Next Shoe to Drop?

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 10 minutes

The end of summer hit investors hard with a heavy set of economic and political surprises. First, the weaker U.S. jobs report changed the narrative that Fed cuts would suffice to right-size returns. Second, China’s military parade and summit made clear that some of the world sees a multi-polar path for growth and policy. Third, the ongoing focus on debt from Japan to France to the U.K. to the U.S. means curve steepening and the cost of borrowing are inextricably linked to politics. The week ahead will continue to present event risks sufficient to keep volatility in play – from the French no-confidence vote to the U.K. budget to Japan’s LDP leadership election to the risk of a U.S. government shutdown as well as U.S. court rulings on tariffs and Fed Governor Cook. The consensus now is that there will be a Fed rate cut and curve steepening. The theme of dollar weakness has returned, with gold rising to record highs.

Countering tariffs and other policy shifts impacting the global economy will require more than just central bank easing. Canada’s push, for example, may be a foreshadowing of the issues ahead as the country establishes a C$5bn fund to support tariff-hit companies, new job training and subsidized loan packages. However, keeping rates supportive across the curve will leave politicians struggling with high government spending and sticky inflation risks. Also notable is the risk of a squeeze-out. The supply of U.S. investment-grade (IG) bonds over the past week was significant, coming in at $67bn for 50 companies – the second-highest volume this year and well above the $55bn forecast. The flattening of 10–30y spreads was also notable, at 14bp vs. 41bp for the15y average. The risk premium for government and IG debt duration looks modest given the pressures ahead.

