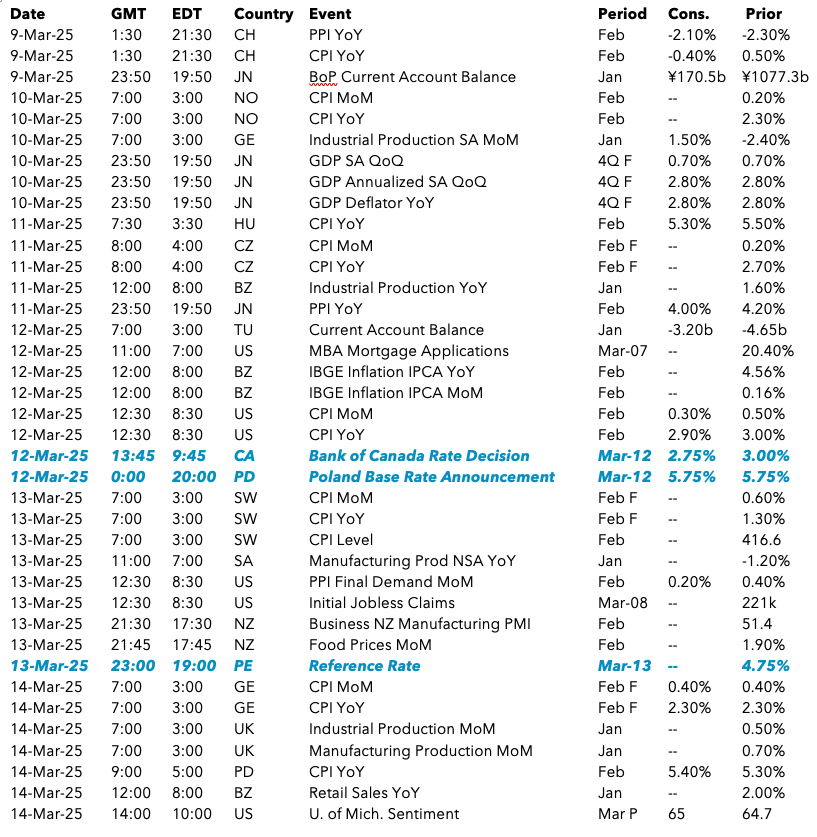

Spring Ahead

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 10 minutes

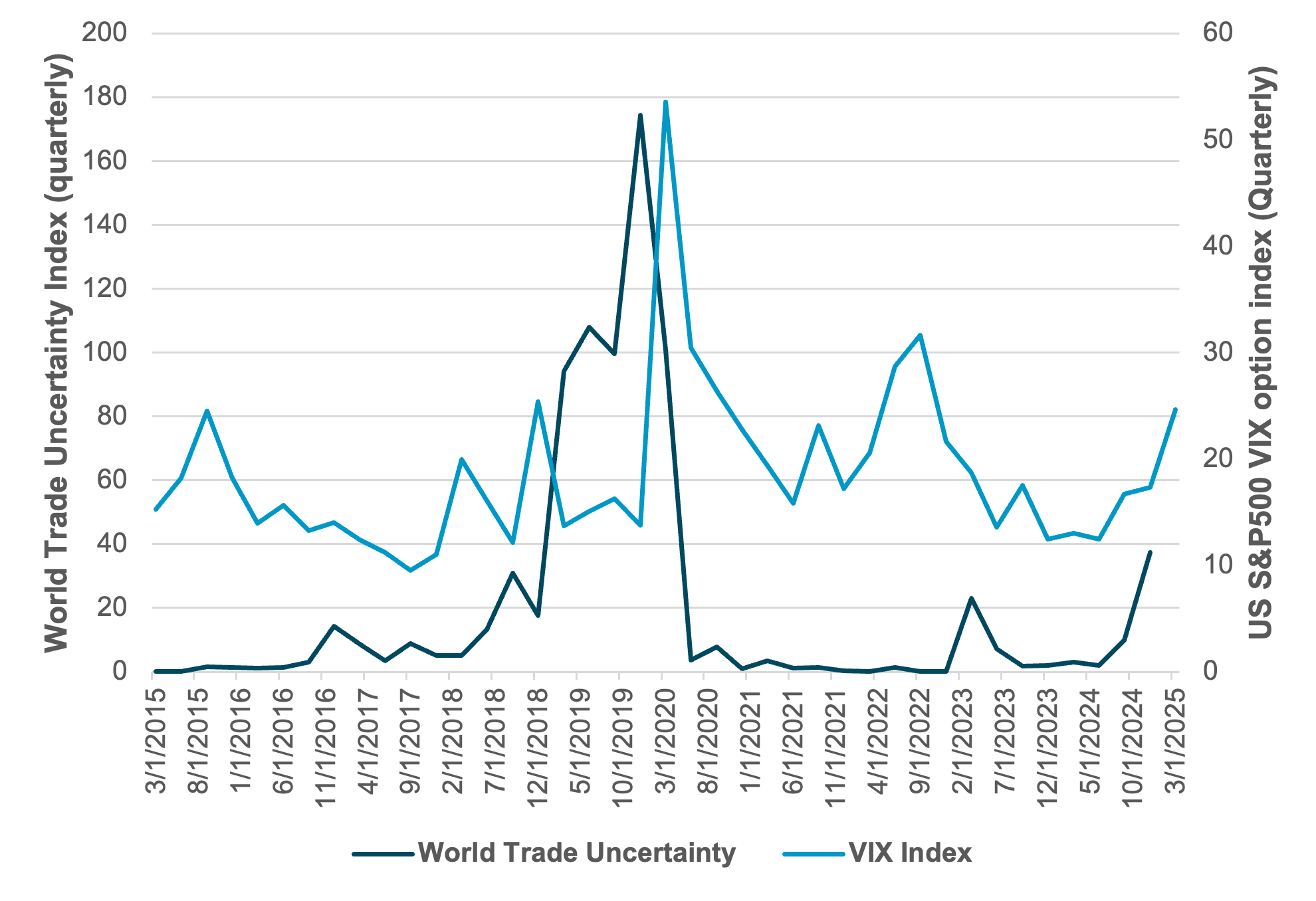

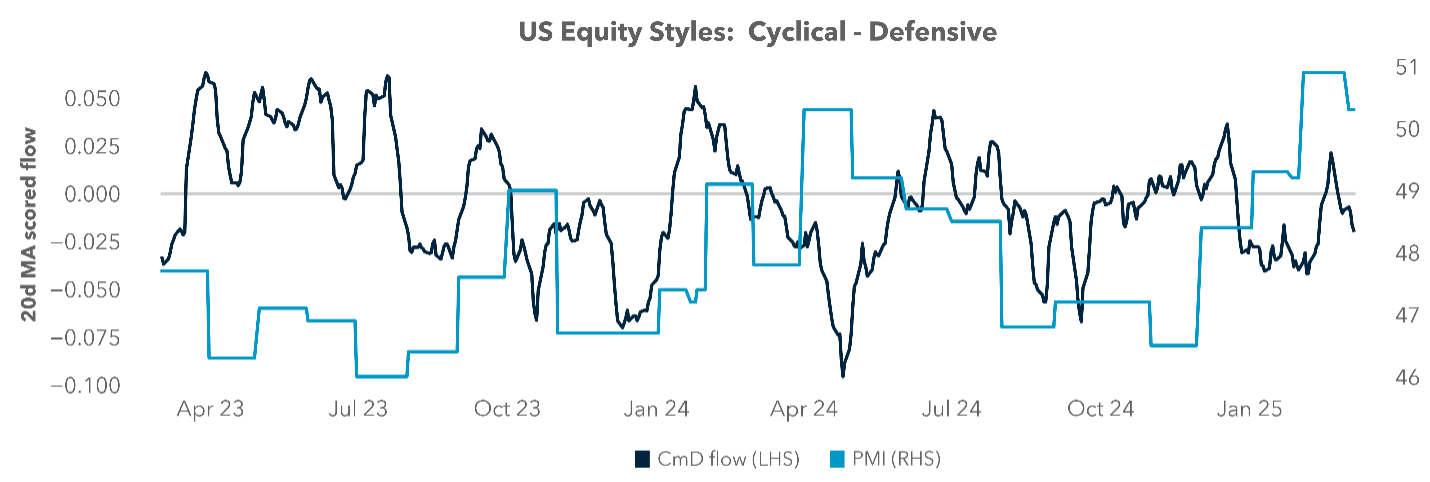

EXHIBIT #1: TRADE UNCERTAINTY AND STOCK MARKET VOLATILITY

Source: Bloomberg, BNY

Uncertainty drives asset price shift from soft to bumpy landing

US growth is set to slow from 2.3% in Q4 2024 to 1.5% in Q1 2025 on trade concerns and lower consumer spending. Political uncertainty predominates with hopes for a Ukraine peace deal and a mixed response to US tariff plans. Investors bought EMEA shares and Chinese tech stocks, while selling US shares. Domestic stocks are mixed, with foreign-facing shares sold. The Nasdaq 100 index fell into correction territory, even as the exchange pushes for 24/5 trading. The S&P 500 fell below its 200-day moving average for the first time since 2023, and USD had its worst week in four months. Growth concerns put talk of a Fed pause at odds with market pricing. Fed rate cut expectations have less impact on stabilizing markets now, with next week priced for an uneasy hold and markets pricing in three cuts in 2025. Yields on 2y and 10y US government bonds fell 6bp and 1 bp, respectively, with EU markets driving rates. Hopes for peace in Ukraine rose as Russia spoke of a truce with conditions, and Europe focuses on defense spending, as German parties agreed to lift the country’s debt brake. This led global bond rates higher as the yield curve steepened.

