Refilling the Punchbowl

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 12 minutes

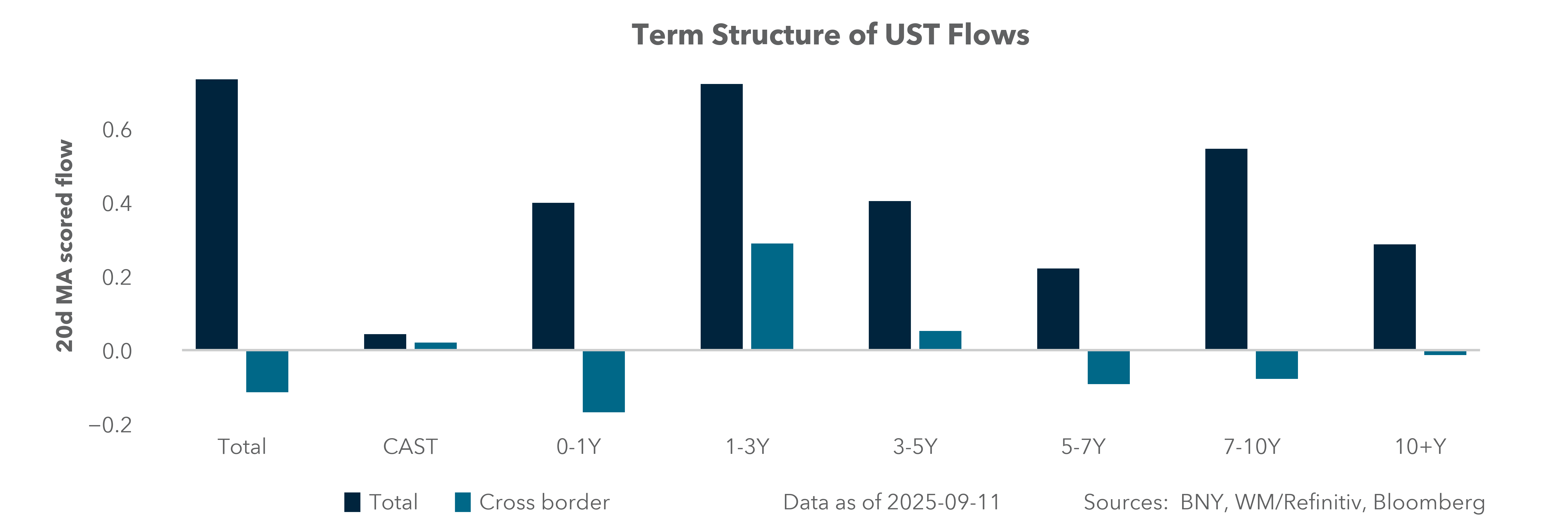

The big question this week is whether the Fed will cut rates. The case for easing is supported by job market weakness, while the case for holding rates steady is based on financial conditions and sticky inflation. For investors, the risk is that the Fed will ease as the economy appears to be running over capacity, albeit at a slower pace, and what this means for the consumer and corporate profits. Equity and bond markets are torn between concerns about stagflation and stagnation. More data is needed, and retail sales and industrial production will provide some this week. Decisions by the Bank of Canada, Bank of England and many emerging market central banks this week will set the tone as well, with divergent policy clashing with recovery expectations. One consensus in the markets to watch – U.S. dollar weakness – will depend on whether lower rates drive weakness and more hedging demand from foreign investors, or if positioning is at an equilibrium. The other thing to watch is U.S. bonds. Yield curve steepening trades have fallen out of favor, with the 5–30y spread dropping to 25bp from over 125bp last week. We start Monday with a focus on tax payments and liquidity adding to the focus on QT and the Fed. All this sets the tone for global relative value momentum in emerging and developed markets, with U.S. investors seeing better yields and returns abroad in dollar terms.

Will the Fed keep the equity rally going?

