May Day

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 11 minutes

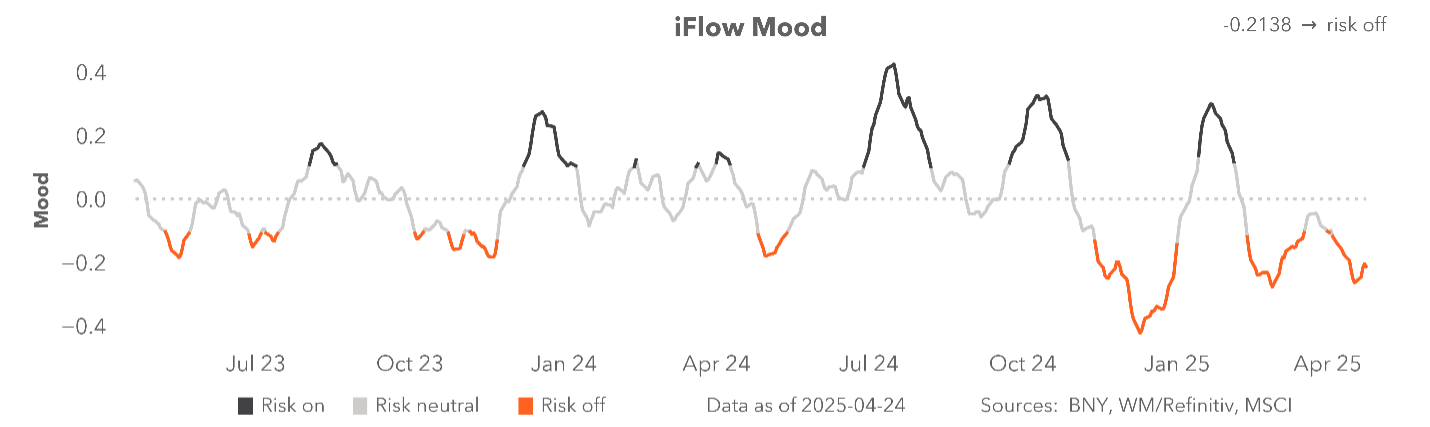

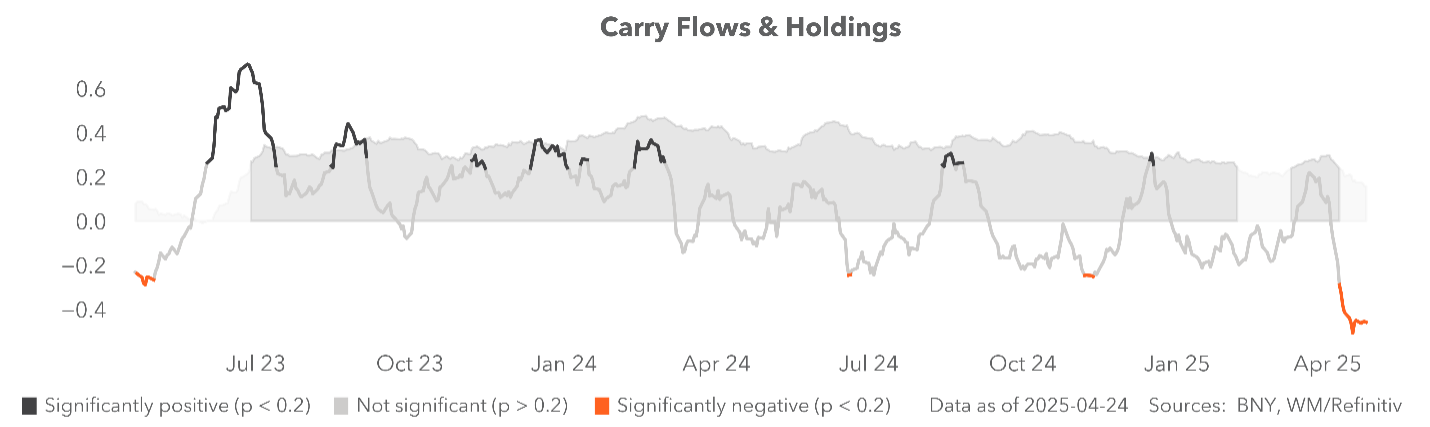

April 30 will be the one hundredth day of U.S. President Trump’s second term. He has seen a tumultuous market and public reaction to his three-legged policy push for growth using tariffs, taxes, and deregulation. The polling suggests he is losing 7% of the public support. 40% approve of his performance, while 59% disapprove of his performance and tariff policies. So far, the Q1 earnings reports have met the 7% S&P 500 average expectations but with more cuts to Q2 outlooks. The focus in the week ahead will be around the big tech earnings beating modest expectations and their upcoming spending plans. The U.S. hard economic data continues to beat the soft surveys on growth and inflation. Markets will be tested by the U.S. ISM and jobs report next week. Global Investors prepare for worst-case scenarios with short holdings of U.S. equities, short USD and neutral fixed income. European optimism continues with ECB appearing more dovish, and Asia seeing hope in China/U.S. trade discussions. The last week delivered relief, as IMF meetings soothed fears about limits in U.S. isolationism and talks over lowering tariffs gained momentum. Our iFlow Mood index is bottoming and the Carry index is in an extreme negative state– suggesting nascent positive risk sentiment for investors.

There were two questions most asked by investors this week:

These questions will be answered in the week ahead, as we see a short-term bottom being put into markets, barring any surprises from earnings, elections, or economic data.

