Secondary havens sought amid uncertainty

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 4 minutes

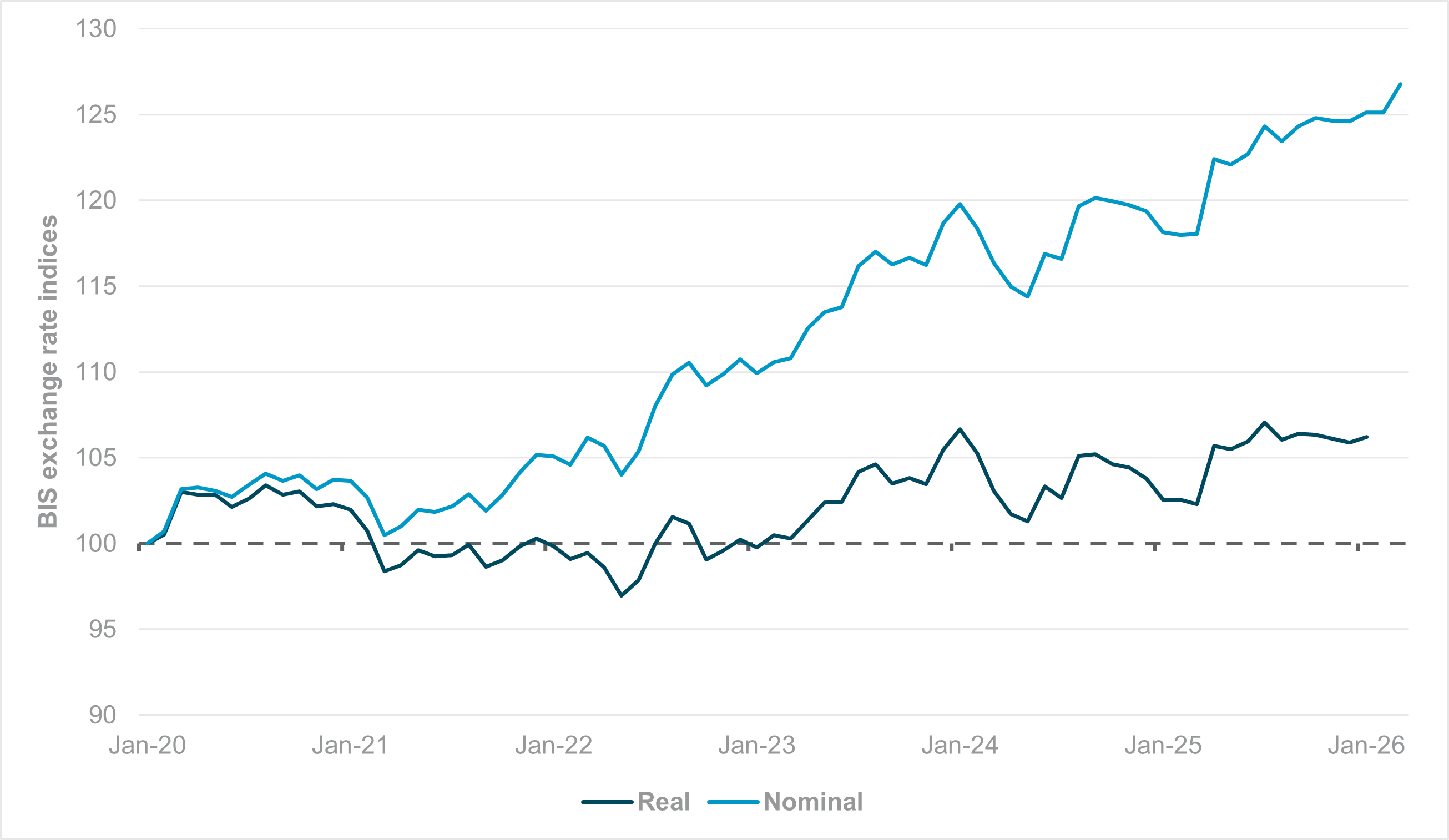

EXHIBIT #1: REAL VS. NOMINAL EFFECTIVE EXCHANGE RATE – SWISS FRANC

Source: BNY, Bloomberg, Bank for International Settlements (BIS)

