Unpredictable

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 12 minutes

The last week provided some relief to markets, as volatility slowed with the shortened holiday week. Still, stocks lost (S&P500 fell 1.5%), bonds gained (10-year yields off 16bps to 4.32%) and USD fell ($ index off 0.75%). Increased policy uncertainty continued to drive all asset classes, focusing on U.S. tariff and monetary policies. The biggest events were the ECB rate cut, FOMC Chair Powell speech and U.S./Japan trade talks. Hard economic data from the last week, like March U.S. retail sales, surprised to the upside. Soft data continued to cause worry when the Philadelphia Fed April manufacturing survey fell to 2-year lows. The ongoing market volatility, driven by concerns about growth and inflation, is causing investor indecision, especially during a week with lower trading volumes. This leads to more “dash for cash” risks across markets, less positioning, less liquidity and more a wait-and-see sentiment for investors. For the rest of the month, this unpredictability is expected to continue. No one factor stands out in markets, but negative carry, poor investor sentiment and high volatility in stocks, bonds and FX are headwinds against hopes for forming a bottom to risk aversion.

There are four focus risks to markets in the week ahead:

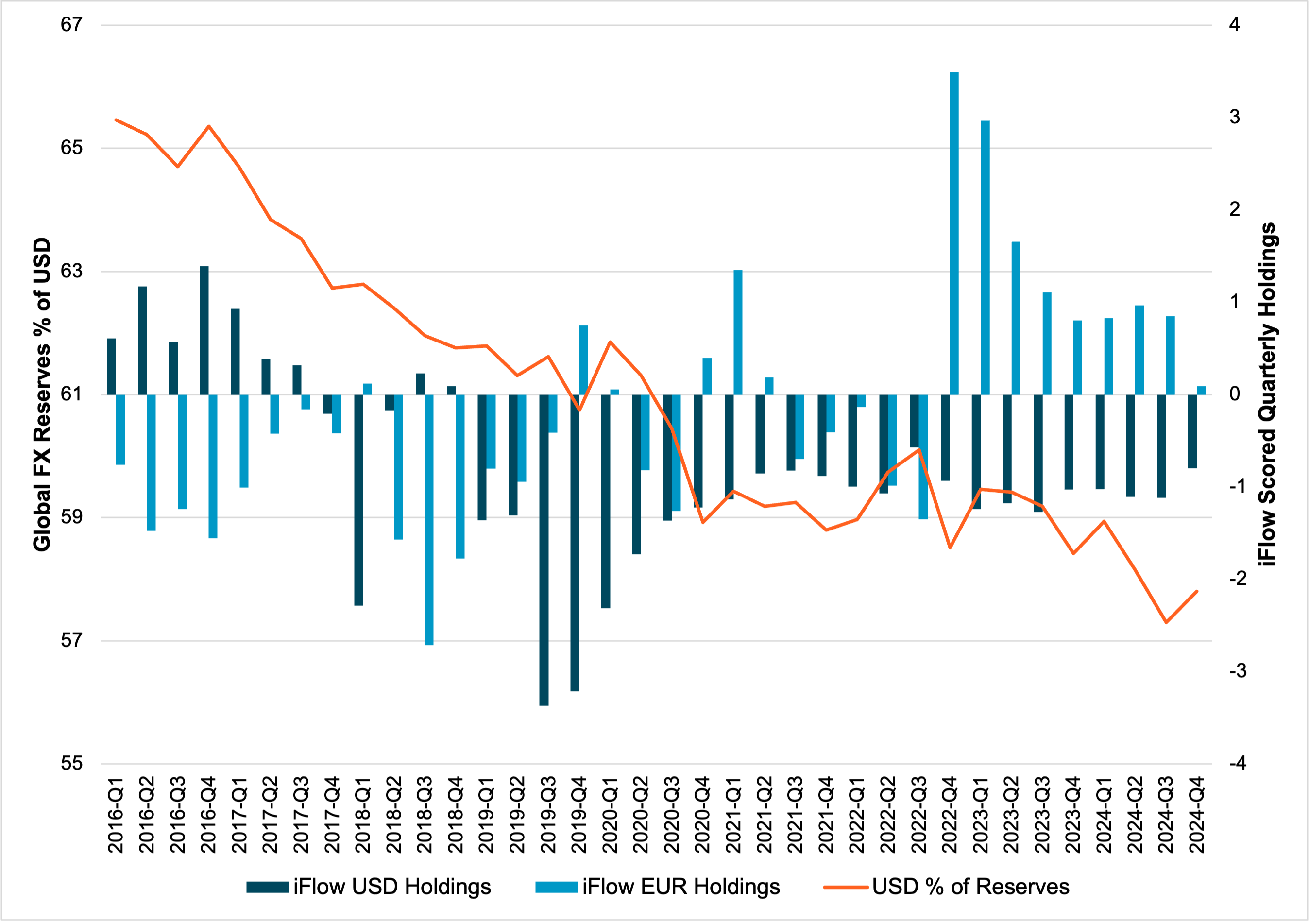

EXHIBIT #1: US SHARE OF GLOBAL FX RESERVES – 25-YEAR LOWS

Source: IMF Cofer, BNY

