clouds

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

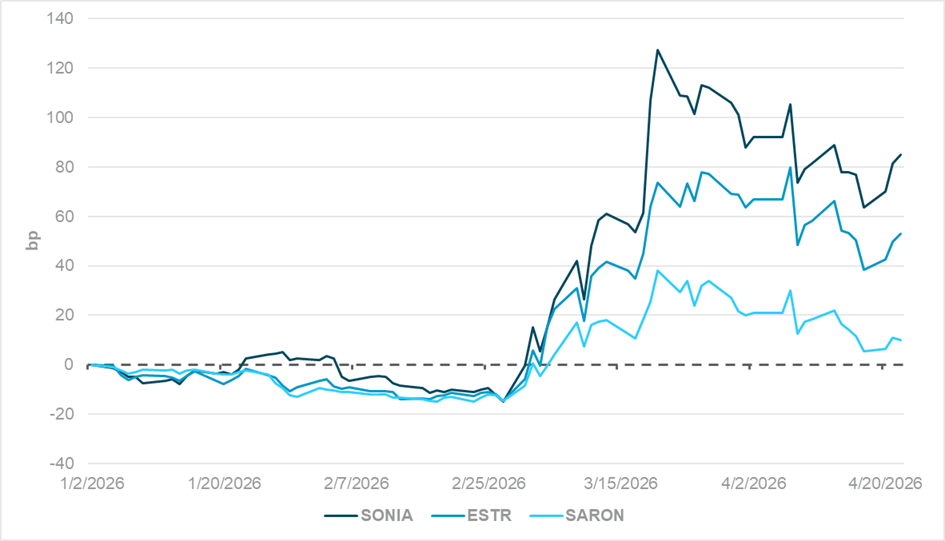

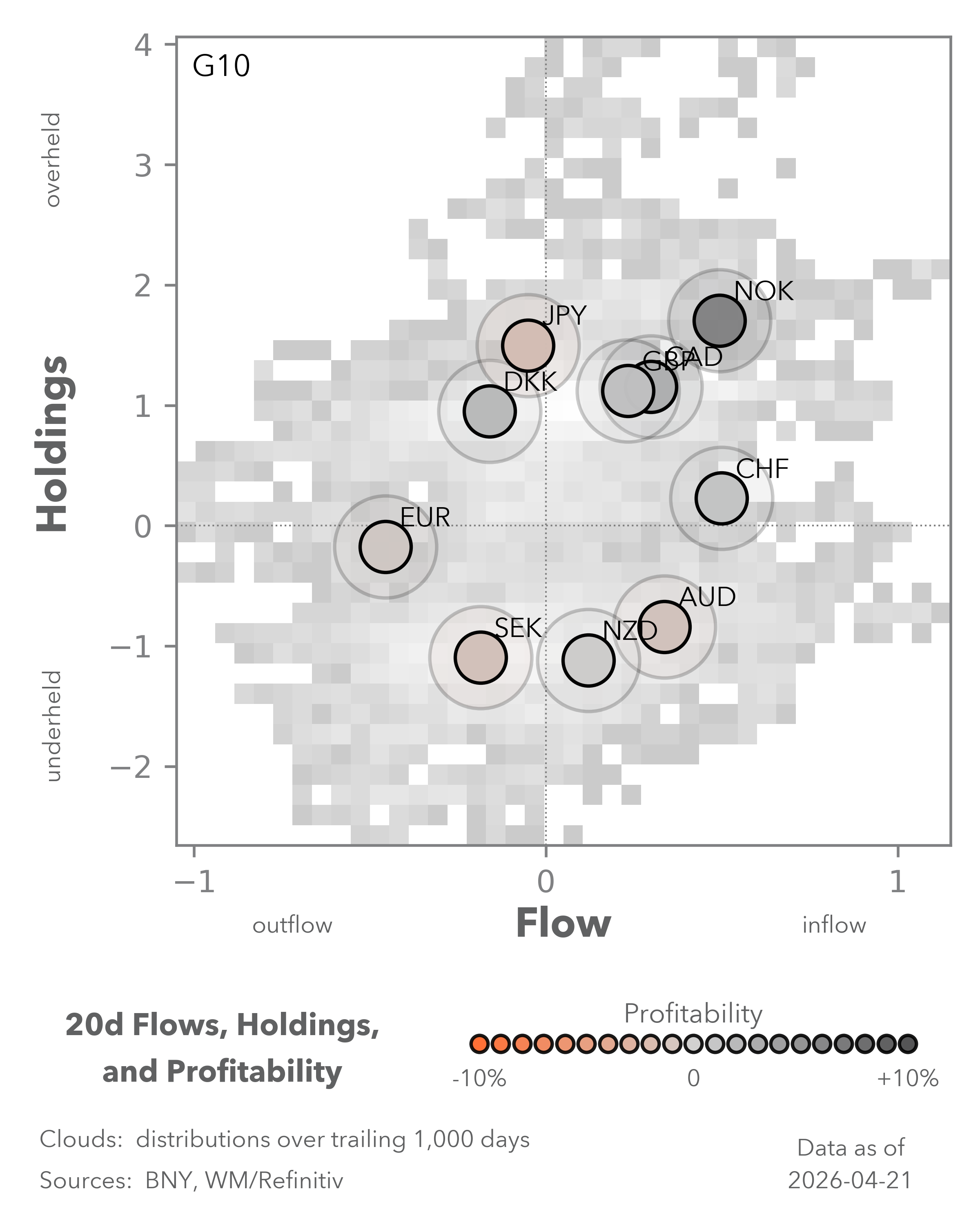

EXHIBIT #1: RATE FUTURES – CHANGE IN DECEMBER 2026 CONTRACT LEVELS

Source: BNY, Bloomberg

Our take

After yesterday’s CPI release, all March inflation data are now available to central bankers ahead of their policy decisions. In our view, the case for a pre-emptive move is not compelling, and on balance we do not expect the European Central Bank (ECB) or Bank of England (BoE) to move next week.

First, there hasn’t been any surge in core inflation figures beyond expectations, and in all cases for core Europe (U.K., Eurozone, Switzerland and Scandinavia), annualized core inflation either held steady or fell. There was no sign of a demand boost, from which we can infer that either wage expectations are well anchored or any earnings growth is not translating into changes in household behavior. We have long held the view that the conflict started at an acutely weak point in Europe’s growth cycle. Consumer confidence surveys point to considerable near-term restraint, reflecting a generally poor economic outlook. Tightening through the interest rate channel now risks doing more harm than good. However, rate futures pricing suggests Swiss National Bank expectations have largely normalized, while the BoE and ECB are still expected to move at least once next quarter.

Forward Look

Based on rhetoric alone, only the ECB stands a chance of moving, but the April decision is unlikely to be unanimous. Some Governing Council members have unequivocally opposed tightening, and fears of household scarring are a recurring concern shaping near-term decisions globally. The biggest swing factor over the next few months will be how corporates pass on higher input costs, which is likely to be prolonged even if energy prices gradually fall. For example, U.K. CPI increased by only 0.7% m/m, but producer input prices surged by 4.4% m/m, and the annualized figure surpassed 5% for the first time in three years. Yet output prices rose only 0.9%. Such a spread is unsustainable for corporate profitability, even though March figures were a one-off due to base effects.

If output prices surge out of necessity, then central banks will feel compelled to act, as wage demands would likely strengthen. On the other hand, if they choose severe cost-cutting to reduce input costs, it would weigh further on demand and remove pressure for policy adjustments. Europe has time to make a more informed assessment, and rates markets can continue adjusting accordingly.

