Supply chain showdown

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 4 minutes

The summit between Presidents Trump and Xi next week will matter to investors tracking supply chain disruptions from the U.S.–Iran conflict and elevated energy prices. Taiwan, North Korea, and the tech and AI competition are all on the table. Risks to global rare earth and critical minerals supply will be a key focus for equity investors.

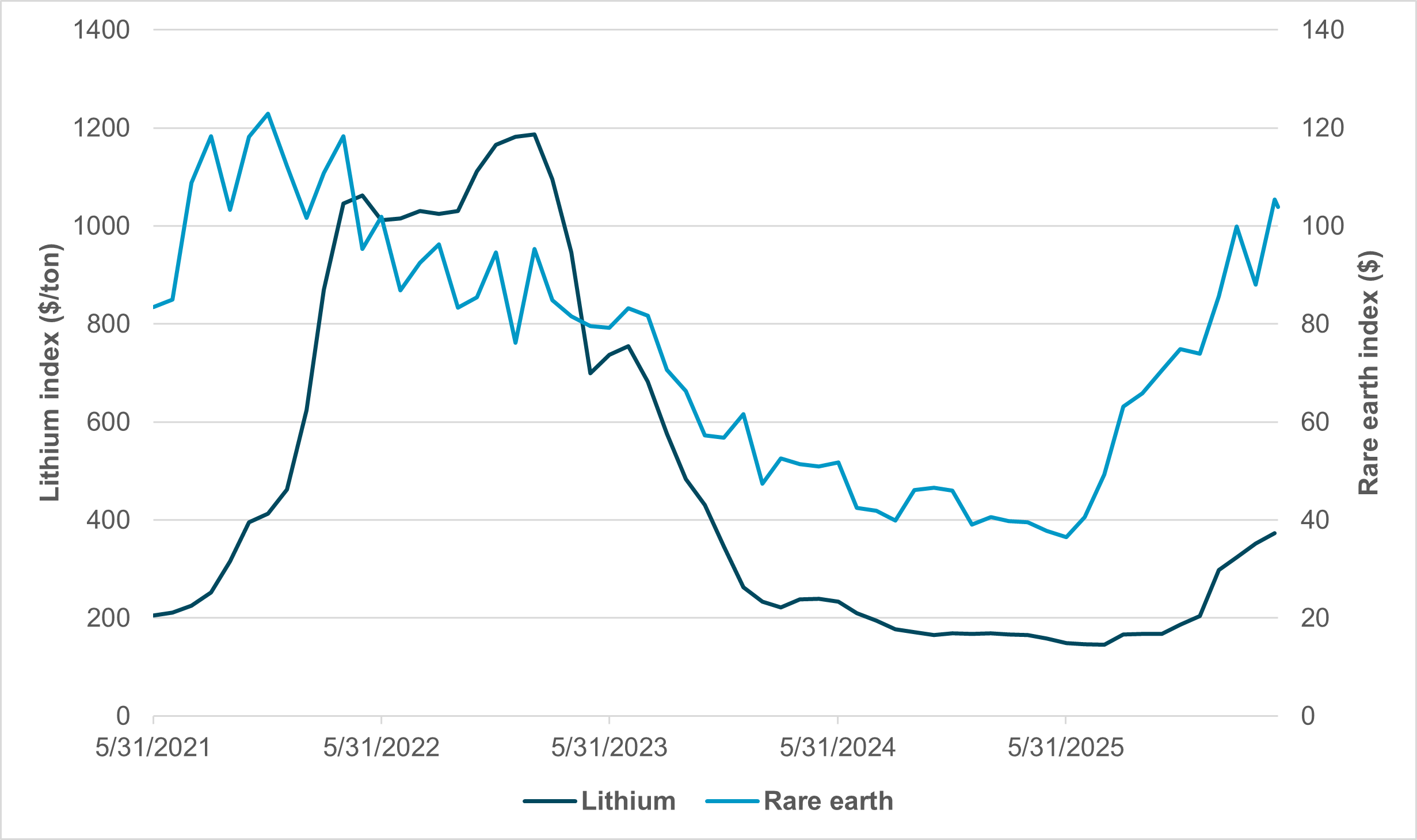

EXHIBIT #1: RARE EARTH AND LITHIUM PRICES

Source: BNY, Bloomberg

Our take

The U.S.–China summit agenda centers on trade, with supply chain access the dominant subtext.