Our take: Questions over the U.S. dollar’s dominance as the world’s reserve currency continue to be part of the current market debate. The USD is still used more than all other FX reserve currencies (AUD, CAD, CNY, EUR, GBP, JPY, CHF) combined, but there is a notable rise in alternatives like gold or other baskets of currencies. In Q1 2016, the USD accounted for 65% of FX reserves, whereas today that number has dropped to 57% - near 25-year lows. We monitor the IMF Cofer data, which tracks global FX reserves, as a tool linking FX to U.S. bonds and stocks. Notably, the iFlow data in FX holdings show that 2023 EUR buying reversed sharply and was near zero at the end of 2024. The link of our investor flows into and out of EUR or USD seem more correlated to economic growth expectations than rate or trend factors. The cracks in U.S. exceptionalism show up in dollar hedging and home bias from cross-border flows. FX reserve holdings correlate more to the amount of USD or EUR held abroad – making trade an important factor as well.

Forward look: The risk of USD holdings quickly dropping in the weeks, months and quarters ahead rests on more than just U.S. tariff concerns. Factors such as the U.S. fiscal situation, risk premium for holding bonds, volatility of a nation’s assets, and confidence in policy continuity are all important. In the week ahead, the IMF meetings are likely to highlight many of the concerns about U.S. bonds, including the independence of the FOMC, the debate about fiscal spending and taxes, the value of the USD, and the appetite of cross-border investors to hold U.S. assets. Last week the focus of concern shifted from Fixed Income to Equity Markets, partially driven by Q1 earnings and Q2 outlooks. The focus may shift back to USD as trade talks with Japan and other countries, combined with the IMF meetings, introduce geopolitical factors across market risks.