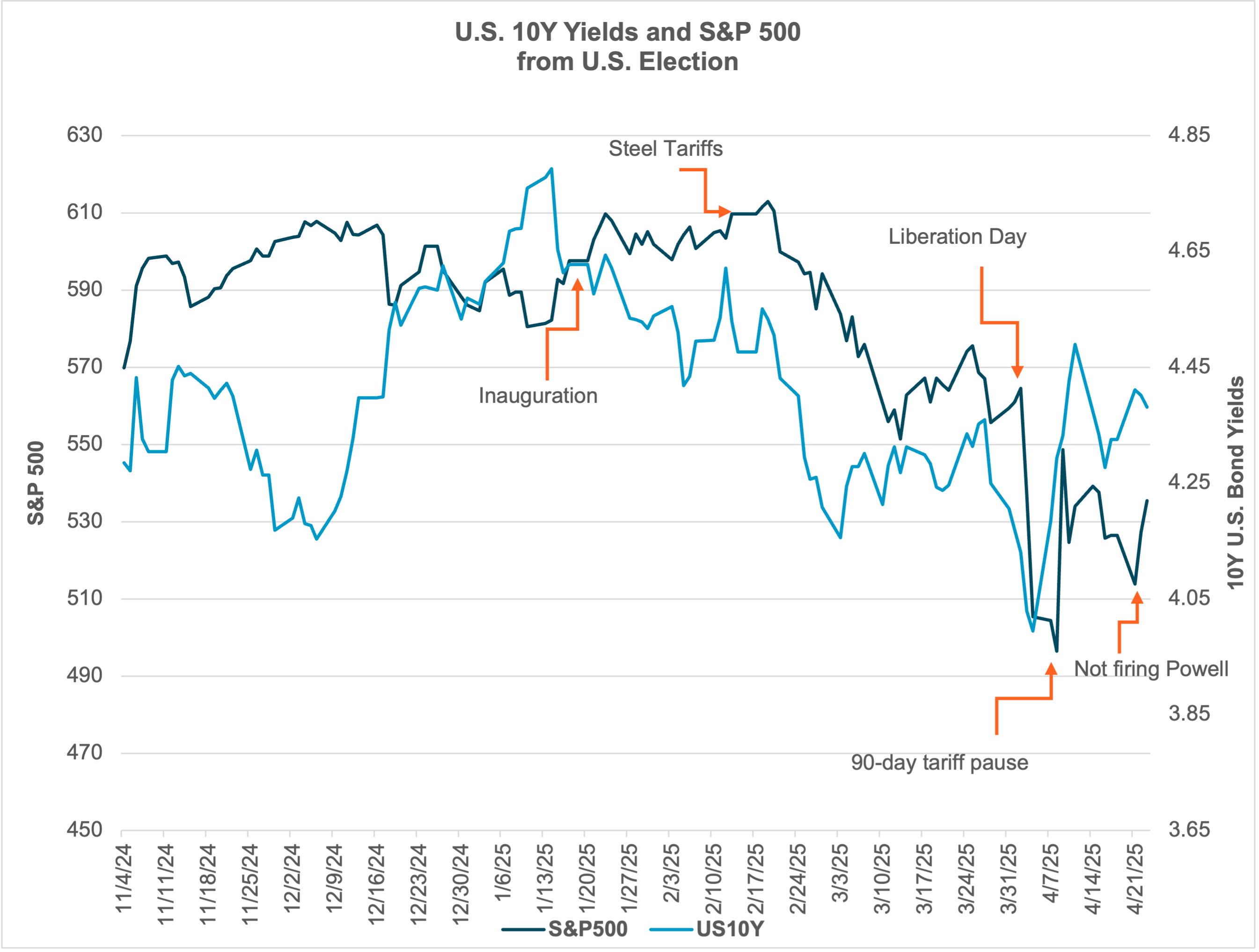

EXHIBIT #1: NEW FINANCIAL CONDITIONS LIMIT S&P 500, 10Y YIELD 4.50%

Source: BNY, Bloomberg

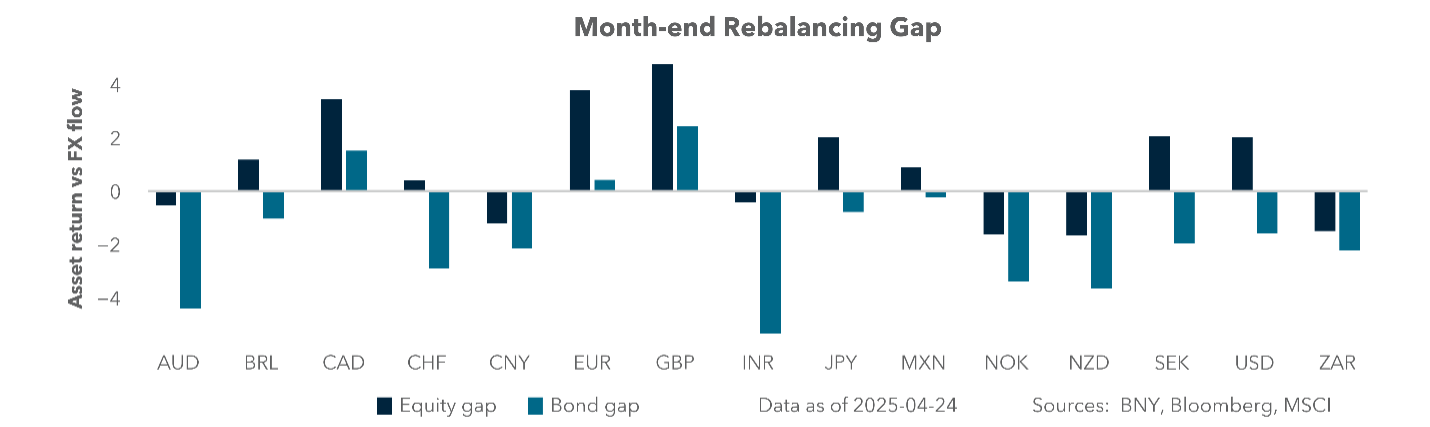

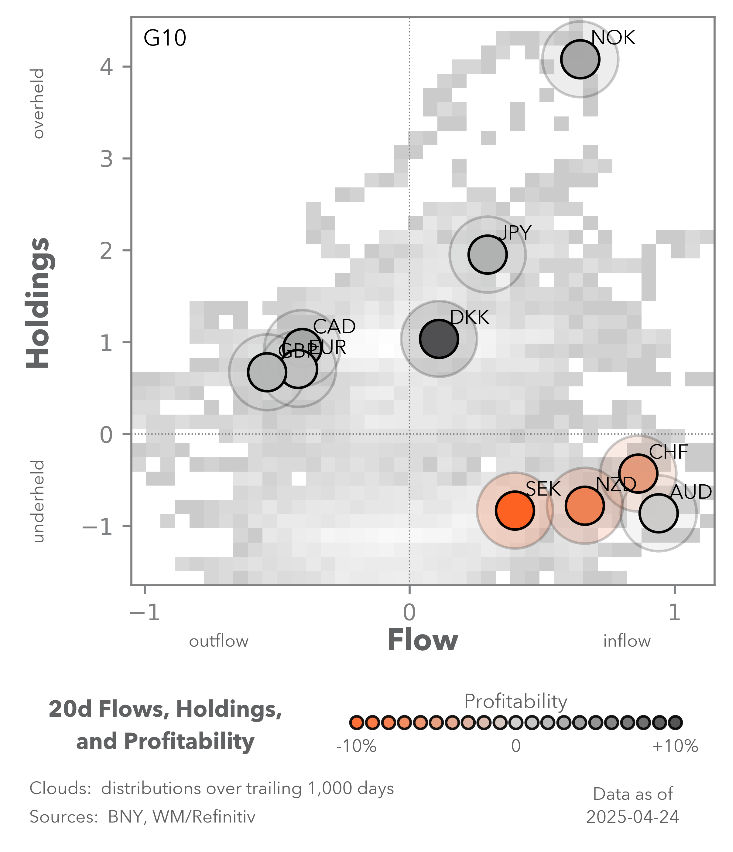

Our take: The biggest surprise from April was in U.S bond moves rather than equities. This makes month-end rebalancing interesting as investors are underweight in both bonds and stocks. The FX markets will be watching EUR, GBP, CAD, SEK, and the USD for demand. The bigger question is around ranges with the financial conditions index, which fell in April = then rebounded after the 90-day pause in reciprocal tariffs on April 9. This move did not sustain, and Trump reversed his threats to fire FOMC Chair Powell. These events indicate that the bond and stock markets are influencing the administration's decisions, though the situation is complex and influenced more by market fragility and liquidity than by specific levels.

