The Four C's

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 10 minutes

There are four new concerns moving the cart of excess cash in and out of markets, with a focus on credit, carry, correlation and corrections key to understanding the week ahead. The key questions to consider are:

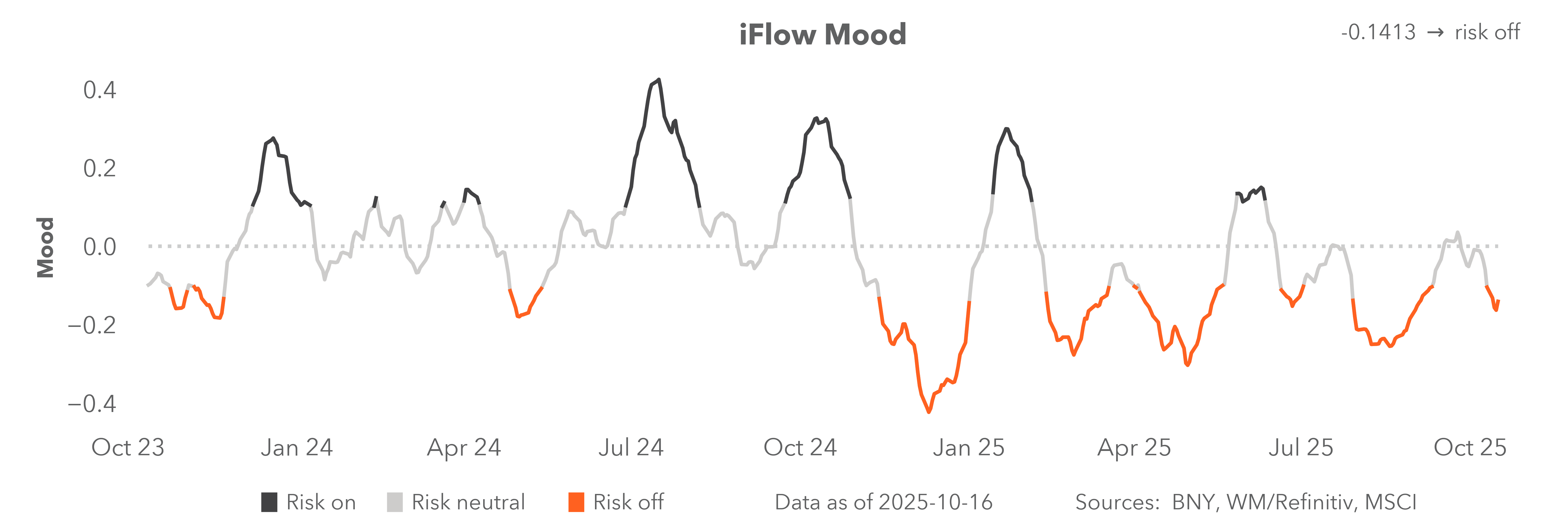

Markets were volatile last week and will likely remain volatile in the week ahead, given the upcoming votes in Japan, Ireland and Bolivia, Q3 earnings releases, central bank meetings, U.S.–China trade talks and the raft of economic data releases. In addition to headlines and the usual themes of gold and AI leading risk moods, including market liquidity, volatility and factor reversals in carry and trend correlations to the USD. How concerned should markets be about the spike in SOFR last week or FOMC Chair Powell’s comments about ending quantitative tightening (QT) versus the price action around credit spreads, basis swaps and stocks? Volatility is higher and investor hopes for an easy October trade have been dashed. Investor conviction in buying the dip of a pullback against the search for safe-haven investments to fund such actions remains in balance but for the U.S. dollar. Emerging hopes of U.S. exceptionalism that surfaced last week ended with regional bank concerns, putting the focus on Q3 earnings reports from tech companies and blue chips along with more bank earnings.

