Watching Not Waiting

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 12 minutes

Investors are heading into the upcoming IMF meetings on high alert, looking for signs of a global mood shift. Behind the scenes, U.S. President Trump and China’s President Xi remain deadlocked on trade, while markets brace for a potential “catch-up” correction after missing critical U.S. jobs and inflation data. All eyes now turn to Q3 earnings for confirmation of consumer resilience and the true extent of tariff pass-through pricing.

Yet the hunt for facts didn’t stop markets from moving sharply last week. Japan’s new LDP leader, Takaichi, and fresh cross-investment schemes among AI companies triggered a surge in the Nikkei, a slide in the yen beyond ¥152 and rising Japanese government bond yields – reflecting Takaichi’s push for bigger fiscal stimulus and less Bank of Japan support. Intervention fears resurfaced as the yen weakened, mirroring emerging market reality when the U.S. Treasury stepped in to defend Argentina’s peso. The peso now hovers just below 1,400 as President Milei prepares for a challenging October 27 midterm election, with currency stability vital to his reform agenda.

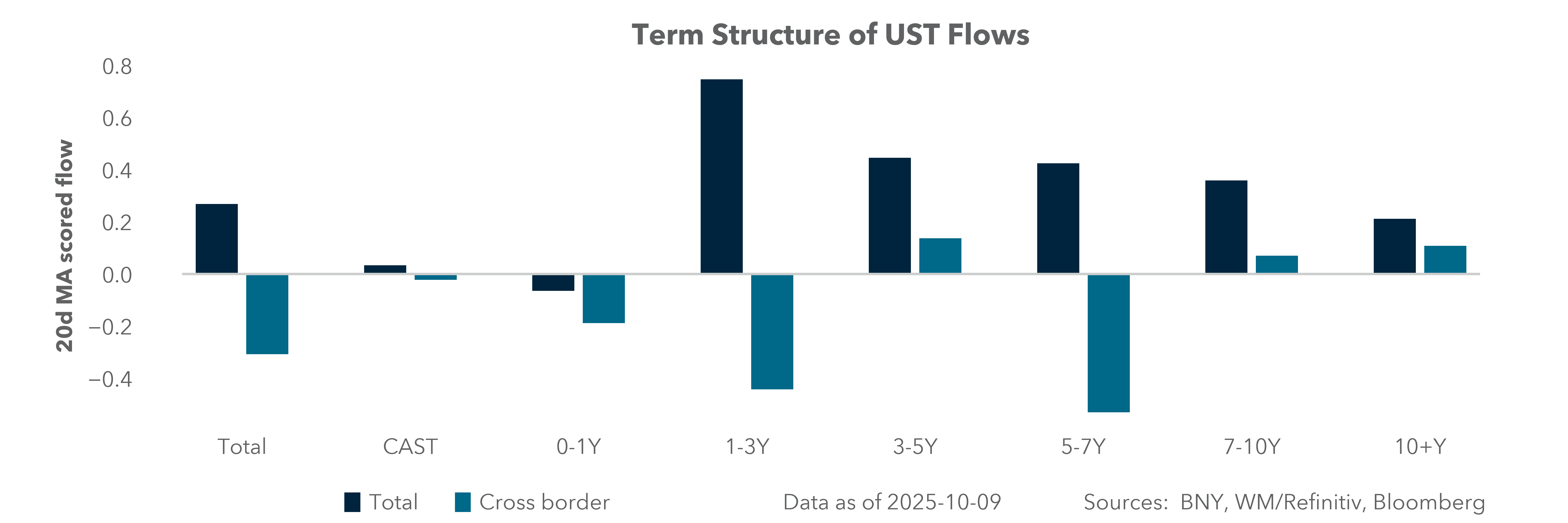

Meanwhile in Europe, political turmoil in France drove the euro below $1.16 as the country awaits its sixth prime minister in two years. Across the Atlantic, the U.S. dollar climbed 1.7% on the week, pushing the dollar index back to July highs. Equity markets slowed their third-quarter rally amid bubble and valuation concerns. Tech shares rallied early before fading late in the week, giving up over 2% of their gains and matching blue chip losses. Gold continued to shine as a hedge against both equity volatility and dollar strength – an outperformance at odds with the dollar’s rebound and a rethink of U.S. rates as we head into 2026. U.S. bonds markets rallied further despite the coupon supply and Federal Reserve minutes hinting at a reluctance to cut rates aggressively.