Forward look: Investors are waiting to buy a dip. Rising cash positions and significantly underheld equity positions are set up for a rally back in for the U.S. Both domestic and cross-border holdings in the U.S. are 5-7% below the long-term average. It is difficult to define the dip due to Q1 earnings and volatility blocking value models. The role of the Trump Administration in the week ahead should not be underestimated as any significant progress on trade talks will dominate all other factors.

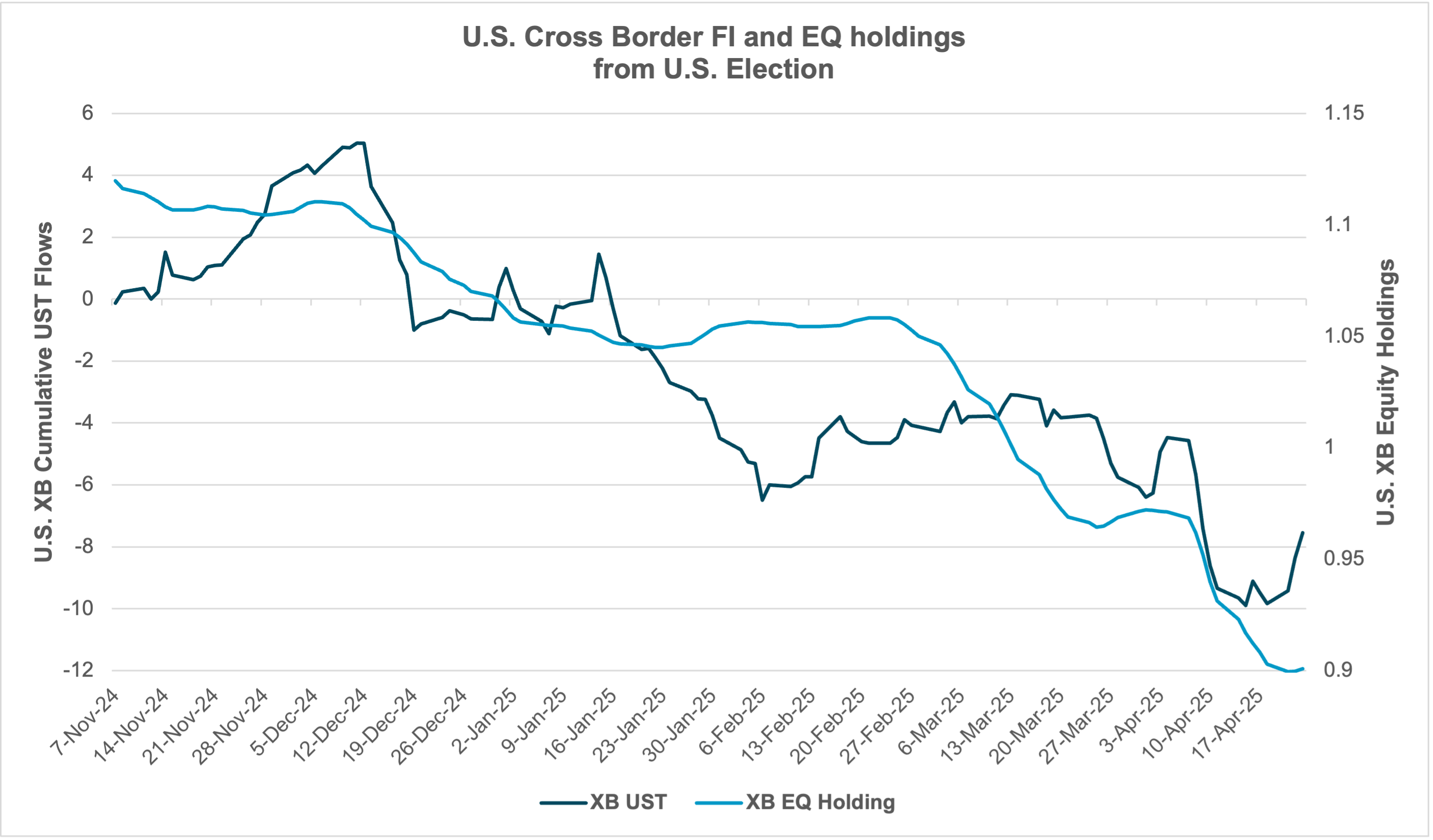

EXHIBIT #2: CROSS BORDER FLOWS INTO U.S. MARKETS RECOVERING FROM PREVIOUS DOWNHILL TREND

Source: BNY

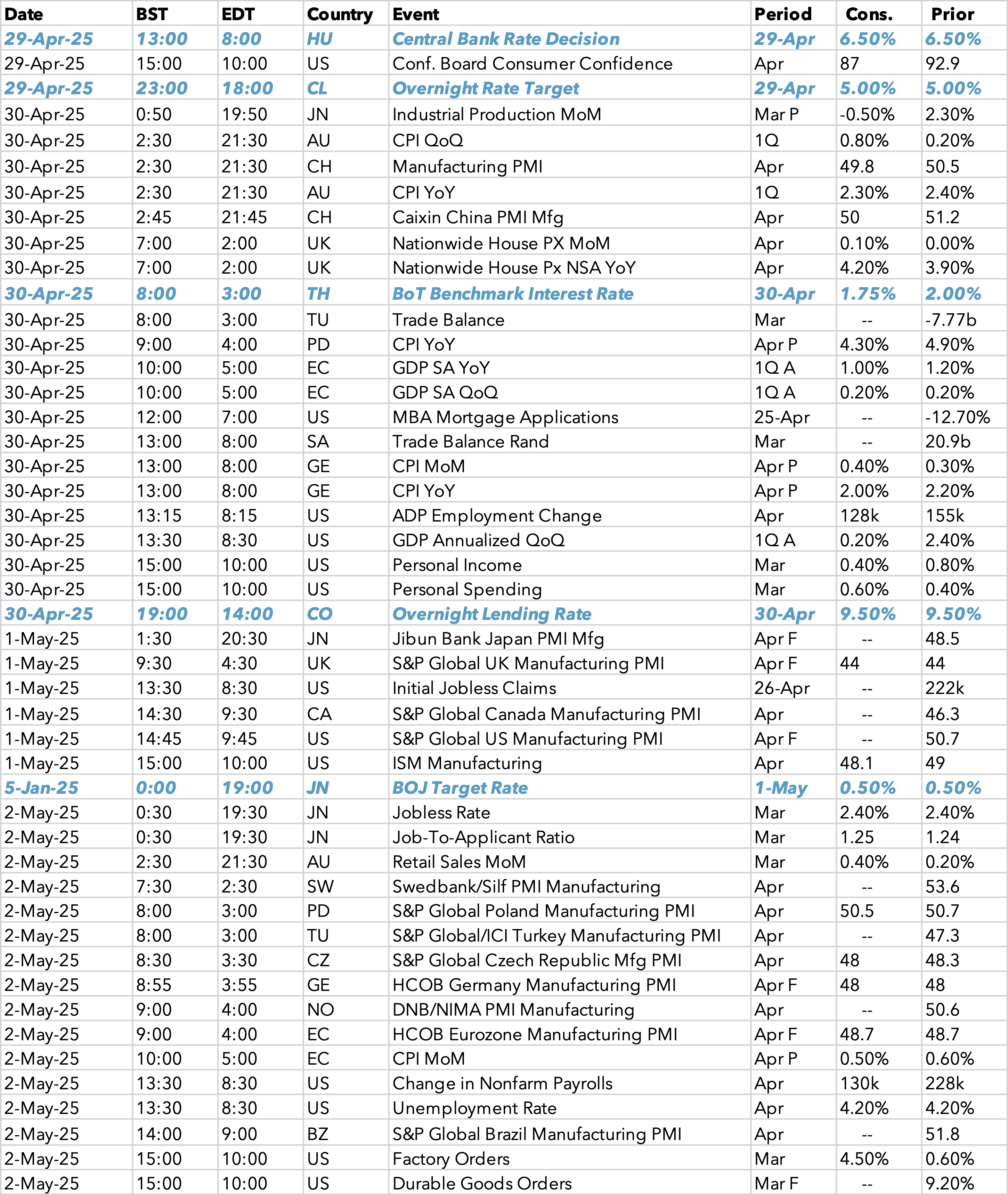

US: Labor report and ISM; Fed in blackout