U.S. focus – Fed Beige Book, Earnings Outlooks, Growth

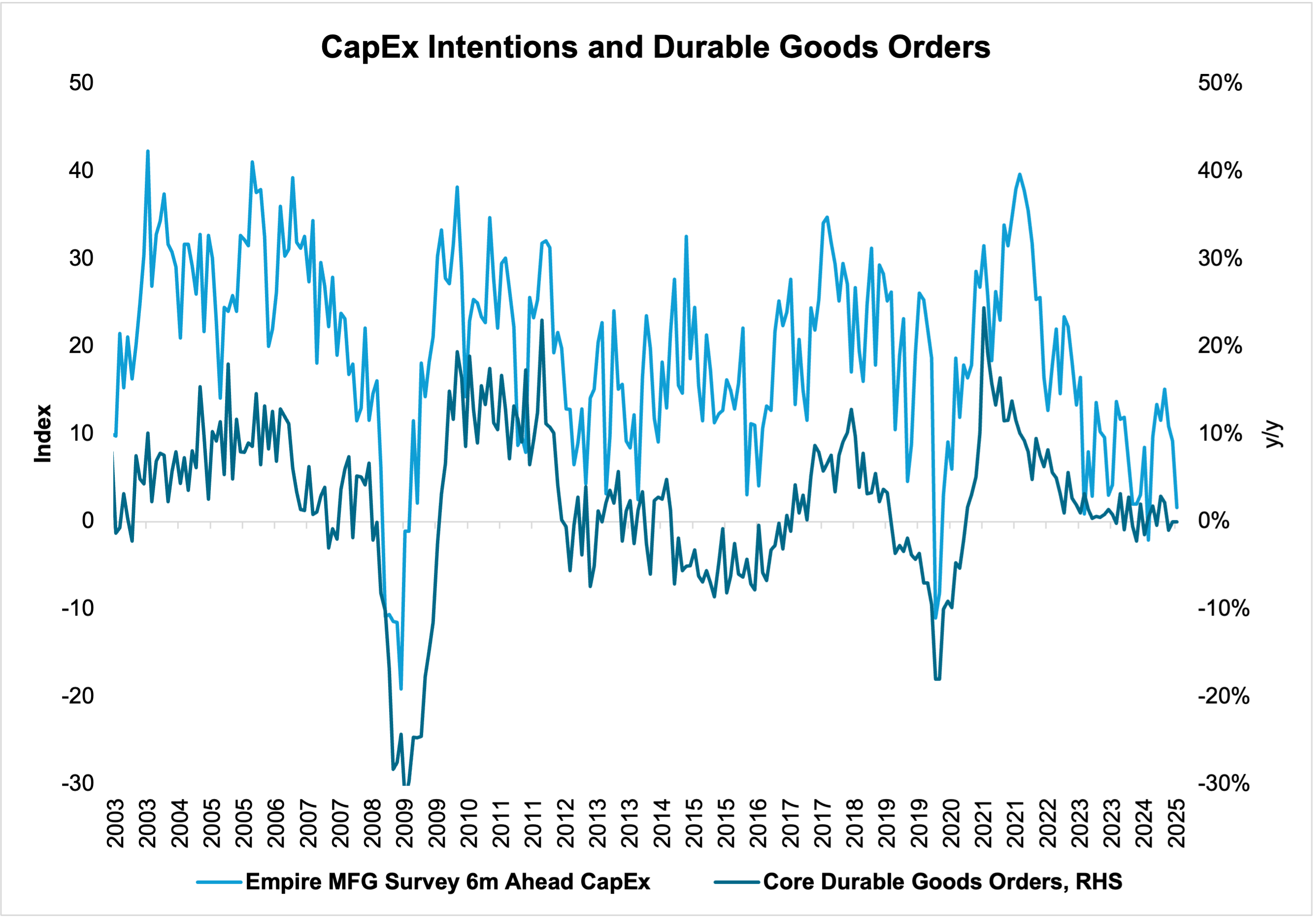

EXHIBIT #2: US CAPITAL EXPENDITURES PLANNED AGAINST DURABLE GOODS ORDERS

Source: BNY, Bloomberg

Our take: Several data events occur this week in the U.S., but we’re not sure we’ll see much other than tariff frontrunning reflected in most reports, like last week’s retail sales data. The S&P Global PMIs are likely to reflect recent regional industrial surveys that highlight a weakening outlook, falling orders, and a generally depressed mood. The Fed’s Beige Book survey will provide more detailed anecdotal information. We hope to get a read on how local businesses and labor and product markets are reflecting the tariff uncertainty, especially in pricing behavior, activity, and job market conditions.

Forward look: Hard data will come via the March Durable Goods Orders release on Thursday morning and could begin to reflect softness in business spending on capital projects. February’s data showed a decline in “core” durables (nondefense and ex aircrafts) which fell slightly to -0.2% last month, even though shipments in this category slightly increased. A second straight decline would not bode well for business spending, even if the headline print is strong like last month. Consumer orders for household durables could still be high thanks to tariff frontrunning, much like we have seen in the retail sales data.

