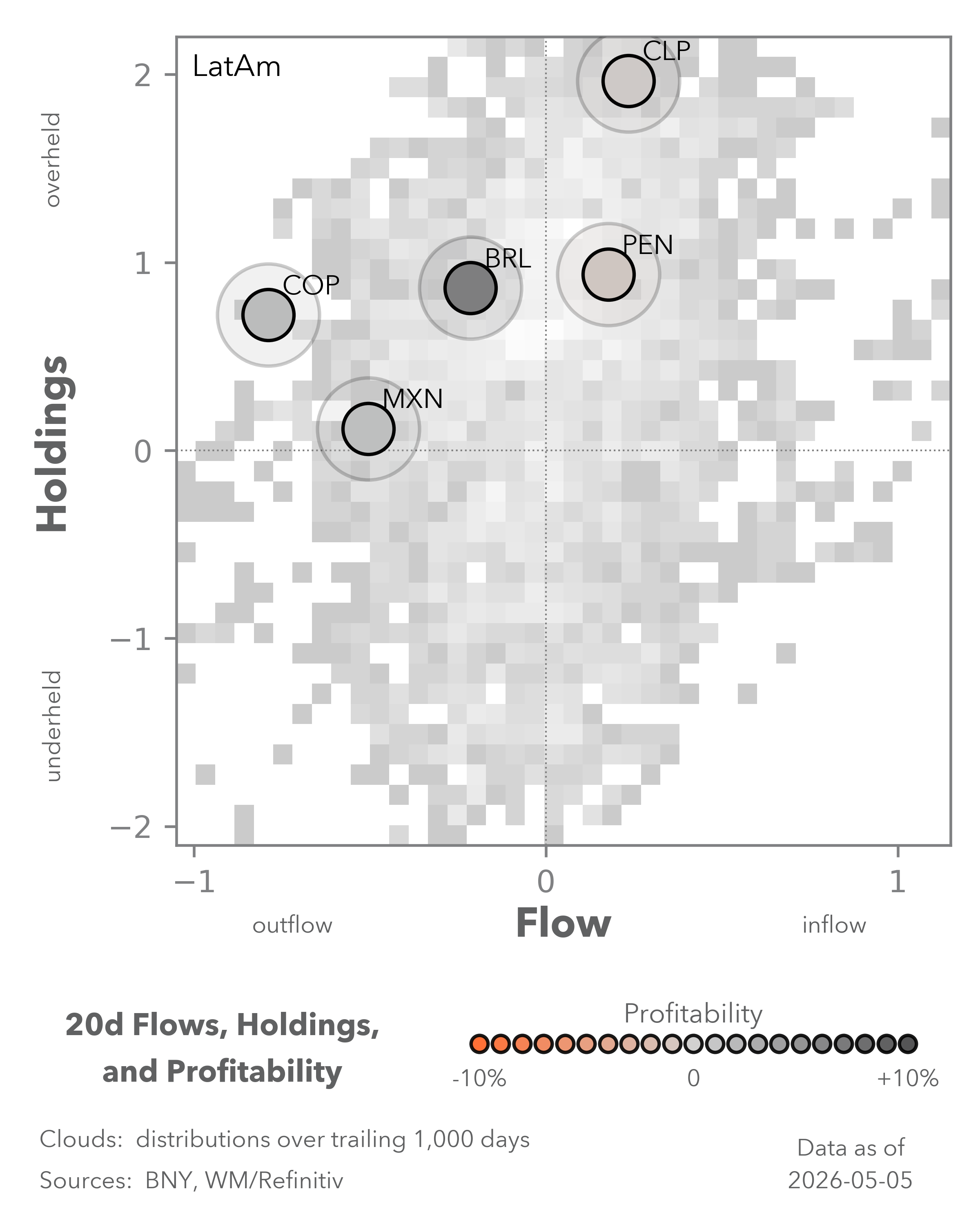

Fiscal premia manifest in different ways

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 4 minutes

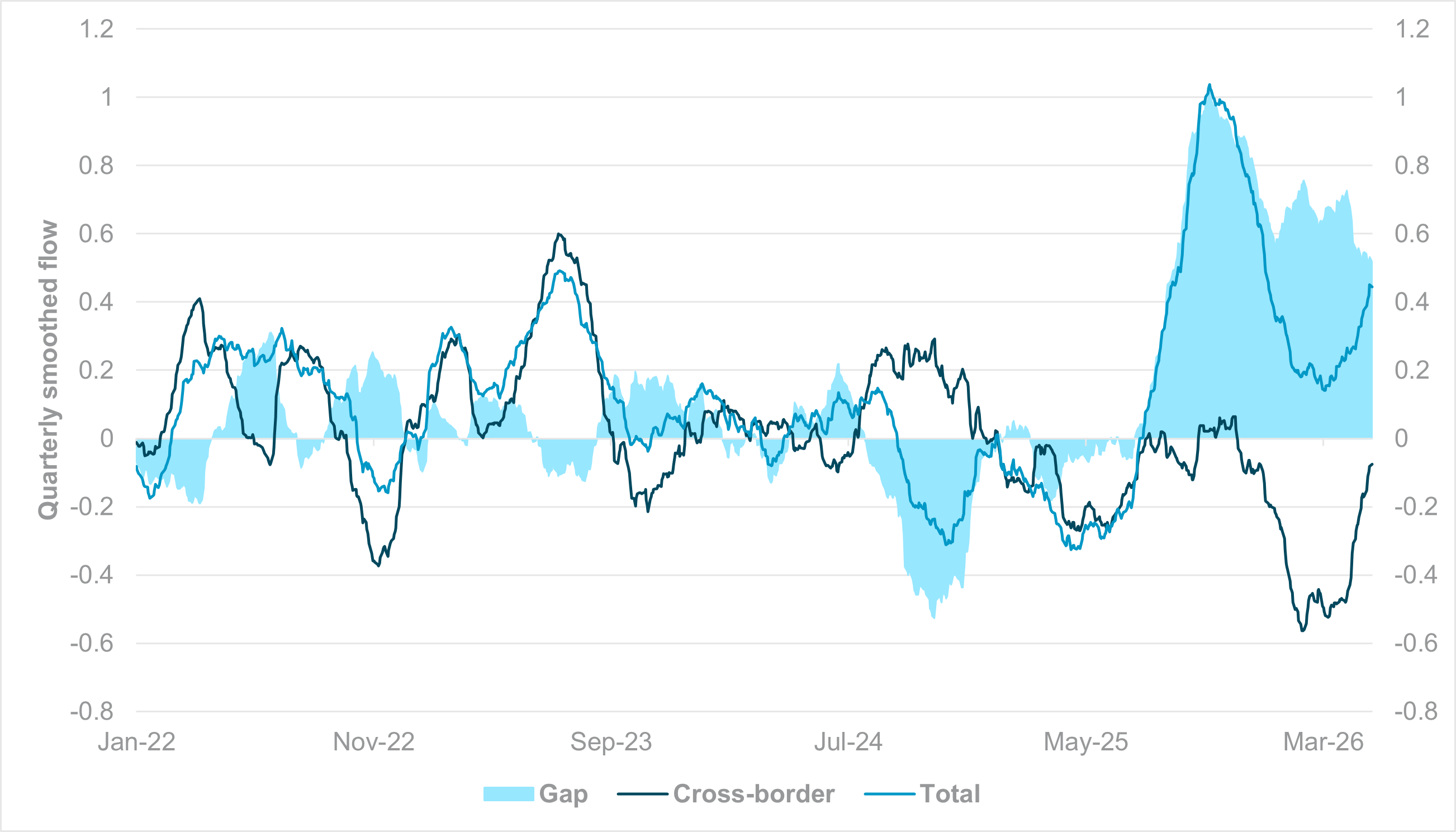

EXHIBIT #1: QUARTERLY SMOOTHED FLOW INTO GILTS, FOREIGN VS. DOMESTIC INVESTORS

Source: BNY

Our take

Wednesday’s rally in global government bonds, driven by rising hopes for a permanent settlement in the Iran conflict, came as a considerable relief to European governments and central banks. Earlier in the week, fears of a more prolonged inflation shock led to markets pricing in an ECB rate hike in June, while U.K. 30y borrowing costs reached their highest levels in nearly three decades. If we assume that inflation premia will be reduced across European government bond curves, then fiscal premia will return to the fore, and this is where the challenges for the gilt market will be more pronounced. Depending on local election results, markets are pricing in policy uncertainty, with most scenarios tilting toward a stronger fiscal impulse. Even if fiscal loosening is the outcome, we don’t foresee an impact along the lines of the 2022 minibudget shock, and GBP’s downside may be more contained this time.

