Through a Glass Darkly

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 12 minutes

To understand the week ahead, it is important to consider the last week, when a U.S. government shutdown and further AI investments mixed with uneven economic data to drive equities to new record highs, leave bonds in a range and send the USD lower. Commodities were mixed as well, with oil prices near four-month lows and gold trading at record highs. The U.S. government shutdown, the first in seven years, is expected to last beyond the weekend, and may even test the 35-day record set in 2018. The markets shrugged off the political impasse except for the lack of economic data, which puts private reports like ADP’s private employment in the spotlight. The AI investment boom continues, with OpenAI’s valuation jumping to over $500bn as the company’s partnerships with Asian tech companies drove a global surge in shares. The focus this week will be on Japan and the LDP’s leadership election. Fiscal policy concerns are colliding with monetary policy worries, as the BoJ is seen hiking rates later this month. Fed speakers will once again be key as they point to policy easing. The University of Michigan’s flash consumer sentiment survey and $119bn in U.S. note and bond supply will be important, too. Q3 earnings from Delta and Levi Strauss will also kick off the focus on margins and consumers. The RBNZ meeting will be watched to see how further easing plans play out after the August cut to 3% failed to shift the mood or the economy much. Investors are looking through the glass darkly for a glimpse of further good news to sustain the current rally up in risk and continue the trends of Q3 into Q4.

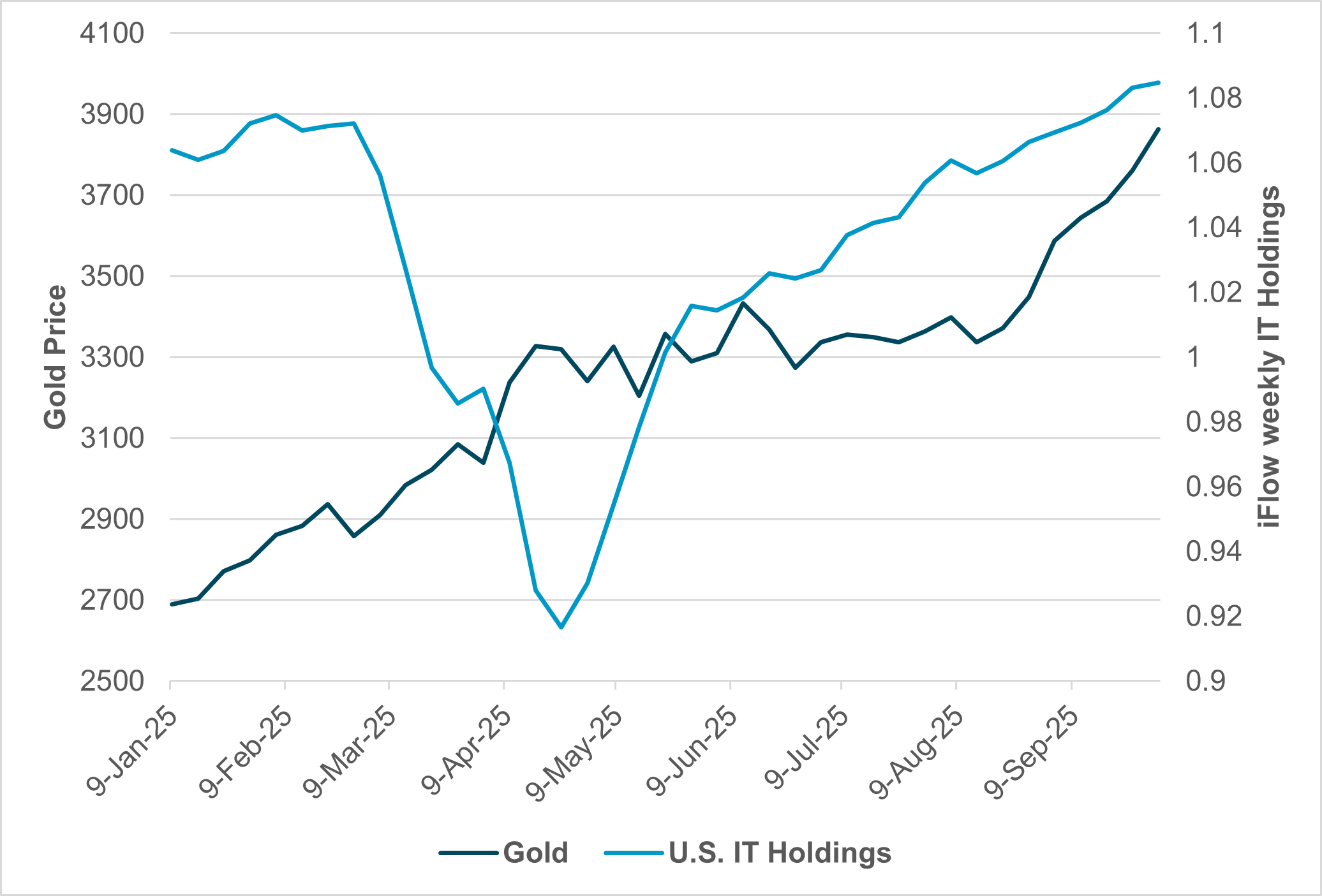

What will lead the market in Q4 – gold or AI tech?