In the week ahead, the focus will be on U.S. private sector data, Asian trade figures, European inflation readings, hopes for a Senate deal to reopen the U.S. government, France’s budget plan and Q3 earnings.

Will U.S. housing bounce back and be a factor in Q4?

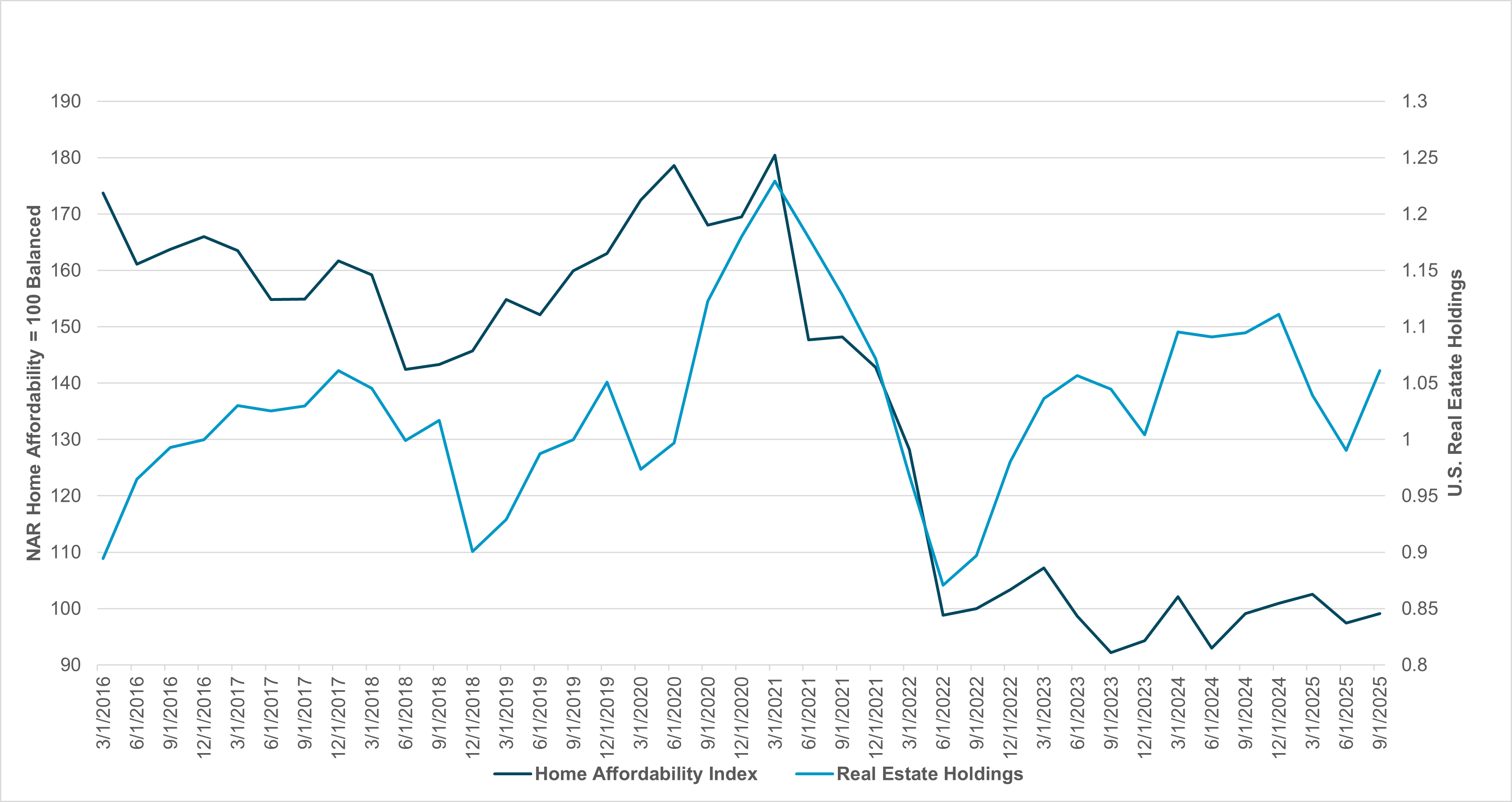

EXHIBIT #1: U.S. HOME AFFORDABILITY VS. IFLOW U.S. EQUITY REAL ESTATE HOLDINGS

Source: BNY, NAR

Our take: The focus of Q3 earnings will be on not only Big Tech, but also consumers and interest rate-sensitive sectors like housing and automobiles. Banks will be the first to report next week, but we’ll also see the National Association of Realtors’ Home Affordability Index (HAI) for October. This report usually doesn’t move markets, but given the focus on rates – with mortgage rates back to 2022 levels at 6.3% – investors are keen to see improvements. NAR home affordability is not just about mortgage rates but also buyers’ income, credit and the supply of homes driving prices. The balanced level is 100, where the average cost of a home matches the average income needed to get a mortgage and service it. The 10-year average for the HAI is 153. The same average for holdings in iFlow is 1.03.

