Tactics Beat Strategy Again

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 9 minutes

There are only two weeks to go for the adage “sell in May and go away” to prove accurate. U.S. shares have bounced back so much from their lows in 2025 the S&P 500 is flat on the year, having returned to February levels. Fear of missing out is impacting short positioning, and momentum factors will continue to work until investors recognize the risk of a sharp rise in tracking error. Inflows into equities have increased holdings at the expense of bonds, adding to asset allocation risks. But a yield of 4.50% on 10-year notes is still an important part of the equation. Growth and inflation pressure are clearly part of the story of money flows and reallocation pressure as we head into the month-end. The U.S. data this past week suggest growth will bounce back in Q2, but there are cracks in consumer demand as retail sales missed and manufacturing production declined. The FOMC is still expected to cut rates two to three times, but recession fears have receded. Chair Powell made it clear that supply shocks ahead make anchoring inflation expectations even more important, and the May flash consumer inflation expectations for 1-year at 7.3% are troubling. For the next week, lack of economic data in the U.S. puts the focus back on politics, with the Congressional tax bill, Trump’s tariff deals, the G7 meeting in Canada, and an ongoing geopolitical focus on Russia-Ukraine peace talks, a possible Iran nuclear deal and India-Pakistan talks all potentially generating significant volatility and stalling momentum buying.

