Fatigue

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 14 minutes

Confessional period for Q1 earnings performance on the docket for risk, along with potential diplomatic breakthroughs for Ukraine and reciprocal tariffs for EU, Canada.

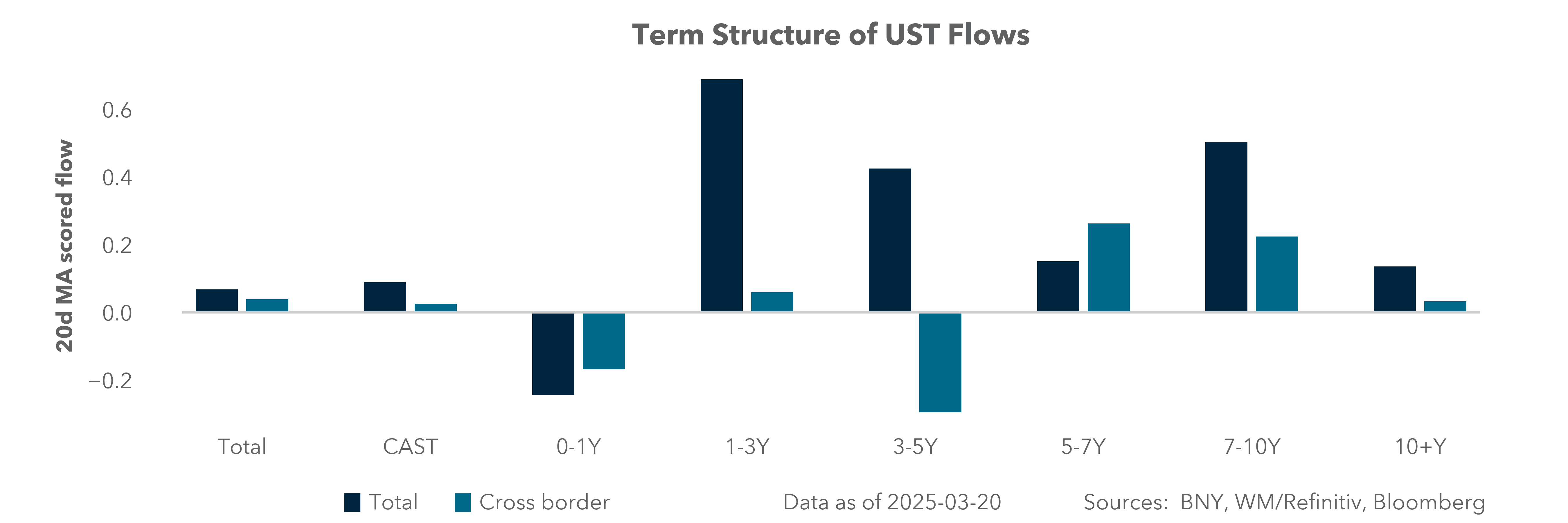

Quarter- end rebalancing favors AUD, NZD, USD, and CHF, while in duration extension risks will balance supply and equities may continue to shift out of growth plays into value.

The burden of proof for Q2 stability will be on Europe and APAC to show growth and justify ongoing money flows, risk next week in global PMI flash reports.

The last full trading week of March is usually focused on Q2 risks and rewards with rebalancing and reweighting of risks after Q1 returns. The clear rotational trade out of US tech into EU defense and China tech looks set to be tested. The confessional period between Q1 ending and company earnings reporting is upon us and that generates real volatility as companies pre-announce unwelcome news. The value proposition of buying US shares after a 10% correction will be part of the balancing game for traders in the week ahead – ongoing uncertainty dominates. Cash and safe havens remain the counterbalance to any larger shift in strategy. In the mix, fixed income with more supply from the US government – 2y $69bn, 2y $28bn FRN, 5y $70bn and 7y $44bn – coupled with ongoing corporate issuance expected at $25-30bn ahead of tariffs. Rate cuts remain in the US price but not enough to change the value calculation in bonds or stocks.

The lessons of Q1 were that the Fed S&P 500 “put,” a.k.a. the Trump “put” on shares is stuck far out of the money – the moves in equities need to be much more dramatic to shift financial conditions sufficiently to spark policy shifts by Powell or Trump. The rest of the world will be watching for geopolitical compromises – a ceasefire in Ukraine or Israel, along with negotiations over trade with the US Trump administration. As for politics – the South Korea court impeachment ruling and expected election to follow it, along with Canada PM Carney snap election call are expected but matter to how markets set up for Q2. A larger focus will be on the UK budget with GBP and gilts both underperforming after the BoE remained on hold and stagflation fears rose. Economic data will become more important amid uncertainty, along with the balance of bond yields. Some of the key economic data and events expected this week include:

Global flash PMI reports, which will be watched to confirm global uncertainty slowdown and inflation risks – along with Japan Tokyo CPI, Australian CPI, US durable goods and US Q4 core PCE.