EXHIBIT #1: U.S. IT SECTOR HOLDINGS VS. GOLD PRICE

Source: BNY, Bloomberg

U.S. market

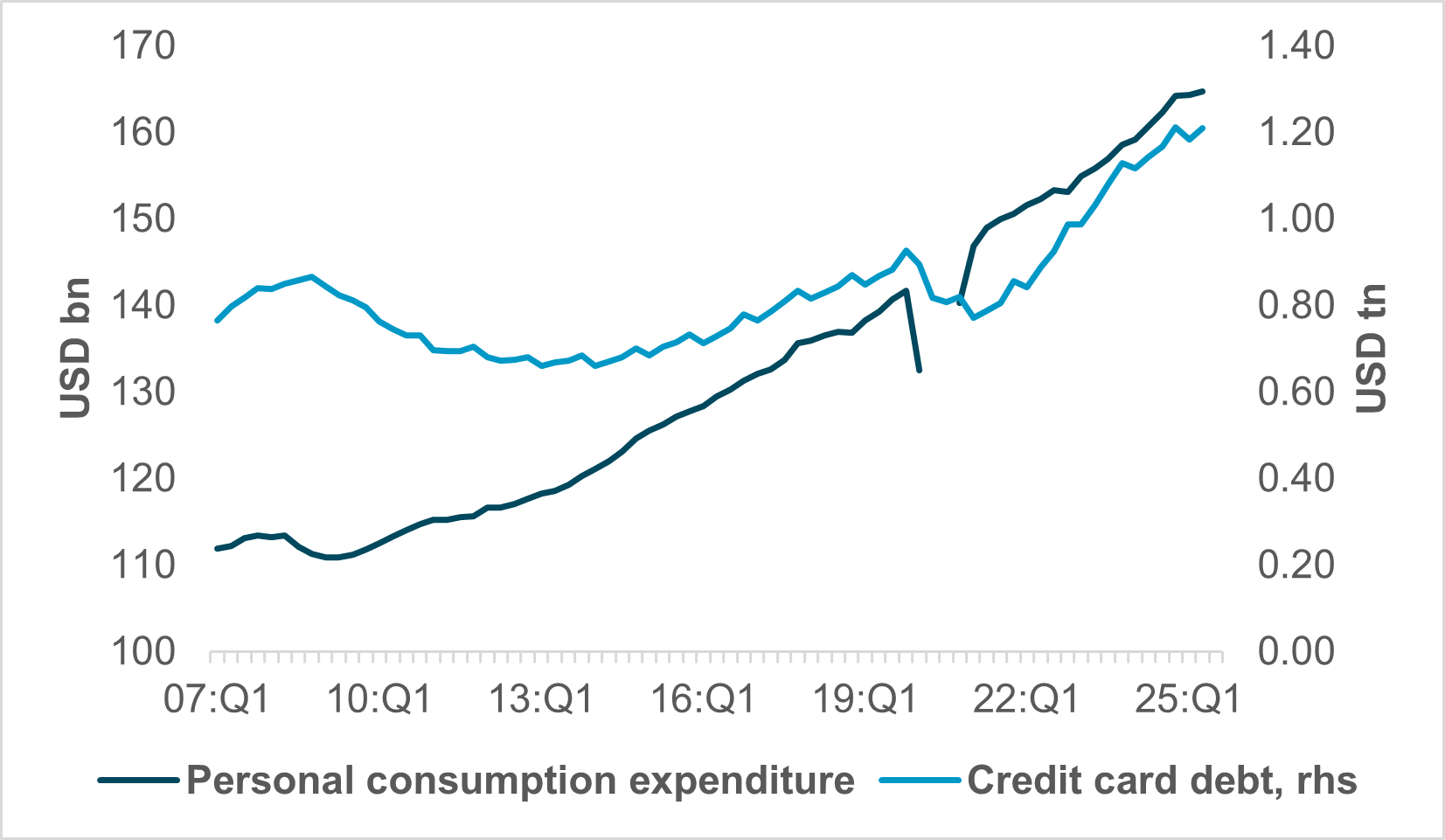

EXHIBIT #2: U.S. CREDIT CARD DEBT AND PERSONAL CONSUMPTION

*COVID period omitted due to scaling

Source: BNY, Bloomberg

Our take:With federal government shutdown likely to last into this week, there is precious little data to be released. In the last shutdown in 2018/2019 – which lasted 35 days – the Labor Department was not shut, as it had already been funded through a separate, earlier appropriation. This time is different, and all employees are on furlough. The same is true for the Commerce Department. This will leave us flying blind on key issues like employment – NFPs last week were not published, nor were jobless claims.