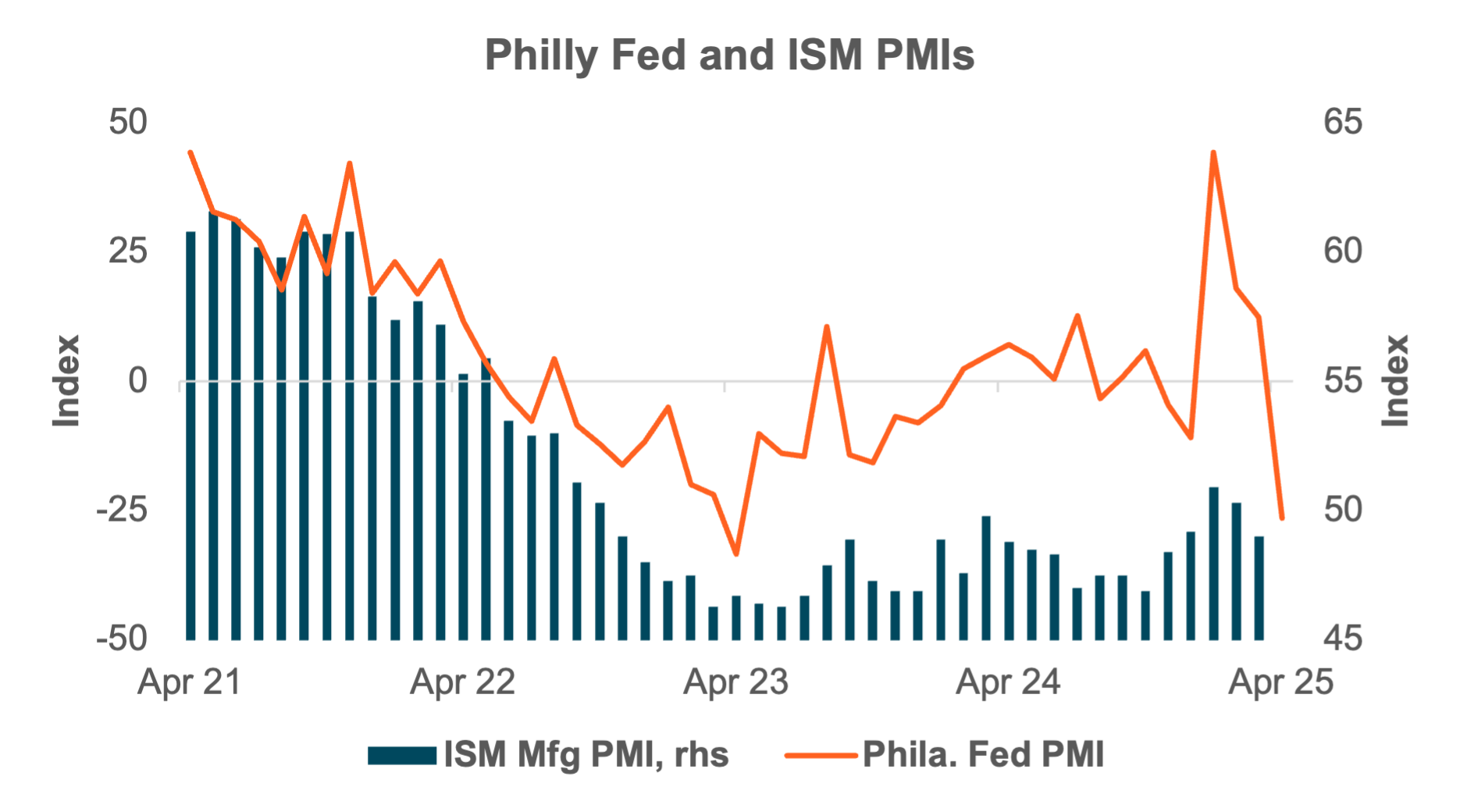

It is jobs data week, with the usual appetizers (JOLTS, ADP) culminating in Friday’s NFP release. This could be the last decent jobs data week for a while. Payroll consensus is greater than 100k m/m, similar to last month’s average. The survey was conducted two weeks after Liberation Day, so firms may have slowed hiring, but haven’t stopped altogether. There is scant evidence from initial claims data, which have been stable, of an increase in layoffs. Thursday’s ISM Manufacturing survey could be more concerning, especially following the Philadelphia Fed’s index publication. It suffered its biggest decline since March 2020 at the onset of the pandemic.