Forward look: U.S. inflation risks in Q4 and beyond will be critical for both Fed policy and investors as they balance the U.S. dollar as a store of value against companies’ margins and their ability to absorb costs versus passing them on. The risk of a 3.5% y/y rise in core CPI in 2026 is an important factor for money flows. iFlow shows a significant increase in holdings of the construction and real estate sectors from August to now as a result of the change in U.S. rates and government efforts to fix the housing market. But boosting the supply of homes will take more than lower interest rate costs. Other factors that builders face include the cost of available properties, construction inputs from labor and materials and local income and taxes. Tariffs on lumber and steel and the impact of immigration policy on construction work (immigrants made up 15% of the construction workforce in 2024) are offsetting rate cuts and fiscal stimulus and adding to inflation risks.

The U.S. market focus remains on growth holding, inflation stable

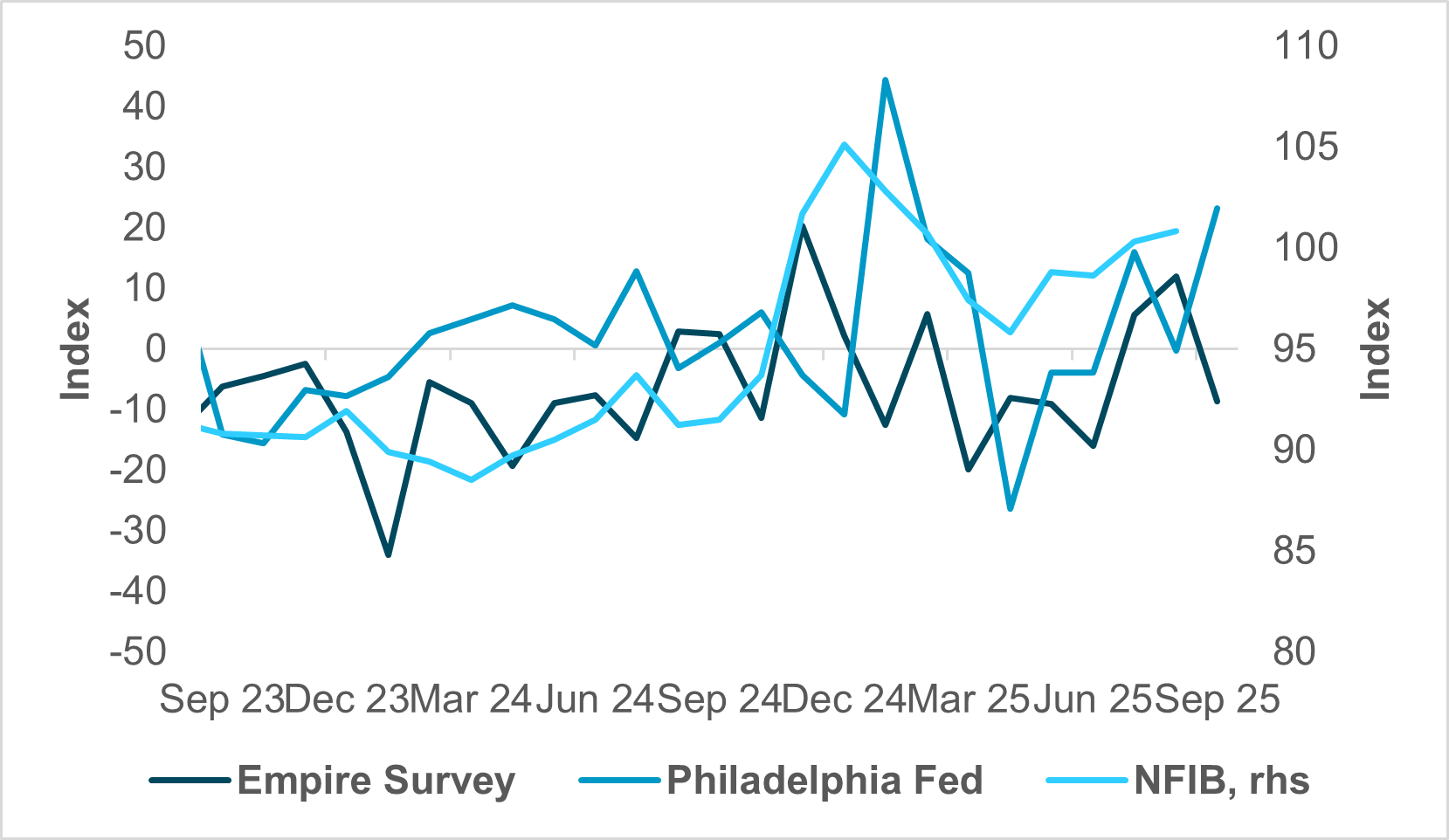

EXHIBIT #2: U.S. SURVEYS FROM THE NEW YORK FED, PHILADELPHIA FED AND NFIB

Source: BNY, Bloomberg

Our take: The news that BLS workers will be recalled during the shutdown for the express purpose of producing the CPI report in time for the FOMC meeting at the end of the month is encouraging, but as of this writing, we don’t have a great deal of visibility as to when exactly it will be published. However, we’re skeptical that it will be out this week. And while CPI data is undoubtedly useful, there are still a lot of other data that will still go unreported, leaving us once again with a light week of information.

Forward look: The data we do get will include a couple of regional Fed PMI surveys, with the Empire report due out on Wednesday, and the Philadelphia Fed reporting on Thursday. The National Federation of Independent Businesses (NFIB) will provide the monthly small business survey on Tuesday, and the National Association of Home Builders (NAHB) will publish its housing market index on Thursday. The most informative report will be published Wednesday afternoon when the Fed releases its Beige Book, a compilation of qualitative observations from local contacts of the regional Federal Reserve banks. In the absence of a slew of official macro data, the Beige Book could provide the best overall assessment of economic conditions.