Fear of a larger correction dominating sentiment

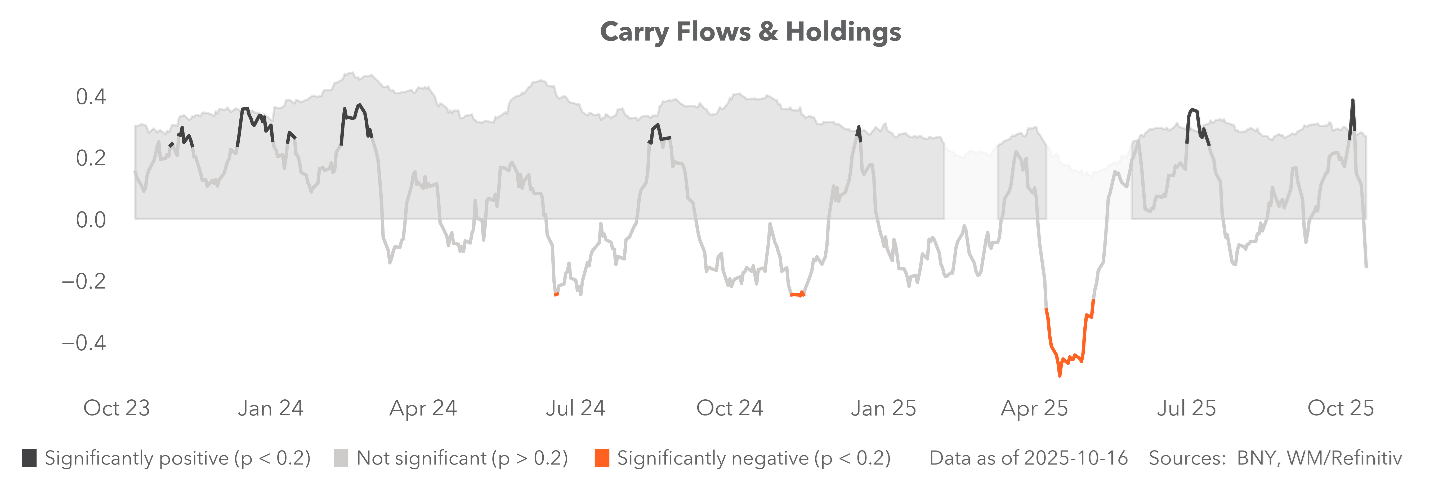

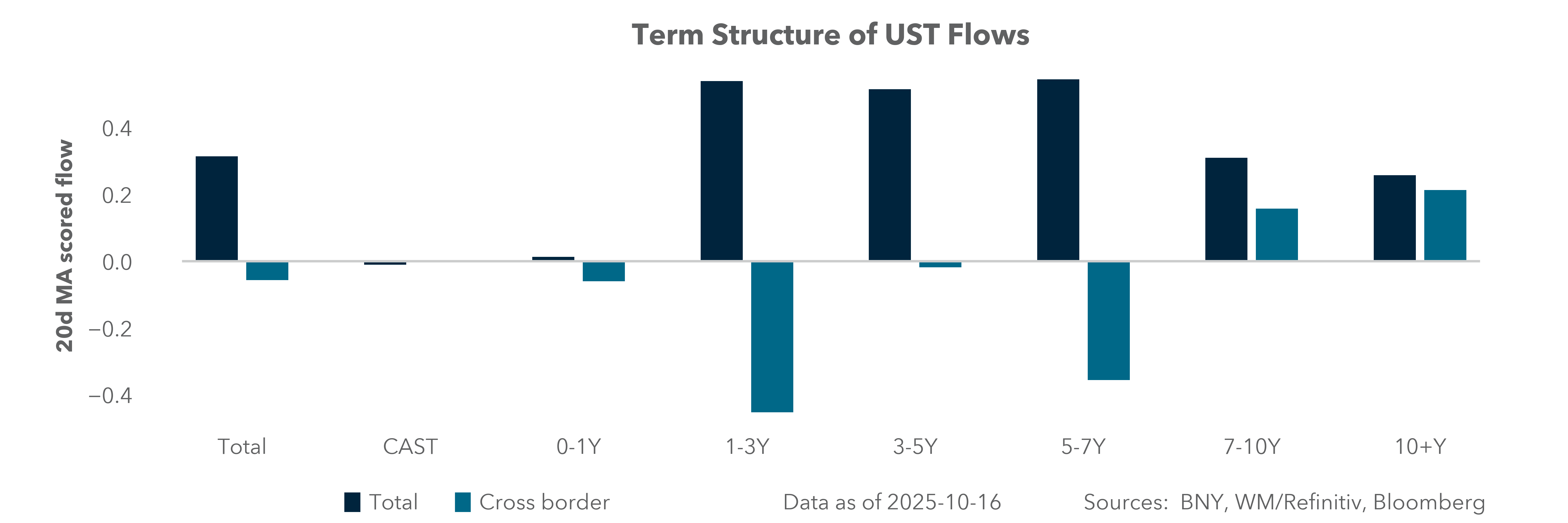

EXHIBIT #1: SHARP REVERSAL IN IFLOW CARRY FLOWS AND HOLDINGS

Source: BNY

Our take: FX Carry trades are part of a macro mood that requires low volatility across not only FX, but equities and fixed income as well. Carry trades also require enough of a risk premium to make currency debasement fears less pertinent. In the last week, the reversal of our carry correlation from +0.25% to –0.15% highlights the reversals across a number of markets, particularly credit. The focus on Q3 earnings, risks to consumers and leverage are clearly part of the picture. Historically, extremely positive carry signals last longer – two weeks rather than two days. The overall holdings that remain long carry trades like BRL, TRY against JPY, CHF are still extreme and suggest ongoing risk of further washout trades.

Forward look: The link of volatility and credit to carry has been part of the surprise of October before this week – where the U.S. government shutdown and lack of new information left investors watching for more news but not waiting to increase returns via carry plays. The reversal this week battles with the “buy-the dip” reactions to any washout trade. What seems clear about the last week is that low conviction trading has been swept away, as investors look for alpha rather than chasing beta. Credit worries and 3Q earnings will continue to be the drivers of volatility as the carry unwind is in full swing.

