Talking Markets Up

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 10 minutes

Risk returns to global markets on the hope that U.S.-China talks lead to real solutions to end the trade war quickly enough to beat back secondary effects on inflation and growth. The U.K. deal with the U.S. was likely the easiest and still leaves 10% tariffs in place – suggesting a few things for the world in the week ahead:

The FOMC’s decision to hold off on a rate cut contrasted with cuts from by the Bank of England and the central banks of Poland and the Czech Republic. The rate hike by COPOM, Brazil’s central bank, was the exception and likely the last in their series of hikes as the carry trade finds a friend in BRL. Markets have returned to pre-“Liberation Day” volatility levels. This is good but not sufficient to unwind the pain of Q1, when uncertainty led to unpredictability. The lessons of April for investors were not lost on May markets but may not test well going forward. Students of markets know that elevated policy uncertainty with demand downside spells trouble for central bankers and politicians. There is another week of heavy foreign news flows – and slightly lighter U.S. data, with the CPI and retail sales key.

The data releases over the next week (including China CPI, tGerman ZEW indicator of economic sentiment, U.K. jobs, India WPI, Australia jobs, China credit growth, money supply, OPEC monthly, U.K. GDP, EU jobs and industrial production, Japan GDP) are all important, making hard data from abroad fundamental to the rising view that rate cuts everywhere are closer to the bottom than they are to continuing.

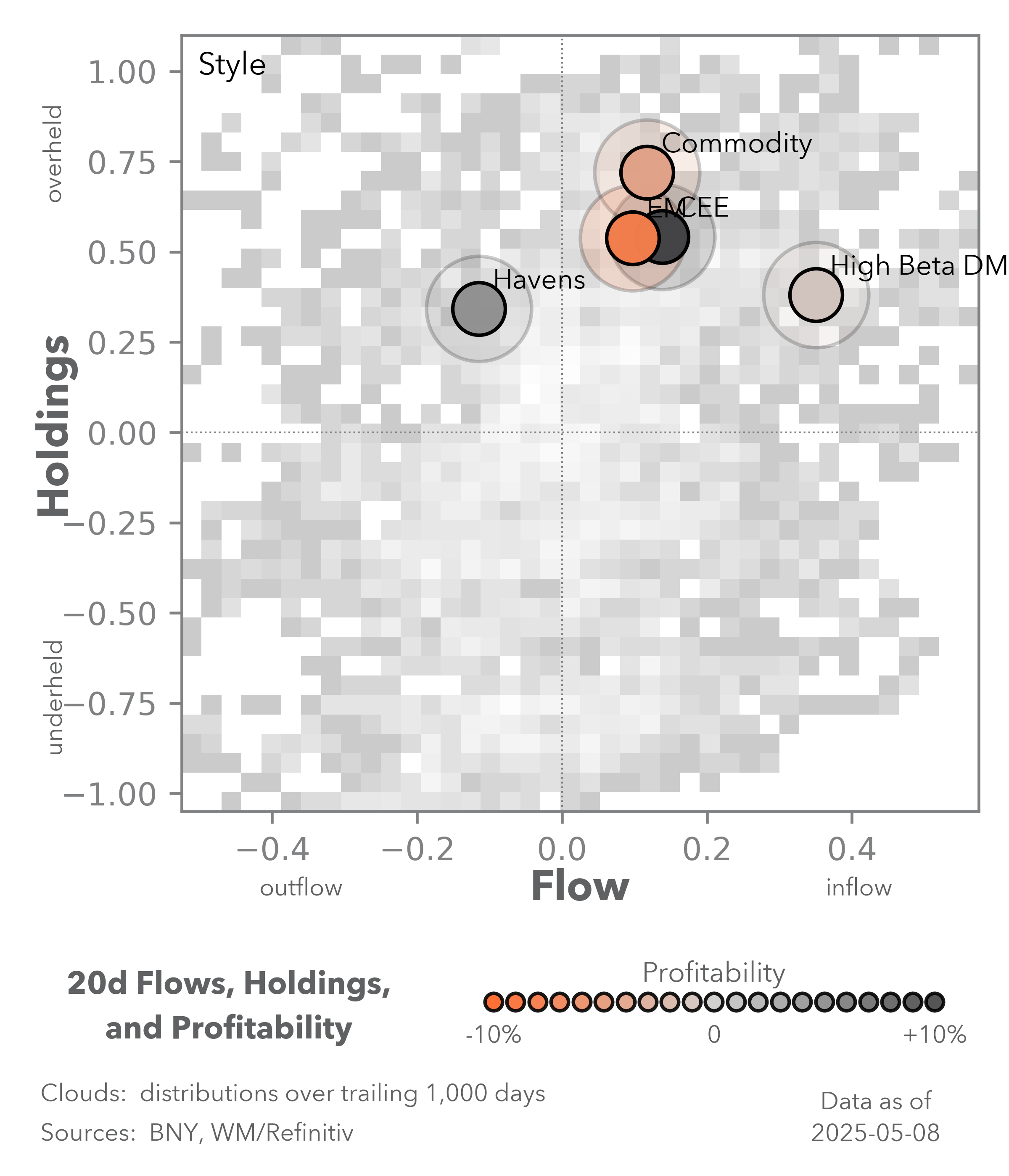

Beyond Brazil, what carry trades stand out?