Forward Look

The debates around Bank of England policy, the growth cycle and real rates are well-trodden ground. In terms of market structure, the biggest change is ownership composition. Our data indicate that aggregate gilt demand is at its highest levels in years – yet gilt selling by cross-border investors also hit multi-year highs (Exhibit #1). There is currently a significant holdings gap between onshore and offshore investors, and we believe the lack of a GBP drag despite higher bond yields points to a lack of exits by international investors. Ownership levels are low, and selling in March was driven by the need to source immediate dollar liquidity rather than a specific U.K. story. If the months ahead point to a need to add to U.K. fiscal risk via gilts, cross-border institutional investors likely do not have the scale to do so.

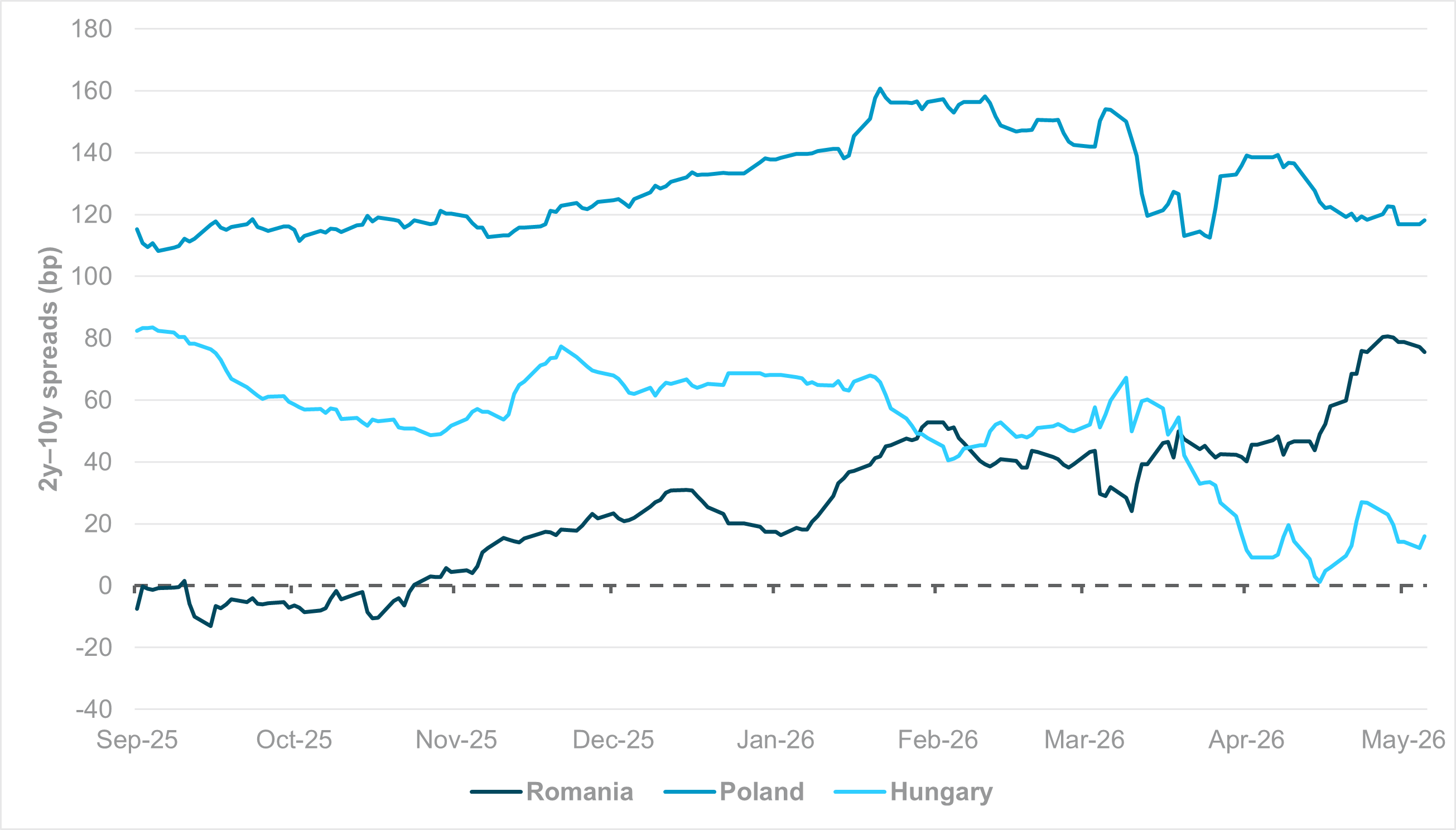

EXHIBIT #2: 2Y–10Y GOVERNMENT BOND YIELD SPREAD FOR CEE ISSUERS

Source: BNY, Bloomberg

Our take

In the near term, the fiscal stress points with the greatest FX implications are in Central and Eastern Europe (CEE). Despite our hopes for a more assertive approach, no regional central bank appears willing to push for higher rates. As in the U.K., the inflation angle will likely prove transitory, and fiscal is the bigger threat to inflation expectations. The recent collapse of the Romanian government points to significant short-term fiscal uncertainty, which is potentially destabilizing for a currency with materially low real rates and very high twin deficits – both nearly hit 8% of GDP as of Q4 2025.

