Venerable Markets

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 18 minutes

Bull markets may not die of old age, as the saying goes, but they can suffer from bouts of volatility, and that has been the case in August. Equity markets rose last week, but so, too, did price movements, as uncertainty over trade, growth, inflation and positioning outweighed hopes for a continuation of July’s market complacency. Last Monday saw the biggest rally by the S&P 500 since May, linked to expectations of a Fed rate cut in September. The rally experienced a reversal on Tuesday, as tariff deals with India, Switzerland, Canada and other nations failed to materialize. Stability returned on Wednesday, but Thursday saw a notable risk reversal, and Friday bounced back to leave the index up over 2% on the week. Paradoxically, the VIX fell by 5%, to nearly 15%, while actual volatility for the S&P 500 is up 2%. Next week isn’t expected to provide any less noise on prices given the ongoing focus on commodities, Trump’s likely meeting with Putin on a Ukraine peace deal, with significant implications for oil and natural gas markets, and significant economic data from the U.S. on inflation, China and the U.K. on growth, and rate decisions from the RBA and Norges Bank. The week after will see more rate decisions and the usual flash PMI reports along with the Fed’s Jackson Hole symposium, which is seen as likely to confirm or deny market hopes for a cut, with the Fed responding to weaker U.S. jobs and sticky inflation. Uncertainty has become a major part of 2025, and while markets look venerable in their ability to rally and see through it all, the risk of more reversals remains, with concern about the dollar and valuations driving the search for alternatives.