EMEA: Expect more pushback on FX flows, more dovish central bank talk

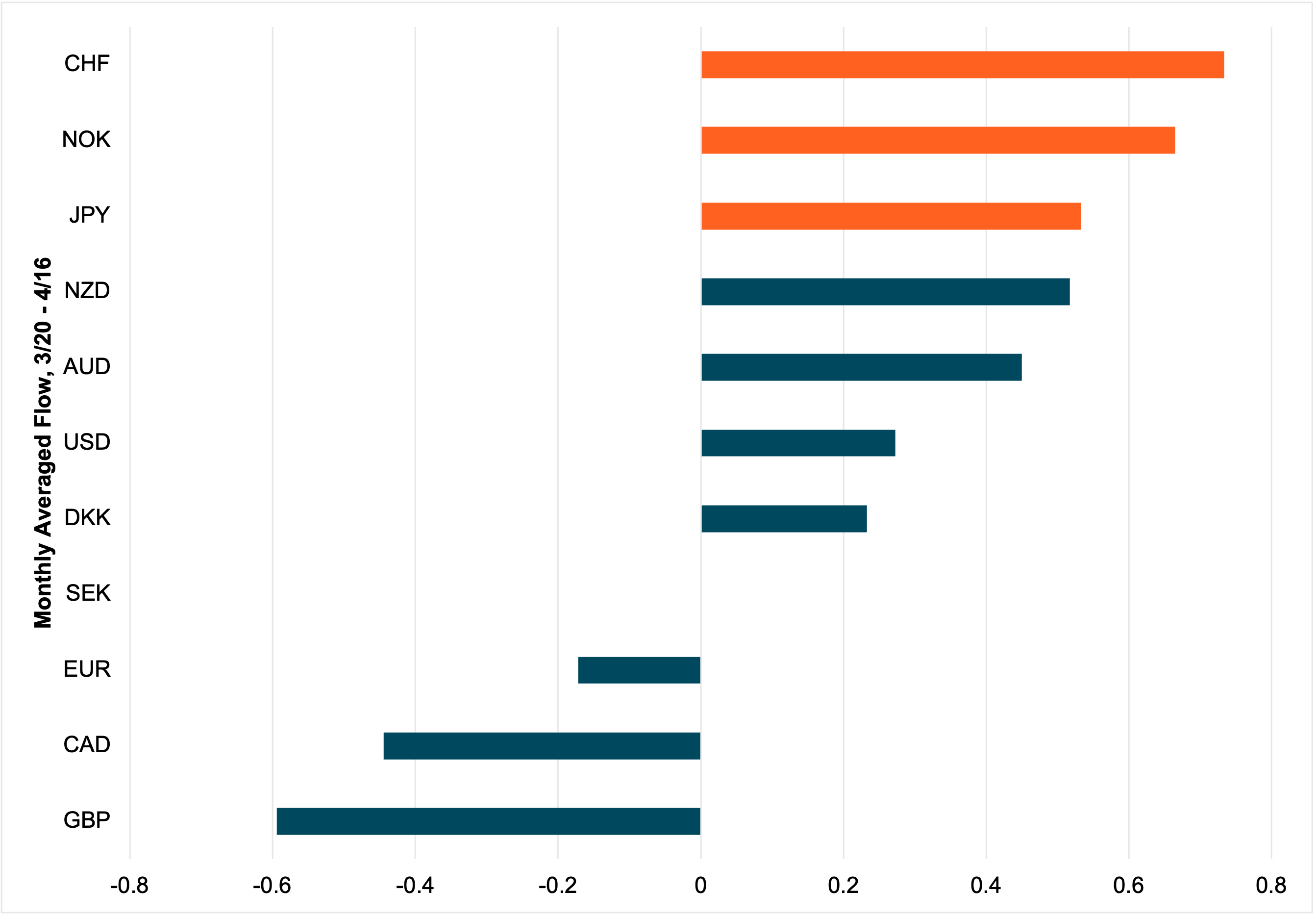

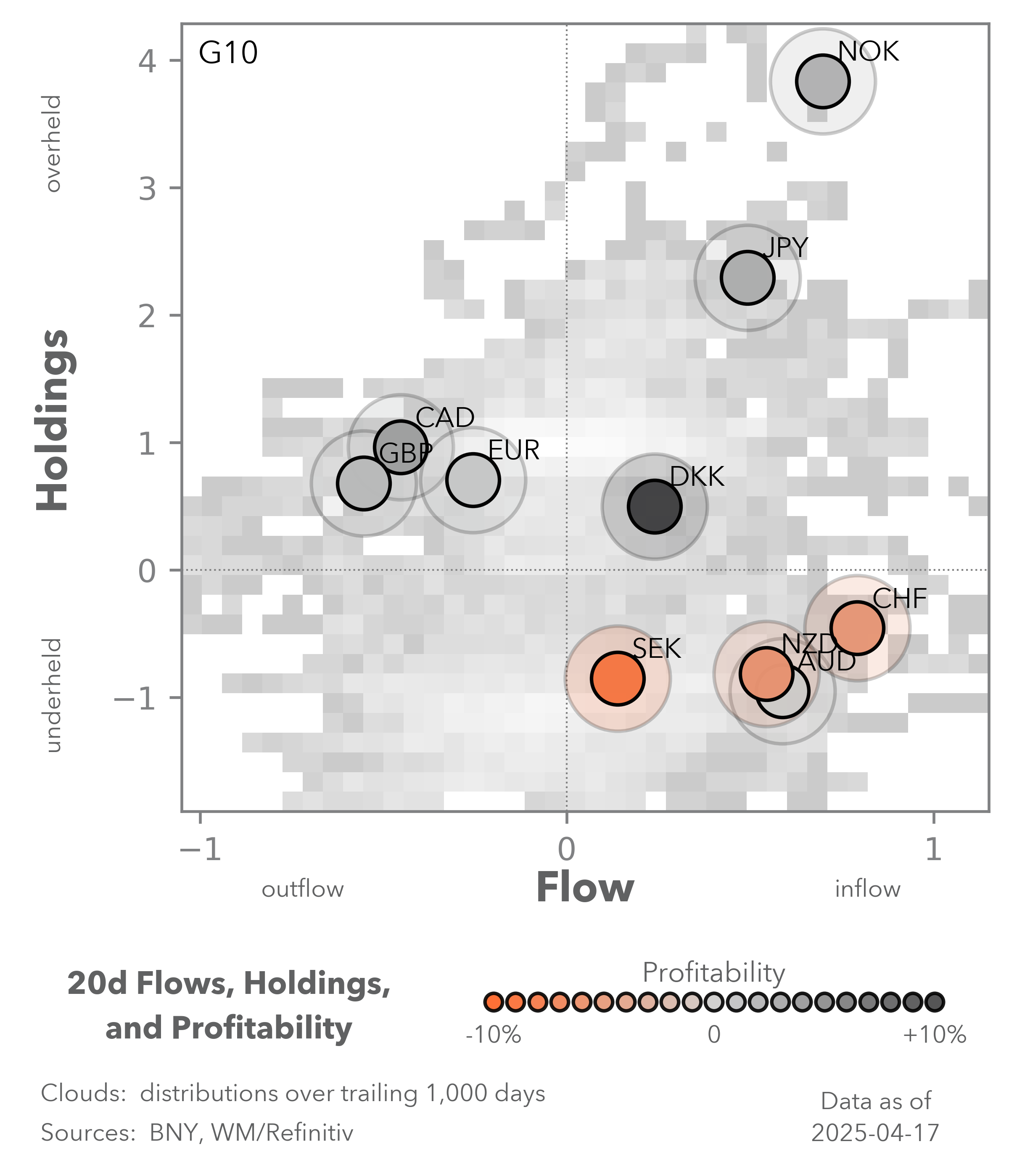

EXHIBIT #3: CURRENT ACCOUNT SURPLUS ECONOMIES SEEING UNWELCOME INFLOWS

Source: BNY, Bloomberg

Our take: The past two weeks’ decisions by G10 central banks have clearly indicated a dovish pivot in response to U.S. tariffs, but the uncertainty is so severe that many policy makers are deliberately abstaining from policy guidance. The best approach, as shown by the Bank of Canada, is to map out various scenarios and respond accordingly. Stubborn inflation is swiftly being pushed out of policy assessments, while the risk of disinflation or deflation due to demand collapse requires swift intervention. Surplus economies that face natural currency appreciation pressure need to be especially vigilant. Our flow data shows that over the past month, the best bought currencies in G10 are the ones with the largest current account surpluses: Switzerland, Norway, and Japan (Exhibit #3). Immediate intervention is unlikely, but we expect a step-up in rhetoric if valuations begin approaching extremes.

