FX carry unwind not necessarily a risk-off signal

iFlow > Investor Trends

Investor Trends provides a deep dive into patterns and behaviors in equity, bond and currency markets around the globe, underpinned with deeper macro insights.

iFlow > Investor Trends

Investor Trends provides a deep dive into patterns and behaviors in equity, bond and currency markets around the globe, underpinned with deeper macro insights.

Geoff Yu

Time to Read: 5 minutes

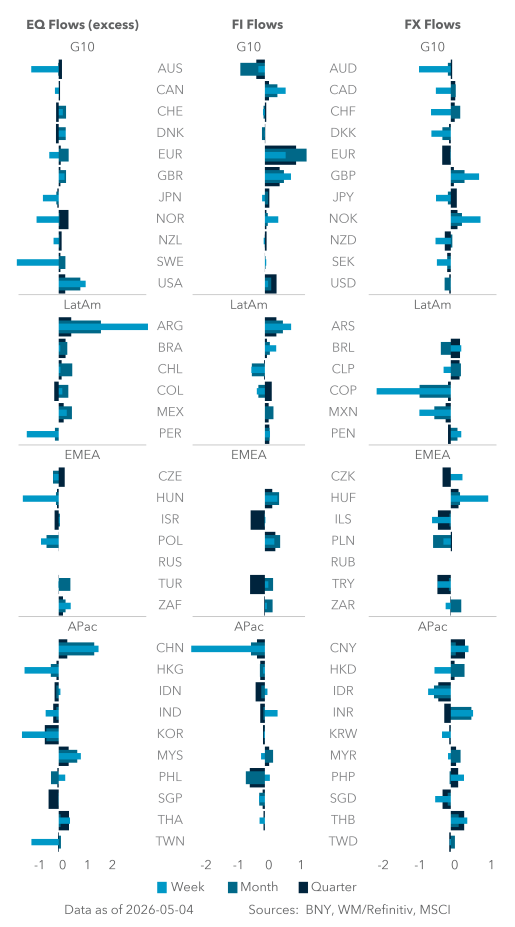

EXHIBIT #1: WEEKLY SCORED HOLDINGS VS. FLOW FOR HIGH-YIELDERS

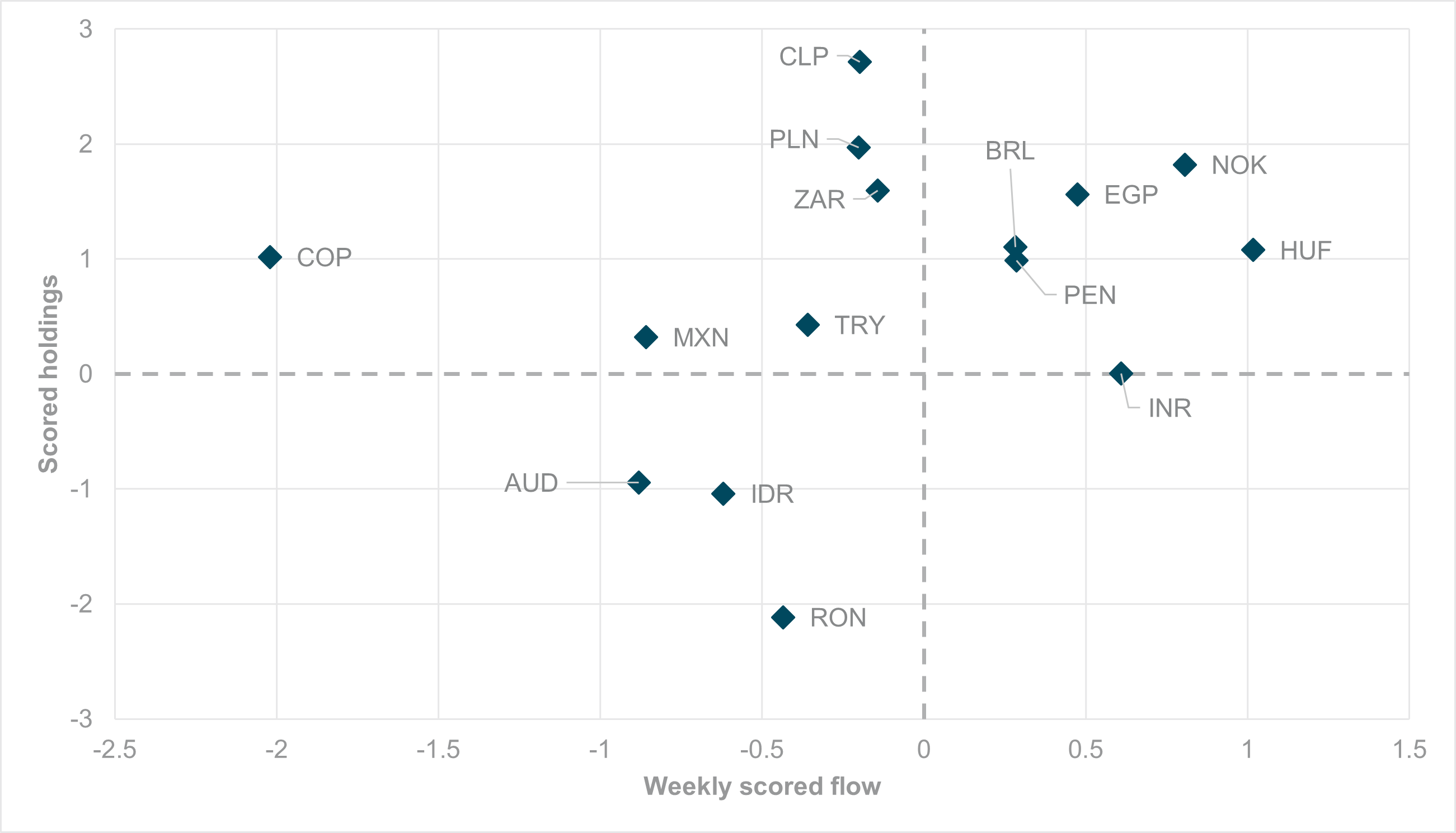

Source: BNY

Our take

For one session last week, our iFlow Carry index touched negative statistical significance. This means that there was strong inverse alignment between currency sales and their corresponding 10y bond yields (where available). At first glance, the carry trade remains resilient as central banks are almost uniformly hawkish. Out of the 15 we track across developed and emerging markets, 12 remain overheld and most still have a relatively comfortable buffer. However, over the past week, nine of the 15 were net sold, encompassing all regions and policy/fiscal views. Most of the flows appear to represent some “trimming” or light profit-taking, and only COP was strongly sold (flow magnitude above 1.0) through the week. However, after a period of resilience through sharp volatility and difficult balance-of-payments conditions, the market appears to have decided that the carry trade’s return profile has run its course.

Forward look

Our iFlow Carry indicator has yet to register an extended period of negative statistical significance this year. In addition, the two episodes from last year, encompassing reaction to “liberation day” tariffs in Q2 and AI-related valuations in Q4 – were the only such phases since 2022–2023, when central banks were also moving toward an aggressive tightening cycle, albeit in response to demand expansion.

Central banks meeting now are signaling that demand is weakening, and rate cuts will follow as soon as conditions allow. Hence, if markets are now looking past resilience to the conflict as a positive driver, the balance of risks will shift to how to stimulate growth thereafter, and lower nominal rates will be a part of that story.

If the carry theme fully preempts such an outcome for H2 – especially in emerging markets, which account for the bulk of positions – profit-taking on longs could speed up quickly. This dynamic could materialize even before Fed easing pushback moves to the fore.

