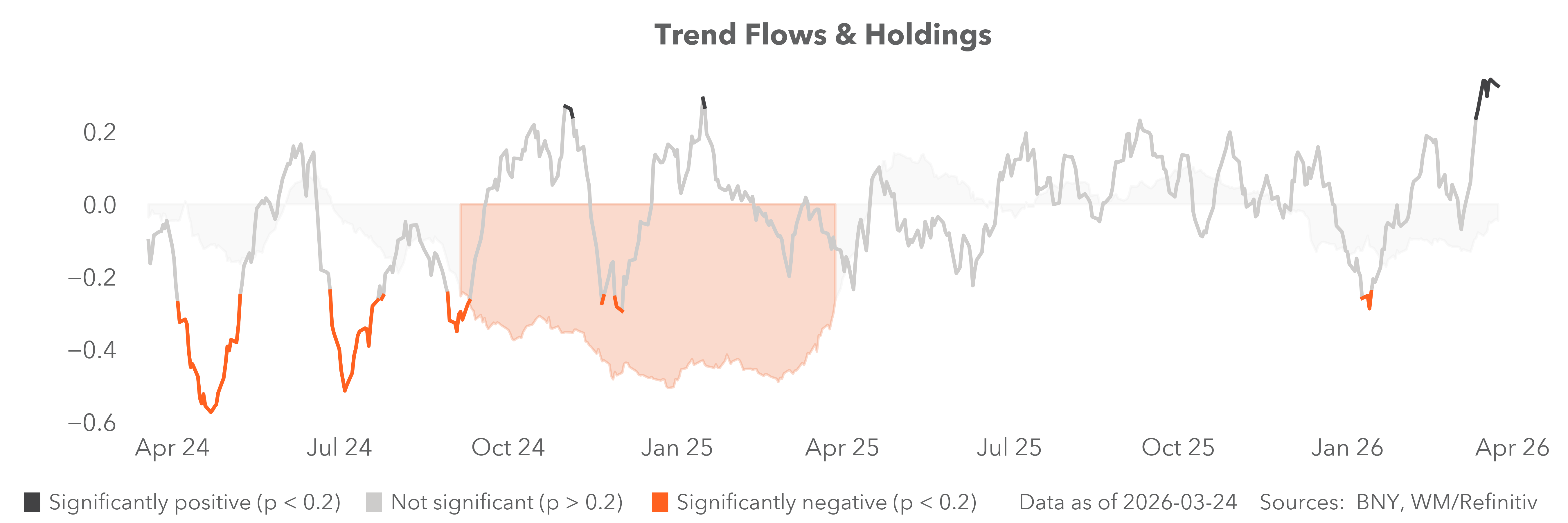

Inflation makes its mark on valuations

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

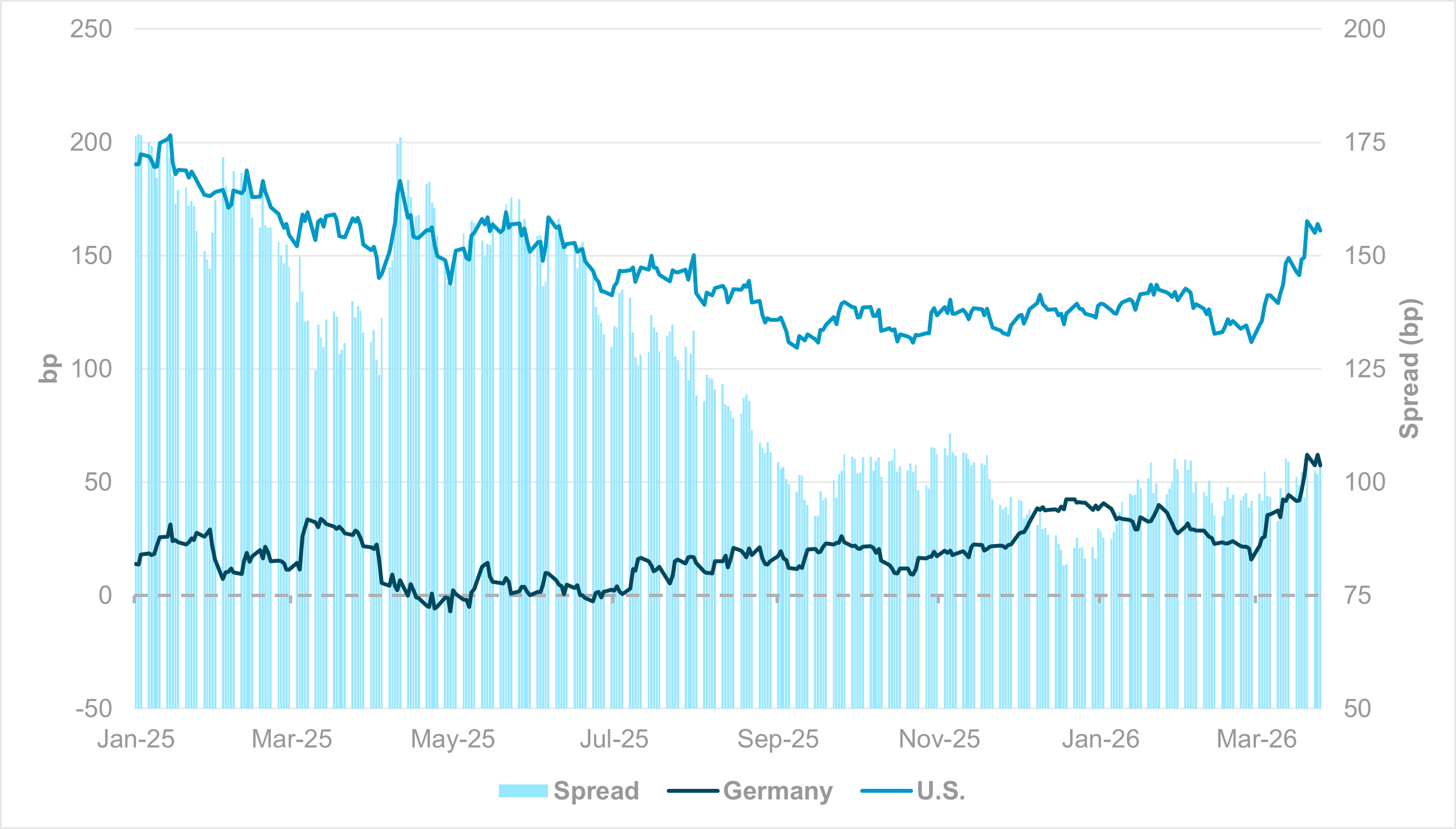

EXHIBIT #1: 5Y YIELD (GERMANY AND U.S.) DEFLATED BY 5Y5Y INFLATION SWAP

Source: BNY

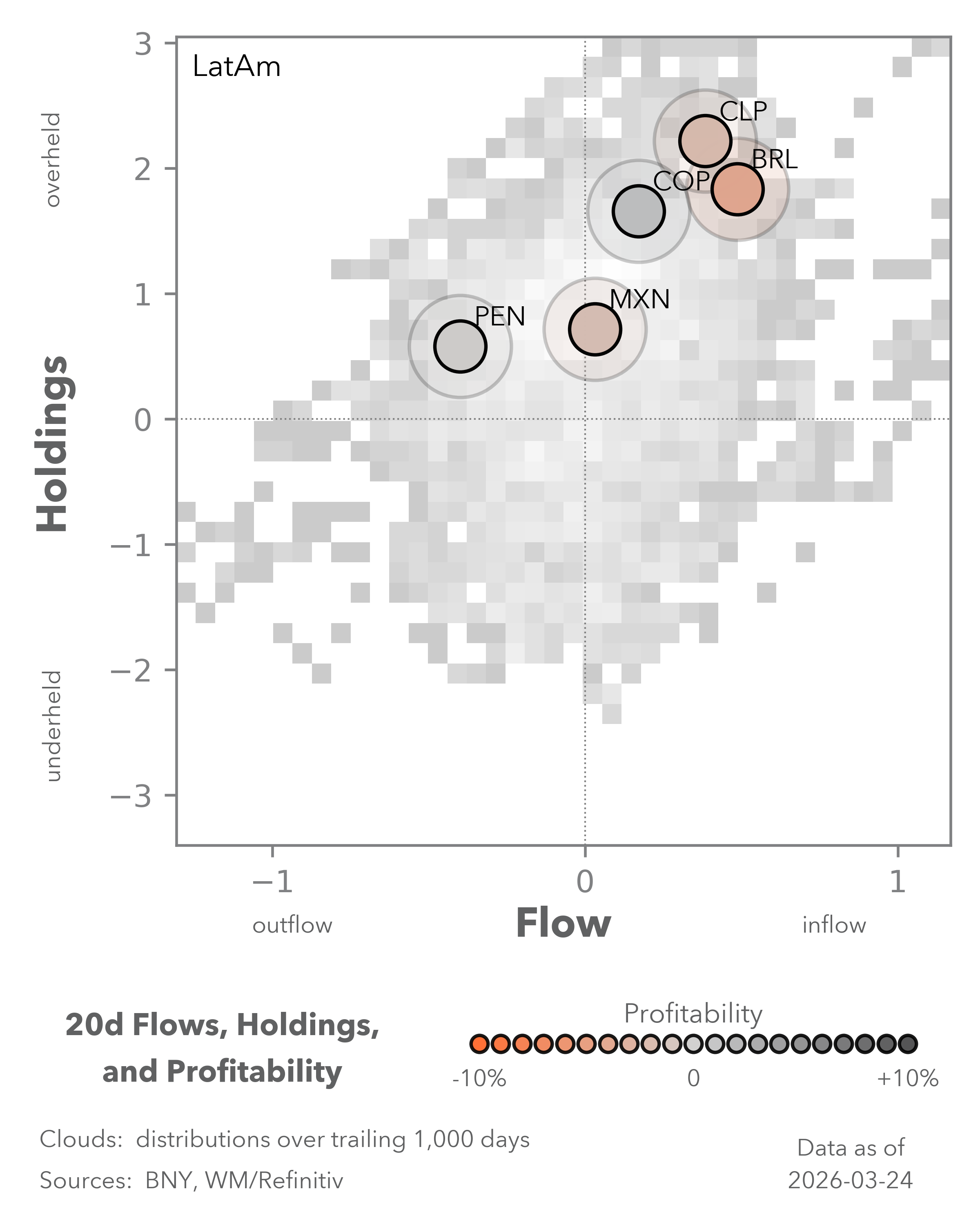

Our take

Even after news of potential peace talks boosted risk sentiment and pared back market expectations of aggressive tightening – especially in Europe – we believe that most central banks will refrain as much as possible from tightening. This week’s keynote speech by ECB President Christine Lagarde fully places the burden of proof on hiking, rather than not hiking. Although the latest European PMIs point to upward pressure on input costs, central banks won’t act until second-round effects become clear. Even hawks