From Teton to Tianjin

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Geoff Yu

Time to Read: 13 minutes

Last week’s run-up to Fed Chair Powell’s Jackson Hole speech was the first indication this quarter that U.S. equity markets need to scrutinize earnings prospects up ahead. As much as Fed easing can help with the “soft landing” narrative, tech holdings, especially in semiconductors, have acknowledged the risk that what was meant to be a secular investment story could have some cyclical aspects to it, especially if end demand to justify capital expenditure levels are not as strong as anticipated. As the summer winds down, central bank officials leaving the Teton Range in Wyoming will be back on wires globally to offer their initial outlook for September decisions and forecast revisions, and as things stand Fed divergence vs. European peers looks set to widen further, and the dollar is already reacting accordingly. However, the sustainability of these trends will be called into question if various Eurozone inflation prints surprise to the downside, while national accounts figures of U.S. trading partners will likely show further weakness in Q2 assessments: Germany already registered a deeper than expected contraction, and the Canadian and Swiss releases this weak are both expected to be soft, and this represents a period even before trade relations with the U.S. deteriorated. Meanwhile, the geopolitical center of gravity will shift east this week to Tianjin, as over 20 heads of state arrive for the summit of the Shanghai Cooperation Organisation (which only has 10 members), including President Putin of Russia and Prime Minister Modi of India. Although we see the theme as still more talked about than actioned upon, “diversifying” from U.S. exposures will likely feature highly on the economic agenda, with India in particular focus as the August 27 implementation deadline approaches.

