Golden Week

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 12 minutes

The markets slipped in the last week as the expectations for the speed and pace of Fed rate cuts shifted – leading to pervasive “good-news-is-bad” thinking. The revision of U.S. Q2 GDP to 3.8% resets the baseline for the Q3 outlook. The Fed’s insurance cut two weeks ago feels less urgent following stronger home sales, better consumer spending and fewer jobless claims. However, the resulting drop in equities and bonds and USD bounce-back highlights the market’s rate sensitivity and the overlay of Q3 rebalancing as U.S. exceptionalism crept back into play. Markets absorbed over $500bn in U.S. government bills and notes this week while also seeing $250bn in IG/HY issuance in September. The borrowing supply met demand, but for how long? Cross-border interest in U.S. debt markets plummeted and may be more than a month-end rebalancing exercise. Most see the next week as pivotal, with U.S. nonfarm payrolls more important than last week’s data. There will also be a focus on China as it starts Golden Week and the U.S. as it faces a potential government shutdown. For some, the shutdown risk isn’t a market story but a political one, but the hit to Federal workers and disruption of courts and some payments could surprise. The one standout market risk revolves around economic data release, starting with Friday’s nonfarm payrolls. If the FOMC is data-dependent, so are markets, and not getting data means markets will look elsewhere for information.

Will markets start to reflect on their expectations?