EMEA: Inflation figures in play, France looks for some stability

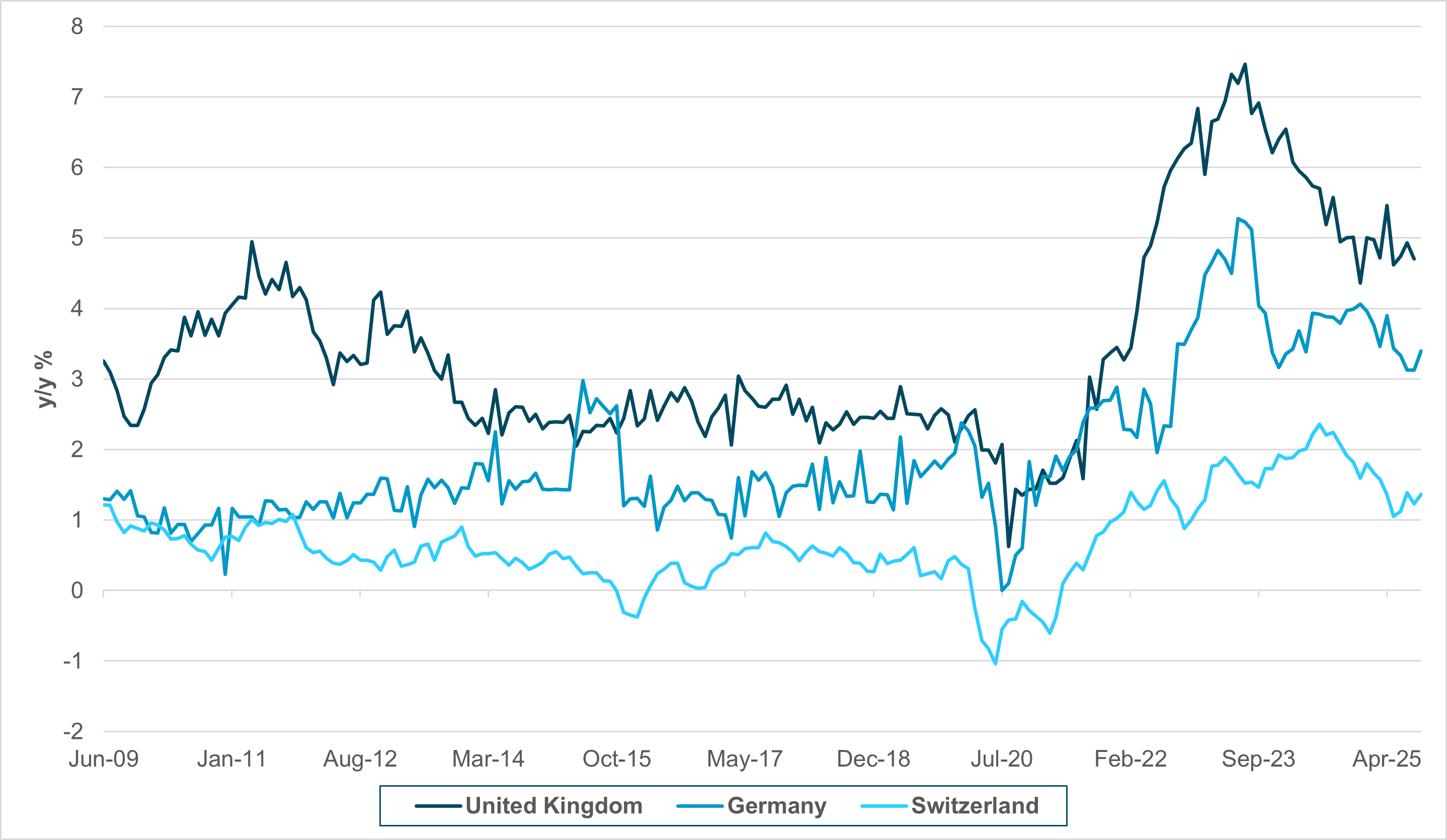

EXHIBIT #3: EXHIBIT #3: EUROPEAN SERVICES INFLATION STRUGGLES TO NORMALIZE

Source: BNY

Our take: Data releases will give way to speeches in the coming week in EMEA as ECB officials begin their guidance ahead of their end-of-October meeting. Barring extraordinary circumstances, the decision is unlikely to be “live.” But we do not think they will completely shut the door to a December cut. Final September CPI figures across the Eurozone will be released and are likely to show that core economies are at or above the inflation target, but we continue to see the mix of inflation as being suboptimal. Across Europe, the labor supply constraints which have kept services inflation robust remain in place (Exhibit #3) and this is disproportionately pushing up headline prices. Even in Switzerland, where headline inflation is struggling to stay positive, services inflation is running at a fairly robust 1.4% y/y, with little sign of downward momentum, even with the surprising escalation in economic challenges.

Where applicable, the excessive cost of labor will continue to be factored into corporate earnings and margins, representing a different form of tightening in financial conditions requiring an offset. However, as the RBNZ decision in October showed, a central bank can chose to overlook elevated non-tradables inflation if the external sector is starting to affect the economic outlook in the real economy, and this is something the ECB (and arguably, the hawkish elements within the BoE) will need to take into consideration. For example, the RBNZ noted that it was likely September inflation was “outside the target band” and “if inflation was to remain higher for longer than expected, there is a risk that this influences inflation expectations and wage- and price-setting behavior over the medium term.” Such comments are being echoed in Europe, but the RBNZ opted to move more than expected due to the level of spare capacity and because “excess