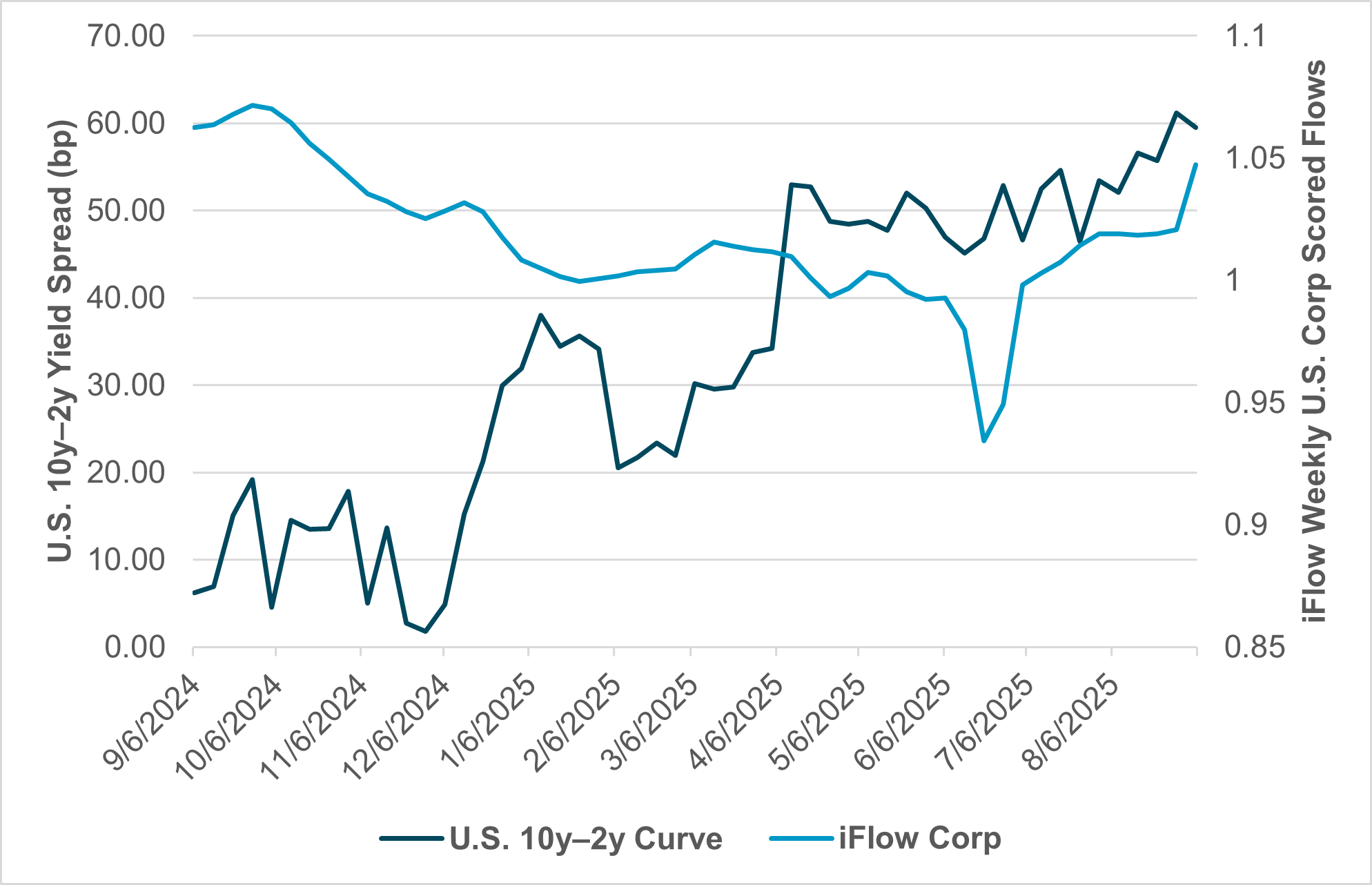

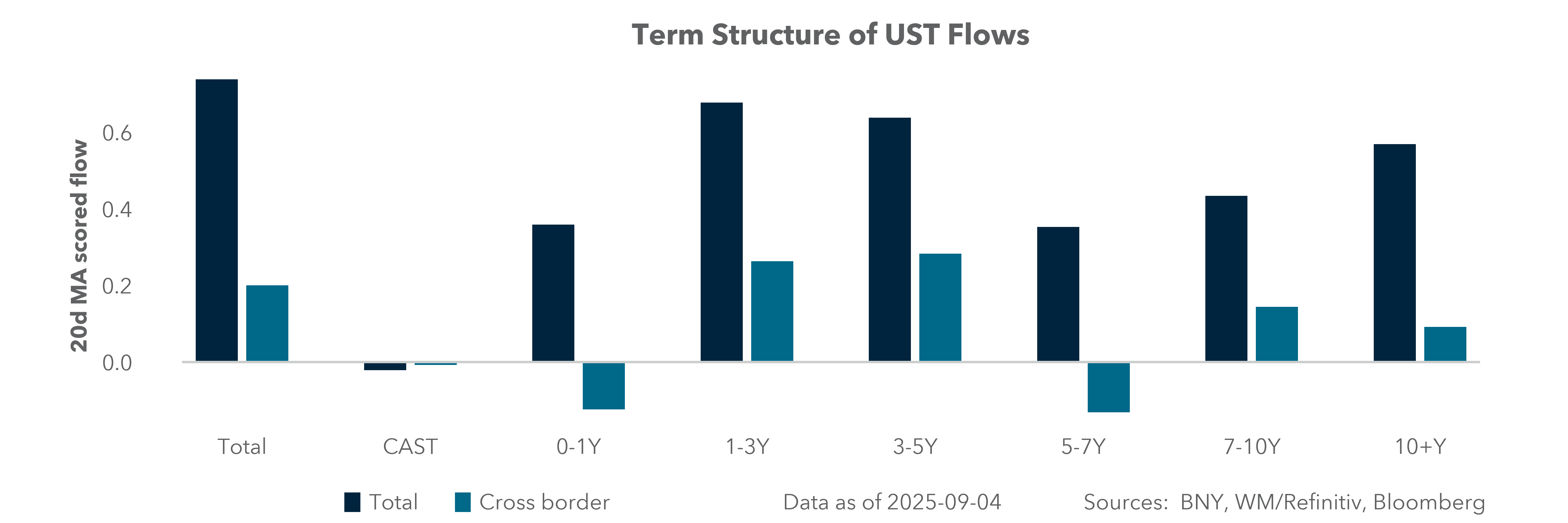

U.S. corporate issuance and U.S. government yield curve in play

EXHIBIT #1: IFLOW U.S. CORPORATE FLOWS VS. THE U.S. 2Y–10Y CURVE

Source: BNY, Bloomberg

Our take: Investors expect greater rewards for incurring greater risks, and the next week will require increasingly higher premia for stocks, bonds and the USD. Bond supply is clearly meeting demand, with higher yields in the U.S. and EU markets finding buyers at the start of the week. The supply of IG debt in the U.S. and the EU was also well received. This is due in part to increased expectations of a Fed rate cut as well as a shift in asset allocation from equities to bonds. The pressure on bond buying only showed up in our flows around the end of Q2, and that matters for the rest of the month as U.S. bond expectations and the shape of the yield curve are a consistent factor for buying, as Exhibit #1 shows. Higher long-end rates have in the past usually led to selling of corporates, not more buying – as credit worries rise.

Forward look: Traders have long been concerned about credit in the current easing environment, and things may finally come to a head this week. The key question is whether these concerns will finally start to show up in the markets. The supply of credit was easily absorbed last week, but with even lower yields and steeper curves it’s not clear this will be the case again this week. Equities and USD duration risks are another point to watch. Lower dollar hedging costs due to expectations of a Fed rate cut could further push markets to chase risk-off trends. In the U.S., the market will have $58bn in 3y, $39bn in 10y and $22bn in 30y to absorb, with considerable supply in the EU (€45bn) and the U.K. (£8bn) as well. Adding to the uncertainty in the week ahead are the impact of corporate issuance and the tax payments due on September 15.