The focus this week will be on US bonds as fiscal concerns mount with the March 14 deadline for an agreement to avoid a government shutdown approaching. Treasury levels are at $58bn for 3y, $39bn for 10y, and $22bn for 30y bonds, along with $45bn in corporate investment-grade sales. Despite their status as a haven against stocks, bond credit spreads have widened as growth concerns increase. Investors will likely turn their focus to trade discussions with China, Chinese CPI and credit data, EU trade and defense spending and Ukraine. The Bank of Canada and the National Bank of Poland are on divergent paths, with Canada cutting and Poland maintaining a hawkish stance. USD weakness is expected to consolidate rather than accelerate.

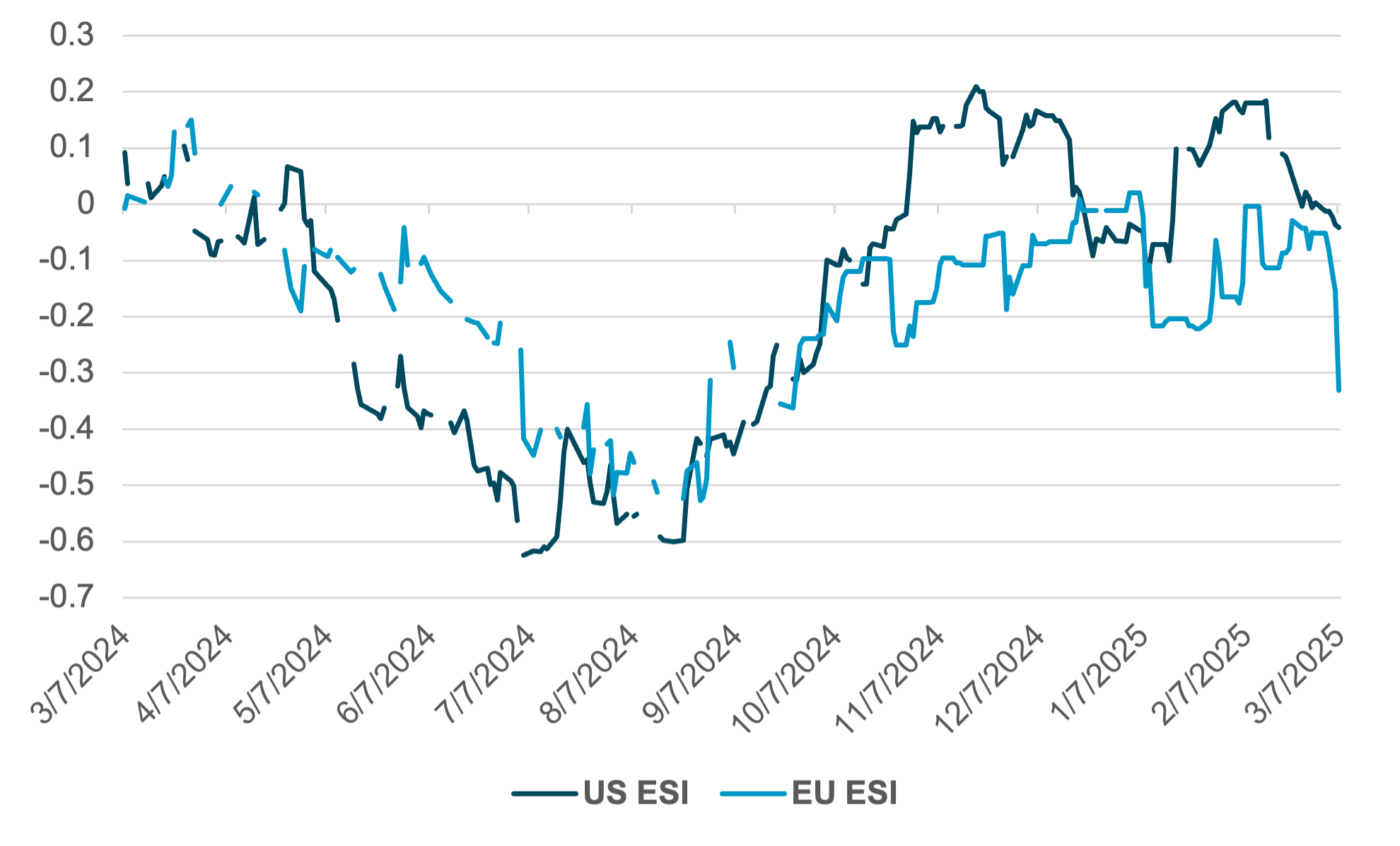

EXHIBIT #2: US VS. EU ECONOMIC SUPRISE

Source: Bloomberg, BNY

US slowdown, EU growth?

