Cross-border holdings find new equilibrium

Appearing every Wednesday, Investor Trends provides a deep dive into patterns and behaviors in equity, bond and currency markets around the globe, underpinned with deeper macro insights.

Appearing every Wednesday, Investor Trends provides a deep dive into patterns and behaviors in equity, bond and currency markets around the globe, underpinned with deeper macro insights.

Geoff Yu

Time to Read: 4 minutes

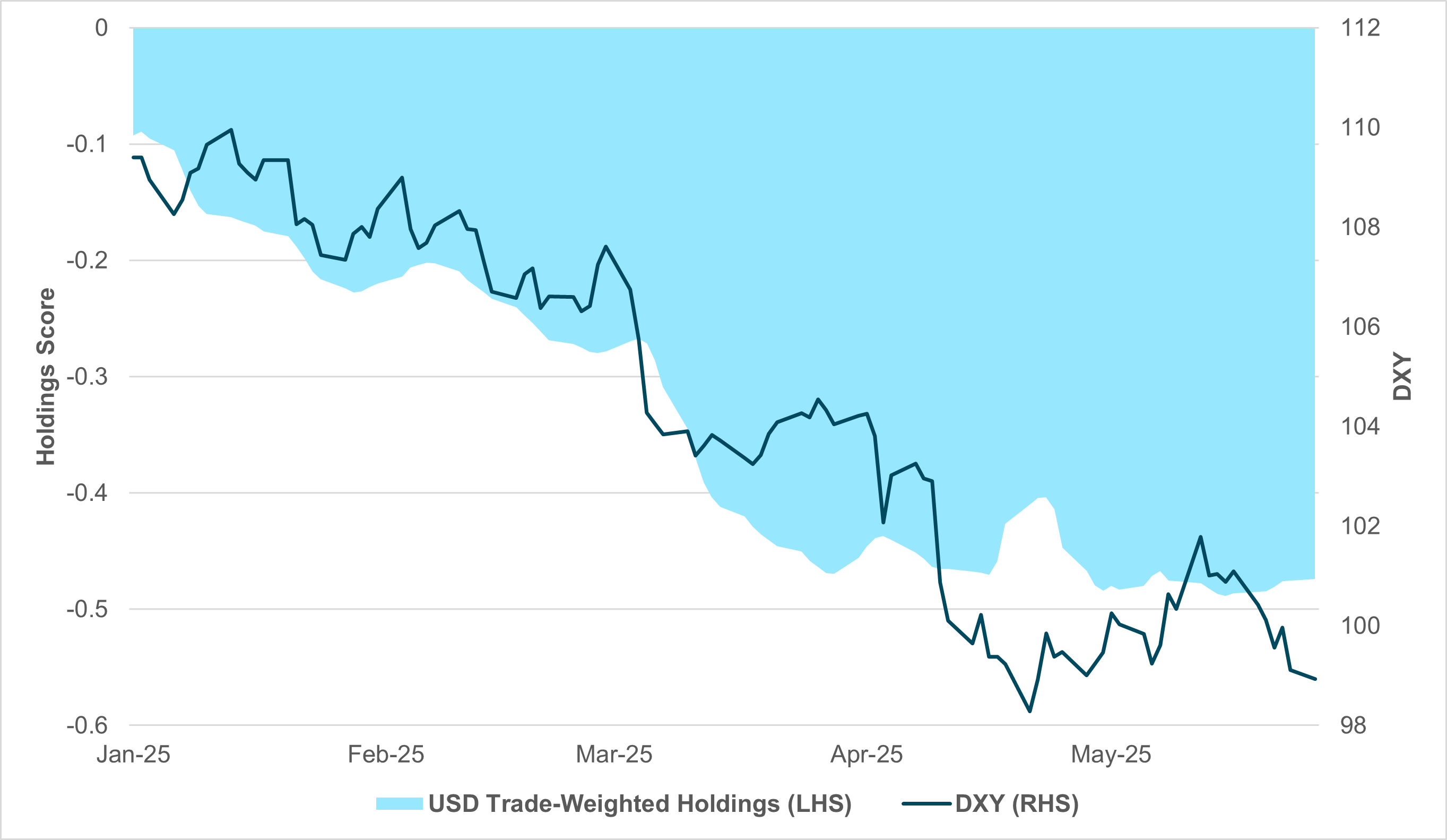

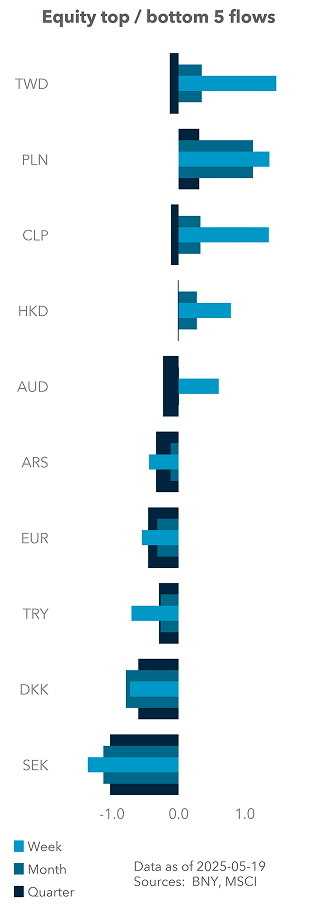

EXHIBIT #1: USD’S TRADE-WEIGHTED HOLDINGS VS. DXY

Source: BNY

Risk sentiment is closing out May on somewhat firmer footing compared to the more cautious tone that prevailed in April. While tariff concerns have not been fully resolved, there are now established mechanisms between the U.S. and its key trading partners that help contain the likelihood of a material escalation. This has contributed to a reduction in associated risk premia across equity markets. However, a new concern is emerging in the form of bear steepening, and investors continue to exhibit very limited tolerance for stagflation dynamics – regardless of whether they stem from supply or demand-side pressures. The U.S. appears particularly vulnerable to fiscal dominance and supply-driven inflation risks. Yet, in an environment where investors remain committed to cross-border positioning in both equity and fixed income markets, the dollar has increasingly become the primary vehicle through which broader shifts in risk appetite are expressed.

Our take

According to iFlow data, the dollar’s trade-weighted holdings – largely shaped by cross-border investor flows – have declined steadily since the start of the year. Initial moves were primarily valuation-driven, but there was a clear acceleration in outflows during late March and early April, coinciding with a notable drop in the DXY. Since mid-April, however, dollar holdings appear to have stabilized. We believe this shift reflects three key factors: improved valuation support, a moderation in asset surge flows, and the market’s adjustment to a less dovish outlook from the Federal Reserve.

Forward look

Looking ahead, we expect the dollar to remain under pressure into the next quarter. Preliminary signals from month-end rebalancing do not suggest a strong return of positive inflows. That said, cross-border positioning now appears more balanced in terms of asset allocation and valuation. While trade and fiscal policy developments continue to pose potential sources of volatility, the dollar’s new equilibrium should cushion against most episodes of risk aversion – absent shocks significantly larger than those experienced in April.