Passive retaliation risks to U.S. policy shifts show up in commodities and rates

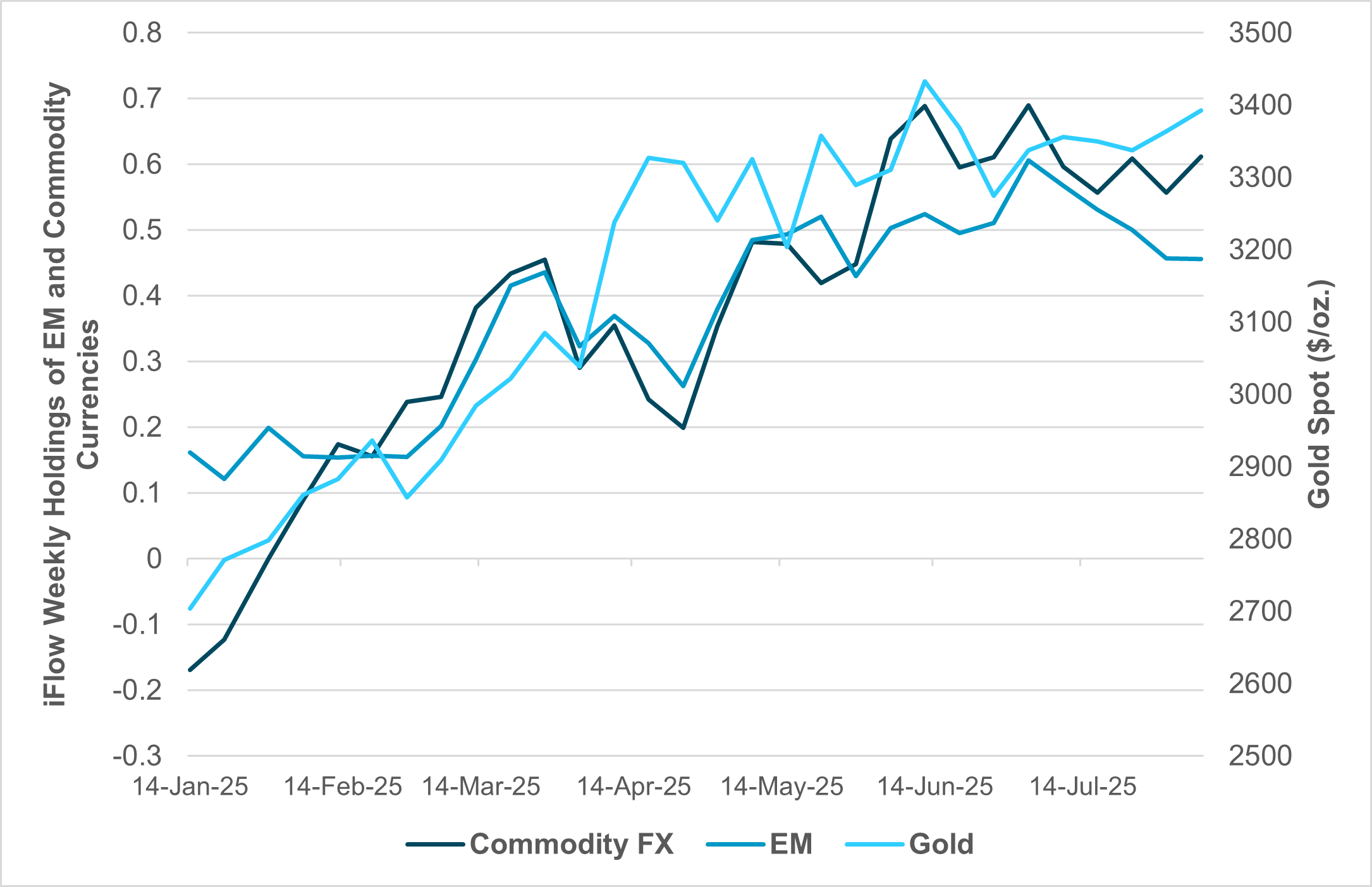

EXHIBIT #1: GOLD VS. IFLOW FX HOLDINGS OF EM AND COMMODITY CURRENCIES

Source: BNY, Bloomberg

Our take: In a significant move last week, the U.S. imposed a 50% tariff on India that caught the Indian government by surprise. INR lost 0.15%, touching new record USD highs at 87.89, while the Sensex stock index fell 0.9%. Indian PM Modi reached out to Russian President Putin and promised to deepen ties, while he also plans a visit with Xi. There is intense focus on the meeting this week between Trump and Putin, with the expectation that the two will discuss more than Ukraine. Investors are watching the meeting closely to see how it impacts alternatives to the dollar and U.S. shares, such as gold. Stagflation concerns have transformed gold into a venerable dollar alternative, while emerging markets have faded and become more idiosyncratic. Our iFlow data reflect this sentiment move up in EM, gold and commodity currencies this year, but the stall in EM stands out while commodity FX look for more momentum.

Forward look: Gold and tariff policy became intertwined this week, as the price of gold imported from Switzerland rose 39% (though the White House has since called this "misinformation" and intends to issue a clarification). The net effect is a weaker USD. But not all countries are feeling this impact, with commodity-linked FX currencies sustaining their winning position against the USD over the last month. Overall USD holdings have increased modestly over the past month and were flat on the week, even as the USD index fell 1%. Key events over the next two weeks should shift the USD focus from tariffs and peace deals to other factors like carry and safety, with U.S. data changing rate cut expectations and anticipated rate cuts in EM and commodity-linked nations like Norway and Australia. Market correlations are changing quickly, and investors are looking for safe alternatives in a world of uncertainty.