EXHIBIT #3: BUSINESS SENTIMENT LIKELY TO SIGNAL PESSIMISM

Source: BNY Markets, Institute for Supply Management, Philadelphia Fed Manufacturing Survey

The Fed is on blackout, as cush labor data will likely be viewed as backward looking. We do not expect much reaction from markets unless there is a surprise outcome (weaker than 50k or over 250k), in addition to yet another week of tariff headlines.

EMEA focus on Ukraine deal; higher real rates favor EM EMEA duration

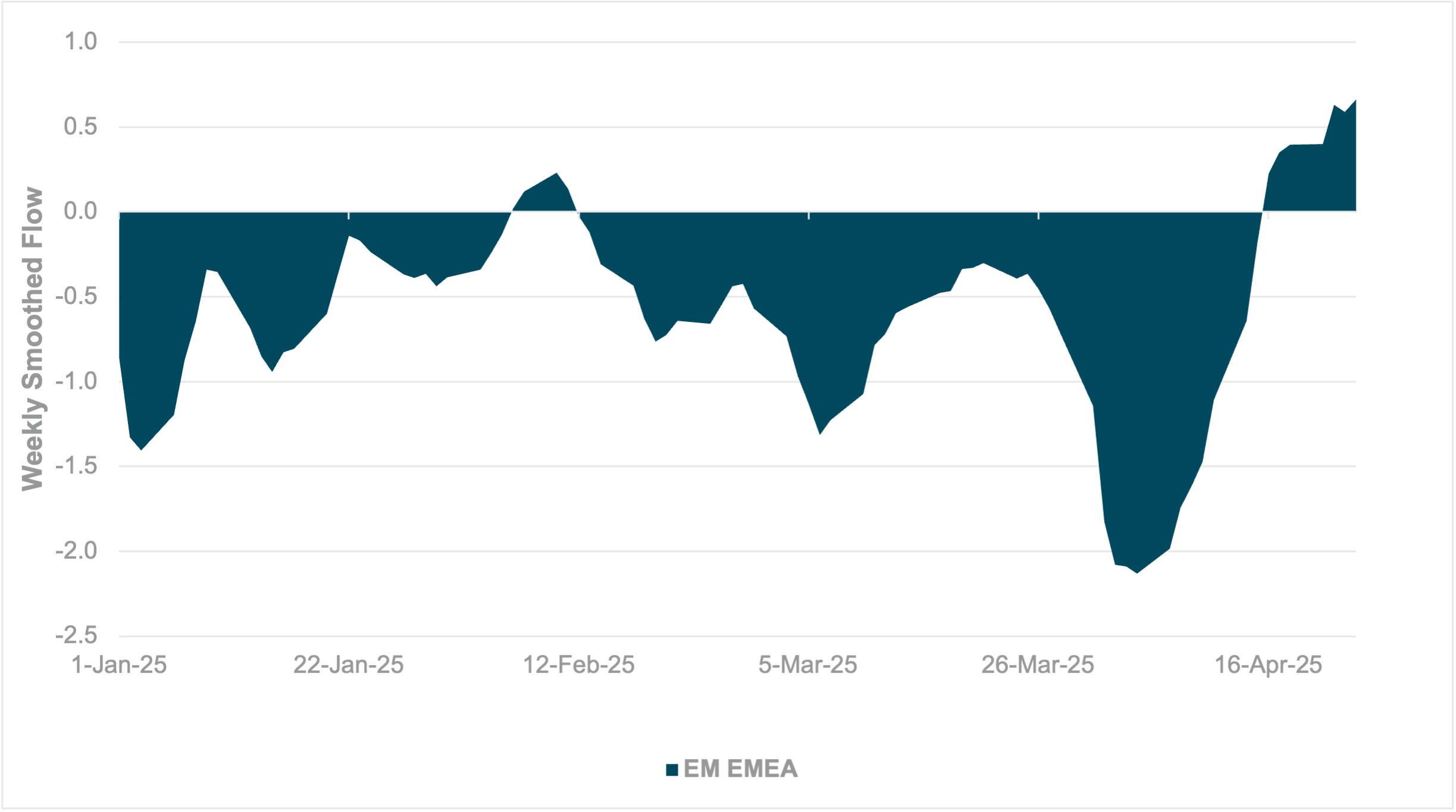

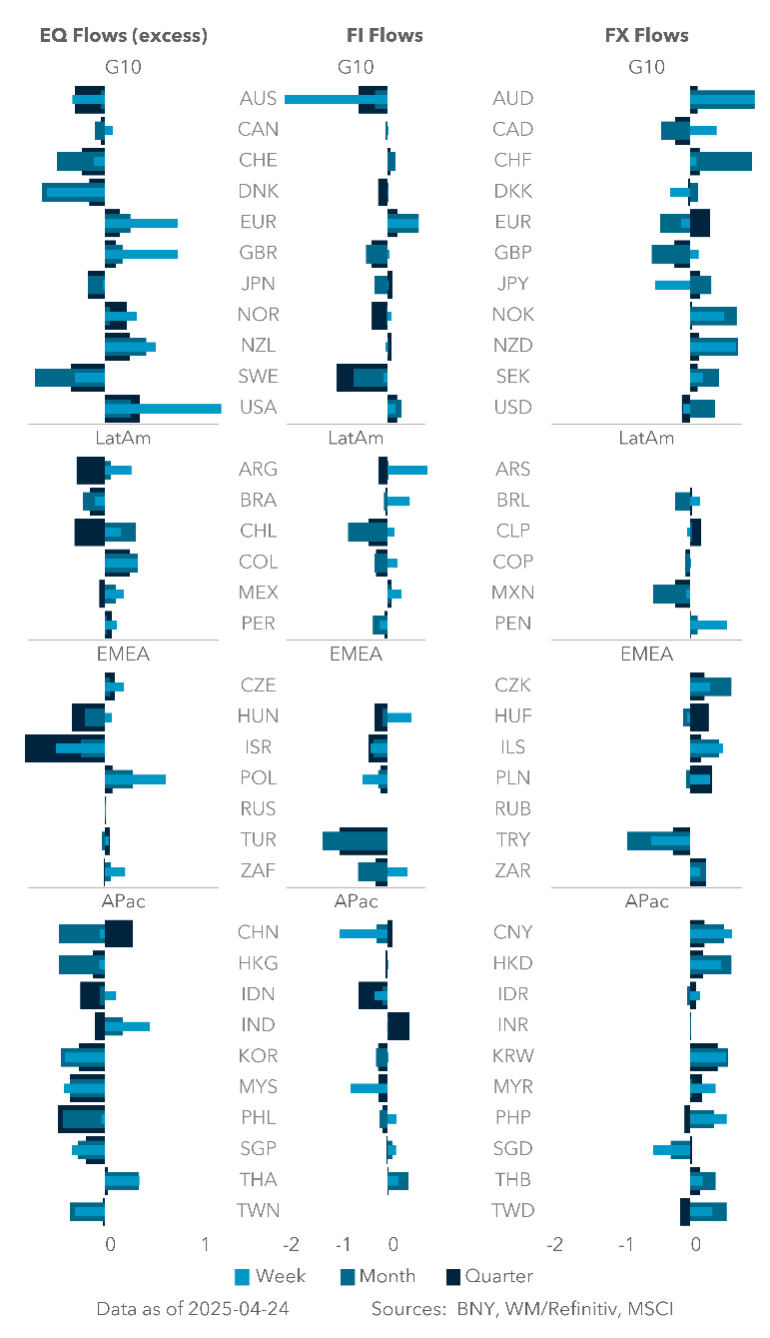

EXHIBIT #4: EM EMEA SOVEREIGN BOND FLOW

Source: BNY

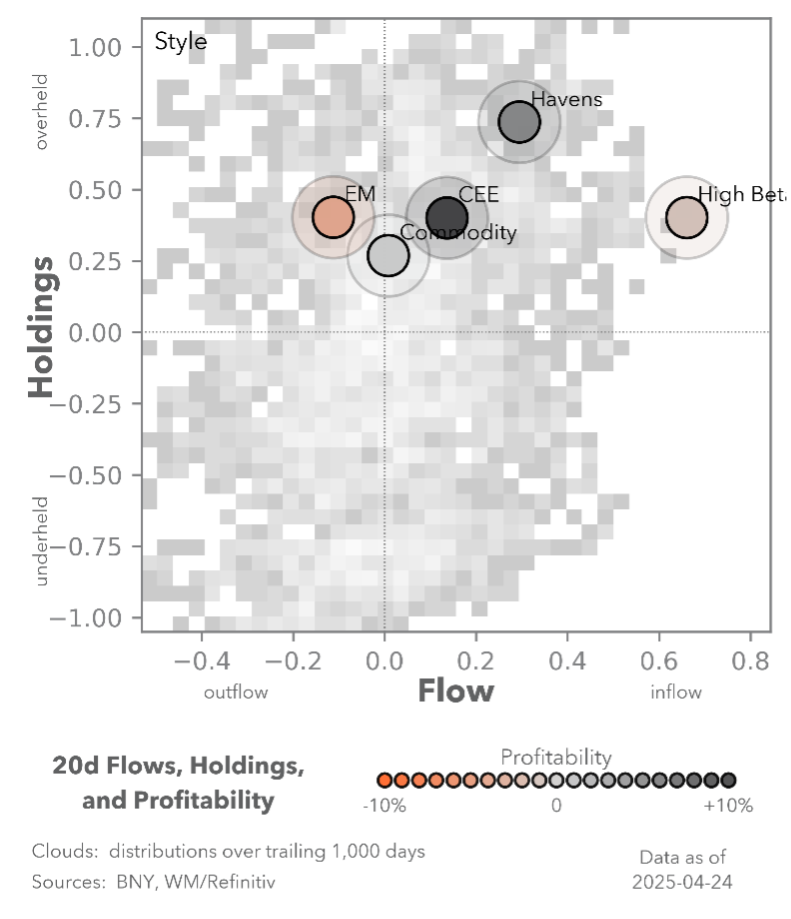

Our take: Our data shows that over the past week, flows into EM EMEA sovereign bonds have picked up strongly. Led by interest in Hungary and South Africa, interest in the region is the strongest year-to-date. Our data shows that liquidation of carry trades has hit extremes and show good prospects for a recovery, assuming the risk environment holds. While Latin America remains the preferred region due to high nominal yields, events next week heavily favor idiosyncratic support for EM EMEA duration as real rates continue to recover. This is a more sustainable proposition for long-term inflows from fixed income investors, instead of relying on short-term interest in FX carry. As global leaders gathered in Rome for Pope Francis’ funeral, reaching a settlement in Ukraine will be front of mind. Any progress there will help further reduce risk premia for CEE economies and Turkey, as the prospect of an end to supply disruptions is supportive of a secular shift lower in inflation expectations.