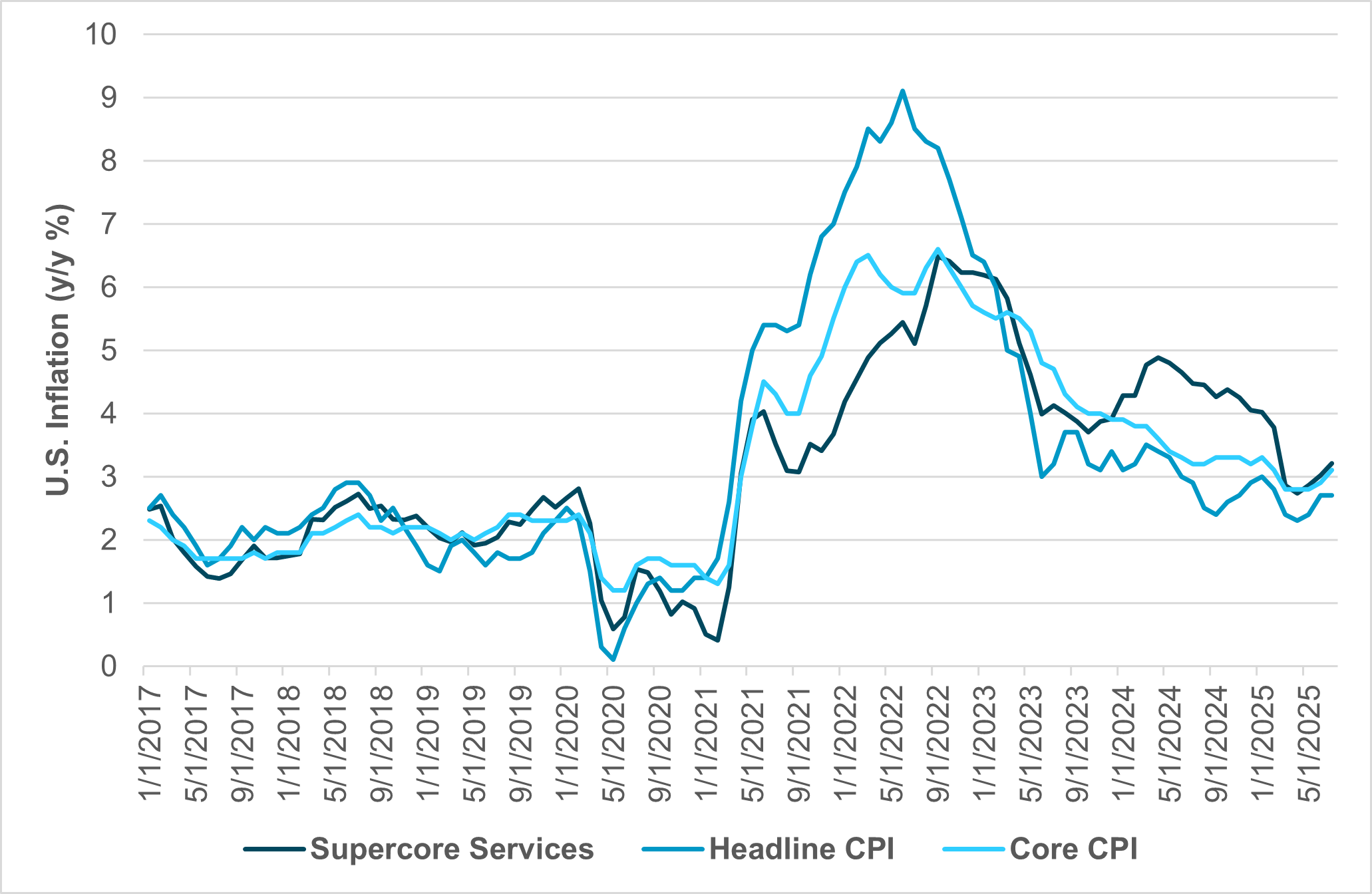

Will U.S. inflation be the next shoe to drop on summer complacency?

EXHIBIT #2: CORE AND SUPERCORE CPI ARE BOTH ABOVE HEADLINE

Source: BNY, Bloomberg

Our take: The U.S. labor market report on Friday pushed expectations of Fed easing higher. The terminal rate, which was previously anchored at 3%, approached 2.75%. The drop in U.S. yields sent the USD lower but didn’t help U.S. equities as bad-new-is-good arguments require some assurances that rate cuts will suffice to drive growth back higher. The other significant worry for investors is that the steepening of the U.S. rate curve reflects some credibility doubts about Fed policy and inflation. The Fed is on blackout next week, so any shift to more than 25bp of easing will require a press leak – which most assume will not happen until after the BLS jobs revision on September 9 and the CPI release on September 11. The odds of 50bp of easing are modest, and we think such a move is unlikely given the risks of sticky inflation.

Forward look: The role of inflation in the FOMC’s rate plan will be the central test of investor mood in the week ahead. Goods moved from disinflation to inflation on the back of tariffs. Although tariffs are viewed as a one-off tax on companies and consumers, the bigger problem for the Fed is supercore services as wage inflation moved higher. The Fed will need further confirmation that job losses are leading to lower wages and lower demand for it to be able to act more aggressively. This puts the FOMC’s SEP “dot plot” into focus for investors forecasting value and growth plays into the end of the year. The risk that the FOMC will disappoint in terms of the speed and size of easing ahead will be higher if inflation remains sticky, making the Thursday report even more critical than the disappointing labor report on September 5.