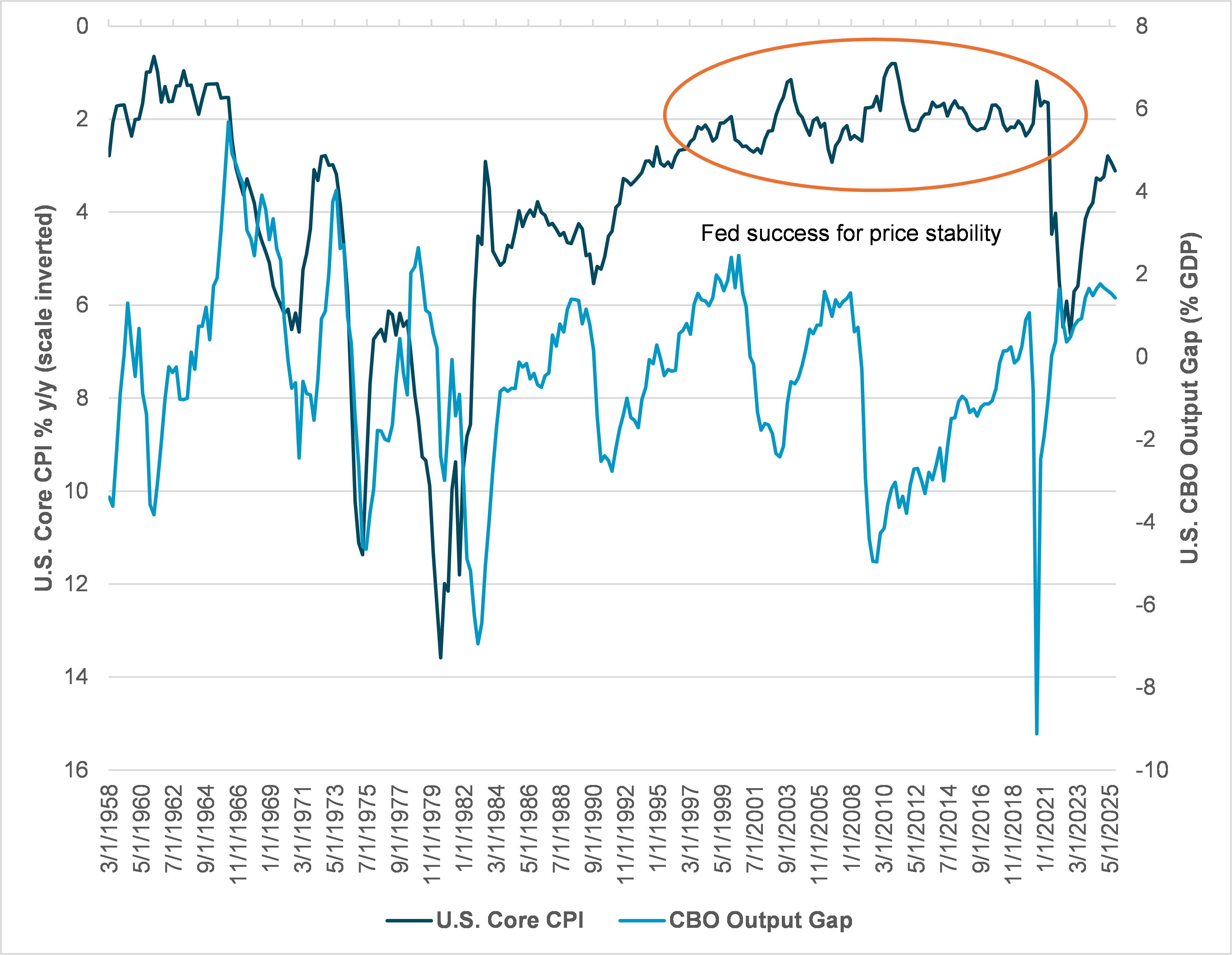

EXHIBIT #1: U.S. OUTPUT GAP AND CORE CPI

Source: BNY, Bloomberg, CBO

Our take: The Fed has a dual mandate to ensure full employment and stable prices, but it hasn’t always fulfilled this mandate painlessly or without falling short for long periods. The U.S. economy from 1964 to 1982, when inflation and growth rode a rollercoaster of boom-and-bust cycles – before the 1977 dual mandate was in place – that provides a lesson for investors: Fed policy doesn’t always dominate. It was during this period that the U.S. shifted from the gold standard to a floating USD. Looking back at history could help investors this week in understanding how a range of central bank policies – from counter-cyclical to pro-cyclical – affects the private sector. There is a risk that dramatic easing by the Fed without causing a recession will remove cash as a safe place for waiting out uncertainty.

Forward look: Next week may force money to be put to work, and this will be the key to future volatility across markets as investors will not accept being paid for doing nothing. Lower returns on cash mean choosing between chasing equities or buying into bonds. For many, this is a choice between a soft landing and recession, between AI productivity and higher energy costs, between consumer resilience and corporate margin compression. There is a dynamic tension between higher asset prices and lower volumes, suggesting the summer calm is about to come to an end. Volatility should follow. The assumption of higher equities, flat bonds and a lower USD will be tested in the week ahead. The Fed may be set to refill the punchbowl, but is anyone still at the party?

