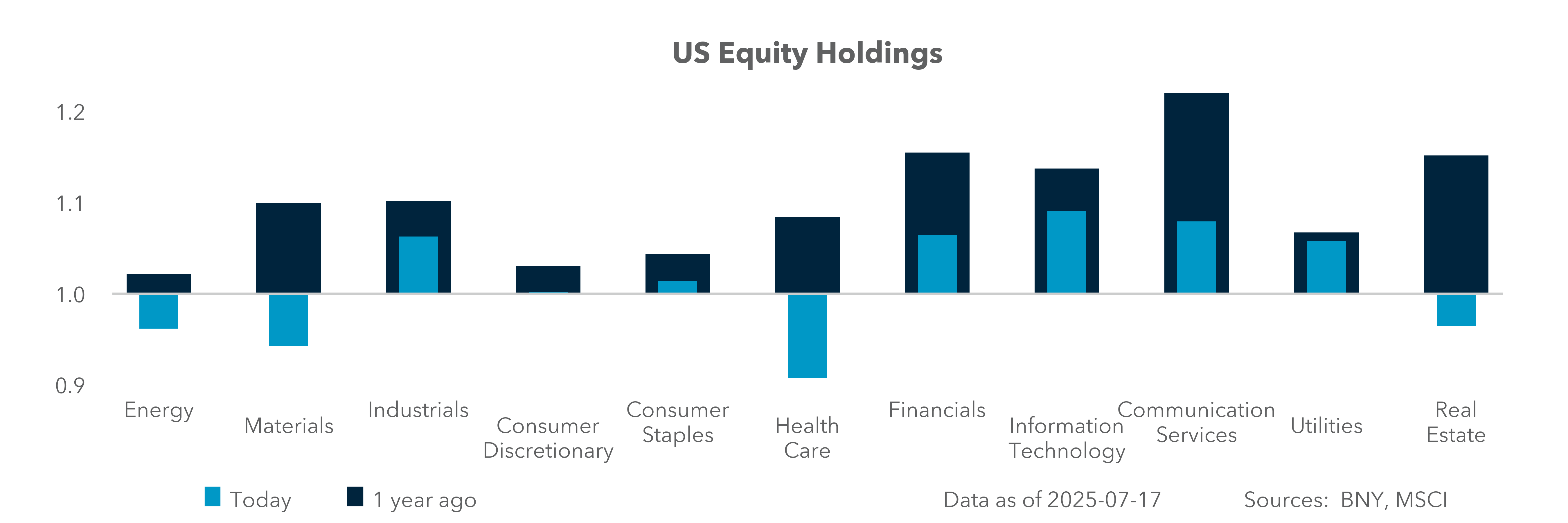

Summer Exhaustion

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 10 minutes

The USD squeeze higher has been supported in the last week by better US economic data instead of facing tariff-linked stagflation. We saw better retail sales, better-than-expected CPI and PPI, and lower jobless claims. The FOMC still faces pressure to ease, but markets have shifted to an October cut, giving up on July and September. The USD bid remains but it’s hardly running given the worries about Fed independence and credibility. The FX carry trade has peaked in our iFlow index and emerging markets are seeing equity inflows but less FX interest. Bank earnings beat but were seen as exaggerated by Q2 trading revenues – viewed as a one-off volatility event, and making next week’s earnings key for sustaining the IT sector with its own spin on AI and revenues goosed by a weaker USD in Q2. The new narrative that Trump is winning the trade war – with more revenue and less inflation – and consequently risk-on sentiment dissipates much of the summer doldrums and the wait-and-see attitude. The next logical risk is for investors to return to momentum and fear of missing out on trading. But this will require more earnings and more data, and the next week isn’t going to suffice. Instead, we will likely see the summer exhaustion trade, with investors holding tail-risk protections that lose value, even with higher volatility moves across asset classes caused by ongoing fear. The last week proves this point given the actual trading volumes and ranges.