Forward look

Supply chain risk remains central to the U.S.–China negotiations, with China controlling rare earth refining. The price of lithium – a key component for electric batteries and EVs – is also linked to China demand, though metal’s supply is global. Whether investors believe the U.S. can diversify away from China – and whether Washington can open trade in strategic materials – will drive capital allocation decisions. Oil is also on the agenda, given recent U.S. actions in Venezuela and Iran. How commodity flows between the two largest economies are managed will set the tone for the rest of the world.

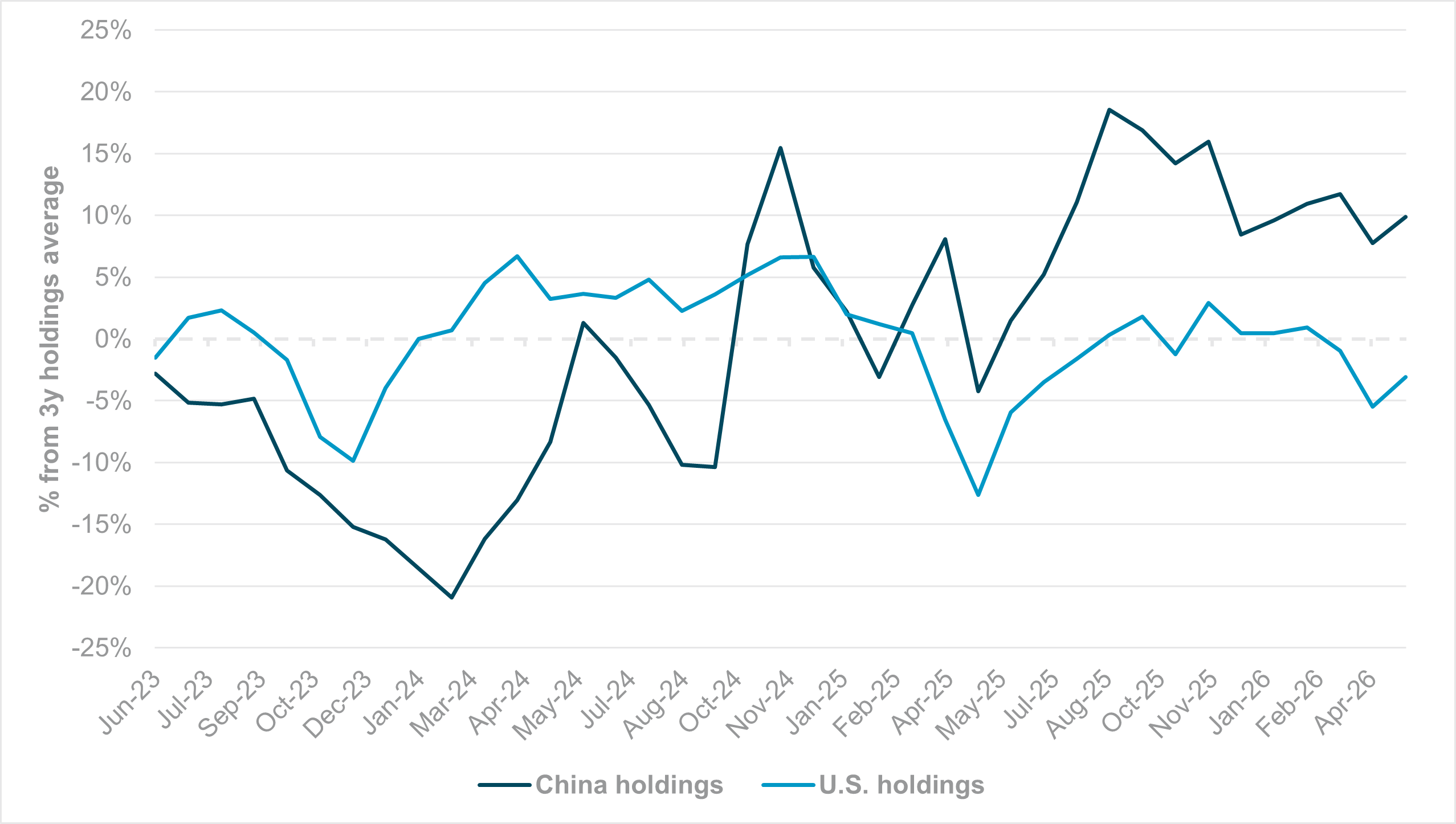

EXHIBIT #2: U.S. AND CHINA EQUITY HOLDINGS VS. THREE-YEAR AVERAGE

Source: BNY

Our take

The buying of China shares from the February 2024 lows to the August 2025 highs was notable but not enough to push China’s shares in our data above 1%. In fact, China remains underweighted in portfolios by 3–4% while the U.S. is overweighted by 4–5%. Nevertheless, the pattern over the past three years shows no clear directional shift in either economy’s holdings. U.S. holdings are in line with the three-year average despite the recent record highs of the S&P 500 and other indices. Similarly, China has seen its holdings dip along with other markets.