Fed cuts and the ongoing data will set pace for market expectations

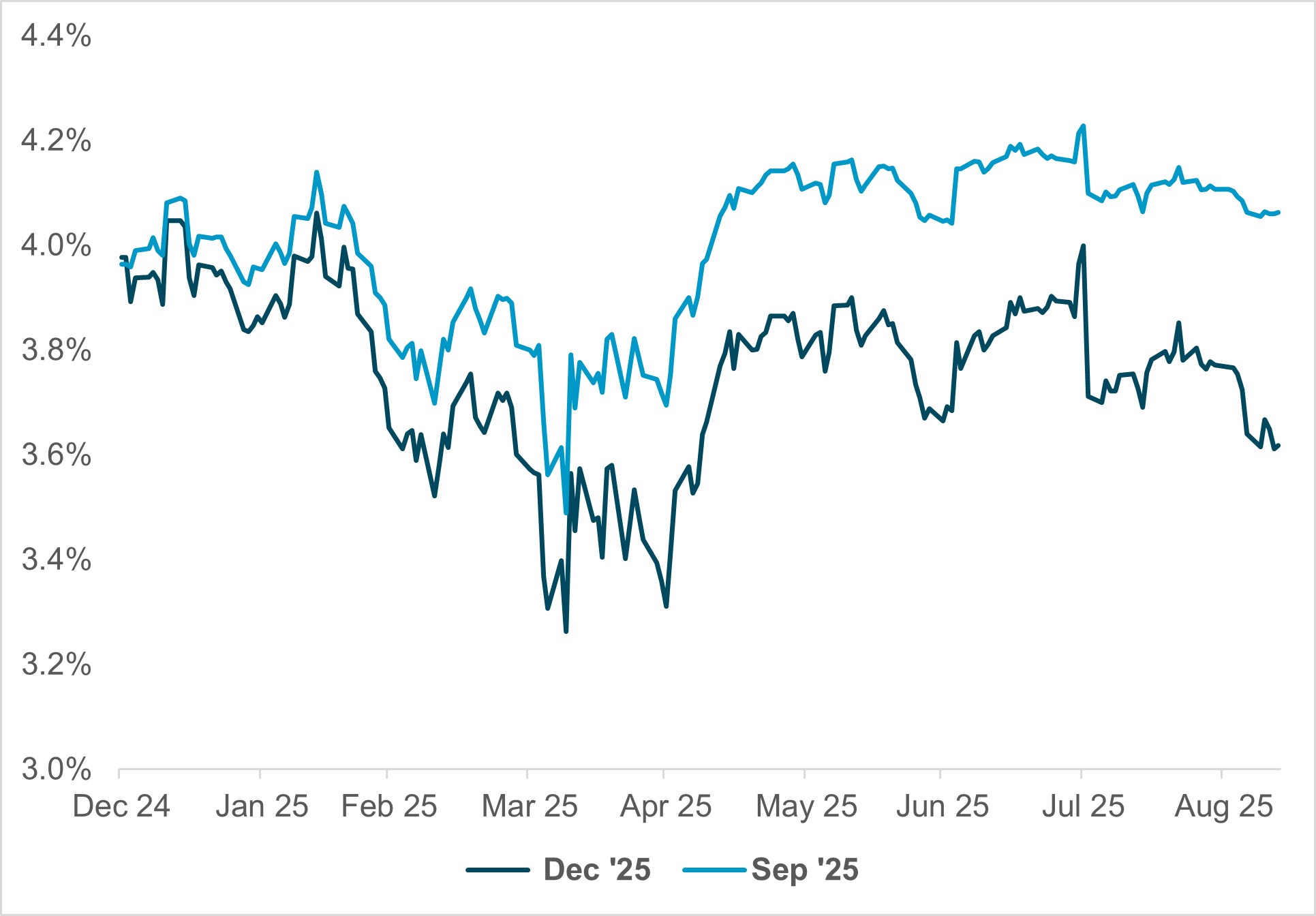

EXHIBIT #2: MARKET-IMPLIED FED FUNDS RATE

Source: BNY, Bloomberg

Our take: A busy week awaits in the U.S., highlighted by the FOMC meeting on Wednesday. Along with the entire market, we expect a 25bp reduction in the funds rate – even though there have been musings of a 50-point “jumbo” cut. We don’t think this is likely, and we remind readers that the September Summary of Economic projections is also due. We expect the median dot to indicate two more 25bp cuts after September at each of the last two meetings of the year. This is one way in which the Fed could deliver a more dovish outcome than just the actual rate cut itself.

Data coming out this week include retail sales, import prices and industrial production. Retail sales will indicate if and by how much consumer behavior is pulling back, while import prices could give us some idea – if they fall – if exporters are trimming their prices to U.S. purchasers to help offset some of the tariff bite. We don’t expect this to be the case, however. Industrial production is important because it is one of the six series that the National Bureau of Economic Research uses to determine if a recession is at hand. It hasn’t yet turned down but is running close to zero lately.

Forward look: The Fed is not the only North American central bank with a rate-setting meeting this week. Also on Wednesday, the Bank of Canada will – we believe – lower its base rate by 25bp to confront mounting recession risk. Market pricing for the rest of the year for the Bank is less aggressive than in the U.S., but we still believe the economy is deteriorating to the point at which more rate cuts will be delivered beyond this week. One thing that could upend our expectations for a cut from Ottawa is a bad inflation print, with CPI due on Tuesday. When you combine the U.S. and Canada outlooks, the risks of stagflation over stagnation are notable with market pricing aggressive to the risk of softer landings.