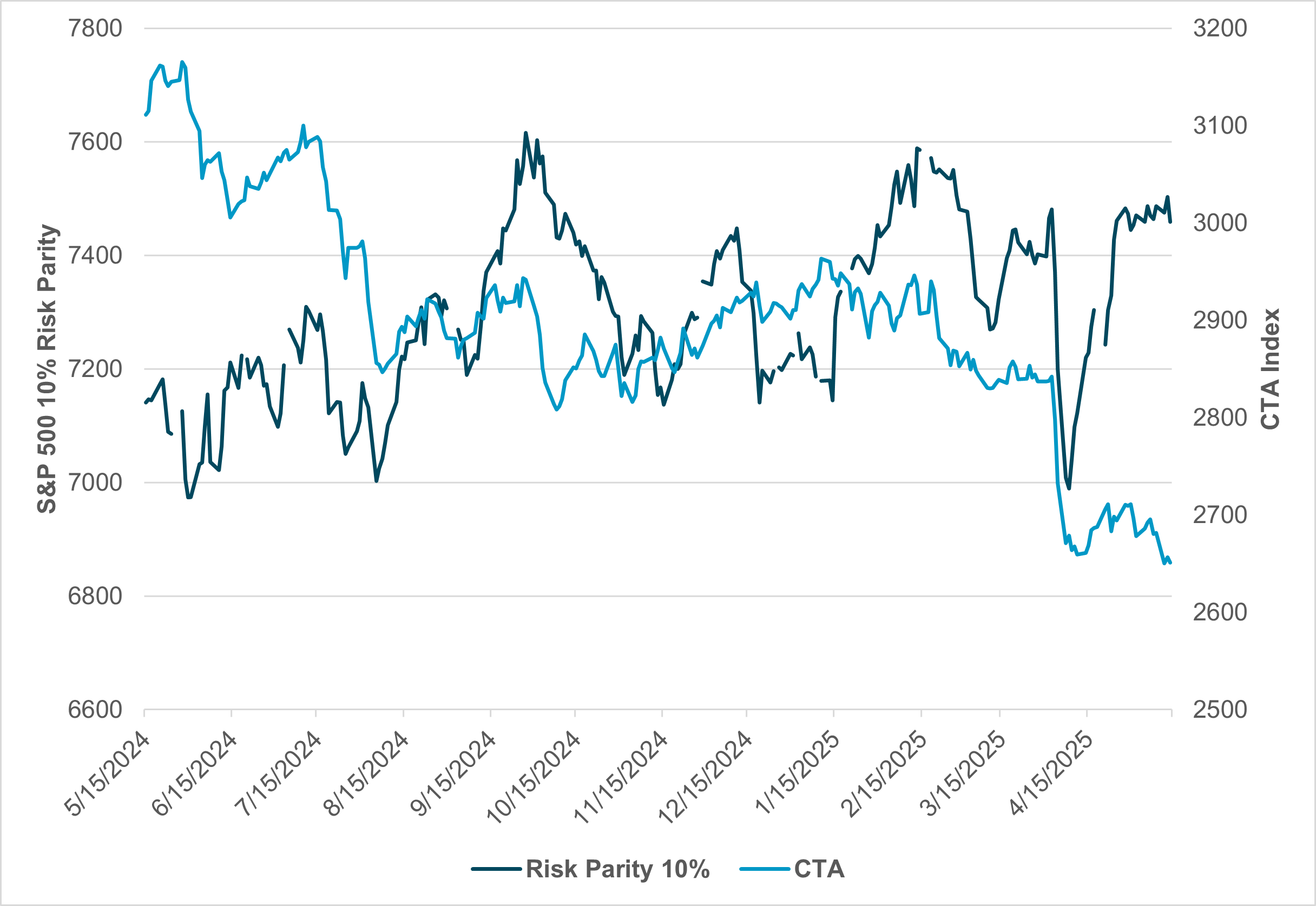

EXHIBIT #1: RISK PARITY OUTPERFORMS IN APRIL AND MAY, AS TREND FOLLOWING FALLS (TREND VS. VOLATILITY)

Source: BNY, Bloomberg

Our take: Despite the sharp gain in stocks from mid-April to Mid-May, trend following programs are losing money. CTA fund managers are frustrated by the shifting correlations and the failure of gold and EUR to extend their upward movement. The volatility and lack of consistent returns are taking their toll on future leverage and trading activity. For many investors who look at the last 12 months of returns, the risk of a slow and quiet summer trading season looms as cash and a wait-and-see attitude could dominate investment styles across asset classes. However, the market volatility has helped asset allocation, and this rewarded the current “buy U.S.” story. Markets are clearly still choppy and nervous, with the scars of April still a significant brake on full risk-on behavior for investors.

Forward look: In the weeks and months ahead, the risk of surprise outcomes remains significantly higher than during previous periods. This is because the tariff pause may be insufficient to resolve all of the risks ahead for growth and inflation and the response by consumers, businesses and the rest of the world. We believe current allocations are unsustainable and expect further U.S. yield curve steepening along with further U.S. dollar weakness. The equity market may have less resistance to enable the S&P 500 to break through 6,000, but value and a lack of urgency will limit fear of missing out. Range trading could dominate in the week ahead until not having a position itself becomes a risk.

U.S. data unlikely to shift view of July Fed cut, as BoC watches CPI and retail sales