U.S. inflation to clash with politics and policy

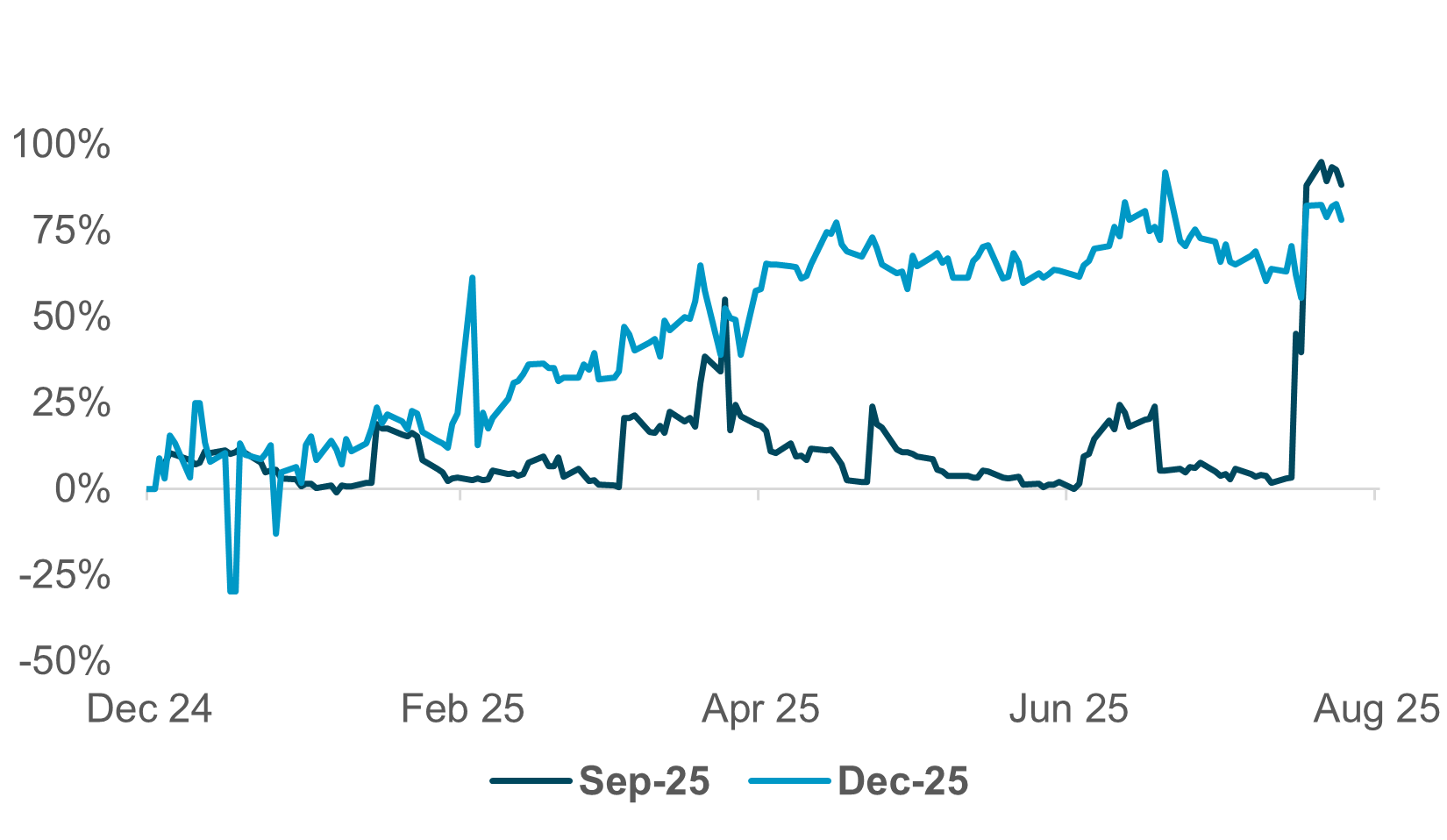

EXHIBIT #2: U.S. FED RATE CUT PROBABILITY IN SEPTEMBER AND DECEMBER

Source: BNY, Bloomberg

Our take: In the coming weeks, key U.S. economic indicators – including inflation data (CPI on Tuesday, PPI on Thursday), retail sales (August 15) and consumer sentiment – will provide insight into trends affecting Fed rate policy. While recent discussions cite a weakening job market as grounds for policy accommodation, inflation remains a concern due to emerging tariff effects. Additional releases will cover import prices, business inventories, capital flows and manufacturing activity.

Forward look: With the Fed continually under scrutiny and pressure from the Trump administration, the short-term appointment of current Chair of the Council of Economic Advisors Stephen Miran has added another consideration into the mix. Miran is a noted Fed critic, and an unabashed dove, almost certain to provide one more vote to reduce interest rates if he is in his seat on the Board before the September 17 FOMC meeting.

The Kansas City Fed will host the annual Jackson Hole Economic Policy Symposium from August 21–23. Although it has not been announced formally yet, it is a given that Fed Chair Powell will speak at the Friday session, a longstanding tradition. Depending on the data over the next two weeks, we could witness the Chair tease changes to interest rate policy at the September 17 FOMC meeting.