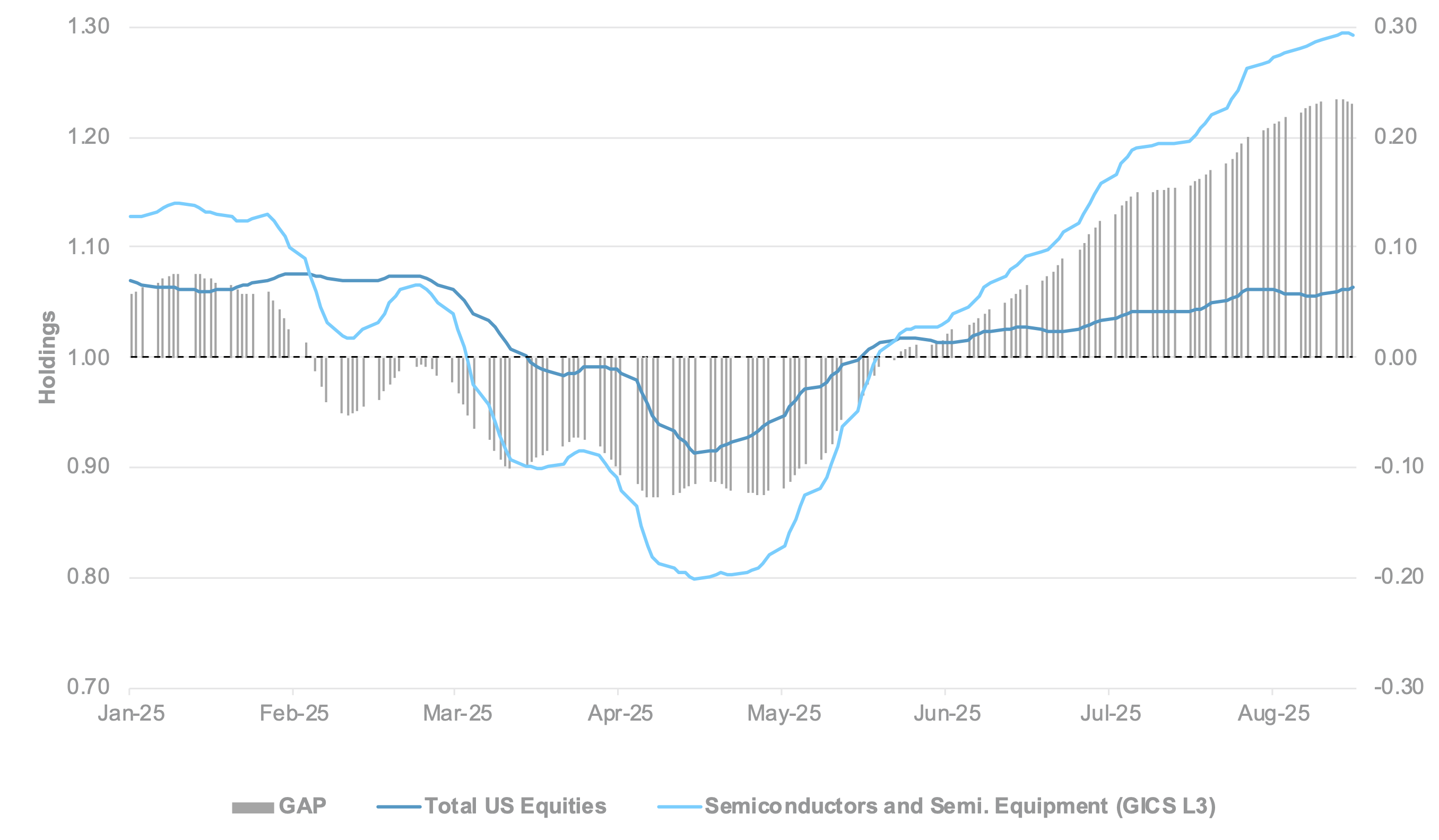

Equity holdings’ reliance on semis now at highest levels of the year

EXHIBIT #1: U.S. SEMICONDUCTOR EQUITY HOLDINGS VS. TOTAL U.S. EQUITY HOLDINGS, ALL CLIENTS

Source: BNY

Our take: Our data show that the holdings gap between total U.S. equities and this segment is now at the highest levels of the year; after Friday’s recovery in the wake of Powell’s comments, the outperformance gap can probably extend until the September Fed decision. Even so, if the excess weighting is due to expectations of long-term revenue and earnings growth through both demand expansion and productivity gains, how the Fed behaved during its much shorter forecast horizon should not have mattered. The fact that it did suggests that these relatively concentrated holdings are now exhausting idiosyncratic drivers and simply relying on a higher market beta up ahead. Geopolitical interference in external demand has not helped matters either. In a benign environment, the convergence or reduction in the holdings gap should be due to other sectors starting to perform better, even benefiting from any “trickle-down” effect from high levels of capex in the tech sector. If this fails to happen, then Powell’s more circumspect view on the state of the labor market and future demand should speak volumes about the decomposition of U.S. growth: consumption’s traditional role cannot be discounted so quickly. Even if wage growth is strong, stagflation will eat into real earnings and purchasing power, and household-exposed companies fear the full effects of this have not fully made their way through the economy.