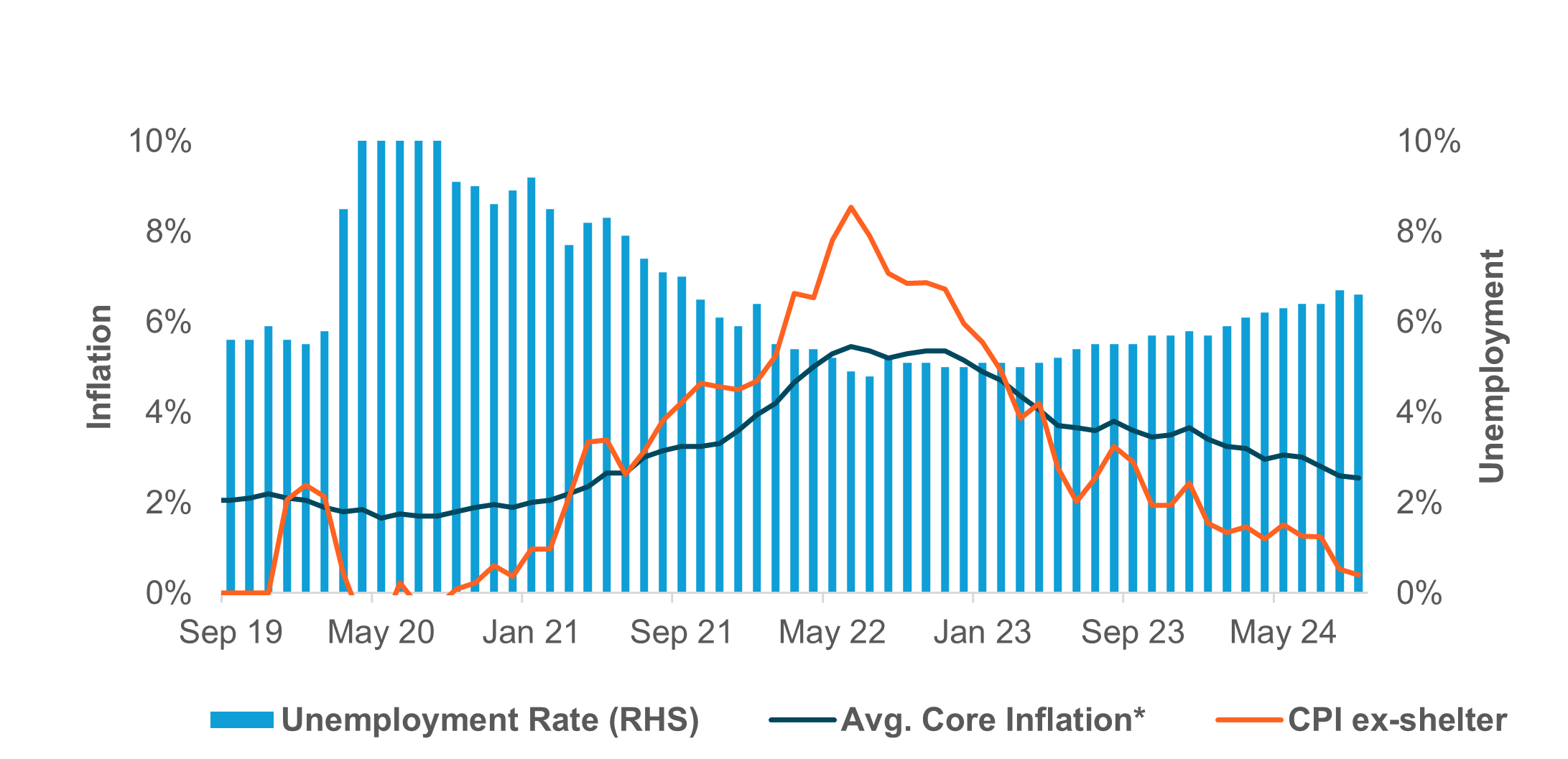

EXHIBIT #2: CANADA INFLATION AND EMPLOYMENT LEAVE ROOM FOR THE BOC

Source: BNY, Bloomberg

Our take: There aren’t a lot of data releases next week in the U.S., although we do start to get some of the purchasing managers’ indices, particularly the S&P Global PMI. Soft data, as we know, have deteriorated for a few months now, and this would be the first survey since the China-U.S. climbdown in Geneva two weeks ago. We still haven’t seen hard data catching up to the soft data and we’re unlikely to start seeing pronounced weakness this coming week. We remain of the view that the May data – available in June, and even more likely the June data available in July – will show enough of a deterioration for the Fed to cut rates at its July 30 meeting.

Forward look: Up north, Canadian CPI will be reported on Tuesday and retail sales on Friday. The former is key to the Bank of Canada outlook, especially considering Governor Macklem’s focus on the inflationary effects of the trade war more so than any economic fallout for the real economy. If inflation misses to the downside, we could see increased expectations of rate cuts for the remainder of 2025. The market is currently pricing in just two more rate reductions out of Ottawa, but we think that the impact of the trade war could be felt particularly hard in Canada, and the central bank will have to pivot to easier policy. Note, however, that the BoC does not have a dual mandate à la the Fed, so a sticky inflation print could firm expectations of just two cuts.