Corporate earnings, starting with the big banks, start to be reported next week (October 14–16), and we’ll be keen to hear their views on the economy, rates and especially consumption trends, as many large institutions have robust payment and credit card data. We’ll also be scrutinizing the Fed’s October Beige Book next week, which Chair Powell recently cited as having much weight in the FOMC’s data analysis. The FOMC minutes for the September meeting will be published this coming Wednesday.

Forward look: Data we do receive next week is mainly of lower importance, but we do get a peek at consumer credit and inflation expectations (Tuesday) and the University of Michigan Consumer Sentiment preliminary October report on Friday. There are a number of Fedspeakers on the schedule this week, and we’ll be keen to see if any views have changed in light of the disappointing ADP jobs report last week and how the Fed will navigate a lack of mainstream data. In addition to normal T-bill issuance, there are two coupon auctions (10y and 30y reopenings on Wednesday and Thursday, respectively) to gauge demand for government debt.

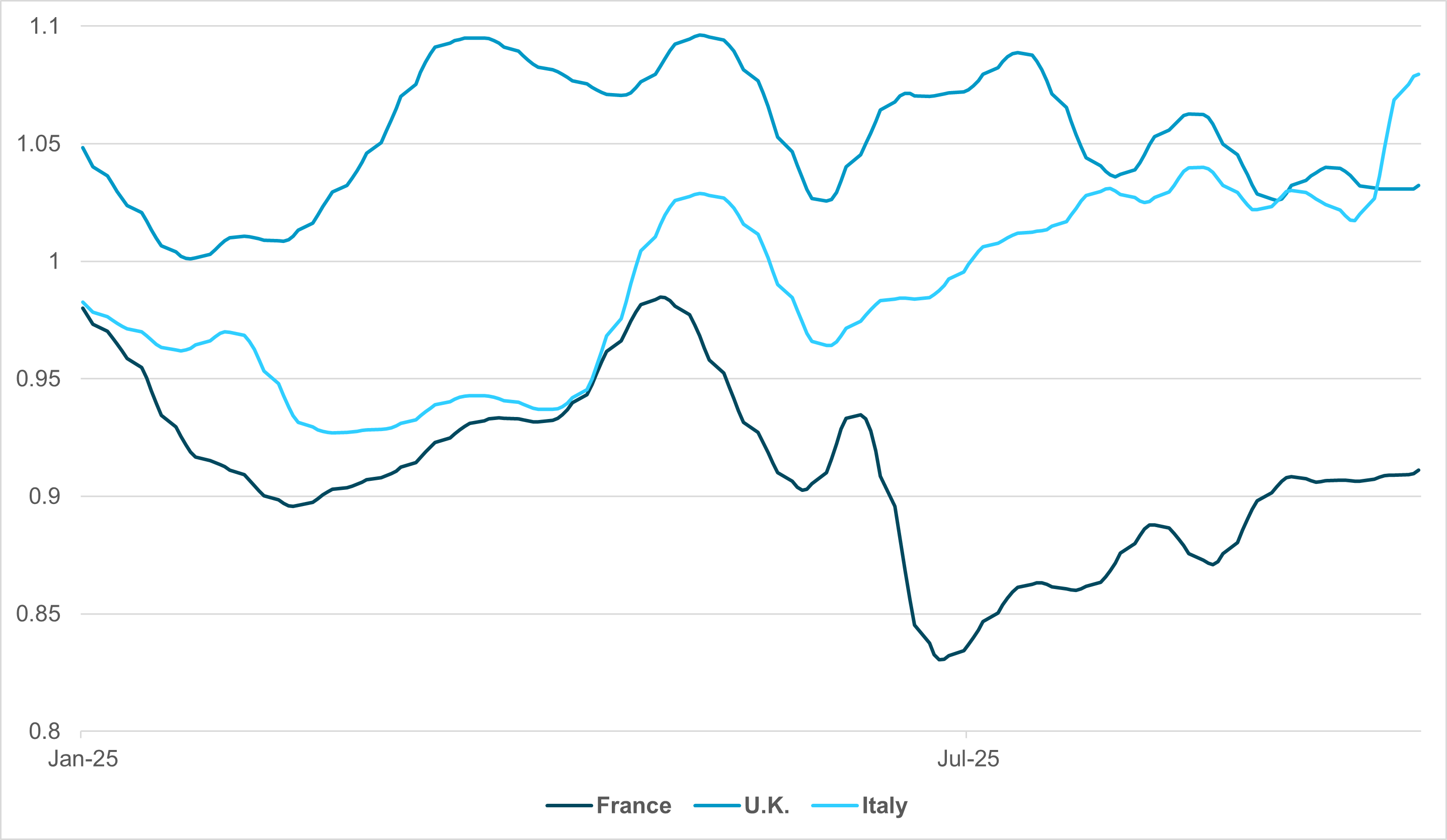

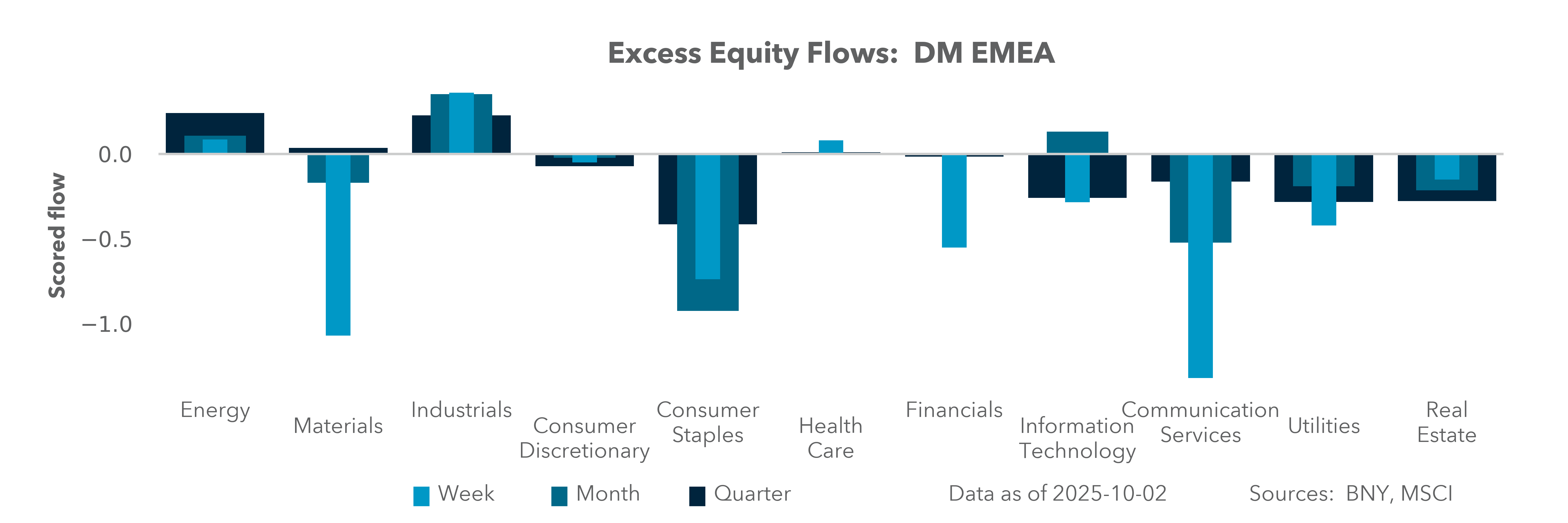

EMEA: Domestic politics to test fiscal credibility, Czech election and NBP decision in focus gaps

EXHIBIT #3: EMEA SOVEREIGN DEBT HOLDINGS, DM AND EM EMEA

Source: BNY

Our take: As markets continue to absorb the impact of the U.S. shutdown, the EUR and other “well-funded” European currencies are not exactly benefiting from a surge in safety-related flow. Although there is always the view that the end results could lead to lower U.S. rates as the economy suffers, there is a fiscal aspect which may not undermine the dollar versus G7 peers: lack of spending and cuts, coupled with strong tariff inflows could even result in a slightly stronger U.S. fiscal position in the near term. In contrast, the narrative is swinging from bad to worse in Western Europe as governments in London and Paris may need to face up to some new political realities.