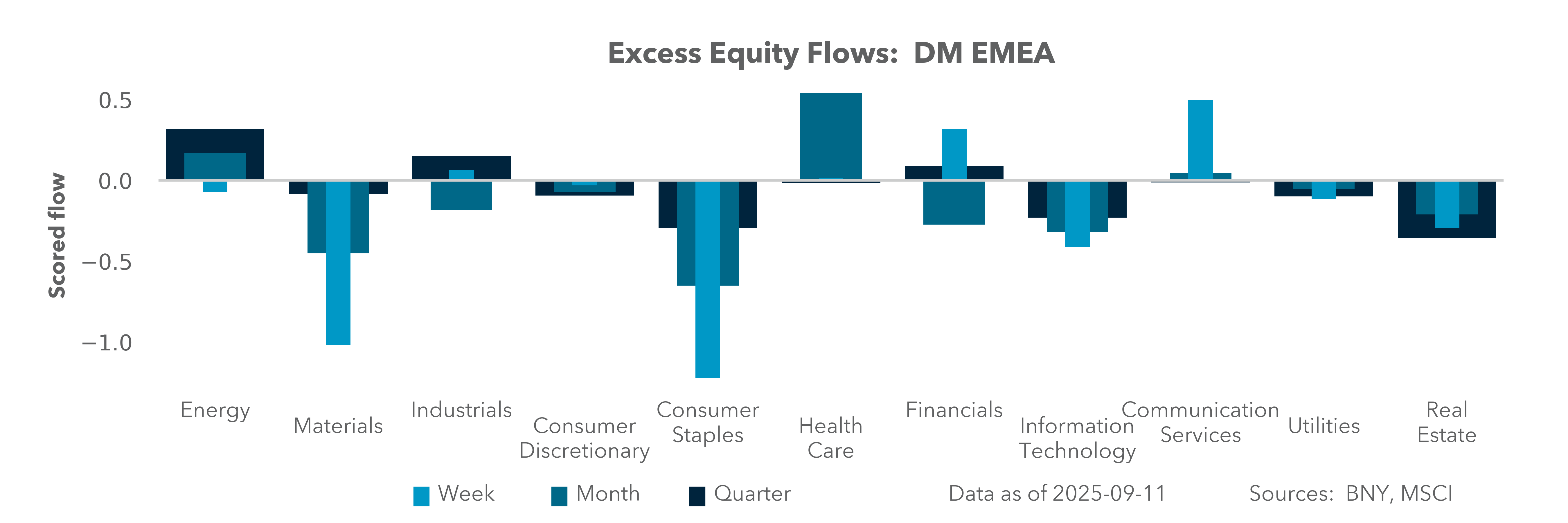

EMEA: Bank of England’s QT choices, Norges faces ongoing inflation constraints

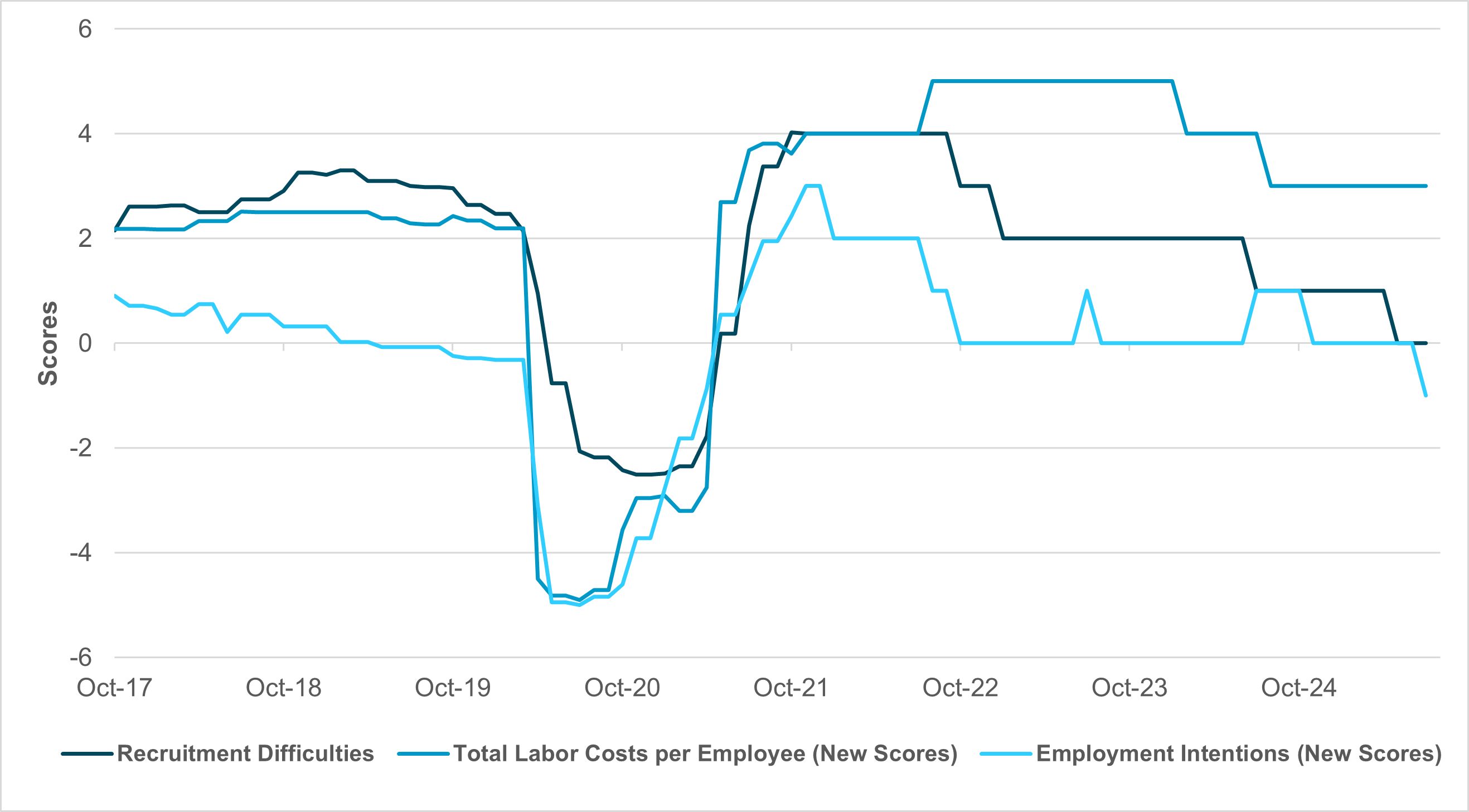

EXHIBIT #3: BANK OF ENGLAND AGENTS’ SURVEY LABOR MARKET COMPONENTS

Source:BNY, BoE

Our take: The Bank of England’s September decision will prove to be a complicated one. To begin with, we wonder whether some remorse might be coming through within the MPC as data since the August decision have been wholly inconsistent with a rate cut. Inflation and activity numbers broadly surprised to the upside, and inflation expectations are hardly well-anchored. The Fed is now perhaps in a position to cut rates amid labor market weakness and softer services inflation, but the U.K.’s services prices – which align exceptionally well with wage growth – are running at closer to 5%, which makes rate cuts very difficult to justify. We note that even during the press conference in August, several MPC members found it a struggle to justify their guidance, and we are broadly in agreement with the market’s guidance regarding limited capacity of rate cuts toward year-end, barring a drastic change in price outcomes. The Bank of England’s own agent surveys point to a “no-fire, no-hire” economy akin to the U.S. (Exhibit #3), whereas hiring intentions are clearly falling, along with recruitment difficulties, but there has been no change in the scores for labor costs for new employees, indicating that those in employment retain significant pricing power. The second core release from the Bank of England will be the gilt selling program review for the coming four quarters. Given the gilt market moves at the beginning of the month – which Governor Bailey was quick to play down – the MPC will need to explore whether their activities could, under some circumstances, amplify moves in gilt markets driven by exogenous factors. We acknowledge that comparisons with 2022 are not appropriate as quantitative tightening hadn’t started. As is often the case with these processes, the marginal change is the biggest at the outset. However, fiscal scrutiny is extremely tight given the U.K.’s current stagflation tendencies. Consequently, there is a case for a softer pace compared to the current £100bn/year, but the move risks being interpreted as the Bank of England having misgivings about the state of the gilt market as well. If any change is needed, it needs to be done in the context of reserve balances reaching critical thresholds, but by the Bank of England’s own estimate, there is still a gap of close to £200bn away from the £480bn upper bound of its Preferred Minimum Reserve Range of Reserves.