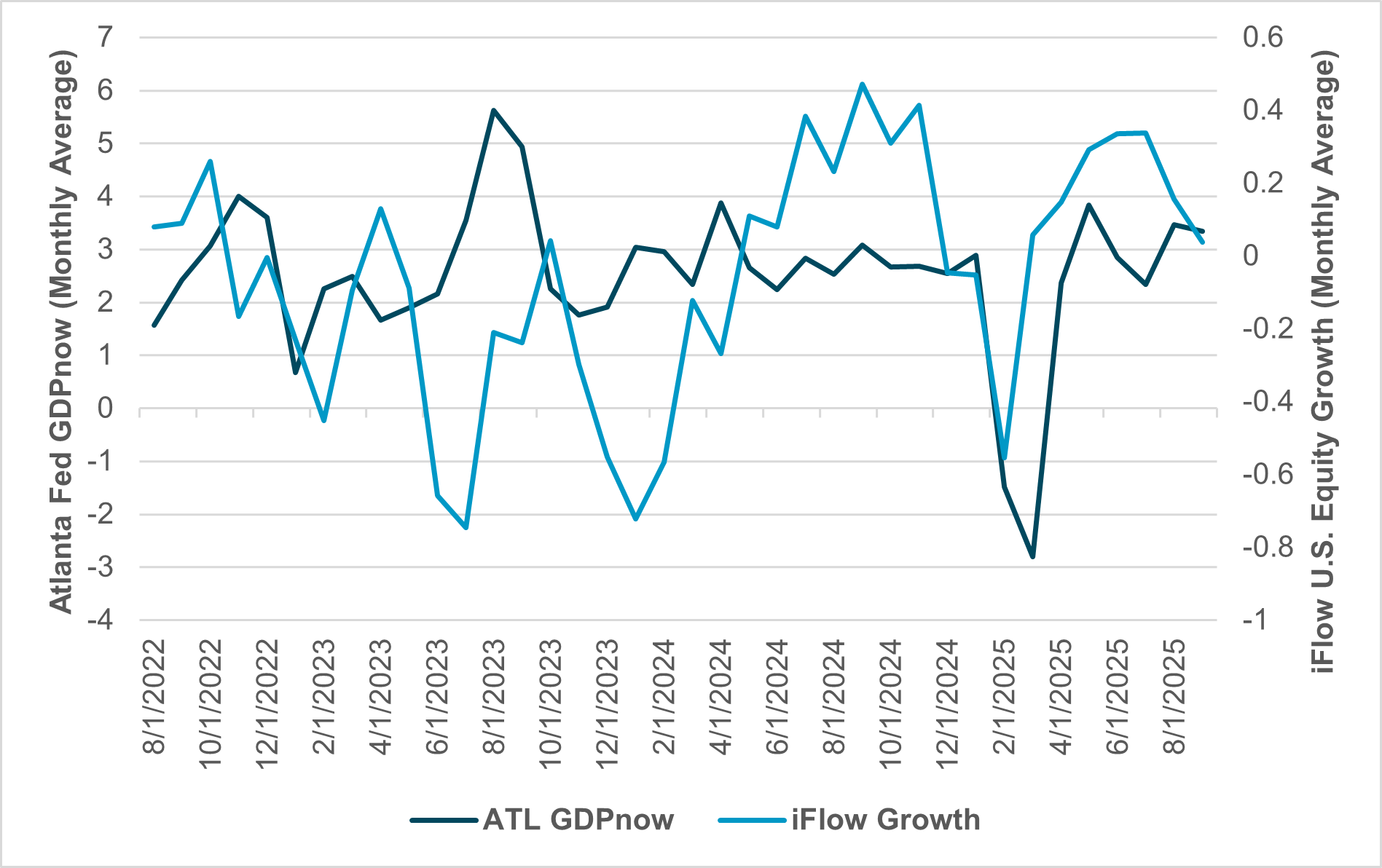

EXHIBIT #1: U.S. GROWTH ALTERNATIVE DATASETS: ATLANTA FED GDPNOW, IFLOW U.S. EQUITY GROWTH FACTOR, S&P COMPOSITE PMI

Source: BNY, Bloomberg

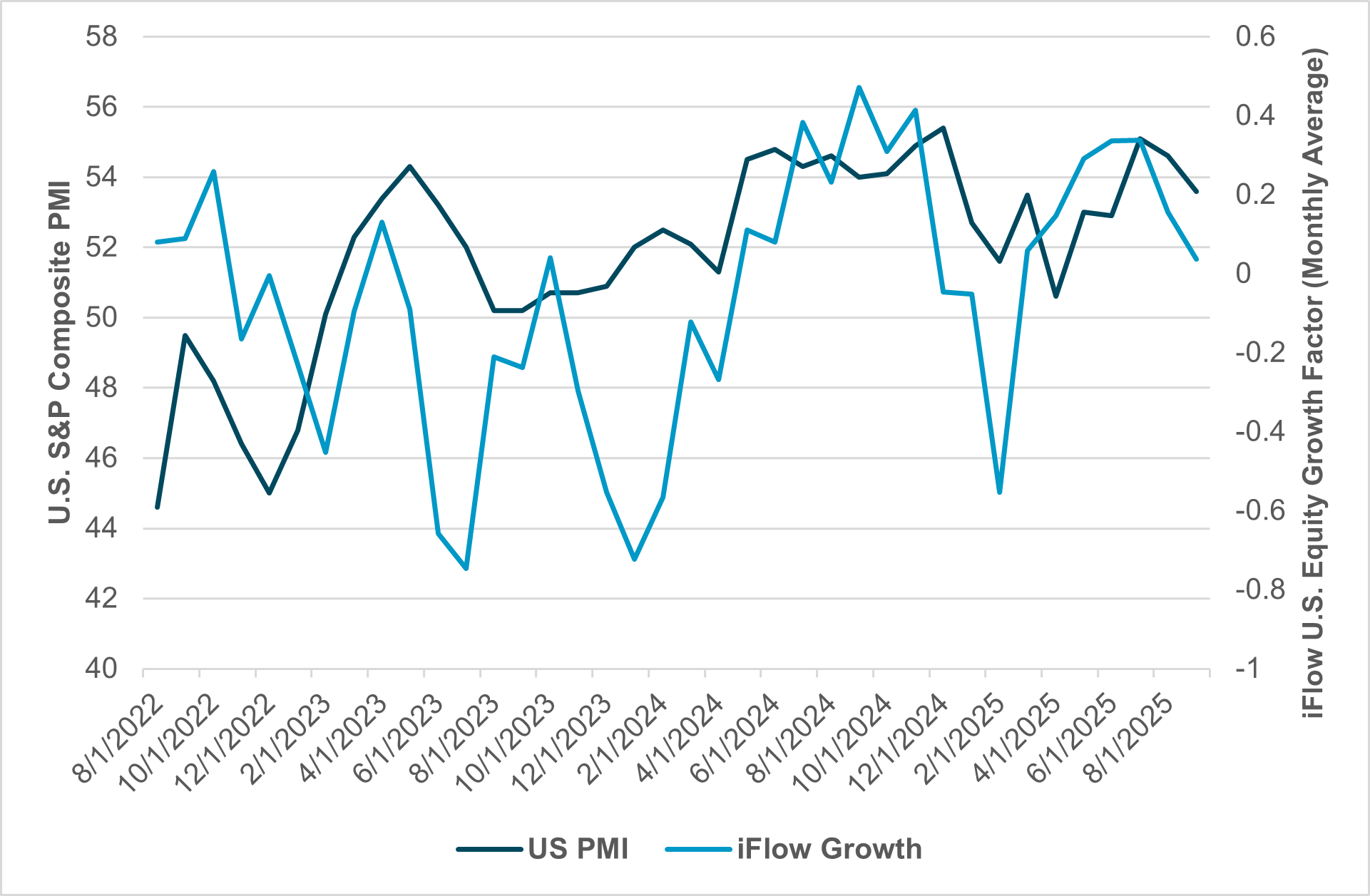

EXHIBIT #2: U.S. S&P COMPOSITE PMI VS. U.S. EQUITY GROWTH FACTOR

Source: BNY, Bloomberg

Our take: The risk of not having government data flips markets to private datasets – like ADP for jobs or PMI/ISM for sector growth. The Fed Beige Book and Fed regional surveys will also become more important, as will faster impulse readings of credit card use, retail store single-name sales and Q3 earnings reports. The risk for markets after seeing stronger July and August growth reports is that they’ll fly blindly into the September data. What seems clear from our equity flows is that growth factors are not the key driver of U.S. equities here. Growth outlooks are turning lower after bouncing back from February/March lows. The Atlanta Fed GDPnow is widely used as a more weekly update to U.S. growth, but it depends heavily on government data. The search for alternatives that correlate to it will be something to consider should the government shut down for more than a few days.