precaution from households and businesses (has dampened) consumption and investment by more than currently assumed.” This is a much more forward-looking judgment which the ECB continues to push back against, even as trade tensions risk escalating again. The EUR’s failure to benefit from developments in the U.S. of late shows that markets are also wary of further tightening financial conditions through the exchange rate channel.

Forward look: ECB communication and inflation print aside, the focus remains on the situation in France, but whether any event will trigger a market response is another question. Even some ECB members are questioning its relevance, with Governing Council member Kazaks noting on Friday that he was not “seeing anything extraordinary,” perhaps hinting that an unstable government in France is now a fact of political life in Europe in the same way that Italy’s fractious politics were in the past. Sovereign debt spreads have normalized as well, and our data showed no sign of liquidation of French bonds across different maturity segments throughout the week. We do expect some caution if parliamentary elections are called – which is the market’s base case for later in the year – but even then the result will probably not break the deadlock. Slowing deterioration of public finances is a long-term concern but does not challenge the performance of OATs, especially with realized backstops from the ECB in addition to higher levels of joint EU issuance in the future as a source of support.

Outside of the Eurozone, the U.K. will release September labor market data and other output-related numbers. Any material drift below 4.5% in annualized earnings could even push the November BoE meeting toward “live” status, which appears to be the intent of Governor Bailey based on his recent comments, but opposition from other MPC members remains strong. In CEE, we continue to monitor the declines in asset positions, with HUF and Polish assets leading the deterioration as easing cycles are brought forward to contain real rates in the region.