Forward look: Data and policy are proving supportive for duration in EM EMEA. The MNB decision on Tuesday is expected to leave policy unchanged. However, with headline inflation continuing to fall across EM, the MNB can afford a stronger easing bias. We suspect their view will mirror recent comments by Poland, where rate cuts – even up to 50bp – are possible if inflation continues to surprise to the downside. Meanwhile, the surprise concession by the South African Treasury on VAT has eased tensions within the Government of National Unity. Final resolution on the budget is expected in the week ahead, paving the way for renewed allocations into South African Government Bonds. Given the risk of recurring volatility, we expect FX ratios to remain high across EM allocations. Even so, the path ahead looks clear for significant recovery in what remains a crucial market for EM fixed income portfolios.

It is a quieter week in developed EMEA as central banks return from the IMF meetings with renewed focus on downside risks to their economies. The market is anticipating consecutive rate cuts from the European Central Bank, which would allow regional peers to act swiftly due to downside risks to growth. Our data points to a turnaround in franc flow and significant rebalancing pressure. This will help policy on the margins, as SNB President Schlegel warned that the country would “feel tariff fallout more than others.” Swiss President Keller-Sutter will report on her talks with U.S. administration officials in the week ahead as pharmaceutical tariffs loom. In the UK, upcoming local elections will be the first test for the Starmer Government since retaking power in last year’s general election.

