No Relief

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 12 minutes

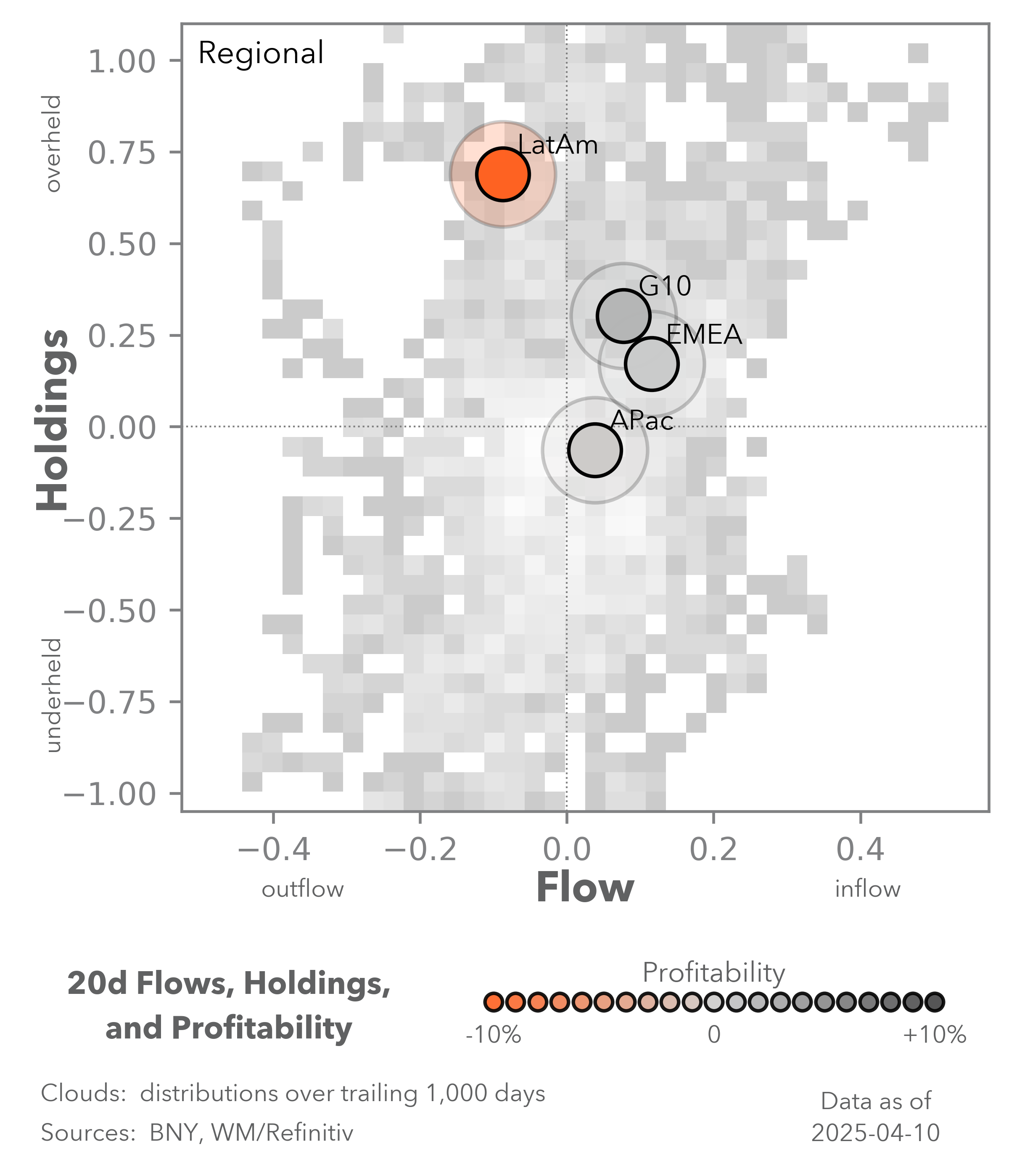

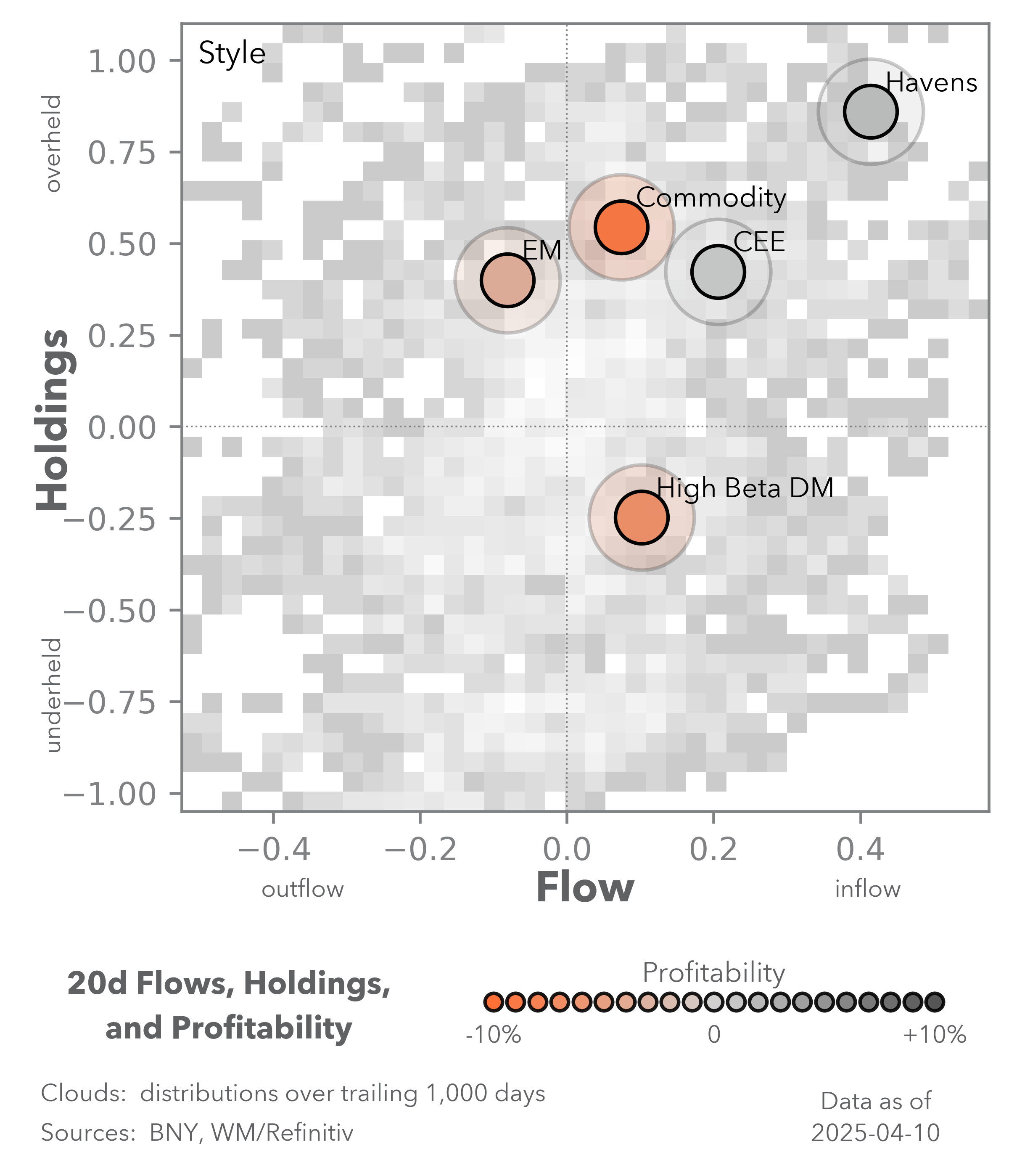

Markets remain volatile as the off-ramp for U.S. tariffs remains unclear (particularly for China) and the rush for alternatives to the U.S. overwhelms many asset classes. Redefining safe-havens has become a key task for 2Q. The money flows we saw in the last week highlight the confusion from U.S. bonds to the USD or EUR to Gold. The role of Emerging Markets as a diversified pool away from the current trade disruptions may be tested as investors search for higher risk premiums uncorrelated to U.S.-China trade tensions. The bottom of this market storm will develop as investors see value and growth more clearly in the quarter ahead.