U.S. CPI and the blackout period

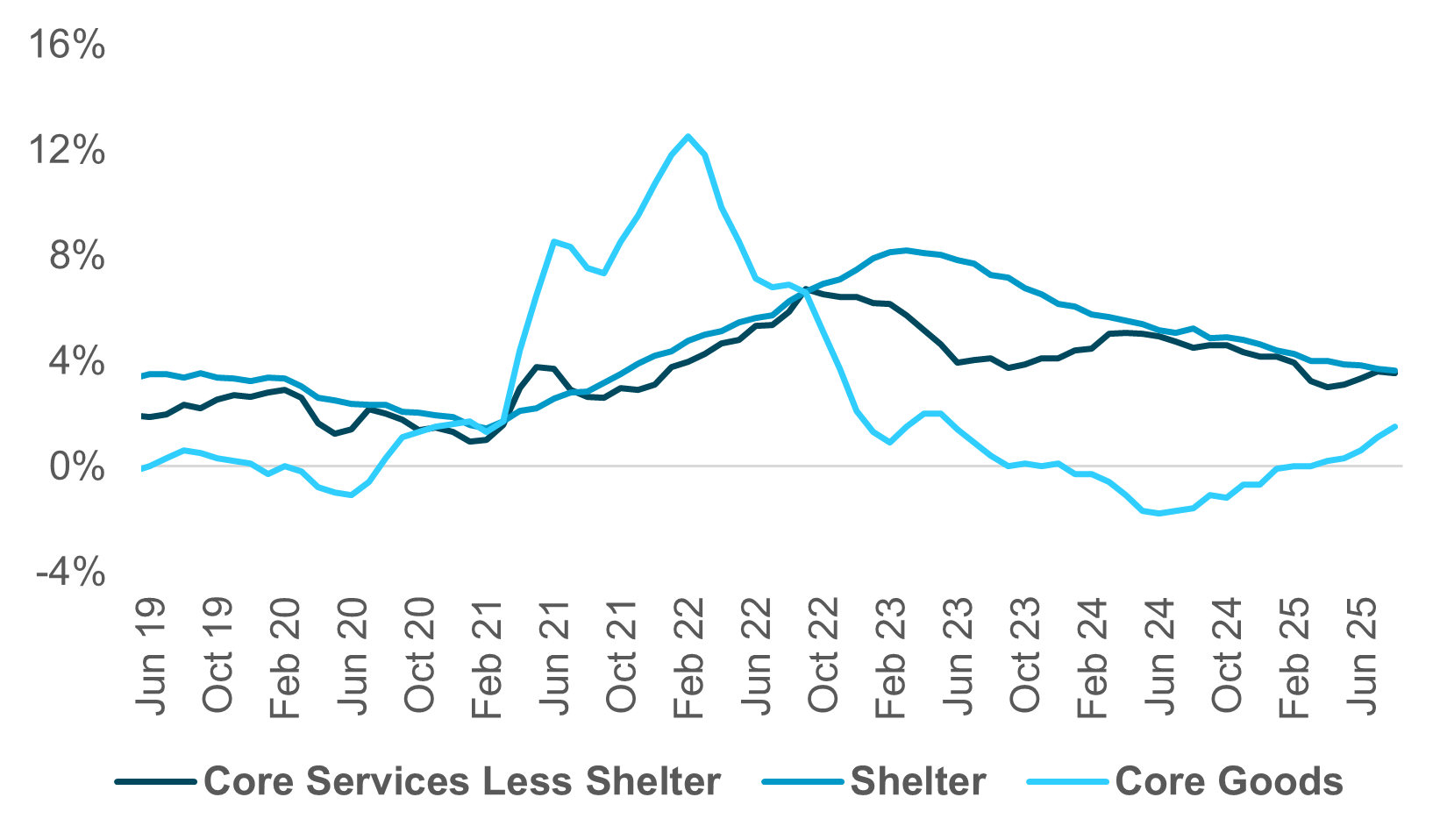

EXHIBIT #2: U.S. CPI CORE COMPONENTS

Source: BNY, Bloomberg

Our take: With the Fed on blackout this week in anticipation of the October 29 FOMC meeting and the government shutdown still dragging on, we have precious little to focus on this week until Friday when the CPI for September will be produced despite the shutdown. The Bureau of Labor Statistics has recalled furloughed workers to produce the report (which was originally scheduled for release on October 14) in time for the rate-setting meeting on October 29. The data that we have received so far indicated that core goods prices are starting to gradually move higher, and services inflation (ex-housing) is steady and elevated.

Forward look: Other data we do get – not subject to the shutdown – include the final Michigan Consumer Sentiment survey, and a few regional central bank PMIs, namely the Philadelphia Fed Non-Manufacturing Survey (also Friday) and the Kansas City Fed manufacturing report (on Thursday). Regional Fed surveys as well as national indices like the ISM reports have indicated weakening outlooks, stubborn prices paid and mediocre employment expectations. The Fed’s Beige Book last week also indicated a slowing economy albeit with stubborn price pressures. Still, CPI will be critical to the velocity of new pricing for U.S. stagflation.

