Beware of the obvious trade

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 4 minutes

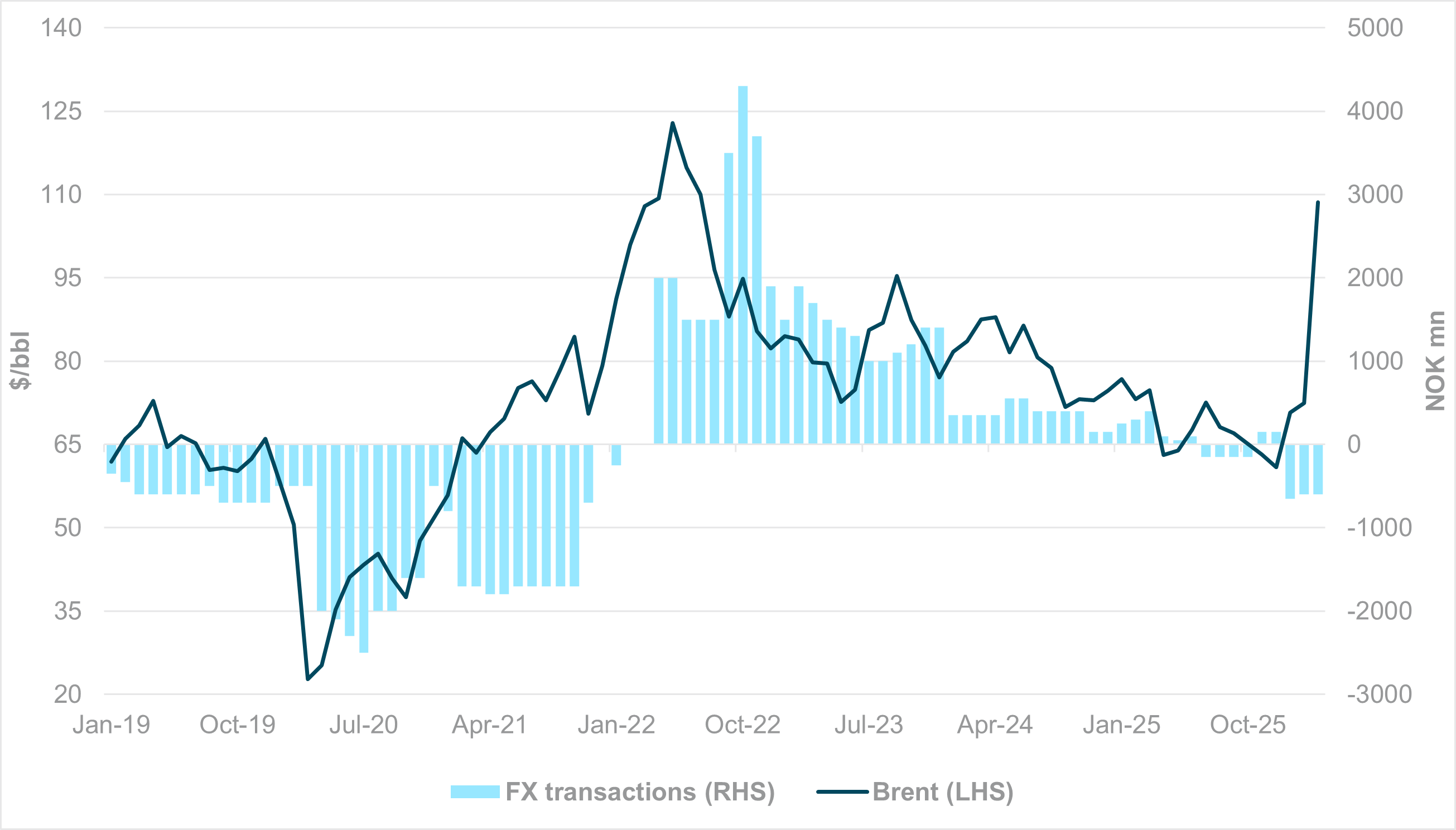

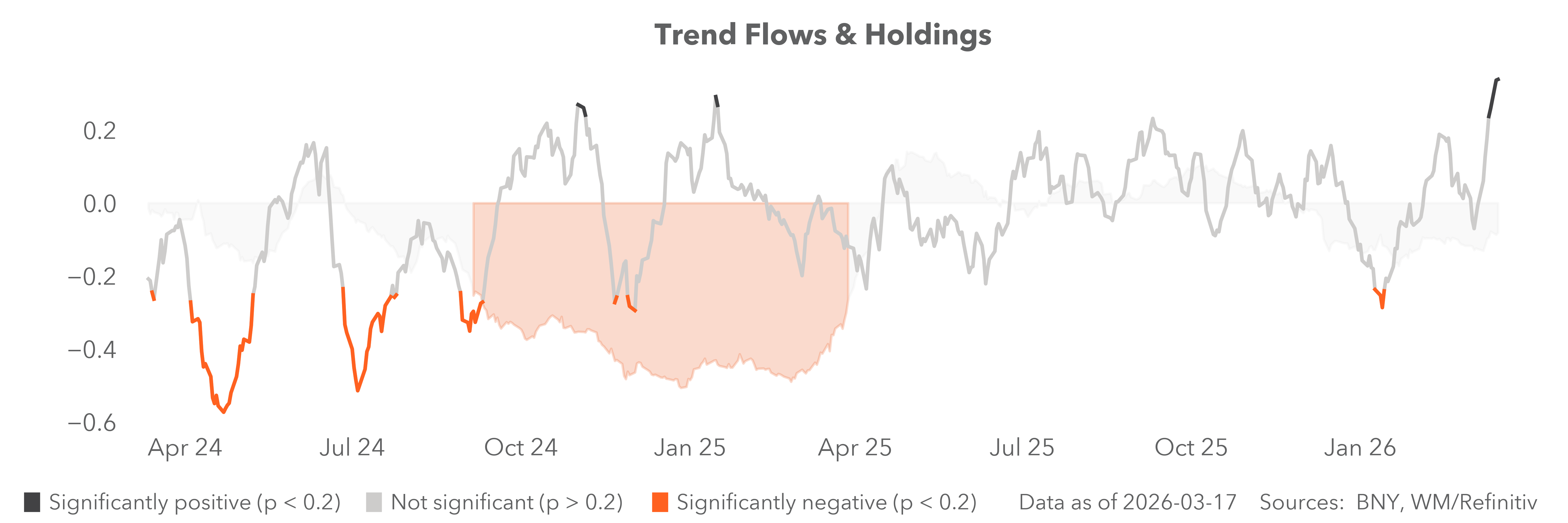

EXHIBIT #1: NORGES BANK FX TRANSACTIONS VS. BRENT

Source: BNY

Our take

As hopes for a swift resolution to the Middle East conflict begin to fade, the market is increasingly adding to defensive strategies. iFlow shows a retreat to traditional safe havens – such as the dollar, Swiss franc, U.S. Treasurys and Bunds – alongside selective positioning in assets that could benefit from a positive, energy-related terms-of-trade shock. In G10 markets, AUD and NOK are the two currencies most favored in this context. Both are large natural gas producers with hawkish-leaning central banks to complement terms-of-trade improvements. Even before the current conflict, the Reserve Bank of Australia (RBA) had resumed tightening, and Norges Bank had all but ruled out rate cuts.