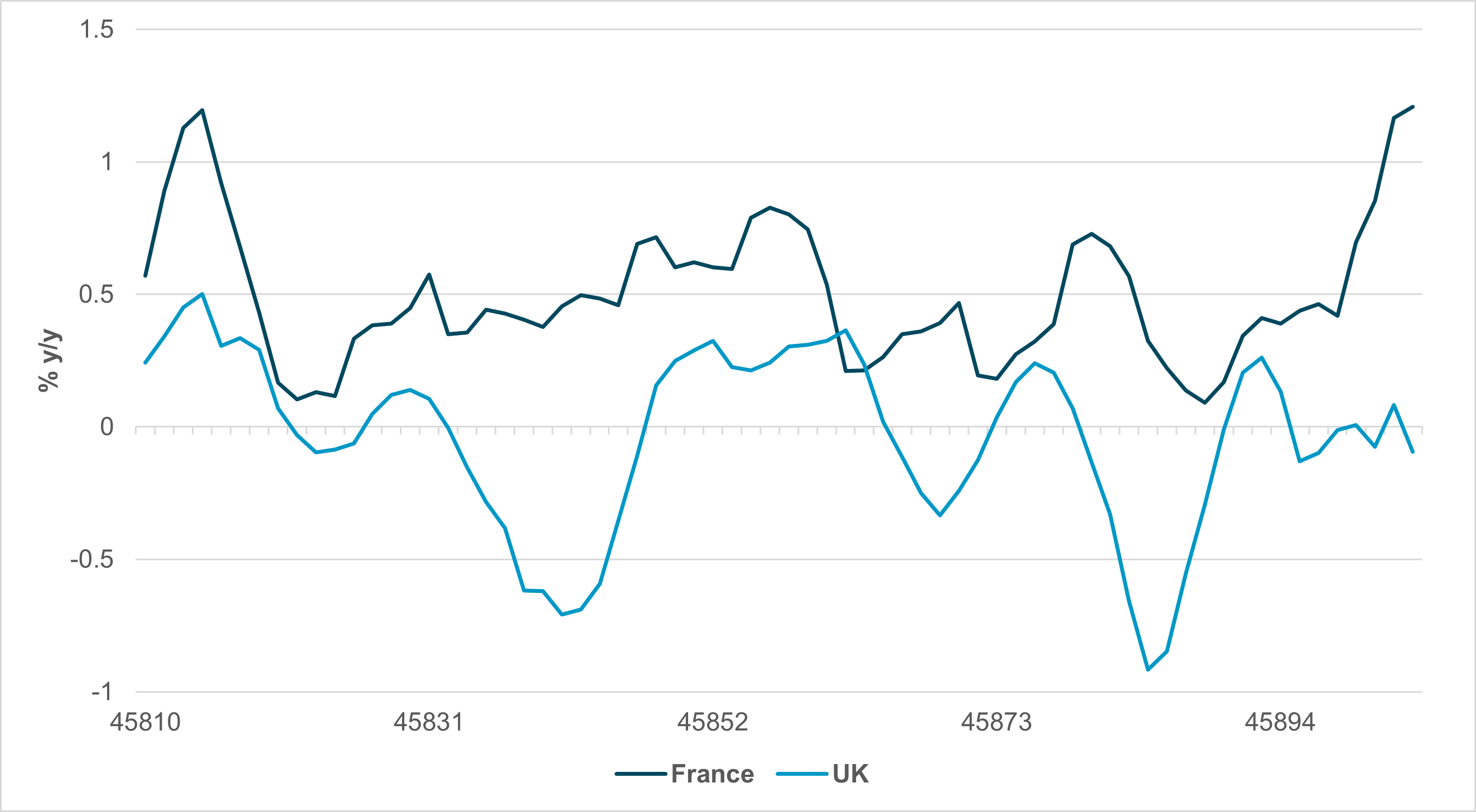

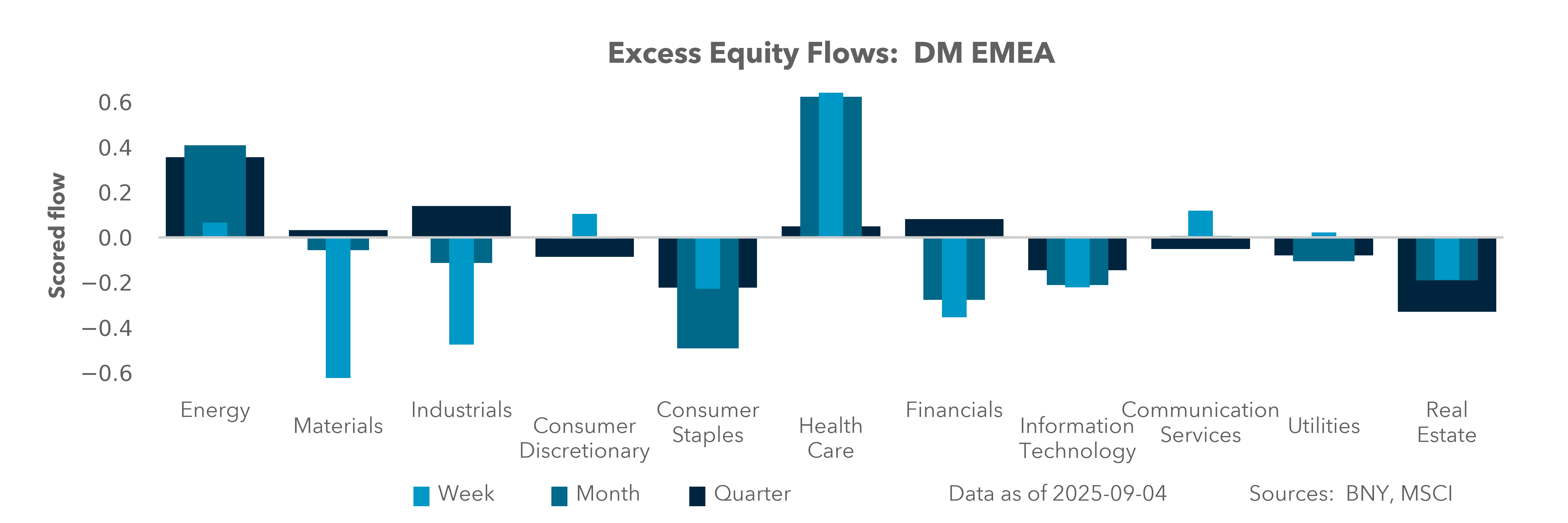

EMEA: ECB and Lagarde hoping for no surprises from Paris

EXHIBIT #3: CROSS-BORDER FLOWS OF U.K. AND FRENCH GOVERNMENT BONDS

Source:BNY

Our take: It has been quite the week for European bond markets, but risks are far from over across both sides of the English Channel. On Monday, French Prime Minister Bayrou faces a confidence vote, which he is widely expected to lose. There are several paths President Macron can choose thereafter, but we doubt he will risk fresh elections, and the search for yet another compromise candidate will continue. Developments in Paris will likely overshadow the ECB decision itself, which is not expected to be suspenseful as most Governing Council members appear comfortable with current policy settings. Current inflation risks seem adequately balanced, with only Governing Council member Simkus stating that a cut can be discussed in October. Realistically, a poor run of inflation numbers toward Q4 will pave the way for a move in December, assuming exogenous factors don’t tighten financial conditions excessively. Eurozone politics is one such risk – and President Lagarde herself acknowledged last week in an interview that the fall of any Eurozone government would be “worrying,” but the ECB does have the tools available for contingencies. Outside the Eurozone, slow progress is being made with the U.S. on the details surrounding a trade deal, but if the U.S. economy itself begins to show further strain and the Fed’s easing path accelerates well beyond what is currently priced, we believe the ECB may need to recalibrate, as financial conditions through the currency channel will move beyond prior assumptions.