EMEA: Trade deal hopes, earnings and equity flows key for markets

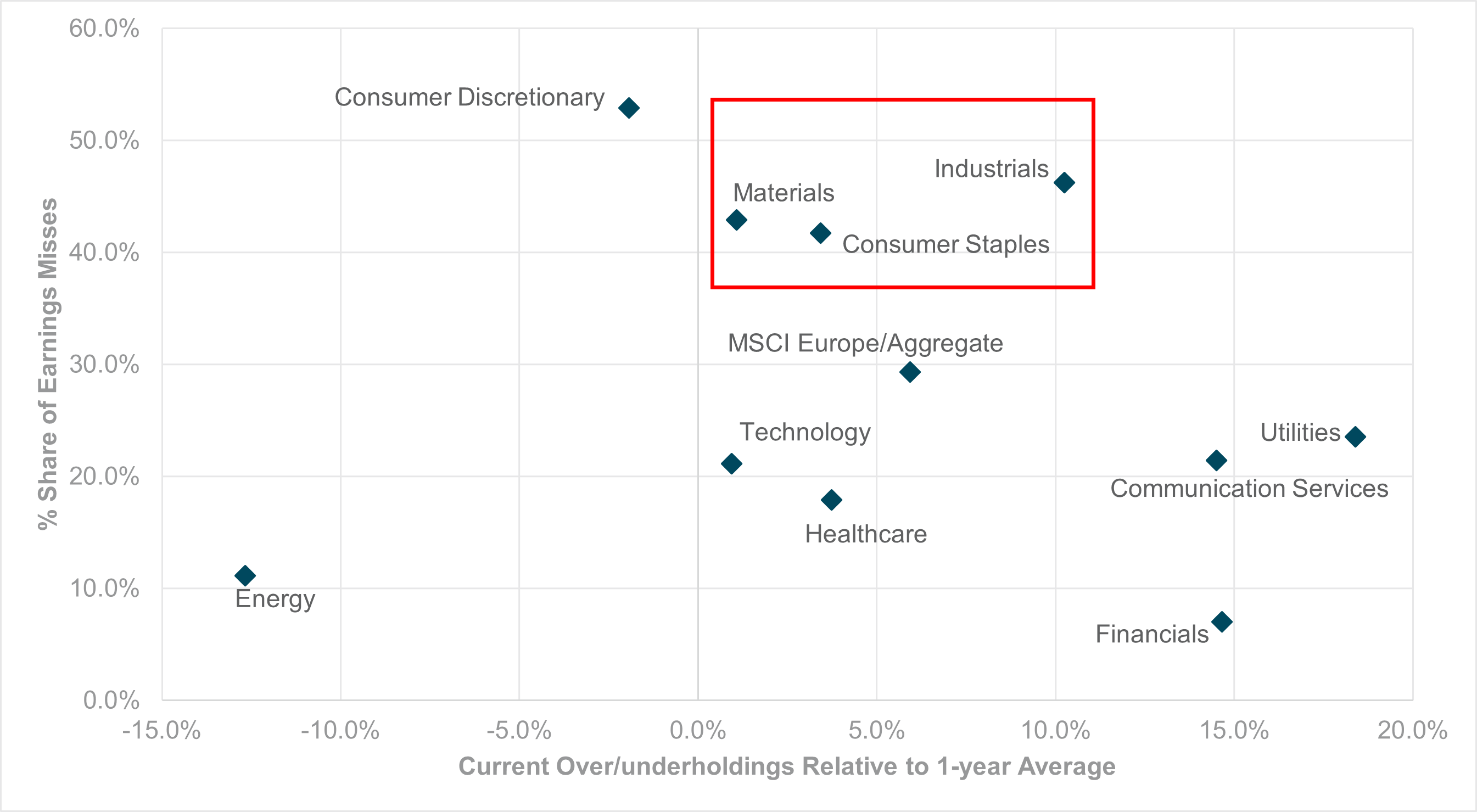

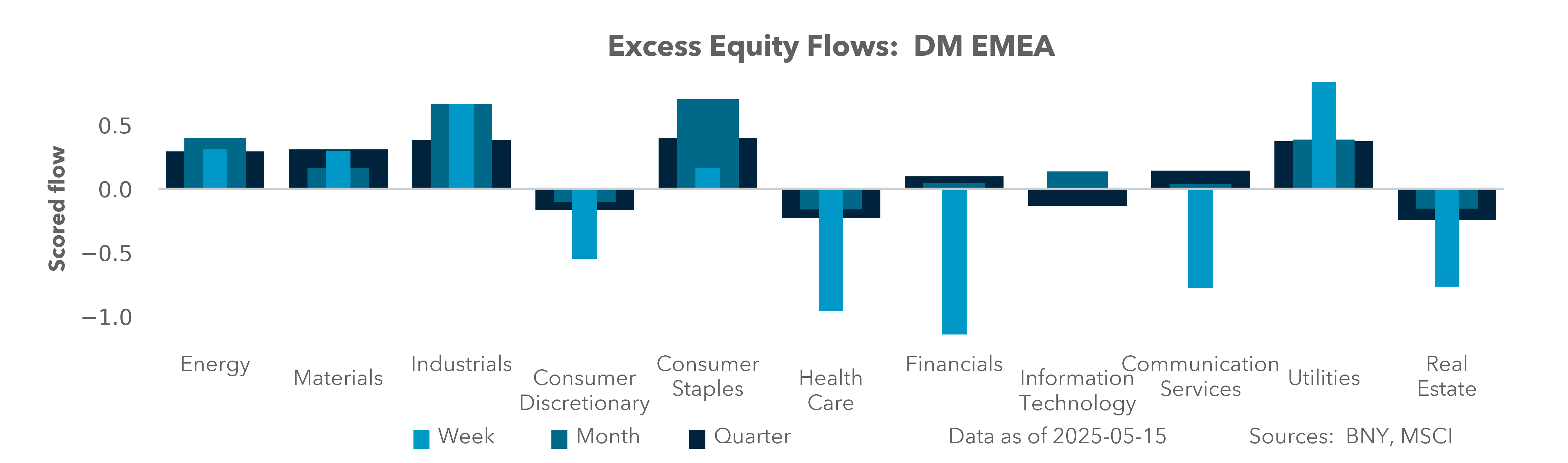

EXHIBIT #3: IFLOW EQUITY HOLDINGS BY SECTOR VS. CURRENT EARNINGS MISSES (Q1 2025)