EMEA: Nordic divergence in play, Swiss to push for a settlement

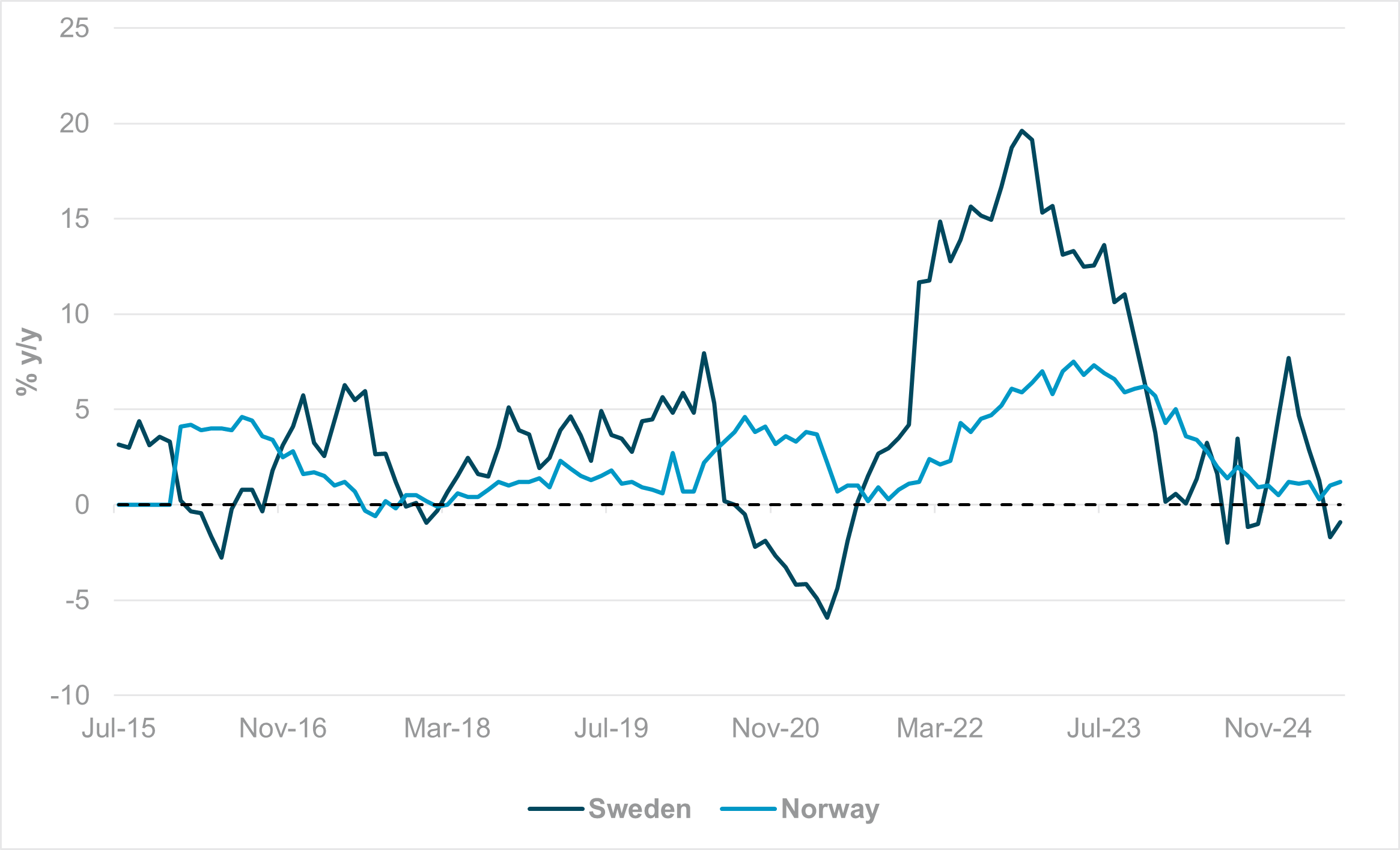

EXHIBIT #3: IMPORT PRICES FOR CONSUMER GOODS, NORWAY AND SWEDEN

Source: BNY

Our take: The Riksbank and Norges Bank will round off European central bank decisions for the summer in the coming weeks. Neither economy is particularly at risk of a tariff shock in the U.S., though Sweden will also need to monitor pharmaceutical tariffs, as there is a medium-sized industry in the country. Although the U.S.–EU deal proposed a tariff ceiling for all exports, including pharmaceuticals, the EU will note from Japan’s experience in its own sectors that nothing is set in stone, and the reaction function for individual companies across the Continent may also not align with national needs. Overall, Sweden and Norway’s economies remain subject to significant external risk and will need to align with pan-European and global conditions in the near term, with downside surprises in growth and inflation still the risk. Both central banks have higher exchange rate sensitivity via import price pass-through, and after a strong start to the year, FX gains have stalled, which normally should be supportive of CPI through the import channel. However, in the clearest sign yet that Continental demand is waning, imported consumer goods inflation (Exhibit #3) remains very depressed in both economies, and in Sweden’s case has turned negative again.

The Riksbank has repeatedly suggested that SEK is undervalued relative to fundamentals, but in a disinflationary environment encouraging a move to fair value may not be the best approach either. As the ECB is maintaining a holding pattern for now, there is scope for the Riksbank to passively shadow financial conditions, but this also means that the odds of a further move in September are high, and we doubt the Riksbank will rule out moves below neutral due to external risks. Meanwhile, barring a serious downside surprise below 3.0%, Norges Bank will remain on hold as well, as there is some more space in inflation to maintain current financial conditions, which the central bank no longer deems as “contractionary” for the economy. Nonetheless, the surprise easing in their last meeting points to more adverse scenarios materializing so nothing can be ruled out.

Forward look: We remain more partial to NOK even though Norges Bank has been surprising to the dovish side over the past quarter. Headline inflation levels continue to constrain policy space, and at best there will be room for one more cut as inflation continues to run at around 3%. Furthermore, the current price of oil means net selling of FX to support government finances will extend for several months, altering the balance of flow while there is no additional marginal downside impact on Norwegian terms of trade through the oil channel. Meanwhile, SEK valuations have corrected higher over the last 12 months, and we doubt the Riksbank will want to encourage further gains due to external risks, even though it sees the currency as undervalued.

Otherwise, the market’s focus will remain on Switzerland as the tariff shock continues to reverberate through the economy. The Swiss government appears far from a deal with the U.S., and less than 24 hours after the departure of an official Swiss delegation, the U.S has clarified that tariffs on imports of one-kilo and 100-ounce bars do not fall under the current exemption (pending confirmation, see above). Refined gold bars also comprise an extremely large share of Swiss exports to the U.S., and the country still has no protection from imminent pharmaceutical tariffs. We have long held the view that the franc can remain a key diversification destination provided tariffs are manageable. However, as things stand, the country is at risk of losing two anchors of the country’s current account surpluses, constituting a fundamental de-rating of the currency. Without a deal over the next month, the SNB may have to materially revise its growth and inflation forecasts and sharply reduce tolerance for CHF strength in real and nominal terms.