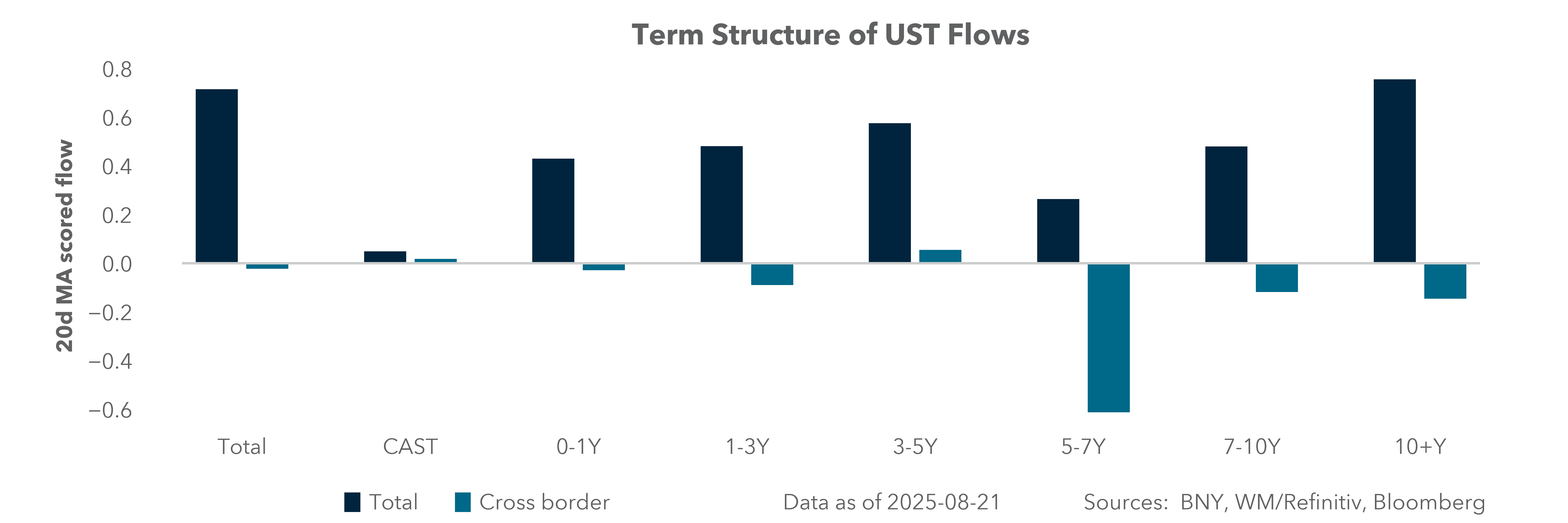

Forward look: If the Fed does realize 50bp in easing for the rest of the year, we expect bond markets to be relatively contained and the recent dip in cross-border holdings of Treasurys to start reversing. Similar to April, policy or institutional discounts, as much as growth, may feature in U.S. asset holdings. When there is adequate compensation in the form of yields and/or the value of the dollar, cross-border flows will continue to find U.S. assets attractive, and such purchases should set a floor for the dollar. Furthermore, we are not suggesting that external markets are not exposed to a similar rotation risk. While geopolitical risks have subsided for now and the Eurozone itself is not at risk of stagflation, the lack of fresh growth narratives and secular weakness in external demand makes Friday’s new record on the EuroStoxx 600 difficult to justify. The rally in Chinese equities to a decade high faces similar scrutiny, as the surfeit of retail participants will need macro and company earnings validation soon. Finally, we stress that tariff issues have not gone away: U.S. semiconductor and global pharmaceutical companies will soon learn about sector-specific tariffs and any retaliatory measures, especially non-tariff barriers. U.S. demand has weighed heavily on the global economy, but the risk of “reciprocation” may also need to be re-priced for U.S. sector and industry holdings as well.

