Green Shoots

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 14 minutes

Hopes for green shoots in Europe and China yet to offset US growth worries and tariffs, markets oversold.

Week ahead will be dominated by central bank decisions by the Fed, Bank of Japan and Bank of England, some key EM markets – most expected to be on hold so any easing will drive upside risks.

Politics still important with South Korean ruling on impeachment, possible Ukraine-Russia ceasefire and Canadian response to US tariffs – response could spark a rally.

Fear of lower growth and higher inflation dominated the last week as US tariffs sparked retaliation by Canada and the EU, and fears of a global trade war rose into the April 2 deadline for reciprocal levies by President Trump. US shares fell nearly 3% on the week, while Europe fell over 1% but China rose 1.5%. US consumer confidence dropped to two-year lows and drove further fears of stagflation. The hope for a reaction to sharply weaker US stock markets proved wrong, and after inflation data in the US, hopes for a faster easing plan from the Fed also faded. Weaker credit data from China and lower imports make clear more will need to be done to stabilize demand there, while German coalition building adds to doubts that spending alone can fix the manufacturing and tariff risks ahead. Volatility has not spiked as in a crisis but has gradually risen, while volumes have receded, suggesting we have changed paradigms for trading markets in 2025. The week ahead will pivot on any good news – whether that shows up in US retail sales or in a peace deal or in rate cuts by central bankers or more spending from governments. Green shoots aren’t expected but could be delivered.