Our take

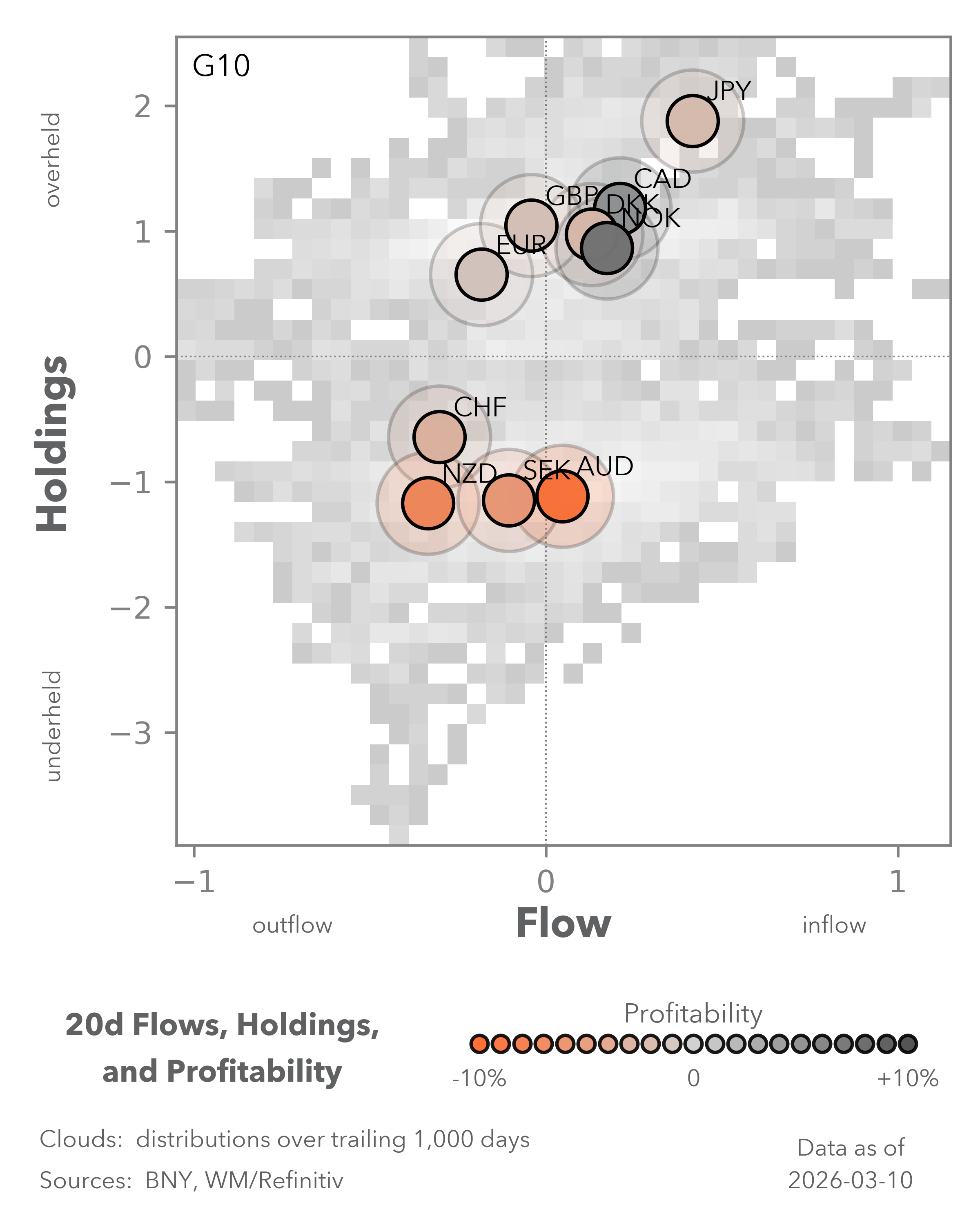

On March 2, the Swiss National Bank warned that it was “increasingly prepared to intervene” in FX markets, citing the conflict in the Middle East. The bank appeared to be anticipating rapid currency appreciation and strong safe-haven inflows that could jeopardize price stability. In our view, this was initially effective – iFlow identified significant CHF outflows during the first few trading sessions of last week. However, more recent price action, particularly in EURCHF, suggests that diversification into the franc is ongoing, in light of concerns about inflation and real rates growth in the Eurozone.

