Market Movers: Contradictions

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 7 minutes

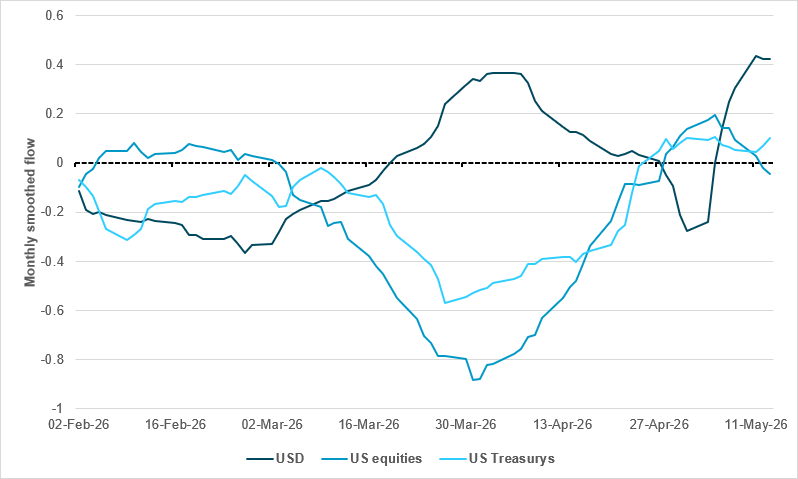

Cross-border focus remains on USD and equities, FI in search of direction

Source: BNY

As President Trump wraps up his brief visit to China, markets will hope that stable trade relations with China will help maintain the current risk setup, which is increasingly showing signs of U.S. exceptionalism again. The inclusion of key technology executives is also raising expectations of broader market and revenues, which would certainly be welcomed heading into upcoming earnings reports. Whether the valuations are justified or not, flows are supporting these narratives. Domestic bias has always been strong, but now there are signs that international investors are returning to the U.S. Assuming that the ceasefire holds and balance of payments recover sufficiently around the world to generate surplus savings, recycling of flows will require new destinations. APAC has a strong story, but much of the flow could also lapse into the U.S. by default. We are already seeing some signs of strength in dollar exposure, led by cross-border investors.

In equities, the U.S. is beginning to outperform developed market peers again: the first half of May saw some of the strongest institutional cross-border equity flows into the U.S. over the past few months. Any selling in March may in any case have been for liquidity preference rather than taking a fundamental view, and most of the outflows have been fully offset. The only area where the notion of U.S. exceptionalism can be called into question is in the U.S. Treasury market, where cross-border interest has been flagging for some time. Prior to the conflict, cross-border interest in U.S. Treasurys was non-existent and leaned toward moderate selling. The ceasefire has produced a degree of recovery, however. Foreign funding has since moved strongly into the UST market, with the first two weeks of May the best for cross-border interest over the past four months. There also remains significant ground to make up.

There is a twist on the familiar end-of-week pattern of risk reduction today, as key assets break out of their month-to-date range limits. Higher oil prices (up 3% overnight) brought higher bond yields (up 5-10bp overnight), driving down equity markets (1-2% lower) and pushing up USD. The headlines behind the moves are all linked to inflation velocity and continuing concerns that the Iran conflict resolution process is too slow. Today investors have to contend with the contradiction between USD being bid this week (up 1% in the biggest rise since March) and the S&P 500 standing at a record high (up 2% on the week). The test today comes from rates, as U.S. bond yields break out of the top end of their ranges on shifting Fed rate hike risks. The probability of a Fed hike now stands at 60% by year-end, based on the CPI/PPI numbers and stable growth outlooks from retail sales yesterday.

Bonds: This week has seen an average global rise in 10y G10 yields of 15bp, with the U.K. leading at over 20bp. Today’s moves account for about half of the weekly story. The 2y U.S. yield is now 4.06%, after it climbed 4bp overnight to a level not seen since March 2025. Meanwhile, the 10y rate rose 6bp to 4.54%. Japanese 30y bond yields rose 14bp to a record-high 4.015%, while 10y yields were up 8.5bp to 2.70%, back at the level of their 1996 high. U.K. 10y gilt yields are up 14bp at 5.13%, while 10y yields on Italian BTPs rose 10bp to 3.87%. The key drivers behind the bond breakouts are inflation data and fiscal dominance fears. The political turmoil in the U.K., where leadership challenges to Prime Minister Sir Keir Starmer are an ongoing story, mixed badly with the Japanese PPI release.