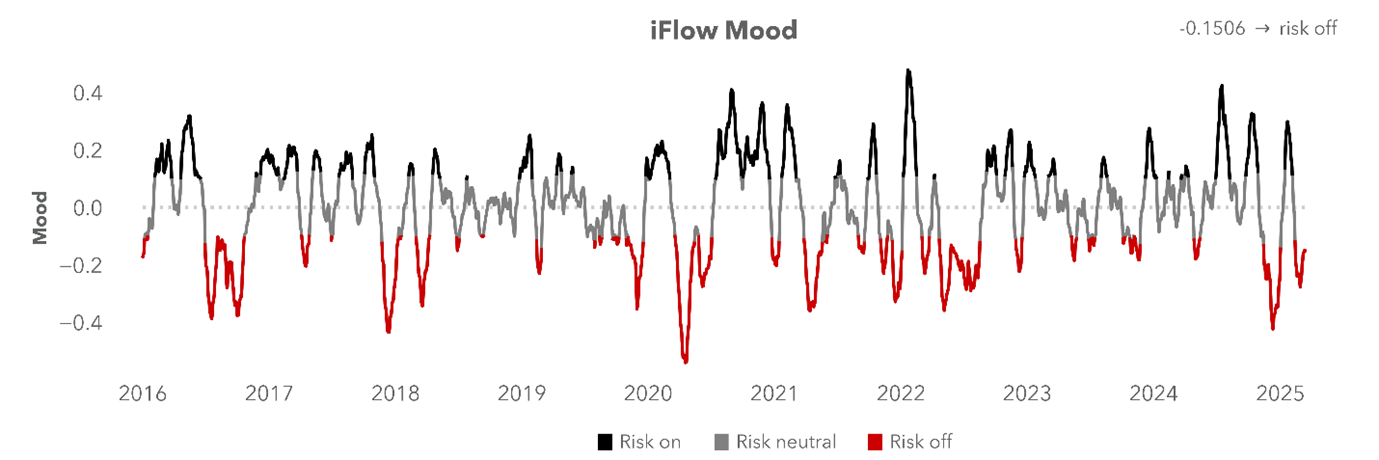

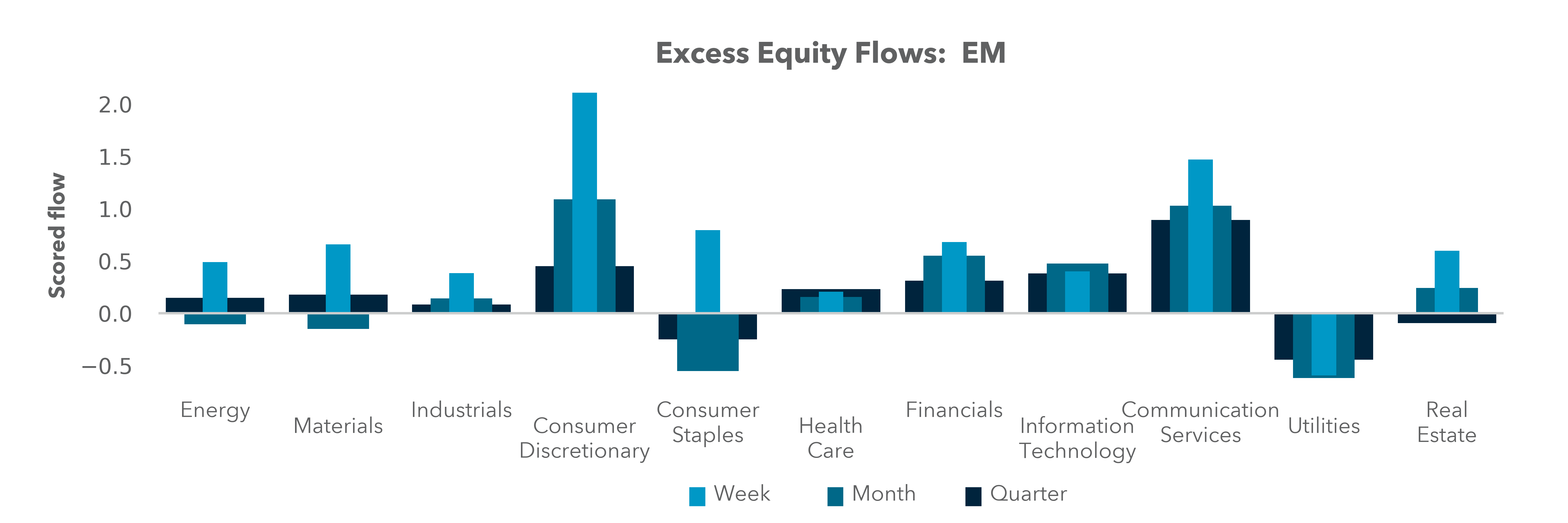

EXHIBIT #1: iFLOW MOOD INDEX STILL EXTREMELY NEGATIVE BUT BOUNCING

Source: BNY

Our Take: The iFlow mood index has been extremely negative for 22 days, but there was a bounce in the week and month as buying of EU and APAC shares offset US selling. We are three days over the average time for this index to be extremely negative, suggesting it’s time to shift to neutral. The most sold equity markets from our data last week were in Sweden and Chile, while the most bought were South Africa, China and Japan. This highlights the role of central bank decisions next week. The Bank of Canada cut linked to tariff uncertainty helped put Canada in our top five winners for inflows in stocks and bonds.

Forward Look: We are in the uncomfortable wait-and-see period as investors hold out for more data into April and a new quarter with moods souring almost everywhere as the US trade war escalates April 2, but the will to sell more risk and run to cash has similarly stalled. Range trading with value hunting in bonds and stocks should follow into the week ahead.

US focus on FOMC

Given the equity market’s latest swoon, growth fears are percolating in the US economy, as the nation careens towards an ever more intense trade war. We’ll get very little growth-related data. Instead, the focus into the week will be on the Wednesday FOMC meeting.

No move is expected, a but new set of “dots” via the March Summary of Economic Projections (SEP) should be heavily scrutinized for clues as to how much – if at all – the Committee has changed its collective thinking on the evolution of the economy via projections for growth, inflation and unemployment. With trade and other key policies still subject to extraordinary uncertainty, the SEP might show very little change, and we expect to see a wide range of forecasts. We don’t expect the two cuts indicated for 2025 in the last set of dots back in September to feature any changes.

In addition, we might get some indications of the Fed’s intentions on the balance sheet, which is coming under more open discussion. As the debt ceiling discussion continues without resolution, the Fed is becoming increasingly concerned about implications for the Fed’s balance sheet liabilities. It’s been suggested that the Fed might slow or pause QT if debt ceiling uncertainty persists. We still don’t expect any announcement this week, but a hint about a future move might emerge at this meeting.