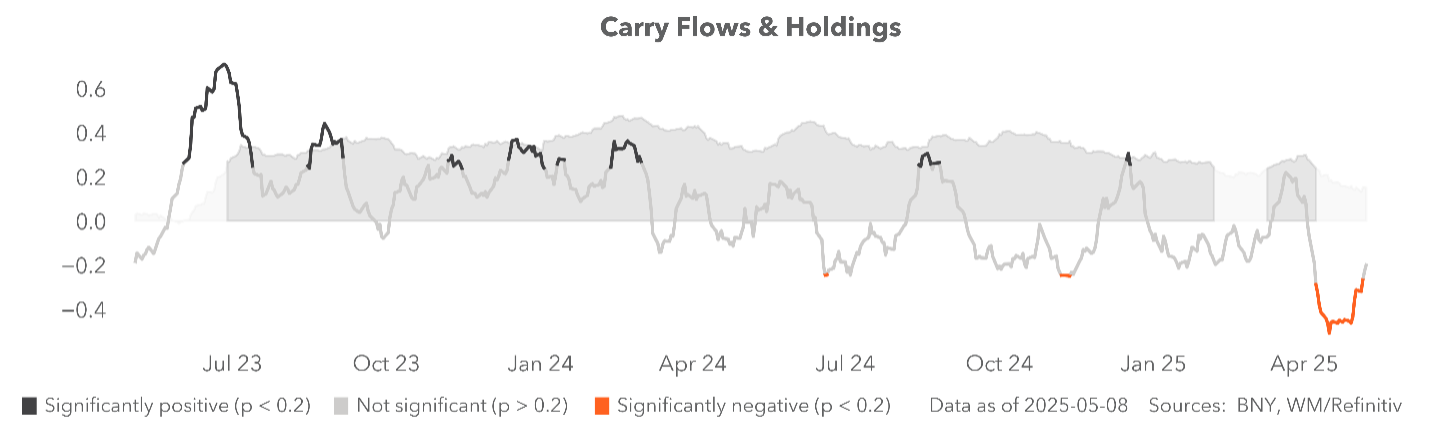

EXHIBIT #1: CARRY FACTORS IN FX RETURN TO NEUTRAL

Source: BNY

Our take: The flows over the last week in BRL stand out, and investors will focus next week on whether the COPOM minutes reveal a pause or peak in rate moves. The carry trade in Brazil is linked to USD movements and the government’s ongoing response to fiscal pressures. There is a lesson for other carry trade favorites in Brazil. The bounce-back in sentiment on all risk correlates well to our iFlow Carry index – global share buying is connected to carry and reflects the normal correlation of rates to equities. The prerequisite for carry success remains moderate to lower volatility.

Forward look: In the week ahead, the focus may shift from Brazil, which quickly became overweight in emerging market books, to Mexico, where the Banxico is expected to cut 50bp even though inflation is stickier than hoped and growth is weaker. Cutting just 25bp would send a message, one that would likely grate on those pushing for growth. The problem for all central bankers is whether the shocks of tariffs and drop in confidence can be revived by faster easing. The role of the weekend trade talks with China may foreshadow the long grinding talks to rewrite the U.S.-Mexico-Canada Agreement (USMCA). The other carry trade favorites – Indonesia and Egypt – stand out in the week ahead as well, with a focus on geopolitics again more dominant than economic data – peace hopes in MENA, whether in Iran or in Israel, matter, just as the China trade talks and Taiwan do to Indonesia.