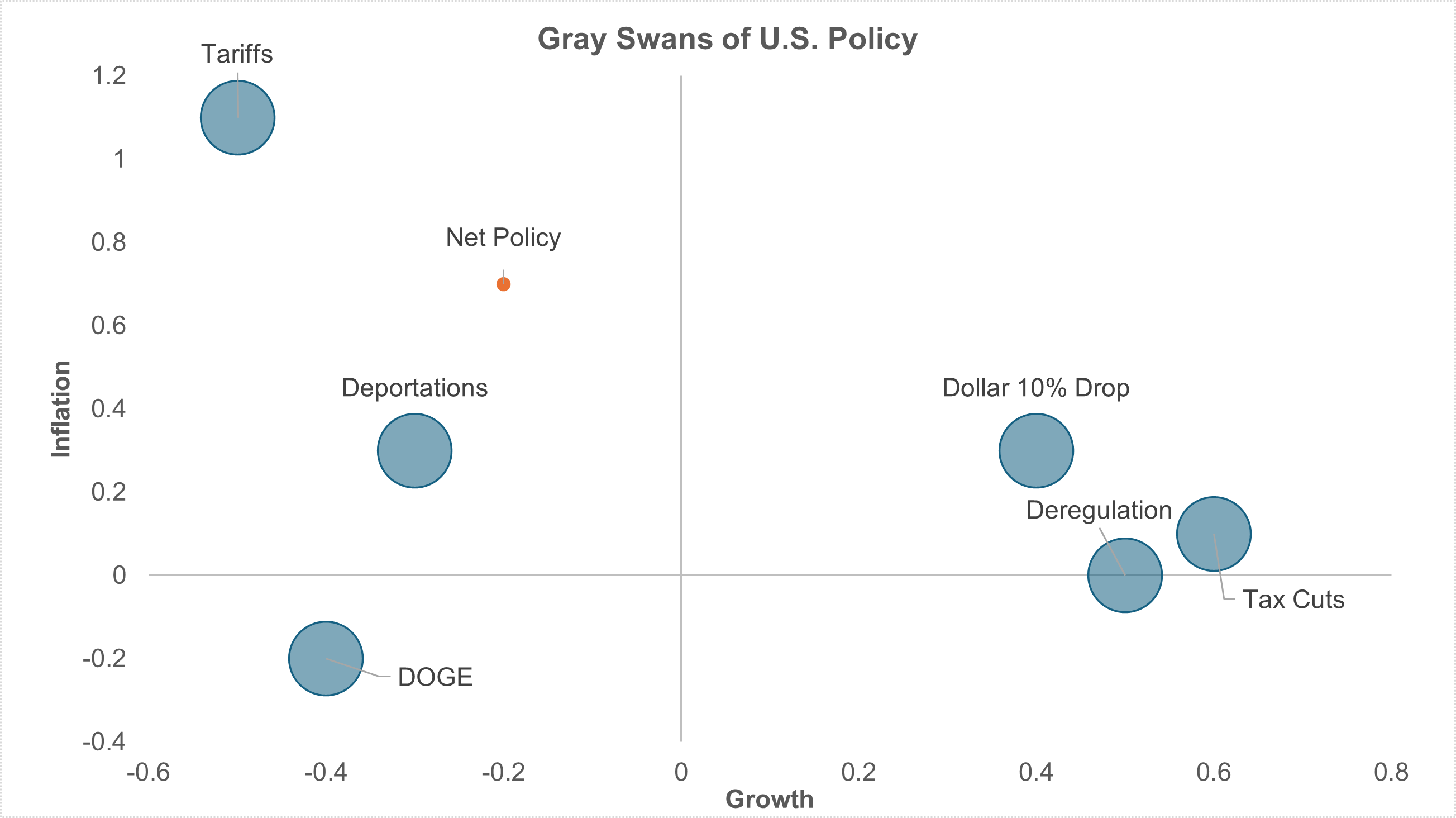

The policy uncertainty of Q2 is changing from black swans to gray ones

EXHIBIT #1: TRUMP POLICY SHIFTS AND THE FORECASTED EFFECTS ON GROWTH VS. INFLATION

Source: BNY, CBO, Tax Foundation, Yale Budget Lab

Our take: The focus for U.S. markets will be on Q2 earnings and durable goods in the week ahead along with expected trade deals with India and other countries. Last week saw better earnings results, but many were discounted as unsustainable. The micro doubts add to the macro analysis. The GDPnow forecast of GDP growth is still over 2% for Q2, but there are doubts about whether this will continue into Q3 given the current labor market standoff, with CEOs reluctant to hire or fire employees. This makes any exogenous shock likely to tip the scale into action. This also makes for a summer of high alerts with exhaustion setting in on those watching price action across assets. The biggest set of known unknowns in 2025 – Trump policy shifts – is becoming clearer, and analysts have pointed to this clarity as helping to put money to work. The same chart three months ago had a smile potential for U.S. growth into 2026, as there was still a narrative that the order of policy shifts from the new administration mattered and pain now would deliver growth later. There is clarity regarding the size and scope of change, but the power of the delivery order has proven less certain even as the numbers around the actual effects of each policy become forecastable. The final bit of noise affecting policy forecast precision comes from tariffs, with August 1 seen as proving out the key hope behind risk – namely that that deadline is not real, that all threats for higher than 10–15% tariffs are negotiation tactics and that the tariff hit to growth and inflation will be moderated from current expectations.

Forward look: We have moved from black swans to gray for risk – and that isn’t sufficient to put money to work in a meaningful way. The net policy forecasts – from a significant set of economic consultants – still suggest slower growth and higher inflation, despite the current positive sentiment. The ability of the Fed to see through tariff noise and cut rates remains a key part of the risk sentiment ahead. Investors are wary of leaning on lower rates to help justify higher valuations, and that adds to the pressure in the week ahead, which has earnings as the mainstay for data watchers. Negative surprises will continue to be punished, while beats remain expected, as we noted in our Equities analysis on Friday.