Source: BNY, Bloomberg

Our take: Europe heads into the end of May with very few geopolitical wins, while the internal outlook could become even more fractured. Difficult election results in Romania and Poland will continue to give credence to the U.S. view that Europe’s “collective action” problem will prevent radical reforms, while the earnings results begin to catch up with current equity holdings. Most developed European equities are overheld relative to their 1-year average. The exceptions are consumer discretionary and energy, with the former the very segment which new fiscal efforts in German and the European Union are intended to reinvigorate. Even with a generally favorable outlook for European equities, markets appear reluctant to price in a turnaround in household spending. The international export component further limits re-rating. However, with nearly two-thirds of companies in the MSCI Europe index having reported earnings, there are some other sectors which are starting to look vulnerable. Industrials have the second highest share of earnings misses among this quarter’s earnings reports but looks disproportionally overheld (Exhibit #3). If the trend continues, current valuations may struggle up ahead.

Forward look: On the positive side, the latest GDP reports for Q1 coupled with April data suggest that momentum was stronger than expected across the Continent, while activity and sentiment did not collapse either – a trend that upcoming PMIs for May should affirm. Headline European inflation continues to fall materially, which means European bond markets will be less susceptible to yield shocks, which are re-emerging in the U.S. The week ahead will see a strong lineup of ECB policymakers as final guidance is provided for the June meeting, where on balance more precautionary cuts are needed to further stabilize the recent recovery in sentiment. However, we also fear that not enough progress is being made on the trade agreement front. Formal talks between the U.S. and Japan are now scheduled and the EU looks set to fall further down the G7 pecking order for near-term détente. As has been the case with asset allocation in recent weeks, a lack of “deals” will not jeopardize equity flows yet, but increased levels of FX hedging will come through to mitigate earnings risk.