Forward look: How much price moves in stocks and bonds reflect expectations vs. the real economy will be critical to how investors view the world in the month ahead. The quality of economic data from private sources is less controlled and less equally distributed. Price discovery on information will return as a factor to consider, implying markets should have a higher short-term volatility risk until they become more efficient at sharing such data. There is also a risk that trusting correlations to the real economy to guide risk will prove insufficient. The week ahead will be critical to see how investors view such risks.

U.S. key jobs data and government shutdown risks focus

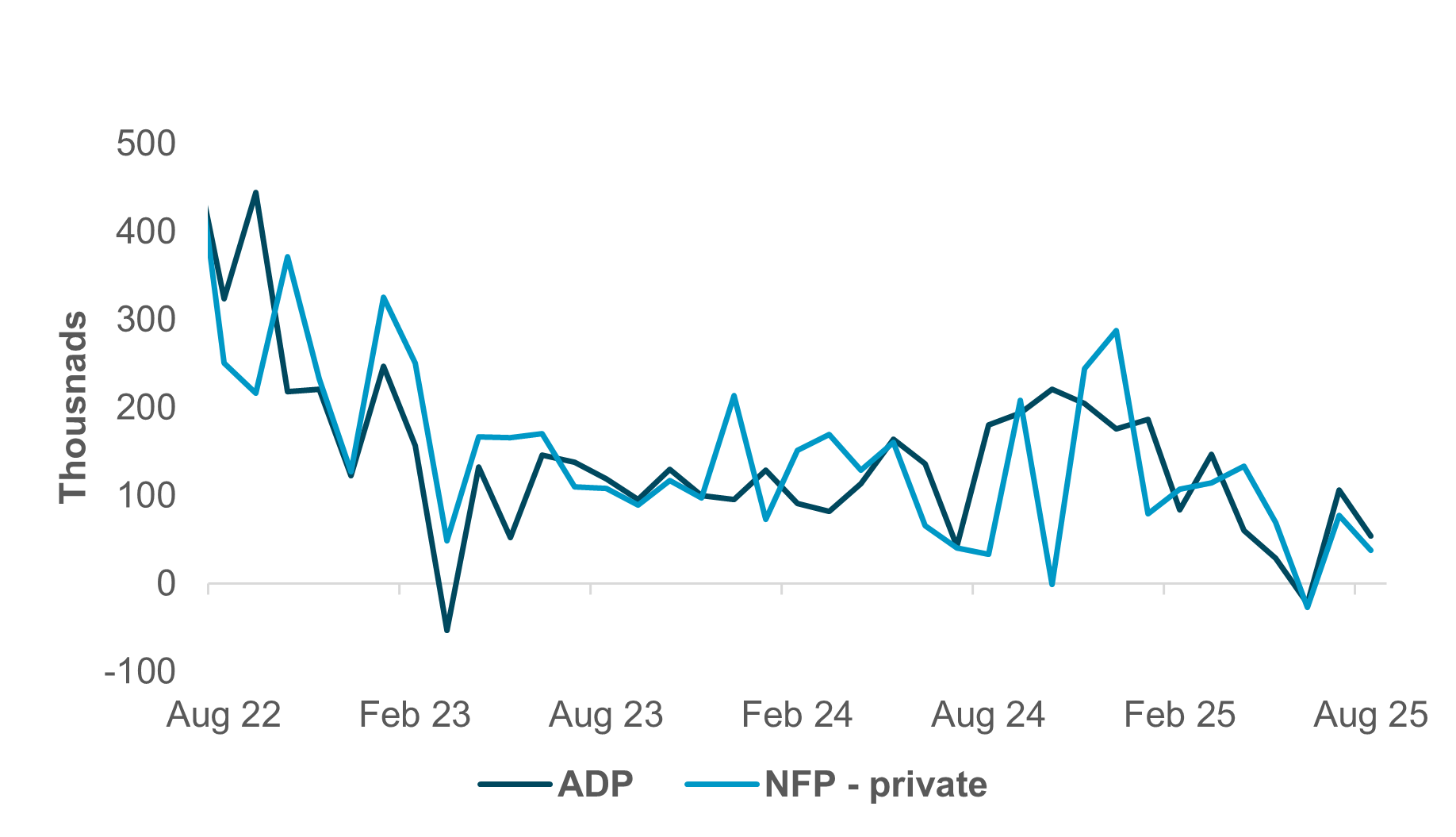

EXHIBIT #3: U.S. ADP AND NFP PRIVATE JOB GROWTH

Source: BNY, Bloomberg

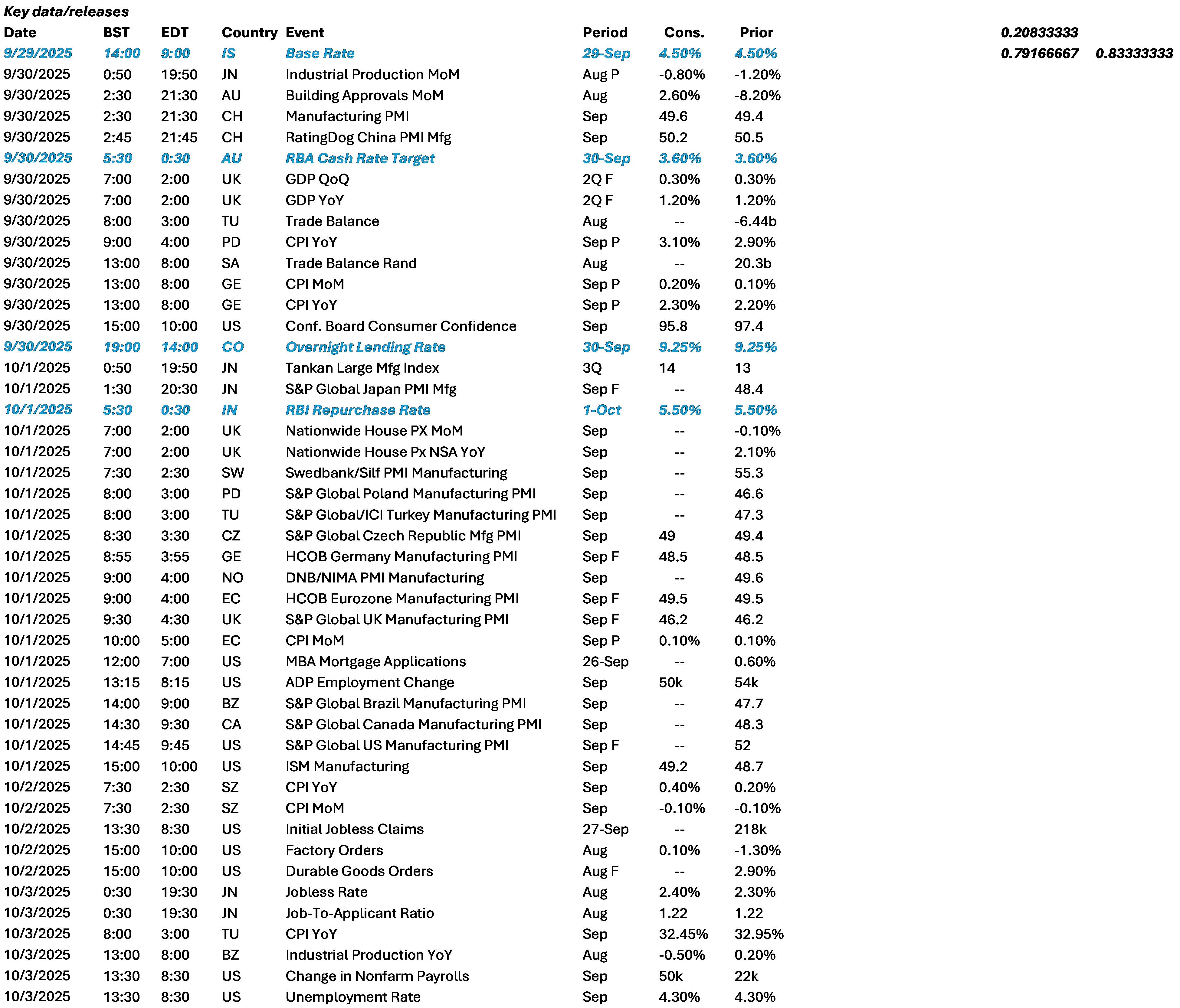

Our take: Beyond the mere data and Fedspeakers on the docket for the week, perhaps the biggest news story will be the likely government shutdown, when current funding runs out at midnight on October 1. The odds of such an event are rising, reaching around 75% in the predicted markets. Given the large swath of data due after October 1 (NFPs on October 3, CPI a little less than two weeks later), a long shutdown – which cannot be ruled out – could hamstring the market’s ability to correctly price the course of the Fed’s easing cycle, although private sources of data could fill some small part of the gap. Speaking of the Fed, the week offers a less busy schedule of appearances than we saw last week.

Forward look: Data we will receive next week include the JOLTS survey (Tuesday), ADP, (Wednesday) and, of course, Thursday’s jobless claims – all of which will give some sense of labor developments, while the ISM manufacturing (Wednesday) and nonmanufacturing (Friday) surveys also offer some insight into job market developments even in the presumed absence of NFP data on Friday (unless the shutdown is averted or abbreviated).