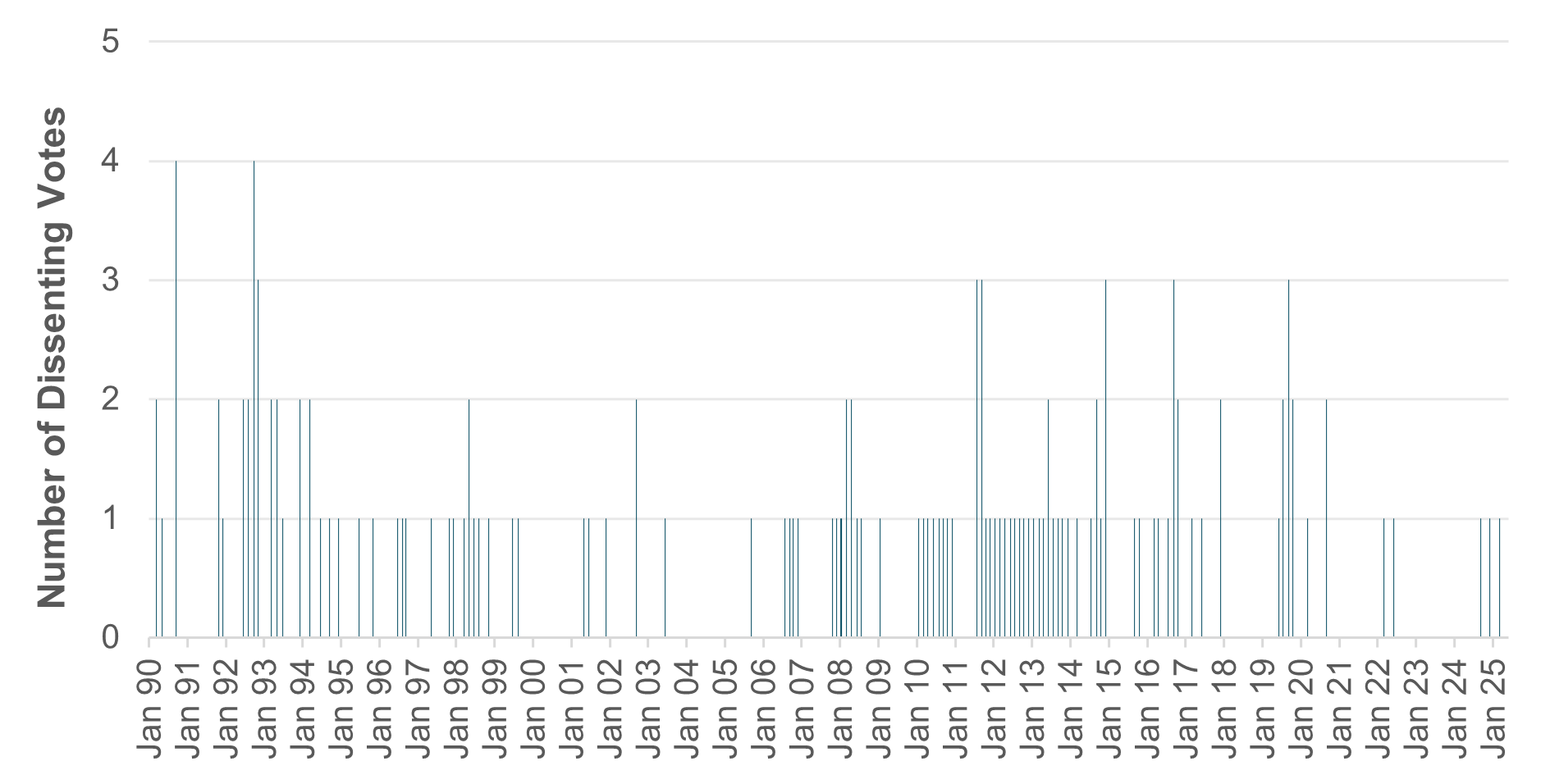

U.S. speculation and the Fed blackout

EXHIBIT #2: DISSENTING FOMC VOTES

Source: BNY, Bloomberg, Federal Reserve

Our take: Last week provided plenty of data on the U.S. economy, and the general message – on the surface, at least – was that the economy is moving along well, so far impervious to tariff effects and other shocks. However, under the hood, we do detect a few signs worth watching. Employment growth in the private sector is slowing, and from the CPI and PPI prints we see goods prices beginning to rise.

This week, we don’t have nearly as many formally scheduled events, although policy shocks and their announcements are an ever-present risk. We’ll get a slew of regional PMIs, which should show some improvement over recent months as threatened tariff rates have waxed and waned, and business sentiment along with it. We get a read on durable goods orders at the end of the week, too.

Forward look: With Fedspeakers on blackout this week in anticipation of the July 30 FOMC meeting, we won’t have any surprises like the one Governor Christopher Waller sprung on markets last week. He made the case for a July rate cut and suggested he might dissent to make his point on the record. If this were to happen, it wouldn’t be unprecedented compared to recent decades. Since 1990, there have been 106 FOMC meetings (out of a total of 291) with a dissenting vote, in some cases more than one. Altogether, 145 dissenting votes have been cast in the previous 35 years.