There are four themes for global markets as they search for a bottom in risk aversion:

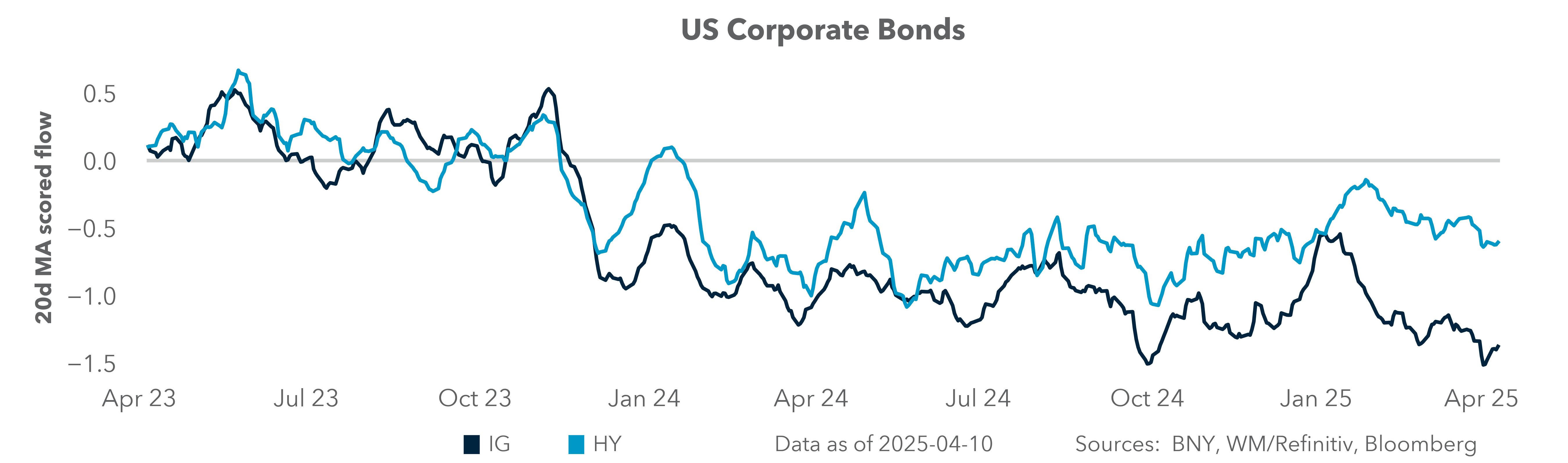

EXHIBIT #1: LAST WEEK’S NEGATIVE CROSS BORDER FLOWS INTO THE U.S. BOND MARKETS

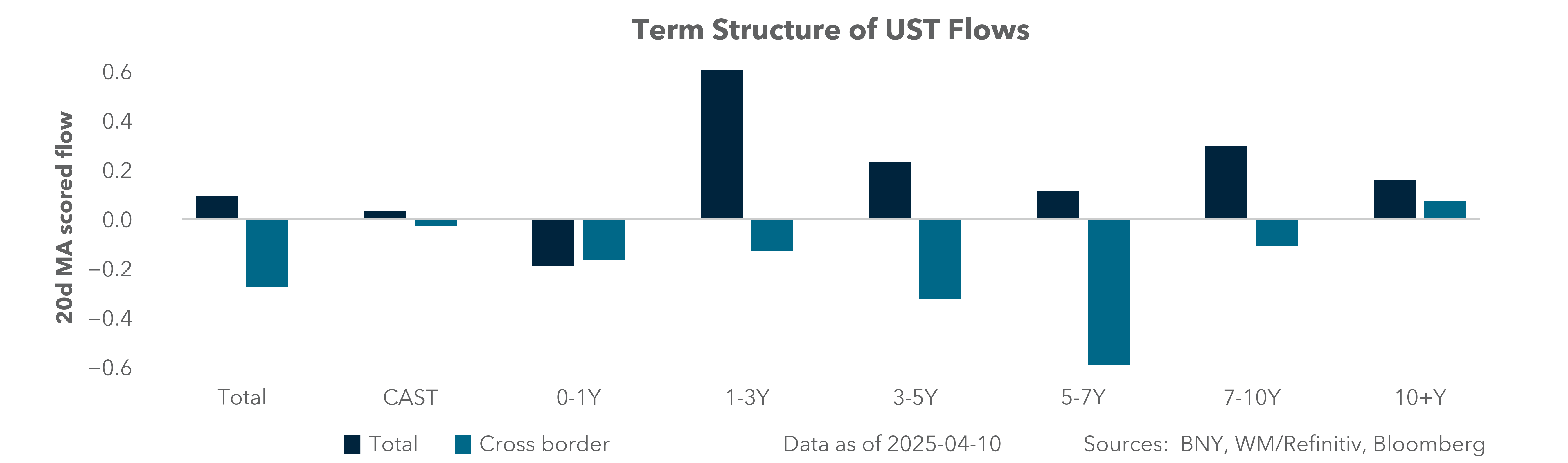

Source: BNY, WM/Refinitiv, Bloomberg

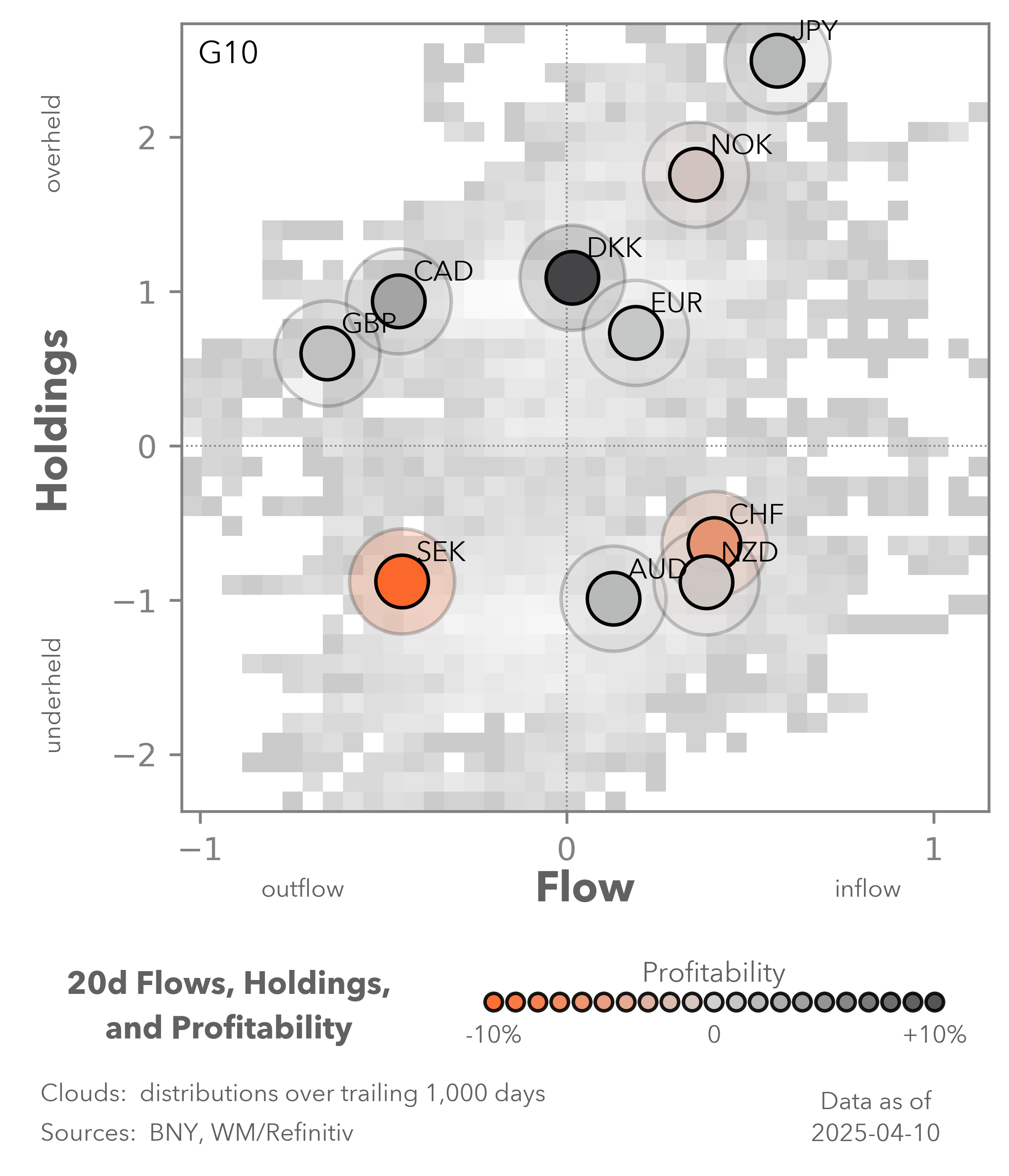

Our take: Last week’s flow data will be an important baseline for future crisis management. The sharp movement in U.S. bond flows stands out, as U.S. 10-year rate increase from 3.80% to 4.50% in a week leaves many investors hurt. No current models are working in this environment other than except for rushing to other safe-haven assets, which the U.S. is no longer considered. However, our flows show the USD inflow as significant, suggesting a more dangerous home bias emerging for the world. U.S. investors are bringing money home. In equities, retail buyers are now selling as their March “buy-the-dip” mantra shifts. After watching the ups and downs of USD, S&P500 and UST last week, the key takeaway is to hedge everything. We are watching for carry trades to return to neutralize and trends to regain positive returns. Both are risk negative but necessary for stabilizing USD, US shares and bonds. Models need to return to work.