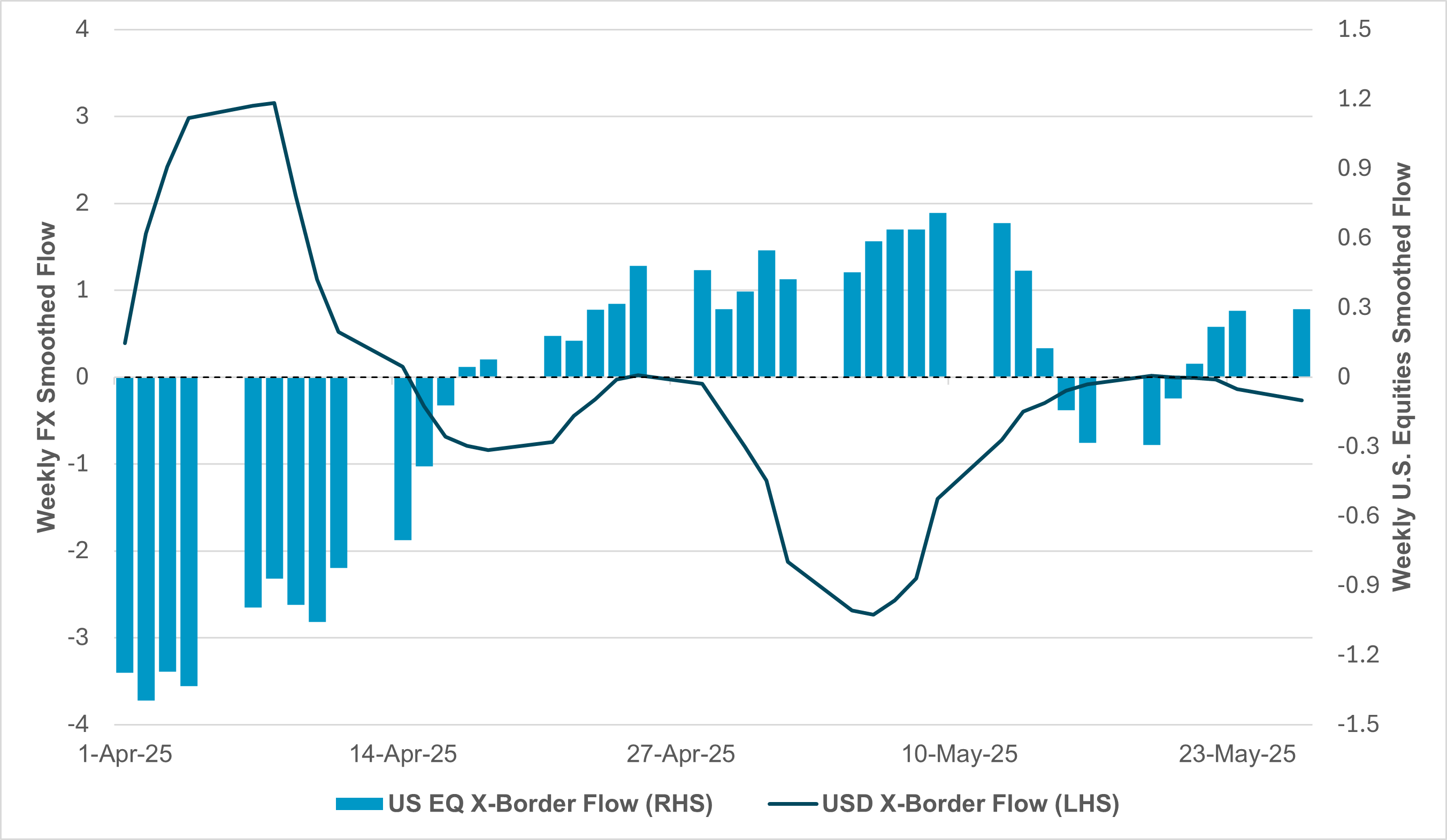

EXHIBIT #2: CROSS-BORDER WEEKLY SMOOTHED FLOW, USD VS. U.S. EQUITIES

Source: BNY

Over the past two years, the “U.S. exceptionalism” trade has been defined by strong investment flows into U.S. assets, typically with minimal use of FX hedging. That dynamic shifted notably in April. Weekly smoothed iFlow data show a near-perfect inverse relationship between cross-border equity flows and dollar flows during this period. Initially, we observed heavy outflows from U.S. equities in response to rising tariff concerns, accompanied by strong inflows into the dollar – suggesting that investors were actively unwinding hedges. Following the suspension of most tariffs (excluding China), this pattern reversed. While the rebound in flows was more gradual, the net effect across the month was a set of offsetting movements in both asset classes, setting the stage for a more complex interaction through May.

Our take

Measured by scored flow, FX flows were significantly more intense than the corresponding equity moves. While other asset classes contributed to these FX dynamics, it is often during unwinding episodes that latent positioning in a currency becomes most visible. Entering April, dollar exposures were already elevated due to the prevailing “exceptionalism” narrative. Despite light hedge ratios – likely a function of fund mandates – strong underlying U.S. allocations meant that any FX adjustments translated into large nominal flows. This underscores the scale of passive hedging activity embedded in cross-border portfolios.

Forward look

Our equity holdings data now show that notional positioning in U.S. assets by international investors is roughly in line with the one-year rolling average, though still below recent peaks. Over the past week, cross-border clients have begun to re-engage with U.S. equities, albeit without signs of renewed hedging pressure. The wave of hedging flows seen in late April and early May appears sufficient to manage current dollar risk, especially as valuations are more attractive. If supported by fundamentals, U.S. equity inflows can resume, potentially lifting the dollar alongside.

