Lambs and Lions

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 10 minutes

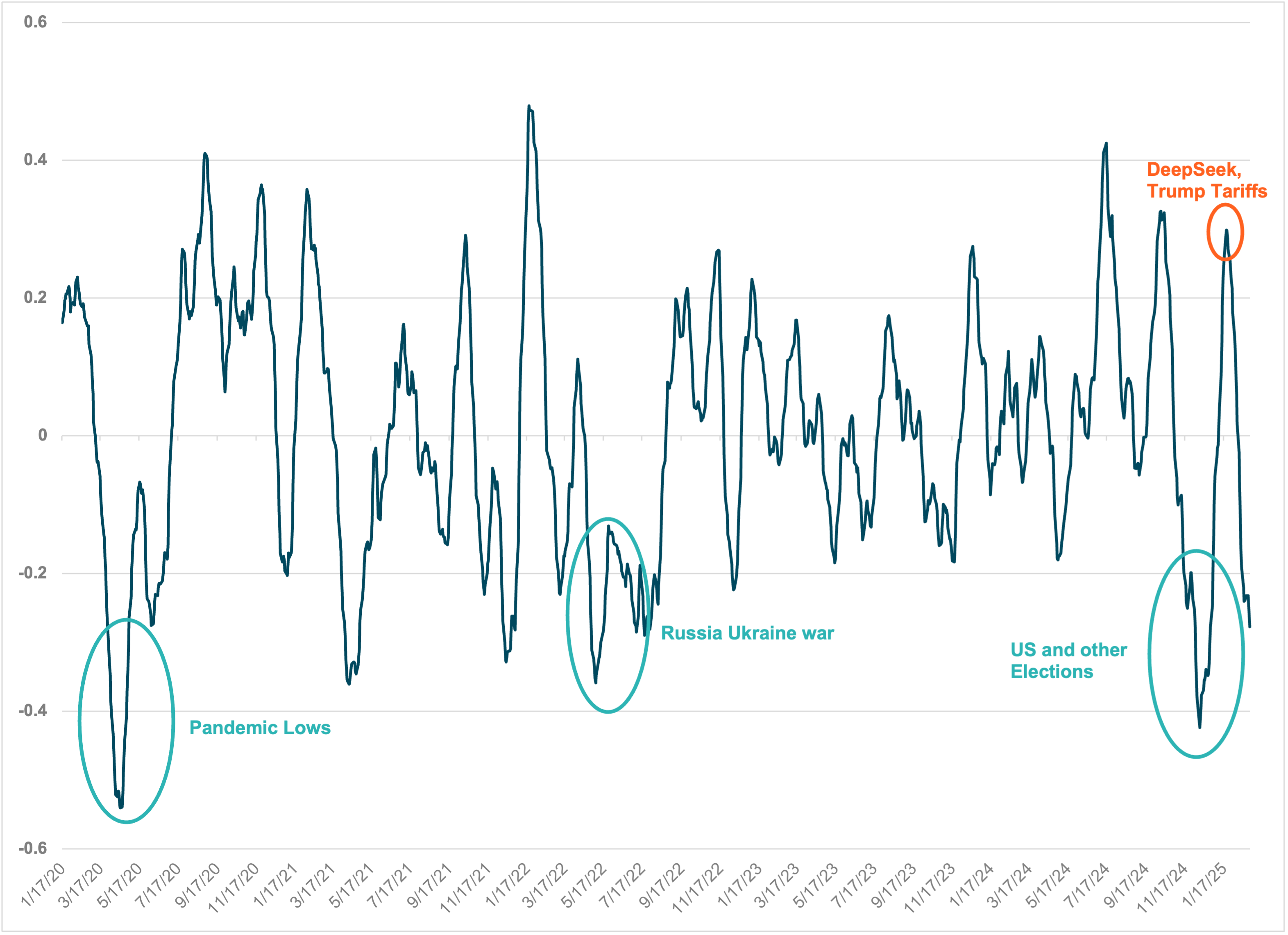

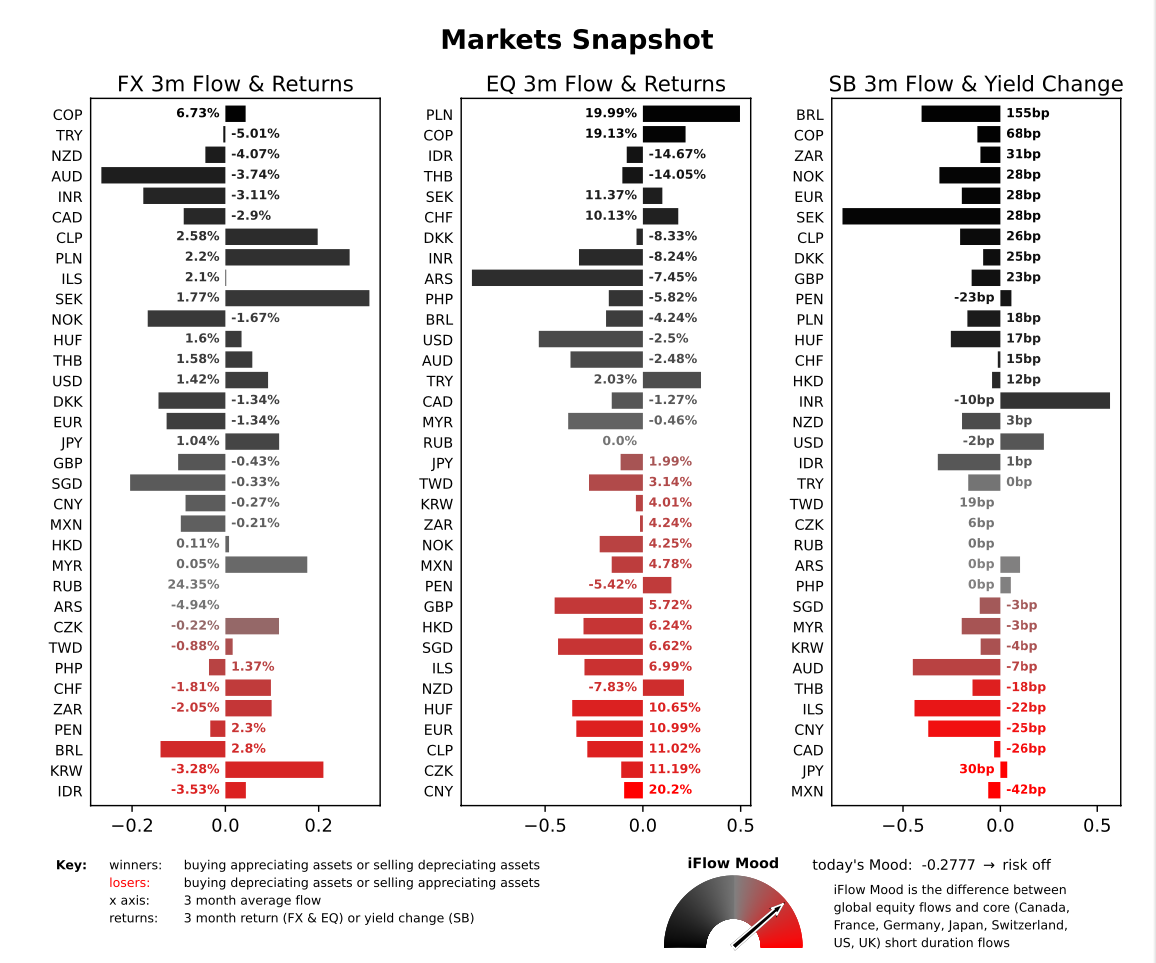

EXHIBIT #1: iFLOW MOOD INDEX

Source: Bloomberg, BNY

This week, markets will focus on trade policy developments, concerns over global growth, and key economic data, including global PMIs, U.S. ISM surveys, and the jobs report. Central banks are also in focus: the ECB is expected to cut rates by 25bp to 2.5%, Turkey’s central bank is likely to ease by 250bp to 42.5%, and Malaysia’s is set to hold steady at 3.0%. February saw a shift away from U.S. market dominance, with the Nasdaq falling 5%, the S&P 500 down 2.25%, and Japan’s Nikkei dropping 3.5%, while European and Asian markets outperformed. Euro Stoxx 50 gained 3.2% and Hong Kong’s Hang Seng surged 13.5%. In currency markets, the U.S. dollar has weakened 1.1% this year, while the Japanese yen is up 4% and the euro has risen 0.5%. As March begins, markets look vulnerable to volatility, with upcoming policy decisions and economic data likely to drive sentiment.