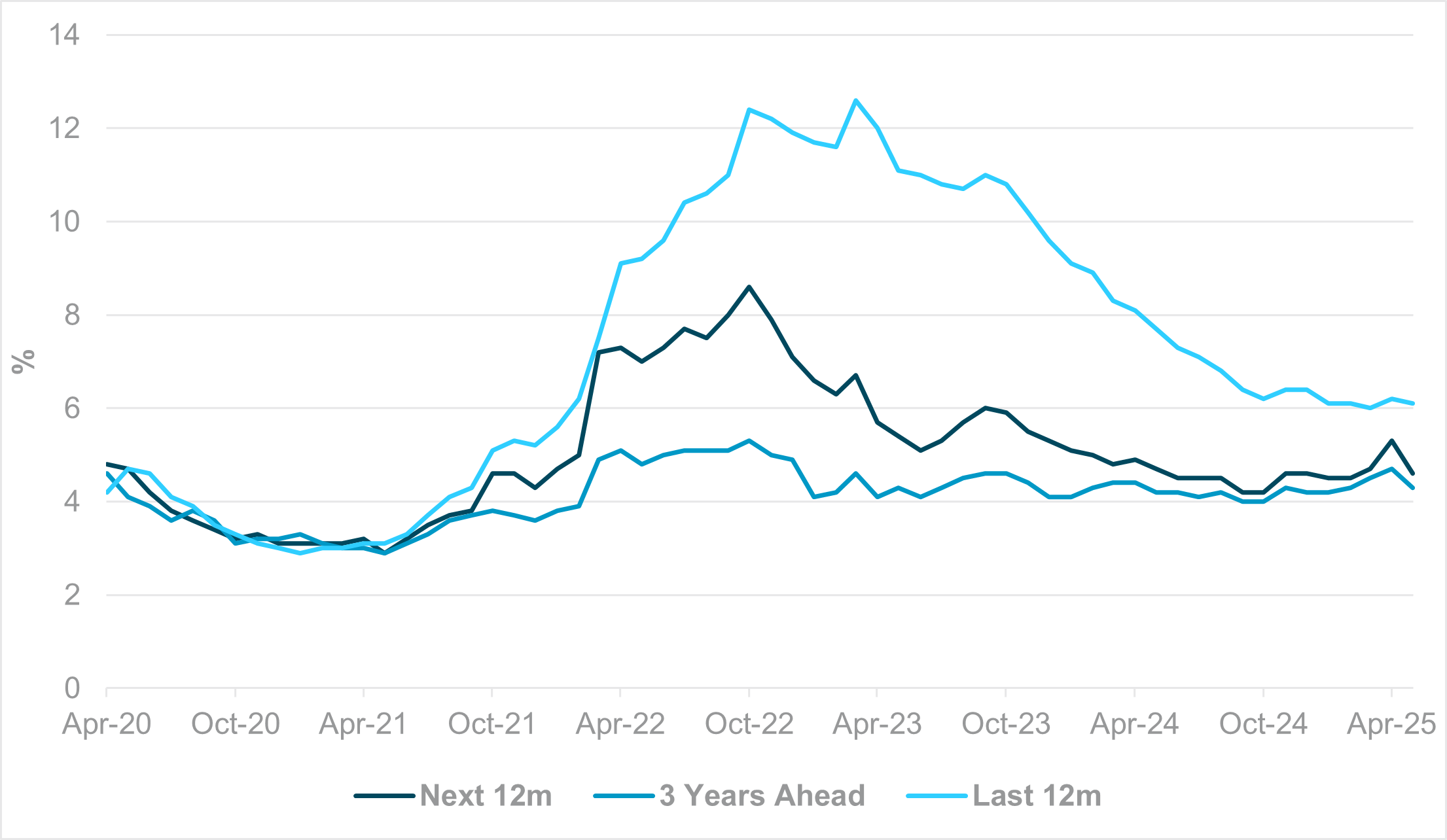

EMEA: Back to April for the ECB, back to Beijing for von der Leyen

EXHIBIT #3: ECB QUARTERLY HOUSEHOLD INLFLATION EXPECTATIONS SURVEY

Source: BNY

Our take: We agree the ECB will likely keep rates on hold this week, but the subtle shift in language by Governing Council members throughout July on the prospect of future cuts all but confirms that the easing cycle is not complete. The bottom line is that with the softening in headline inflation in Germany and tariff risks looming large, the ECB can ill afford to pre-commit. As Bundesbank President Nagel stated, a “steady hand” is needed but it would be better to reassess in September. We broadly agree with this view as there will be greater clarity on tariffs at that point, and households would have had time to react accordingly. In many respects, the ECB is back to its April position during which significant volatility surrounding the growth and trade outlook required strong vigilance. At the time, like many peers, the ECB viewed the aggregate risk to prices from tariffs as skewed to the downside. However, this is not how households have reacted – the ECB’s own household inflation expectations survey clearly showed a jump in forward inflation (both 12 months and three years ahead) in April, before broadly normalizing in May as most tariffs were suspended. Given that the EUR was already rallying in March and surged further in April, the household reaction function clearly pointed to the risk of another supply shock which would impact prices, especially if the EU decided to retaliate. This means that no firm decision can be made before tariffs are finalized and the ECB can discern whether inflation expectations have been anchored. It is also evident that outright levels of inflation expectations have settled well above pre-pandemic levels, and this also mandates higher neutral rates.