The immediate risk is in France, where Prime Minister Sébastien Lecornu is attempting to secure passage of the 2026 budget without the benefit of a parliamentary majority. Following the collapse of François Bayrou’s government, Lecornu has pledged not to invoke Article 49.3, the constitutional mechanism allowing budgets to bypass debate, instead seeking cross-party compromise. This decision significantly increases uncertainty over budget approval and raises the prospect of a no-confidence vote, which would lead to serious scrutiny over institutional credibility given the short span of time since the last such vote. To mitigate political resistance, the government has withdrawn contentious measures, such as cuts to public holidays, and abandoned Bayrou’s complex fiscal methodology in favor of a year-on-year accounting framework, while a wealth tax is never far from the conversation. Such a contentious measure appears to be off the table in the U.K. as the ruling Labour Party largely ignored calls for a similar levy during last week’s Party Conference. However, as the Office for Budget Responsibility’s productivity downgrades continues to add to the fiscal burden, new revenue measures are essential as a fiscal hole of up to £30bn is seen for the November fiscal event. There are differences between the U.K. and fiscally-stretched Eurozone economies, and the difference is the acute reliance on external financing of its current account deficit, and the prospect of direct wealth or property taxes – which are likely to comprise a part of the upcoming budget – will have an impact on the financial account.