Forward look: The updated September ECB staff projections will contain new currency assumptions in their scenario analyses. We expect the central tendency to move from 1.11–1.12 in the June projections to around 1.15–1.16, but with minimal impact on the inflation path for now. However, the margin for error will be increasingly tight as external demand continues to soften, and we do not see scope for further adjustments which would signal greater tolerance for currency strength. President Lagarde will also likely face questions over reaction functions to further volatility in sovereign debt market, and whether their balance sheet roll-off process requires a review – a process which the ECB conducts every cycle, but normally any material shifts are highlighted in advance. Unlike the U.S., there isn’t a liquidity or financial stability aspect to the current moves in bond markets and European money markets are behaving normally. A sudden shift in quantitative tightening may result in political complications, which the ECB will be keen to avoid unless absolutely necessary. Meanwhile, the U.K. also faces ongoing political stress as the Labour Party’s leadership team and executive operations face comprehensive changes in light of last week’s developments. We believe an opportunity may arise for a policy reset, and as the Autumn Budget has been pushed back to the end of November, there is enough time to come up with a credible path to meet funding shortfalls, and spending cuts will need to be a part of that particular discussion. Our data show that cross-border interest in gilts is lacking relative to OATs (Exhibit #3), but both markets are still seeing good inflows despite recent uncertainty. Any additional risk premia should be reflected in a weaker currency rather than sovereign spreads, especially as the BoE and ECB will both likely stay put in September.