Australia and UK budgets, which will be watched for fiscal stimulus and market responses – rate volatility expected to return to global bonds

Norway, Hungary and Czech central bank rate decisions expected to remain on hold, while Mexico is expected to cut 50bp. Fed and ECB speakers are also important given ongoing uncertainty.

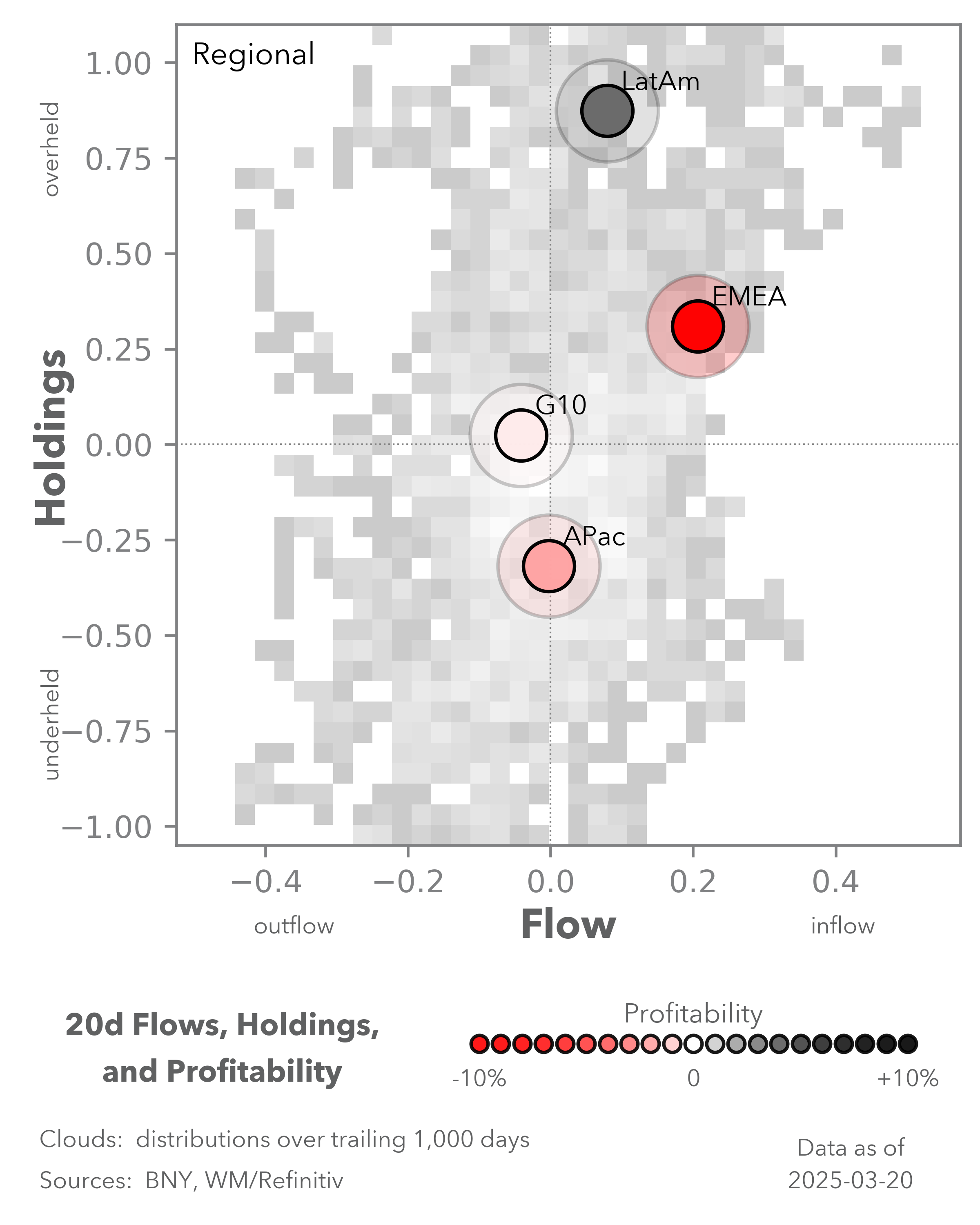

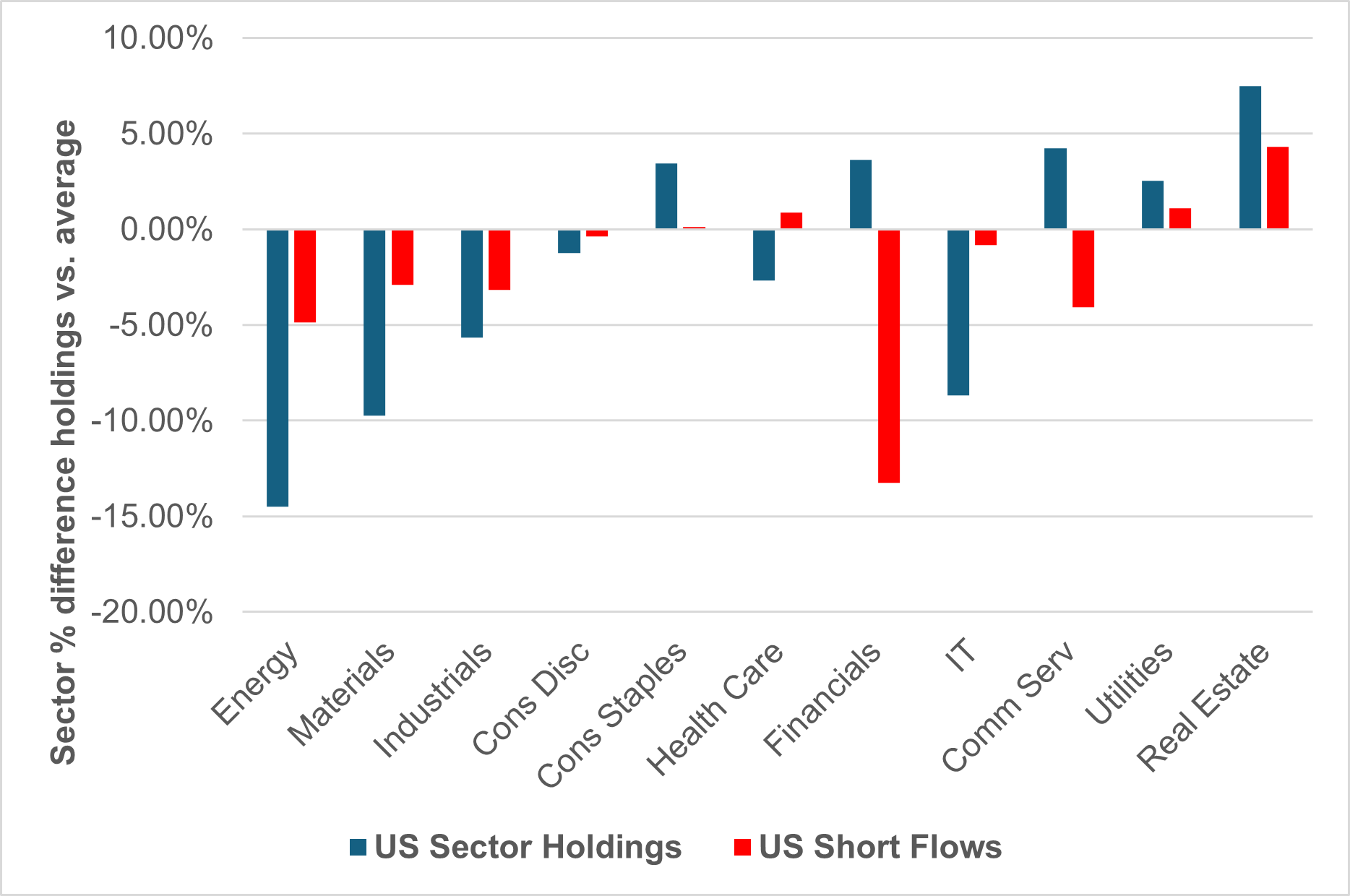

EXHIBIT #1: DOMESTIC VS. FOREIGN FOCUSED SECTORS IN US SECTORS – AND SHORT FLOWS

Our data shows that US sector flows have been domestically biased. Net holdings in energy, materials, industrials and IT reflect outflows, while more domestic-facing sectors are holding near their average. Our short equity positioning suggests faster more active clients are betting against slower real money underweights. This suggests range trading could prevail in the week ahead with Q1 rebalancing. We expect a series of diplomatic meetings to avert extreme tariffs eventually, but not by April, leaving the sequencing concerns over Trump’s policy shifts continuing to move markets with ongoing economic uncertainty.

Source: BNY iFlow

Our View: The lack of clarity on how global economies will manage the planned tariffs set for April 2 will be the dominant driver for risk going forward. The consensus calls for tariffs across markets shifted from wait and see to pre-emptive reactions by Europe and China and new fiscal stimulus, but most central bankers see tariffs causing transitory inflation and it is impossible to forecast the long-term impact on their economies. The consensus now is for downside risks to growth and upside risks to inflation, making 2025, like 1975, a year of stagflation.

Forward Look: US stocks could be less volatile, but US bonds and the USD remain at risk for tariffs. US tariff policies have three seemingly incompatible goals: 1) to drive trade partners to negotiate lower tariffs and fairer trade with the US; 2) to retore the US industrial base, from computer chips to autos to shipping; 3) to shift federal receipts from income taxes to tariffs. However, if point 1 is successful,, then point 2 will require other incentives, and point 3 will prove insufficient. All of which puts the key focus on US jobs and corporate cost-cutting for determining the cost of uncertainty on the economy.