Forward Look

Given the franc’s close eurozone trade links, pass-through can be swift which tends to increase the SNB’s tolerance for nominal franc strength. Higher eurozone inflation will raise the euro’s real effective exchange rate (REER) relative to the franc, especially as inflation differentials remain wide, compounding over the past few years. This will open up greater SNB tolerance for franc appreciation. We can see that on a nominal basis, the franc is moving toward new highs, though there hasn’t been much movement in the currency’s REER over the past two years. Furthermore, during the 2022 to 2023 cycle, the SNB moved ahead of the European Central Bank in Q2, which suggests the SNB is willing to move proactively in both directions.

We expect the SNB to adopt a more tactical approach at its meeting next week. There is also scope for some unwinding of liabilities, such as buying back bills or not rolling out repurchase agreements. We would not rule out any market activity if the nominal move is severe, such as several big figures within a single session. However, such activities should be viewed only in a volatility smoothing context in response to events, rather than carry much policy information for the broader cycle.

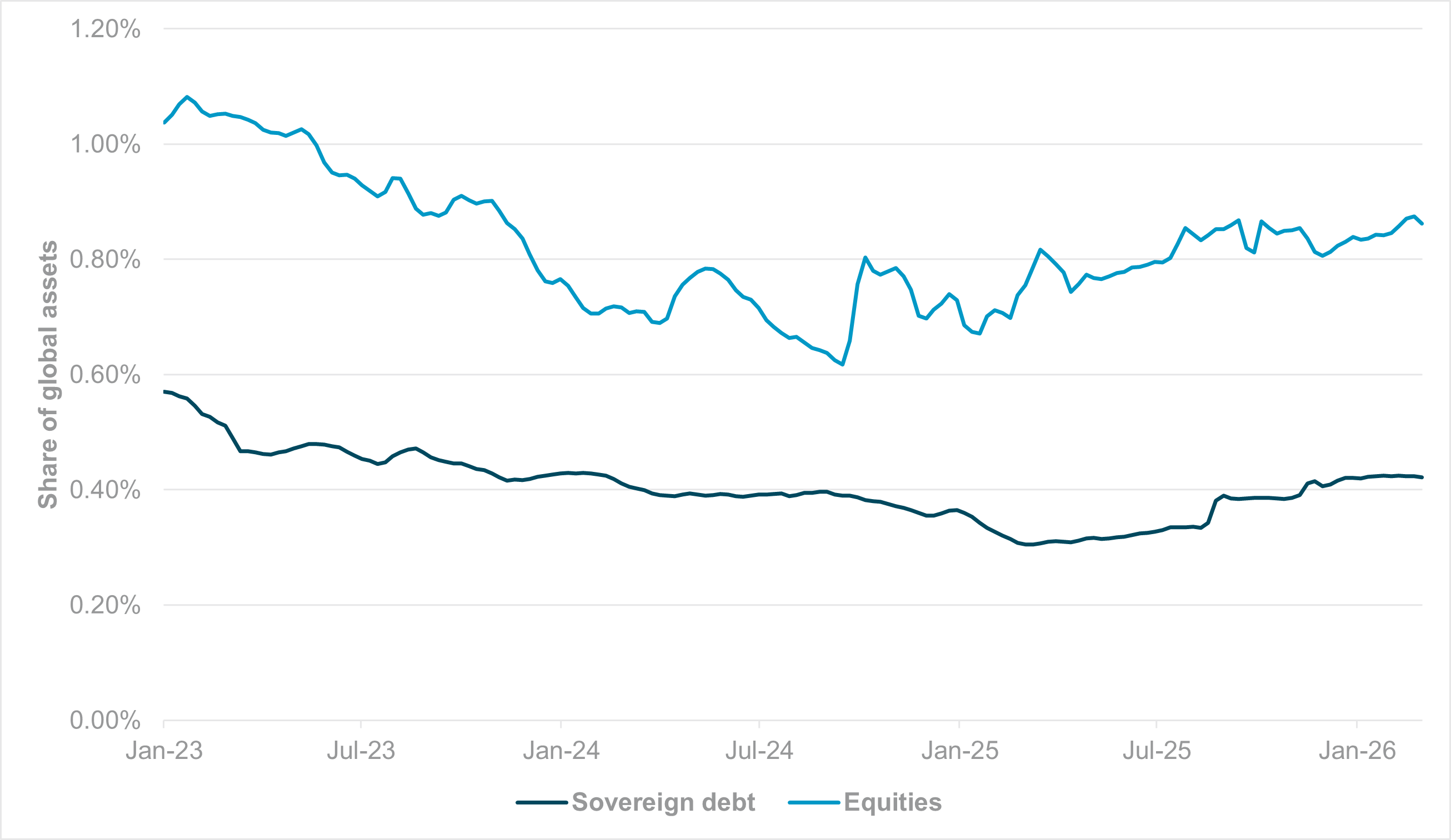

EXHIBIT #2: HOLDINGS GAP IN BRL AND BRAZILIAN EQUITIES

Source: BNY

Our take

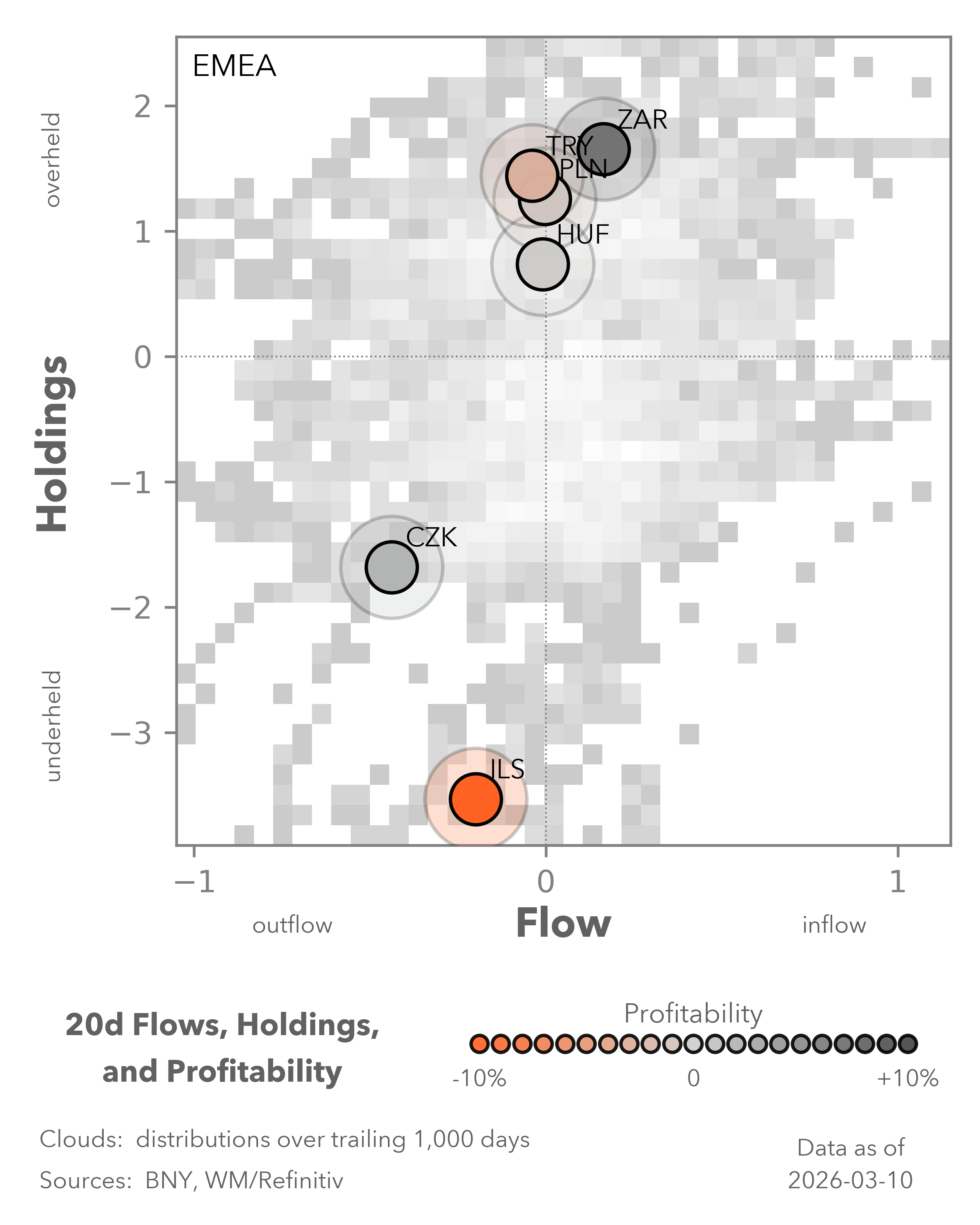

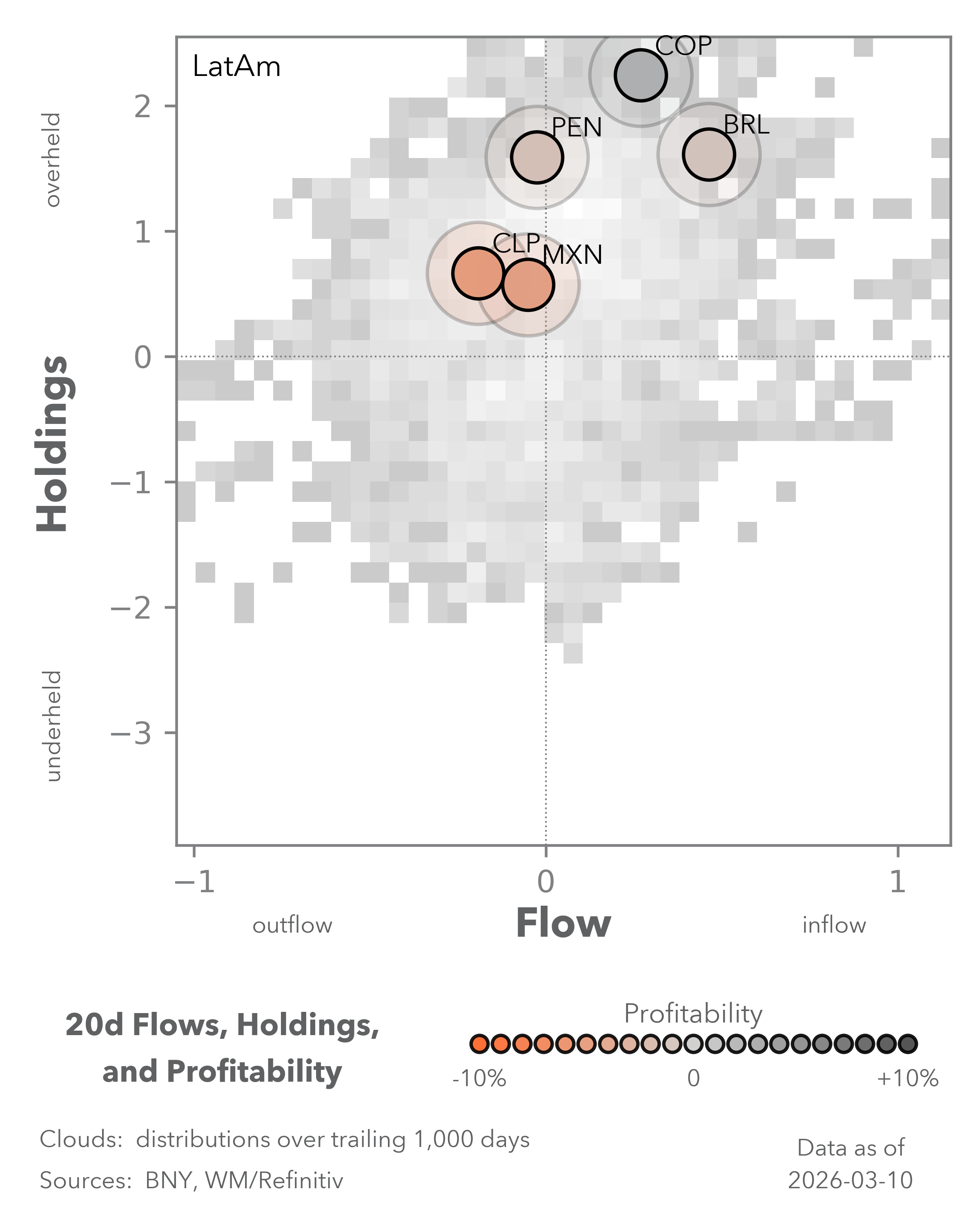

The FX carry complex continues to fade as the conflict drags on. So far, however, the biggest outflows have materialized across Eastern Europe, the Middle East and Africa, especially in currencies and fixed income. The LatAm region, by virtue of geography and resource exposures, has largely been shielded from strong outflows.