Supply: U.S. IG issuance this week topped forecasts at over $50bn, but today will likely see a shift with rates higher. The last seven auctions of U.S. government coupons all tailed, highlighting that carry from higher yields is not sufficient to offset worries about future inflation. Overnight, Alphabet sold $3.6bn in JPY bonds, in the largest issue in Japan by a foreign company. The ongoing logic for hyperscalers to borrow to build more AI capacity is adding to the squeeze on yields globally.

Aftermath of Trump/Xi talks: Fears of decoupling have been averted, but the focus will be on the actual results for trade. Boeing shares fell after China placed just 200 plane orders following the meetings. The fear of escalation in Iran in a bid to unblock the Strait of Hormuz also stands out. Nevertheless, the meetings are seen as a positive geopolitical shift. “This visit is a historic and landmark visit. Thus far, we have established a new bilateral relationship – a constructive strategic stable relationship – which constitutes a milestone event,” noted China’s President Xi.

Bottom line: The breakdown in bonds globally sets a new limit for equities, as the correlation between bonds and stocks flips from positive to negative. The shift in central bankers’ policy outlooks is one factor; the ongoing rise in inflation is another. The importance of fiscal spending to offset the pain of the current energy shock makes it clear that this is not a repeat of 2022 and the Russia/Ukraine war. The U.S. trading session is unlikely to unify the logic of risk reductions, as we have seen from other equity market reversals from the KOSPI to the DAX. The inflows into U.S. equities and the rapid surge in yields leave USD and its role as a shock absorber for volatility in question. The other limit may lie in currency weakness, specifically in JPY as it tests 158.50 again, or EM, where ZAR, MXN and HUF have all reversed their carry gains again.

China has called for a lasting truce in the Middle East and for the Strait of Hormuz shipping lanes to be reopened “as soon as possible” to restore regional stability and ease global market jitters. The strait, which is vital for about 20% of global oil and LNG shipments, has been largely closed since the conflict erupted between Iran and the U.S./Israel on February 28. During a summit in Beijing, Chinese leader Xi Jinping assured President Trump that China would not provide military aid to Tehran and expressed willingness to help reopen the strait. Iran has allowed some Chinese ships passage recently. Brent +2.904% to 108.79, WTI +3.292% to 104.5, Omani crude +0.039% to 104.78, Dubai crude +0.249% to 102.605.

U.S. Trade Representative Jamieson Greer has announced that China has committed to making large purchases of U.S. agricultural products, including soybeans, over the next three years. Annual purchases are expected to be in the tens of billions. President Trump has emphasized China’s strong demand for U.S. farm goods. The agreement covers soybeans and other products such as corn, wheat, DDGs and ethanol. China has already begun fulfilling some commitments, with most soybean sales anticipated later this year, returning trade to historic norms. China has also renewed import permits for hundreds of U.S. beef plants, signaling progress on bilateral agricultural trade. NASDAQ Mini -1.26% to 29315, DXY +0.348% to 99.162, 10y UST +6.1bp to 4.542%.

New York Fed President John Williams has commented that monetary policy is mildly restrictive and well-positioned, with no justification to raise or lower rates currently. He emphasized that all inflation measures are considered without reliance on a single indicator, reflecting cautious comfort amid persistent above-target inflation. Williams expects strong productivity growth to continue, driven by broad factors beyond AI, and views the Fed’s ample reserve system as effective. He acknowledged market optimism and elevated equity valuations as understandable, signaling no intention to adjust rates to temper financial conditions. The Fed remains on hold, awaiting clearer economic signals.

Federal Reserve Governor Michael S. Barr has argued that shrinking the Fed’s balance sheet is the wrong objective for reducing its financial system footprint. He asserted that the Fed’s footprint includes its roles in bank oversight, payment system support and financial stability, not just balance sheet size. Barr highlighted the importance of ample reserves for banking system resilience and efficient monetary policy implementation. Proposals to reduce reserve demand or liquidity requirements risk undermining financial stability. He advocated for a holistic approach, cautioning that many balance sheet reduction ideas could increase market intervention and volatility rather than diminish the Fed’s presence.

U.S. May NY Empire Manufacturing is forecast to ease to 7.3 vs. 11.0.

U.S. April industrial production is forecast to rise to 0.3% m/m vs. -0.5% m/m while manufacturing production is expected to rise to 0.2% m/m vs. -0.1% m/m and capacity utilization is expected to rise to 75.8% vs. 75.7%.

Canada housing starts are expected to rise to 245.0k vs. 235.9k.

Canada March manufacturing sales are expected to ease to 3.5% m/m vs. 3.6% m/m.