APAC: China growth and ongoing tariff uncertainty

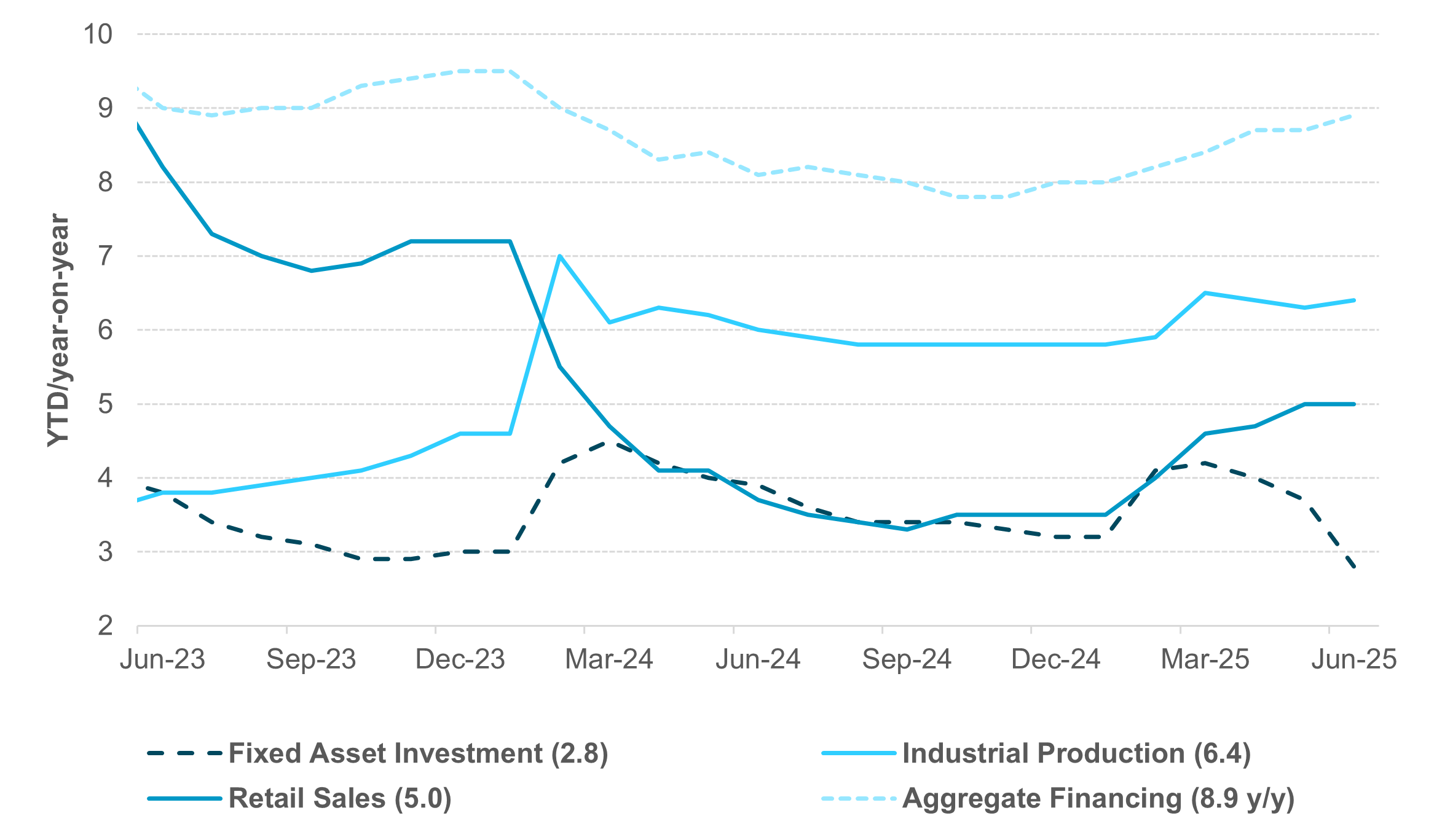

EXHIBIT #4: DIVERGENCE BETWEEN CHINESE FIXED ASSET INVESTMENT AND PRODUCTION

Source: BNY, Bloomberg

Our take: In the Asia-Pacific region, the focus this week will be on China, South Korea, the Reserve Bank of Australia and Bank of Thailand policy meetings. Better-than-expected Chinese exports in July (+7.2% y/y) have boosted the outlook for H2. Continued divergence between soft fixed asset investments and steady industrial output reflects ongoing real estate weakness and a shift toward high-tech sectors. July FAI is expected to slow to 2.7% ytd y/y (June: 2.8%), while industrial production may ease to 6.0% y/y (June: 6.8%). The high-tech sector, especially industrial robots (+37.9% ytd y/y), will be closely watched. Domestic consumption is expected to slow slightly to 4.6% y/y from 4.8%y/y in June. July housing data will be scrutinized after June’s disappointing figures: new and used home prices fell –0.27% m/m, –3.7% y/y and –0.61% m/m, –6.1% y/y, respectively. South Korea’s first 10-day export data will offer an early read on August exports and tariff impact. Household bank lending rose by KRW 16tn in Q2 (Q1: KRW 4tn), a key input for the Bank of Korea. Taiwan, Singapore and Malaysia will release final Q2 GDP (flash: 7.96%, 4.3%, 4.5% y/y). Japan’s Q2 GDP is expected to rebound to 0.1% q/q, 0.3% y/y from flat growth in Q1. India will publish July CPI and exports data, overshadowed by U.S. tariff tensions targeting up to 50% of Indian imports.

South Korea’s 20-day export performance, Japan’s July CPI, and August PMIs for India and Australia will also be in focus. China’s August loan prime rate is expected to stay at 3.0% (1-year) and 3.5% (5-year). Despite trade headwinds, regional exports have remained resilient, aided by front-loading. While China’s and Hong Kong’s exports to the U.S. plunged –21.6% and –12.1% y/y, others outperformed: Taiwan (+91%), Thailand (+41%), the Philippines (+35%), Singapore (+21%), South Korea (+1.4%), Malaysia (+16%) and Indonesia (+25%) as of June/May 2025. New U.S. tariffs, including a 40% penalty on countries aiding Chinese transshipments, will be closely watched for trade impacts.