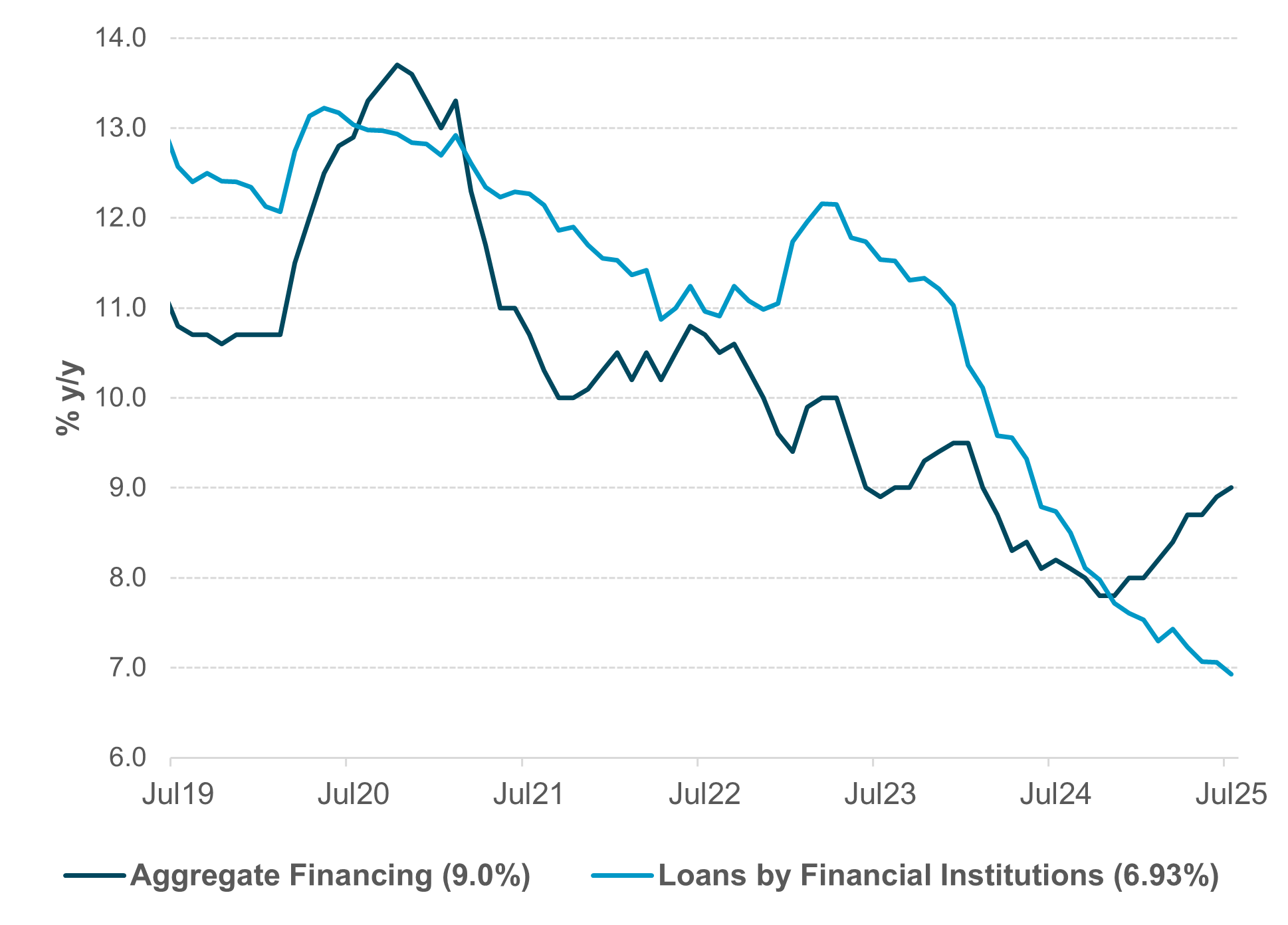

APAC: China credit and loans, South Korea bank lending and Japan Q3 BSI in focus

EXHIBIT #4: DIVERGENCE BETWEEN CHINA CREDIT GROWTH AND BANK LOANS

Source: BNY, Bloomberg

Our take: In the Asia-Pacific region, the focus this week will on China exports and trade, credit and financing data, and August inflation; Japan Q3 BSI business conditions; and South Korea August bank lending to households as well as the first ten day of exports for September. Other data releases include Taiwan August exports, Malaysia July industrial production, Thailand and Indonesia consumer confidence, Philippines unemployment rates, India August CPI, and FX reserves data from India, Indonesia and Singapore. China August credit data will be closely scrutinized given the increasing dislocation between aggregate financing, which was predominantly by government and local government bonds issuance, and loans by financial institutions. We will be paying extra attention to loans by financial institutions as a gauge of domestic sentiment. July loans by financial institutions declined by CNY 49.9bn, the first contraction since July 2005. Domestic loans to households dropped by CNY 489bn, with short-term loans down CNY –383bn and medium-to-long term loans lower by CNY –110bn, indicating that borrowers are reluctant to borrow and are choosing to pay down debt instead. China August headline CPI is likely to remain low, dragged down by lower food prices, but services inflation could see upside momentum. July services inflation was 0.5% y/y, up from –0.4% in February 2025. Elsewhere, export data from China and South Korea indicate a possible fading of front-loading activities, while Taiwan exports are likely to be supported by strong demand for semiconductors. Taiwan July exports stood at 42% y/y, with information & communications exports coming in at a stellar 87% y/y.

Elsewhere, South Korea will release figures for August bank lending to households. Strong demand for loans on top of already high levels of household debt is an increasing concern, one that is becoming a factor in the Bank of Korea’s policy decisions. Japan Q3 BSI will serve as an important input for the Bank of Japan’s policy decision next week. BSI for large manufacturing firms and large non-manufacturing firms declined in Q2 to –4.8 (Q1: –2.4) and –0.5 (Q1: 4.1), respectively, weighed down by the impact of tariffs. It remains to be seen whether the U.S.–Japan trade agreement announced in July (and signed in September) will turn sentiment around.

In Australia, August business confidence and September consumer inflation expectations will be closely watched following the Reserve Bank of Australia’s hawkish comments on private-sector growth.

Forward look: Asian currencies have been trading in a tight range since August, moving less than 1% between their monthly highs and lows, the narrowest band since July 2024. Markets may be due for a breakout depending on catalysts, whether that’s a key FOMC meeting next week or Chinese macro data and asset evolution in the near term. Indeed, China’s sharp injection of liquidity, with CNY 1,000bn in outright reverse repo operations with a 3-month tenor, is likely to continue to be supportive of the domestic equities market. We remain positive on the Shanghai Composite even though it suffered its biggest weekly loss last week since mid-April 2025. Renewed foreign interest in Chinese equities is the new driver of the appreciation of Chinese yuan. The return of foreign investors can be seen in renewed buying momentum in the Taiwan and South Korea equities markets. Elsewhere, the main focus is on the high-yielding Indian rupee and Indonesia rupiah. USDINR reached an all-time high last week on the back of concerns about the 50% tariff rate and the potential negative fiscal impact following the latest Goods and Services Tax (GST) cut in India. Domestic unrest that began last week has subsided somewhat but lingering concerns remain. USDIDR remains vulnerable to the upside, but so far has been well managed by active Bank Indonesia smoothing activities.