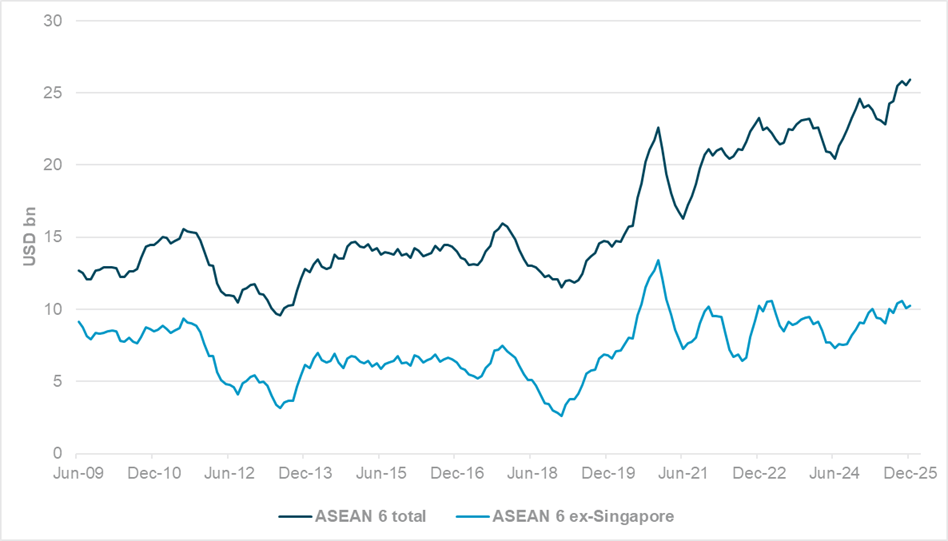

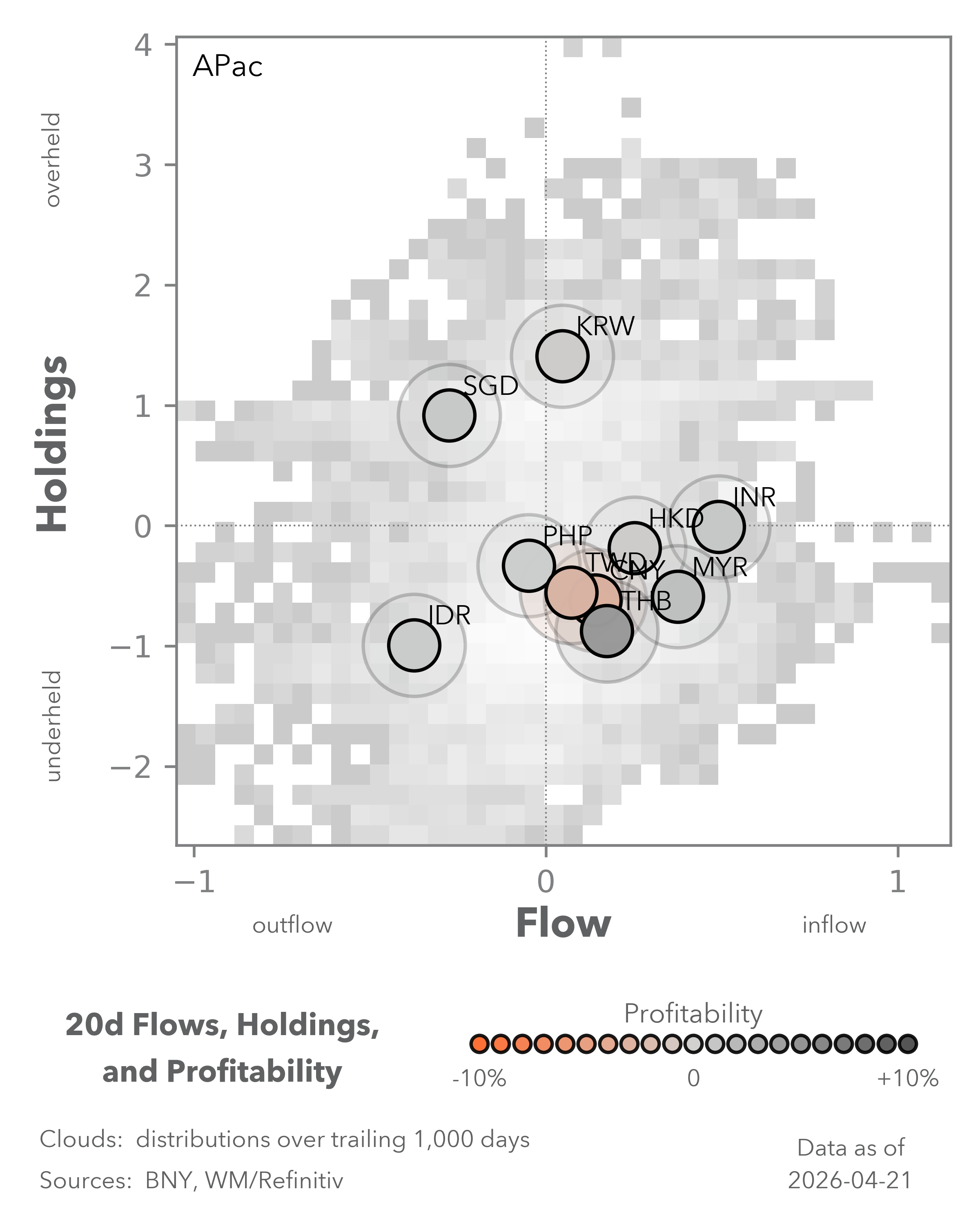

EXHIBIT #2: ASEAN TRADE BALANCES, SIX-MONTH MOVING AVERAGE

Source: BNY, Macrobond

Our take

Bank Indonesia’s (BI) interest rate decision was largely in line with expectations, and the central bank committed to preserving currency stability, calling it an “all-out” effort to maintain IDR stability. Reserve declines across Asia remain significant – a major source of dollar and U.S. Treasury sales by non-U.S. accounts – suggesting dollar liquidity needs remain elevated. Intervention will remain targeted, but BI also stressed that balance of payments “must be strengthened” to mitigate the impact from the war, as the country’s current account forecasts were revised sharply down from a deficit of 0.5% of GDP to 1.3%. In our view, every emerging market (EM) net energy importer will need to address balance of payments risks in their central bank decisions, especially Indonesia’s peers in Southeast Asia.

Forward Look

ASEAN’s struggles throughout the conflict have been well-documented, but the hard numbers are not insurmountable. The core ASEAN economies – Indonesia, Malaysia, Thailand, Vietnam, the Philippines and Singapore – currently run a combined rolling six-month surplus of around $25bn, 60% of which is attributable to Singapore, whose trade patterns are sui generis. For the remaining names, the combined surplus is close to $10bn. In 2022, during the last global energy shock, this fell near $5bn, and most nations except the Philippines continued to generate modest surpluses. The net shortfall is manageable, especially relative to reserve levels. The concern is more about the pace of drawdown, which can generate significant market volatility. Thailand attempted to stabilize oil prices with a reserve fund during the first week of the conflict but swiftly abandoned it. We agree that in the current environment, reserves should be used as smoothing operations, and balance of payments correction should come through demand-side adjustments. Fiscal measures to restrain activity are a useful stopgap, though this falls beyond the remit of local central banks. Furthermore, external FX-denominated liabilities are far more manageable than previous crises. Nonetheless, a prolonged global growth shock would weigh on export earnings and require additional offsets through fiscal or monetary measures, which could increase risk premia over time.