APAC: China exports watching for the rebound and front-loading

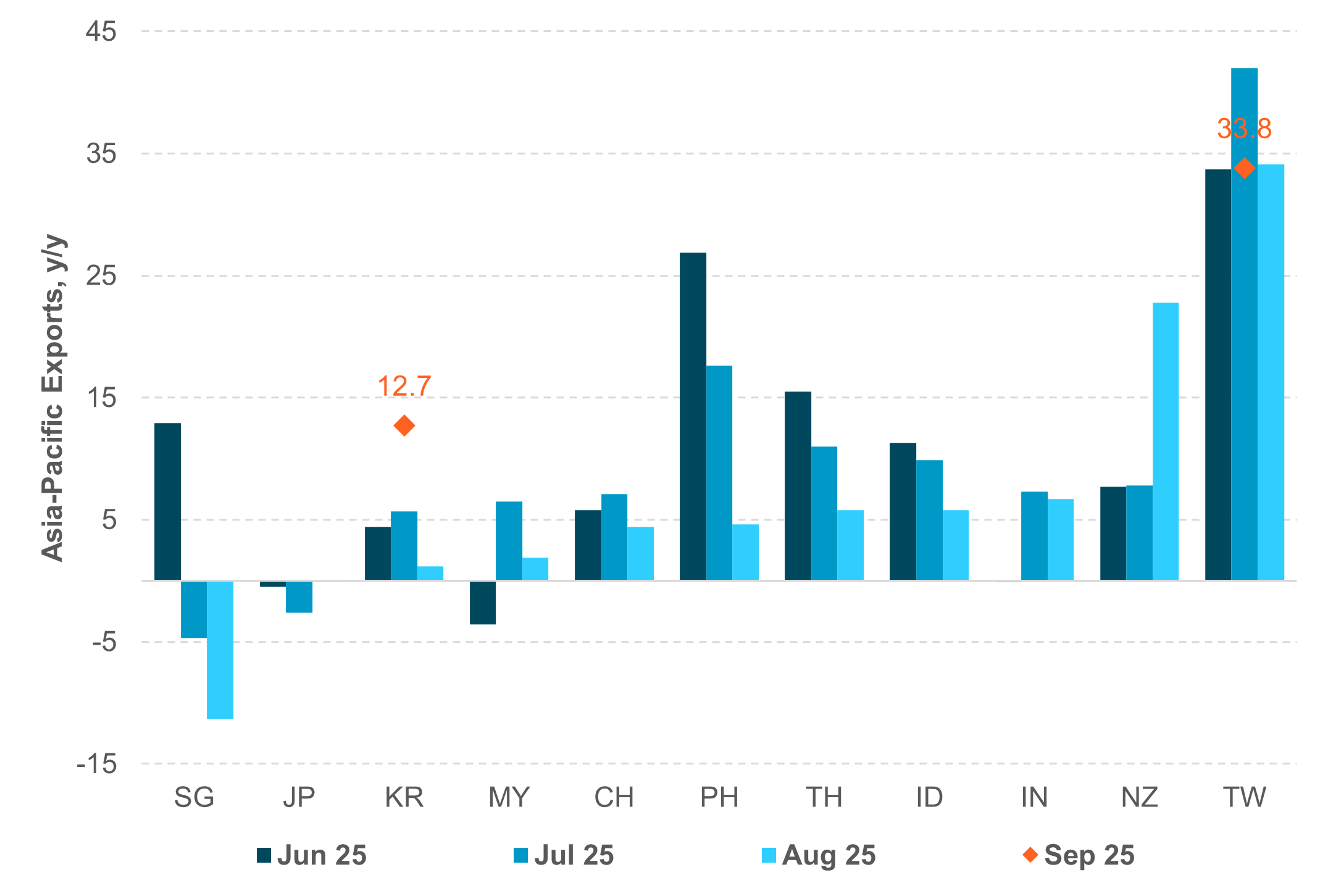

EXHIBIT #4: UNCERTAIN EXPORT GROWTH PROFILE FOLLOWING FRONT-LOADING ACTIVITIES

Source: BNY, Bloomberg

Our take: The focus in APAC this week is on China’s September exports and trade balance data as well as trade balance data from Malaysia, India and Singapore. South Korean export data for the first ten days of the month will likely be severely distorted due to an extended holiday in that country. India will release September inflation and wholesale prices, while South Korea will release the latest data on unemployment and bank lending to households. Singapore and Malaysia will release Q3 GDP. Elsewhere in the region, we will get Australia’s September business confidence and employment data, New Zealand’s Performance Services Index and food prices, and Japan’s nationwide departmental sales and industrial production data for September. Following the sharp rebound of South Korean exports in September to 12.7% y/y (August: 1.2% y/y), it will be interesting to see if there is a similar rebound in exports or if they continue to suffer following substantial front-loading activity in H1 2025. Chinese exports in August moderated to 4.4% y/y or 5.9% year-to-date y/y, while export growth in Singapore (–11.3% y/y) and Malaysia (1.9% y/y) was sluggish. India’s exports were steady at 6.7% y/y. We will also be paying attention to exports to the U.S., which stood at –33% y/y for China and –28.8% y/y for Singapore in August. South Korea’s bank lending data will be closely watched, with ongoing elevated housing prices. While bank lending growth has slowed on year-on-year basis at 3.4% y/y, the high monthly increase in lending to households remains a top policy concern. There have been reports of a possible fresh round of cooling measures as early as this week. Australia will release September jobs data, and the unemployment rate is expected to rise from 4.2% to 4.3% y/y. Sticky inflation in Australia is keeping the Reserve Bank of Australia (RBA) from easing further in the near term. India’s September CPI and wholesale prices are likely to drift lower, encouraging renewed interest rates cuts in December after a pause in August and October. Lastly, Malaysia and Singapore will release Q3 GDP data, with both growing at 4.4% y/y in Q2 2025.

On the monetary policy front, the Monetary Authority of Singapore (MAS) will hold its quarterly policy meeting. An uncertain growth outlook and disinflationary trend will likely lead MAS to maintain an easing stance but might not be sufficient to trigger policy action just yet.