Reports this week suggest that premiums are even rising for available oil in Brazil, up to $13/bbl above current benchmarks. For now, commodity-exporting LatAm economies will probably avoid a strong terms-of-trade shock, but high real rates are needed to maintain currency resilience, especially as the U.S. dollar’s interest expectations are starting to shift. Within emerging market fixed income, Chile and Colombia are the standout performers.

LatAm currencies and equities are facing greater downside risk due to a strong holdings start to the year, but figures still look strong on an aggregate basis. This is largely due to resilience in Brazilian assets, where outperformance relative to regional peers strengthened significantly since the end of February (Exhibit #2).

Forward look

If the BRL and commodity-exposed Brazilian assets are now seen as the regional haven, then there may be a case for Brazil’s central bank, COPOM, to calibrate communication slightly at next week’s policy decision. A 50bp cut to 14.50% is expected. Even with such a move, real rates will remain comfortably in the double digits and help anchor the exchange rate. Duration may also start to perform better if Brazil emulates its fiscal discipline it showed during and after the COVID pandemic, avoiding excessive stimulus. On the other hand, if external flows have helped limit the tightening in financial conditions, the global inflation environment warrants greater caution in easing. LatAm economies have similar qualities that help shield the region from global stress. However, caution is also settling in, and we doubt Brazil can continue its current divergence from neighboring economies.