Our data indicate that the U.K. and France continue to struggle to attract stronger bond holdings (Exhibit #3). Even though our data indicate good inflows into French debt, we believe this is largely concentrated in the front end, while duration has heavily affected overall holdings. The poor performance of these two large markets stands in sharp contrast with Italy’s, and BTPs are now the best-held large developed European debt market apart from bunds. The latest Italian budget now has a target budget deficit of 3%, down from an earlier forecast of 3.3% as stronger revenue growth outpaced spending increases (5.5% y/y vs 3.1% y/y). Although the multi-year framework envisages another 2.5pp rise in the total deficit, fiscal discipline has improved and this is being rewarded by markets, as this week’s holdings surge clearly show.

Forward look: CEE remains on the agenda as well and we continue to express concerns over the region’s holdings vulnerabilities ahead of the NBP meeting on Wednesday, where rates are expected to remain on hold at 4.75%. We do not dispute the attractiveness of real rates in the region but total asset exposure remains very high, and there is a case to revisit the tightness of financial conditions given the recent softness in Polish data. Domestic demand remains strong and is underpinned by strong wage growth in a tight labor market. However, there are signs globally that higher incomes are no longer automatically translating into stronger demand, and the balance needs to be addressed. Should the NBP establish that some policy space exists, the rest of the region could start to see higher hedging interest. Meanwhile, the EU will also need to manage the result of the Czech parliamentary elections and the potential impact on Ukraine policy, among other risks. CZK’s funding status within CEE currencies is largely intact, but as we have seen in Romania and Poland this year, every supposed “populist” surge in elections has resulted in heavy hedging flow, so additional losses are possible in what is already a very overheld regional market.