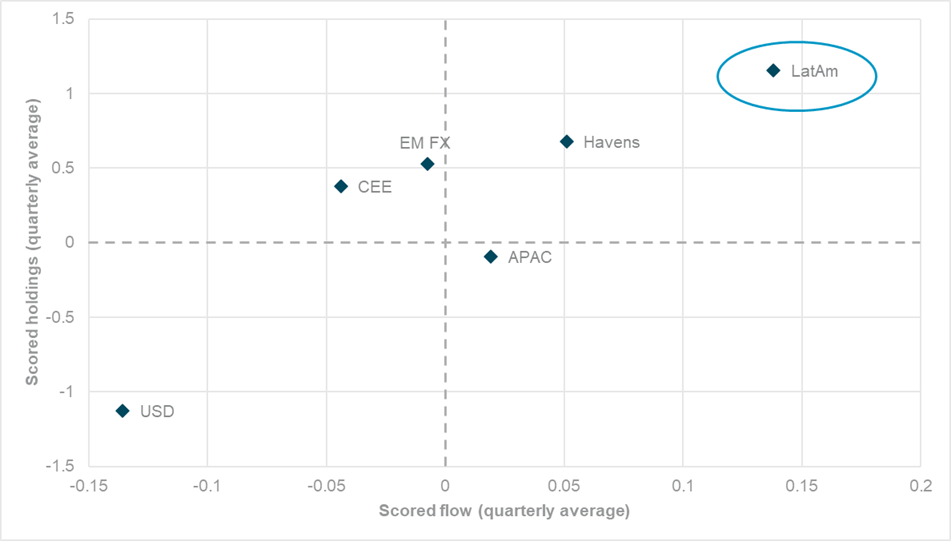

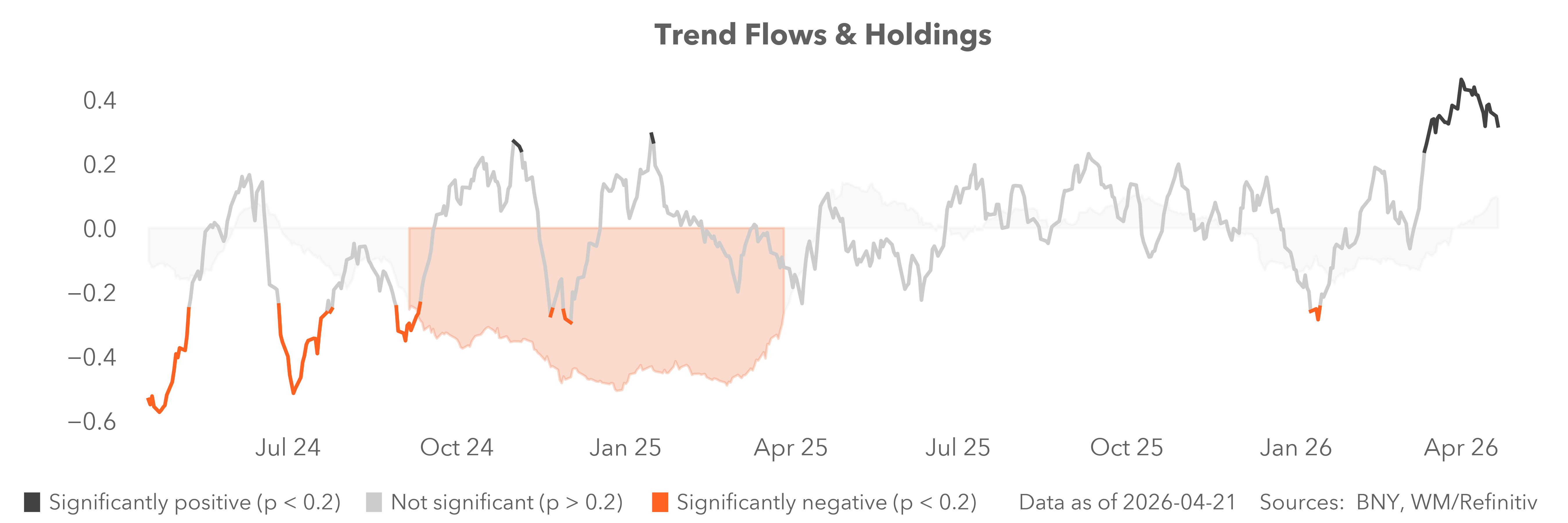

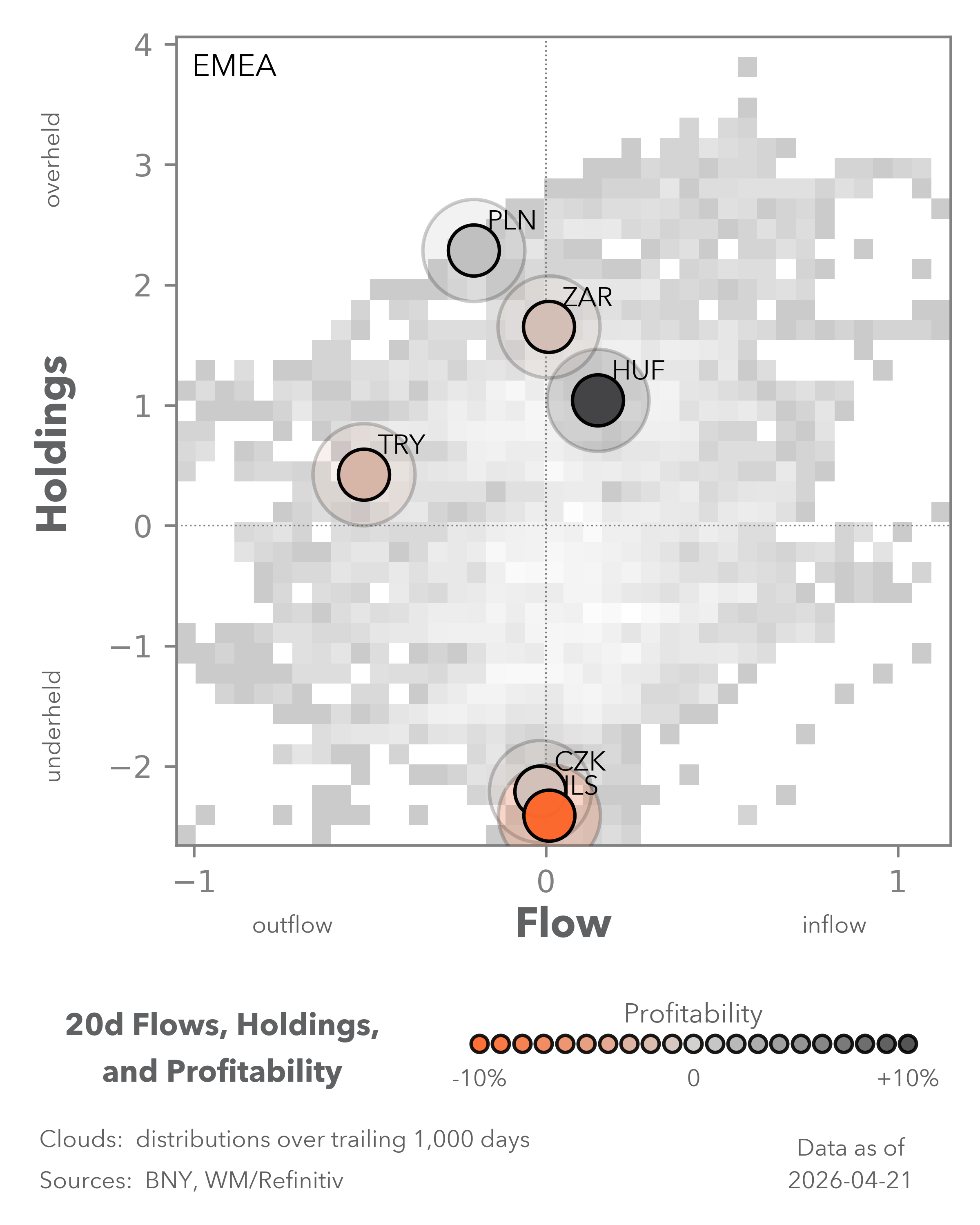

EXHIBIT #3: TREASURY INTERNATIONAL CAPITAL OFFICIAL AND PRIVATE SECTOR FLOWS

Source: Bloomberg, BNY

Our take

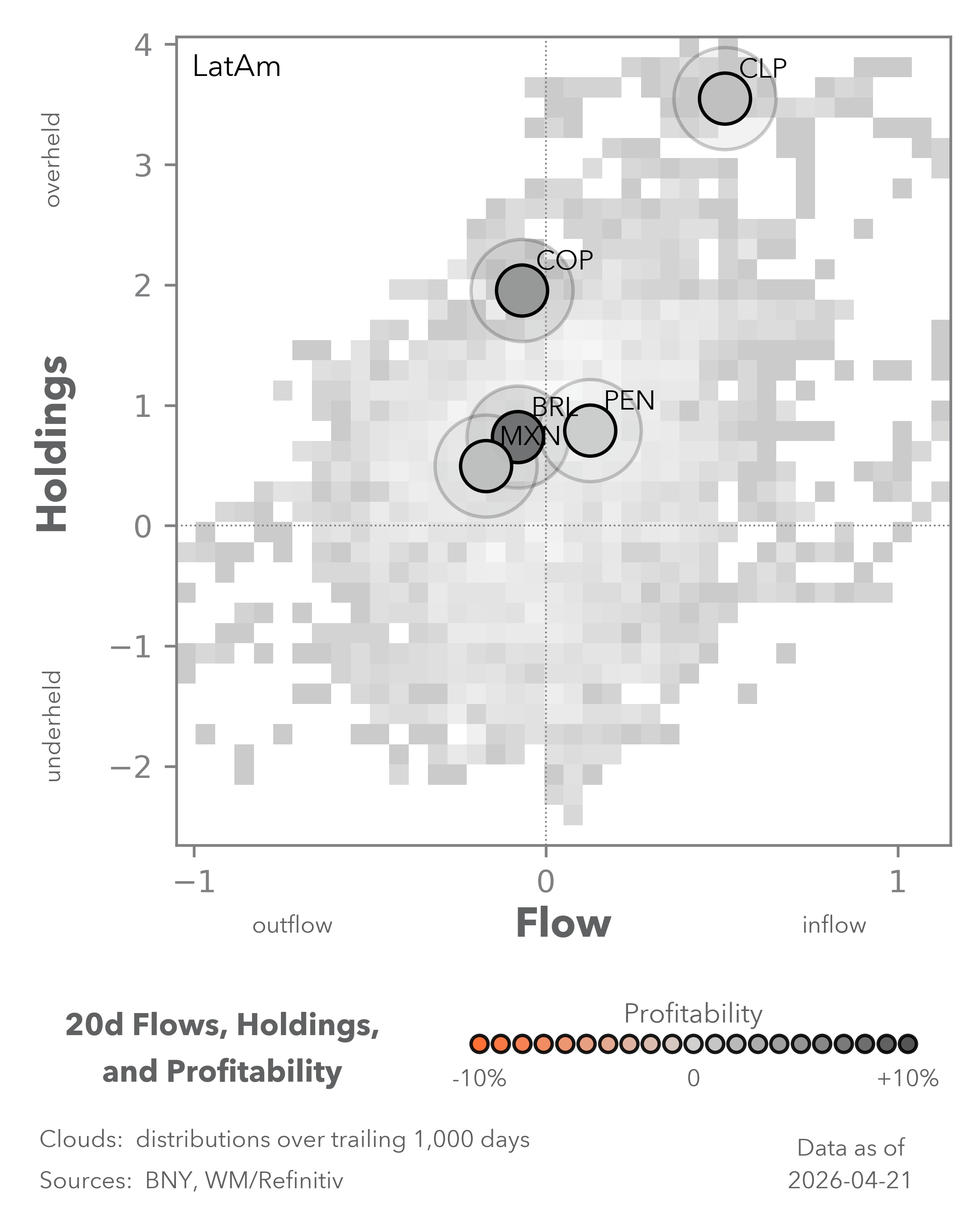

In FX markets, the recovery in risk sentiment is still tentative, but EM FX holdings are starting to pick up gradually. Performance distribution remains uneven, however. Holdings in CEE and APAC remain near year-to-date lows and are unlikely to recover meaningfully until balance of payments conditions improve. A lack of rate pricing to support APAC carry is another drag.

Over the past quarter, the dollar has remained under cross-border pressure driven by hedging demand that dominated in January and February and has re-emerged since the ceasefire. LatAm, at the other end of the spectrum, delivered a tremendous quarter and was by far the best-bought region. It remains the best-held. Throughout the conflict, not a single currency came close to moving into underheld territory. Next week brings another round of LatAm central bank decisions, and nominal and real rates are expected to remain supportive.

Forward look

If the ceasefire holds and risk appetite picks up, the scope for holdings recovery across risk assets means it will be difficult for Latin American currencies to build on current positioning. Initially, this need not mean carry deteriorates, which would entail significant Latin American currency sales. However, APAC and EMEA could become more attractive valuations improve. Risk rotation could accelerate materially, driven by the progressive cheapening of USD funding costs. We do not question fundamentals in the region, but vigilance in risk management is necessary.