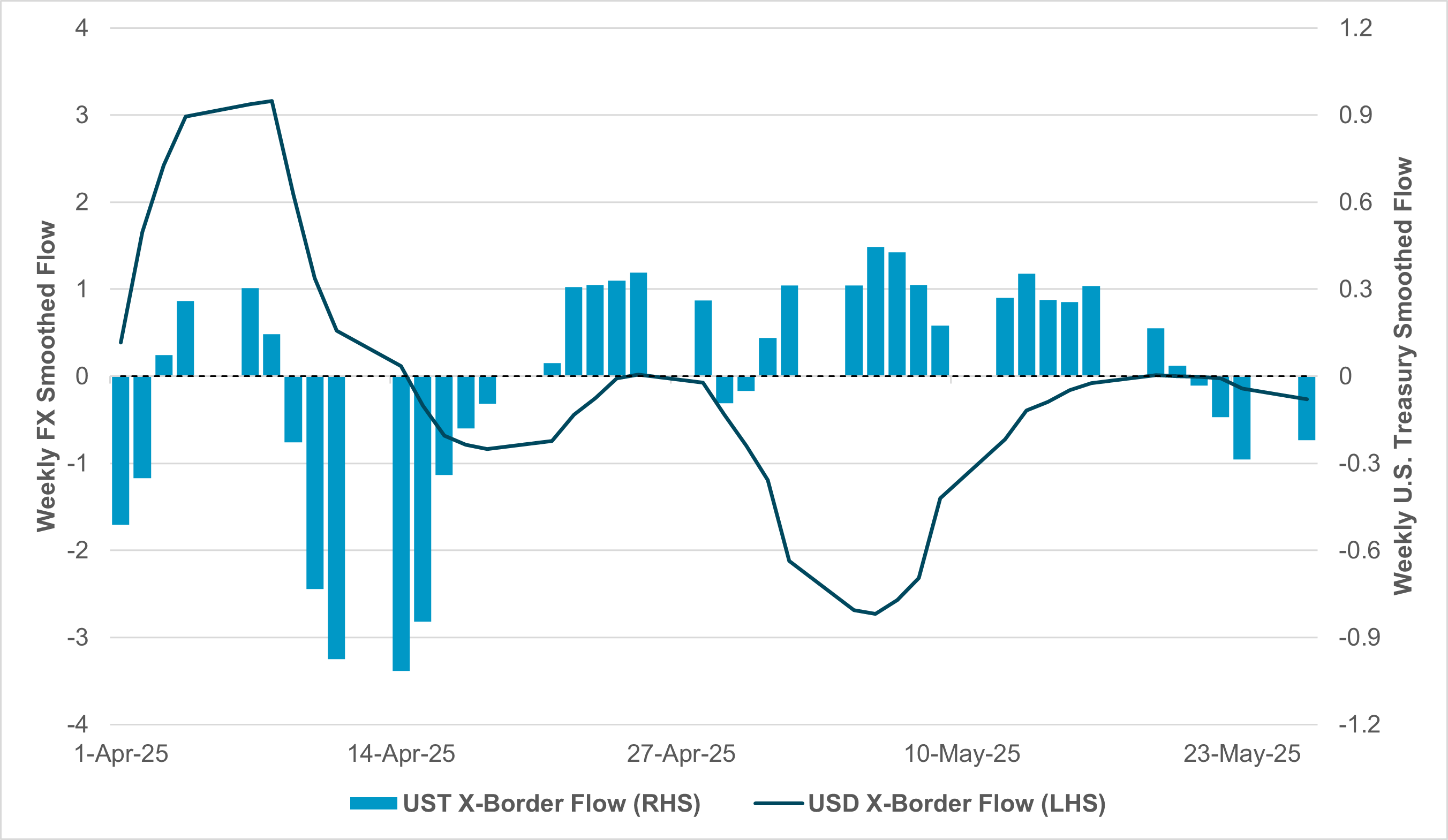

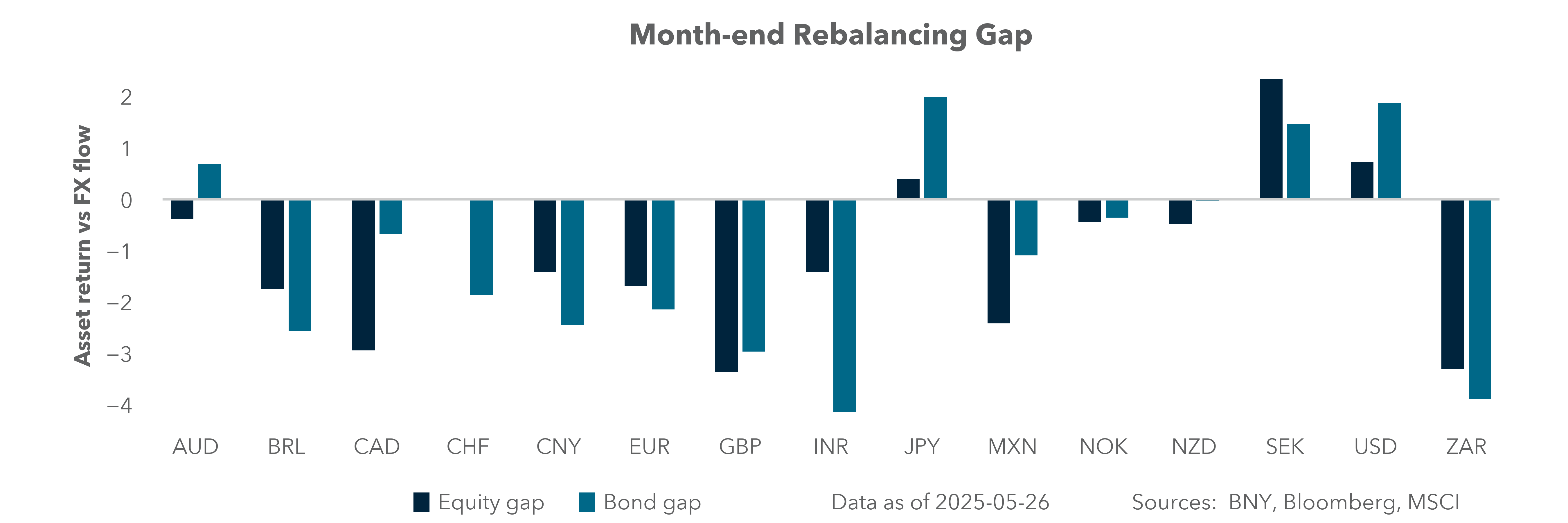

EXHIBIT #3: CROSS-BORDER WEEKLY SMOOTHED FLOW, USD VS. U.S. TREASURY SECURITIES

Source: BNY

Cross-border flow patterns in U.S. Treasurys have closely mirrored those seen in U.S. equities over the past eight weeks. Outflows were evident in April, though they occurred slightly later than in equities. From the final week of April onwards, we observed a more sustained period of inflows. While the timing of hedge unwinding by cross-border investors aligns more closely with equity flows, we believe the broader dollar selling seen through late April and early May was primarily driven by renewed inflows into U.S. Treasurys – particularly concentrated in the long end of the curve.

Our take

The current round of bear steepening raises the possibility of a repeat of the April dynamic. In our view, fiscal concerns present a more fundamental challenge to the reserve and haven status of U.S. Treasurys than short-term trade developments. Despite this backdrop, our data continue to show steady inflows into the 10+-year segment of the curve, likely reflecting attractive valuations relative to both current yield levels and the dollar. However, these inflows have been partially offset by selling in other well-held parts of the curve, leading to continued net outflows on an aggregate basis. This has likely contributed to more balanced dollar flows.

Forward look

Given the elevated fiscal risks in the U.S., it is likely that hedging activity among international investors in U.S. Treasurys has increased at the margin. Still, we believe that outflows would have been more pronounced had starting positions and valuation levels been less favorable. As it stands, we anticipate a holding pattern to dominate in the near term, particularly as markets await further clarity on the U.S. budget process and its progress through Congress.

Markets will not hesitate to extract a higher risk premia if fiscal credibility is questioned, but the bar for incremental dollar sales is now higher due to Fed expectations and current positioning. The recovery in U.S. exposures has been accompanied by far greater caution over excessive currency exposures. Light rebalancing-related purchases aside, this is likely the new reality for the dollar, which in fairness is not unwelcome for U.S. policymakers seeking accommodation in financial conditions in any shape or form.