There are signs that US growth is expected to slow. The Atlanta Fed’s GDPNow – admittedly an imperfect tool – fell from +3.9% to –2.4%, a move that is hard to ignore. The drag on trade in Q1 is a sign of tariff concerns that have led companies to bring inventories back to the US. Weaker consumer and business surveys in January and February also surprised investors. By contrast, German plans for €500bn in infrastructure spending will boost growth in 2025 and 2026. However, there hasn’t been any spending yet and German factory orders, manufacturing PMI and construction data all still point to a risk of recession.

Our take: These are soft data and may not play out in the same way. Consumer spending in January was lower and may be a fluke of winter weather or could be worse. Trading on US and EU growth spreads now points to the need for Europe to surprise to the upside more than the downside risks for the US.

Forward look: This week’s CPI may be low enough to allow the Fed to continue its dovish tone, leading it to ease rates before June. The mid-March consumer sentiment survey from the University of Michigan could also surprise on lower gas prices and good weather. Upside risks to US data seem underpriced.

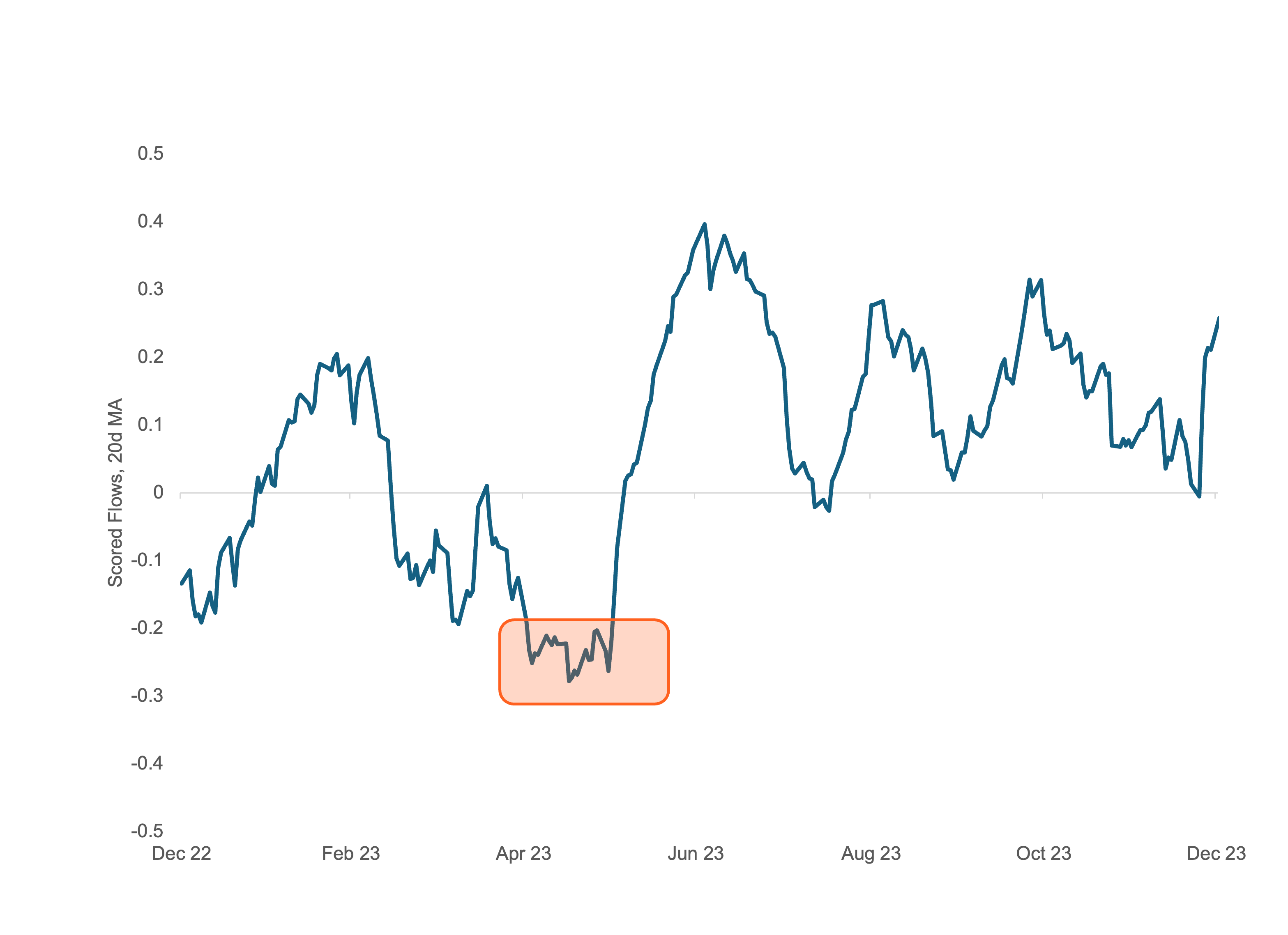