China activities and investment, APAC trade and BI and RBA meetings

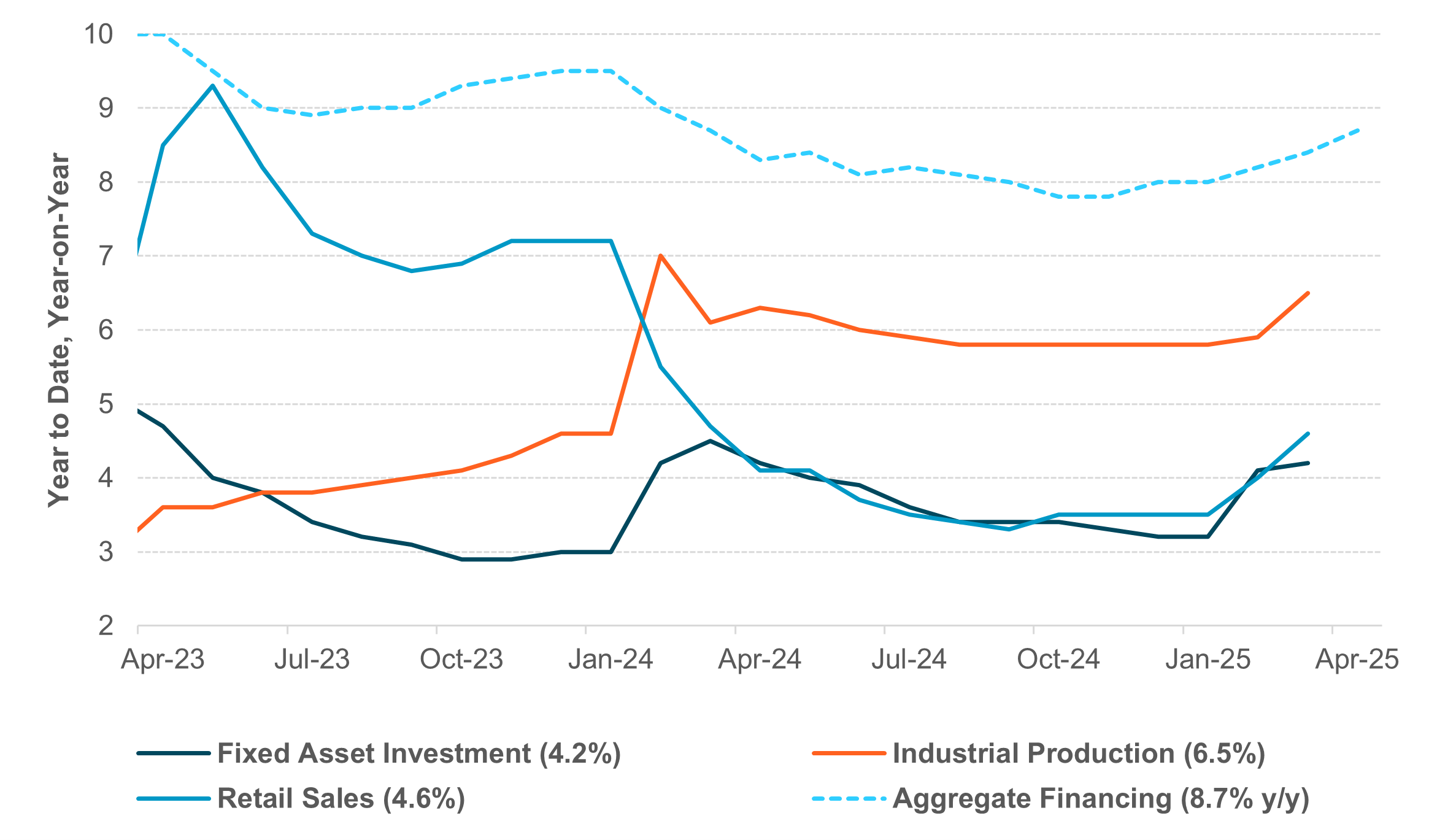

EXHIBIT #4: GRADUAL RECOVERY IN CHINA ACTIVITIES AND INVESTMENT DATA

Source: BNY, Bloomberg

Our take: In the Asia-Pacific region, the focus this week is on China’s April activity and investment data, alongside developments in the housing sector. Despite external uncertainties, China’s economy showed resilience in Q1, driven by domestic consumption and high-tech advancements. Key indicators include:

The easing of U.S.-China trade tensions and a new financial policy package are expected to bolster confidence in Q2 2025. A recent reduction in the 7-day reverse repo rate is anticipated to lead to a 10bp decrease in the 1-year and 5-year loan prime rates, currently at 3.10% and 3.60%, respectively. Housing prices have improved sequentially since Q4 2024, with residential building inventory growth slowing to 6.8% y/y from 24.6% y/y in May 2024, the lowest since December 2021.

Elsewhere in the region, export data from South Korea, Japan, Taiwan, Malaysia, Thailand and New Zealand are under scrutiny. April exports from Singapore and India exceeded expectations, driven by demand for machinery and electronics. Upcoming CPI releases from Singapore, Malaysia and Japan will provide further insight into inflation trends. Singapore's headline and core inflation have significantly decreased to 0.90% and 0.5% y/y, respectively, as of March, which may prompt the Monetary Authority of Singapore to adjust the SGD NEER policy slope to zero appreciation at the July meeting. Conversely, Japan’s Nationwide CPI faces upward risk following a spike in Tokyo’s CPI. In monetary policy, the Reserve Bank of Australia is expected to implement a 25bp rate cut, while Bank Indonesia is likely to follow suit, capitalizing on reduced IDR depreciation pressure to mitigate growth slowdown momentum.

Forward look: While downside growth and inflation risks continue to weigh, the overall stabilization and positive progress from trade negotiations is likely to be positive for Asia risks in the near term. Near-term policy easing is supportive for equities and fixed income, while we expect further normalization of APAC currencies against the U.S. dollar after a long period of dislocation in Q1 2025.

The coming week is poised to be pivotal, with key events and data releases set to shape market sentiment. Reduced fear may logically imply diminished upside.

The prevailing mood in global markets is stable but not overwhelmingly so, allowing momentum and other factors to steer trading activities. This equilibrium is precarious; position watching and any surprise developments could swiftly alter market dynamics, underscoring the importance of vigilance.