U.S. markets focused on trade talks and inflation expectations

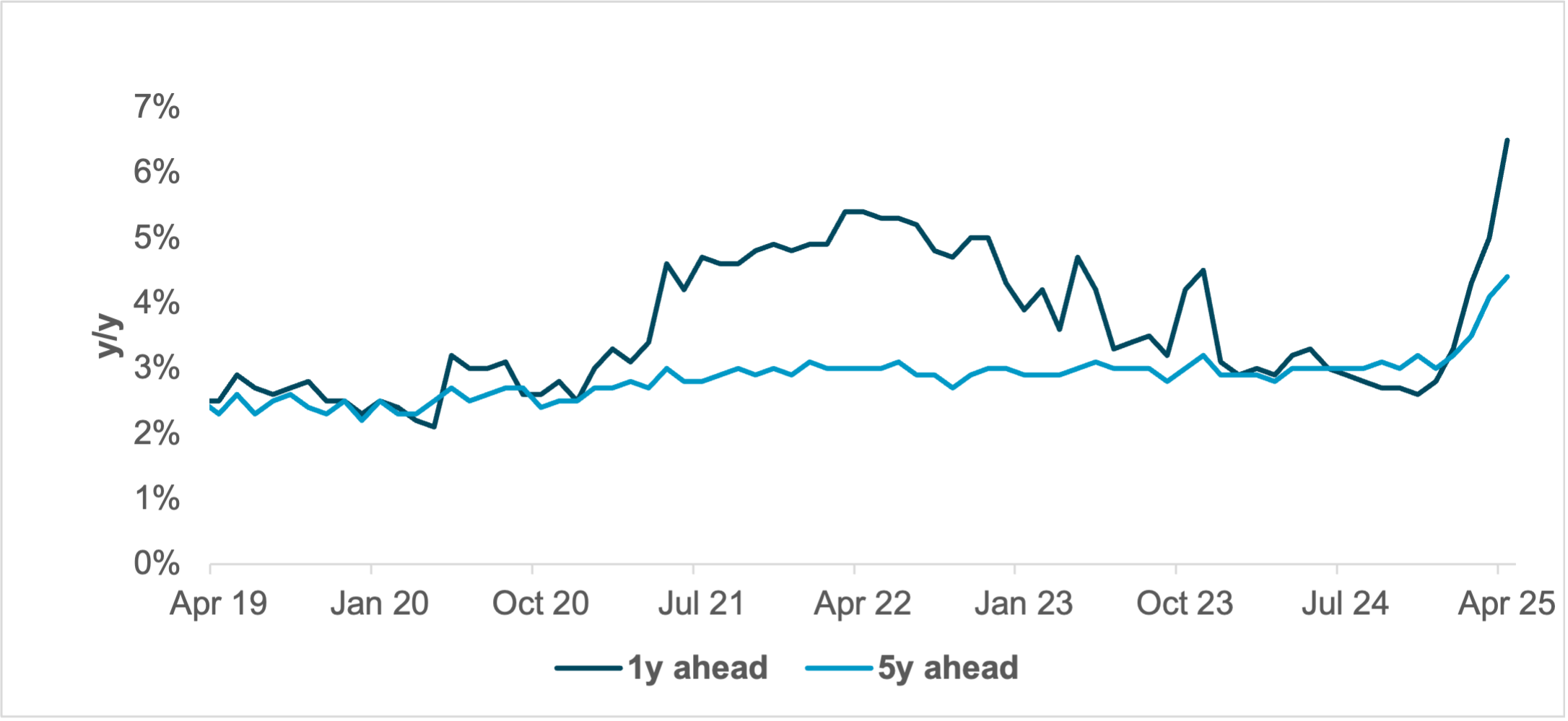

EXHIBIT #2: UNIVERSITY OF MICHIGAN INFLATION EXPECTATIONS MOVE HIGHER

Source: BNY, University of Michigan

The tone at the start of the week will be largely determined by what we learn about the administration’s meeting with its Chinese counterparts in Switzerland to discuss tariffs and trade. But there are some noteworthy data points to come in the next week that could also affect markets.

Our take: Inflation, via the CPI and PPI releases, will be among the key events thisis week, starting on Tuesday. DDespite lower oil prices, we believe we believe goods inflation could start to show up already in April. We can see if and how consumption reacted in April with Wednesday’s retail sales report, and we will check in on Friday to see to see whether the soft data on consumer sentiment from the University of Michigan continues to deteriorate. So, all in all there will be enough data coming out next week on enough topics to help us determine the effect of tariffs and uncertainty so far.

Forward look: The current Fedspeakers’ schedule is not extremely crowded for the week. Governor Waller and Chair Powell each take turns at the microphone, although the listed topics for each of their speeches don’t seem to promise much chance of either of them discussing the policy or economic outlook in detail. Congress will start debating the budget package this week as well, although our view is that the reconciliation package will have trouble getting passed quickly as there is still much to be hammered out.

As Merz begins his term, the clock is ticking on a comprehensive domestic investment plan in Europe