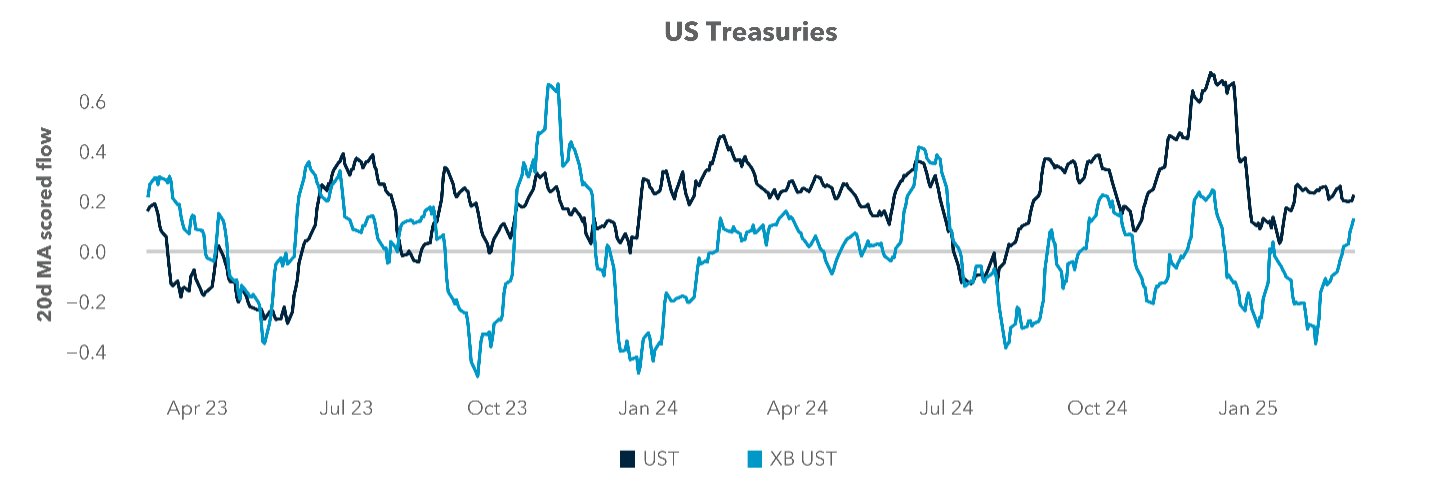

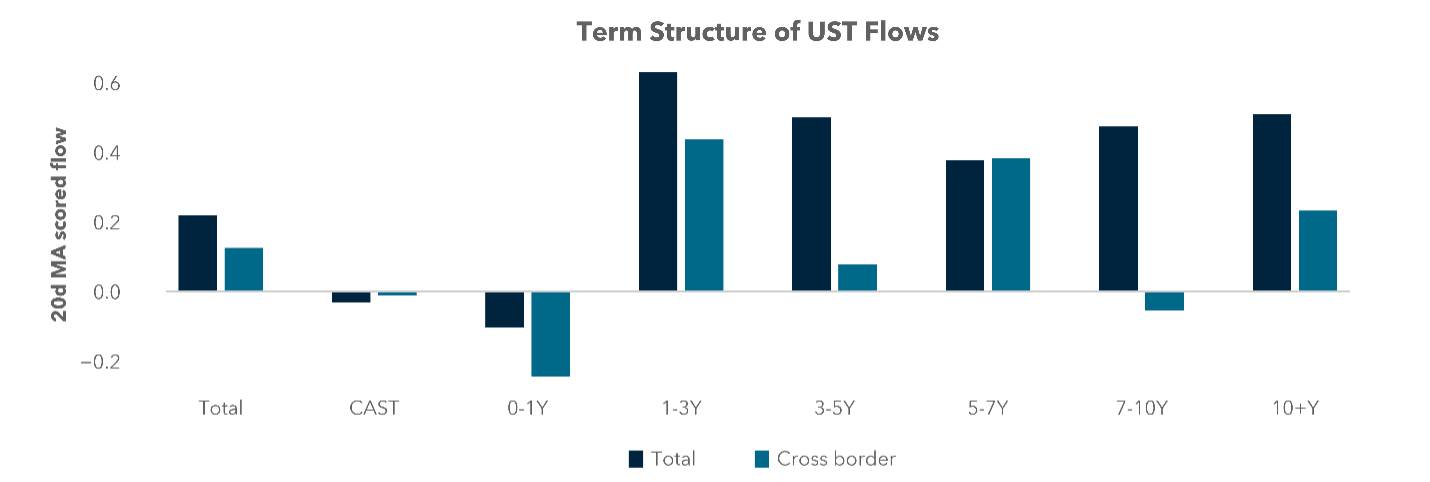

EXHIBIT #3: UST FLOWS DURING 2023 DEBT CEILING EPISODE

Source: BNY iFlow

US and Canada – CPI and BoC

US inflation data for February is a key part of the outlook. Last week’s volatile sessions were somewhat tamed by Friday’s good job report, which was in line with expectations. Monday’s JOLTS data will provide valuable information about the impact of DOGE job cuts and the general job market picture.

Wednesday’s consumer price data is expected to show that prices rose less than the prior month, when there were upside surprises to both CPI and PPI data. An inline print will support increasing expectations of further Fed rate cuts, a view that has been gaining in the markets. Nevertheless, Chair Powell’s final remarks on Friday before the FOMC went on media blackout didn’t indicate any specific concerns over the labor market or downside economic risks.

In the US, the budget process will be a key focus. While both houses of Congress have passed budget resolutions which define key spending and revenue targets, they remain far apart. A budget – even just a stopgap spending plan – must be passed by March 14 to avoid a government shutdown.