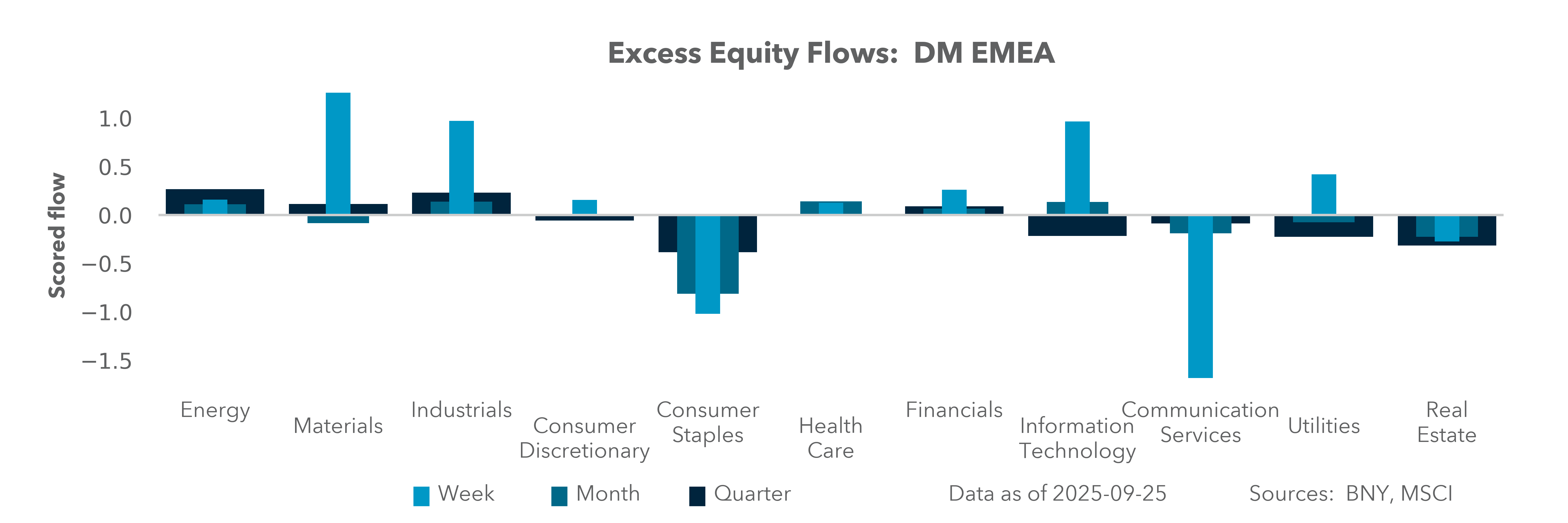

EMEA: September inflation prints to test policy gaps

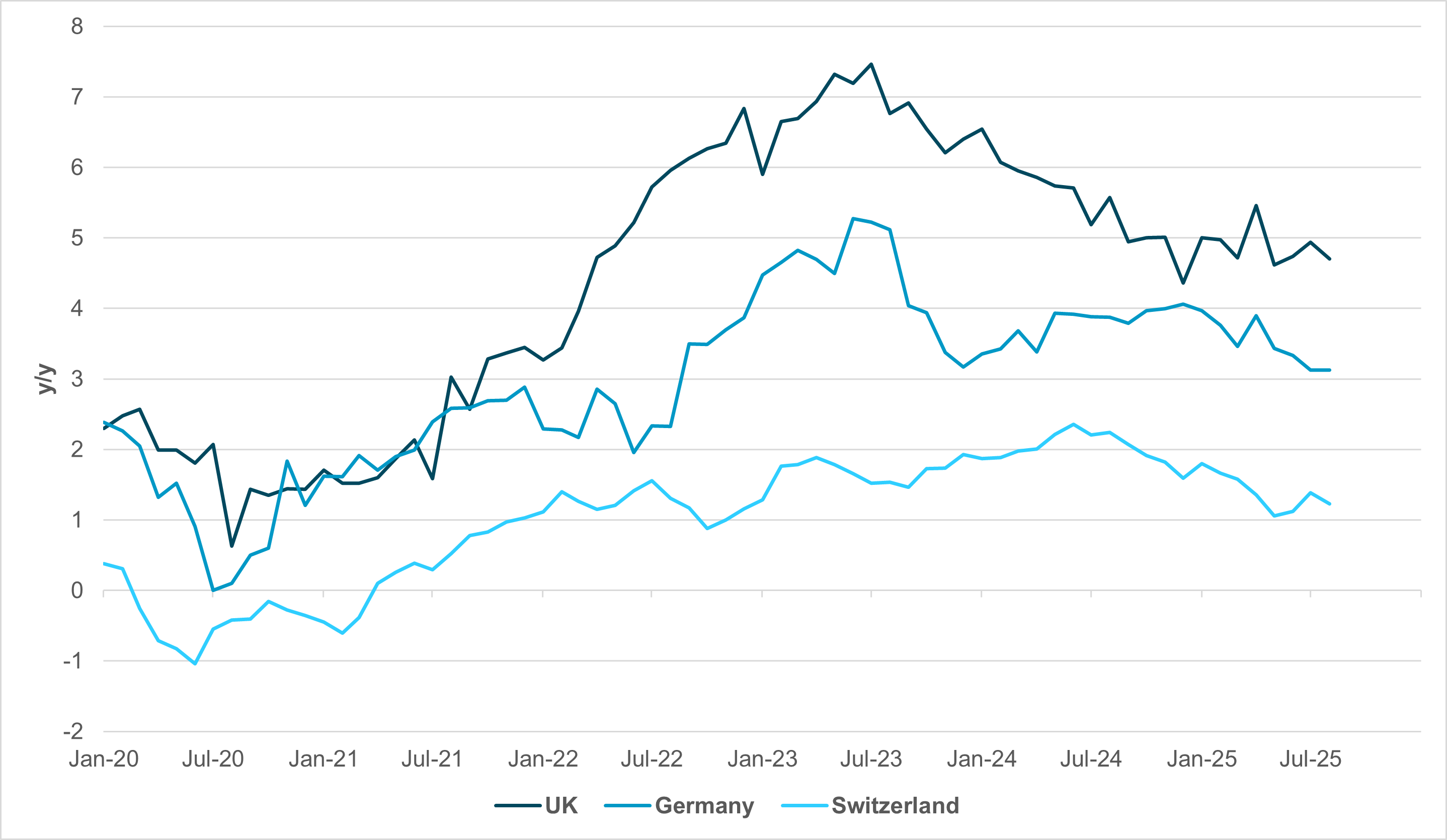

EXHIBIT #4: SERVICES INFLATION IN THE U.K., GERMANY AND SWITZERLAND

Source: BNY

Our take: Commentary from political and monetary authorities will continue to dominate proceedings in the week ahead as Europe seeks to maintain momentum in defense-led domestic investment, while ensuring that the Eurozone itself stays in “a good place” for inflation as preliminary September price prints arrive. For national leaders, recent developments in EU and NATO airspace have added urgency for a renewed push on defense. On the other hand, Europe is under no illusion regarding the nature of President Trump’s recent comments regarding the prospect of military success in Ukraine, as the U.S. does expect further shifts in the distribution of financial and equipment burdens. However, this is exactly the area where markets continue to hold out hope for various pro-growth factors, from fiscal stimulus to joint debt issuance to innovation. Backed by Germany, there is now clear momentum to deploy the €140bn in frozen Russian assets to support various initiatives, and national leaders continue to push for clarity on pooled resources. Greek Prime Minister Mitsotakis confirmed last Friday that “there is much more momentum for joint borrowing for defense,” but we acknowledge that the process will take time and differences in national priorities – such as the recent dispute between France and Germany over the Future Combat Air System (FCAS) – means that progress will be slow and heavily managed.

Greater momentum for defense does not imply greater market forbearance on fiscal priorities either. Key fiscal decisions loom in the U.K., France and Italy, all of which are not pointing in a favorable direction from markets’ perspective. The U.K.’s ruling Labour Party will hold its annual conference this week, and there are clear splits emerging within the party, including the prospect of a