Japan’s national CPI is expected to soften following Tokyo’s print. Still, headline inflation remains above 3%, and core CPI (ex-fresh food and energy) rose to 3.4% y/y in July (from 1.9% in July 2024), reinforcing the case for BoJ tightening. India’s August manufacturing PMI is expected to stay strong after July’s 59.1 reading, matching March 2024’s high. Australia’s PMI (July: 51.3) is also expected to continue rising.

On the central bank side, consensus points to a 25bp rate cut by the Bank of Thailand to 1.5%. However, our view is that the central bank will hold rates steady, deferring any policy shift to the incoming BoT governor at the October meeting. Meanwhile, the RBA is expected to cut by another 25bp to 3.6%, while the Reserve Bank of New Zealand is anticipated to cut its policy rate by 25bp to 3.00%, as antipodean inflation remains well-anchored.

Forward look: Tariff uncertainties continue to linger across Asian economies, with the latest 50% levies on Indian imports to the U.S. (effective August 27) posing significant headwinds that might force the Reserve Bank of India to implement further rate cuts in Q4 2025. The RBI maintained rates unchanged in August, citing insufficient data to revise GDP forecasts amidst global uncertainty. Meanwhile, the broader 100% tariffs on semiconductor imports to the U.S. would materially impact Malaysia, Singapore and the Philippines – with semiconductors constituting 70% of Philippine exports (approximately USD 30bn in 2024), of which 15% (USD 6bn) are U.S.-bound – while South Korea and Taiwan face reduced exposure through exemptions for Samsung, Hynix and TSMC. Counterbalancing these tariff pressures are ongoing foreign investment inflows, USD weakness, and regional central banks' readiness to intervene against FX volatility. In China, recent Politburo comments have reaffirmed the commitment to macro policy support aimed at effectively unleashing domestic demand potential, with October’s fourth plenum of the party’s Central Committee set to discuss the nation’s next five-year plan. Overall, we remain constructive on Asia risk assets, underpinned by expectations of increased foreign investment inflows, a weakening U.S. dollar and supportive regional monetary and fiscal policies.

The next two weeks will deliver more volatility and likely more opportunities for investors who have clarity on where to put risk. The problem of uncertainty remains the biggest obstacle to growth and investments for the rest of the year, making traditional growth and trend strategies less attractive. Policy shifts on tariffs and geopolitical alliances are confusing global investors more than inspiring them. We have seen price shifts in gold, oil and copper, which are important to the bottom line of many companies and are, in turn, driving down hopes for better earnings. The news agenda ahead is hardly light and not kind to those setting up for last chance of summer vacations. There are three key points to consider before putting on sunscreen and heading to the beach:

While the weeks ahead will be busy, they won’t be frenetic, if only because of the lack of conviction and the timing of key events ahead. If August is uncertain, September could be chaotic.

Central bank decisions

Australia, RBA (August 12, Tuesday) – The Reserve Bank of Australia is expected to cut rates by 25bp at its August 12, 2025 meeting, bringing the cash rate down from 3.85% to 3.60%. June quarterly CPI, released by the Australian Bureau of Statistics on July 31, showed trimmed mean inflation slowing to 2.7% y/y – well within the RBA’s 2–3% target band – and headline inflation easing to 3.1% y/y, with the monthly indicator for June falling to just 2.0% y/y. This marks two consecutive quarters of core inflation inside the target range, fulfilling one of the RBA’s key preconditions for easing. Market pricing reflects near-certainty of a 25bp cut, and Governor Bullock noted in her recent speech that monetary policy is “restrictive” and must now be assessed considering weakening domestic demand. This meeting will also include updated forecasts in the Statement on Monetary Policy.

Thailand, BoT (August 13, Wednesday) – Market consensus is for Bank of Thailand to cut rate by 25bp from 3.85% to 3.60%, on the back of sharp disinflationary pressure. Note that July headline CPI at –0.7% is the fourth straight decline in inflation. We don’t disagree with the easing cycle, but our bias is for the BoT to wait for a full assessment of tariff impacts before making the move. The August meeting will be Governor Sethaput’s final policy meeting before Vitai assumes the role in October.

Norway, Norges Bank (August 14, Thursday) – There is a tail risk that Norges Bank will cut rates by 25bp to 4.00% at its August 14 meeting, following its surprise cut in June – the first since 2020 – which lowered the policy rate from 4.50% to 4.25%. June inflation data confirmed the disinflationary trend that prompted the earlier move: core CPI (CPI-ATE) rose slightly to 3.1% y/y, from 2.8% in May, but remains well below the 4.9% level seen at the start of the year. Headline CPI held steady at 3.0% in June, reinforcing the view that inflation is moving closer to target. The June Monetary Policy Report noted that inflation was falling faster than projected and that “the policy rate is no longer as contractionary.” Market pricing and recent surveys suggest further cuts are likely this year, but mostly likely Norges will wait until Q4.