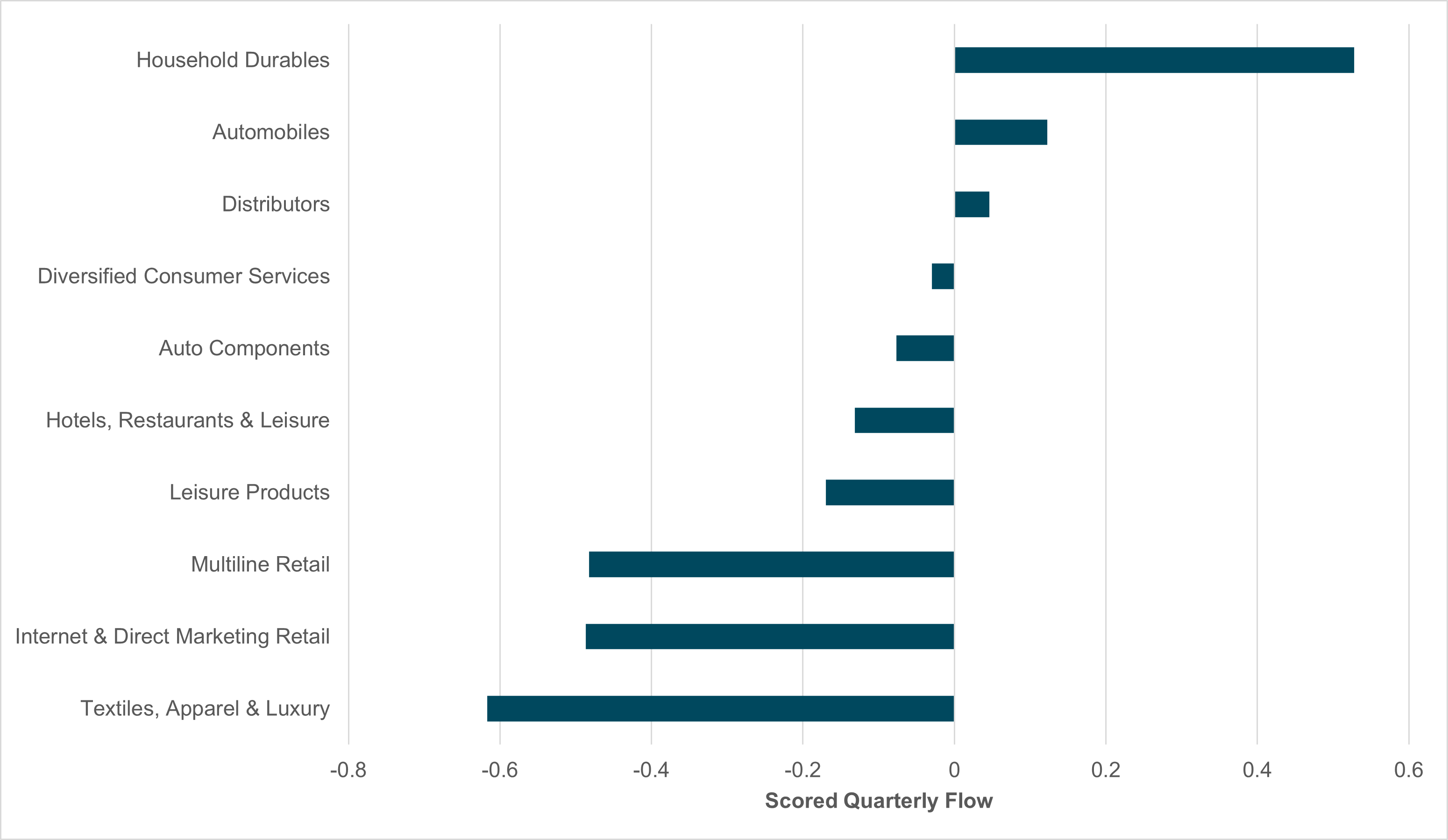

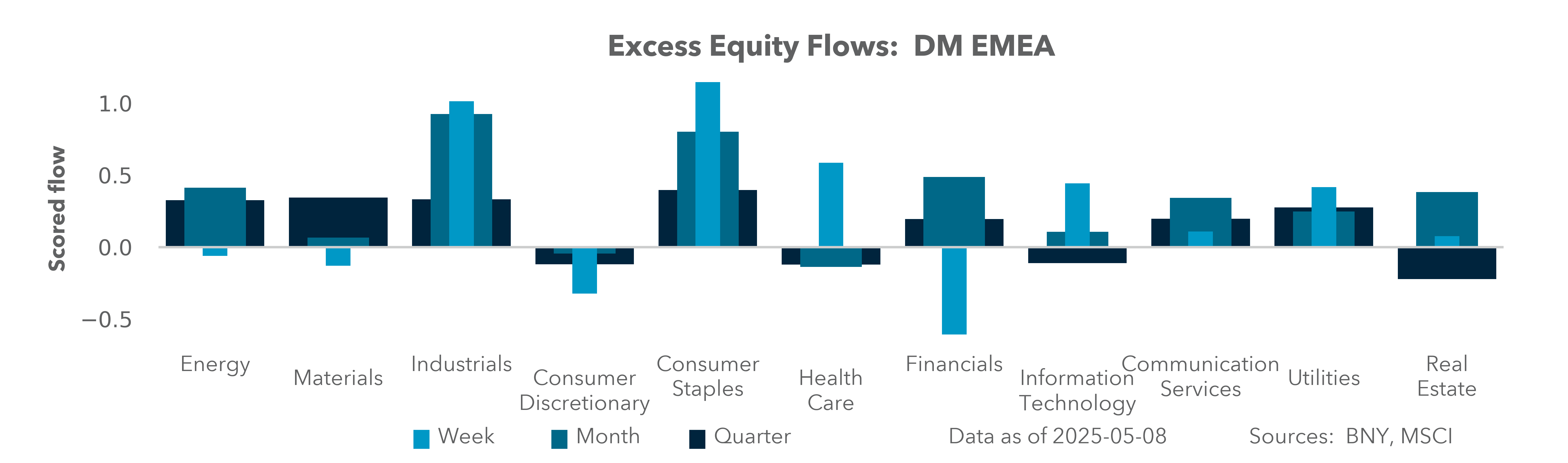

EXHIBIT #3: EUROPEAN EQUITY CONSUMER FLOWS, PAST QUARTER

Source: BNY

Our take: As the U.S. has announced its first trade deal with the U.K. and now begins talks with China, the EU could be forgiven for feeling somewhat left out. The mood music at present is not positive and the past week has seen multiple announcements surrounding countermeasures against the U.S. rather than progress toward an agreement. The insistence by the U.S. on pushing for VAT concessions is a red line for Europe. Compared to the U.K., which has a flat goods trade balance with the U.S., Europe’s surpluses will present more of a challenge given the U.S. administration’s stated preferences to reshore highly value-added manufacturing on a large-scale basis. Elsewhere, hopes of greater rapprochement with Beijing over trade also appears to be stuttering, with European Ambassador to China Jorge Toledo warning on Friday that “China has not been taking EU seriously on trade issues, and the situation of EU companies in China is worsening.” Our base case is for European trade détente with the U.S. and China, but progress is needed soon. The earnings outlook globally is challenging and Europe finds itself in the unusual situation of heading into such a phase from a preferential position in asset allocation at the end of Q1. Consequently, rebalancing bias will now move against European companies and raise the bar for sustained outperformance or overweight allocations. Meanwhile, the outlook for the U.S. has improved slightly, while the market is clearly shifting toward APAC, to the extent that regional central banks now need to ease aggressively to prevent equity inflows from strengthening currencies excessively. In contrast, the valuations risk to Europe is now to the downside, especially with the level of the euro looking restrictive, and we expect ECB speeches next week to ramp up the pressure.

Forward look: Our main concern for European assets is that the re-rating flow seen in Q1 will begin to reverse. Trade and Ukraine were always going to take time to resolve, but these topics initially supported flows into Europe under the Franco-German banner of European strategic autonomy, supported by the swift constitutional adjustments in Berlin to restructure the European economy toward domestic demand (especially in defense) and consumption growth. However, Merz’ chancellorship could not have started in worse fashion after the failure his first appointment vote immediately called into question the durability of the German government. Meanwhile, domestic data show struggling household sentiment, likely to be compounded by a loss in export earnings. Investors remain overheld in specific sectors in Europe such as defense and industry, which have propelled the DAX to a new record. However, over the past quarter, our data show the majority of consumer-related industry groups have struggled severely (Exhibit #3). Some sectors reflect external condition, such as luxury goods, but flows generally match sentiment. We fully believe Chancellor Merz understands the urgency, but without a comprehensive investment program in the coming quarter, coupled with weak earnings and euro strength, European equities run the risk of sharp unwinding.