leadership challenge in the near future to Prime Minister Starmer, which could result in an abrupt leftward shift in domestic policy. The U.K.’s unique sensitivities to the prospect of capital outflows due to wealth taxes has already impacted sterling’s performance, and gilt markets will remain nervous amid disappointing bid-to-cover ratios in recent auctions. Meanwhile, new French Prime Minister Lecornu has also expressed some sympathy for wealth taxes, but industrial action looms in France, which could impact stability in a market which remains relatively over-owned compared to established risk premia. Italy may also confirm that the pension age will be frozen, which could renew scrutiny over BTPs, which hitherto had been one of the biggest success stories this year in European sovereign markets.

Forward look: Key data releases this week are the preliminary September inflation figures. They are not expected to generate any surprises, and the ECB made it clear in its September forecasts that EURUSD’s current levels do not represent a strong downside risk of inflation. Even so, the risk is asymmetrical for most G10 central banks. Current pricing for almost every single Western European central bank is very limited for the rest of the year, but this is assuming that core inflation numbers hold up well, which in turn requires labor markets to limit any further loosening. This remains a tall order given the mixed set of PMI results, but we acknowledge that with services growth still expanding across Europe, central banks have every reason to expect wages to hold up enough to drive services inflation higher. The U.K. and Germany all have very elevated services inflation figures (Exhibit #4), but similar to rate expectations, this means the risks are strongly skewed to the downside. We continue to see limited gains for the EUR and GBP from these levels as fiscal issues come to the fore, and the bar is low for a strong reaction to downside inflation surprises, especially in wage-related prints.