Forward look: On balance, we expect a handful of votes for further easing at best by the Bank of England, and the MPC should not be as split as it was August. The August labor market and inflation print ahead of the decision will likely determine the scale of the minority opinion. On the quantitative tightening program, £100bn should be the baseline but quarterly adjustments cannot be ruled out, and the BoE may need to converge to a Bank of Japan-like scenario, which ultimately will pressure the currency, which remains the main source of pressure release for fiscal risk. Norges Bank, in contrast, is broadly expected to cut rates again but we believe there is scope for a break. Inflation continues to run above target and NOK’s recent performance will represent some form of tightening. Given the debate surrounding the country’s wealth tax during the recent election, the new government may tweak legislation with the effect of limiting outflows, which is another form of marginal support for the currency. We note that oil prices and broader commodity exposures have started to stabilize even though demand weakness has been well-flagged globally, and NOK is seen as the strongest benchmark in G10. iFlow indicates positioning, while very high, is no longer at extremes. The week’s speech circuit will be dominated by ECB officials, and if the post-decision commentary is anything to go by, many Governing Council members will be denying that more cuts have been ruled out and highlight the disinflationary impact of the strong euro.

APAC: Focus on China’s housing, activities and investments, regional exports and BoJ

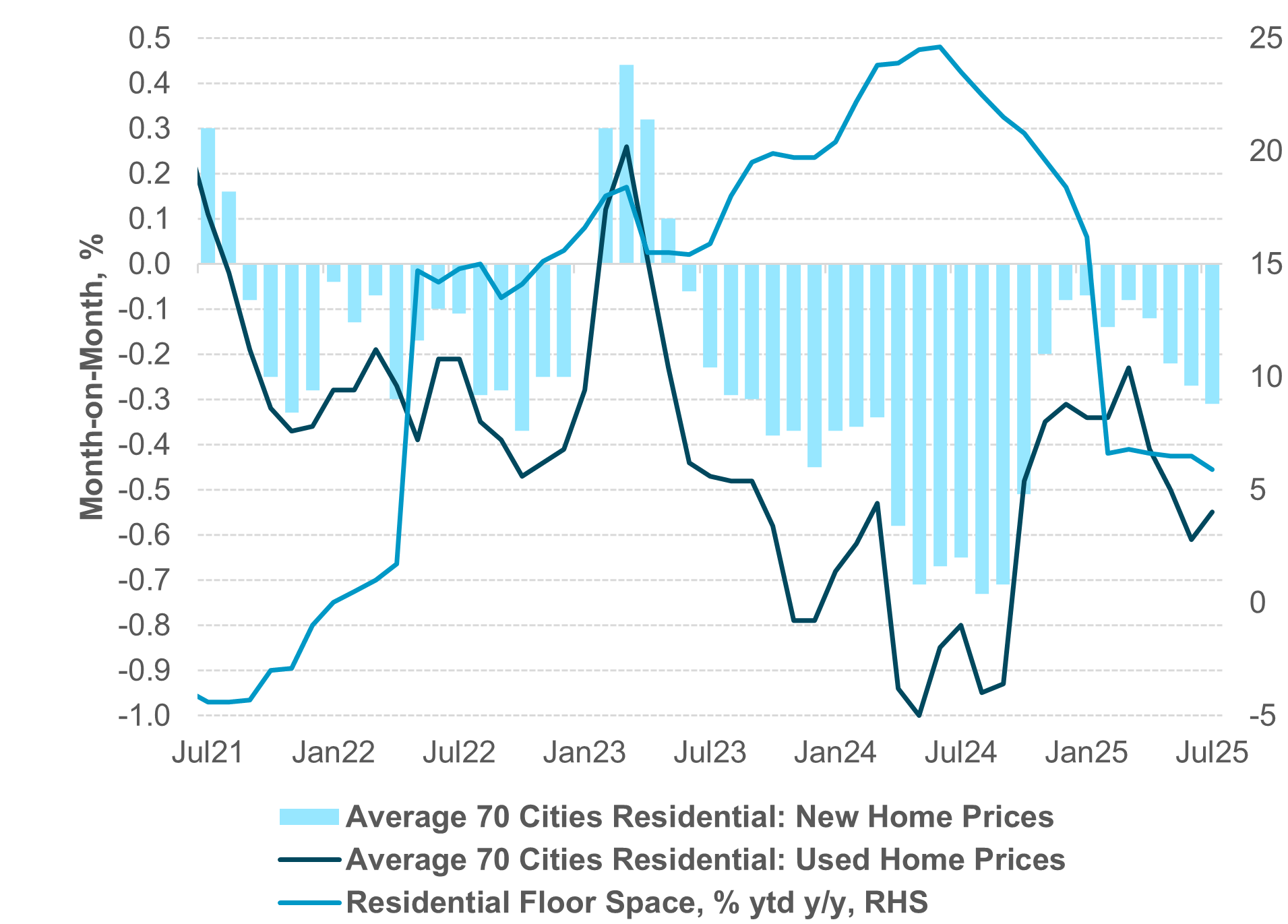

EXHIBIT #4: LOOKING FOR SIGNS OF STABILIZATION IN THE CHINESE HOUSING MARKET

Source: NBS

Our take: In the Asia-Pacific region, the primary data focus this week will be China’s August activity, investment data and the latest housing market developments. There will also be August exports and trade balance releases from Malaysia, Thailand, India, Singapore, New Zealand and Japan. Elsewhere, Australia will release August employment data. China’s investment momentum dropped significantly in Q2, despite accelerating money growth and aggregate financing. As of July, fixed asset and infrastructure investment stood at 1.6% ytd y/y and 3.2% ytd y/y from 3.2% and 5.8% in Q1 2025 respectively. Industrial production slowed to 6.3% ytd y/y in July while high-tech production growth continues to be strong with the output of 3D printing devices, industrial robots and new energy vehicles growing by 24.2%, 24.0% and 17.1% respectively. Domestic consumption, which showed strong upside momentum in H1 2025, eased in July to 4.8% ytd y/y from 5% ytd y/y in June. Downside activities and investment momentum might see further data deterioration before stabilizing later in the year ahead of the new five-year plan (2026–2030). August housing data will be closely scrutinized following the relaxation of the rules for home purchases in Beijing and Shanghai in August and Shenzhen in early September. Both new and used home prices for China’s average 70 cities posted a 26th straight monthly decline since June 2023. Total residential floor space is one of the key indicators of inventory pressure.

August export and trade data for the region is at risk of a downside surprise following the weaker-than-expected Chinese and South Korean export data, which came in at 4.4% y/y and 1.3% y/y respectively. Indeed, South Korea’s daily export average for the first 10 days in September plunged to –8.4% y/y from 9.3% y/y over the same period in August. Trade and export data ahead should reflect any real impact from tariffs following strong trade activities in H1 2025 on the back of front loading. Finally, Australia’s August jobs data will be closely watched in the context of tight labor conditions and the implications for the Reserve Bank of Australia’s policy decision at the end of September.

With respect to monetary policy, the Bank of Japan is expected to maintain the status quo and keep rates at 0.5%, leaving open the option of policy tightening in Q4 2025. Bank Indonesia is expected to keep rates unchanged at 5% following the back-to-back rate cuts at its July and August meetings while maintaining a dovish bias, and Taiwan’s central bank is seen as keeping rates unchanged at 2.0% at its quarterly meeting.With respect to monetary policy, the Bank of Japan is expected to maintain the status quo and keep rates at 0.5%, leaving open the option of policy tightening in Q4 2025. Bank Indonesia is expected to keep rates unchanged at 5% following the back-to-back rate cuts at its July and August meetings while maintaining a dovish bias, and Taiwan’s central bank is seen as keeping rates unchanged at 2.0% at its quarterly meeting.