Forward Look

Both currencies could benefit in the near term, and Norges Bank’s view next week will likely resemble the RBA’s – adding to vigilance on the external side while stressing that domestic inflation will remain the key policy driver. We stress, however, that Norges Bank’s FX transactions – marginally positive for NOK now – tend to reverse once energy prices sustain a rally and the initial terms-of-trade adjustment runs its course. High energy prices lead to greater revenues from petroleum activities, which generate sufficient income to meet government spending requirements. Any surplus to the non-oil budget deficit will result in Norges Bank selling NOK and purchasing foreign currency for the Government Pension Fund Global. During the previous energy surge in 2022 to 2023, daily FX transactions hit NOK 4bn – a strong marginal headwind against further NOK appreciation. Furthermore, for a small open economy, positive terms-of-trade adjustments will bring down tradables inflation to the extent that more aggressive monetary paths will prove difficult to realize.

In the past, the main concern driving higher rates was property prices, but central banks are more inclined to use macroprudential measures to calibrate borrowing and lending, rather than use interest rates outright. Without taking a view on the duration of the current energy price surge, we would be wary of excessive NOK positioning based simply on energy receipts.

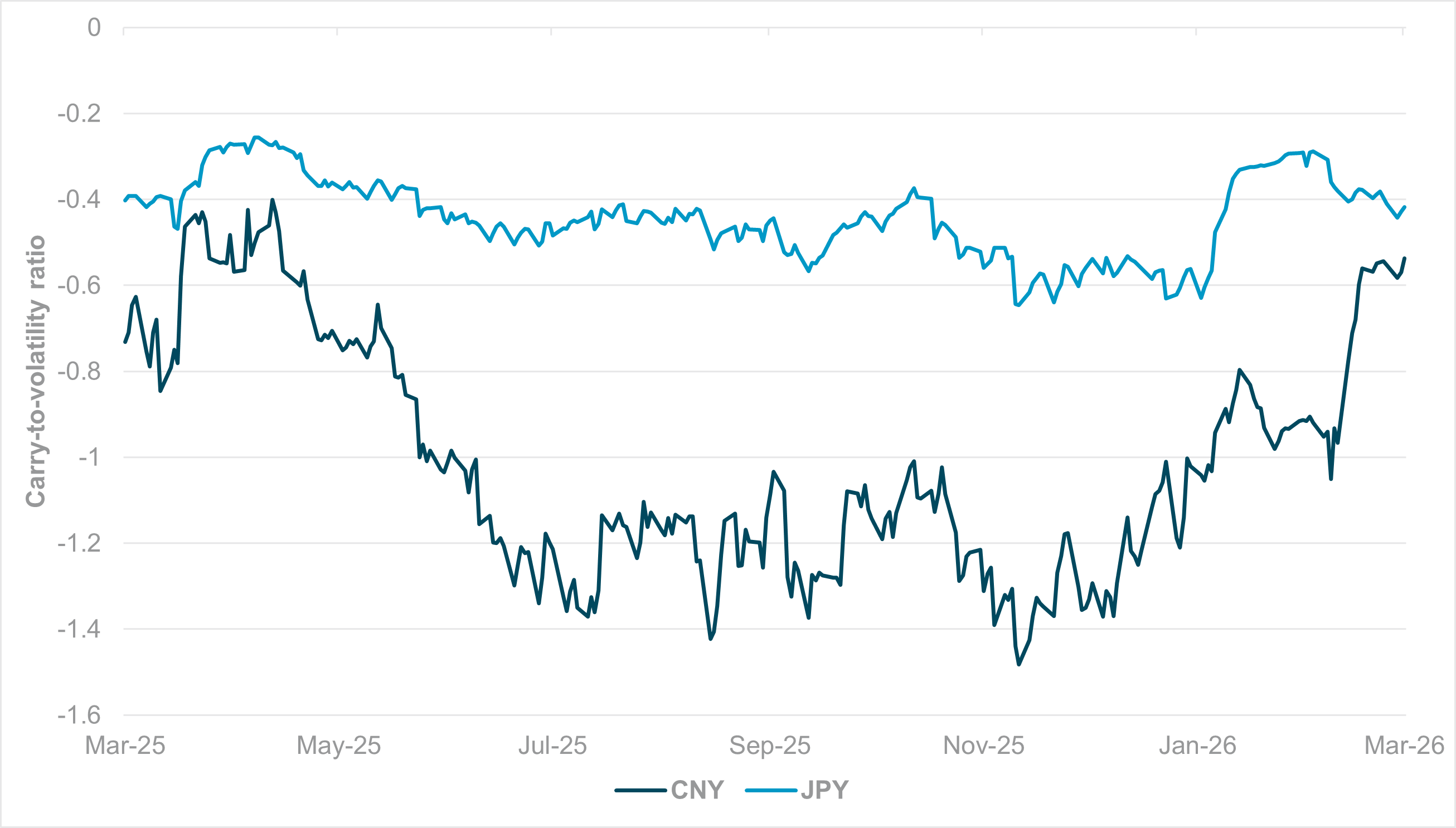

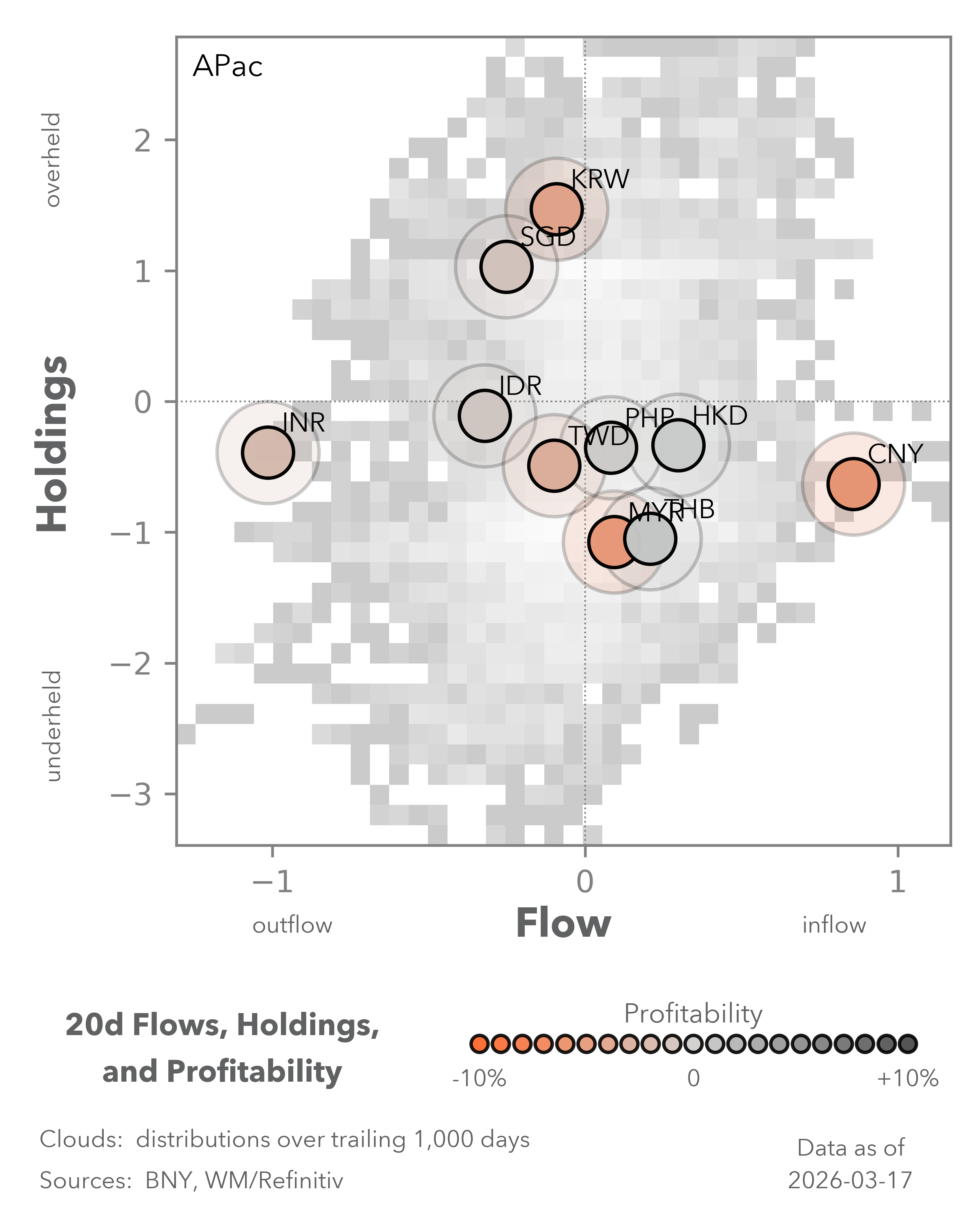

EXHIBIT #2: FX CARRY-TO-VOLATILITY RATIOS FROM ONE-MONTH FORWARD RATES AND REALIZED VOLATILITY

Source: BNY

Our take

iFlow data show CNY remains one of the best-performing currencies. Compared to other savings-heavy APAC currencies, China is less exposed to balance of payments stress. While imported oil exposure from the Middle East is high, oil itself as a primary energy source is materially lower compared to South Korea and Japan, thereby reducing scope for a sudden shift in the trade balance. FX markets also show little doubt in the People’s Bank of China’s ability to manage the exchange rate through the fix. Lower realized volatility is plausible in the current environment, particularly relative to traditional funding currencies where rates are never expected to rise sharply.

Forward look

Short-term flows into CNY are understandable but we would not overplay positive risk-reward based on lower volatility alone. A durable safe-haven currency requires the right balance between rates and volatility, and China is clearly lacking on the rates side. This is where the market has shifted its view on the JPY: realized volatility will remain high but the Bank of Japan is now in a different place compared to prior decades of zero-interest rate policy. Based on annualized one-month USD forward rates, CNY at present can only generate a 70bp gain over JPY versus several times that level in the past. Both remain at a disadvantage relative to the dollar.

Furthermore, with realized volatility coming from a low base, any shock from exogenous conditions – even under a managed FX regime – can generate an outsized decline in risk-reward. The doubling in CNY realized volatility has now forced near-convergence between CNY and JPY in carry-to-volatility ratios. As the CNY regime is gradually liberalized, higher realized volatility will follow by definition as the currency moves away from a managed system and sees greater two-way flow. The People’s Bank of China understands this dynamic well and will likely use any future periods of suppressed volatility to accelerate reform.