North America: Fedspeakers to continue post-Jackson Hole guidance

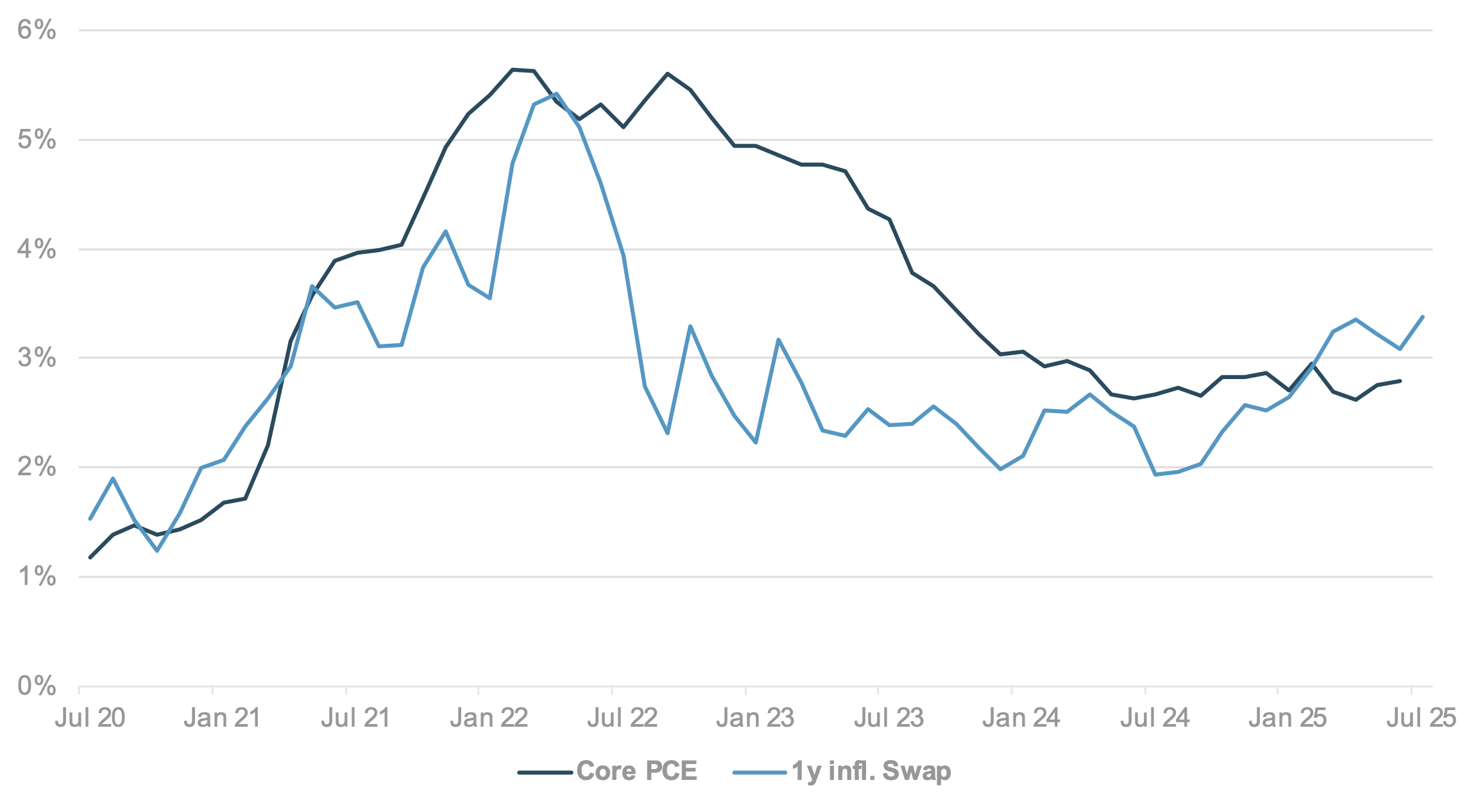

EXHIBIT #2: CORE PCE AND INFLATION EXPECTATIONS

Source: BNY, Bloomberg

Our take: With Jackson Hole behind us, and the FOMC likely to cut rates in September, we still need to watch the incoming data over the next few weeks to determine how dovish the Fed can actually be after September. We are somewhat concerned that inflation developments will worsen as tariff effects come through, even as the economy slows. We don’t think Powell’s speech was a full-throated cry – yet – for an aggressive easing cycle, as he clearly shares our concern over potential inflation developments going forward. In this context, the week’s data – and the roster of Fedspeakers slated to make appearances during the week – will go a long way toward determining the course of policy after September. Furthermore, despite a strong defense of central bank independence by various officials in Wyoming, the matter will remain the center of attention in the U.S. as President Trump has stated he will remove Fed Governor Cook if she doesn’t resign.

Forward look: Real economy data comes through early in the week, with durable and capital goods orders on Tuesday and a number of manufacturing and services PMIs throughout the week. The second print of Q2 GDP on Thursday will be less important, while consumer confidence from the Conference Board (Tuesday) will give us a read on inflation expectations and the household sector’s current mood. Finally, inflation itself will be addressed on Friday with the PCE deflator. Given the read from CPI and PPI earlier in the month, we have a pretty good idea that core inflation will be running at close to 3% a year, setting up a situation where we see rising inflation but dovish policy expectations. In Canada, there appears to be some movement on trade relations with the U.S., which was not previously adequately reflected in CAD performance, in our view. News of retaliatory tariff removals on U.S. products will be an important step forward, and there may be added impetus on such measures if upcoming national accounts confirm a significant economic contraction in Q2 (–0.3% q/q expected), with June’s growth (0.2% m/m expected) only marginally better than the May contraction of –0.1%m/m.