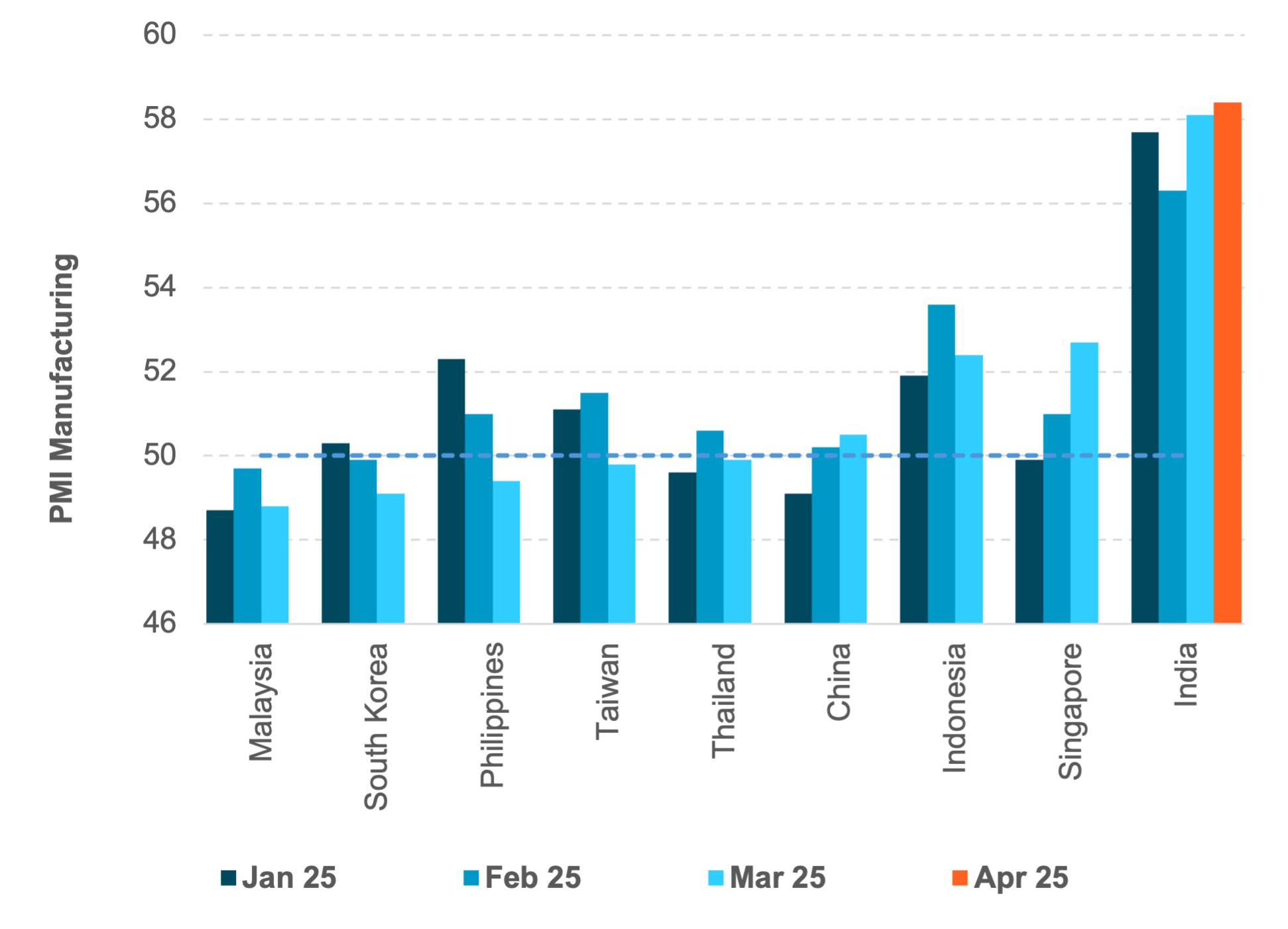

APAC PMIs to affirm tariffs related slowdown.

Our take: Labor Day means a shortened trading week in APAC, as China will be off for 5 days from May 1 to May 6. The key focus in APAC this week will be on the regional April Purchasing Manager Index (PMI) with special attention on China. Will China sentiment maintain a strong upward momentum, or will it crack under heightened tariff uncertainties and global growth slowdown? We will be looking at both the new order (March: 51.8) and new export order (March: 49.0) subcomponents within PMI manufacturing to assess the impact of U.S. tariff policies. For the non-manufacturing sector, the service business activities subcomponent has been hovering just above the neutral fifty reading, lagging the recovery seen in China retail sales. We will be watching to see if construction business activities can sustain the recent upward trajectory from 49.3 in January to 53.4 in March.

Forward look: Thailand, Taiwan and the Philippines dropped into a contractionary zone in March, so the market will be bracing for further sentiment deterioration. Surprises in negative domestic data and limited progress on U.S. tariff negotiations could see regional PMI stay depressed in the month ahead, which might weigh on the Q2 growth prospect. Indonesia PMI is one of the best in the region at 52.4 compared to most of ASEAN, namely Thailand (49.9), Malaysia (48.8) and Philippines (49.4). On-going downside growth, inflation risk and high real interest rates call for further monetary easing in the region.

EXHIBIT #5: DOWNSIDE PRESSURE ON APAC PMI KEY

Source: BNY, S&P Global

Elsewhere, South Korea’s April exports data will be closely watched after a poor first 20 days report at -5.2% y/y. The risk is on the downside, which does not bode well for export growth in the rest of the region. Thailand’s March manufacturing production should serve as insight into the latest Bank of Thailand growth forecast. South Korea and Indonesia will release April CPI. South Korea is likely to drift lower (March 2.1%) while Indonesia headline CPI (March: 1.03% y/y) is likely to rise on the end of electricity rate discount program as of March. Lastly, Australia’s March and Q1 trim mean CPI, exports and retail sales will be key inputs into RBA policy decisions at the end of May where market is pricing more than 25bp rate cut.

In terms of foreign equities flows, we have observed a divergence of sentiment, with positive net inflows in India and Taiwan and reduced selling pressure in South Korea and Indonesia. There is an interesting dynamic with foreign investors in Thailand where accelerated selling in Thai equities was accompanied by a greater magnitude of buying in fixed income complex. As for China, iFlow data showed persistent outflows in Chinese equities and CGB selling over the past two weeks. China’s “national team” absence in the market this week can be based on the CSI 300 ETFs flows.

The end of the month is always about rebalancing and rethinking risk. This April will be bigger than usual given the outsized volatility. We have seen a notable washout in risk across global markets. A bounce back in May makes sense, but ongoing doubts about monetary and fiscal policy and tariff responses will have an impact. Q1 earnings, like the upcoming jobs report, are seen as backward looking but the underlying outlooks are fragile. Any guidance matters for how the world balances between growth and inflation risks. The set up for a bottom in equities and the USD is in play. The ability for it to extend requires good news but not too much as the financial conditions require a larger response after the financial scaring done in April.