Tariffs

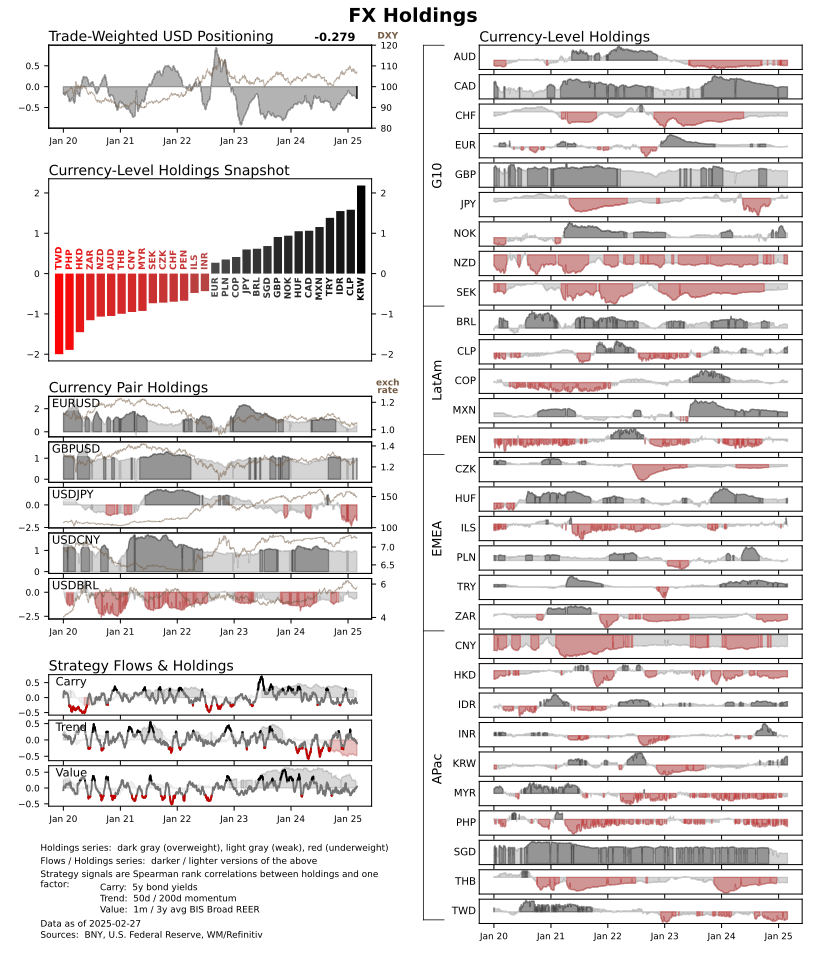

With the delay in tariffs expected at the start of this week, the USD fell to 106.12 lows on Monday and the dollar again tested the lows Wednesday. We saw dollar outflow in iFlow to match prices until tariffs returned to headlines on Thursday. The USD is up 0.7% on the week and back over 107.30 on the index. We expect more central bank reactions – lower rates, more USD upside – and further doubts about the March 4th, April 2nd deadlines.

G20 no communique: There was no consensus on how to deal with protectionism as the meetings in Cape Town, South Africa were skipped by US, China, Japan, Canada, India and Mexico. However, there is expected to be a bigger push to counter US tariff plans with EU leaders and others visiting Washington. The most notable comment around the G20 central bankers and finance ministers came from BOJ Ueda, stating “My impression is that there are great uncertainties — and there are many of them,” including US tariff measures and the reaction to them. Ueda told reporters: “We will make a decision on monetary policy by assessing how they will affect our outlook for Japan’s economy and inflation — the same approach we have taken.”