Central bank decisions

Reserve Bank of Australia (RBA) (Tuesday, May 20) – The RBA is expected to cut rates again, to 3.85%, but maintain caution in easing due to domestic and external uncertainty. Soft economic expectations require some support, but price pressures remain robust, with various indicators such as PPI, wages and consumer inflation expectations all at elevated levels and surpassing their most recent prints. Business confidence remains soft, however, while household credit impulse is also weak and the general resilience in AUD should help the RBA avert tradables inflation risk, even though current levels are well below target and diverging strongly from non-tradables inflation. We do not see much carry interest in G10 at present, though AUD may benefit from China-related tailwinds if stimulus materializes.

Bank Indonesia (BI) (Wednesday, May 21) – We expect Bank Indonesia to cut 25bp to 5.5% and to put an emphasis on FX stability. Asset price volatility has eased, but they are not completely out of the woods yet. Since the last meeting in April, global asset prices have normalized and reversed all their losses, with the JCI back to its February 2025 levels. However, USDIDR implied volatility remains high while macro data has been affected by uncertainties surrounding U.S. tariffs. We see the easing of trade uncertainty providing a window of opportunity for Bank Indonesia to stimulate domestic growth and provide a boost to domestic government bonds. Bank Indonesia is expected to continue its triple intervention strategy as well as via offshore NDF.