Central bank decisions

Hungary MNB (Tuesday, April 29) – The National Bank of Hungary is expected to keep its benchmark interest rate unchanged at 6.50% at next week’s meeting. Inflation slowed to 4.7% in March from 5.7% in February, driven mainly by lower fuel prices, although food and services costs remain sticky. Despite this progress, the MNB raised its 2025 inflation forecast to a range of 4.5%–5.1%, reflecting concerns over a weakening forint and the impact of new global tariffs. Core inflation pressures, wage growth, and geopolitical risks in Europe also heavily influence policymakers’ considerations. Governor Matolcsy has emphasized that maintaining tight policy is essential to anchor expectations and prevent second-round inflation effects. Given the external environment and fragile recovery prospects, markets are confident the MNB will continue its cautious approach, but given NBP is openly flagging a cut and headline inflation set to fall further, MNB will likely show a stronger easing bias in future decisions.

Chile BCC (Tuesday, April 29) – The Central Bank of Chile is widely expected to leave its benchmark rate unchanged at 5.0% next week. Inflation rebounded to 4.9% from 4.7% in March, led by core and headline items and leaving little room for cuts. Policymakers have previously signalled that although inflation has moderated in general, the path back to the 3% target remains uneven and vulnerable to external shocks. Chile’s economy is growing slowly, and uncertainty surrounding copper prices poses an additional risk to the outlook. The central bank recently emphasized its commitment to a “gradual and data-dependent” approach, suggesting that further easing is unlikely in the near term. Markets are pricing in a steady policy stance until there are clearer signs that inflation is sustainably returning to target without jeopardizing financial stability. Even though we see a pick-up in carry interest, with MXN, COP and BRL leading the way in LatAm, Chile’s rates are not favourable compared to peers.

Thailand BoT (Wednesday, April 30) – We expect a 25bp rate cut to 1.75% with downward growth revision. Despite the BoT February warning that the bar for the next rate cut is high, and the February rate cut is not an easing cycle, weakening growth profile, sluggish domestic equities (SET at -18% ytd) and the strong THB at +1.8% ytd, argues for a back-to-back rate cut. Note that Thailand inflation is back on a downtrend with headline inflation at 0.84% y/y. Business sentiment index is rising but has not translated to the recovery in manufacturing. One potential source of concern is the elevated USDTHB volatility.

Colombia BdlR (Wednesday, April 30) – Colombia’s central bank is set to hold its benchmark interest rate at 9.50% at next week’s meeting, underscoring limited easing capacity in EM at present. After surprising markets in March by pausing rate cuts, policymakers have stressed that inflation remains too high and too volatile to loosen policy just yet. March inflation eased to 5.09%, the lowest rate since October 2021, which could help open further policy space. However, fiscal uncertainty ahead of proposed tax reforms is also weighing on the central bank’s decision-making. Despite recent improvements in core inflation measures, external risks like U.S. monetary and tariff policy and commodity price swings have prompted caution. Board members have reiterated that their priority is anchoring inflation expectations around the 3% target. As a result, stability over early easing is preferable. iFlow suggests COP could benefit strongly from carry demand, which should help with the inflation path.

Japan BoJ (Thursday, May 1) – The Bank of Japan is expected to leave its benchmark interest rate unchanged at 0.5% following its April 30–May 1 policy meeting. Core inflation in Tokyo rose to 3.4% in April, marking the highest level in two years, with food prices and reduced energy subsidies driving the increase. However, growth risks are mounting. The IMF cut Japan’s 2025 GDP forecast to 0.6%, citing weaker exports due to new U.S. tariffs. Governor Ueda has stressed that while inflation remains above target, wage growth needs to become more sustainable before additional tightening. Policymakers are also concerned about potential disruptions to global trade and supply chains, which could further dampen Japan’s recovery. Markets now expects the BOJ to stay on hold for several months, waiting for clearer evidence of domestic resilience before contemplating further rate moves. In the near-term we see JPY being undermined by renewed carry interest after recent volatility in such positions.

Data Calendar

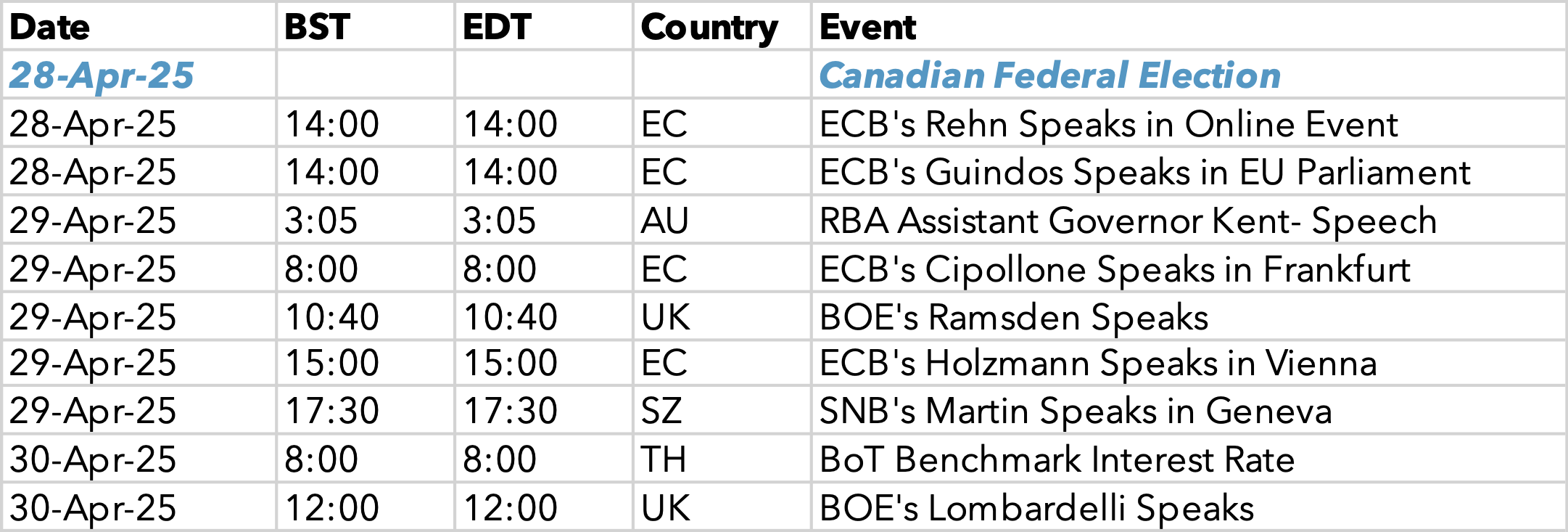

Event Calendar