Introduction

From my work with a wide range of corporate treasury teams, it’s clear that technological and organizational shifts are fundamentally reshaping how treasury functions operate and contribute to business strategy. These changes go well beyond simply adopting new tools—they are redefining the role of treasury within organizations.

At the center of this transformation is the modernization of treasury infrastructure. As legacy technology stacks age and become less suited to today’s digital environment, many organizations are moving to centralize and upgrade their platforms. Doing so not only improves efficiency and visibility over liquidity and payments, but it also creates the foundation required to support emerging capabilities – including real-time payments, application programming interfaces (API) connectivity, and new forms of digital money.

But technology alone won’t determine the success of this transformation. Organizations must also invest in the skills and capabilities of their teams to work with technologies like artificial intelligence (AI) and advanced analytics. This is becoming just as important as upgrading the underlying infrastructure.

In this article, I explore how four trends – centralization, payment modernization, upskilling, and AI – are reshaping modern corporate treasury and redefining the role of tomorrow’s treasurer as a critical driver of business strategy.

Modernizing and centralizing treasury infrastructure

Treasurers increasingly require faster and more responsive cash and liquidity management capabilities in order to keep pace with emerging innovations. However, many legacy treasury management systems (TMS) were not designed to support the speed, data intensity and connectivity of a more real-time treasury environment. This is triggering a wave of modernization efforts across organizations of all sizes.

Many corporates run older TMS platforms that lack the flexibility needed to adapt to evolving market demands, while others rely on end-of-life systems or infrastructure originally deployed on-premises. This often creates persistent operational challenges, from inefficiencies in payment processing to limited visibility over global liquidity positions and fragmented control over treasury activities.

The need for treasury modernization is especially pronounced among large, multinational corporations (MNCs). Having expanded through mergers and acquisitions, these organizations frequently operate multiple treasury platforms across regions. Rationalizing and integrating these systems is therefore becoming a strategic priority in order to enable global treasury processes to operate more efficiently and consistently.

Meanwhile, connectivity models are evolving. Many companies are moving beyond legacy, file-based transmission towards API-driven architectures that enable faster and more flexible integration between banks, treasury platforms and internal systems.

This shift lays the technological foundation for digital payments and plays a crucial role in enhancing working capital optimization and providing real-time visibility into liquidity positions. By consolidating fragmented platforms, treasurers can gain a holistic view of cash flows across the enterprise, enabling more effective management of liquidity and better-informed decision-making that directly supports strategic business objectives.

As a result, many organizations are increasingly upgrading existing platforms or evaluating new providers – often moving toward cloud-based solutions that provide greater scalability, interoperability and resilience. These modern architectures provide the flexibility needed to support future-ready treasury models.

Balancing the old with the new in payments

A recurring theme I encounter is the delicate balance required when embracing new payment technologies while managing legacy processes. Around the world – and particularly in the United States – the payments landscape increasingly reflects two parallel realities: long-standing legacy instruments such as checks and Automated Clearing House (ACH) payments continue to play a critical role, even as a new generation of digital rails and payment options emerges.

For many corporates, the starting point of payment modernization is often the gradual reduction of check usage. In the U.S., for instance, the federal government recently issued an executive order directing agencies to stop issuing checks, thereby reinforcing the broader shift toward digital payments.[i] Yet eliminating checks is easier said than done: they remain widely used in certain industries and supplier networks, meaning corporates must manage the transition carefully, while maintaining compatibility with legacy processes.

Concurrently, a new generation of payments infrastructure is emerging. Real-time payment networks, API connectivity and new digital payment options are expanding the range of ways funds can move. Among the most closely observed developments is the emergence of new forms of digital money, such as stablecoins, which enable always-on, programmable settlement of funds – and will potentially streamline certain cross-border or liquidity-management processes.

Corporate awareness of digital assets is already widespread, even if adoption remains at an early stage. Stablecoins have emerged as one potential area of interest within the broader digital asset universe, although a 2025 EY-Parthenon report found that while all surveyed organizations were familiar with stablecoins, only 8% of participating corporates have used them. Among these early adopters, the benefits are clear – particularly around cost efficiencies and the potential for competitive advantage.[ii]

For most treasury teams, such digital asset innovations remain an area of active exploration as opposed to immediate deployment. Treasurers are closely monitoring how digital money is evolving – assessing potential use cases, regulatory developments and infrastructure maturity – while continuing to support established payment methods that remain essential to day-to-day operations.

Readying treasury teams for a more strategic role

Against this backdrop of rapid modernization, fintech innovation, and evolving end-user expectations, treasury has switched from a back-office function to a more strategic hub within organizations. Modern treasury teams increasingly operate as cross-functional centers, working alongside IT leaders, CFOs and CTOs to help shape how financial infrastructure evolves and how new technologies are adopted across the business.

Treasurers must now distinguish between emerging concepts, technologies already in practical use, and those that are truly relevant to their own organizations. Navigating this rapidly shifting landscape has become an important part of the treasury mandate.

Further reinforcing these changes is the treasury’s increasing proximity to customers and business operations, where they are increasingly engaged in improving payment experiences, supporting digital commerce, and enabling smoother financial journeys for end users. This underlines a broader shift within treasury: modernization is not only about upgrading technology, but also about strengthening the capabilities of the people responsible for implementing and managing it.