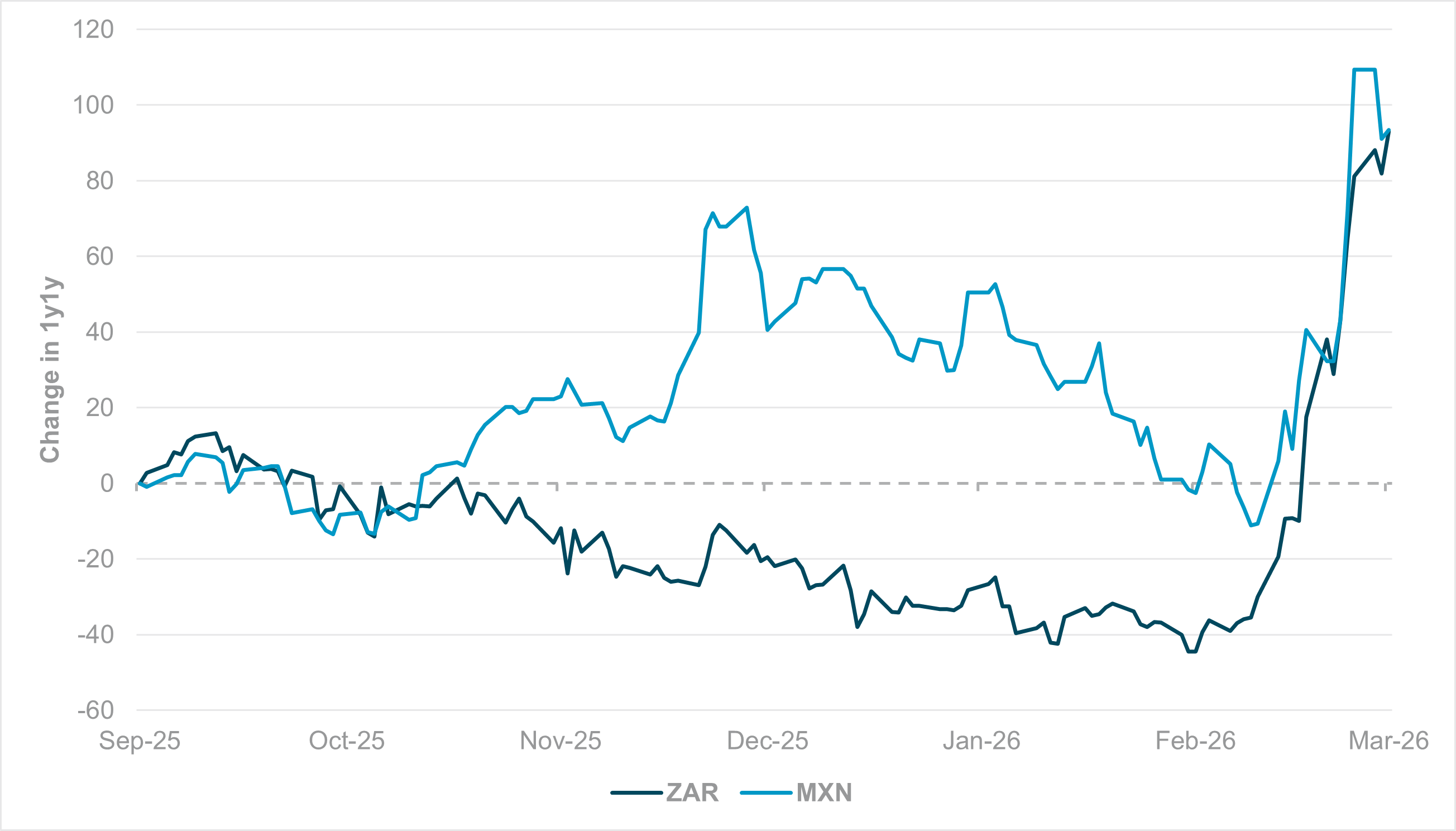

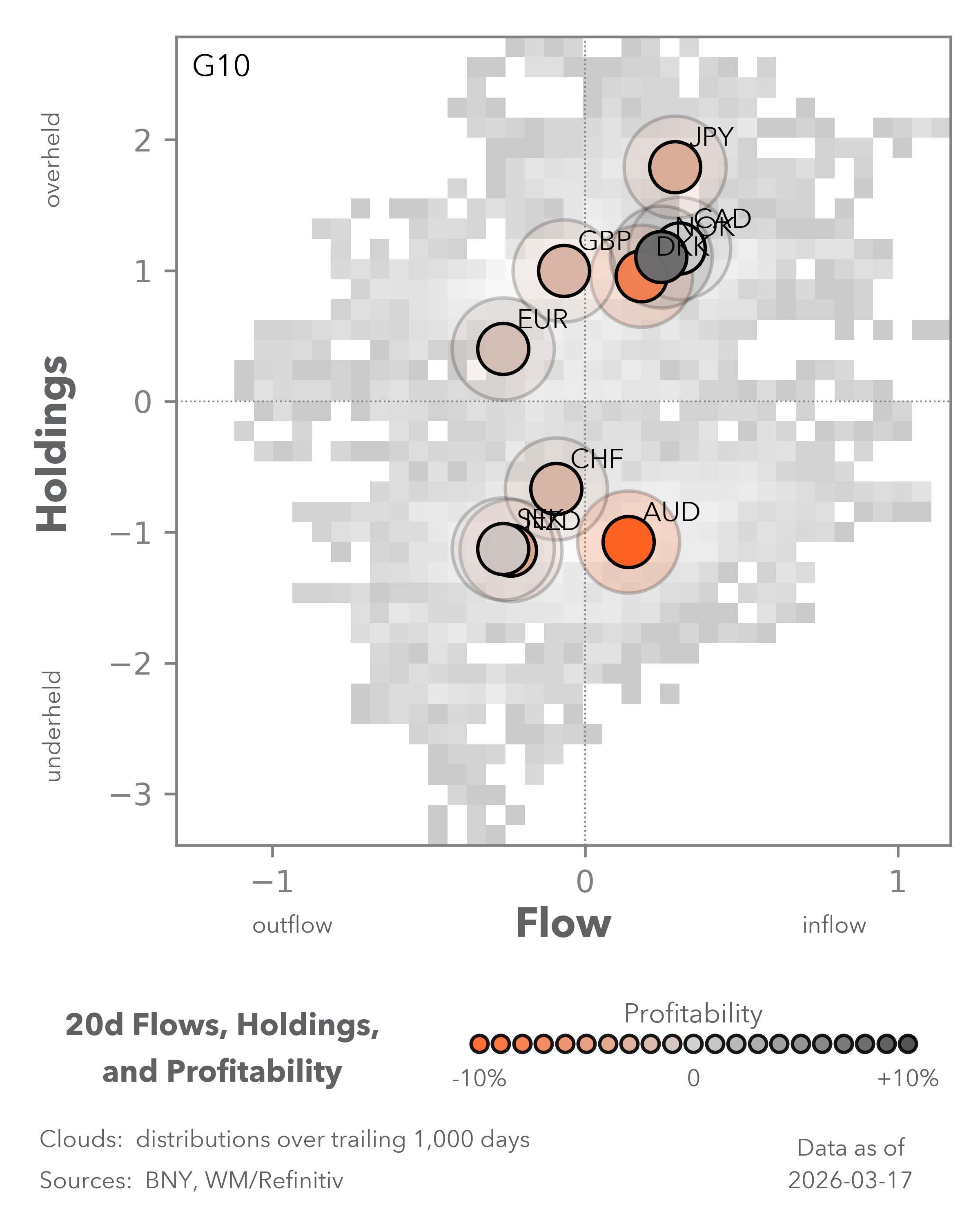

EXHIBIT #3: CHANGE IN 1Y1Y FORWARD RATES, ZAR AND MXN

Source: Bloomberg, BNY

Our take

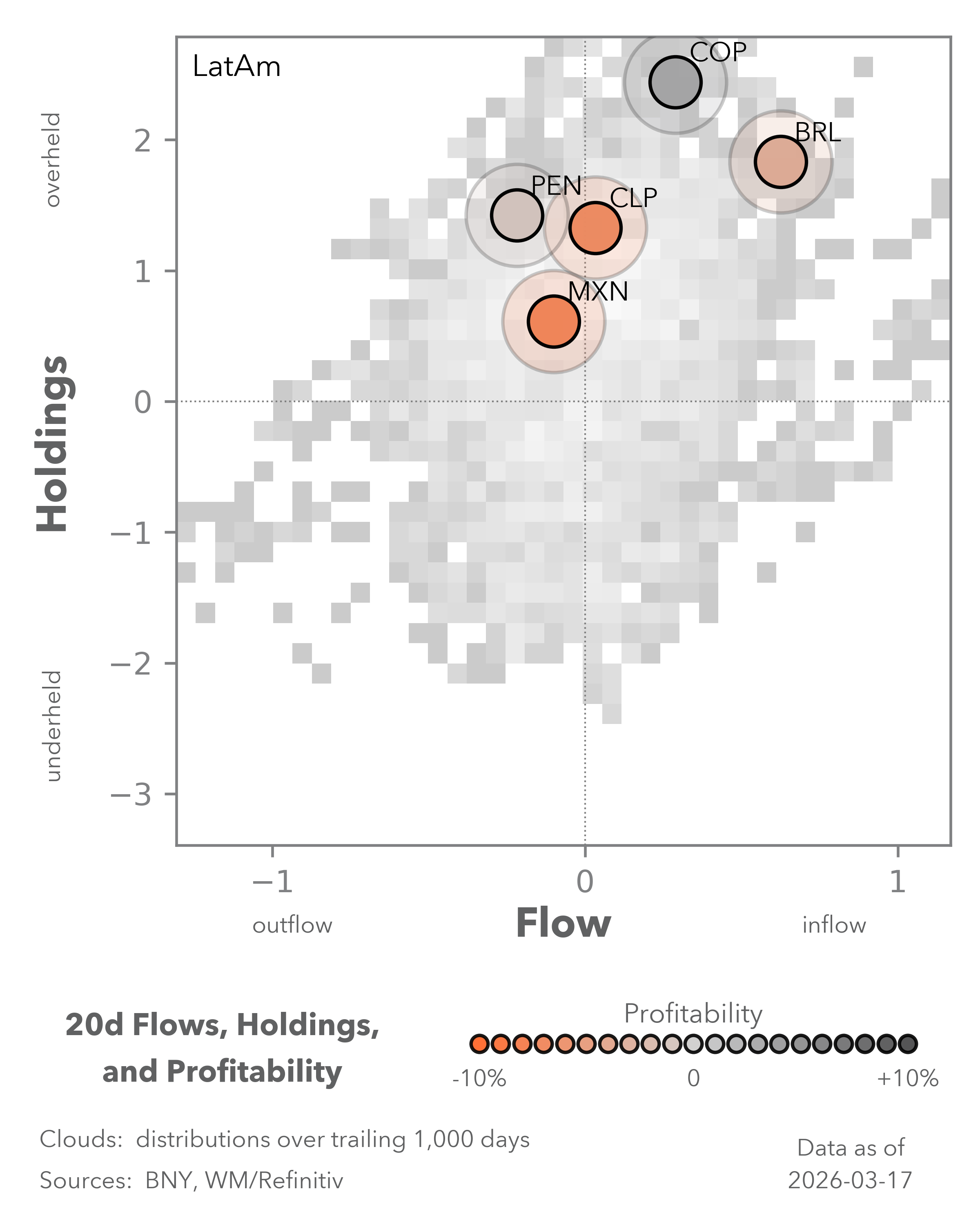

Central bank decisions in Mexico and South Africa next week will present renewed challenges for high-performing carry currencies. We remain concerned that positioning in high-yield names looks excessive. Our flows also show that MXN and ZAR purchases are continuing, much of it on an outright basis rather than hedge unwinding. Since the beginning of the conflict, the sudden shift in inflation risk has proliferated throughout emerging markets (EM), even for commodity producers. We can see that 1y1y rates for ZAR and MXN have wiped out easing expectations. This is sufficient to anchor real rates for now, but markets should begin to differentiate between carry names in general.

Forward look

For much of the last 18 months we have been very positive on ZAR and South Africa as many of the structural issues have seen clear resolution through the efforts of the Government of National Unity. It also helped – and hurt less – that these adjustments occurred during a period of gradual easing in global financial conditions. The early 2026 commodity rally gave South Africa its own terms-of-trade lift, but that could be quickly unwound by energy stress.

However, we don’t see conditions as problematic as with India or Turkey, for example. Nonetheless, on an institutional basis, new reforms such as fiscal rules will take time to bed in, which again can only be done while global financial conditions are loose. Meanwhile, recent wage settlements remain to the high side, and the market may demand even higher nominal rates to compensate for raw inputs and labor supply risks. We retain a positive view on EM fixed income broadly, but currency exposures require much closer risk management – especially if central banks fall short of the proactive response inflation risk demands.