EMEA: October PMIs to test the European industrial narrative

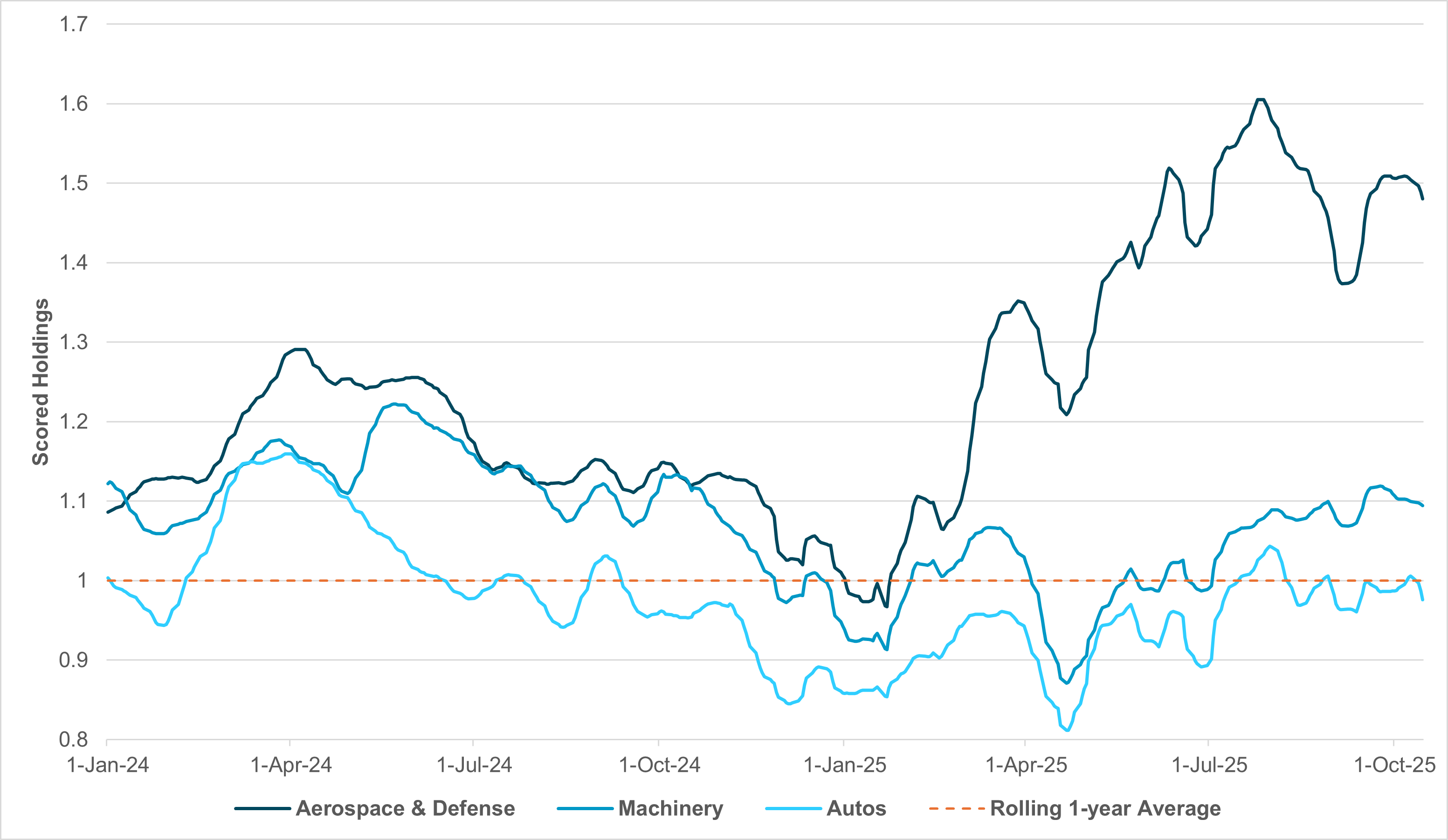

EXHIBIT #3: SCORED HOLDINGS IN INDUSTRIALS, AUTOS AND DEFENSE, DEVELOPED EMEA MARKETS

Source: BNY

Our take: Today marks the start of the ECB’s blackout period in anticipation of its rate decision at the end of the week. However, we doubt there will be a material change in their outlook unless market performance takes a severe turn for the worse such that financial conditions require an offset. This may be the path the Governing Council needs to tread as sentiment in the U.S. is still supported by the prospect of the “firepower” the Fed retains. In contrast, the ECB – given its narrower mandate – is only marginally open to the prospect of easing if downside inflation risks materialize. But repeated talk of the Eurozone being in a “good place” sounds increasingly hollow as markets begin to adjust.

The week ahead will see the release of October PMIs and we doubt there will be signs of expansion in any major Eurozone economy. Any evidence of a larger-than-expected slowdown in the service sector may support the case for keeping the December meeting “live” as the main driver of realized inflation begins to weaken, if only on a seasonal basis.

On the positive side, risk aversion is clearly raising additional interest in the government bond market as intra-Eurozone spreads begin to normalize. The fact that OATs responded positively to French Prime Minister Lecornu’s concession on pension reform – which is fiscally expansionary – speaks to a market that values policy and governance stability over long-term fiscal credibility. Then again, this is probably more of a Eurozone factor given there will be balance sheet support elsewhere. However, we still see the lack of fiscal consolidation risking crowding out much needed investment growth in other areas which deliver stronger competitiveness and supply chain resilience.

Forward look: If the ECB is unable to provide additional reassurance on rates and financial conditions, very well-held sectors in the Eurozone will face similar adjustment risk if data continues to deteriorate. Like the tech and AI-related sectors in the U.S., defense remains the most crowded position in developed European markets, solely based on expectations of secular public investment in the sector. Yet, other priorities for public finances remain pressing, even with stronger German fiscal impulse and defense spending the consensus in the EU. The prospect of some form of resolution regarding Ukraine is moving up the agenda again with another U.S.-Russia summit scheduled.

The risk for Eurozone defense stocks is that any settlement could swiftly divert attention away from re-armament and industrial revival. This explains some of the recent adjustment (Exhibit #3), while there is very little investor interest in adding to industries seen as facing structural decline such as machinery and automotive production. These are not issues which can be resolved through monetary policy and currency valuations alone, and it is imperative that long-term Draghi and Letta report recommendations remain on track.