Forward look: The German Ifo survey next week is expected to rise to near highs on the year despite tariff risk, supporting the current gap between hard data and soft data. Even amongst corporates, there hasn’t been excessive concern over euro strength, but current ECB rhetoric on the currency is also resembling President Lagarde’s April affirmation that “an appreciation of the euro could put downward pressure on inflation.” Even so, there is very little room for maneuvering. The June staff projections have the euro technical assumption at 1.11 for EURUSD and 1.13 for the next two years. Hence, if the market continues to hold at 1.15 or higher, then the risk to inflation will remain to the downside and possibly exacerbated by the trade situation as any final settlement with the U.S. will have a demand impact on some of the Eurozone’s highest value-added sectors. Consequently, if the ECB is able to guide the euro lower with rhetoric without resorting to more assertive easing, that would be desirable, but it will depend on the inflation outcomes. Our data indicate that cross-border investors are already picking up on such risks and hedging of Eurozone assets has picked up again, though current hedging levels remain at half the lows seen at the end of 2024.

On the broader matter of trade, we also note that EU President Ursula von der Leyen and European Council President Antonio Costa are scheduled to meet with Chinese leaders, including President Xi Jinping or Premier Li Qiang, in Beijing on July 24. We had anticipated closer relations between the two sides in the face of trade tensions with the U.S. for both, but recent developments leave much to be desired as the EU steps up scrutiny over China’s industrial policy and trade redirection to the European Union. Talks regarding a new tariff/minimum-pricing regime for Chinese new energy vehicles (NEVs) have stalled and our data indicate that the European equity sectors which hitherto had the most to gain from Chinese demand – automobiles and luxury goods – continue to struggle. A “reset” is not entirely needed but pragmatism is – especially for the EU, which risks being squeezed on trade by both China and the U.S.