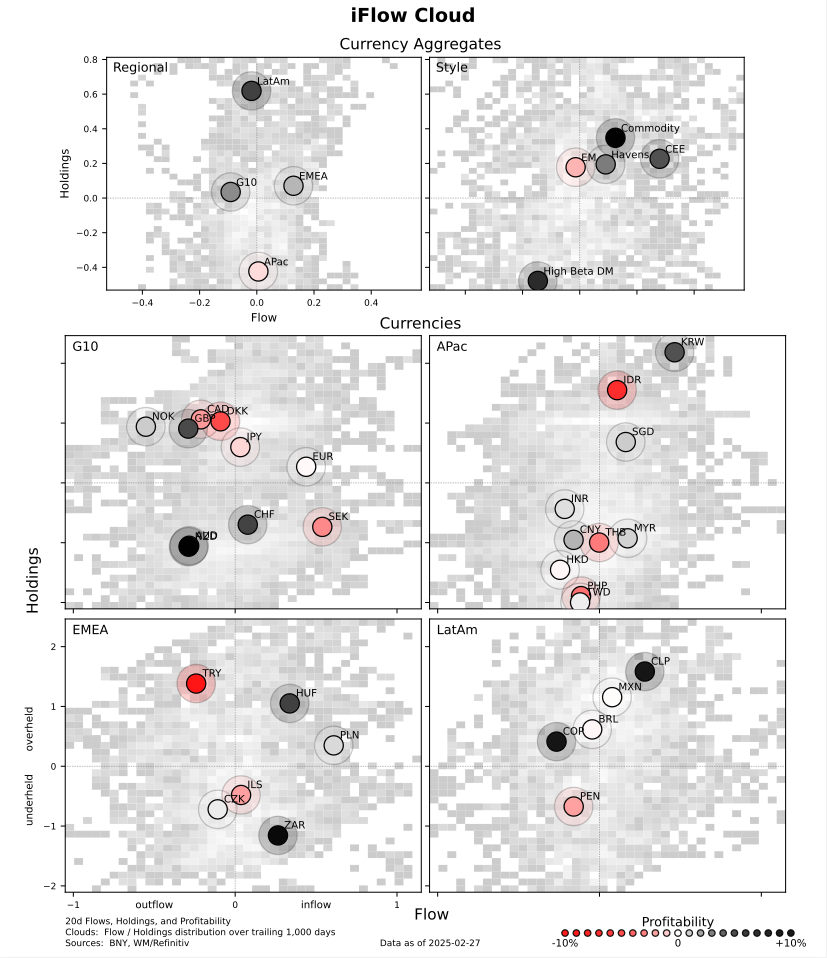

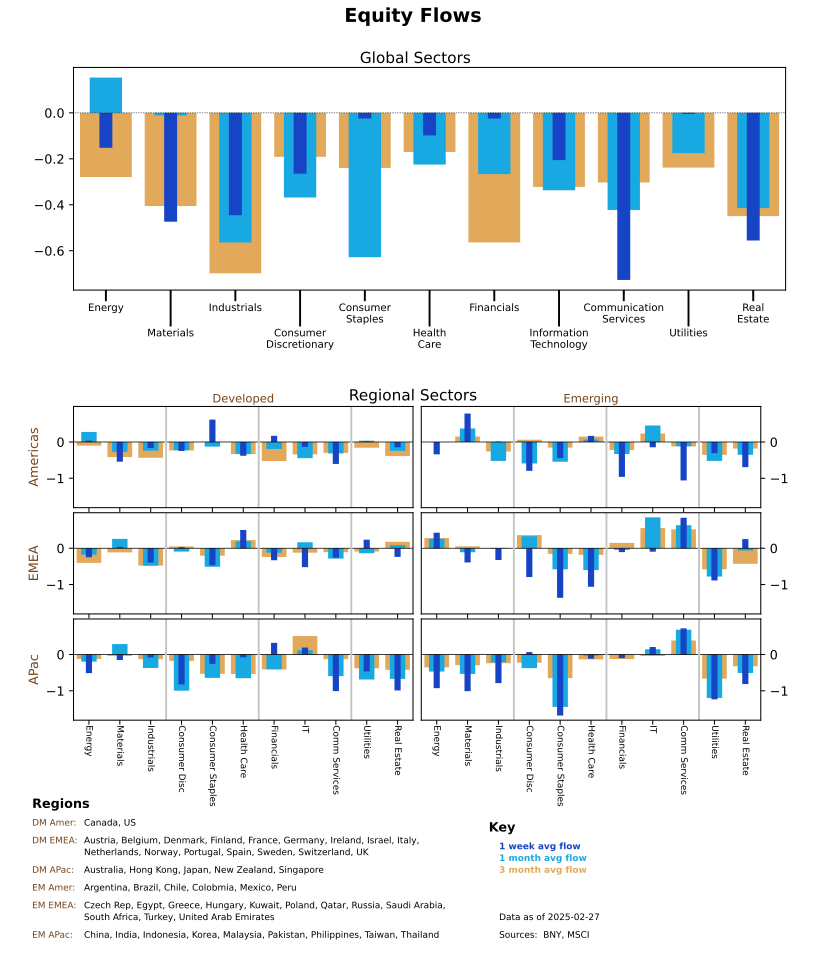

Our take: FX remains a key barometer for tariffs and global coordination: Notable iFlow long commodity FX (AUD, CAD, NOK), long Haven FX (SEK, CHF, JPY) and long CEE (PLN, HUF) while EUR is overheld, as is JPY. The USD short position is back. Expect more central bank reactions with lower rates and more intervention risks in FX.