ECB publishes its May Economic Bulletin.

Mood: Risk aversion is beginning to emerge, reflected in the rapid selloff in equities alongside steady demand for core government bonds. The iFlow Mood index has fallen toward recent lows, standing at -0.138.

FX: EMEA currencies saw broad-based selling, while flows across the rest of the universe were mixed and relatively moderate. Substantial outflows were observed in DKK, GBP and SGD, offset by inflows into AUD, NZD, EUR and HKD.

FI: Australian government bonds led the selloff, followed by JGBs. In contrast, demand was concentrated in Eurozone sovereigns, alongside Hungarian, Colombian and Mexican government bonds, U.K. gilts and U.S. Treasurys.

Equities: Outflow pressure remained intense in South Korea, with additional selling in Poland, Hungary, broader Europe and Sweden. Inflows were strongest in China and Thailand, followed by South Africa and Brazil. G10 equity flows were largely muted.

“Propositions show what they say: tautologies and contradictions show that they say nothing.” – Ludwig Wittgenstein

“In contradiction and paradox, you can find truth.” – Denis Villeneuve

Italy’s CPI inflation for April was 1.1% m/m and 2.7% y/y, up from preliminary estimates of 1.0% m/m, 2.5% y/y and from 1.7% m/m, 0.5% y/y in March. Inflation was driven mainly by sharp increases in unregulated energy prices (+9.6% y/y from -2.0%) and regulated energy (+5.3% from -1.6%), alongside higher unprocessed food prices (+5.9% from +4.7%). Prices of recreational, cultural, personal care services and transport services slowed. Core inflation excluding energy and fresh food eased to +1.6% y/y from +1.9%. Goods prices accelerated (+3.1% y/y), while services slowed (+2.4%). The harmonized index (IPCA) rose 1.6% m/m and 2.8% y/y. FTSE MIB -1.67% to 49216, EURUSD -0.658% to 1.1632, 10y BTP +9.2bp to 3.866%.

Norway recorded another exceptionally strong month for exports in April, driven mainly by surging oil and gas revenues. Total exports reached NOK 176.7bn, up 20.9% y/y, while the trade surplus rose to NOK 84.2bn. Crude oil exports hit a record NOK 61.4bn, supported by both higher export volumes and sharply rising prices linked to Middle East tensions and the blockade of the Strait of Hormuz. Natural gas exports also remained elevated due to high European gas prices and low storage levels. However, mainland exports weakened, particularly seafood exports, partly because of a stronger Norwegian krone. Imports remained broadly stable overall, although diesel and refined fuel imports rose sharply as energy prices increased. OSE +1.12% to 2008, EURNOK -0.796% to 10.8678, 10y NGB +3.1bp to 4.533%.

Poland’s CPI rose by 0.6% m/m, 3.2% y/y in April (March: 1.1% m/m, 0.3% y/y) with services prices up 5.2% y/y and goods by 2.4% y/y. Key contributors to the y/y increase included housing, water, electricity, gas and fuels (+4.8%), food and non-alcoholic beverages (+1.9%), transport (+3.5%), alcoholic beverages and tobacco (+6.7%), health (+5.0%) and recreation, sport and culture (+4.6%). Clothing and footwear (-2.8%) and furnishings (-0.8%) exerted downward pressure. M/m price rises were led by food and non-alcoholic beverages, housing and fuels, clothing, recreation, information and health. WIG -1.3% to 132090, EURPLN -0.255% to 4.2488, 10y PGB +9.5bp to 5.959%.

The Turkish central bank’s May survey of expectations shows year-end consumer inflation expectations rising to 28.94% (previously 27.53%), with 12 and 24-month ahead expectations at 23.82% (23.39%) and 18.43% (18.02%), respectively. The year-end USD/TRY exchange rate expectation increased slightly to 51.57 (51.23), with the 12-month ahead measure up to 54.69 (53.62). The BIST repo rate expectation remains at 40.00%, while the CBRT policy rate for June is expected at 37.00%. GDP growth forecasts for 2026 and 2027 are 3.3% (3.5%) and 4.1%, respectively. BI 100 -1.88% to 14370, USDTRY -0.244% to 45.5453, 10y TGB +39bp to 34.86%.