Forward look: We will pay close attention to BoE Governor Bailey’s and SNB President Schlegel’s keynote addresses this week, which will be the first opportunities for their central banks to respond to recent developments, since neither have decisions scheduled in April. Before trade tensions escalated, we stated that the solution for an economy in stagflation such as the UK is a recession driven by fiscal conclusion. However, the BoE and its peers are now expecting a significant demand shock based on external factors, which would require a positive fiscal offset. In recent sessions we have observed surprising gains in short utilisation in various G10 sovereign bond markets. Even though global growth is facing serious downside risks, we caution against asset allocations responding in the traditional way of moving into savings-heavy currencies and expecting significant flattening. A strong monetary and/or fiscal policy response would push back against both positions.

APAC: Bracing for downside growth and inflation risk

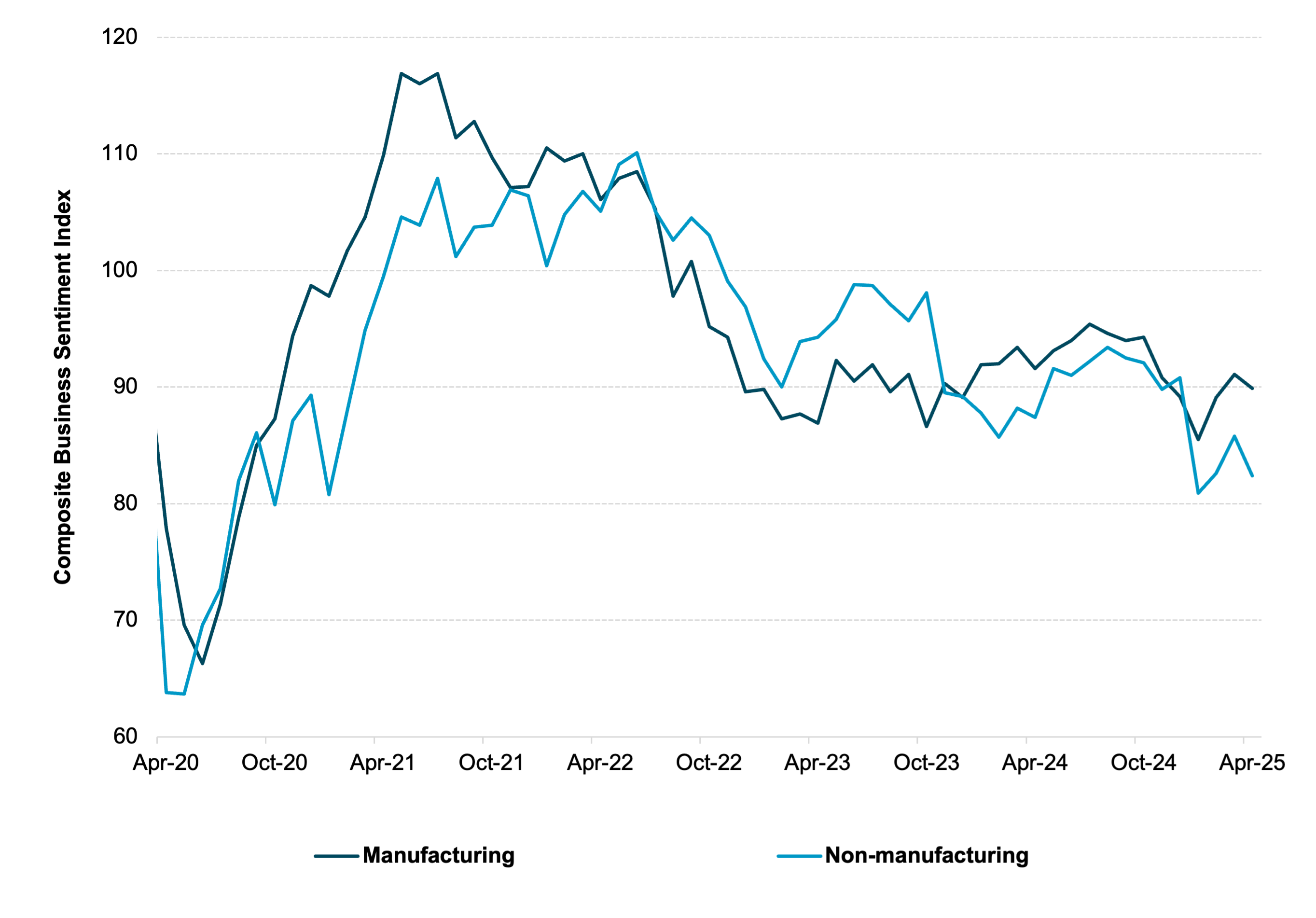

EXHIBIT #4: KOREA BUSINESS SENTIMENT BASELINE FOR DATA WATCHING NEXT WEEKS

Source: BNY, Bank of Korea

Our take: The economic data focus this week will be on South Korea, including April’s first 20 days exports, composite business sentiment index, consumer confidence and Q1 2025 GDP. Sentiment in South Korea has been negatively impacted by domestic political uncertainties and exacerbated by recent U.S. tariff policies, particularly on auto sector and tech-related trades in the semiconductor industries. While KOSPI is up 3% on the year, the auto sector has been hit hard, down 8% year-to-date. The semiconductor sector has lost all of its 25% gain from earlier in the year and is now flat on the year. Q1 GDP should confirm the sluggish growth recovery after 0.1% q/q quarterly growth in Q3 and Q4 2024 respectively. The market consensus for Q1 2025 growth is 0.1% q/q, but the risk is firmly on the downside. April’s first 20 days of exports and the composite business sentiment index will be closely watched and used as a gauge of the immediate impact of U.S. tariffs policies.

Forward look: The other noteworthy data in the region is the Singapore March CPI. Singapore inflation has been on a sharp downward trajectory since 2022 and hit sub 1% for both headline (Feb: 0.9%) and core (0.60%) inflation. Continued low inflationary pressure should pave the way for the Monetary Authority of Singapore (MAS) to flatten the SGD NEER policy slope of appreciation to zero at the July policy meeting. Disinflation pressure is widespread in the region, with Korean inflation standing marginally above the 2% inflation target. Headline