The result of this is that leading organizations are now investing in both treasury infrastructure and talent development – ensuring teams are equipped to manage traditional responsibilities such as cash, liquidity, and payments, while also acting as technology partners capable of guiding the business through an increasingly digital landscape.

Harnessing AI – from widespread adoption to practical impact

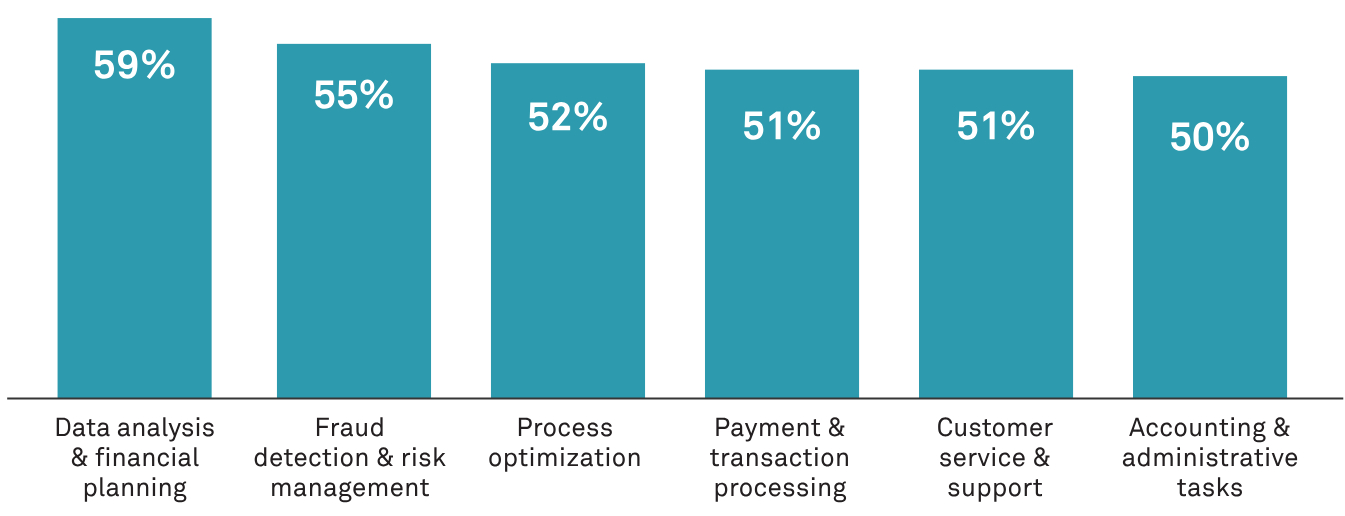

AI has long been part of the financial landscape and we’re now seeing a significant acceleration in the adoption of Large Language Models (LLMs) and generative AI across treasury functions. Many corporations are actively modernizing their treasury technology stacks to integrate generative AI capabilities that enhance operational efficiency and decision-making. They are also leveraging solutions from their financial institutions, achieving comprehensive operational enhancements spanning core banking functions—from financial planning and risk management to payment processing and customer service delivery (Figure 1)

Figure 1: Corporations' Use of Banks' Generative AI Capabilities Shows Healthy Growth

Q. What specific tasks or processes have been enhanced by using AI for banking and payments capabilities?

(Base=490, already using AI)

Source: Datos Insights survey of 1,036 midsize and large organizations, Q3 2025.

However, as with any transformation, treasury leaders face the ongoing challenge of balancing competing priorities—modernizing infrastructure, managing risk, and upskilling teams—all while delivering measurable outcomes. At BNY, we take a democratic and people-first approach to AI adoption. We invest considerable effort in understanding how employees interact with AI tools and focus on enabling smooth adaptation to new platforms. This human-centered strategy ensures that AI acts as a true partner to our teams, augmenting their expertise rather than replacing it.

Our experience shows that successful AI deployment in treasury hinges on combining automation with expert oversight—a “human-in-the-loop” framework. This approach builds confidence in AI-driven processes while improving accuracy and speed in areas such as cash forecasting, fraud detection, and payment reconciliation.

As treasury functions evolve, embracing AI thoughtfully and strategically will be key to unlocking its full potential and supporting the broader business in an increasingly digital and data-driven environment.

Building a future-ready treasury function

Corporate treasury sits at the intersection of several powerful forces. Treasurers must modernize infrastructure, navigate an evolving payments landscape, evaluate emerging forms of digital money, and equip their teams with the skills needed to operate in an increasingly automated and data-driven environment.

In this context, treasury’s role is expanding in an exciting way. No longer confined to just managing cash and liquidity, treasury functions are increasingly acting as strategic partners to the wider business – helping organizations adapt to new technologies, strengthen financial resilience, and enable more efficient global operations.

Ultimately, success will hinge on building a treasury architecture that is both robust and adaptable. Organizations that invest in modern infrastructure, stronger connectivity, and skilled teams will be best positioned to harness emerging innovations while continuing to support the core financial operations that underpin their businesses.