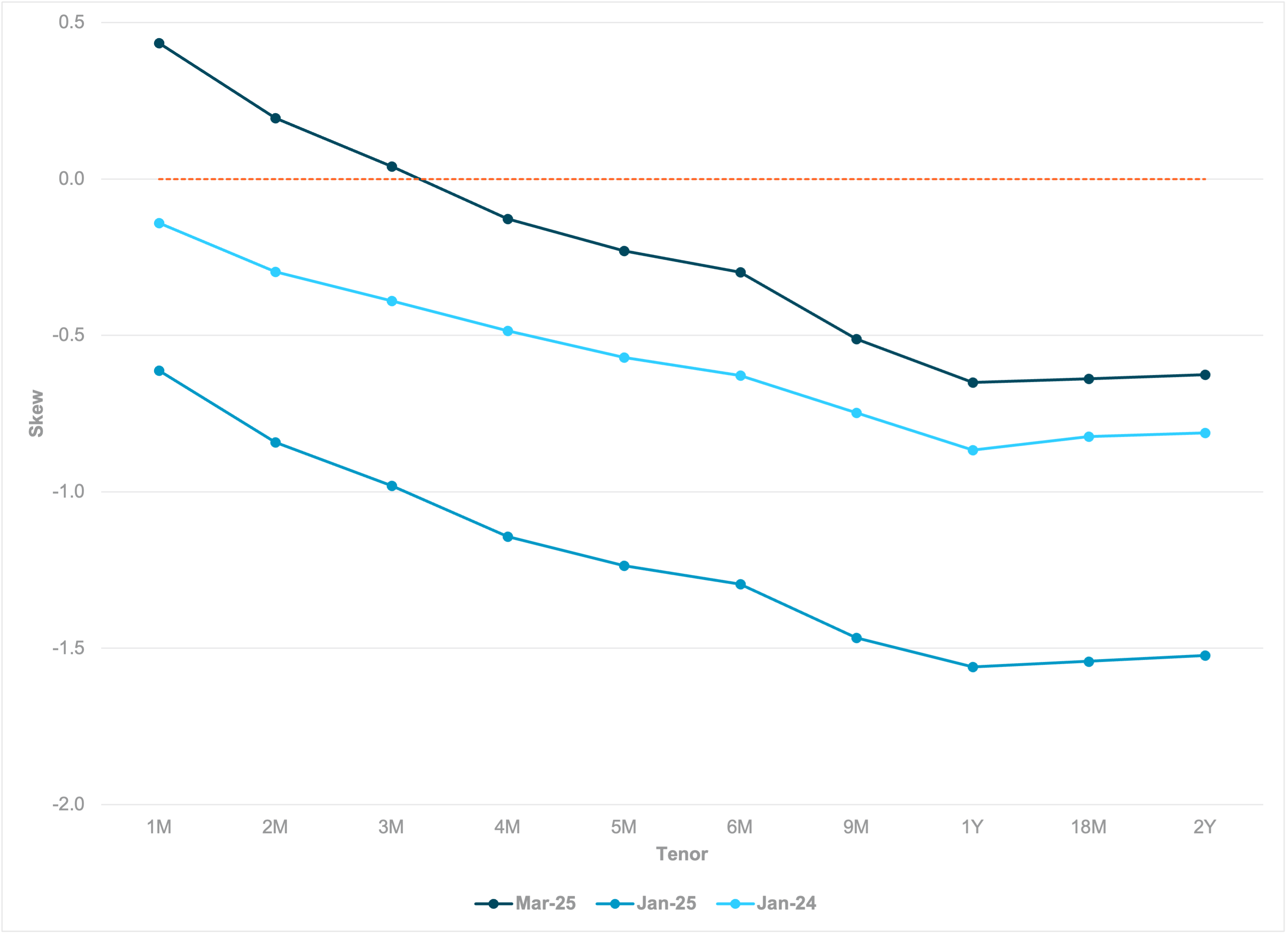

EXHIBIT #4: SHIFT IN EUR SKEW SHOWS MEDIUM TERM DOUBTS ABOUT EUROPE

Source: Bloomberg, BNY

EMEA: EU spending plans, German debate, EUR skew

Political developments will dominate in Europe as national governments and the EU attempt to finalize plans to increase defense spending. For the comprehensive and positive re-pricing of European assets to continue or simply be maintained, firm spending plans need to be clear. The key debate will be on March 13 