APAC: Regional PMI, Japan Tankan, exports and trade, and RBA and RBI in focus

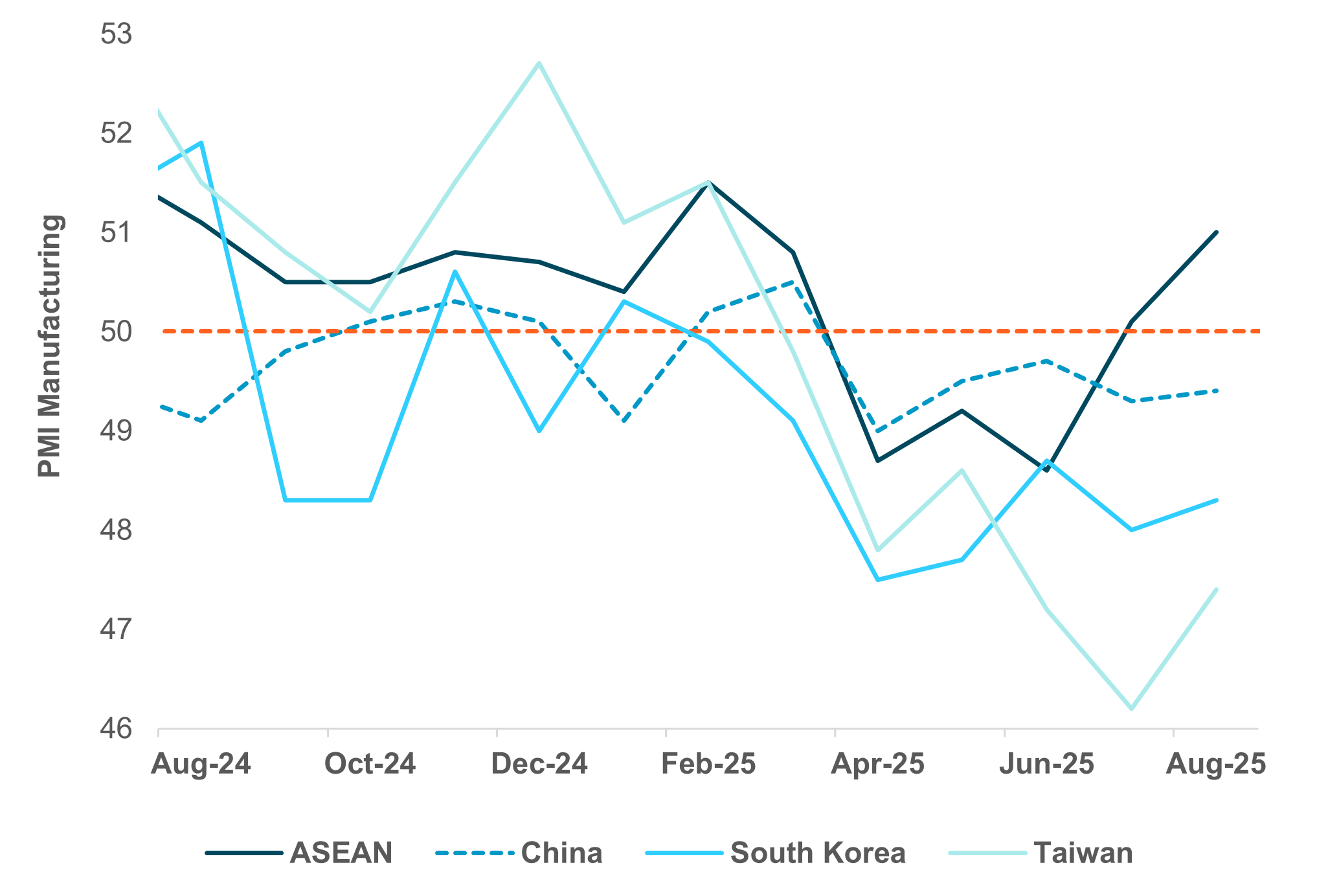

EXHIBIT #5: ASEAN PMI RECOVERY VS. CONTRACTION IN CHINA, TAIWAN, SOUTH KOREA

Source: BNY, Bloomberg

Our take: In APAC, this week’s focus will be on September PMI, export and trade data, Japan’s Q3 Tankan survey, and inflation data from South Korea and Indonesia, as well as housing-related data from Australia and New Zealand. Regional PMI will be closely monitored this week, especially in China, Taiwan and South Korea, which has showed minimal improvement in sentiment despite ongoing strong asset price performance. China’s business sentiment remains sluggish, with August PMI manufacturing in contraction at 49.4 and nonmanufacturing hovering just above neutral at 50.3. We will be closely monitoring three key subcomponents: new orders (49.5), new export orders (47.2), and imports (48.0), all of which are in contraction. Services and construction business activities in the non-manufacturing sector will be closely scrutinized, especially the latter, which hit a new all-time low of 49.1, falling below the previous low of 49.3 in January 2025. We will see if services will be able to achieve further upside momentum on the back of the recently announced stimulus plan aimed at unleashing domestic consumption. The services business activities index rose 0.5ppt in August to 50.5, the fastest monthly gains since December 2024.

Taiwanese semiconductor exports remain strong, while trade talk between South Korea and the U.S. have stalled due to the recent immigration raid at a South Korean battery plant in Georgia. Talks with a view to reaching an agreement may resume during the APEC Summit from October 28–31, 2025, where President Trump and President Lee are due to meet. Taiwan’s August PMI came in at 47.4, off the July low of 46.2, and South Korea’s is hovering at the bottom of the range at 48.3. In contrast, sentiment in ASEAN rebounded strongly into expansion territory at 51, the strongest reading since August 2024, led by strength in Thailand, Malaysia and Indonesia. All eyes are on the potential impact of recent unrest and policy uncertainty on Indonesia PMI manufacturing, which surged 2.3 points to 51.5 in August. Japanese manufacturing and non-manufacturing sentiment, as measured by the Tankan survey has been relatively steady, hovering at the top end of the range. Market consensus is for such optimism to continue.