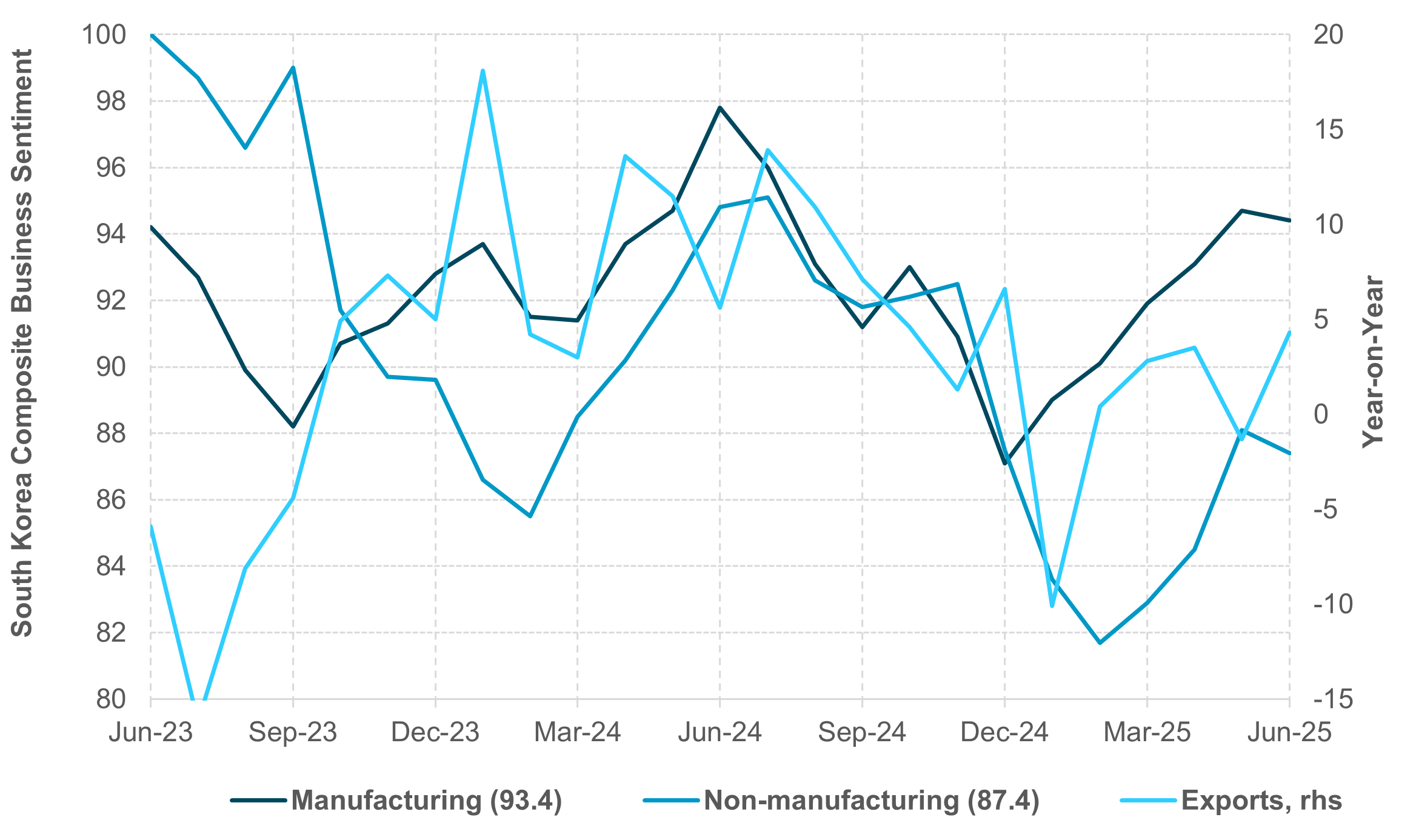

APAC: Japan election, trade talks and economic data lead the week ahead

EXHIBIT #4: S. KOREA BUSINESS SENTIMENT IMPROVES WITH EXPORT RECOVERY

Source: BNY

Our take: In the Asia-Pacific region, the focus this week will be on the aftermath of this weekend’s upper house election in Japan and a heavy data week in South Korea, including Q2 GDP, the composite business survey index outlook, consumer confidence and the first 20 days of export growth. China will release its monthly 1-year and 5-year loan prime rates, which are expected to be unchanged at 3.0% and 3.5%, respectively. But the focus will be on the follow-up to the Central Urban Work Conference last week, which targeted an acceleration of a “new model” for property development and advocated a more measured approach to urban planning and upgrades. Investors will be watching inflation releases from Malaysia, Singapore, New Zealand and Japan, as well as export data from Taiwan, Thailand and New Zealand.

Political uncertainty and instability will be an increasing focus in Japan. Losing its majority in the upper house election would present further challenges for the ruling LDP-Komeito coalition, threatening to destabilize economic policy and push up government spending. The LDP-Komeito lost its majority in the lower house for the first time in 15 years in the general elections in 2024. Tariffs and domestic politics and fiscal uncertainty have exerted significant bear steepening pressure in the Japanese bond market.

The South Korea composite business sentiment index (BSI) has recovered from its lows at the end of 2024, but it remains below the 100 neutral level. At 93.4 and 87.4, respectively, the manufacturing and non-manufacturing indexes are both below their five-year averages of 97.2 and 98.6, which they achieved from 2015 to 2019. Further upside momentum is expected, with a rebound in export growth supported by a combination of monetary easing and expansionary fiscal stimulus.

Singapore’s June inflation will be closely watched given its relevance for the policy decision by the Monetary Authority of Singapore (MAS). We expect MAS to maintain the status quo on its Singapore dollar nominal effective exchanged rate (S$NEER) policy band but to slow SGD appreciation via lower front-end interest rates at its forthcoming policy meeting. Elsewhere, Japan’s July Tokyo CPI and July PMI will be scrutinized on the Bank of Japan tightening expectations. Japan’s PMI saw an expansionary reading (a PMI >50) for the first time since June 2024.

Elsewhere, the July PMI from Australia and India will likely show ongoing strength in business sentiment.

Forward look: Over the last month, APAC FX have traded well, benefiting from a weaker U.S. dollar despite neutral to slightly worsening domestic macro fundamentals. In other words, APAC FX valuation is now expensive given the region’s policy easing cycle as well as the aggressive fiscal push, especially in China, South Korea, Indonesia and Thailand. The tariffs deal between the U.S. and Indonesia (19% tariffs on U.S. imports from Indonesia) and the anticipation of other trade deals in the region are positive for sentiment. That said, the positive impact on the foreign exchange complex might be limited. Japan’s election may be a catalyst for change, particularly with USDJPY at 150 viewed by the market as a trigger for Japan MOF intervention risks and BoJ anxiety over weaker FX effects on policy. As we noted, the reaction of IDR to the trade deal was muted, while Indonesian equities were nearly 4% higher on the week. In other words, the near-term evolution of APAC FX is, in our view, heavily dependent on the U.S. dollar, with a potential upside dollar squeeze in the summer trading session ahead.

While many would like to see next week as another quiet, light summer trading week, the risks tilt toward more noise if not clear signals for changing positioning. The net effect should show up across markets as investors look more exhausted than refreshed from summer trading. There are three key points for the week ahead:

Robust U.S. retail, CPI, PPI and claims lift DXY and push the first expected Fed cut to October, yet USD upside is capped by worries over Fed independence as the FOMC enters blackout with dissent risk alive.