EMEA: September cut to rely on downside inflation surprises

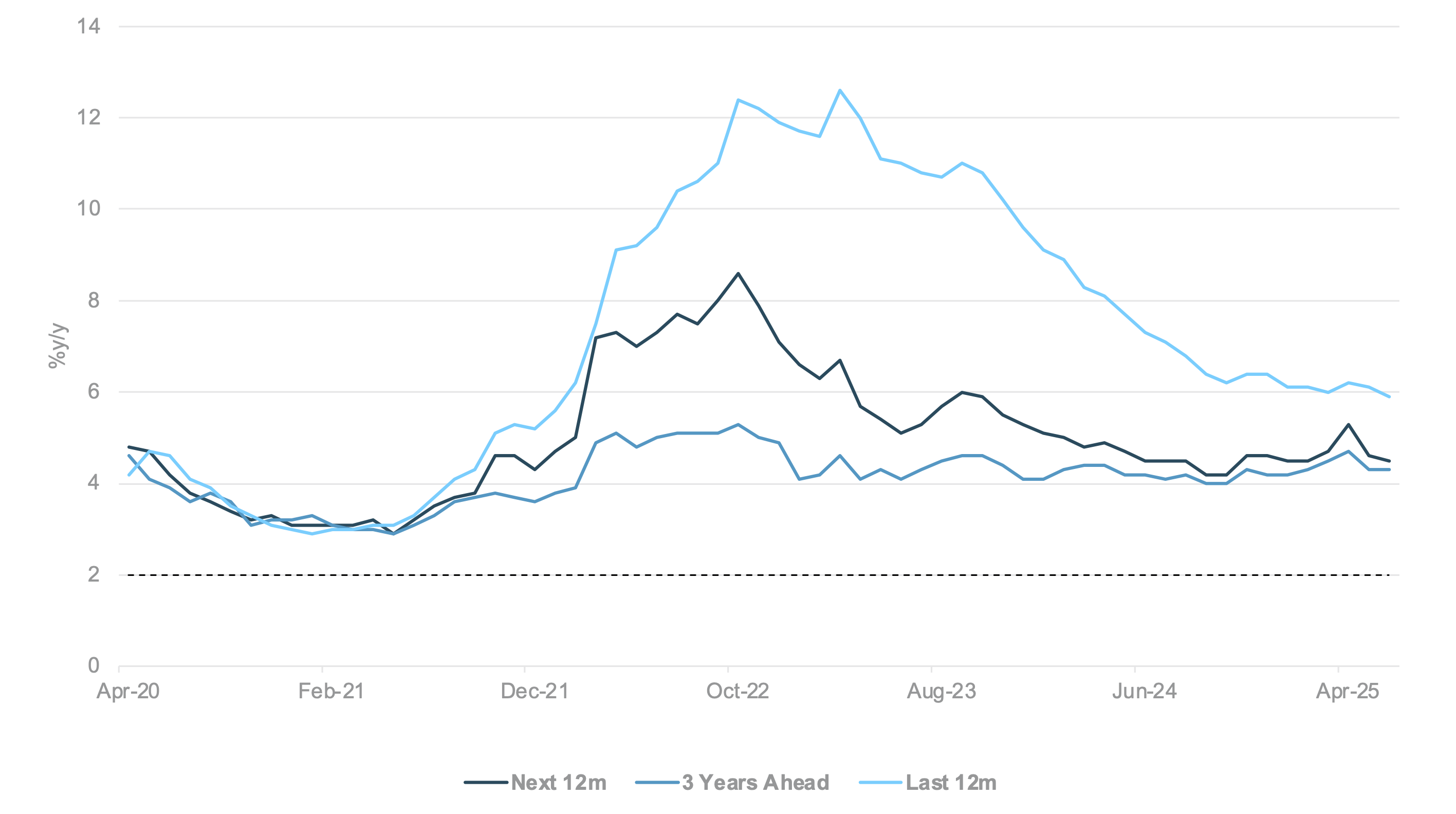

EXHIBIT #3: ECB SURVEY SHOWS INFLATION EXPECTATIONS REMAIN WELL ABOVE TARGET

Source: BNY

Our take: European Central Bank participants at Jackston Hole were amongst the most vociferous regarding central bank independence, but also needed the least vigilance on inflation or stagflation. Bundesbank President Nagel stressed the need to “fight” for central bank independence but was even confident enough to say that inflation was “not the point anymore,” and was very much at ease with the level of the euro, ultimately warning against expecting rate cuts due to the “high bar.” Such confidence will be tested in the weak ahead as Germany’s preliminary August CPI figures are released, but the market is anticipating a slightly below-target print of 1.9% y/y in HICP, but monthly sequential inflation is expected to remain flat. We continue to take issue with the notion that this, in Nagel’s words means, that inflation is “not the point.” Notwithstanding other price drivers, this take is not symmetric with respect to the ECB’s inflation target, as it implies greater downside risk to prices for the rest of the year is less of an issue compared to the prior overshoot, which required aggressive intervention. The current external demand environment does not justify benign neglect on the euro. Furthermore, we also challenge the notion that current euro levels are tolerable or, in Nagel’s words, “near the long-term average,” so are not cause for concern. Similar arguments were made by his peers in July, but there was a sharp shift in price data and growth expectations due to trade challenges. Most importantly, EURUSD is still significantly above the June base case and we have more sympathy with President Lagarde’s recent intimation that September forecasts would entail some changes.

Forward look: Germany aside, inflation figures will be released across the Eurozone, along with the latest ECB inflation expectations update. French inflation is expected to remain at 1.0% y/y, but sequential prints may pick up strongly to 0.5% m/m. By contrast, Italian inflation is expected to contract on a monthly basis and annualized HICP is expected to remain well below target. Spain’s general economic outperformance continues to be reflected in price strength, though another annualized HICP print close to 3% is not expected to meaningfully lift overall numbers. As for soft data, the ECB will also release its latest monthly inflation expectations survey, and the hawks can point to a forward outlook that remains well above 4% (Exhibit #3) to justify price growth vigilance. For industry, the Ifo Business Climate figure is expected to remain broadly unchanged at 88.8, but this will be the first Ifo release since the U.S.-EU trade deal was broadly agreed and not to the best of receptions. Given the ongoing pressure on the European automotive industry, we believe downside risk to the expectations index (expected to dip to 90.5) remains in place, though this has not been borne out by the recent PMI surveys, leading to some reports suggesting that the ECB believes the worst trade-related stress is over. Even if tariff arrangements are stable for now, the demand outlook remains challenging and this is where tolerance of a strong euro could come back to hurt the ECB’s policy assessment.