U.S. jobs data, global political tensions and rising debt burdens have unsettled markets, driving volatility and curve steepening. Investors now expect more Fed cuts, but doubts remain about inflation and whether easing alone can stabilize growth. In the U.S., heavy corporate bond issuance has been absorbed, yet credit risk looms as long-term yields rise. Europe faces political stress from France’s confidence vote and the U.K.’s fiscal challenges, while the ECB watches inflation and sovereign volatility carefully. In Asia, China’s weak loan growth, Japan’s softening business sentiment and South Korea’s household debt add to concerns, making inflation and upcoming central bank decisions key market drivers. The risk mood has flipped for markets, with bonds, gold and the focus on central bankers and their ability to provide stability all key elements. Gold’s rise and oil’s decline reflect more than geopolitical concerns, as some worry that all fiat currencies face debasement risks in a slowing global economy.

Central bank decisions

Chile, Banco Central de Chile (Tuesday Sep 9) – The BCC is expected to pause policy, holding its rate steady at 4.75%. In July 2025, consumer prices rose 0.9% m/m – well above expectations – and annual inflation reached 4.3%, up from 4.1% in June, exceeding the upper bound of the 2%–4% target range, driven by higher electricity, housing and food costs. In response, the central bank cut rates by 25bp but emphasized that future decisions will hinge on the broader macroeconomic outlook and inflation convergence. The latest minutes reaffirmed flexibility and confidence that inflation will reach the 3% target over a two-year horizon, while preserving room for adjustment as needed.

Turkey, Central Bank of the Republic of Türkiye (Thursday Sep 11) – The TCMB is expected to continue easing – but with caution. In August 2025, annual inflation eased to 32.95%, down from 33.52% in July, while monthly inflation rose to 2.04%, driven by food and services. In its August Inflation Report, the bank introduced interim targets of 24% by end-2025, 16% by end-2026, and 9% by end-2027, reinforcing its commitment to a disinflation path. Governor Fatih Karahan emphasized that monetary policy would remain tight and data-dependent, noting upside risks from administered prices. The policy rate was lowered to 43% in July, and officials have stated that the pace of cuts will be carefully calibrated. With inflation decelerating but remaining well above target, the next move is likely to be a measured reduction, allowing flexibility while sustaining disinflation momentum.

Eurozone, European Central Bank (Thursday Sep 11) – The ECB is broadly expected to keep rates unchanged at 2%. Despite our concerns that the euro’s valuations remain excessive and not conducive to price stability, most ECB members are not concerned about these risks. Most survey data show that trends in output are improving but remain contractionary. The latest German factory order figures should be another warning to the ECB that external demand will be challenging for the rest of the year. We expect President Lagarde to be queried on the situation in France as the confidence vote will be over before the meeting itself. For now there does not appear to be any need to put emergency facilities on standby as spreads are well-behaved. We still see the need for one more cut by year-end.

Peru, Banco Central de Reserva del Perú (Thursday Sep 11) – The BCRP is expected to hold its reference rate at 4.50%. In July 2025, consumer prices rose 0.23% m/m, with annual inflation at 1.69% – well within the 1%–3% target. Inflation expectations for 12 months dropped to 2.2%, and core inflation (excluding food and energy) is expected to remain near 2%. In its August statement, the bank noted global uncertainty and heightened financial volatility but maintained its rate for the third consecutive month. This cautious stance reflects balanced risks amid stable inflation, reinforcing that policy will adjust only as new data warrants.