Peru, BCRP (August 14, Thursday) – The Central Reserve Bank of Peru is expected to hold its reference rate at 4.50% at its August 14 meeting. In June, headline inflation rose 0.13% m/m and core inflation increased by 0.07% m/y, while year-on-year rates remained at 1.7%, comfortably inside the 1–3% target range. One-year-ahead inflation expectations were anchored at around 2.3%, reflecting confidence in price stability. In its July 10 Monetary Policy Statement, the Board underscored that future rate adjustments will be conditional on added information regarding inflation dynamics and external factors. With the current neutral real policy stance and no emerging inflationary pressures, markets anticipate the BCRP will maintain rates for now.

New Zealand, RBNZ (August 20, Wednesday) – The Reserve Bank of New Zealand is expected to cut rates by 25bp to 3.00% at its August 20 meeting. June quarterly headline CPI inflation eased to 2.7% y/y, within the 1–3% target band, while core inflation moderated to 2.8%, reflecting subdued domestic price pressures. Unemployment rose to 5.2% in Q2, with employment dipping 0.1%, reinforcing disinflationary pressures. In its July Monetary Policy Statement, the Committee noted that rising spare capacity, a softening labor market and slowing wage growth pointed to a need for further accommodation. Interbank futures imply a near 90% probability of a 25bp cut, in line with consensus forecasts. Updated macroeconomic projections accompanying the meeting are expected to show weaker growth momentum and continued disinflation toward the midpoint of the target range by mid-2026.

Indonesia, BI (August 20, Wednesday) – Bank Indonesia is expected to keep its policy rate unchanged at 5.25% while maintaining an easing bias. The central bank is likely to reiterate its intention to “continue to look for room to further lower rates” and “make efforts to encourage bank lending and economic growth,” as well as maintain its triple intervention strategy and utilize offshore NDF instruments. The recent trend of rising inflation is not expected to alter Bank Indonesia’s easing bias.

Sweden, Riksbank (August 20, Wednesday) – The Riksbank is expected to hold its policy rate at 2.00% at its August 19 meeting. Preliminary July data showed CPIF inflation accelerated to 3.0% y/y – up from 2.9% in June – while CPIF excluding energy eased to 3.1%, both above the 2% target. In its July Monetary Policy Update, the Executive Board observed that persistent inflationary pressures and sluggish growth warranted a cautious stance and a pause in further easing until there is unambiguous evidence of inflation returning sustainably to target. Market pricing reflected this view, assigning low odds to an August rate move. Updated projections on inflation, growth and the krona will accompany the decision and we would also expect some additional scenario analysis based on the impact of tariffs and the U.S.-EU trade agreement.

Israel, BoI (August 20, Wednesday) – The Bank of Israel is expected to hold its key rate at 4.50% at its August 20 meeting. June’s Consumer Price Index rose 0.3% m/m, bringing annual inflation to 3.31%, above the government’s 1–3% target range. Core inflation, which strips out energy and fresh food prices, held at 3.1%, reflecting persistent underlying price pressures. In its July Monetary Committee press release, the Bank highlighted ongoing inflation volatility driven by global energy costs and domestic housing rents as justification for maintaining the current stance. Survey measures of one-year-ahead inflation expectations remain anchored near 2.5%. With growth forecasts for the remainder of 2025 revised slightly lower and geopolitical tensions posing upside risks to prices, markets have fully priced in an unchanged rate outcome.