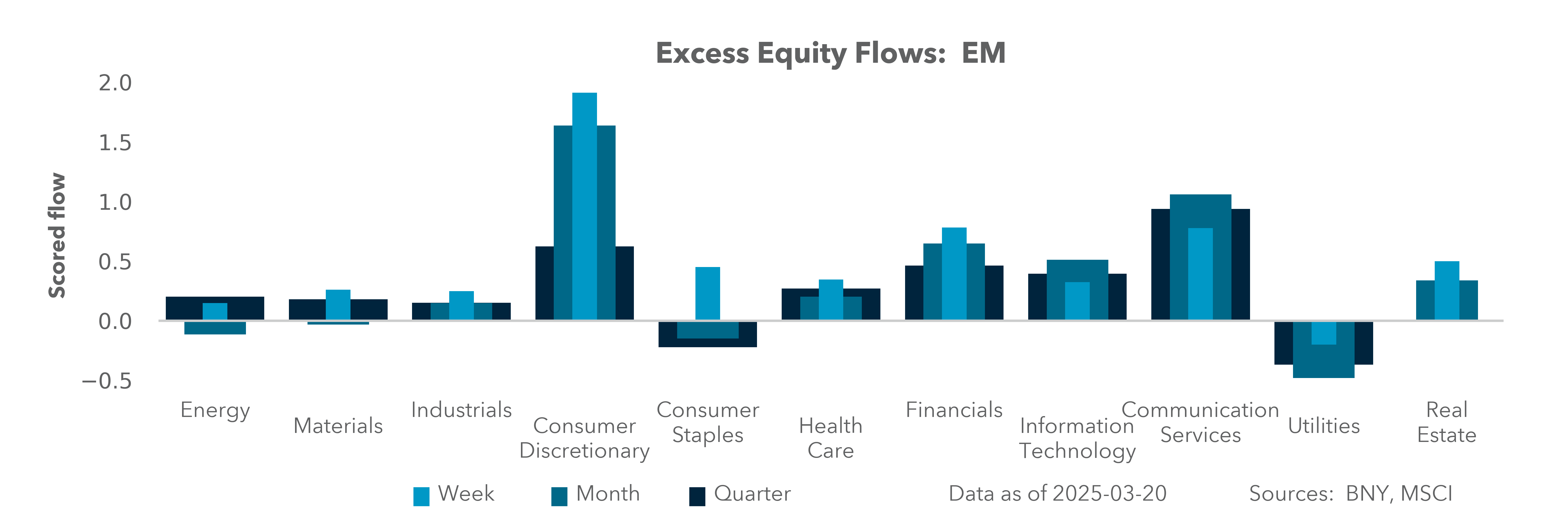

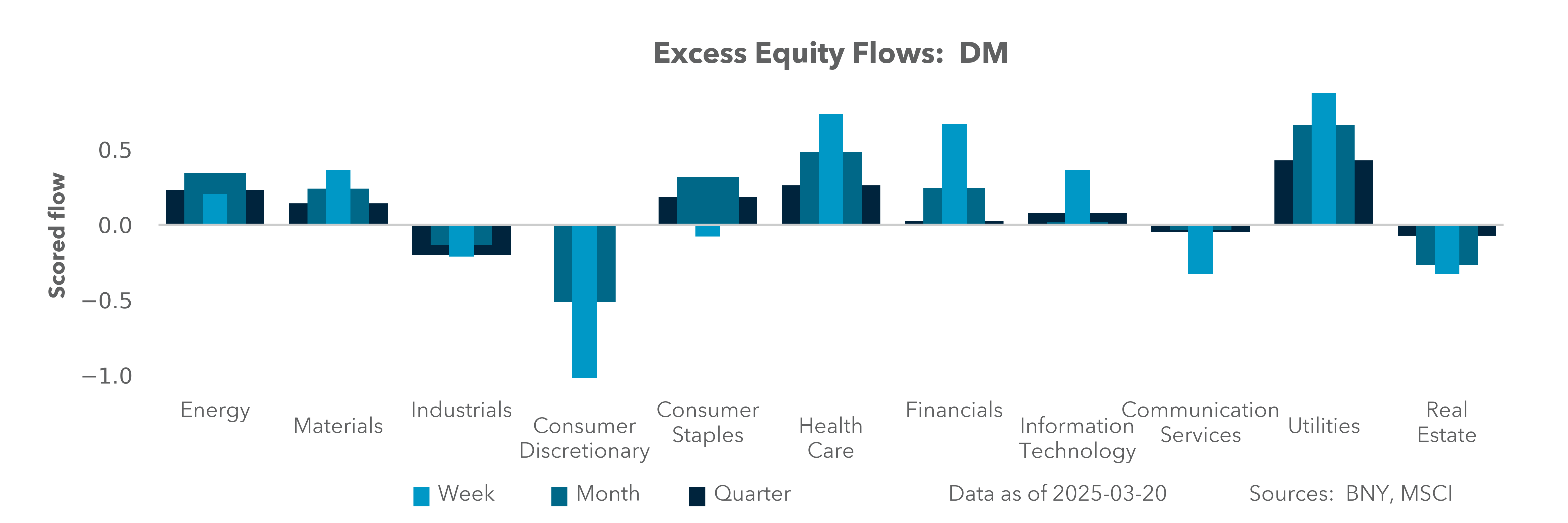

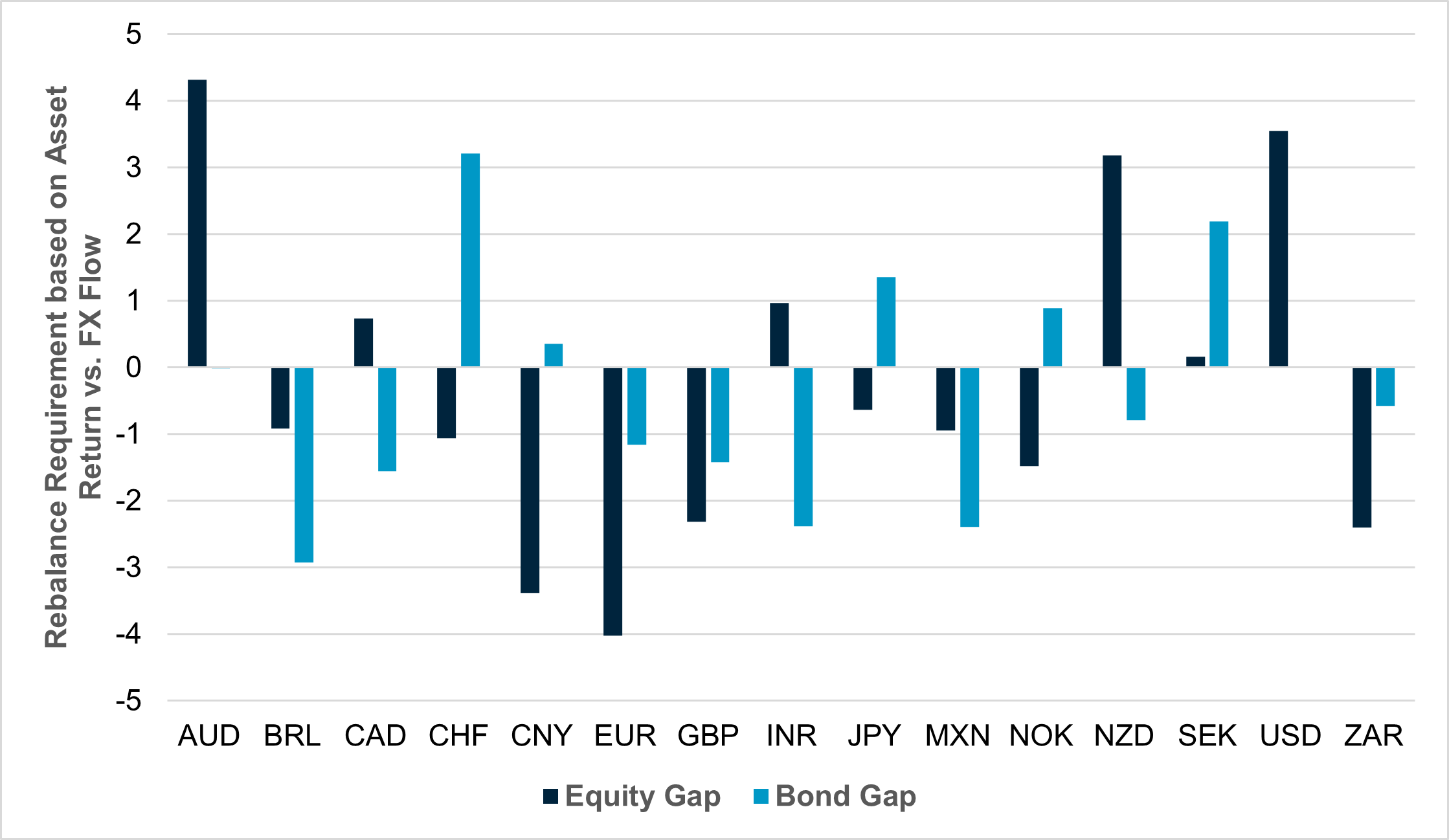

EXHIBIT #2: MONTH-END REBALANCING GAPS FROM STOCKS AND BOND PERFORMANCE IN MARCH

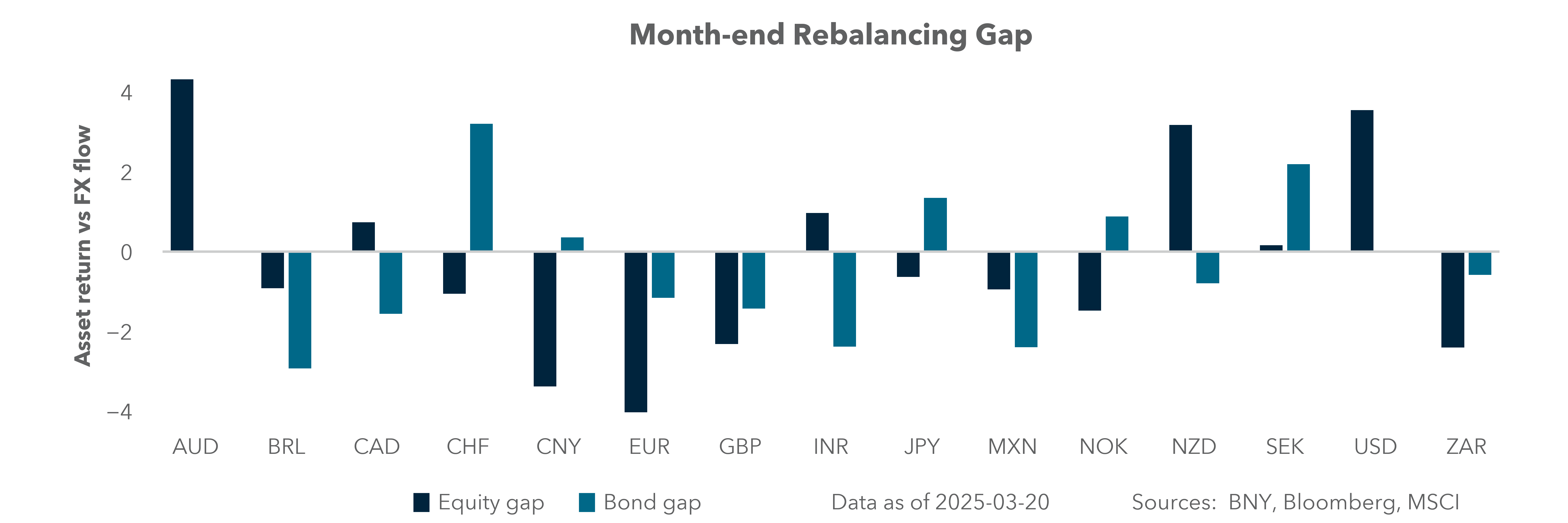

Source: BNY, Bloomberg, MSCI

Our View: The selling of US shares and buying of EU shares stands out in the month, but the start of the earnings season in the US is still three weeks away, with many investors willing to wait rather than aggressively rebalance into tariff uncertainty. Similarly, bond markets are stuck, with central bankers waiting for clarity before further easing cycles. Fiscal spending has revived concerns about debt-to-GDP ratios, causing a return to yield curve-steepening trades.

Forward View: Unless markets get a surprise solution to geopolitical risks and tariffs, triggering a rally back in risk, expectations for less of a Q1 rebalancing dominate. Some of the recession risks will find solace in duration. Bonds will be balanced by supply. Leaving the biggest risks for month-end in FX, with buying of AUD, NZD, USD and SEK against EUR, CNY, BRL and ZAR expected.