inflation in the rest of the APAC region is well below and tracking towards the lower bounds of the inflation target range. Interestingly, Bank of Thailand commented last week that inflation is expected to cool further despite it being below 1% since July 2023. Slowing growth momentum and disinflation pressure is likely to cause the regional central bank to deploy a more aggressive easing measure to stimulate growth and address foreign exchange market volatilities via macro prudential measures.

In terms of capital flows, foreign investor outflow momentum continues. Foreign equities outflows in Taiwan totaled $19bn year-to-date, matching the $19bn sold in 2024. Foreign equity outflows in India are at a record year-to-date pace of $16bn and investors net sold $12bn in Korea. For China, iFlow equity data shows a shift in behavior, with investors turning to sellers for the first three weeks in April.

The next week will be difficult for investors as the IMF meetings, U.S. trade talks, ongoing Russia/Ukraine geopolitical concerns and the U.S./Iran nuclear talks add another layer to volatility. The commonality across all global markets is their corelation and unpredictability, making any gathering of monetary and fiscal officials an opportunity to address doubts about financial stability. In our data, we see that there is no one factor dominating global markets, which hasn’t happened in the past 20 years other than extreme events like Covid or 2008. Finding value and growth factors to buy the dip in asset prices requires a level of calm and clarity on future policy – neither of which seems easy to see in the economic data releases ahead. The short-term urge to run to safety and wait-it-out remains an option as shown by JPY, CHF, Gold and the dash for cash in our U.S. flows. We are expecting more USD troubles as the ability to prevent a weaker dollar requires a premium that makes the U.S. bond auctions for 3Y, 5Y and 7Y bonds even more important next week.

Central bank decisions

Indonesia BI (Wednesday, April 23): We expect Bank of Indonesia to keep rates unchanged at 5.75%, maintain a dovish stance and continue to “look for room to cut rate”. The lowering of headline inflation and downside growth risks argue, and high positive real interest rates argue for interest rate cut, but cut now might create greater FX volatilities. FX stability is the key priority for now. IDR is the worst performing APAC currency this year, down more than 4% ytd against +1% in Asia dollar index. We maintain our view that BI may deliver further rate cuts later this year.

Russia CBR (Friday, April 25): The CBR is expected to keep policy rates unchanged at 21.00%.

Economic Releases

Events