China credit growth recovery but downside risk for regional exports

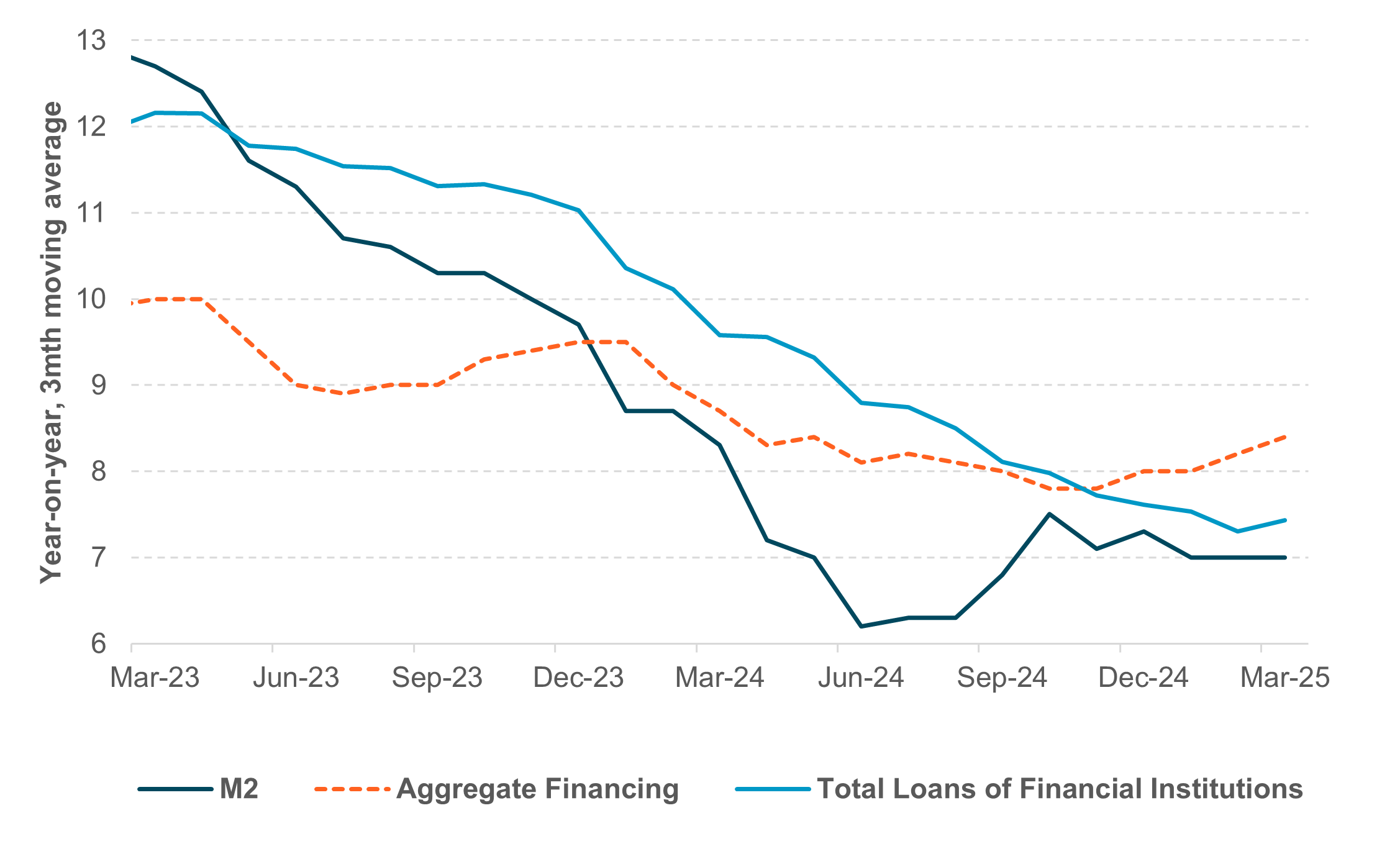

EXHIBIT #4: FURTHER RECOVERY OF CREDIT GROWTH MOMENTUM

Source: BNY

Our take: APAC macroeconomic data over the past two weeks have confirmed downside growth and inflation risks in the region. April inflation had surprised to the downside, while Q1 GDP was weak and dominated by considerable uncertainty about the outlook. While market sentiment had improved over the optimism of a potential trade deal with the U.S., hard data are likely to stay sluggish in the near term.

The key focus in APAC this week is China April credit data, regional April exports data from India, Indonesia and Singapore as well as Australia April jobs data and New Zealand Q2 inflation expectations. China credit data had shown sign of a turnaround, with aggregate financing back at May 2024 levels at 8.4% y/y. Such an upward trend is likely to continue, supported by higher central and local government bond issuance. All eyes will be on the growth of loans by financial institutions, which halted 16 monthly declines and ticked up in March at 7.43% y/y. The latest reduction of the China Reserve Requirement Ratio, which will release CNY 1tn in long-term liquidity, is likely to be supportive and encourage more bank lending to the real economy.

Elsewhere, April exports in India, Indonesia and Singapore as well as the latest export data as of the first 10 days in May in South Korea will be crucial as a gauge of the immediate tariff-related impact. China exports were stable at 8.1% in April with strong exports to Europe and ASEAN countries, but persistently sluggish China imports might not bode well for the region considering the country is one of the top export destinations for ASEAN. The risk is to the downside after relatively subdued exports growth in Q1 2025.

Lastly, Australia May consumer inflation expectations and April job market data and New Zealand April PMI manufacturing and Q2 inflation expectations will be key parameters ahead of RBA and RBNZ policy decisions later in May.The key focus in APAC this week is China April credit data, regional April exports data from India, Indonesia and Singapore as well as Australia April jobs data and New Zealand Q2 inflation expectations. China credit data had shown sign of a turnaround, with aggregate financing back at May 2024 levels at 8.4% y/y. Such an upward trend is likely to continue, supported by higher central and local government bond issuance. All eyes will be on the growth of loans by financial institutions, which halted 16 monthly declines and ticked up in March at 7.43% y/y. The latest reduction of the China Reserve Requirement Ratio, which will release CNY 1tn in long-term liquidity, is likely to be supportive and encourage more bank lending to the real economy.

Elsewhere, April exports in India, Indonesia and Singapore as well as the latest export data as of the first 10 days in May in South Korea will be crucial as a gauge of the immediate tariff-related impact. China exports were stable at 8.1% in April with strong exports to Europe and ASEAN countries, but persistently sluggish China imports might not bode well for the region considering the country is one of the top export destinations for ASEAN. The risk is to the downside after relatively subdued exports growth in Q1 2025.

Lastly, Australia May consumer inflation expectations and April job market data and New Zealand April PMI manufacturing and Q2 inflation expectations will be key parameters ahead of RBA and RBNZ policy decisions later in May.