Japan’s producer price index (PPI) rose 2.3% m/m, 4.9% y/y in April, accelerating from 1.0% m/m, 2.9% y/y in March. Key contributors included petroleum and coal products, chemicals and electric power. The export price index climbed 3.3% m/m (up from 1.6% in March), driven by jet fuel, chemicals and electronic products. The import price index surged 4.9% m/m, led by petroleum, coal, natural gas and electronic products. Y/y, the PPI rose by 4.9%, exports by 18.9% and imports by 17.5%. The report highlights significant price pressures in the energy and chemical sectors, reflecting ongoing global commodity market volatility. Nikkei -1.99% to 61409, USDJPY -0.341% to 158.47, 10y JGB +8.3bp to 2.717%.

Japan’s preliminary machine tool orders for April totaled ¥188.971bn, down 2.3% m/m but up 45.1% y/y (March: +28.0% y/y). Domestic orders were ¥49.292bn, down 2.3% m/m and up 43.4% y/y (March: +2.5% y/y). Foreign orders reached ¥139.679bn, down 2.3% m/m and up 45.7% y/y (March: +40.4% y/y). The strong y/y growth reflects robust demand, particularly from overseas markets, despite a small m/m decline.

New Zealand’s manufacturing sector showed marginal expansion in April, with a seasonally adjusted PMI of 50.5, down from 52.8 in March and 54.6 in February (long-term average: 52.5). Employment (53.4) and production (51.7) were the strongest sub-indexes, while new orders (48.2) and deliveries of raw materials (46.5) contracted. Micro-firms struggled most, with a PMI of 39.2, whereas medium-large firms led at 56.8. Rising freight and fuel costs, linked to the war against Iran, negatively impacted raw material deliveries and business performance. The data suggest potential weakening ahead for the sector. NZX 50 -0.46% to 12965, NZDUSD -1.383% to 0.5851, 10y NZGB +1.6bp to 4.747%.

New Zealand saw significant fuel price rises in April: petrol increased by 12.6% m/m and diesel 36.6% m/m, continuing a sharp upward trend in place since February 2026 (petrol +33.6%, diesel +94.9%). Over 12 months, petrol rose 30.1% y/y and diesel 91.3% y/y. Electricity and gas prices also increased by 2.4% and 0.3% m/m, respectively, with y/y rises of 13.1% and 10.8%. Domestic and international airfares rose 4.2% and 6.2% m/m but fell around 6.9% and 6.5% y/y. Food prices were flat m/m but up 2.6% y/y, led by meat, poultry and fish (+7.8%).

Peru’s Central Reserve Bank (BCRP) kept the reference interest rate steady at 4.25% at its May meeting. April inflation was 0.52% m/m, with core inflation (excluding food and energy) at 0.87% m/m, driven by higher local transport fares and fuel prices amid rising global oil costs. Annual headline inflation increased from 3.8% in March to 4.0% in April, while core inflation rose from 3.7% to 4.4%, exceeding the target range. 12-month-ahead inflation expectations edged up to 2.8% but remain within target. Economic activity indicators remain positive despite some weakening in expectations. Global risks are persisting due to the Middle East tensions. BCRP has reiterated its forward-looking statement and reaffirmed its commitment to take all necessary actions to ensure inflation returns to the target range within the projection horizon. MSCI NUAM Peru General -1.12% to 53762, USDPEN -0.161% to 3.4225, 10y PGB +2bp to 6.74%.

South Korea’s export price index (KRW basis) rose 7.1% m/m and 40.8% y/y in April, while the import price index fell 2.3% m/m but gained 20.2% y/y. The export volume index grew 12.4% y/y, with the import volume index slightly down 0.1% y/y. The export value index surged 50.2% y/y, while the import value index rose 16.8% y/y. Within imports, raw materials prices fell -9.7% m/m after a sharp 40.4% m/m gain in March but remain 33% higher on a y/y basis. Intermediate goods prices were up 2.1% m/m, 21.9% y/y vs. 12.7% m/m, 17.3% y/y in March. KOSPI -6.12% to 7493, USDKRW -0.567% to 1501.15, 10y KTB +3.2bp to 4.087%.

Hong Kong’s GDP expanded by 5.9% y/y in Q1, matching estimates and up from 4.0% in Q4 2025. Q/q growth was 2.9% (1.1% in Q4 2025). Key contributors included a 17.7% y/y rise in investment (11.7% in Q4), 23.7% growth in goods exports (15.4% in Q4) and a 4.9% increase in household spending (2.5% in Q4). Goods imports surged 29.8% y/y (18.2% in Q4). Services exports and imports grew moderately. Government spending rose 3.0% y/y (1.5% in Q4). Overall, broad-based growth was supported by strong trade and investment. Hong Kong revised its 2026 headline CPI forecast up from 1.8% to 2.6% while maintaining the GDP growth forecast at 2.5-3.5%. Hang Seng -1.62% to 25963, USDHKD +0.037% to 7.8299, 10y HKGB -1.2bp to 1.417%.