Bank earnings beats deemed a one-off volatility windfall; spotlight shifts to GOOG, TSLA and INTC, where tech results must shine to sustain momentum and stave off summer FOMO amid fading carry appetite.

Gray swan mix – August 1 tariff cliff, Japan election eyeing a breach of 150 for USDJPY, and an ECB hold with EURUSD near 1.15 – meets a peaked iFlow carry index; tail-risk hedges erode, hinting at a USD squeeze in thin trade.

Mixing it all together, we should be in for more volatility, with the risk of the U.S. dollar testing a wider range for the EUR of between 1.1450 and 1.17, JPY testing 145–150, U.S. 10-year bonds ranging from 4.25–4.55%, and the S&P 500 reaching for 6,225–6,375. The micro bottom’s up information flows from earnings clashes with the ongoing macro speculation for policy changes whether monetary or fiscal.

Central bank decisions

Hungary, MNB (Tuesday) – The MNB is expected to remain on hold at 6.50%, keeping the HUF’s high-carry status. Headline inflation accelerated to 4.6 % year-on-year in June – remaining above the 2–4 % tolerance band – and monthly prices rose 0.1 %. Deputy Governor Kurali has ruled out rate cuts until disinflation toward the 3% target is clearly entrenched, citing persistent inflation expectations and effective monetary transmission via a stable forint. Government-imposed price controls and deferred fee increases risk reigniting inflation pressures when lifted. With GDP growth forecast to remain subdued through 2025, markets anticipate the Council will pause rather than adjust rates, focusing on updated inflation projections and any tweaks to reserve management. The Council’s post-meeting communiqué and published minutes will be closely scrutinized for any hints of eventual policy easing or adjustments to reserve management strategy.

Turkey, TCMB (Thursday) – The Central Bank of the Republic of Türkiye is expected to cut the 1-week repo rate by 250 basis points to 43.50 %, resuming its cautious easing cycle after 18 months of tightening, whereby the original cycle was also cut short due to Q2 market stress. Annual inflation slowed to 35.05 % in June, helped by softer food prices, while monthly CPI slipped marginally. With market volatility easing and disinflation on track, markets foresee further rate reductions toward year-end, contingent on stable inflation expectations and external risks. Some additional guidance on the medium-term path and any tweaks to unconventional liquidity measures is also expected.

Eurozone, ECB (Thursday) – The European Central Bank is expected to keep rates on hold at 2.0% but we expect the door to additional easing will be opened again. This is quite a turnaround after the last decision and multiple statements at Sintra signaling the end of the cycle. However, downside inflation surprises in Northern Europe and the lack of certainty over tariffs and trade talks means the ECB cannot fully discount downside growth surprises, and the overall price outlook is no longer symmetrical. Commentary since the second week of July have shifted toward a more cautious view, though few Governing Council members advocate an immediate move. Crucially, the EUR’s valuations are a key part of the inflation calculus, and this has been acknowledged more forcefully by officials. We expect language on the currency akin to the April meeting, but any cut will probably come in September at the earliest.