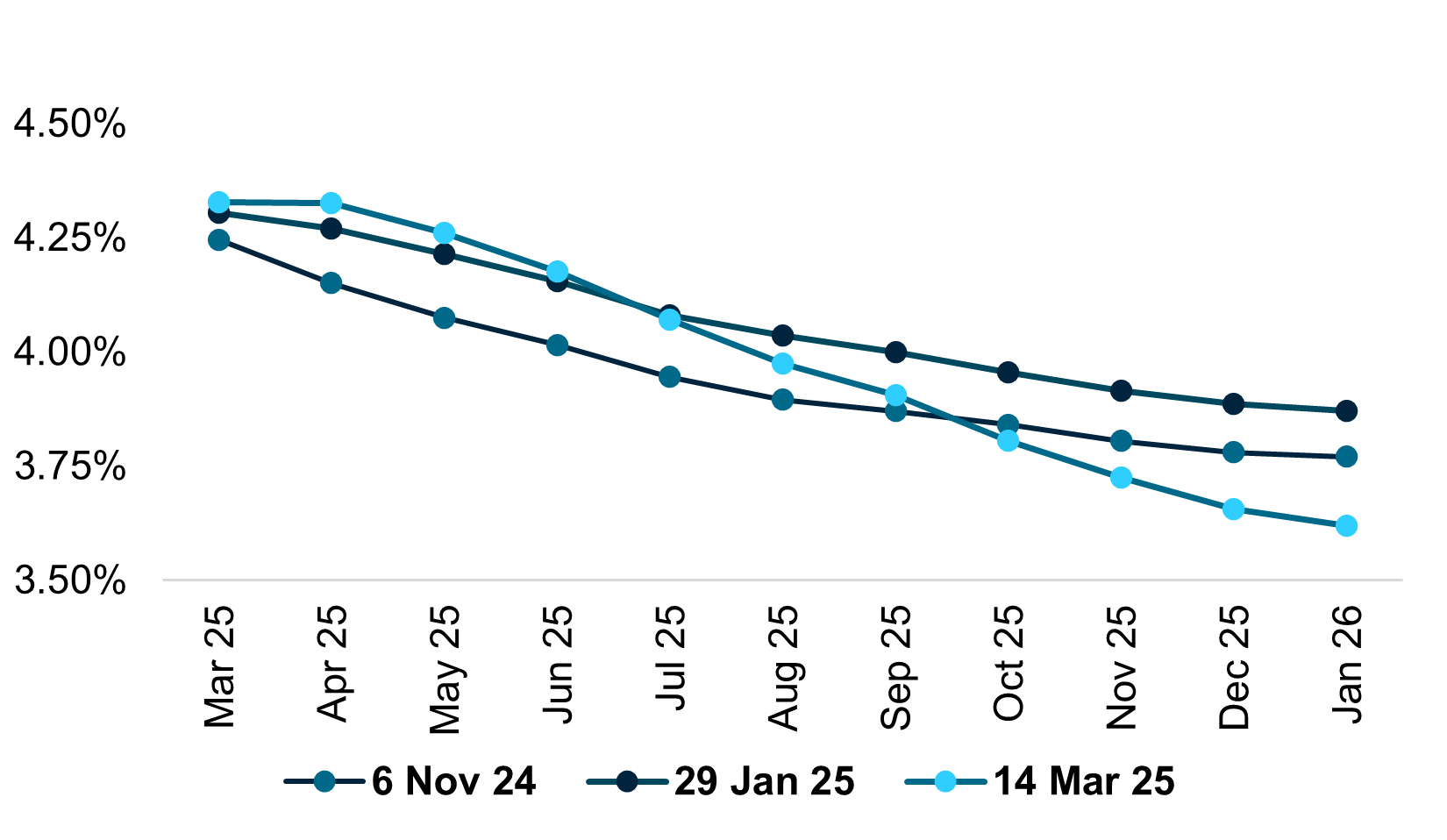

EXHIBIT #2: CHANGE IN US IMPLIED FED FUNDS RATE

Source: Bloomberg, BNY

Bank of England to stay “careful” as budget looms

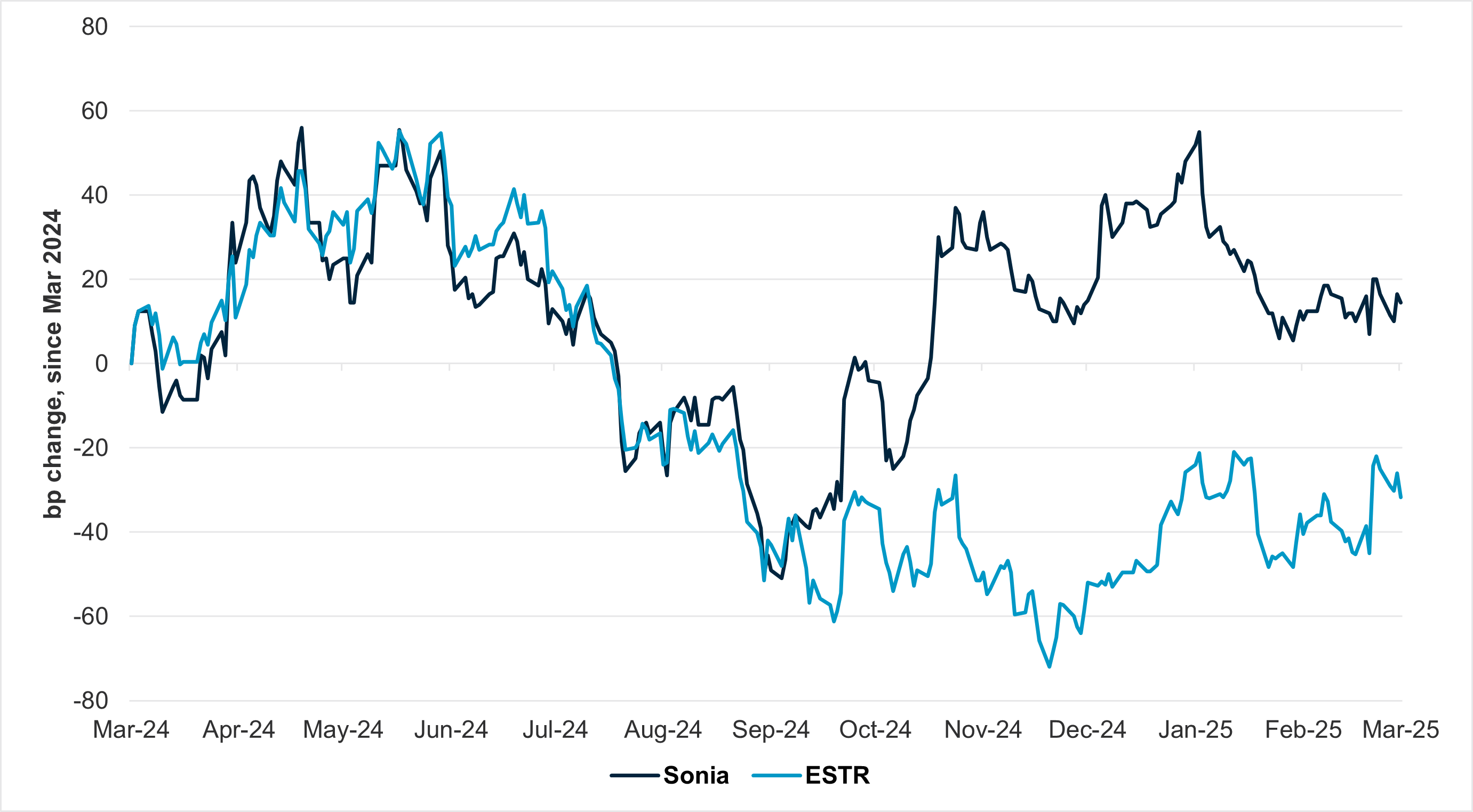

No change is expected by the Bank of England for their March decision, but the vote split would further complicate their communication, especially as members of the Monetary Policy Committee now have quite different views on how the vote itself should be deployed to manage communication. Although the UK is slightly less exposed to current gyrations over tariffs, BoE Governor Bailey has clearly communicated the downside risks to the economy arising from external pressures. Whether that can help with the overall inflation situation, however, is another matter, especially in services inflation which is holding at 5% due to stubborn wage growth. Since Q3 last year, there has been material divergence in rate expectations for 2025 between the BoE and ECB. Even after the latest round of re-pricing in positive sense in the Eurozone, coupled with a less dovish ECB, expectations for end-2025 rates in the Eurozone remain lower compared to a year ago, whereas this is the opposite for BoE expectations. As agent surveys point to a sharp rebound in expectations for total labour costs, most of the BoE will opt for slower cuts but hope that the government can help do the heavy lifting regarding wage growth. That Prime Minister Starmer had to stress that upcoming reforms to government spending would not constitute renewed “austerity” is, in our view, the latest sign that the government is bracing the general population for large-scale spending cuts.