EXHIBIT #2: KRW MONTHLY SMOOTHED FLOW VS. SOUTH KOREAN EQUITIES

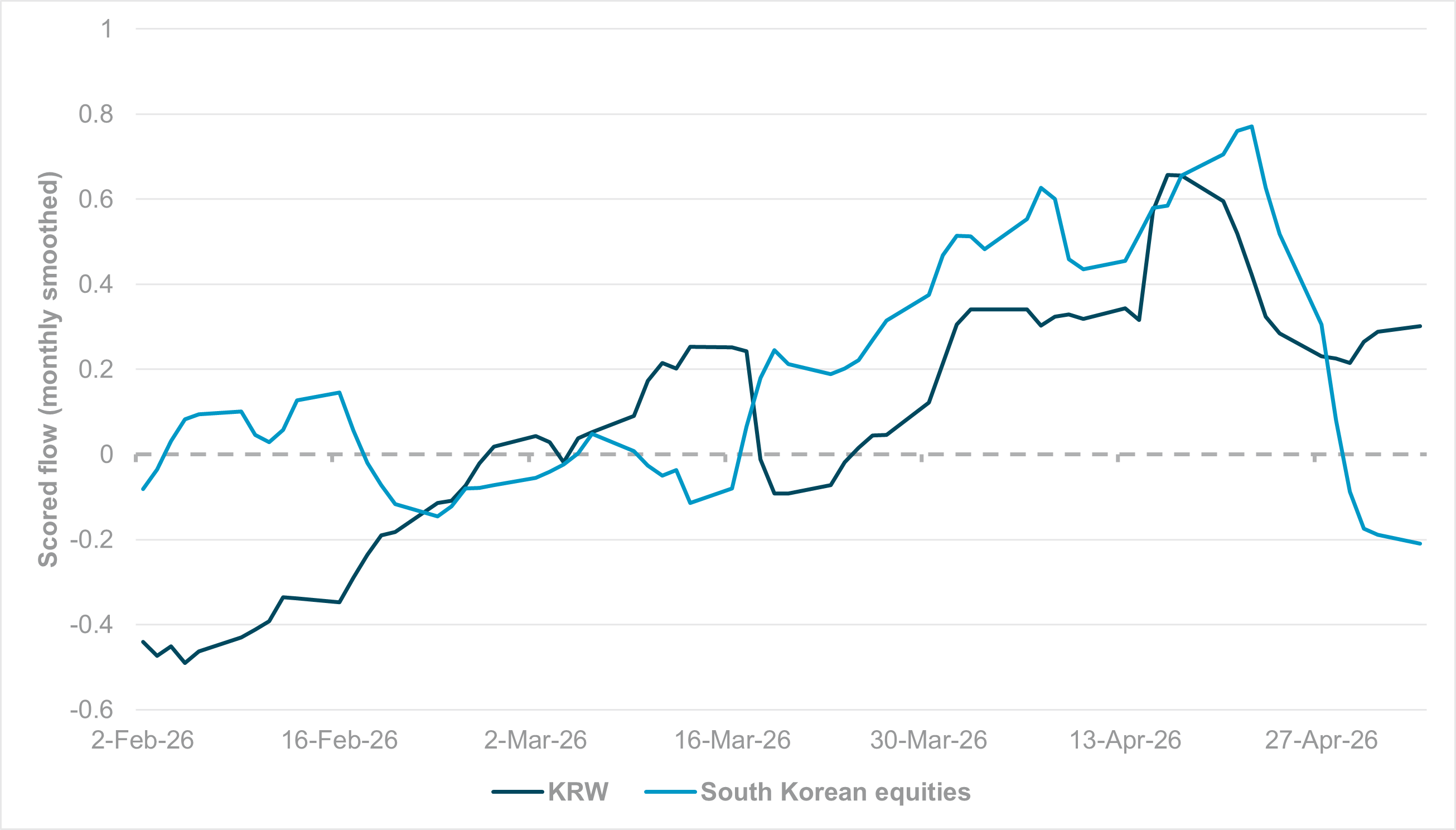

Source: BNY

Our take

Equity holdings remain unsurprisingly concentrated. The best-held major developed markets are Canada and Norway, reflecting the energy theme. The best-held large emerging markets are South Korea and Taiwan, reflecting the semiconductor theme. After being extremely well-held heading into the Iran conflict, South Korean equities faced a dry spell, but from mid-March onwards, markets evidently decided that the theme itself was secular, and earnings could deliver independently of supply risks. However, holdings have struggled to recover prior losses, especially among institutional investors, and the past few weeks have seen a sudden reversal to the extent that South Korean equity flow on a monthly smoothed basis reached the lowest point since early February.

Valuations and earnings are a recurring theme and a similar shock in Q4 2025 did not derail the AI theme in related global equity markets. Fundamental factors can be overcome, but we believe cross-border investors’ total exposures (asset + FX) are also looking excessive, given the most recent round of purchases appear to have very little hedging interest.

Forward look

Due to low headline rates, KRW has traditionally served as a funding currency, but this has changed in recent months, as cross-border investors have been increasingly willing to own KRW on an outright basis due to seemingly attractive valuations. The conflict-driven damage to balance of payments should have extracted a near-term discount on the KRW, as was the case in 2022–2023. In contrast, current KRW flow alignment with South Korean equities is very strong.

The last few sessions have seen some deterioration in KRW interest, but currency flows are now even outperforming equity interest. Japan’s latest round of USDJPY intervention could further reveal downside USDKRW potential, and we suspect South Korean authorities are not averse to allowing some appreciation to offset pass-through.

We do not dispute the positive case for flows, but on a combined basis, cross-border holdings in South Korean assets remain at extremes through both channels. KRW is 18% above its rolling 1y average magnitude, and South Korean equities are 61% above theirs – both outliers relative to peers, with equities likely concentrated in a handful of names.