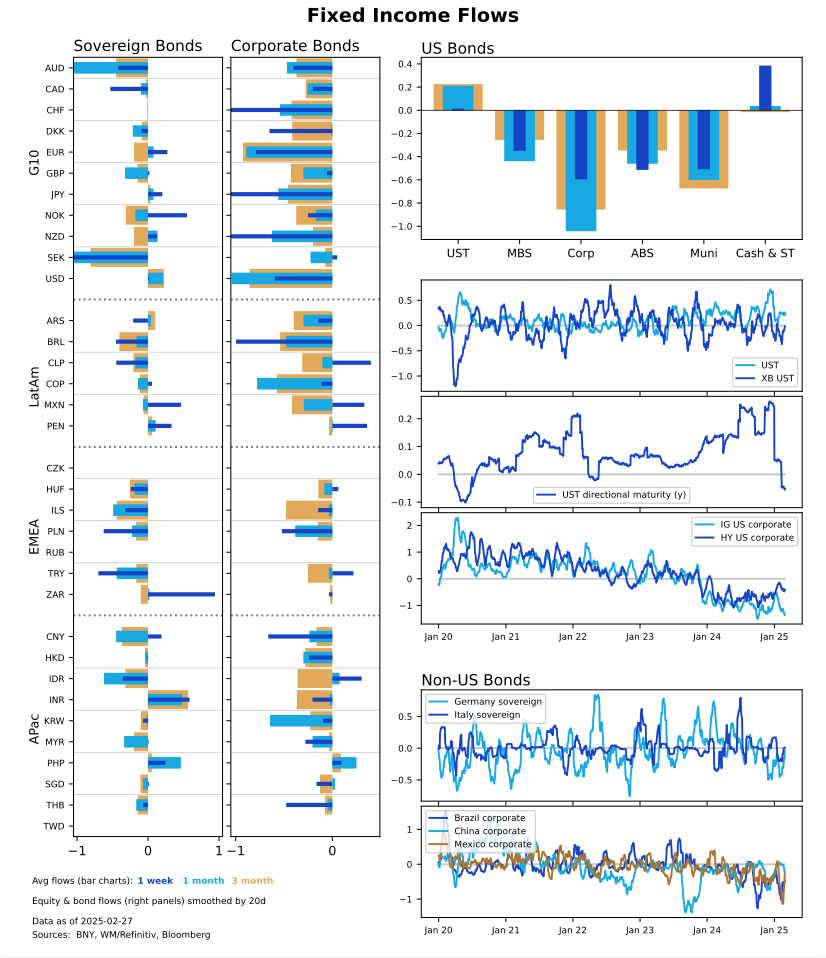

Global growth doubts and markets: The week ahead will focus on PMI, ISM and US jobs to confirm what started in February -with the US economic surprise index now negative. Doubts around US growth are rising after US conference board consumer confidence fell to 8-month lows. Consumer spending for January fell to -0.2% m/m, the first drop in 2 years. US bonds had their best rally since July 2024 with 10Y touching 4.22%. Equities shifted to growth concerns in the US after tariff talk rose and Nvidia outlooks failed to convince investors.

Our take: Equities face question of rotation or correction: Markets in the US saw lower volume, while Europe and China saw increased interest in equities. There is Regional Bias and benchmarks bias as Investors are continuing a trend that started in 2024 of keeping money close to benchmarks and in-region. This is clearly illustrated in APAC equities. APAC asset prices posted divergent performances in February, with Chinese and chip sector gains against selloffs in the rest of the region, especially in Indonesia, Thailand and India. The same story holds for the S&P500, where the Magnificent 7 heads to correction zone while the rest of the index remains up on the year. March will test buying the dip and putting cash to work.

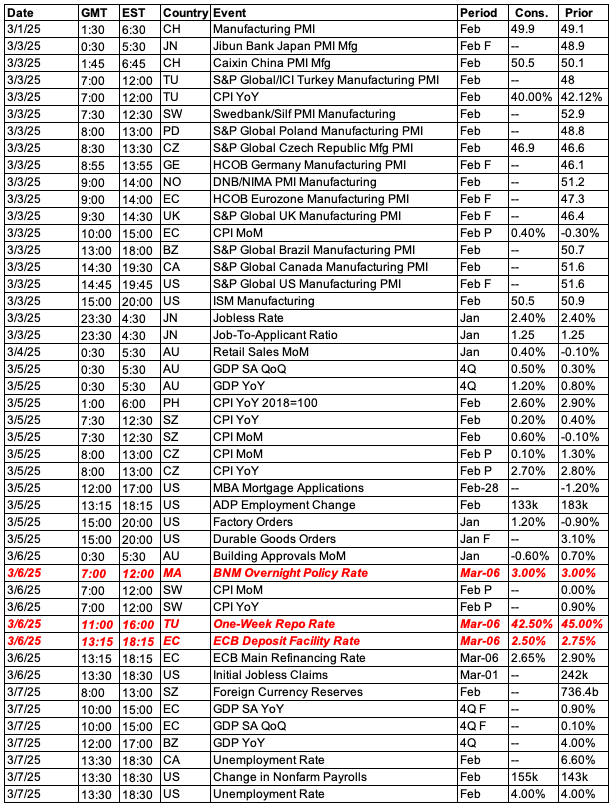

US: Tariffs, taxes, ISM and non-farm payrolls

Next week’s US data releases include the ISM purchasing managers’ indices, however most of the attention will be on the labor market report for February. It’s not clear how many DOGE-related cutbacks have been tallied during the data collection week in early February, but we’ll be keeping an eye on the Federal Government’s payroll data. It is still too early to know how many government (and related) jobs will be lost because of DOGE. A mild set of layoffs could see the unemployment rate tick up by a few tenths of a percent, while an extreme case could add nearly a full percentage point to that number.

As for policy from the new administration, the President has confirmed that 25% tariffs on Canada and Mexico will go into effect on March 4th, while an additional 10% would be levied against China on April 2nd. We were concerned that tariff risk was underpriced in FX markets, especially weakening in CAD and MXN, but the confirmation we received last Thursday finally caused some movement in currencies. We take a dim view of economic prospects in the US’s two next door neighbors should the tariffs go ahead. If retaliation occurs, the outlook will deteriorate even more.

On fiscal policy, Congress will continue its efforts to advance budget legislation, with a March 14th deadline looming for a government shutdown. The House budget resolution, which is more a blueprint for an eventual budget, passed narrowly. The plans are much more ambitious in their tax-cutting aspirations than the “skinnier” Senate version. A deal will have to be worked out by both houses. However, packaging it into one “big, beautiful bill” that can pass with just Republican support could be challenging and promises to be the center of attention in the upcoming weeks.