Forward look: Asian currencies posted strong gains last week supported by the softer trending U.S. dollar, renewed foreign capital inflows and falling crude oil prices. The key market driver for the week is the FOMC meeting. China data will be closely watched, but the current positive market sentiment, driven by tech and AI, is likely to overshadow downside data surprises. The recent rise of Chinese equities as well as Taiwanese, South Korean and Japanese equities reaching all-time highs has raised some concern about a possible correction, but we remain constructive on further upside potential and do not see the current moves as extreme yet, technically speaking. The ongoing asset allocation shifts from developed market to emerging market, as shown in iFlow equities, will provide additional support to APAC assets. Indonesia asset volatilities stemmed from social unrest, and the unexpected cabinet reshuffle was short-lived. Indonesia equities and fixed income market has reversed most of the selloff, with Indonesia rupiah lagging. We see limited upside for USDIDR and a gradual shift toward 16000 as the uncertainty subsides. Elsewhere, there are plenty of relative value opportunities in the region. TWD and CNY are likely to benefit from capital inflows and positive equities momentum, while INR is the weakest link on the negative impact of tariffs. THB’s valuation looks stretched on weak macro fundamental and asset prices, while KRW looks cheap following recent divergence.

The week ahead will be dominated by the Federal Reserve’s expected rate cut, which could reframe market dynamics and challenge assumptions around stagflation, bond market stability and dollar weakness. Other central bank decisions (BoC, BoE, Norges, EMs) add to policy divergence that will likely drive volatility across global assets. In the month ahead, the key theme is that lower returns on cash will force investors to allocate into equities or bonds, increasing the risk of sharper volatility once the summer calm fades. New themes include the importance of China’s fragile stabilization, relative value shifts from developed to emerging markets and the test of whether U.S. easing truly “refills the punchbowl” or merely accelerates volatility. After the Fed and other central bank decisions there will be a sprint to month-end rebalancing and the rising odds of a U.S. government shutdown. Whether this makes the week ahead a waiting game and a relief trade – selling the rumor and buying the fact of easing for the USD – may matter most as correlations between all markets have broken down due to policy uncertainty.

Central bank decisions

Indonesia, BI (September 17, Wednesday) – We expect Bank Indonesia to keep the policy rate unchanged at 5.0% while maintaining an easing bias. The central bank is likely to reiterate its intention to “continue to look for room to further lower rates” and “make efforts to encourage bank lending and economic growth,” as well as maintain its triple-intervention strategy and utilize offshore NDF instruments. Maintaining financial stability is the top priority in the near term.

Canada, BoC (September 17, Wednesday) – We expect the Bank of Canada to cut its rate 25bp and deliver a dovish message in its statement and at its press conference, suggesting further reductions ahead, which is not yet fully priced into the forward curve.

United States, FOMC (September 17, Wednesday) – The FOMC will deliver a 25bp cut, and the quarterly Summary of Economic Projections will indicate two additional cuts for the remainder of the year. We view the 2026 outlook as particularly murky from here, so we wouldn’t read too much into the dots beyond this year.

Brazil, COPOM (September 17, Wednesday) – The Banco Central do Brasil is expected to keep the Selic rate on hold at 15.00%. Official communications since the last decision to hold rates in July indicate that this stance is consistent with the strategy for inflation to converge toward the target over the relevant forecast horizon. August consumer price inflation (IBGE’s IPCA inflation) eased to 5.13%, helped by lower electricity and food costs, though inflation remains above the central bank’s target, especially in services. The committee emphasized that while inflation is cooling, it is not yet sufficiently anchored to support a rate cut. Recent signs of weakening economic activity and moderating inflation suggest any policy easing will be considered only after there is clearer evidence of sustained disinflation.