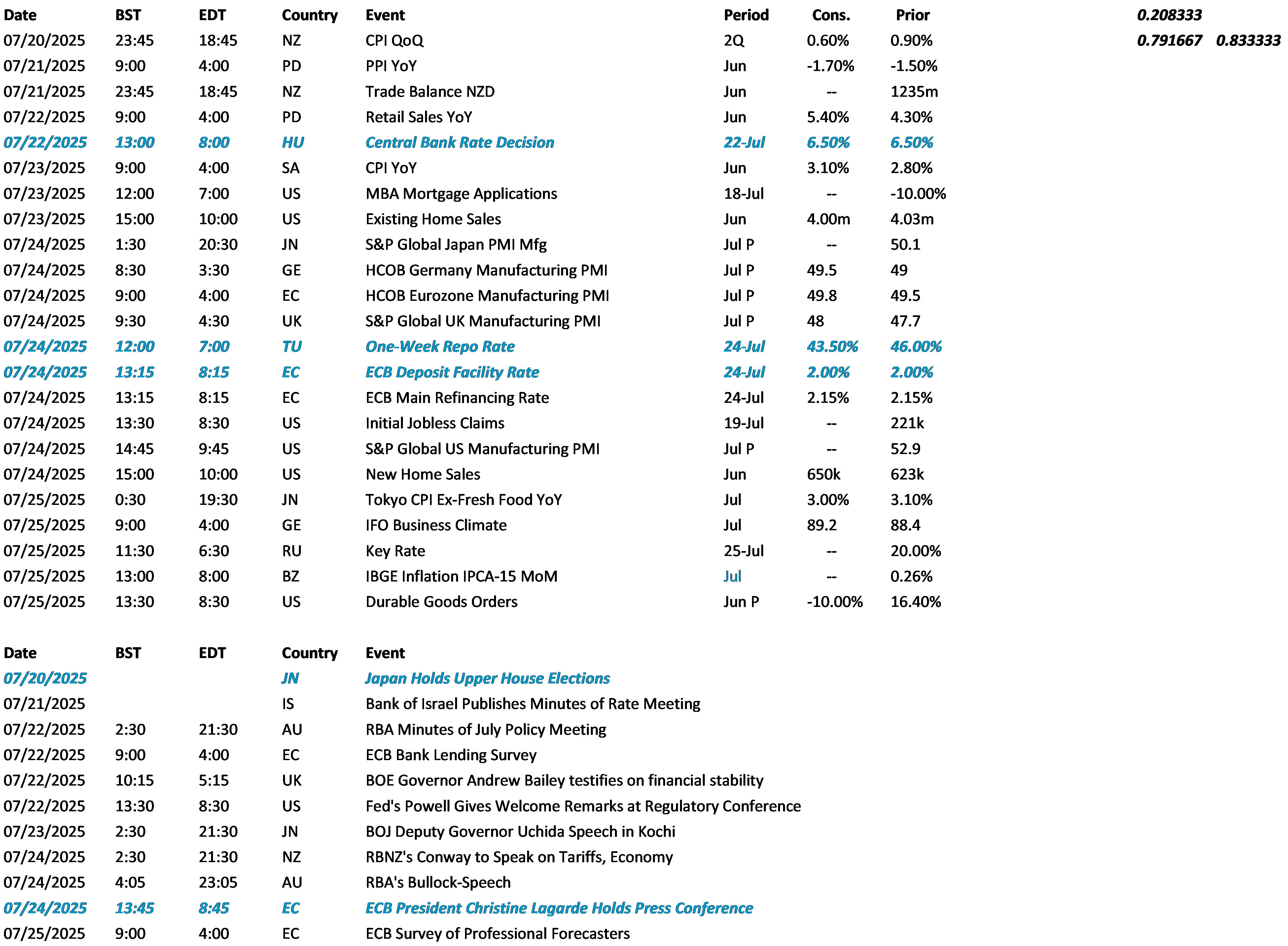

Data Calendar

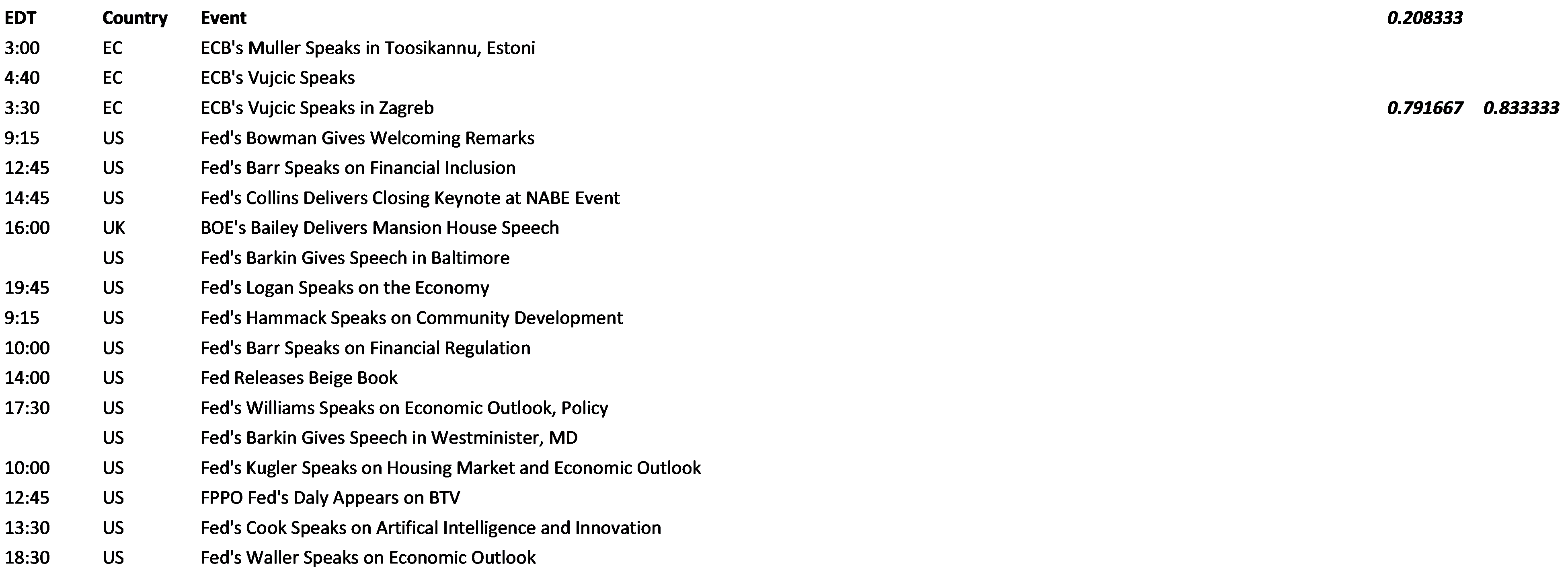

Event Calendar