as the Bundestag begins deliberating the constitutional amendments, with the aim of completing the process by March 18.

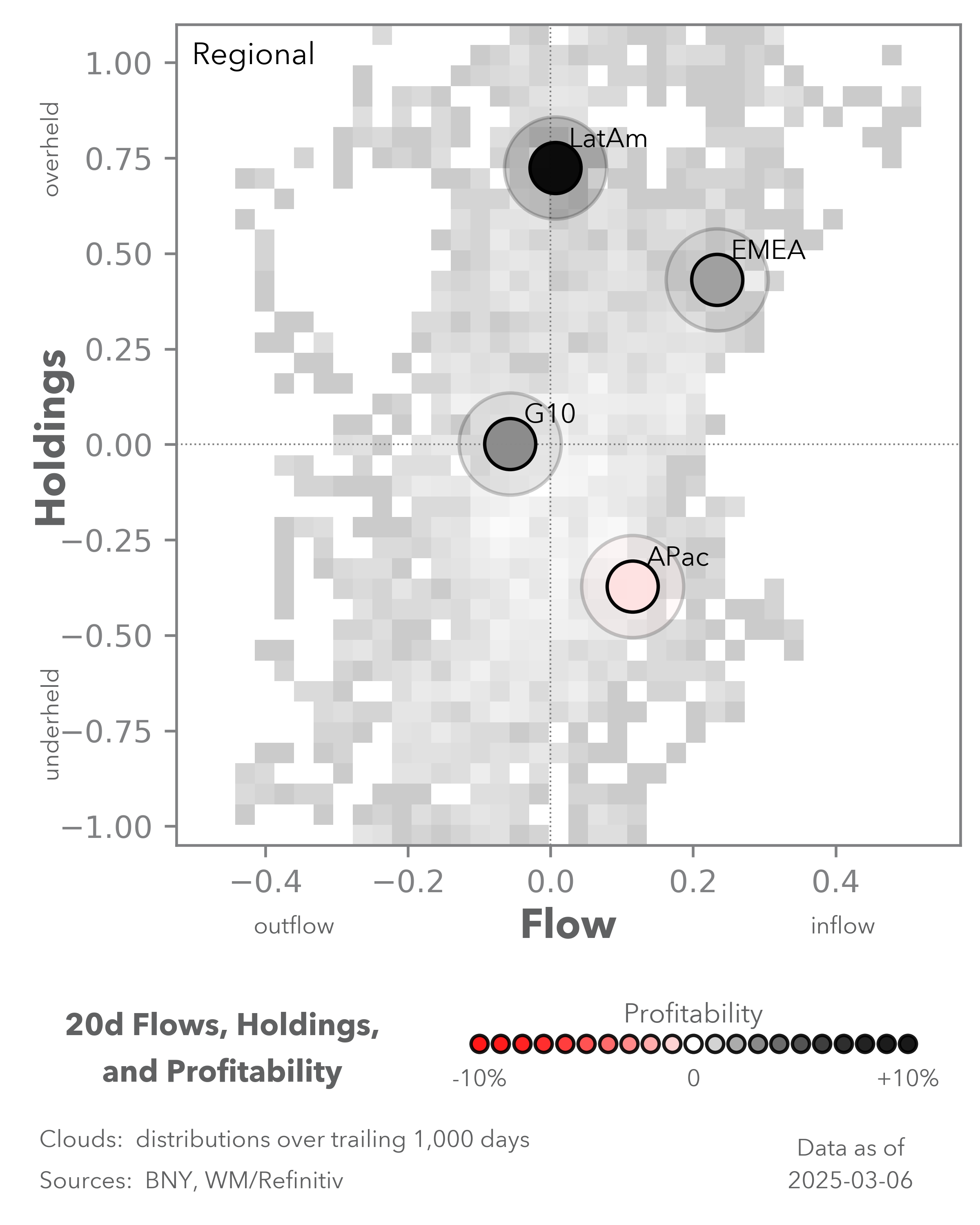

Despite the surge in the EUR we believe there is still much hesitation over the medium- and long-term outlook for Europe and its assets. iFlow indicates that participation in the recent rally by cross-border investors is modest. Even with domestic equities struggling, the reluctance to shed home bias is striking for US investors.