such as the Bank of England’s Megan Greene have highlighted that downside risks to demand are greater compared to 2022, and households and firms are “more aware” of inflation risks and will respond swiftly with restraint. This is why we have seen strong inflows into bond markets, as real yields have increased materially due to well-anchored, long-term inflation expectations. German real rates are now above 2025 highs. Backed by a solid credit rating, these levels should attract very strong demand from domestic and international investors seeking to lock in rates above 100bp. U.S. real rates are traditionally higher due to structural factors, and real rates have risen but remain around 25bp below January 2025 highs.

Forward Look

While we acknowledge that the market will always be more partial to higher USD real rates, the move in European equivalents is stronger, which will serve as a buffer against further dollar strength for now, especially if safe-haven demand has peaked. The U.S. growth cycle and other idiosyncratic factors, including its status as a net energy exporter, have kept the pricing of hikes comparatively muted, thereby limiting any knock-on effect on the curve. Consequently, the spread between U.S. and European real rates has kept to the tight range seen over the last six months. Dollar hedging may have come off due to haven interest, and we don’t expect a return to the pre-conflict status quo. Nonetheless, the dollar is currently not making a case for a broader recovery based on nominal or real rates. The market will likely wait to see where real rates settle as the growth impact from the conflict becomes clearer over time.