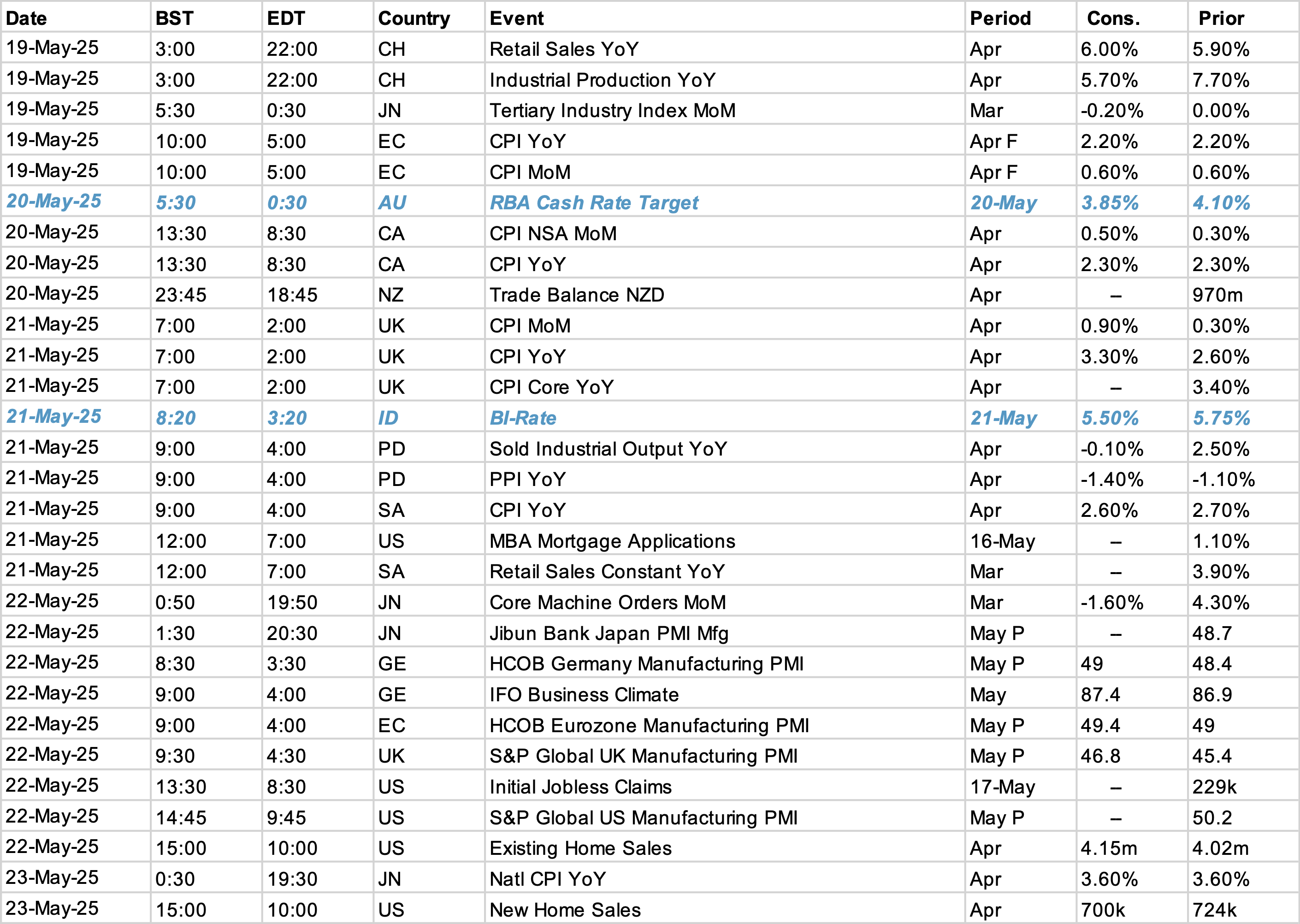

Data Calendar

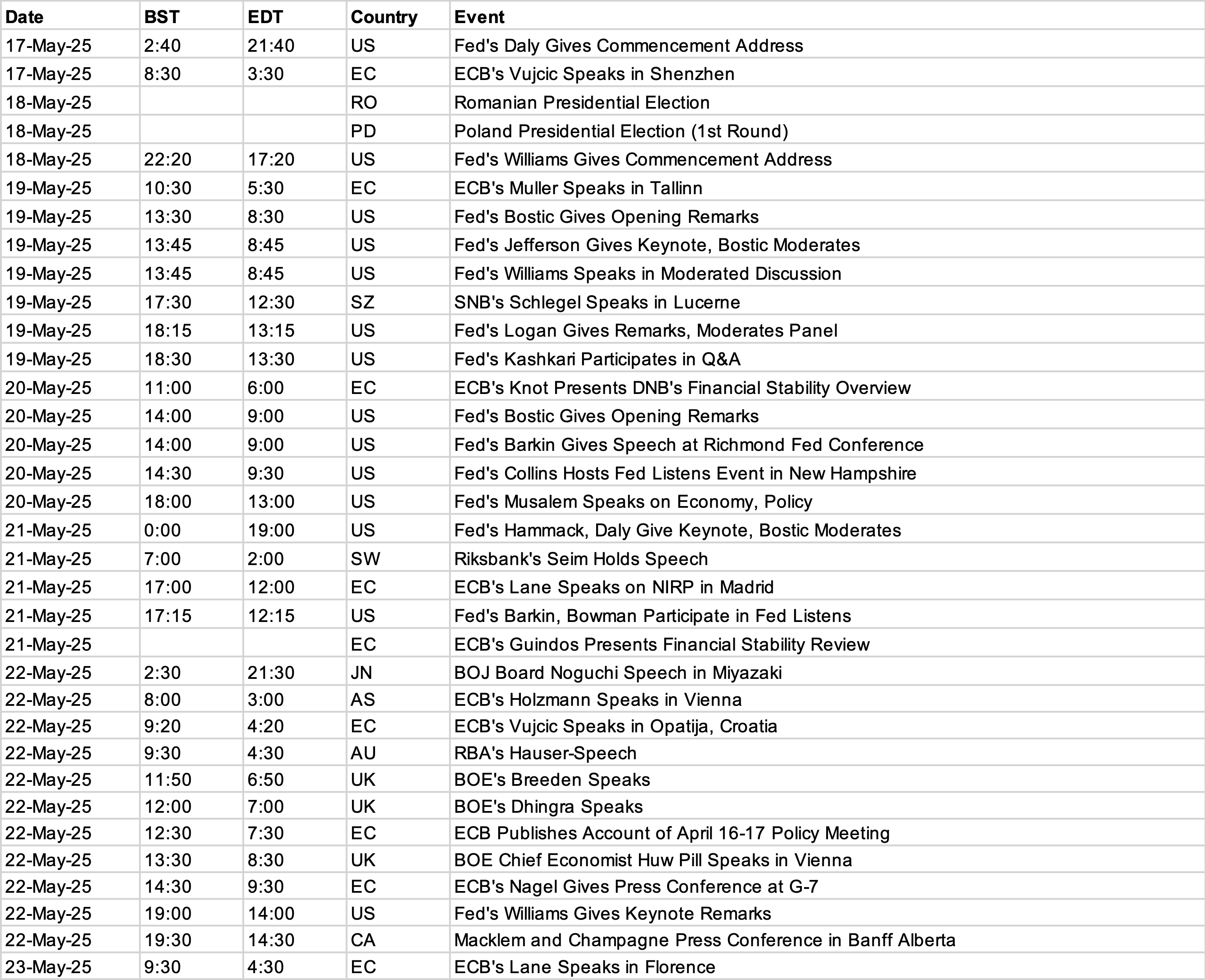

Event Calendar