South Korea, Thailand, Indonesia and the Philippines will release August export and trade data. The fading of front-loading activities is likely to weigh on regional trade data, which has already been seen in the rest of APAC. The risk for data is firmly to the downside. Elsewhere, South Korea and Indonesia will release September inflation data. While it is important data to track, it is unlikely to have significant influence on near-term monetary policy decisions, with the Bank of Korea focusing on lending to households and growth sentiment, while Bank Indonesia is focused on near-term financial market stability.

On the monetary policy front, Reserve Bank of Australia (RBA) and Reserve Bank of India (RBI) will convene this week. The consensus is for both RBA and RBI to keep rates unchanged at 3.6% and 5.5%, respectively. That said, there is a small chance for RBI to deliver a pre-emptive rate cut to complement the decrease in the Goods and Sales Tax (GST) in view of the downside growth risk of 50% tariffs on exports to the U.S. Beyond that, the Reserve Bank of New Zealand, Bank of Thailand (under new Governor Vitai), as well as central banks in the Philippines, Singapore, Indonesia and South Korea are set to hold their meetings in October.

Forward look: Asia’s macroeconomic indicators are expected to remain volatile due to ongoing disinflation risks from low crude oil prices and uncertainty around export recovery, except for persistent export momentum in the semiconductor and chips sector. We are hopeful that governments and central banks will continue to implement supportive measures to limit downside growth risks. That said, the renewed strength of the U.S. dollar poses a fresh concern for APAC currencies and thus equity market sentiment. Indeed, we have seen foreign equity outflow pressure in Taiwan, following a long period of inflows for most of August. The recent market selloff in INR, IDR, KRW, PHP and THB has been significant and worth monitoring closely. Upcoming factors include potential measures in Thailand to address THB strength, Japan’s LDP leadership election on October 4, 2025, and the 4th plenary session of the 20th Communist Party of China Central Committee in October, which will focus on discussing the next five-year plan.

Markets are entering a period of heightened sensitivity to both data availability and political uncertainty. The potential U.S. government shutdown could temporarily deprive investors of official data, forcing them to rely more on private-sector indicators that are less transparent and widely shared, likely amplifying short-term volatility. In the U.S., the interplay between labor data and Fed policy expectations will be decisive, while in Europe, elevated services inflation and fiscal challenges will test central banks’ credibility and investor tolerance. APAC remains bifurcated: ASEAN shows resilience, but China’s sluggish sentiment and renewed USD strength add risks, particularly to local currencies and equity flows. For investors the coming weeks will require a sharper focus on alternative datasets, active monitoring of cross-market correlations and preparedness for higher volatility as markets recalibrate expectations. Positioning should balance defensive hedges against event risk, with select opportunities in regions or sectors benefiting from resilient growth dynamics (e.g., semiconductors in Asia, fiscal momentum in Europe) balanced by the FX rate and views of monetary policy being supportive. Gold is likely to continue to be the barometer of fear for USD and other fiat currency weakness overlayed by debt concerns.

Central bank decisions

Israel, BoI (Monday, September 29) – The BoI is expected to maintain rates at 4.50%, extending the current policy narrative amid sustained fiscal impulse and a tight labor market. Sequential inflation picked up materially in August to 0.7% m/m, well above expectations and contributing to combined price gains of 1% over two months in July and August. The real rate buffer of around 1.5pp is seen as adequate to anchor inflation expectations and the recent Fed cut would have provided further room for maneuvering. We doubt that a serious discussion regarding rate cuts is possible for the rest of the year. iFlow continues to support ILS’ strong funding status but recently selling appears to have moderated.

Australia, RBA (Tuesday, September 30) – The RBA is expected to keep rates on hold at 3.6% amid mixed signals in the economy. The August labor market report clearly pointed to the need for additional support, but inflation surprised to the upside on a headline basis for the same month, and broader indications of household demand remain relatively firm. We continue to see the RBA easing up ahead, but terminal rates will stay well above 3.0% and the pace of easing will be cautious at best. AUD valuations remain relatively attractive, and we continue to see strong upside potential on a relative value basis. However, much will also depend on the willingness for domestic funds to reduce their FX exposures, which will be a slow process.

Colombia, BdlR (Tuesday September 30) – Rates are expected to remain unchanged at 9.25% in Colombia as annualized inflation rebounded above 5% y/y again in August. However, sequential inflation is manageable, and the real-yield buffer is very strong at well over 400bp. However, we have started to see some hedging flows pick up in COP as LatAm exposures remain very high across the board. The Fed cut and high local real yields will continue to support duration – which is reflected in flows – but currency hedging will rise, even for very high yielders such as COP. Relations with the U.S. and tariff issues could lead to incremental hedging interest as well.

India, RBI (Wednesday October 1) – We expected the RBI to deliver a pre-emptive 25bp rate cut to mitigate the potential drag from 50% tariffs on exports to the U.S. This expectation is reinforced by recent rate reductions in the U.S. Although a weaker rupee may argue against easing, past precedent suggests otherwise – RBI cut rates in February 2025 when USDINR hit then record all-time highs in February 2025. iFlow shows strong inflows into the INR at present. Although there is a case for carry, such purchases combined with asset exposure adjustments point to an element of hedge unwinding in place.

Data Calendar

Event Calendar