Meanwhile, the broader risk environment has generated sharp swings in volatility across asset classes, with bond markets the latest casualty as the reaction function from European authorities to tap the fiscal went well beyond any expectations. Assuming Germany and the EU manage to push through fiscal reform, there is a stronger case for higher euro equilibrium effective exchange rates (EER). Exhibit #4 above shows how EUR skew has adjusted across the front end and up to a three-month horizon. However, beyond this point markets continue to favor downside risk, even with the term structure now reflecting greater risk premia in the US. While we acknowledge that short-term growth risk for the Eurozone and the Continent means the current rally will run out of steam, there is a regime shift taking place across Europe and FX vols will need to heed the signals from fixed income markets, whose moves last week were generation-defining.

EXHIBIT #5: CHINA CREDIT STABILIZATION FOCUSED ON CNY LOANS

Source: Bloomberg, BNY

APAC: China credit data, CPI, regional equity flows

The key economic data focus in APAC this week will be February’s credit data and the latest inflation releases for China. China credit data will be closely watched. With the announcement of higher fiscal deficit target to 4% of GDP from 3% in 2024, and the increment of other bond issuance plan, there are high expectations that credit growth will stabilize and pick up this year after a fast-paced slowing over the past few years. China January 2025 aggregate financing and loans by financial institutions stood at 8.0% y/y and 7.53% y/y compared with 9.5% y/y and 11% as of December 2023, respectively. Within credit, households medium- and long-term loans will also be closely scrutinized. The latest January 2025 loan figure of CNY 493bn is encouraging. Elsewhere, we will be paying attention of the sustainability of services inflation, which has been on an upward trend from 0.2% lows in September 2024 to 1.1% as of January 2025.

Foreign investors flow into APAC equities, except for China, has been on the sell side, brushing aside the recent improving of market sentiment. According to official statistics, foreign investors net sold $15bn, $8.9bn and $4.1bn year-to-date of India, Taiwan and South Korean equities year against southbound stock connect net inflows of HKD302bn year-to-date as of first week of March 2025 compared with HKD 68bn ytd in equivalent period in 2024.

Traders in 2025 look dazed and confused. We turn clocks ahead this week in US markets, but we all still wish for 2024 volatility. The rise of uncertainty should not be a surprise, but its effect has been to lower market risk appetite. VAR shocks in stocks have caught up to FX markets. Global forces from political change last year are playing out now. The risk and reward for investors remain finely balanced but we see the upside more clearly now with corrections in US exceptionalism not derailing recoveries in Asia or Europe. The ongoing supportive policy from central bankers helps just as the newfound fiscal fervor in China and Germany. While the Trump 1.0 playbook of understanding US policy isn’t working, the new Trump 2.0 version has made clear risk across all markets is here to stay and can’t be ignored.

Central bank decisions

Canada BoC (Wednesday, March 12) – We expect the Bank of Canada to enact another 25bp rate cut on Wednesday. Friday’s jobs report was weak – although possibly affected by weather during the month, and more importantly, as Canada stares down increasing tariff risk, this cut would be a preemptive move aimed at supporting the economy.

Poland NBP (Wednesday, March 12) – No change is expected in the NBP’s outlook for now but if the recent moves in Germany and broader European Union are anything to go by, the fiscal pressures leading to more restrictive NBP rates are only just beginning. Prime Minister Tusk has already called for immediate increases in defense spending to 3% of GDP and practically, much of the defense lift across Europe will be implemented in the CEE region. iFlow is tracking heavy inflows into various PLN assets but re-rating is taking place, and this will drive up neutral rate levels.

Peru BCRP (Thursday, March 13) – Given the current risks in the Americas regarding tariffs, BCRP will probably acknowledge that the need to maintain relatively high real rates is a necessity. The performance of BRL of late is a good example, while we have tracked good inflows into Americas frontier bond markets. At 4.75%, BCRP’s nominal rate buffer is not as comfortable compared to peers so additional vigilance is necessary through various aspects of financial conditions. However, with inflation now running well below 2% annualized (though slightly higher on a sequential basis), policy settings are adequate for now.

Source: BNY

Source: BNY