EXHIBIT #3: CHANGE IN DECEMBER 2025 RATE CUT EXPECTATIONS, BOE AND ECB

Source: Bloomberg, BNY

German fiscal pivot to support SNB and Riksbank outlook

The first Swiss National Bank decision of the year is likely to yield a further cut of 25bp, though we suspect that the SNB was hoping for a more positive outlook, based on their assertion in December that inflation was set to improve at a faster clip toward the end of their forecast horizon as conditions improved. Even so, their forecasts pointed to inflation dropping close to zero in H1 2025, and this was before the recent tariff risk which will have material consequences for the Swiss economy in the worst-case scenario. As we have highlighted in the past, the Swiss balance of payments has unique sectoral exposure to pharmaceuticals, and this is a key focus area for the US administration. Only recently has the non-pharma trade balance for Switzerland turned positive (Exhibit #4), but a demand hit to such a high value-added sector would require material revisions to the economic outlook. Further rate cuts are warranted on a precautionary basis alone.

On the positive side, the recent re-rating of Germany’s fiscal outlook is potentially highly reflationary for Europe and Germany’s key trading partners. While German industrial demand for intermediate goods produced in non-Eurozone economies cannot immediately offset sectors impacted by demand loss in the US, trend growth improvement will support the more positive forecasts in the SNB and Riksbank’s forecast horizons. Crucially, the move in German and Eurozone yields without sovereign credit risk will obviate excessive positioning in CHF and SEK, permanently removing a strong source of currency-based disinflation or deflation risk.