Forward look: Aside from the ongoing timing of the end of U.S. government shutdown, the key near-term regional focus is the political disarray in Japan, with the collapse of the ruling LDP-Komeito coalition, and China’s fourth plenary session. While LDP leader Sanae Takaichi is the likely candidate to be the new prime minister, the loss of Komeito’ s support might mean greater barriers to implementing a new stimulus-inducing budget or stimulative measures. Japan’s government and ruling coalition are reported to be convening an extraordinary parliamentary session to vote on a new prime minister the week of October 20. Political uncertainty and anticipated fiscal stimulus led a depreciation of the yen by more than 3% last week.

The fourth plenary session of the 20th Communist Party of China Central Committee on from October 20–23 will be closely watched, with a focus on the 15th Five-Year Plan, China’s strategic roadmap for national economic and social development between 2026 and 2030. Market sentiment remains strong, as evidenced by the limited equities and currency market volatility on the back of the rebound of the U.S. dollar so far in October. We expect tech- and AI-related optimism and the potential bottoming out of China’s ability to attract foreign investors in the region.

iFlow equities data have shown persistent inflows to EM APAC since Q2 this year following outflows for the past three years. Within EM APAC, differentiation is in play, and we are negative on INR (tariffs concerns) and MYR (fiscal concern), but positive on CNY, KRW and TWD on capital inflows and IDR given its attractive valuation and the stabilization of sentiment. THB valuation has normalized from extremely stretched levels in early September.

The global investment landscape is entering a pivotal phase as IMF meetings coincide with mixed signals on inflation, growth and policy direction. These meetings will form a consensus view for investors that usually leads to position shifts across markets. U.S. investors face the delicate balance between resilient consumer demand and fading disinflation hopes, with upcoming Q3 earnings a key test of pricing power and margin sustainability.

In Europe, stubborn services inflation and political instability in France threaten to complicate monetary policy normalization, while Asia’s shifting political and trade dynamics – notably in Japan and China – inject both risk and opportunity. The U.S. dollar’s renewed strength underscores global caution, even as gold’s resilience hints at ongoing hedging demand. Looking ahead, investors must prepare for greater policy divergence and data-dependent volatility.

The coming quarter may favor disciplined exposure to quality growth and rate-sensitive sectors poised to benefit from eventual easing, while maintaining strategic diversification across currencies and regions amid an increasingly fragmented macro backdrop.