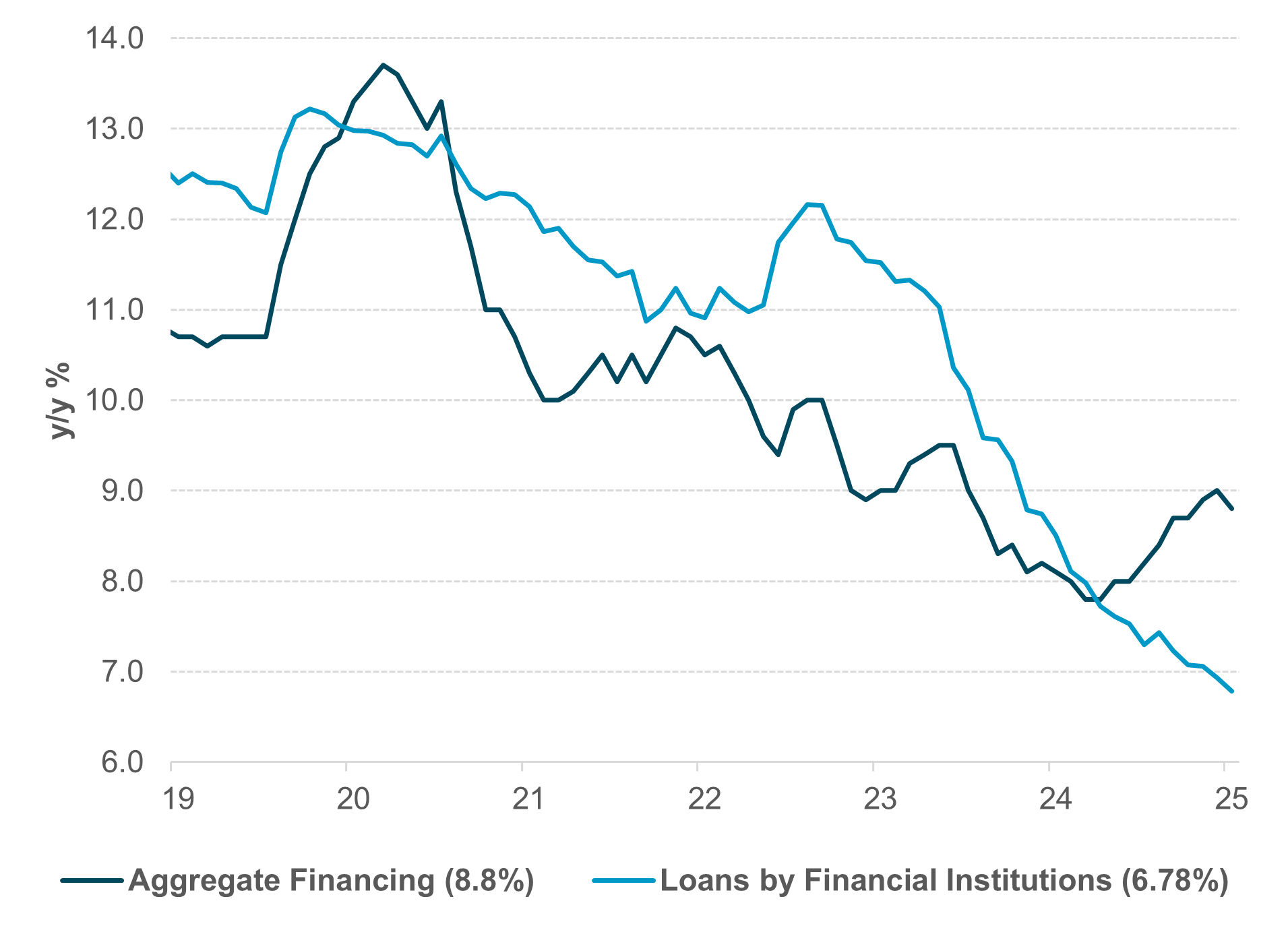

APAC: China credit, Japan spending, Singapore Q3 GDP and RBNZ, BoT, BSP in focus

EXHIBIT #4: DECELERATION OF CREDIT GROWTH A TOP CONCERN

Source: BNY, Bloomberg

Our take: In APAC, this week’s focus is on China September credit data, Japan household spending and cash earnings, South Korea bank lending to households, Singapore Q3 GDP and regional September CPI releases from Taiwan, Thailand and the Philippines. There will also be consumer confidence releases for Australia, Thailand and Indonesia, as well as Taiwan export data. China September credit data will be closely scrutinized given the increasing dislocation between aggregate financing and loans by financial institutions. Aggregate financing has been dominated by government and local government bonds issuance, with over 20% y/y growth. That said, the recent pickup in funding activities from corporate bonds and equity financing are encouraging but remained small in absolute terms. We will be paying special attention to loans by financial institutions as a gauge of domestic sentiment. China loans by financial institutions remain sluggish and have reached a new all-time low of 6.78% y/y as of August 2025. Domestic loans to households increased by CNY 30bn in August, of which medium-to long-term loans accounted for CNY 20bn, reflecting the depressed sentiment in the housing market. Indeed, the latest construction business activities index within PMI non-manufacturing recorded consecutive contractions for the first time ever. Overall, the positive asset price recovery over the past two quarters has yet to translate into domestic and household confidence.

Japan’s August labor cash earnings and household spending will be closely watched, serving as key input for the Bank of Japan policy meeting at the end of October. An overall positive sentiment in Japan, with a solid Q3 Tankan survey for both the manufacturing and non-manufacturing industries is likely to overshadow the lower inflation trajectory, allowing for further monetary policy tightening. That said, the outcome of the weekend LDP leadership election should dictate near-term sentiment in the Japanese yen.

South Korea’s bank lending to households will be closely watched given the authority’s recent focus on financial stability. Thailand and Philippines CPI will be good to follow but their impact will be overshadowed by Bank of Thailand (BoT) and Bangko Sentral Ng Pilipinas (BSP) policy meetings this week. Lastly, Singapore will release Q3 GDP, which is expected to decelerate after a strong H1 2025, and Taiwan export data is likely to stay buoyant with strong semiconductor demand.

On the monetary policy front, Reserve Bank of New Zealand (RBNZ), BoT and BSP will convene this week. Deterioration of the growth outlook warrants further RBNZ easing. BoT, under the new governorship of Vitai Ratanakorn, is likely to continue its easing cycle to boost economic growth. The BSP is expected to deliver its fourth straight cut to 4.75% given the worsening macro outlook.

Forward look: With China, South Korea and Taiwan markets closed most of the week, trading will likely be subdued. Sentiment hinges on ongoing tariff uncertainties and possible effects of a U.S. government shutdown. We remain positive on Asia assets and risks, on the back of AI-related optimism and continued foreign capital inflows. The upcoming event to watch is China's fourth plenary session, scheduled for October 20–23.

Risk appetite is comfortably navigating the shutdown so far, but this will rely on AI-based investments globally managing to defy the current cycle. Meanwhile, corporate earnings and not just in the tech sector will also need to overcome all aspects of fiscal and household stress. Such a scenario has not been stress-tested in the past, and with cross-market volatility now moving toward lower percentiles, the market will need to return to an “insurance” bias, especially as growth momentum falters as manufacturing continues to struggle. For APAC markets, which increasingly exhibit behavior akin to AI/capex-driven markets in the U.S., expectations will be high for renewed stimulus communication from Beijing as markets return from Golden Week and prepare for policy signals ahead of the upcoming plenum.

Central bank decisions

New Zealand, Reserve Bank of New Zealand, RBNZ (Wednesday, October 8) – The upcoming RBNZ meeting will be the first for Governor Breman, formerly of the Riksbank. The market is looking for rates to move to 2.75% as the easing cycle continues, but there will be scrutiny over her policy assessment and general approach, setting the tone for years to come. Markets are already skeptical regarding the capacity for further easing as economic conditions are still manageable, and high levels of non-tradables inflation still point to domestic price pressures requiring some degree of restraint. Markets are pricing in terminal rates at around 2.25%.