APAC: South Korea sentiment, Tokyo and Australia CPI and BSP and BoK policy meetings

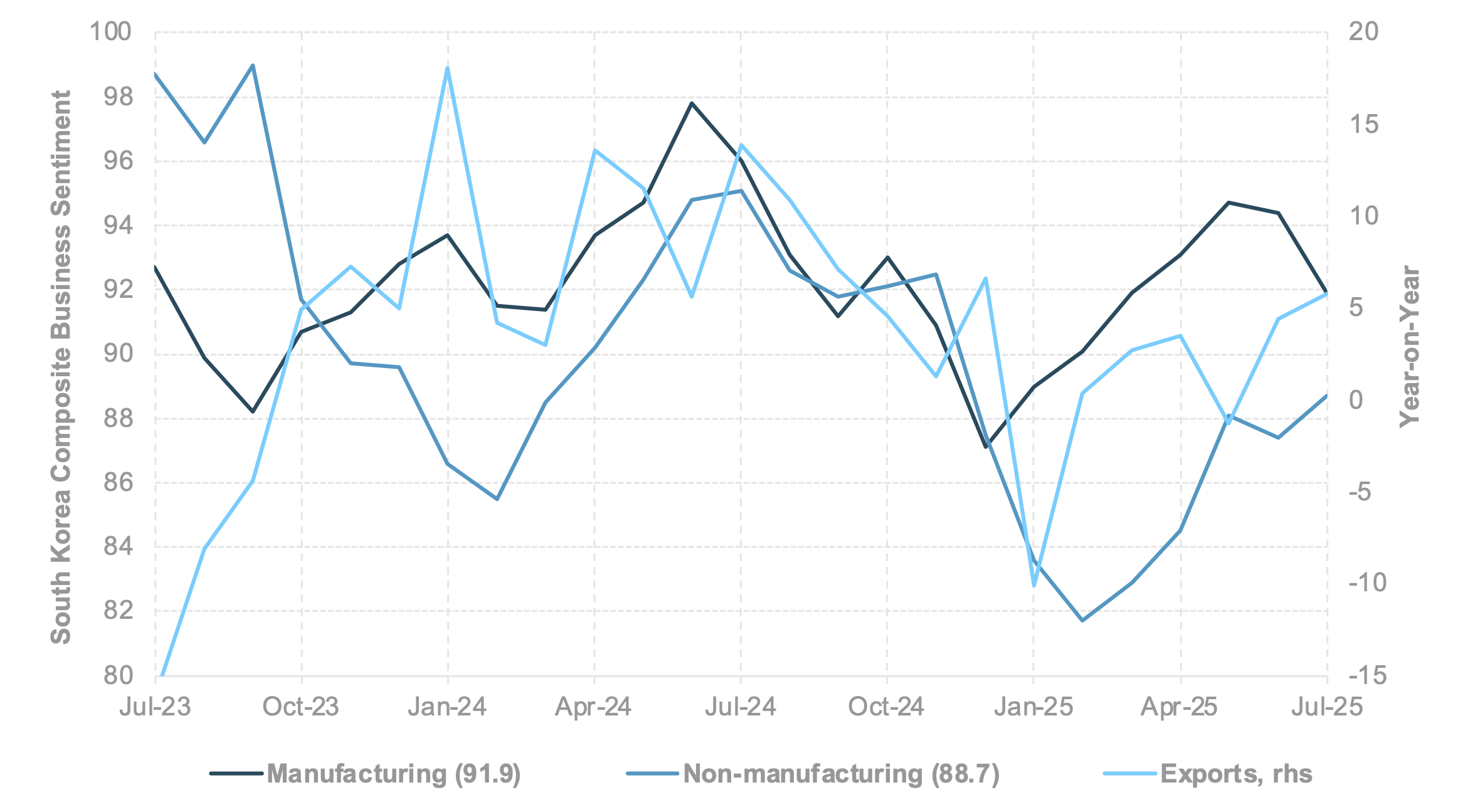

EXHIBIT #4: BUSINESS SENTIMENT RECOVERY IN SOUTH KOREA

Source: BNY, Bloomberg

Our take: In the Asia-Pacific region, this week’s focus will be on consumer confidence and business sentiment in South Korea, industrial production data in Taiwan, Thailand, India and Singapore; inflation readings in Singapore, Australia and Japan; and monetary policy decisions from the Philippines’ BSP and the Bank of Korea. As tariff-driven front-loading fades in H2 2025, upcoming economic data will be closely watched for signs of sustained momentum. South Korea’s composite business sentiment has softened over the past two months following a strong H1 recovery, driven by monetary and fiscal stimulus. While sentiment is expected to stabilize, it will depend on the pace of domestic recovery. The Bank of Korea’s policy decision this week, along with updated macro projections, will offer further insight. The latest forecast from May 2025 anticipates GDP growth accelerating from 0.8% in H1 to 1.4% in H2, with continued momentum into 2026. Production data will provide early signals for Q3 growth. Taiwan’s output should benefit from semiconductor strength (June: +18.6% y/y), while Thailand’s manufacturing remains weak (+0.58% y/y) amid soft demand. India’s slowing industrial growth (+1.5% y/y) may worsen under new 50% U.S. export tariffs. Inflation updates from Singapore (June headline: +0.8% y/y, core: +0.6% y/y), Australia (June trimmed mean CPI: +2.1% y/y) and Tokyo (CPI: 2.6% y/y) will be key. Singapore’s disinflation trend suggests front-end rates may stay low. Australia’s CPI and labor data will be pivotal ahead of the RBA’s September meeting. Japan’s inflation and jobs data continue to support further Bank of Japan tightening. On the policy front, the consensus expectation is a 25bp rate cut from both BSP (to 5.0%) and Bank of Korea (to 2.25%).