Forward look: U.S. markets could stabilize if 1Q earnings beat expectations. Stabilization could also show up in the 20-year bond sale next week as investors return to duration and hold expectations of a FOMC reaction to financial conditions and liquidity. However, this is unlikely given the current set up for positions. The markets were uneven and at times illiquid in the last week but remained functioning. We remain in a melt-down mode that surprises us in its following of almost every other crisis. Overcoming fear requires the building up of cash and push back on any other positioning. Treasury market cross-border flows into the U.S. don’t reflect this capitulation yet.

US inflation exceptions, not retail sales, Bank of Canada meeting and more tariff talks

Canada’s BoC rate setting meeting on Wednesday will be the first chance for us to gauge how central banks are reacting to tariff measures. In Ottawa, Governor Macklem has been adamant that the Bank’s priority is to contain inflation and inflation expectations due to the trade war. Coincidentally, the Canadian CPI for March will be released on Tuesday, the day before the Bank’s meeting and will include the latest Quarterly Inflation Report. Market expectations reflect only a 37% chance of a cut, a move would be surprising. Our call is for a hold, but with a dovish message on growth, especially if inflation comes in at an acceptable rate.

To us, the US data highlight of the week might not be what one would expect. Yes, retail sales will clue us into March consumer behavior, but it will likely be dismissed as pre-tariff data, and therefore “old news.” Rather, Monday’s NY Fed Survey of Consumer Expectations will provide important insight into long-term inflation expectations, which Fedspeakers have continually referenced as paramount. The U.S. central bank is likely to be cautious about easing policy too soon, preferring to make sure they keep long-term inflation expectations anchored before beginning to ease policy into potentially weaker hard data.

UK Jobs, CPI, German ZEW, EU Current Account

Tariffs have tested reserve currency shifts, giving the EU an opportunity to differentiate from U.S. policy and expand their global trade relationships with Australia, New Zealand and China. The risks for such a push will be in how China deals with its domestic growth needs, redirection of goods that previously destined for the U.S. The decoupling of the U.S.-China trade relationship raises questions about Europe’s role, potentially rising from a confederation of nations to a coordinated federation. This week, the way in which the German ZEW and the new German government handle U.S. talks around the EU will be important, along with Germany’s defense spending in NATO and Ukraine. All eyes are on geopolitical pressures more than economic, as the first drives the second. The ECB’s actions as the bridge between EU nations combined with Lagarde’s leadership on the April decision may influence how the EUR trades beyond interest rate spread and growth differentials to the rest of the world.

In the week ahead, UK jobs data will be key for how the GBP manages with the EUR flows clearly dominating. Better GDP in the UK for 1Q surprised Friday could lead to a better job market and higher wages, testing the BOE as it deals with stagflation worries and fiscal concerns. Volatility remains an issue as the Gilt market is still more linked to the UST than to Bunds. One of the most important factors for trading risk in the UK and beyond may be how the UK rates trade.

Challenging Q1 APAC growth, more easing and stimulus ahead

The 90-day pause on US tariffs is unlikely to boost confidence in APAC given the 145% tariff rate on Chinese imports. Escalating trade tension puts investors on maximum alert, increasing downside growth risk and encouraging reduction of risk exposure to the region. The economic data focus this week will be on China’s Q1 GDP and March investment, activities and consumption data. Consensus is for an upbeat sequential quarterly GDP growth of 1.5% q/q after 1.3% q/q and 1.6% q/q in the prior two quarter growth in Q3 and Q4 2024 or a 5.2% y/y, supported by AI-driven sentiment and potential pre-tariff trade activities ahead of April. China infrastructure investment showed growth at the beginning of the year at 5.6% ytd y/y from 4.1% ytd y/y bottom in September 2024, the fastest pace of fixed asset investment growth since April 2024 at 4.1% ytd y/y as of February 2025There was a pickup of retail sales at 4.0% ytd y/y and steady industrial production 5.9% ytd y/y supported by high-tech sector production such as industrial robots (27% ytd y/y) and new energy automobiles (47.7% ytd y/y).

Malaysia and Singapore will release March exports and Q1 GDP data, while India will release March exports and inflation data. Australia’s March jobs data will be closely monitored for signs of loosening its tight labor market condition. New Zealand’s Q1 CPI release should support further RBNZ easing after the 75bp rate reduction so far this year.