APAC: Positioning for growth, resilience and easy financial conditions as the plenum meets

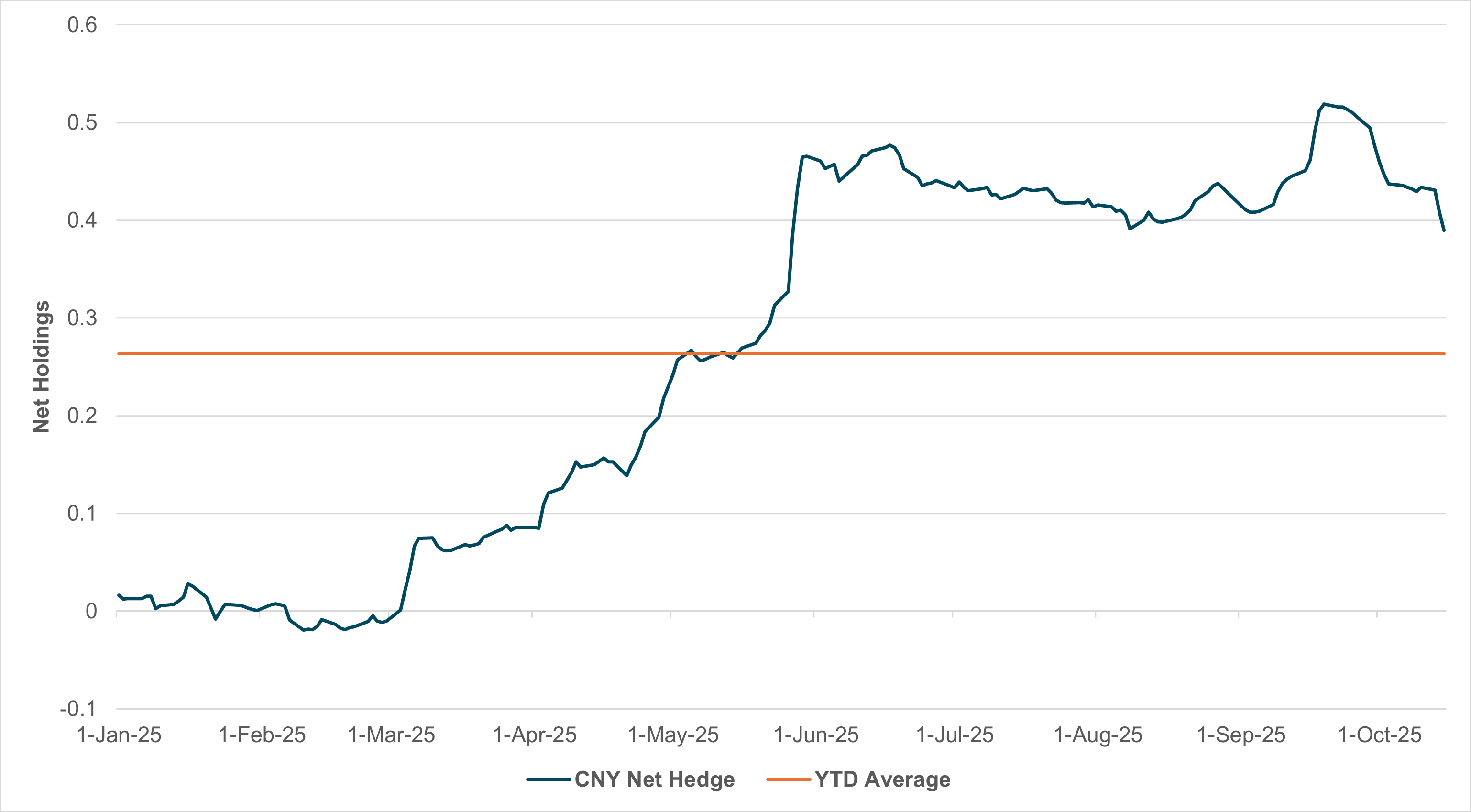

EXHIBIT #4: CNY EXPOSURES – CURRENCY HOLDINGS NET OF EQUITY AND FIXED INCOME HOLDINGS (40:60)

Source: BNY

Our take: Beijing will be at the forefront of attention as the fourth plenum of the 20th Communist Party Central Committee opens on Monday. We stress that this is not the right forum for asset allocators to look for short-term stimulus measures, especially as the blueprint for the next five-year plan (2026–2030) is at the forefront of deliberations. Measures with a short-term time horizon will be announced separately and concurrently, such as Friday’s decision by the Ministry of Finance to front-load local government debt quotes. Nonetheless, even with a five-year view, the state of households and household demand will feature heavily. Expectations are already high for guidance surrounding stimulating consumer spending and directing investment into new infrastructure, tech innovation and social services. However, it won’t be an “all-out” push for growth either as “common prosperity” remains at the heart of long-term economic planning, featuring policies aimed at reducing inequality, improving the social safety net (pensions, healthcare) and promoting a more balanced distribution of wealth. The last point is important for cross-border investors looking at equity exposures: even though there are signs of demand picking up from wealth effects related to the recent run higher in domestic assets, general equity ownership in China as a share of household is far smaller compared to developed market peers, so there won’t be any “doubling-down” in an equity push and we doubt it was a central strategy in the first place.