Forward look: Despite fundamental expectations for APAC currencies to weaken amid growth concerns and tariff uncertainties, the opposite has occurred. Year-to-date, APAC currencies and asset prices have posted strong gains, driven by robust foreign investment inflows, a softer U.S. dollar, and supportive monetary and fiscal policies. In China, while this week’s data calendar is light, market attention is turning toward October’s Fourth Plenum of the Central Committee, where the next five-year plan will be discussed. Meanwhile, the focus is on the fresh round of consumption-targeted stimulus measure and sharp bear-steepening of the Chinese government bond curve. Excluding the influence of the U.S. dollar, the Indonesian rupiah (IDR) stands out as our top pick within APAC. It is supported by a favorable 2026 budget outlook, a constructive asset environment, and strong inflows into Indonesian government bonds. In contrast, we remain neutral on the Chinese yuan (CNY), despite a strong rally in domestic equities. The rally has been largely driven by local investors, and we continue to monitor foreign inflows into Chinese equities as a potential catalyst. The Indian rupee (INR), however, remains vulnerable to the negative impact of tariffs, particularly those affecting exports, which could weigh on sentiment and performance.

Fed Chair Powell delivered his Jackson Hole address without incident, but this doesn’t mean the coast is clear for equities to continue rallying into the September Fed decision. After all, Powell stressed that the downside risk to employment is rising, which justifies some policy adjustment, and this will directly challenge the current demand narrative in the U.S. Even if risk sentiment can rely on a secular technology capital expenditure narrative, tolerance for industrial vs. household divergence can only go so far as these industries do not operate in isolation. If households begin to retrench due to fears over employment income, primary investment intentions will also follow, which will subsequently impact technology and communication services names, which rely on sustained growth from business and household demand. Global sentiment has also cheered the prospect of easier financial conditions from the Fed, but the risks from softer U.S. growth cannot be dismissed. With European equities hitting record highs and Chinese equivalent rallying to decade highs, both with significant concentration risk in investment target (defense and tech) and investment source (excessive retail participation in China), the bar is low for adjustments if companies struggle to deliver on expectations. If we take the ECB’s statements at face value, they have limited capacity to ease further, while APAC rates are almost universally lower than European peers. The Fed is fast becoming the sole global source of easing in financial conditions, through rates and a weaker dollar. These are not strong push factors for the global growth cycle to reverse, and allocations will need to be highly vigilant against rotations in a defensive direction, and much more forcefully than what was observed last week.

Central bank decisions

Hungary, Magyar Nemzeti Bank (August 26, Tuesday). We believe the MNB will keep its base rate on hold at 6.50% at its policy meeting on August 26. July CPI was 4.3% year-on-year (0.4% m/m), remaining above the 3% target and the 2–4% tolerance band, negating any need for easing as restrictive conditions are necessary. The July meeting minutes highlighted persistent upside risks and still-elevated household inflation expectations, and said forward guidance remained unchanged, calling for a careful, patient approach. July’s communication also noted inflation is expected to decline back to the tolerance band only in early 2026 and to reach the 3% target in early 2027. With short-term rates aligned with policy settings and only one option discussed in July (no change), guidance points to stability next week. Hungarian assets are very well-held at present, and we believe some FX hedging could rise.

South Korea, Bank of Korea (August 28, Thursday). We expect the BoK to cut rates by 25bp to 2.25% at the August meeting and maintain a dovish stance. While H2 GDP is likely to be better than H1, risks remain firmly to the downside. The ongoing concern over household indebtedness is, in our view, not sufficient to halt the BoK easing cycle. All eyes will be on the BoK’s latest update on the macroeconomic forecast. As of May, the BoK forecast H2 GDP to rebound at 1.4% y/y (H1: 0.8%) to bring the 2025 GDP forecast to 0.8% and rebound to 1.6% in 2026. Headline and core inflation are seen at 1.9% in 2025 before easing to 1.9% in 2026.