EXHIBIT #3: POSITIONING IN CHINESE GOVERNMENT BONDS AND EQUITIES

Source: Bloomberg, BNY

Our take

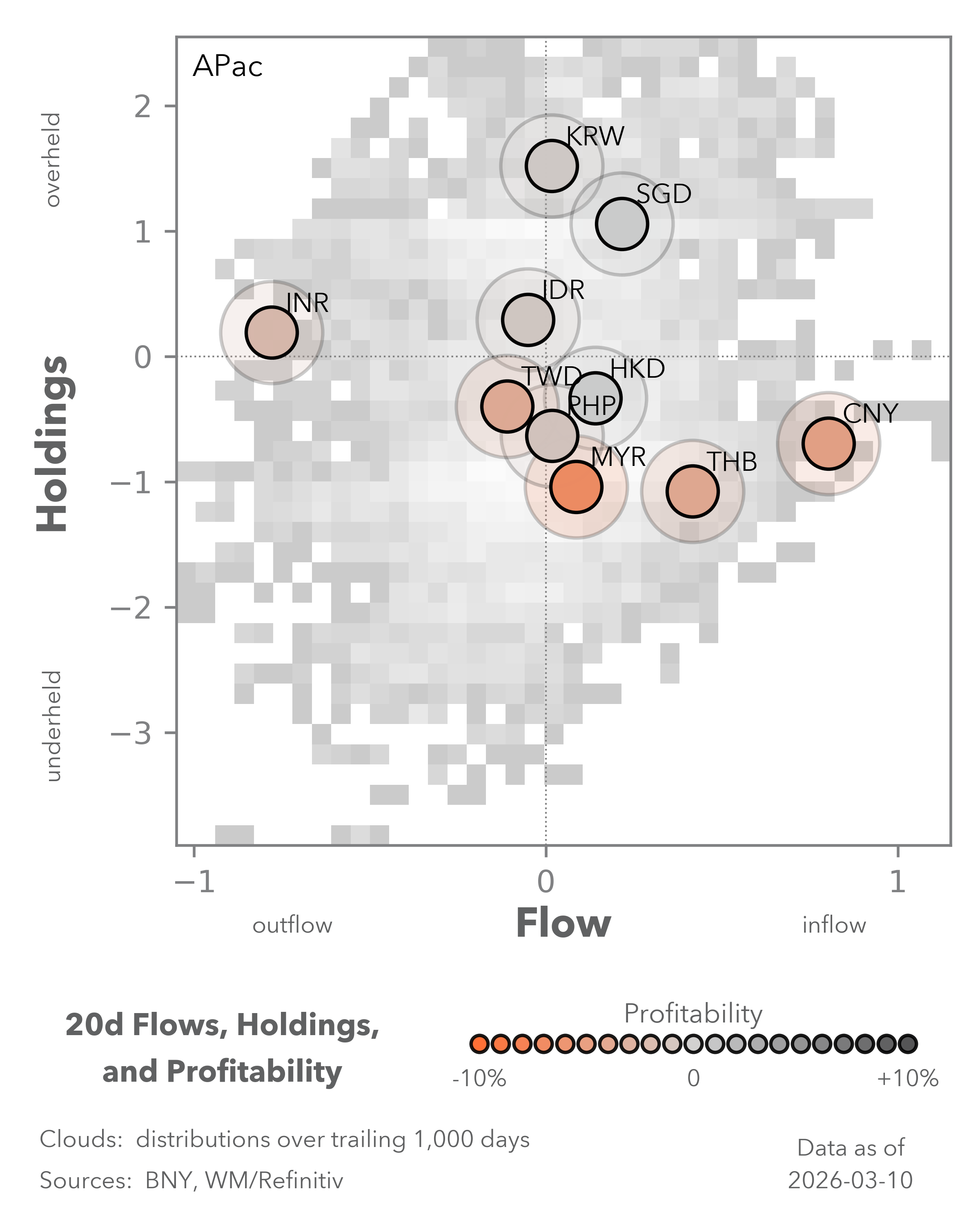

One of the most surprising flow patterns we have observed since the conflict began has been a surge in CNY buying that cannot be attributed to hedge unwinding. Hedging levels in the currency are now around 30% below the rolling 1y average, suggesting that underheld positions have been removed. Asset values have also held up well, particularly in equities. At the beginning of the year, we made the case for gradual appreciation of CNY, in addition to valuation adjustments in other high-surplus APAC currencies. In the near term, all such surpluses are at risk from energy bottlenecks, but China is less exposed than peers in North and East Asia. A low starting point for inflation is also helpful in a supply shock.

Careful official CNY management will also limit realized volatility, which will be viewed favorably in the current environment. Broader APAC appreciation to limit pass-through disinflation is possible, but excess asset positioning in the likes of South Korea and Taiwan is probably necessary first.

Forward look

The lack of such holdings extremes may be one reason why the CNY is also doing relativity well in the current environment. Chinese equity markets were not seen as a direct proxy for the AI trade, so there were not the same concentrated foreign inflows that have contributed to recent volatility. Over the long term, provided greater access and capital market reform continues apace, we expect Chinese assets to attract improved allocations within diversified global portfolios. However, this need not come at the expense of U.S. assets. Our positioning data show that Chinese equities and fixed income shares of portfolios remain below 2023 levels at the beginning of China’s post-pandemic reopening, with CGBs at just above 0.8% at present and Chinese equites around half that level (Exhibit #3). Overseas interest can pick up significantly, further supporting the CNY, but the base is too small to meaningfully affect overall U.S. portfolio allocations.