Norway, Norges Bank (September 18, Thursday) – On balance, markets expect a cut by Norges at its September meeting, front-loading the one available easing move for the rest of the year. We believe that a hold is the best option as official inflation data show that headline CPI remains elevated year-on-year, coming in at 3.5% in August, with core inflation also stubborn. Underlying CPI is also running at 3.1% y/y even after a strong sequential contraction. These metrics, together with firm output growth outlooks from the flanking business surveys, indicate the Bank will wait for more convincing evidence of disinflation and easing pressures before easing policy. The recent general election result should also not materially alter the Central Bank’s outlook as fiscal continuity is expected, subject to potential wealth tax adjustments.

United Kingdom, BoE (September 18, Thursday) – The Bank of England is expected to keep the base rate on hold at 4.00% but a three-way split is less likely this time as inflation and output numbers have been very robust during the intervening period. We sensed a deep reluctance on the part of the MPC to cut rates in August, and given the recent moves in gilt markets, the BoE will also need to be mindful of limiting the decline in real rates. However, Governor Bailey has also made his views known on the gilt market and this should not be a major factor in the September decision, especially relative to services inflation, which continues to push against the 5% y/y figures. The Bank of England will also release its latest gilt sales program review. Given the recent gilt market volatility, markets may assess whether the BoE would “do a BoJ” and begin to soften its pace of quantitative tightening, which stands at £100bn per year.

South Africa, SARB (September 18, Thursday) – The South African Reserve Bank is expected to keep its repo rate unchanged at 7%, given most recent inflation readings remain within or close to its target range. The latest official CPI figure from South Africa’s statistics agency shows annual headline inflation at 3.5% y/y in July 2025, up from 3.0% in June (the August number will be available before the decision). This increase represents the highest inflation rate in approximately 10 months. Core inflation (excluding food, non-alcoholic beverages, fuel and energy) also rose slightly to about 3.0% y/y in July. Food inflation remains one of the biggest contributors, especially in meat, vegetables and other food items, which have shown notable annual rises. Given these figures, as well as moderate domestic price pressures and external risks (including import costs), the Bank is likely to emphasize data-dependence in its communications before making any moves.

Taiwan, CBC (September 18, Thursday) – We expect the CBC to maintain rates at 2%. The latest macro forecast will be closely scrutinized. As of June 2025, CBC sees 2025 GDP at 3.05% (vs. the statistics office forecast of 4.45% and 2.81% for 2025 and 2026 as of August 25) and 2025 CPI at 1.81%. Strong GDP and stable inflation call for steady policy for now. There is no urgency for a preemptive move. We expect CBC to maintain the reserve requirement ratio and no changes in measures on real estate loans. The series of macro prudential measures over the past few years are finally working, with slowing house price appreciation and mortgage loan growth.

Japan, BoJ (September 19, Friday) – The Bank of Japan is expected to maintain its policy rate at 0.50%, having kept this level since January 24, 2025. At 2.8%, Japan’s inflation – including core measures – remains well above its target, though recent wholesale inflation trends have shown mixed signals: food and beverage prices continue to rise strongly, but other sectors are less uniform. The BoJ’s official outlook report released in the past month highlights ongoing risks from import costs (including the effects of a weak yen) and wages that have yet to sustainably accelerate. The Bank is likely to continue its cautious stance, emphasizing data-dependence before any further adjustments. Markets will also take a keen interest in potential shifts in BoJ policy depending on the outcoming of the LDP leadership elections.