Philippines, Bangko Sentral Ng Pilipinas (August 28, Thursday). We see the BSP delivering a third consecutive rate cut, trimming the rate by 25bp to 4.75% at the June meeting, given the declining inflation trajectory. We expect the BSP to maintain a dovish stance and reiterate its commitment to a measured approach in deciding on further monetary easing. The BSP has indicated a possible 50bp rate cut for the remainder of the year. The pace of easing, if any, into 2026 is likely to be more constrained with projected higher inflation, driven by the normalization of food prices. Note that rice inflation was

–15.9% y/y, and the latest 2025, 2026, and 2027 risk-adjusted inflation forecasts are 1.6%, 3.4%, and 3.3%, respectively, as of June 2025.

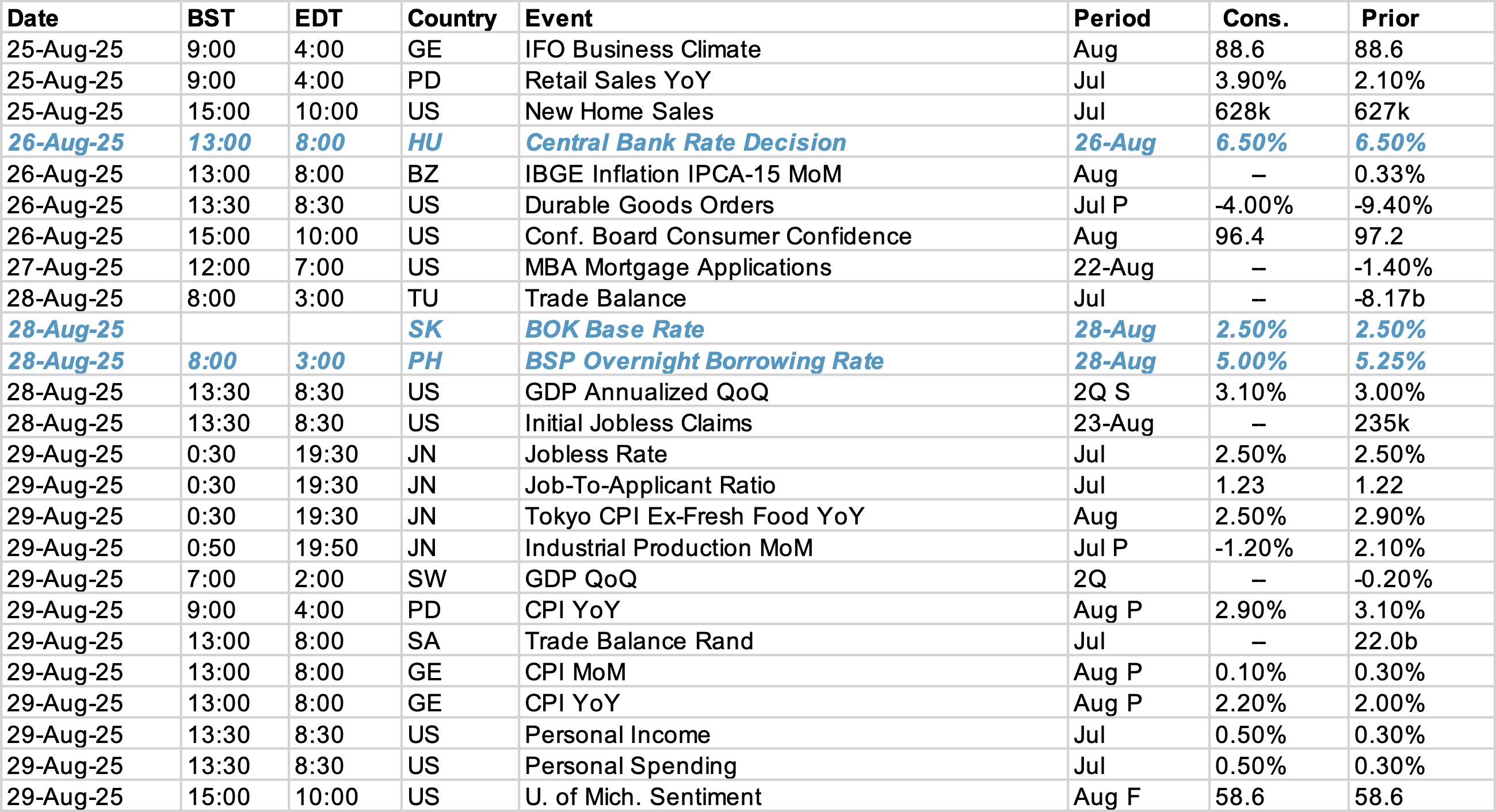

Data Calendar

Event Calendar