Forward look: While downside growth and inflation risks continue to weigh, the overall stabilization and positive progress from trade negotiations is likely to be positive for Asia risks in the near term. Near-term policy easing is supportive for equities and fixed income, while we expect further normalization of APAC currencies against the U.S. dollar after a long period of dislocation in Q1 2025.

The week ahead has the makings of being quiet, but there are ongoing tail risks that look important and just won’t go away. Talking up markets has been the task of the Trump team this past week, and whether this continues into the next week will likely matter more than the economic data. The hope of soft data bouncing and hard data holding remains central to keeping the summer ahead stable. However, none of that is really sufficient to heal the April pains in bonds and stocks. The shock absorber of the USD remains in play and the rally back in the dollar has been fast. Whether this continues to play out will be how hedge ratios shift in May month-end and whether fiscal issues start to matter as much as tariffs to investors. The only real certainty for the week ahead is that time is needed to heal the wounds of April sufficiently to see U.S. exceptionalism put back together. We may have to wait for Nvidia earnings on May 28 to see this really turn around for AI and U.S. shares, and until then we need to wait and see how the rest of the world catches up.

Central bank decisions

Mexico Banxico (Thursday, May 15) – The Bank of Mexico is widely expected to cut rates by 50bp to 8.5% at its May meeting, as inflation remains within target and economic growth falters. Annual inflation rose slightly to 3.93% in April from 3.80% in March, with core inflation also at 3.93%. Monthly consumer prices climbed just 0.33%. Deputy Governor Jonathan Heath noted that sluggish first-quarter growth of 0.2% has helped ease inflationary pressure, creating space for further monetary easing – though he cautioned that a slower pace may be warranted later in the year. Meanwhile, U.S.-Mexico trade relations have come under strain following the imposition of new U.S. tariffs, raising risks for external demand. Market expectations remain aligned with Banxico’s cautious easing path amid both domestic and external headwinds. iFlow indicates some recovery is now afoot in carry interest but enthusiasm is limited.