India’s trade deficit widened to $28.38bn in April, up from $20.67bn in March, as imports surged to $71.94bn from $59.59bn, outpacing exports which rose to $43.56bn from $38.92bn. The Middle East conflict has disrupted energy imports, raising costs as crude oil prices spiked at $120 per barrel. India, which is heavily reliant on Middle East oil and cooking gas, faces inflation and growth concerns. Services exports and imports came in at $37.24bn and $16.66bn, respectively. Measures including fuel conservation and travel limits have been urged to manage foreign exchange reserves. SENSEX +0.14% to 75504, USDINR -0.184% to 95.945, 10y INGB +5.5bp to 7.075%.

India raised petrol and diesel prices by around ₹3/liter on May 15, 2026, ending a two-year freeze. State-run oil firms cited mounting under-recoveries amid elevated crude prices, with petrol at ₹97.77 and diesel at ₹90.67 per liter in Delhi. Private refiners had increased prices earlier. The government had cut excise duty by ₹10 per liter in March to delay hikes. OMCs face losses of about ₹300bn/month due to high crude costs. The price rise is expected to drive up inflation and impact GDP growth. PM Narendra Modi has urged citizens to rationalize fuel use to save foreign exchange.

India has imposed stricter limits and monitoring on gold imports under the Advance Authorization (AA) scheme, capping imports at 100 kg per authorization. This follows the government’s recent hike in import duty on gold and silver to 15% to curb rising bullion imports and support the rupee. New rules mandate physical inspection of manufacturing facilities for first-time applicants, require exporters to fulfill at least 50% of previous export obligations before new authorizations and enforce fortnightly import-export reporting by permitholders. These measures aim to prevent misuse of the scheme for price arbitrage as gold import bills surge.

Malaysia’s GDP grew by 5.4% y/y in Q1, down from 6.2% in Q4 2025 and beating the flash estimate of 5.3% y/y. The services sector led growth at 5.6% y/y, supported by the wholesale and retail trade, information and communication, and transportation sub-sectors. Manufacturing rose 5.9%, driven by electrical and electronic products. Mining and quarrying contracted by 2.1%, mainly due to declines in crude oil and natural gas. Agriculture grew 2.6%, led by oil palm and livestock. Construction growth slowed to 7.7%. Private consumption and gross fixed capital formation supported demand, while exports rose 5.2% and imports eased to 4.6%. Bank Negara Malaysia commented that while growth in 2026 will be affected by external headwinds, Malaysia is facing these challenges from a position of strength. 2026 GDP and CPI are projected at 4%-5% and 1.5%-2.5%, respectively. KLCI -0.31% to 1740, USDMYR -0.519% to 3.9515, 10y MGB 0bp to 3.579%.

Malaysia’s international investment position showed net liabilities of MYR 67.8bn at end-Q1, up from MYR 26.1bn in Q4 2025. Total financial assets were MYR 2.59tn, with liabilities rising to MYR 2.66tn. Direct investment abroad (DIA) edged down to MYR 589.1bn (Q4 2025: MYR 589.3bn), mainly relating to the services sector (MYR 434.2bn). Top DIA destinations were Singapore (MYR 155.0bn; 26.3%), Indonesia (MYR 63.2bn; 10.7%) and the Cayman Islands (MYR 41.2bn; 7.0%). Foreign direct investment rose to MYR 1.113.8tn (Q4 2025: MYR 1.088tn), led by services (MYR 625.8bn) and manufacturing (MYR 411.8bn), with Singapore, Hong Kong and Japan as key sources.

In the Philippines, approved foreign investments (FI) reached PHP 42.64bn in Q1, up 52.3% y/y from PHP 27.99bn in Q1 2025. South Korea led with PHP 25.37bn (59.5%), followed by Singapore (PHP 3.18bn) and China (PHP 2.54bn). Key sectors included arts, entertainment and recreation (PHP 10.38bn), manufacturing (PHP 9.08bn) and accommodation and food services (PHP 9.07bn). Central Luzon received 77.6% of FI pledges. Total approved investments (foreign and Filipino) fell 30.8% y/y to PHP 125.95bn, with Filipino nationals contributing 66.1%. Employment from approved projects is expected to decline by 31.9% y/y to 21,623 jobs. PSEi -0.64% to 5977, USDPHP -0.132% to 61.725, 10y PHGB -8.3bp to 7.199%.