Forward look

The recent momentum – buying U.S., selling China – may be the clearest signal of whether investors see the two markets as alternatives. The U.S. accounts for 25% of global growth but 60% of global equity market cap. China, with 1.4bn people and the world’s second-largest economy, holds less than 6%. China’s goal is to build global companies to match the U.S. big tech brands.

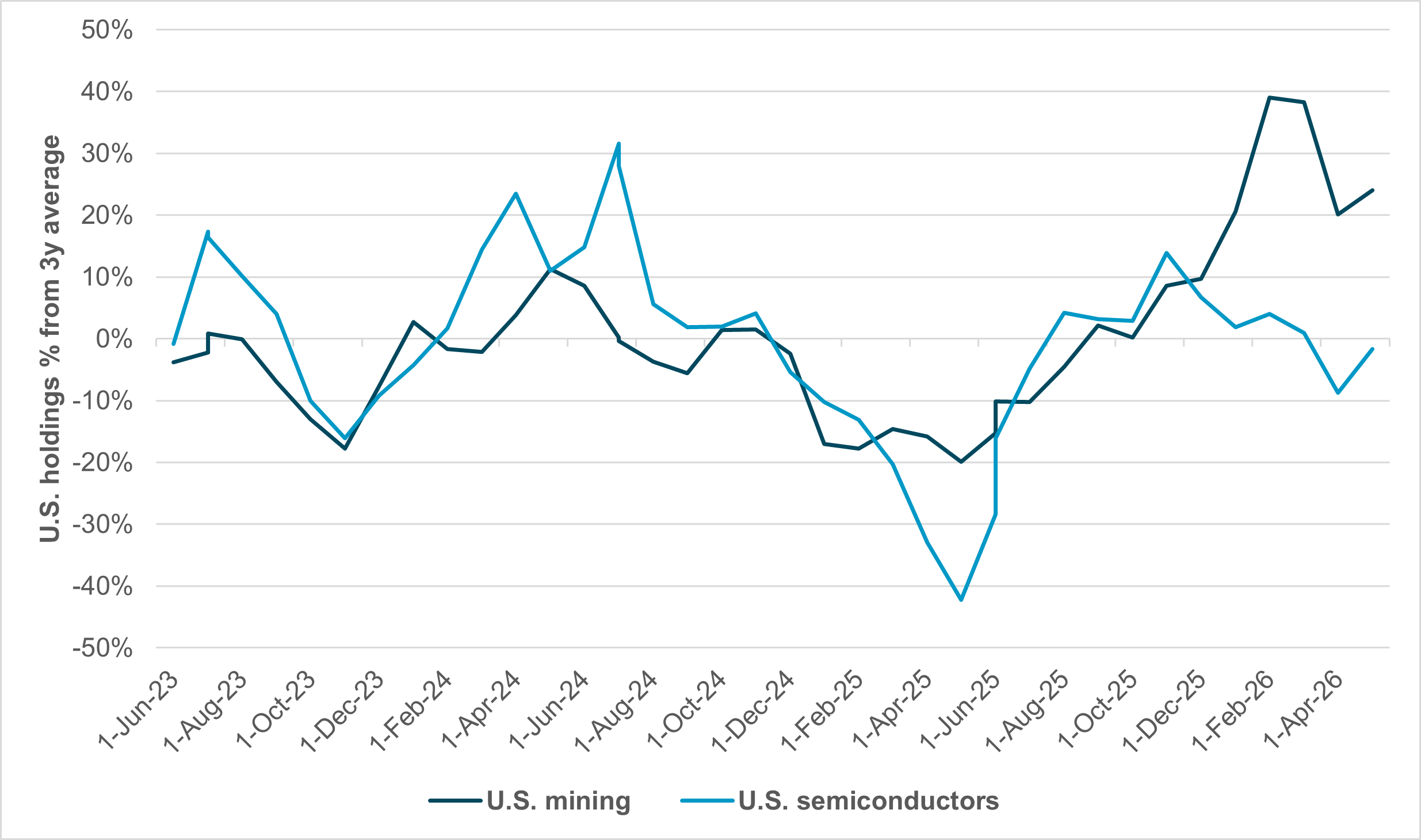

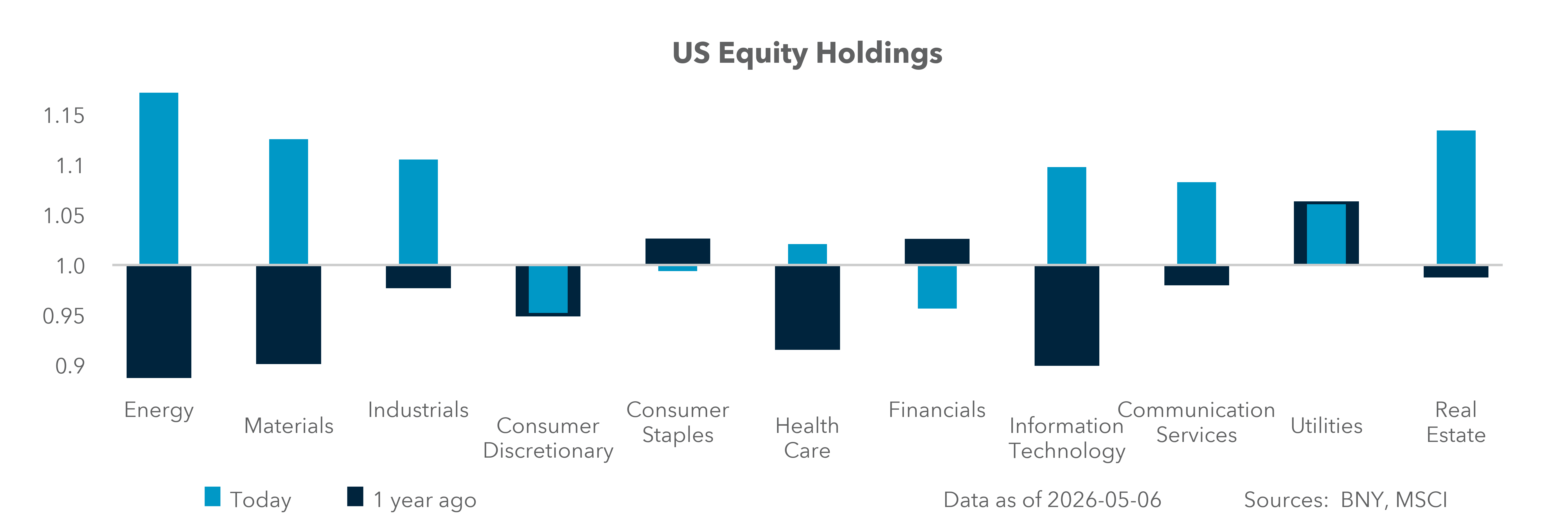

EXHIBIT #3: U.S. EQUITY HOLDINGS VS. THREE-YEAR AVERAGE – SEMICONDUCTORS AND MINING

Source: BNY

Our take

The push to develop U.S. mining capacity for copper, rare earths and other key metals and minerals is reflected in equity holdings. Mining sector holdings are up 20% over the past year, running well above the three-year average. Investors appear less concerned about by U.S. semiconductors investment efforts. The holdings are just at the three-year average and have witnessed a 70% drift from June 2024 highs to May 2025 lows. Semiconductor shortages remain central to concerns about the durability of the AI investment thesis.

Forward look

Materials tension are visible in U.S. equity performance across sectors. GM and Tesla have been clear about their EV dependence on lithium, nickel, cobalt, and some rare earths. Tesla has a $4.5bn raw material inventory to help mitigate some of the volatility. Semiconductor stocks carry greater exposure and have felt the pain of China’s supply controls since 2024. Key companies like Skyworks, Navitas, Qorvo and Power Integrations rely on gallium and germanium for their chips used in power and RF applications. Nvidia holds a $3.8bn raw materials inventory, with 50% of its supply chain costs exposed to these dynamics. Investment flows suggest mining and semiconductors are deeply interlinked, suggesting China will retain a key role even as alternative supply chains develop.

The upcoming Trump–Xi summit could reset expectations across global markets, particularly around supply chains, trade and strategic commodities. While oil has dominated recent headlines, the longer-term focus is shifting toward rare earths, lithium and critical minerals that underpin AI, semiconductors, and energy transition technologies. Investors will be watching for signs of whether the U.S. can diversify supply chains away from China or whether interdependence remains entrenched. Equity positioning suggests skepticism, with China still underweighted despite its central role in global production networks. At the same time, U.S. markets continue to command premium valuations, supported by AI leadership but increasingly exposed to supply chain vulnerabilities. Geopolitical tensions and corporate investment decisions – particularly in semiconductors and mining – will shape capital flows. Ultimately, clarity on trade frameworks and resource access will determine whether markets can sustain current valuations or face renewed volatility.