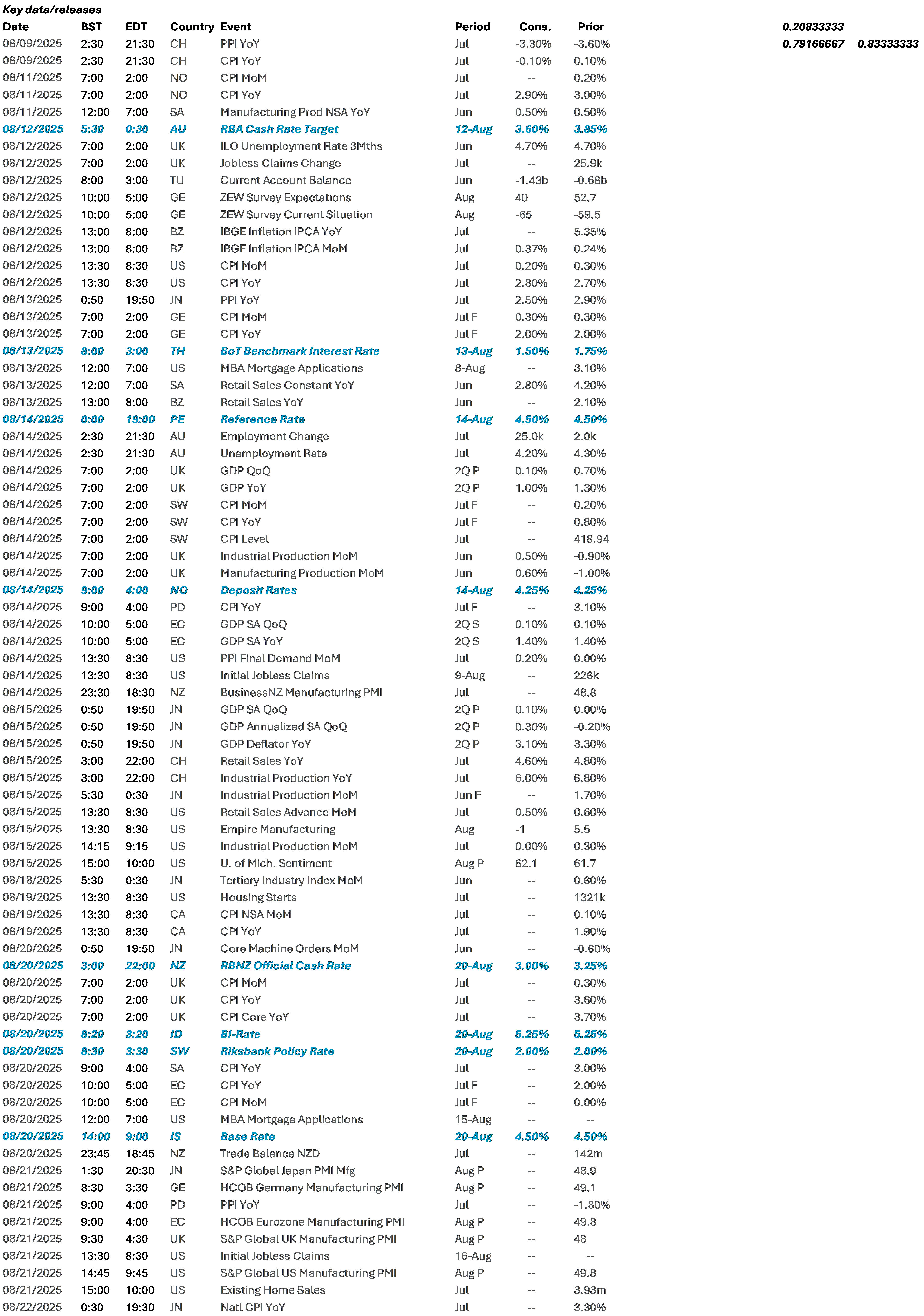

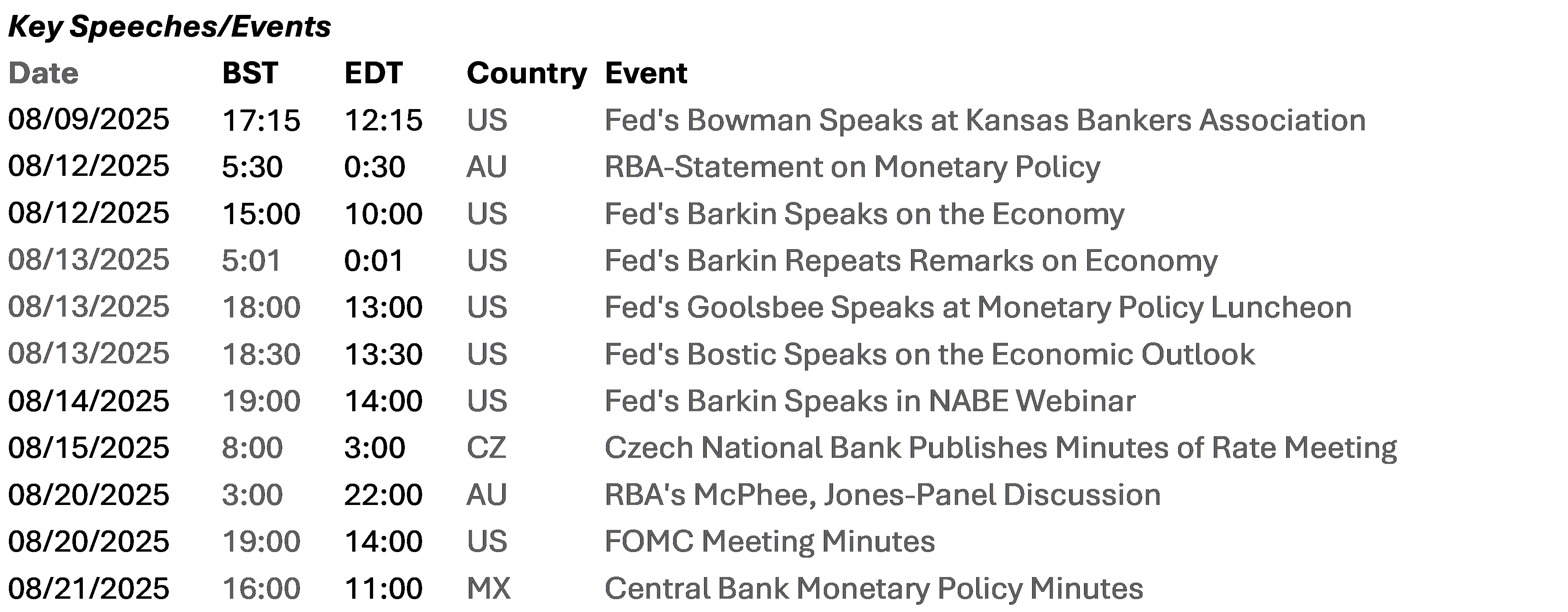

Data Calendar

Event Calendar