Central bank decisions

Singapore, Monetary Authority of Singapore, MAS (Thursday, October 14) – Singapore disinflationary pressure and lower projected GDP growth will likely lead the MAS to maintain an easing bias. SGD NEER valuation has eased a touch since its August highs but remains elevated despite an easing bias for far this year, including a flattening of the SGD NEER slope in January and April. We expect the MAS to maintain the status quo on SGD NEER at its October meeting. All eyes will be on a potential revision of the macro projection. MAS’s stance was neutral in July, when it said that “MAS is in an appropriate position to respond to risks to medium-term price stability.” In the meantime, front-end rates are likely to remain low in an effort to cap SGD appreciation pressure.

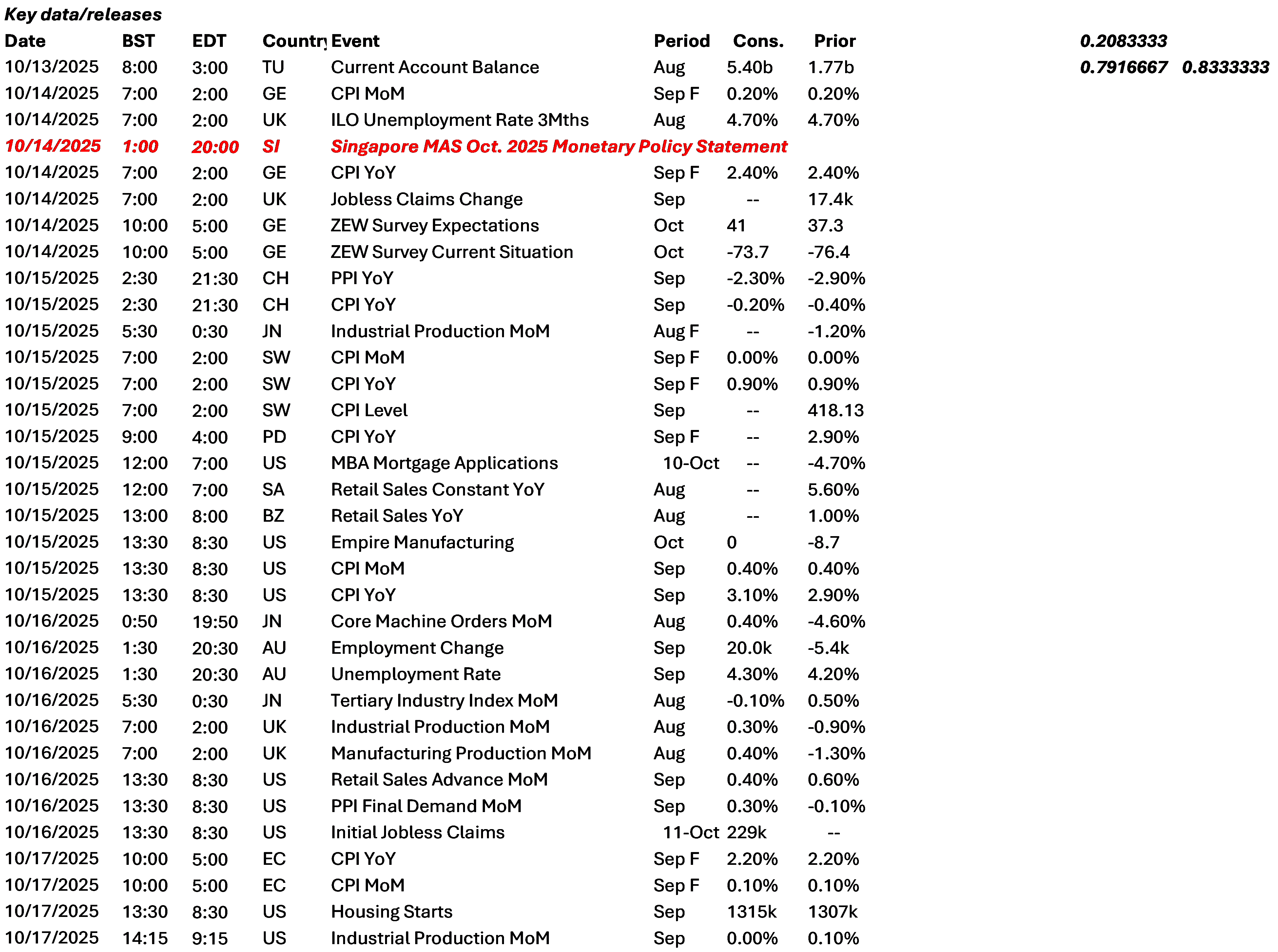

Data Calendar

Event Calendar