North America: Fedspeakers and Canada election watch

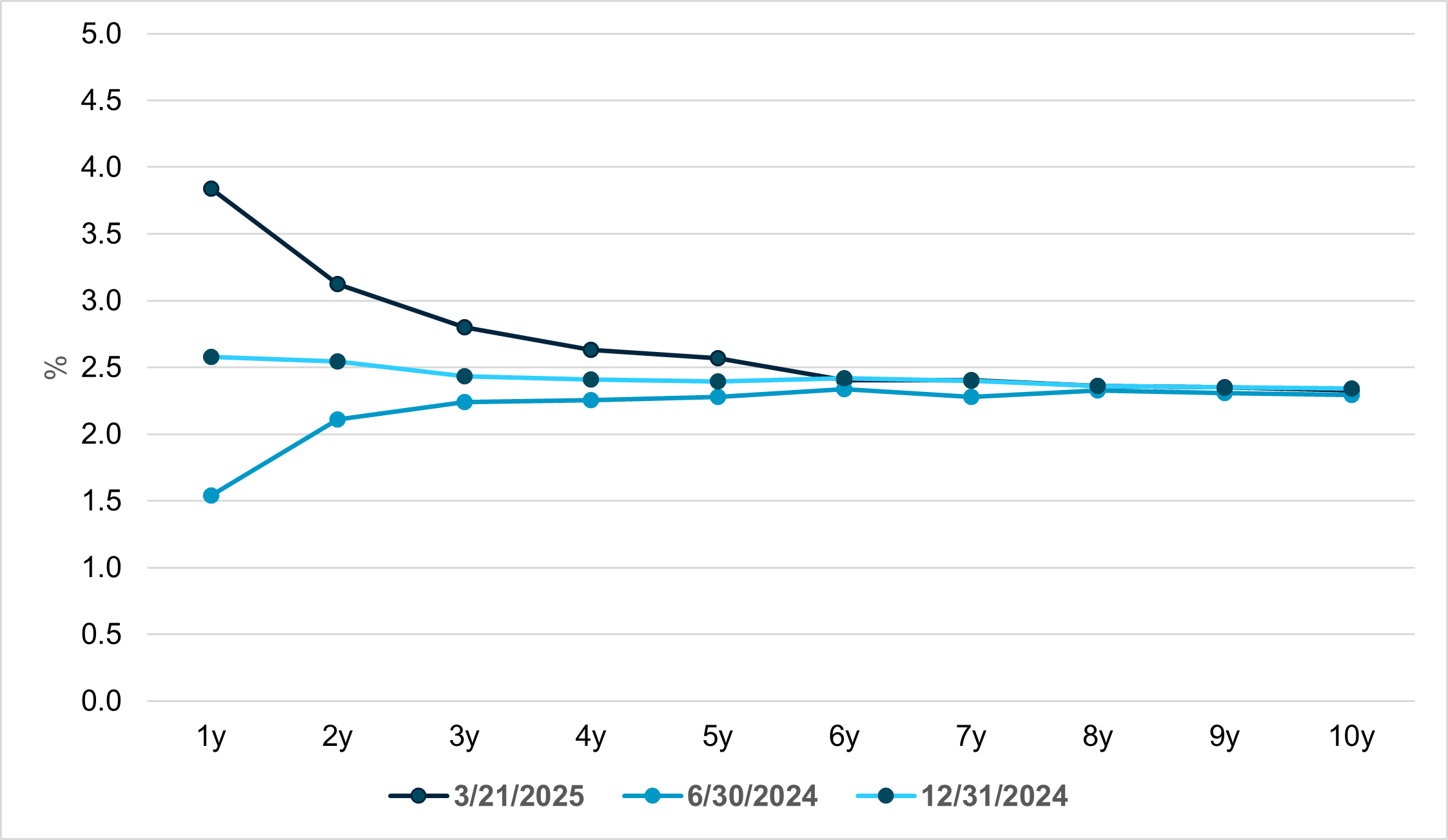

In North America, it is a quiet week for the economic data calendar, although in the wake of last Wednesday’s FOMC a number of Fedspeakers will be out to explain their views. We do not expect too much to come from these appearances given the uncertainty that has plagued markets and the Fed since the new administration’s inauguration in January. This was highlighted by the number of mentions of “uncertain” and “uncertainty” in the press conference, which by our count was 18 times. Chair Powell’s assertion that the Fed did not believe that short-term inflation stemming from tariffs would not be persistent (he even used the discredited term “transitory”) led to a dovish reaction in markets during the second half of last week. We note that in the chart below, 1- and 2-year inflation expectations are quite elevated, but longer-term inflation expectations are indeed contained and “anchored,” something the Fed will keep an eye on.

On the other hand, Bank of Canada Governor Macklem, in a speech last week, seemed more concerned about short-term inflation coming from a trade war with the US, declaring that keeping inflation expectations under control was essential, and casting doubt on another rate cut at the Bank of Canada’s April 16 Governing Council meeting. While we have been bearish on the CAD since November, this potential pause in the cutting cycle could see some consolidation of USD/CAD around current levels. We are also on watch for Canada PM Carney’s snap election call – his choice of timing matters to how both Canada and US markets trade with tariffs clearly a key part of the election.

EXHIBIT #3: US INFLATION EXPECTATIONS ARE STILL ANCHORED IN THE LONG TERM

Source: Bloomberg, BNY

UK budget

When a recession is perhaps the solution

As the OECD warns of global stagflation risk in its latest forecast round, many governments may need to reluctantly acknowledge that they themselves are the problem. In 2023, ECB President Lagarde remarked that the public services sector was one of the sectors with low productivity holding up wage-based inflation. One way out is for public spending to be redirected toward productivity, which the Eurozone is now making a good attempt at, but only because Germany can credibly do so with its fiscal resources.

Another rarely deployed tool to generate faster disinflation is deep spending cuts. As the Trump administration is currently discovering, doing so is fraught with political risk. Last week Brazilian Finance Minister Haddad also stressed that the country “did not need a recession to bring inflation down.” Implicitly, this means recession is an effective inflation-fighting tool.