EXHIBIT #4: SWISS PHARMACEUTICAL VS. NON-PHARMACEUTICAL TRADE BALANCE

Source: Macrobond, BNY

China retail sales, industrial production, APAC trade and central banks

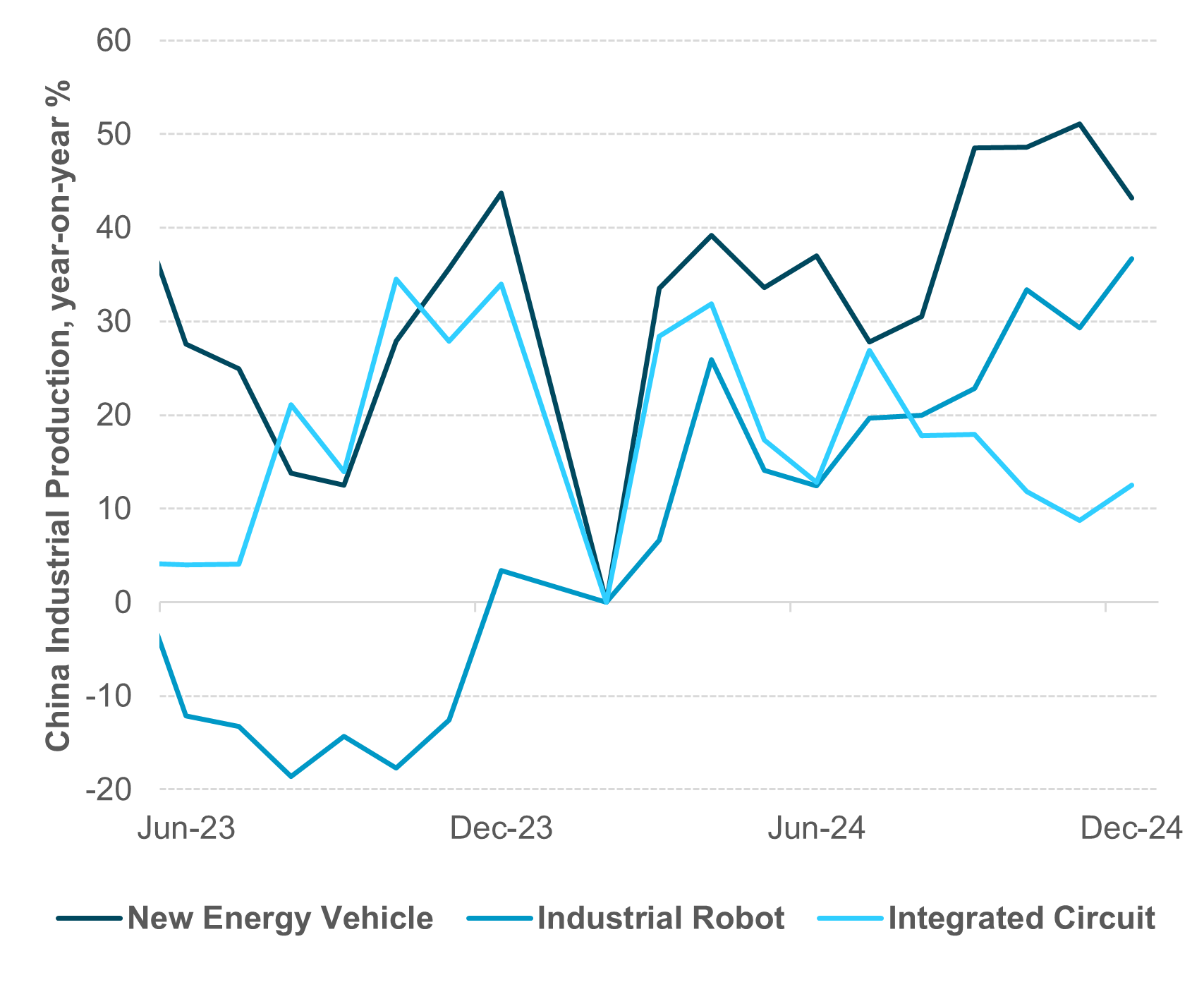

The key economic data focus in APAC this week will be China retail sales data of the combined first two months of the year. Consensus is for an uptick in retail sales, which had stayed steady at 3.5% YTD y/y since Q4 2024, and further momentum in industrial production, especially in the high-tech sector. Note that industrial robots, new energy automobiles and integrated circuits posted a strong pace of 36.7%, 43.2% and 12.5% y/y, respectively, at the end of 2024. We will also be looking for further stabilization in China’s housing market. Note that new and used home prices for Tier-1 cities have increased on a sequential basis over three straight months. However, in aggregate term, the average China 70-cities new used home prices remain in negative territory, at -5.4% y/y and -7.8% y/y, respectively.

Elsewhere, Taiwan, Malaysia, India and Indonesia will publish February exports data. This, along with the latest export data for the first 20 days of March, should serve as a barometer of the health of global trade.

Foreign investor flows into APAC equities, except for China, have been on the sell side, notably net $3.5bn and $1.5bn selling of Taiwan and South Korea equities, respectively, last week. We are also closely monitoring the potential shift in investment stance to selling of Korean equities by “government pension funds” after a multi-month buying program since November 2024. South Korea and the supreme court decision on impeachment will be a key focus for the politics of the nation with expectations of a new election in May.

Lastly, the Bank of Japan (BoJ) is expected to be on hold at 0.5% with hawkish comments from BoJ Governor Ueda clearly pointing to a May or June hike. Wage round allows them to normalize rates despite tariff risks to growth. The Bank Indonesia (BI) and Central Bank of the Republic of China (CBC) will convene this week. Market consensus is for both BI and CBC to maintain status quo at 5.75% and 2.0%, respectively. Bank Indonesia is looking for room to cut but is hindered by currency depreciation pressure and the rising core inflationary pressure, while CBC is likely to maintain a relatively hawkish tone to guard against elevated housing price.

EXHIBIT #5: CHINA EVS, ROBOTS AND CHIPS

Source: Bloomberg, BNY

There will be a change in the message from central bankers in the week ahead. Being in no hurry to change rates is not going to help stabilize markets or support confidence. Rather, the need to react to the uncertainty and unpredictability of tariffs will drive more forward guidance but without much confidence, as economic models have wider bands of possible outcomes and longer tail risks for the year ahead. For the Fed, it’s likely to show up in a plan to pause their balance sheet run-off if the government shutdown is averted and the debt ceiling debate results in a real budget by summer. Investors are likely to take little comfort and the risks of stagflation becoming the phrase for shunning risk will continue as bonds stay close to 4.25% for 10y yields and stocks scuttle along the bottom, near 5,500 on the S&P 500.

Central bank decisions

Japan BoJ (Wednesday, March 19) – No change is expected from the BoJ, with the target rate expected to remain at 0.5%. Even if the latest wage negotiations point to some need for additional tightening, the recent trajectory of the JPY and general market volatility can already be seen as an effective tightening in financial conditions. Even so, we do not think the policy trajectory will change as national CPI is expected to run at 3.5% for February, with the core number at 2.9%.