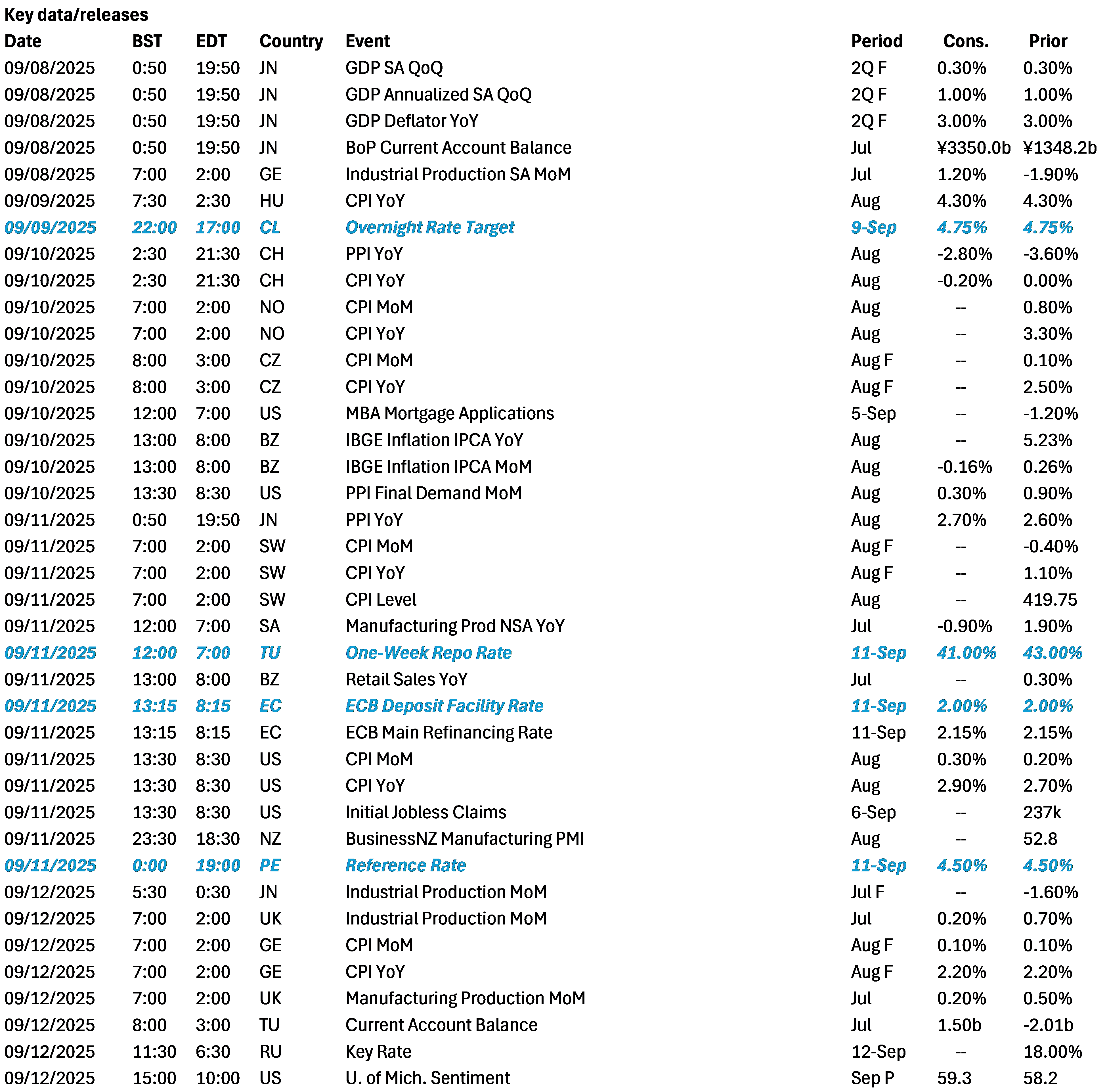

Data Calendar

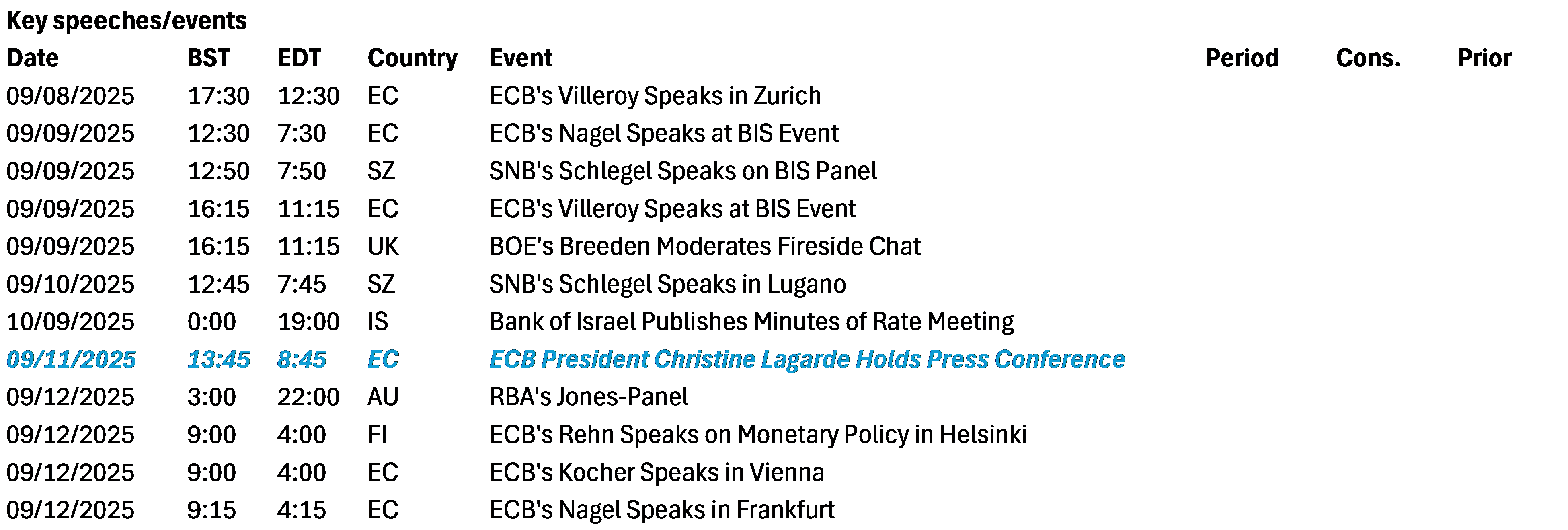

Event Calendar