While China’s Q1 economic data might be supported, growth risk in the region is on the downside according to official growth projections. In its policy meeting last week, the Reserve Bank of India lowered its FY2025-26 GDP and CPI forecasts from 6.5% y/y and 4.0% y/y to 6.7% and 4.2% y/y, respectively. The broad economic slowdown should pave way for policy easing and fiscal stimulus in the region. This week, the Monetary Authority of Singapore is expected to ease by flattening the SGD NEER policy slope. The consensus is that the Bank of Korea (BoK) will stay status quo but prepare the market for a rate cut at the next meeting in May, along with the release of latest economic projection. We can’t rule out a back-to-back BoK cut considering increasing downside growth risk.

Risk aversion continues to dominate capital flows with persistent foreign equities outflows across the region. The brief buying interest in India equities at the end of March swiftly reverted to selling, including their government bonds. For China, iFlow equity data shows investors halted two months of buying and turned net selling so far in April.

EXHIBIT #2: CHINA GDP GROWTH PROFILE

Source: Bloomberg

Central bank decisions

Singapore MAS (Monday, April 14): MAS is expected to flatten its SGD NEER policy curve. With easing inflation and slower growth, MAS is likely to further unwind the aggressive tightening policy moves from October 2021 and October 2022. MAS easing measures might support the stabilization of the housing market. URA residential decreased to 3.1% q/q from 3.9% in Q4 2024, the lowest since Q4 2020. Our view is for MAS to ease by flattening the SGD NEER slope and possibly revise the downward GDP forecast, which is currently at 1.0-3.0% for 2025. The latest CPI projection was 1.0-2.0% for core and 1.5-2.5% for headline for 2025.

Canada BoC (Wednesday, April 16): We don’t expect a rate cut from the bank this week, since Governor Macklem is focused on fighting inflation because of the trade war. Market expectations only see a 35% chance of a cut. Recent employment data disappointed with -62k jobs created. Despite tariff news, the Canadian dollar (currently below 1.40) is holding steady, although that is as much of a USD phenomenon as it is a Canadian one. The bank’s Quarterly Inflation Report will be released alongside the rated decision, and we might get a dovish message regarding tariffs.

South Korea BoK (Thursday, April 17): BoK is expected to cut rates by 25bp to 2.50%. South Korea data has been mixed. South Korea March PMI manufacturing is in contraction (49.1), while Composite Business Sentiment Index for manufacturing and non-manufacturing sectors increased from 90.1 to 91.9 and 81.7 to 82.9 in March. April outlook is expected to lower from 89.9 and 82.4 respectively. Consumer confidence and retail sales (4.4%) both slowed. Inflation stayed above 2% for the 3rd straight month and renewed upward momentum in bank lending to household. Consensus is for the BoK to keep rates unchanged at 2.75%. but we see risk of a quicker rate cut to 2.50% due to downside growth risk and lower inflation expectations due to the lowering of commodity prices. We expect BoK to maintain a dovish stance.

Eurozone ECB (Thursday, April 17): ECB is expected to cut rates by 25bp to 2.25%. ECB was cautious in March when they delivered a 25bp rate cut to 2.5% and commented that “monetary policy is becoming meaningfully less restrictive”. Over the past few weeks, global growth prospects have deteriorated significantly due to tariff uncertainties and extreme market volatility. The EUR was up 4% in March and hit 1.13, while EuroStoxx was down 4% in March and 8% in April. The 10yr Bund was up 33bp in March before dropping 15bp to 2.74% at the time of writing. Market volatility and the prospect of lower inflation from lower commodity prices and a measured tariffs response argue for ECB to cut deposit facility rate by 25bp to 2.25% and keep its options open for further moves.

Turkey TCMB (Thursday, April 17) – The sharp decline in the lira last month due to domestic factors and additional global risk aversion last week means that TCMB is in no position to cut rates. Therefore the repo rate is expected to remain at 42.5%. Last month, in an unscheduled meeting, the central bank raised its overnight lending rate by 200bp to help defend the lira so any step in the opposite direction would not be consistent with current objectives. A weaker TRY will once again risk the de-anchoring of inflation expectations, which even before recent events were struggling to adjust lower. With inflation in Turkey holding just below 40%y/y, it remains imperative for TCMB to maintain an adequate real rate buffer.

Source: BNY, Bloomberg, MSCI

Source: BNY and WM/Refinitiv