Indonesia BI (Wednesday, March 19) – The market is expecting BI to keep rates on hold, but the central bank is looking for room to cut. Taking the Bank of Thailand decision as an example, BI could use falling equities sentiment, the sharp re-widening of INDOGB-UST spreads (from 220bp in mid-February to 260bp) as an argument to cut, but this would be at odds with the rising momentum in core inflation if IDR falls. Our view is for Bank Indonesia to maintain the status quo and wait for an opportunity to cut. USDIDR evolution ahead would be a key determining factor.

US FOMC (Wednesday, March 19) – No policy moves are forthcoming this Wednesday at the FOMC meeting, but the March Summary of Economic Projections will be scrutinized for any change in the outlook. Given the extraordinarily high policy uncertainty still present in markets, the dots might not change too much. We will also be looking for any indications on balance sheet policy going forward.

Brazil COPOM (Wednesday, March 19) – The market is expecting a 100bp jumbo hike by COPOM to 14.25%. Not only would this push the Selic rate above the post-pandemic cycle high but it would also match the highs during the 2013-2016 tightening cycle. Depending on the inflation measure, BRL real rates remain comfortably positive, but the fiscal pressures continue to demand restrictive policy. LatAm currencies are overheld at present but vigilance over global growth is needed and we remain skeptical regarding any material turnaround in inflation expectations.

Taiwan CBC (Thursday, March 20) – We see the central bank keeping rates unchanged at the March meeting, supported by easing in the latest inflation data. February headline and core inflation have fallen to 1.58% (January: 2.66%) and 0.98% y/y (January: 2.26%), respectively. That said, elevated house prices remain a source of concern, even though year-on-year growth is slowing. The CBC sounded hawkish recently saying that “Taiwan faces pressure of rate hike,” but despite the need to curb loan growth we do not see any urgency for a policy rate hike or further adjustment in RRR.

Switzerland SNB (Thursday, March 20) – The SNB is expected to cut rates by another 25bp to 0.25%, and we continue to see a material chance of zero nominal rates given the central bank itself is expecting a major dip in price growth around H1 this year. The improvement in the outlook through the forecast horizon did not consider the current problems in the global economy and Switzerland being very exposed to tariff risk, especially in pharmaceuticals, which anchor the country’s trade surplus.

Sweden Riksbank (Thursday, March 20) – The Riksbank is expected to keep policy unchanged at 2.25% but there may be a shift in the policy board’s bias due to global trade instability. On the other hand, Sweden will be a major beneficiary of the re-investment drive in Europe, and we can see the SEK’s robust performance of late reflects a shift in the regional outlook. Given current underlying inflation levels have picked up again, such a move is welcome and will not require a policy offset.

UK BoE (Thursday, March 20) – The Bank of England is expected to keep rates on hold at 4.50% but the vote split will show very divergent views on the economy yet again. Surprisingly, the domestic economy contracted in January and with fiscal pressures continuing to rise, the overall growth outlook is problematic, which we believe would require a large policy offset at the right time. The BoE will reiterate its “careful” stance given external policy volatility, but the near-term focus will now shift to the fiscal statement toward month-end.

South Africa SARB (Thursday, March 20) – The SARB is expected to keep rates on hold at 7.5%. which will keep real rates high at 4%, but domestic fiscal wrangling is now weighing on asset performance, even if the flows so far have been muted. Resolving the impasse may yet require some loosening of fiscal policy relative to baseline expectations, and this always narrows operational room for emerging market central banks. Meanwhile, mining production and manufacturing continues to decline, indicating further softness in the global outlook which is weighing on commodity currencies.

Chile BCC (Friday, March 21) – Despite current dollar weakness, EM currencies with low levels of nominal rates are not able to move further on easing due to uncertainty over global flows. CLP, which is approaching the decision from a position of strength, will also face unwinding risk, hence the BCC will need to anchor expectations by staying on hold. With Brazilian nominal rates likely to move close to a full 10pp above the Chilean equivalent, operational space is becoming limited, especially if the fiscal outlook becomes more problematic up ahead.

Russia CBR (Friday, March 20) – The Central Bank of Russia is expected to keep the key rate on hold at 21%.

Source: BNY

Source: BNY