EXHIBIT #3: MXN MONTHLY SMOOTHED FLOW VS. MEXICAN BONOS

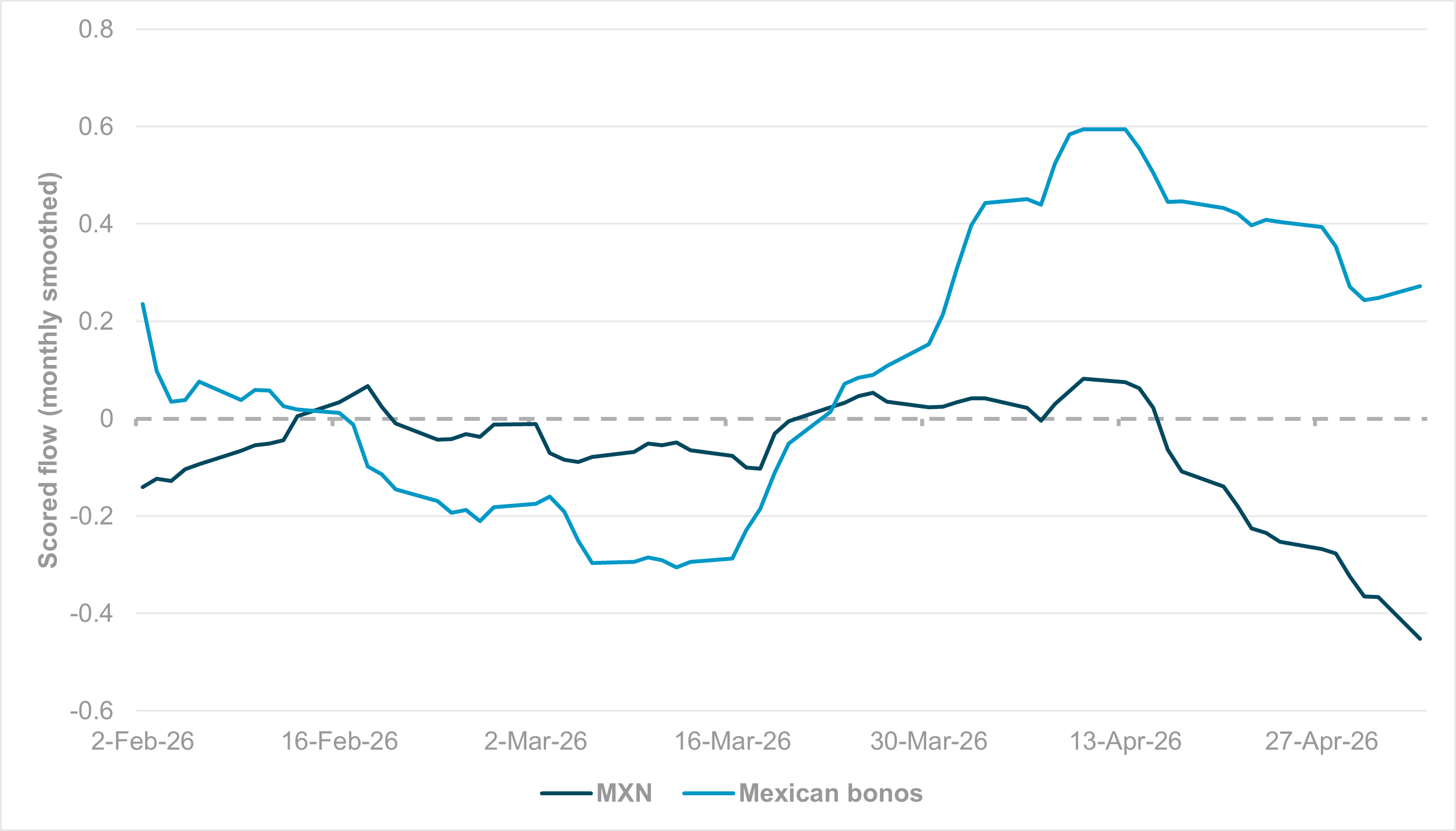

Source: BNY

Our take

iFlow signaled throughout this year that Latin American equities and Latin American currencies are now essentially the same position: every Latin American currency remains net overheld. Until recently, every single sovereign bond market in the region was also comfortably overheld. Despite offering liquidity and good real yields to complement cautiously hawkish central banks, these holdings are finally starting to reverse, but progress is uneven. In Brazil, holdings are particularly volatile, but there has been clear co-movement between bond and FX flows through April. In Mexico, we are seeing the clearest evidence yet that forward or even realized expectations for lower rates are starting to generate additional hedging interest, even if interest in sovereign bonds remain firm. As we head into the Banxico decision later this week, where a 25bp cut is expected, the market is likely viewing the Mexican policy approach as in stimulus/growth mode. After all, Mexico benefits less from energy-driven terms-of-trade gains than its regional peers. Meanwhile idiosyncratic risk from the U.S. is high, both from swift transmission of less dovish policy expectations and any challenges in upcoming trade negotiations.

Forward look

The question is whether the “total return” theme in Latin America can decline outright. Banxico does appear to be an outlier in global emerging markets, whereby the real rate buffer is being compressed to the absolute minimum (we believe 100bp is needed to justify positive real rates), but the central bank is pre-empting idiosyncratic downside risk.

Growth factors are clearly coming into play across the region. Brazil’s latest COPOM minutes acknowledged that rate hikes have “slowed the economy,” and our flow data reveal a strong preference for CLP as a terms-of-trade play on a structural basis due to the conflict. Colombia, in contrast, is moving in the opposite direction, but starting from a high point means significant room to ease (e.g., 350bp in 2024) once easing is justified by inflation and growth outlook.

If markets (and the carry theme) are now “forward looking” enough in this respect, FX hedging will likely pick up in size, but fixed income can stay resilient as fiscal impulse is limited.