This year’s equity surge has caught cross-border investors off-guard and we have not detected much participation throughout the run. Nonetheless, the improvement in asset values has been enough to generate a significant overweight exposure in CNY, but finally we are seeing signs of a catch-up in hedging. If the current sell-off extends, pressure to add to USDCNY forward purchases may also ease. The plenum aside, headlines surrounding the proposed month-end summit between Presidents Xi and Trump in Seoul will also be a core sentiment driver. The market’s base case remains for the summit to take place on the October 30, but some détente on export restrictions is needed first, even if only behind the scenes.

Forward look: Elsewhere in APAC, the key event is Japan’s special diet session to elect a new prime minister on October 21. With the Ishin party’s withdrawal from talks with opposition members and tentative agreement with the ruling Liberal Democratic Party, in addition to confidence from LDP’s traditional partners Komeito, Sanae Takaichi looks on track to become Japan’s first female prime minister. Markets are very cautious on her fiscal strategy and its impact on monetary policy, but recent BoJ commentary and the JPY’s better performance amid global risk aversion suggests the currency’s haven status is intact for now. Policy decisions in Indonesia and South Korea are also due: no change is expected in either, but emerging market central banks globally have begun to surprise to the dovish side throughout the month so positioning will reflect a similar lean, not least to complement the current risk-off tone in global equities.

The convergence of credit fragility, carry trade stress and uncertain policy signals have left global markets vulnerable to further correction. Investors are transitioning from passive “buy-the-dip” behavior to active alpha-seeking strategies, as volatility and liquidity risks redefine short-term positioning. U.S. earnings and inflation data will determine whether stagflation fears become embedded, while Europe’s industrial malaise and China’s policy recalibration test the global growth pulse. The next phase favors tactical flexibility: overweight quality credit and defensive duration, underweight crowded carry and cyclical exposures. With geopolitical and macro catalysts clustered into late October, the balance between risk-taking and capital preservation will hinge on whether inflation moderation offsets credit tightening. In this environment, capital discipline, selective exposure to high-quality assets, and readiness for asymmetric volatility are key to navigating the evolving macro landscape.

Central bank decisions

Hungary, MNB (October 21, Tuesday) – The National Bank of Hungary is expected to keep rates on hold at its upcoming meeting, maintaining the base rate at 6.50 %. The bank faces persistent inflation above its 3% ±1pp tolerance band and sticky inflation expectations, leaving little justification for an easing move. Even with October’s flat monthly inflation print, annualized inflation remains at 4.3% and wages are running well above CPI at 8.7%. The risk of renewed fiscal impulse requires additional restrictiveness but this is not a new challenge for the MNB. iFlow is showing significant unwinding of HUF exposures so managing pass-through is also necessary.

Indonesia, BI (October 22, Wednesday) – BI is expected to cut rates by 25bp to 4.50% as both headline and core inflation remains well-anchored enough on the 2-handle to ensure enough policy space exists for easing. The market was surprised by the cut in September, though the bank had warned beforehand that it was going to “look for room to further lower rates” and support growth, so maintaining this stance should not have come as a surprise. Nonetheless, with markets now in a more febrile mood regarding risk appetite, maintaining financial stability and orderly functioning is just as important, necessitating the affirmation of its triple intervention strategy, complemented by the utilization of offshore NDF instruments.

South Korea, BoK (October 23, Thursday) – The BoK is expected to keep rates on hold at 2.50% for the third consecutive meeting to maintain relatively restrictive financial conditions while credit impulse continues to advance. Bank lending to households surprised to the upside in September and inflation is once again ticking up, with headline prices moving above 2% in September. iFlow shows that cross-border hedges on South Korean assets have started to wane, indicating strong belief in KRW valuations, but tolerance for appreciation will face sterner tests in a more subdued external demand environment. How low-yielding APAC currencies behave amid a U.S. equity selloff will also be a factor in managing financial conditions.