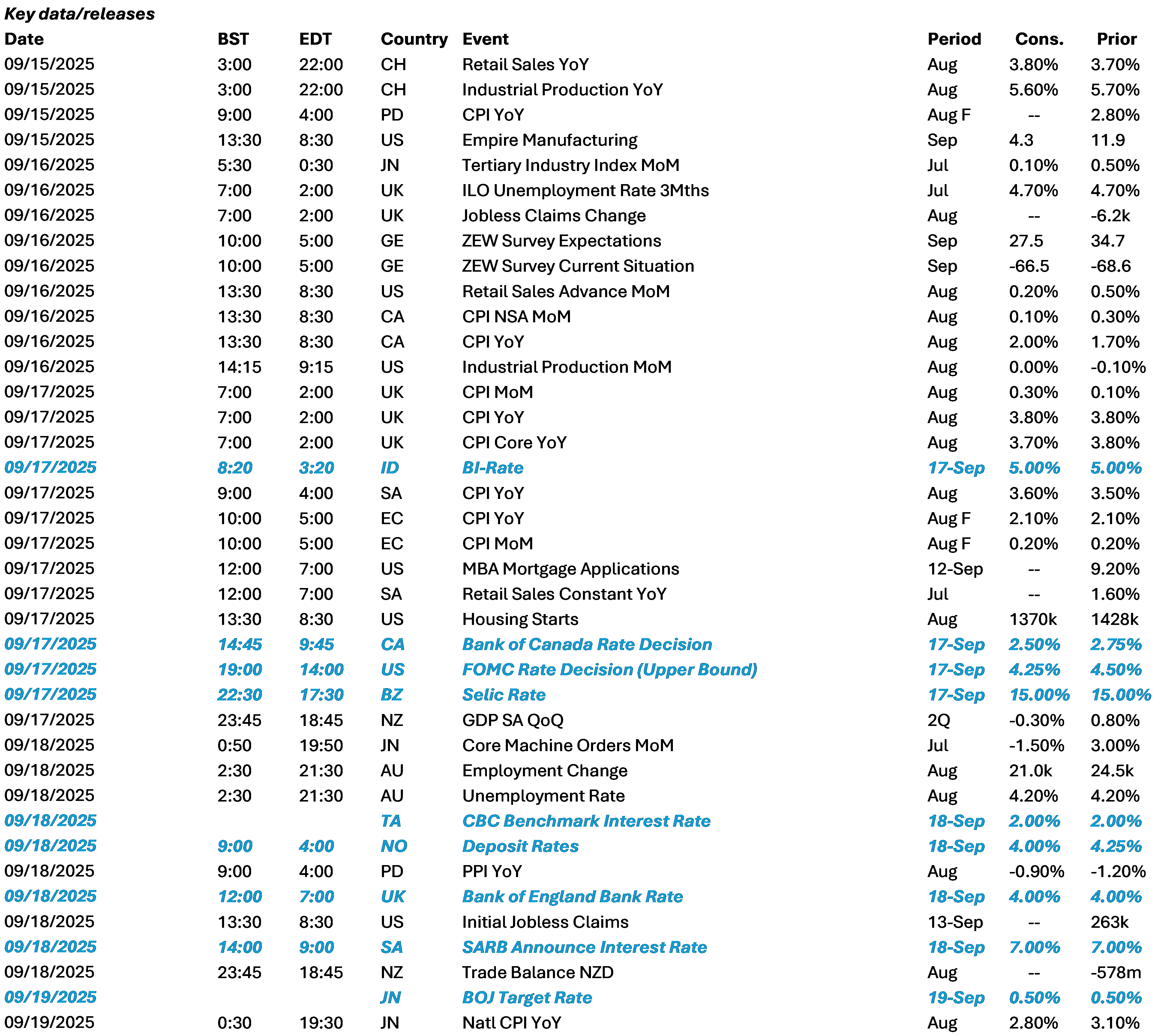

Data Calendar

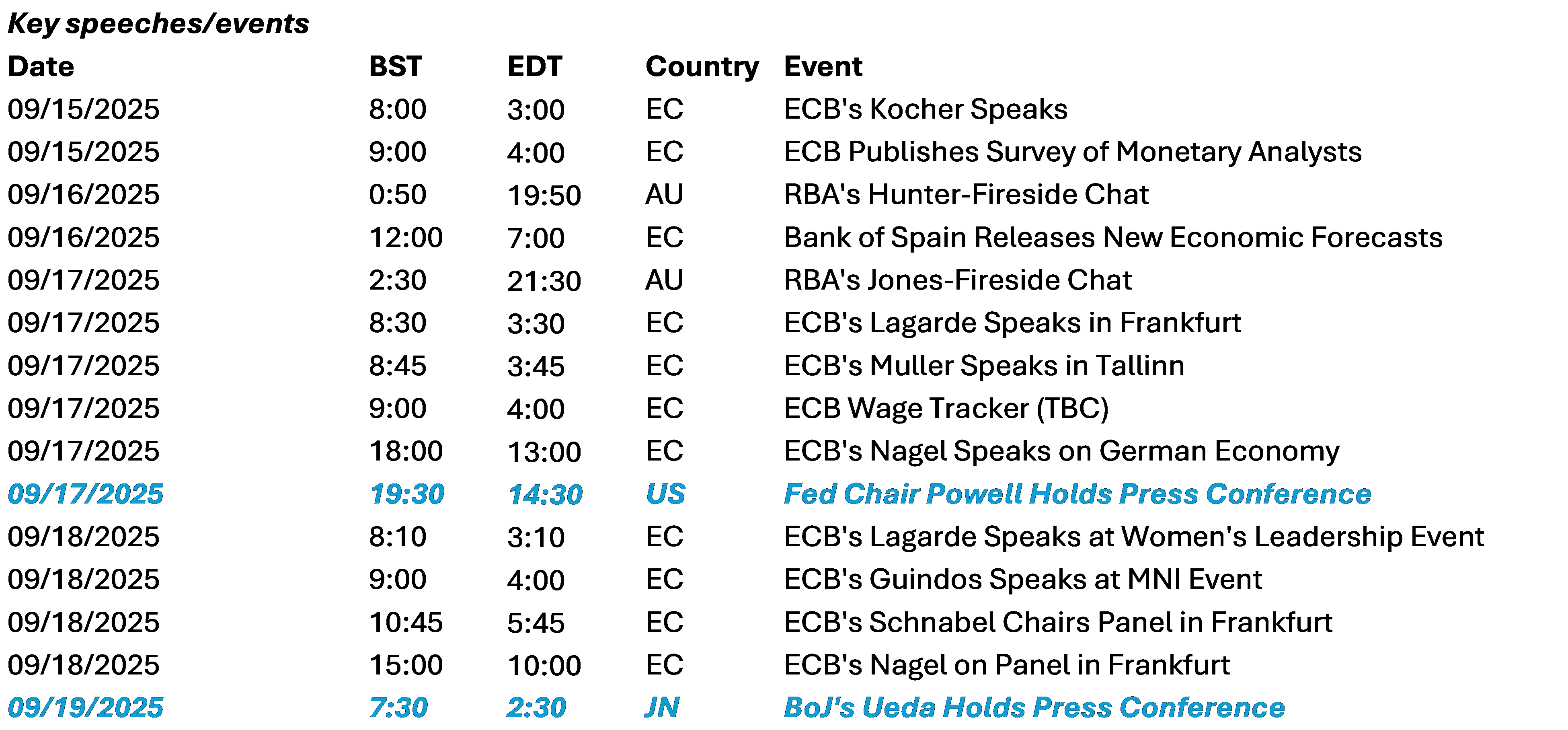

Event Calendar