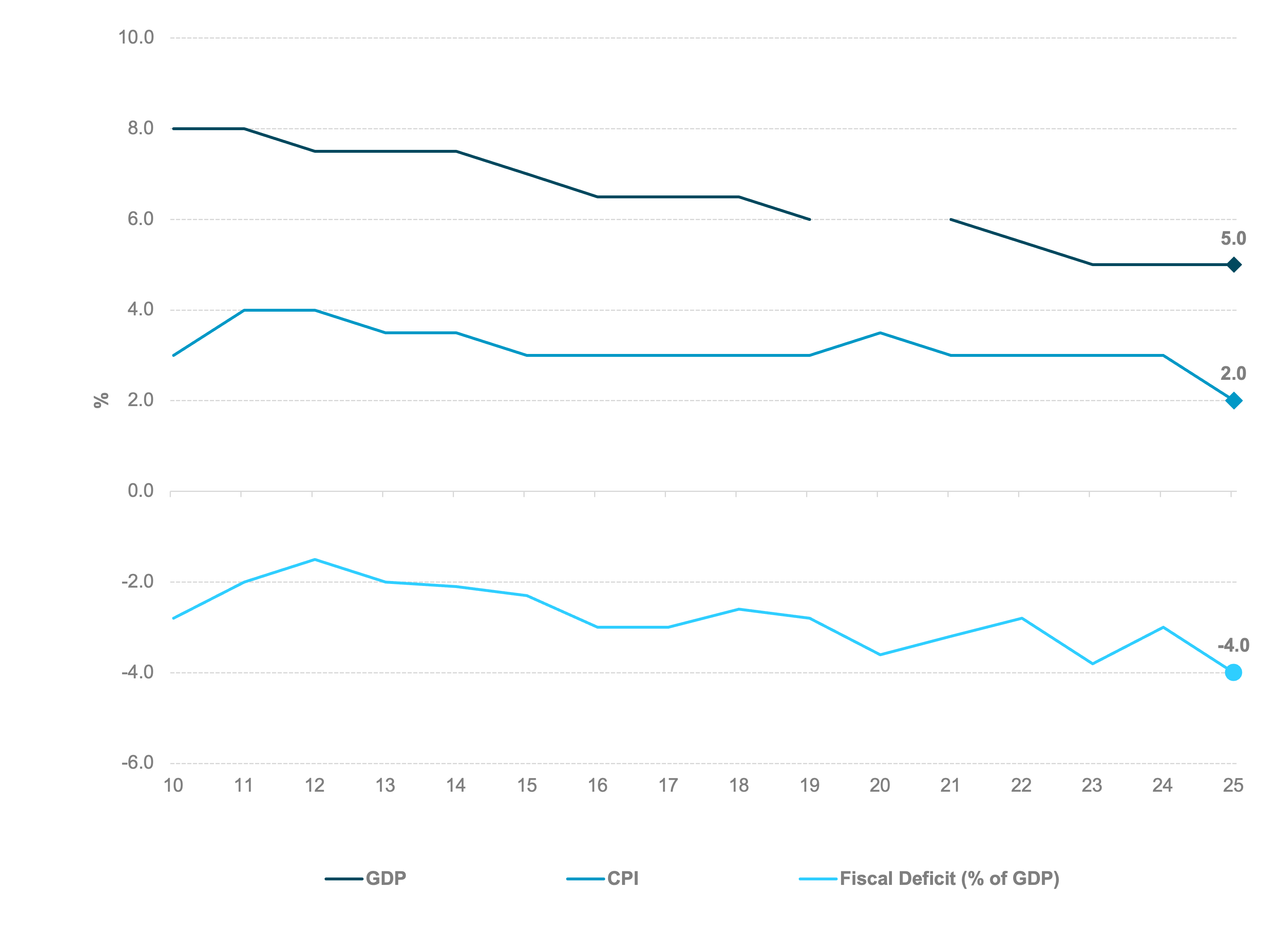

EXHIBIT #2: CHINA GDP, CPI AND DEFECITS

Source: Bloomberg, BNY

China growth and the two sessions: CPI, trades and tariffs

The key focus of the week is the Two Sessions in China, the annual meetings of the National Committee of the Chinese People’s Political Consultative Conference (CPPCC), beginning March 4th and the National People’s Congress (NPC), beginning March 5th. Both NPC and CPPCC meetings will conclude around March 11th. We expect the sessions to focus on high-tech development, ways to boost private consumption, the private sector and how to mitigate financial risks. All eyes will be on the 2025 macroeconomic target, especially on growth and budget deficit. Market consensus is for China to maintain 5% GDP growth with a wider 4% of GDP fiscal deficit ratio and to lower inflation to around 2% from 3%.