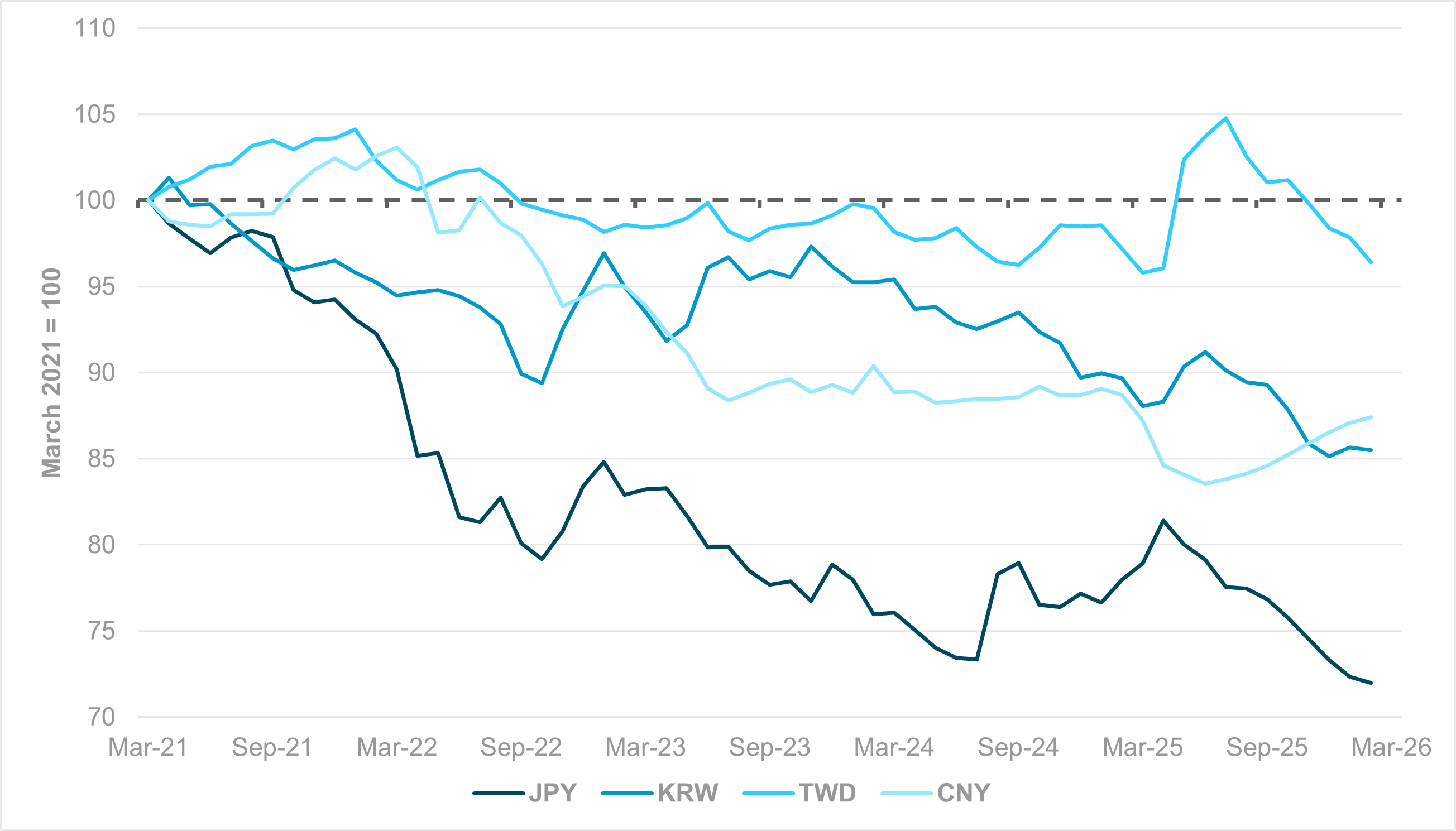

EXHIBIT #2: REAL EFFECTIVE EXCHANGE RATES (REER) – CNY, JPY, KRW AND TWD

Source: BNY

Our take

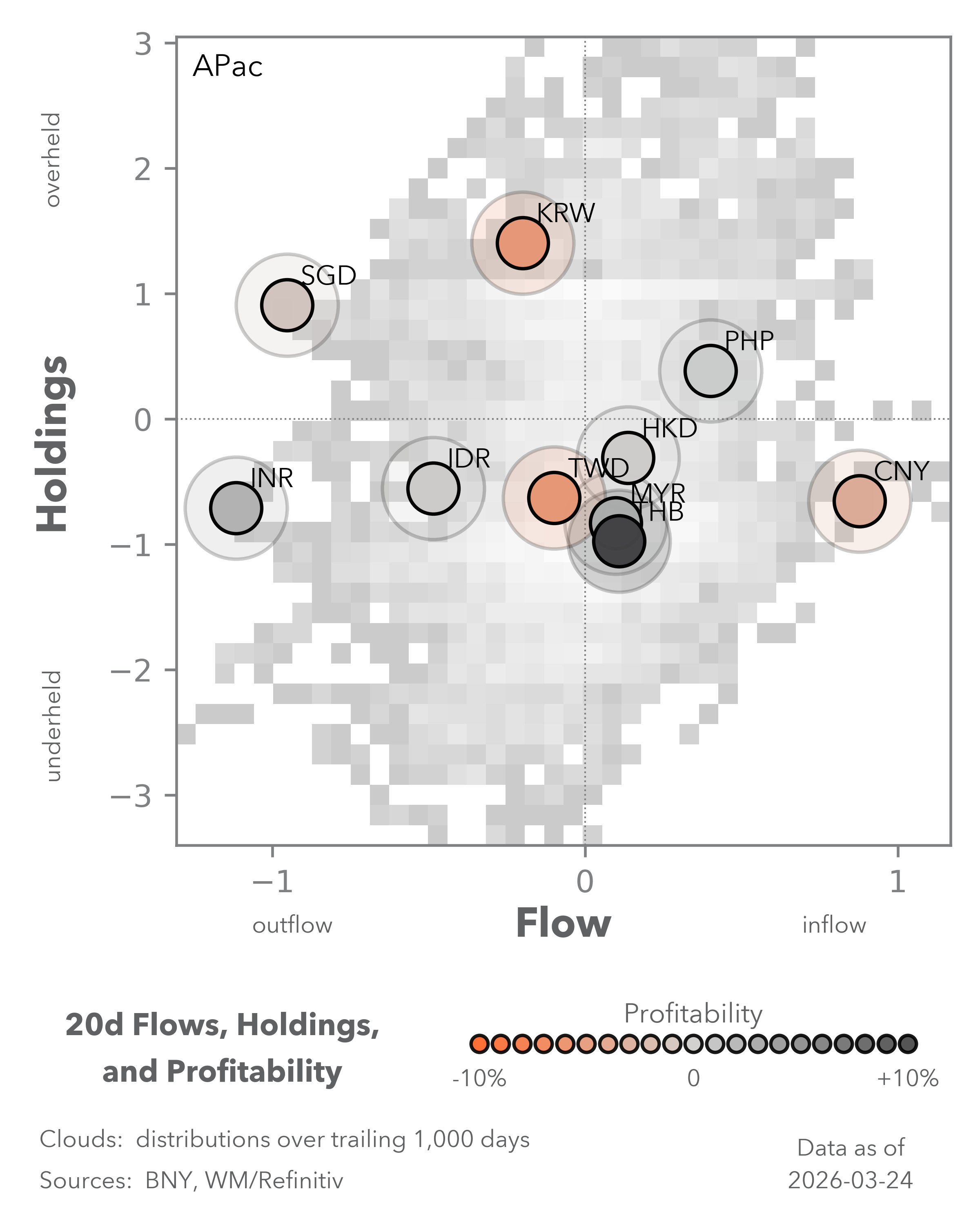

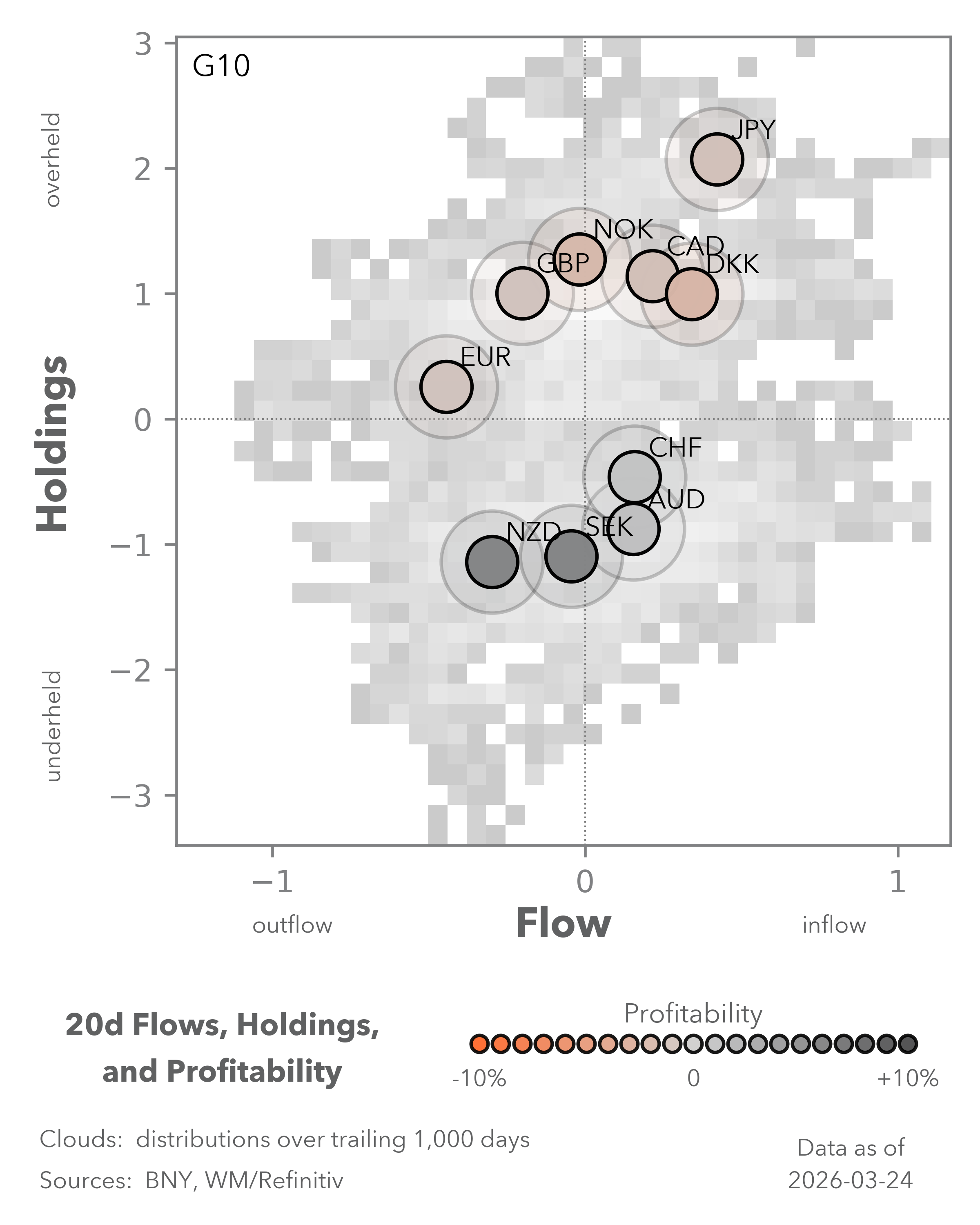

Despite reports of ample energy reserves, North Asian economies and currencies continue to face supply-related risks to their balance of payments. Although some fiscal resources to limit energy price gains will be deployed, headline inflation will likely rise in the near term, and central banks will need to respond accordingly. However, we believe there are structural differences compared to Europe, where markets are equally fearful of stagflation. Japan aside, and only recently for that matter, wage growth in these economies has been very low. In contrast, developed market partners have seen sticky wages driving inflation, thereby leading to price differentials that are heavily depressing APAC real effective exchange rates (REER). Meanwhile, low front-end rates have also limited gains in nominal effective exchange rates, and domestic asset pools have been keen to invest in the U.S. to take advantage of high-growth themes. A renewed global supply-based inflation push represents an opportunity to shift mindsets. These economies in particular can withstand higher REERs through the inflation channel.

Forward look

Out of the four north Asian currencies in this group, JPY remains the most undervalued. The recent wage round in Japan settled at above 6% wage growth. If repeated across the broader economy, where wage growth has been slowing prior to the conflict, this momentum should help generate a buffer against the USD and EUR in real terms. The risk – as highlighted by European policymakers – is that second-round effects prevail very quickly, leading to renewed upward wage pressures in the region, even though there is much greater demand restraint. Even if wages merely stabilize rather than grow, there will be greater scope for inflation to “do the work” for north Asian currencies, as inflation differentials will provide a wider buffer that either nominal effective exchange rate adjustment or higher domestic inflation can help close. The bottom line is that within the region, high-savings APAC economies should not fear above-target inflation – especially if it translates into wage growth – as traditional competitiveness fears are overdone given current valuation gaps.