Poland and Hungary’s fiscal trajectories are also approaching high single-digit percentages of GDP. However, both have seen notable current account improvements over the past two years, and inbound FDI and current transfers – particularly for Hungary post-election – provide a better sustainability profile.

Forward Look

External circumstances have determined common near-term inflation pressures in the region. However, further fiscal divergence is expected, which should be reflected in currency flow and holdings. Tracking the 2y–10y yield spread as a proxy for long-term fiscal sustainability, Romania has seen the biggest gains recently, with outright yields are also running higher than for Poland and Hungary. Romania’s curve was flatter before markets fully priced in the Hungarian election outcome – and indeed in the early days of the U.S.–Iran conflict. Anticipating euro entry before maturity has reduced term premia, but current financing gaps are so extreme that there was likely some mispricing, particularly considering iFlow indicated RON was comfortably overheld until very recently.

Meanwhile, the Hungarian curve has almost fully flattened out as global assets rush in after the election. EU funding support is also helping reduce risk premia, but even the Magyar Nemzeti Bank’s governor has warned against excessive asset performance. It’s looking increasingly like too much, too soon.

Poland’s size and economic integration with larger economies, especially through FDI, suggest that the current steepening looks excessive. We continue to believe productivity gains and a stable current account mean fiscal trajectories can be corrected in time. Any residual risk premia should be reflected in softer FX holdings rather than an excessively steep curve.