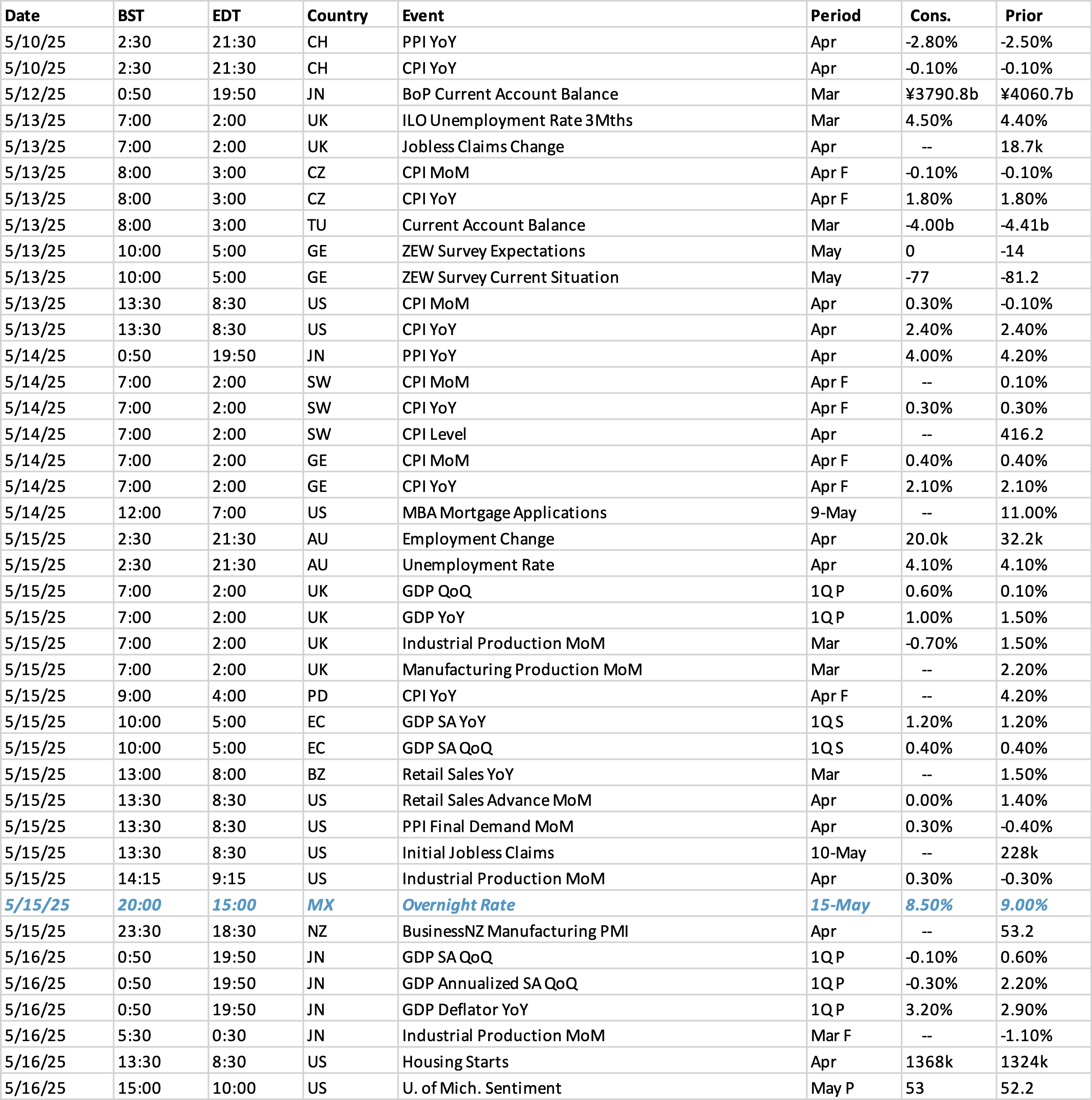

Data Calendar

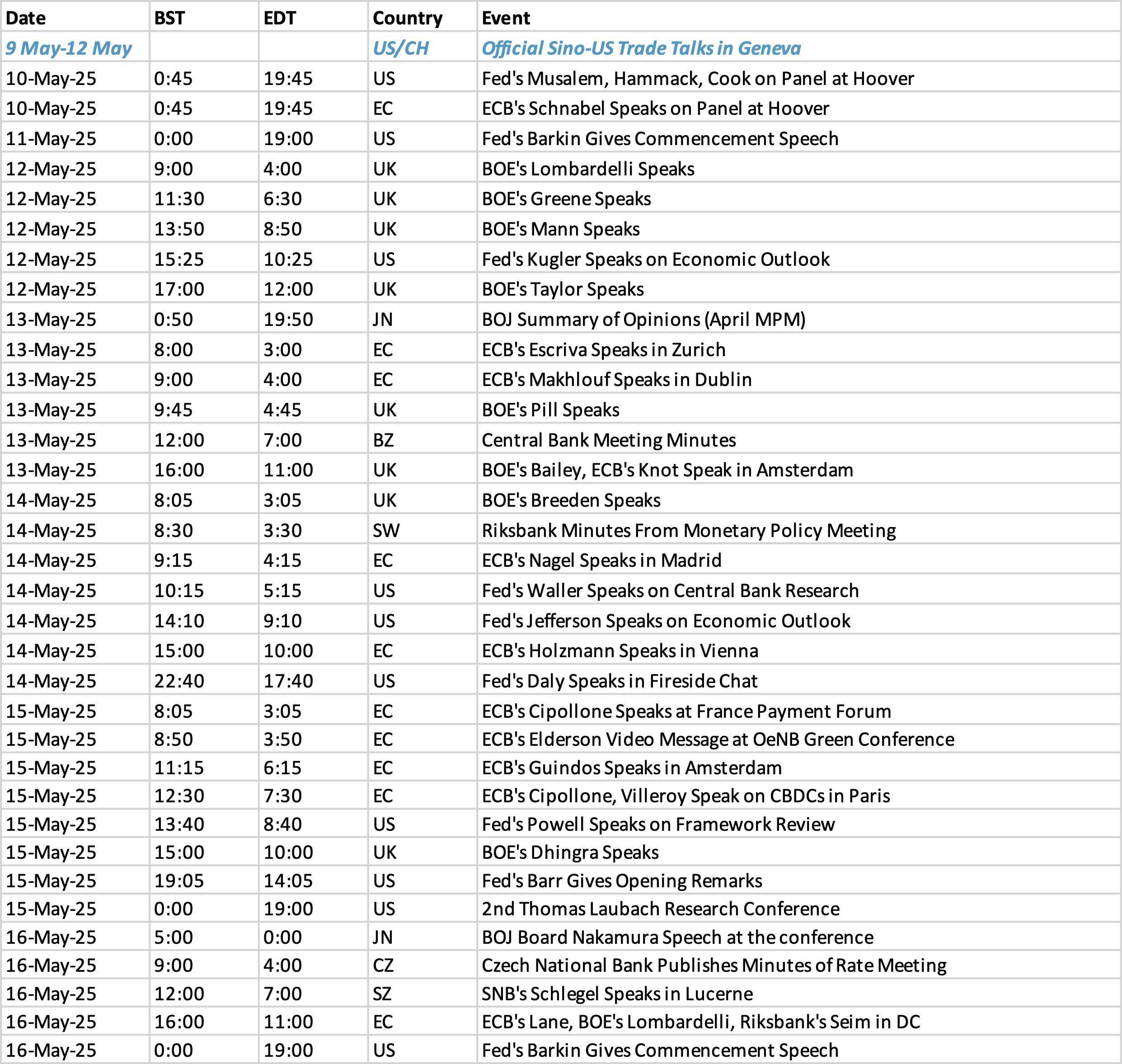

Event Calendar