Türkiye, TCMB (October 23, Thursday) – The TCMB is expected to cut rates by an additional 100bp even as the path toward inflation normalization remains frustrating. Expected inflation over the next 12 months has ticked up again to 23.25% and questions over real rates, especially in a risk-off environment, will remain challenging for TCMB. Imported prices should not have much of an impact, but managing domestic financial conditions remains a struggle, with house prices continuing to rise at a pace close to the TCMB’s repo rate, a clear sign that inflation expectations require stronger anchoring. In a risk-off environment, caution is necessary for EM easing, especially with foreign inflows softening.

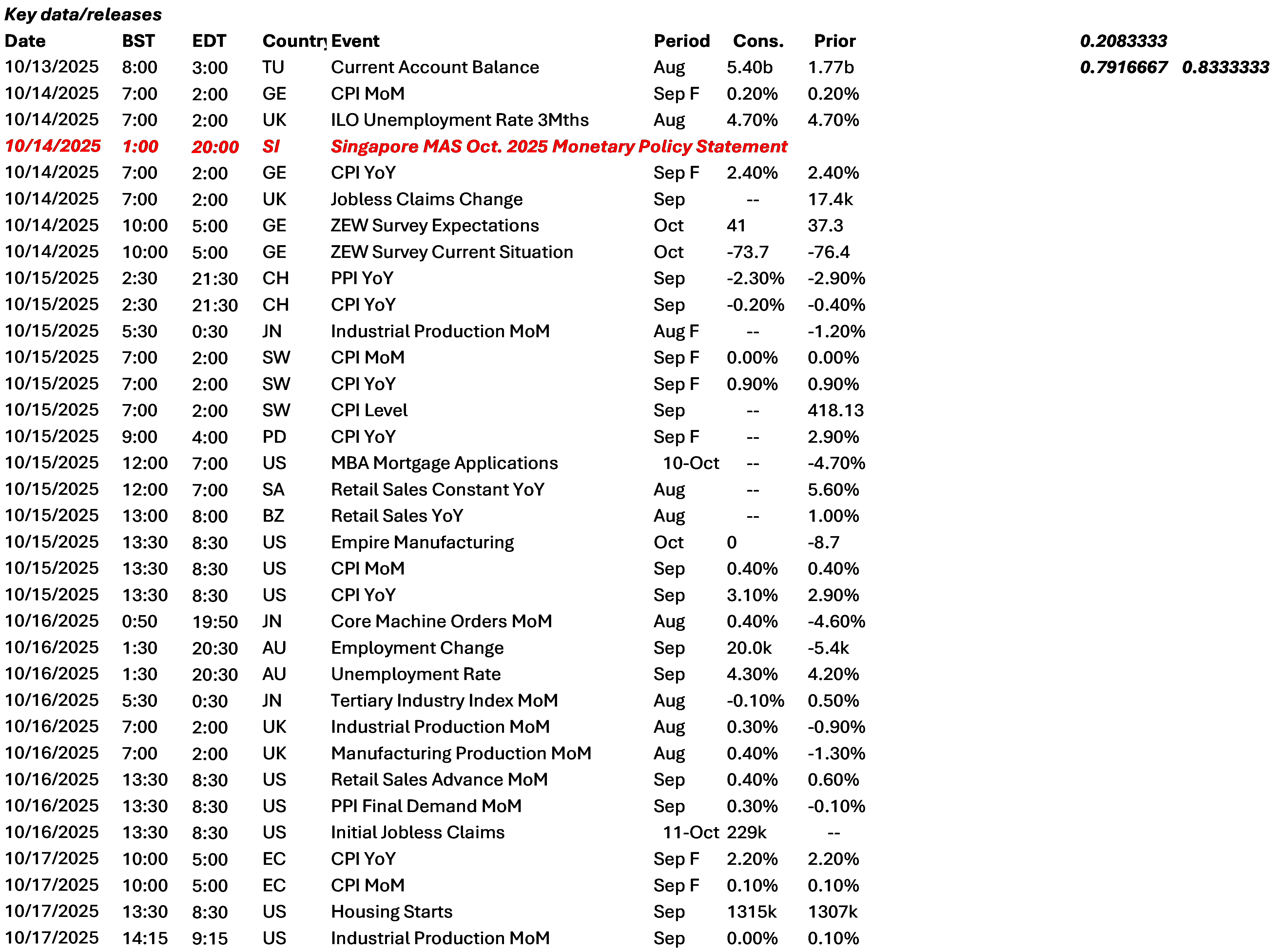

Data Calendar

Event Calendar