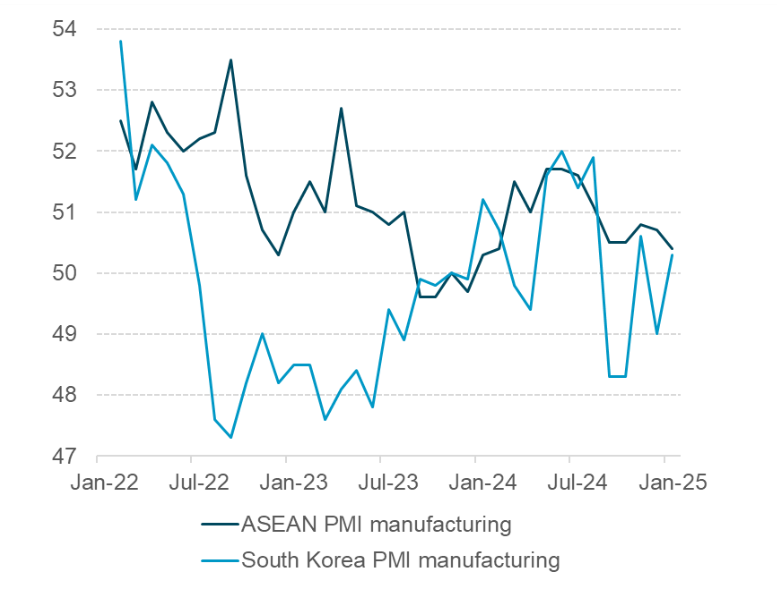

EXHIBIT #3: APAC AND DIVERGENCE

Source: Bloomberg, BNY

APAC: PMIs, inflation and central banks

The key economic data focus in APAC this week will be the regional February PMI and inflation releases. It is expected that one central bank decision, Bank Negara Malaysia, will have no change in rates and stay at 3%. Regional sentiment has shown mild improvement, but recovery remains uneven with Malaysia, Thailand and Singapore in contraction zone. Thailand and Indonesia PMI releases will be closely watched following the sharp equities selloff. Uneven recovery and downside growth risks is likely to keep monetary policies alive in the region, hinging on the domestic foreign exchange market evolution.

This week is the release of inflation reading from South Korea, Taiwan, Thailand, Philippines and Indonesia. Regional headline inflation has increased slightly over the past few months but remains within respective inflation target range. Lower commodity prices in February may halt the rising momentum. Overall, regional inflation pressure is relatively contained. Taiwan inflation reading is the most interesting this week following CBC comments that Taiwan faces pressure to hike rates.