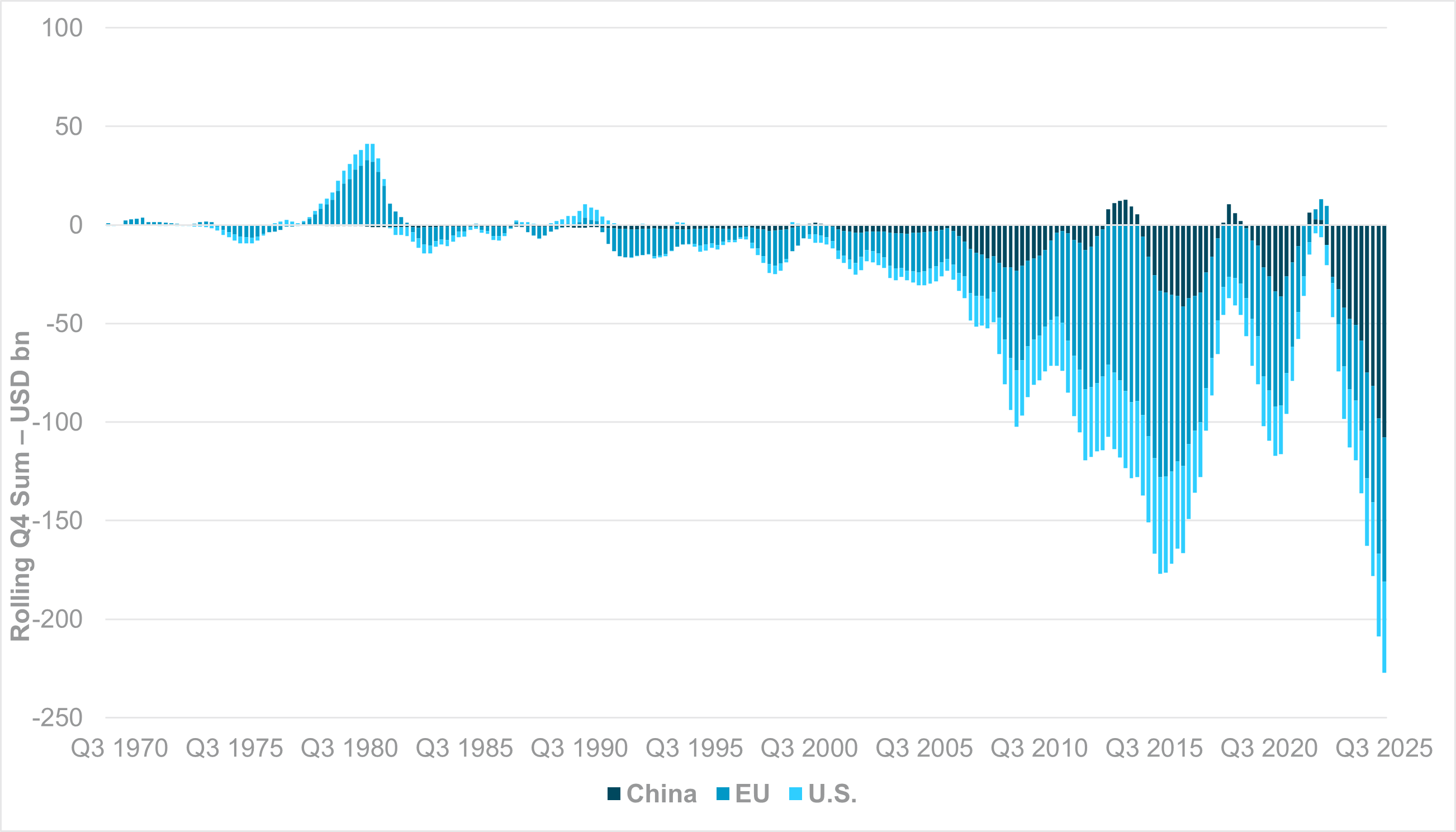

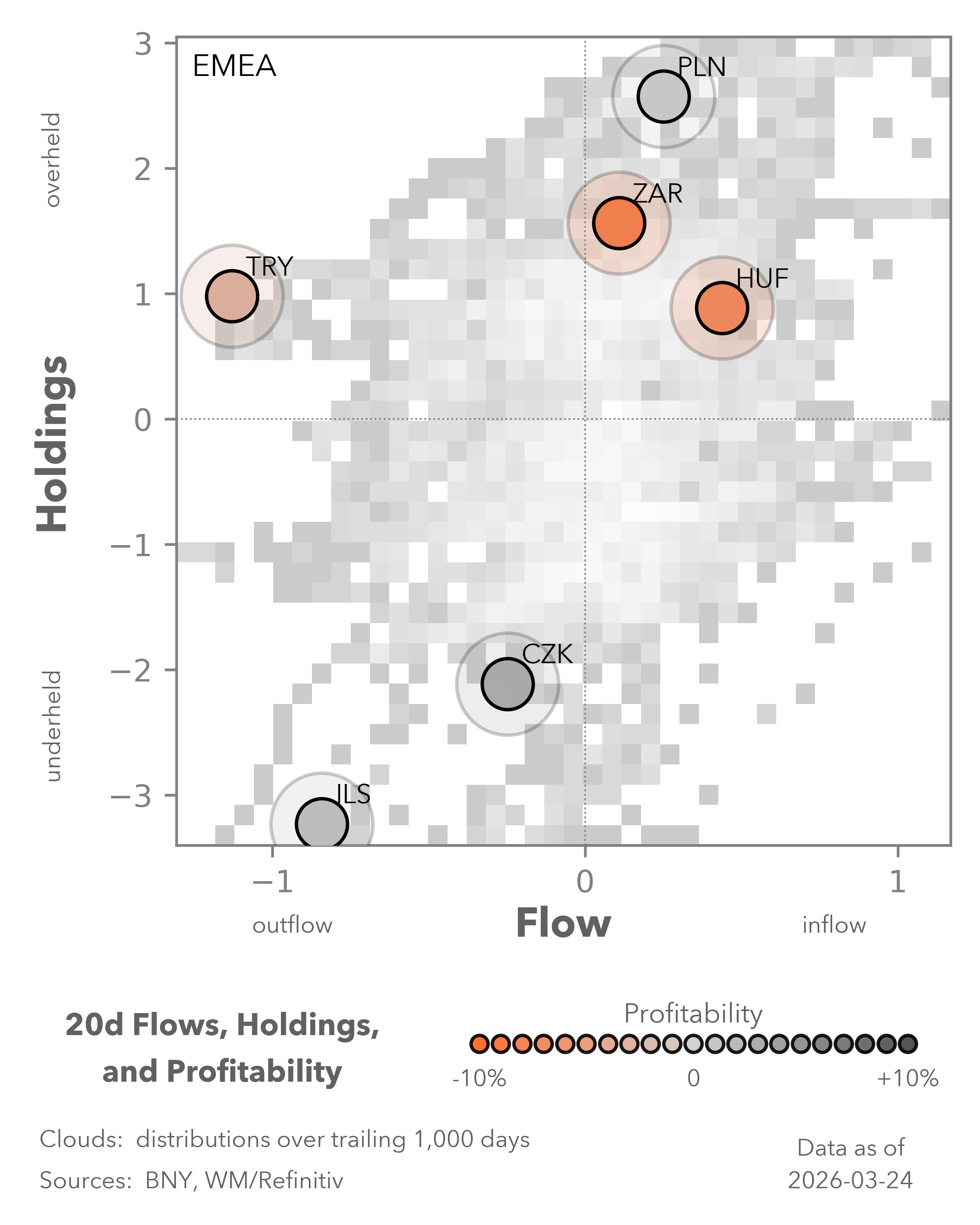

EXHIBIT #3: MIDDLE EAST TRADE BALANCE WITH CHINA, EU AND THE U.S.

Source: Bloomberg, BNY

Our take

Although the market’s current balance-of-payments focus is squarely on net energy importers – both in developed and developing markets – the impact on Gulf economies will also need to be assessed in time. This is especially true if the disruption to oil supplies is prolonged, with direct consequences for energy-related revenues. For global asset markets, the immediate focus will likely be on these countries’ financial accounts. Buoyed by strong surpluses accumulated from 2022 to 2023, these countries have invested heavily globally and contributed to the global easing of financial conditions, especially with vast financial resources being channeled into U.S. tech firms as part of the artificial intelligence theme. We expect investment priorities to change ahead: lower near-term revenues will reduce accumulation of overseas liabilities in general, while any remaining resources will likely be spent on defense and reconstruction. Global asset markets should even watch out for some liquidation of investments by sovereign entities in support of such efforts.

Forward look

Gulf countries have also been ramping up domestic investment in infrastructure and other projects over the last few years, which means that the region is currently running a deficit (Exhibit #3), especially since oil prices fell materially from 2022-2023 highs. On a four-quarter rolling sum basis, the combined trade deficit between the Middle East and China, the EU and U.S. combined has surpassed $200bn. All three economic entities have stepped up exports of highly value-added goods to the region. Much as we expect on the capital account side, there will likely be a shift in priorities that reshapes trade dynamics with core economies. While China, the EU and the U.S. are large and diversified enough to withstand some degree of demand retrenchment, other economies and currencies will struggle more. We would be particularly attentive to countries where remittances from the region are also essential to their balance of payments, as valuation discounts will open up if labor demand falls or becomes more selective.