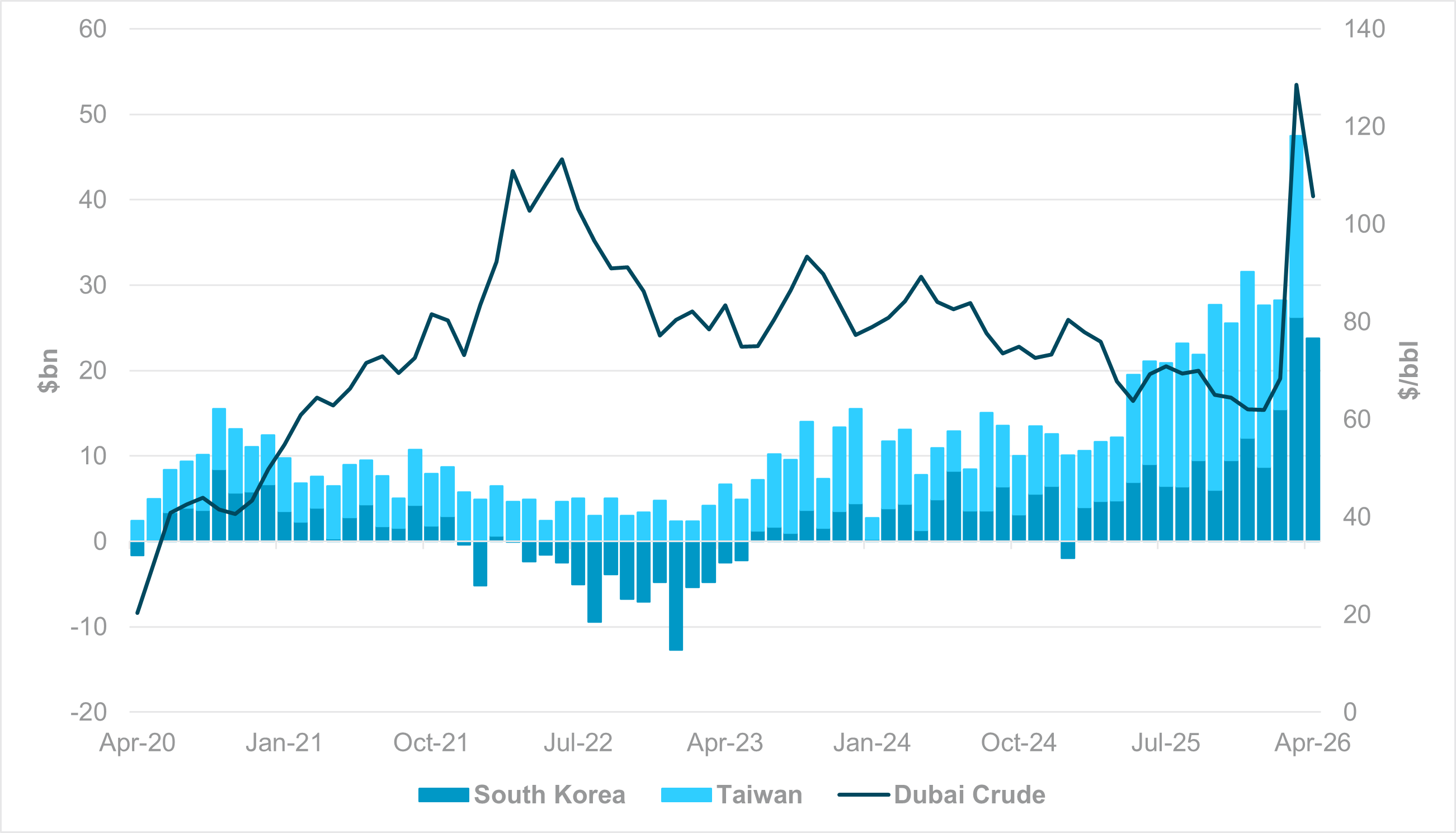

EXHIBIT #3: COMBINED SOUTH KOREA AND TAIWAN TRADE BALANCE VS. DUBAI CRUDE

Source: BNY, Bloomberg LP

Our take

South Korean equities rallied by almost 7% on Wednesday alone as foreign investors rushed to access the market as a direct proxy for the global semiconductor trade. Valuation concerns around this theme will continue to challenge performance in South Korean and Taiwanese equities. We also acknowledge supply-side risks to the semiconductor industry in both economies, given their heavy dependence on imported inputs. We can see that the oil price surge in 2022 had a material impact on balance of payments, with South Korea running a sustained deficit until the second half of 2023 (Exhibit #3). This March, the price surge coincided with a record combined trade surplus for both economies, even as their central banks ran down reserves to stabilize currencies. This is the macro equivalent of U.S. tech names “letting the earnings do the talking” – both economies are underscoring their resilience to supply shocks. If the oil price decline continues, the positive case is even stronger.

Forward look

We agree that holdings in South Korean and Taiwanese equities are now excessive, but institutional holdings remain below pre-conflict levels and may be forced to participate and chase the retail flow in place. If cross-border flows are increasingly unhedged, currency appreciation may overshoot – a risk that would eventually force a correction. The path for KRW and TWD strength is clear: Japanese authorities are capping USDJPY, and Beijing is openly tolerating further CNY appreciation in both nominal and real effective terms. Even risk aversion is no longer a reason for central banks to hold back the necessary adjustments. If financial conditions tighten strongly through the currency channel, asset volatility could start to rise, but we would consider it a healthy process to reintroduce two-way flow.