Thailand, Bank of Thailand, BoT (Wednesday, October 8) – Market consensus and the rhetoric from Governor Vitai suggest a likely 25bp rate cut to 1.25%. The October meeting will be chaired by new governor. Governor Vitai said that he will pursue an accommodative monetary policy to support growth. We have reservations about the effectiveness of monetary policy to boost growth, and all eyes will be on fresh government stimulus.

Poland, Narodowy Bank Polski, NBP (Wednesday, October 8) – No change is expected from the NBP as rates are expected to remain at 4.75%, but the monetary policy council will need to acknowledge a material deterioration in data through September on the output and household demand side. There are signs that the economy is weakening further as indicated by the latest PMI result, and flat sequential inflation for September suggests steady progress is being made toward anchoring inflation back at target ranges.

Philippines, Bangko Sentral Ng Pilipinas, BSP (Thursday, October 9) – Worsening macro developments argue for further monetary policy easing. We expect BSP to deliver the fourth straight rate cut to 4.75%, while the consensus calls for status quo. The pace of easing, if any, into 2026 is likely to be more constrained with projected higher inflation, driven by the normalization of food prices. Rice inflation, at –17.0% y/y, and the latest risk-adjusted inflation for 2025, 2026 and 2027 are at 1.7%, 3.3% and 3.4%, respectively, as of August 2025.

Peru, Banco Central de Reserva del Perú, BCRP (Friday, October 10) – There is very limited capacity for further rate declines in Peru as the BCRP is expected to keep the reference rate at 4.25%. However, maintaining an easing bias is more than manageable with Lima CPI running at 1.36% and monthly sequential figures largely flat. Current activity levels remain relatively robust and the country is not at the forefront of tariff issues for now. The capital’s unemployment fell to 6% in August, which is near cycle lows and warrants some caution on wages.