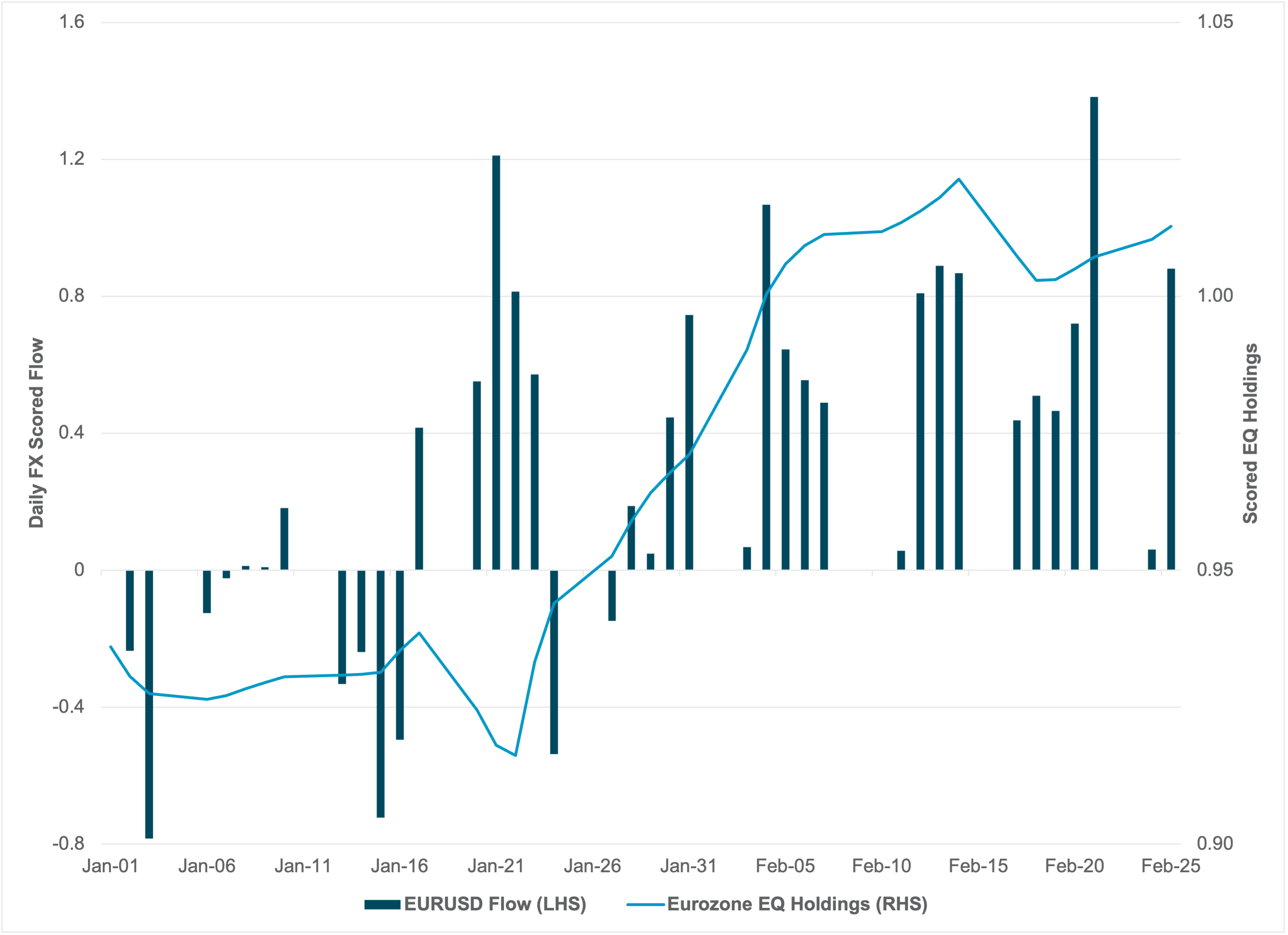

EXHIBIT #4

Source: Bloomberg, BNY

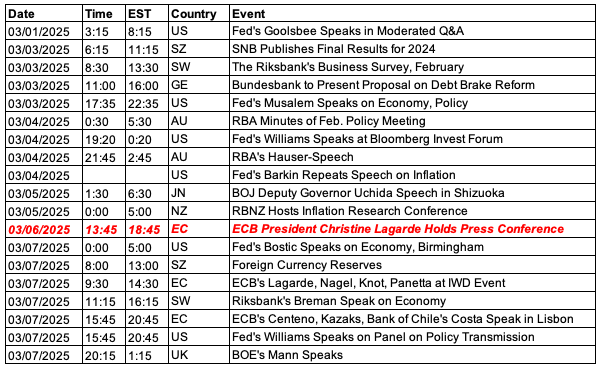

ECB: Beware the hawkish cut

Another 25bp cut is expected from the ECB.Communication from traditionally hawkish Governing Council members indicate that the path forward is far more uncertain. Earlier this week, Bundesbank President Nagel warned that “We are coming closer to a level where we are more or less leaving the restrictive territory, getting more into the neutral term.” ECB Schnabel introduced another angle: As the ECB reduces the size of its balance sheet, it may be pushing up the neutral rate of interest, calling for a relatively higher deposit rate. As European leaders move towards a new investment drive to meet rapidly deteriorating external trade and security conditions, markets would expect the ECB to act pro-cyclically. There is even a case for the Eurozone to start running its industrial sector “hot”. Some ECB members have called for rate cuts as a reaction to US tariffs, which is already being adopted in other export-based economies. Lack of commitment by the ECB would be seen as unnecessarily tightening financial conditions just when the growth narrative is shifting across the region.

We remain positive on Eurozone re-rating and asset allocation support, but we are concerned that too much is happening too quickly. Impending tariff and policy risk aside, flows have reversed sharply in the EUR’s favour through February. Rebalancing can take some steam out of EUR performance. iFlow shows that EUR/USD has demonstrated a consistently strong performance since the initial changes surrounding tariffs passed in January, accompanied by a sharp rise in equity holdings. In the near-term the risks are firmly tilted to the downside in news flow, especially from the external side. We expect additional risk management to prevail ahead of the ECB decision, most likely executed through fading the recent gains in EUR flow and holdings.

The search for balance continues to stand out in our data. Investors have pushed down their US equity holdings towards the long-term average. Underweights in Asia and EMEA have been erased. The USD holdings are back to normal, but the JPY and EUR are now slightly overweight. The risk for March will remain in US policy shifts and surprises with the Fed ability to organize a soft-landing being tested by tariffs, DOGE spending and job cuts and risks to the consumer as their mood swings with winter weather.

Central bank decisions

Malaysia BNM (Thursday, March 6) – Since the previous meeting in January, domestic data had been mixed. Jan PMI manufacturing continued to be contradictory and exports were lower than expected at 0.3% y/y, causing the lowest trade surplus since April 2020. On the positive side, Q4 GDP came better than expected at 5.0% y/y with steady private consumption growth at 4.9% y/y, while headline inflation was unchanged at 1.7%, and core inflation at 1.8%. Overall, BNM is in a good place. We expect BNM to keep rates unchanged at 3% for at least the first half of the year. There is no rush to ease with GDP growth momentum intact.

Turkey TCMB (Thursday, March 6) – The TCMB is expected to continue with its pace of 250bp rate reductions. Even though there is ongoing pressure from a stronger USD in place, the pace of reduction is manageable as the country’s financial account is generally solid after consistent inflows over the past year. However, annualised CPI is only expected to soften to just below 40%. The sequential rate of inflation at close to 3%m/m is still high, which would begin to reduce policy space up ahead. Turkey remains relatively insulated from US tariff matters with level rates acting as a buffer, but we caution against erosion of the latter.

Eurozone ECB (Thursday, March 6) – The ECB is expected to cut rates by another 25bp, but the path ahead will far more uncertain. Recent comments by Governing Council members have clearly indicated that there is divergence regarding the level of neutral rates and the near-term inflation outlook, as hawks are finding their voice and calling for caution from next quarter onwards. The fact that European equities have re-rated materially also supports the view that financial conditions have eased substantially, to the extent that additional offsets are not required. We question this view given that much of the re-rating remains isolated to defence-exposed sectors are there is precious little sign of any broader pick-up in activity. To signal a policy pivot while tariff risk is escalating will also receive heavy pushback. Consequently, we believe the ECB will need to avoid any notion of a “hawkish cut”.

Source: BNY

Source: BNY