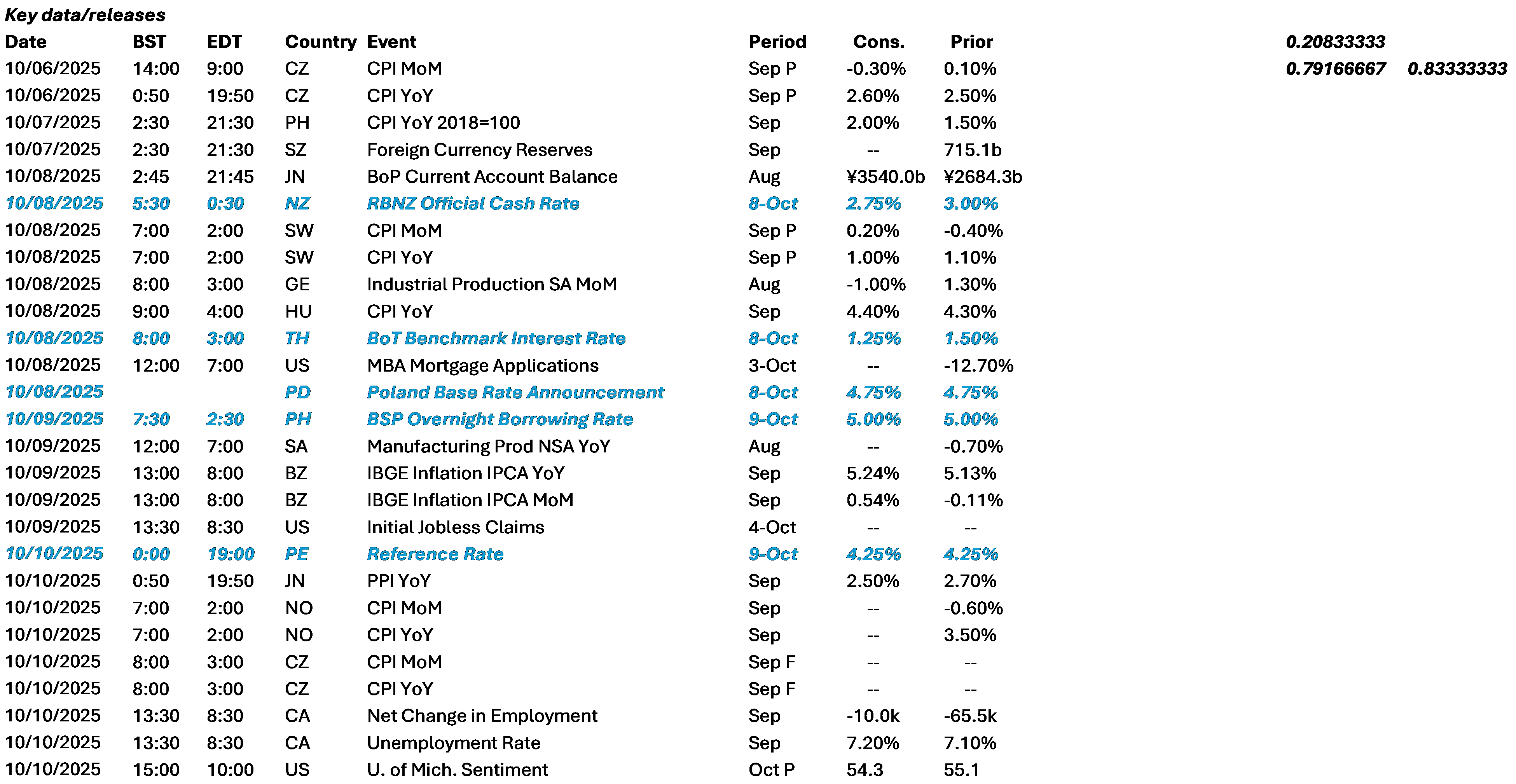

Data Calendar

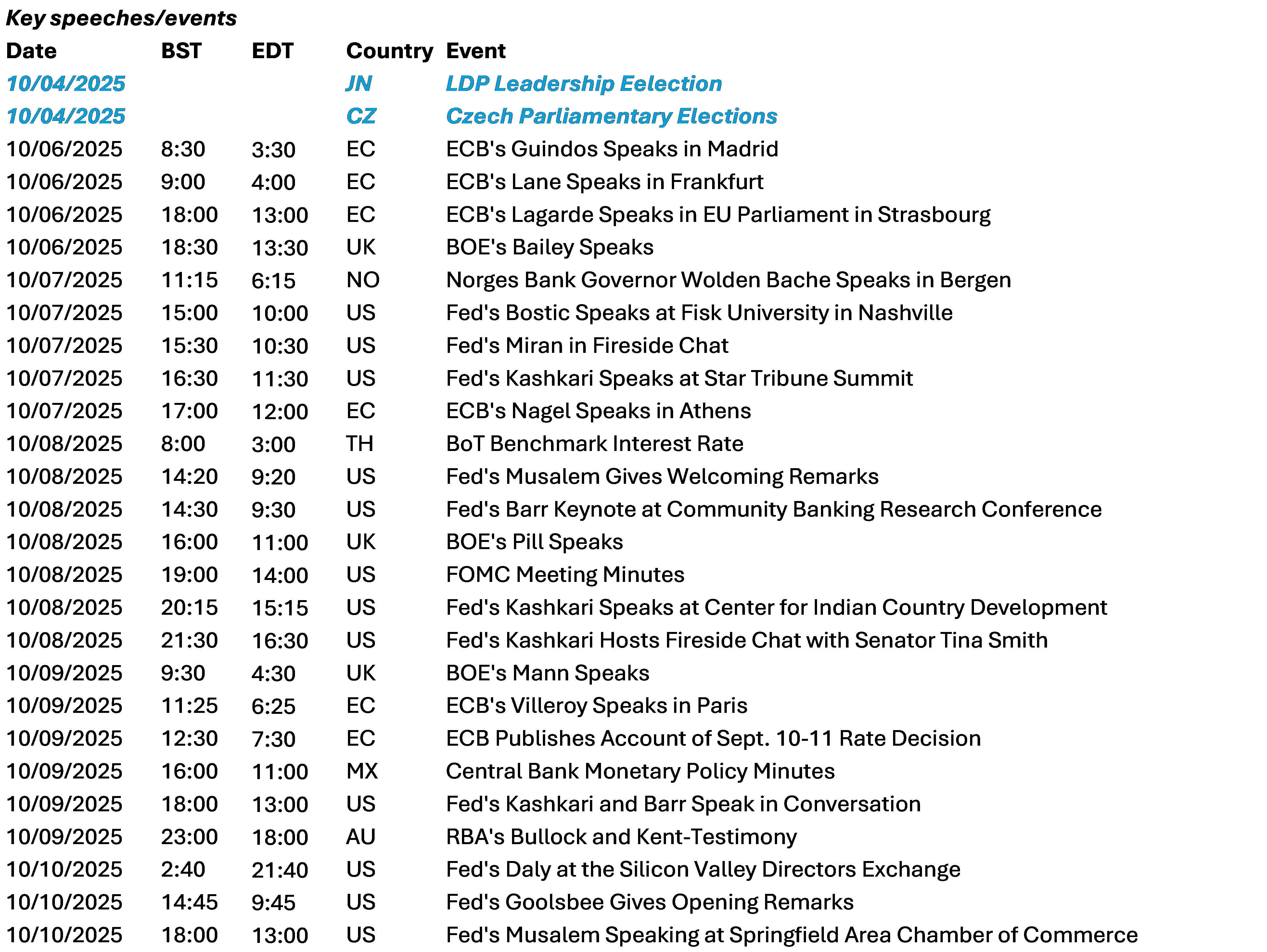

Event Calendar