However, if we take the case of New Zealand, this is exactly what happened and in hindsight this was the least painful path. The country has now officially exited a short recession and inflation slowed quickly enough for the RBNZ to subsequently cut rates aggressively. We acknowledge, though, the current New Zealand government was elected on a fiscal consolidation mandate.

This week, we expect UK Chancellor Reeves to also start this difficult journey. The experience of the mini budget in 2022 has rendered UK chancellors exceptionally welded to fiscal rules. As fiscal headroom has run out (Exhibit #4) and debt issuance is expected to rise materially, there is little choice but to cut aggressively. In doing so, not only can fiscal credibility be maintained but borrowing costs may even fall if the Bank of England feels able to emulate the RBNZ by moving more aggressively on rates. This also means that GBP’s outlook is similarly fraught up ahead and we expect material sterling underperformance in Q2.

EXHIBIT #4: UK BUDGETS HAVE LITTLE ROOM FOR GROWTH

Source: ONS, BNY, Bloomberg

Busy week ahead for APAC

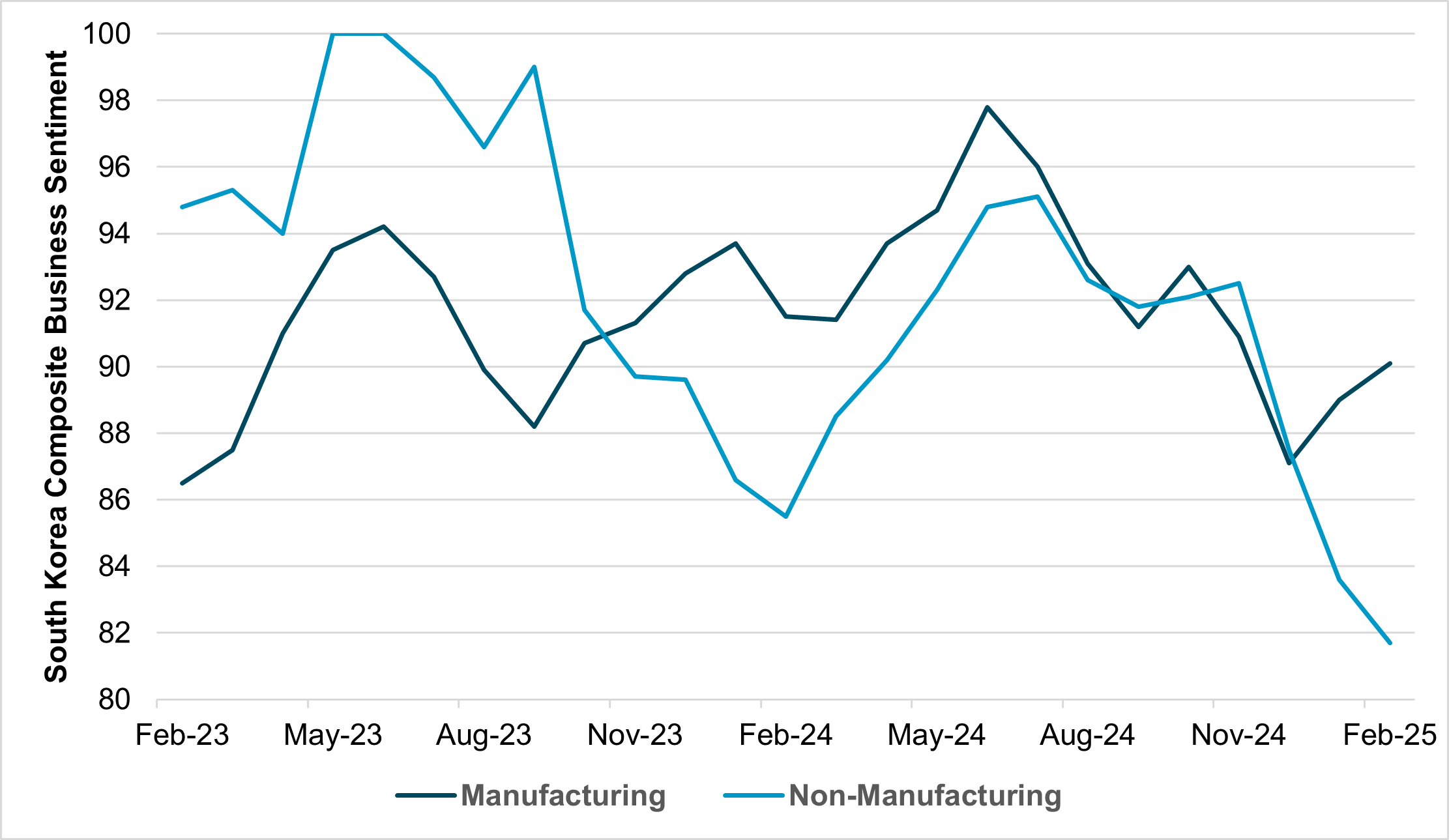

The economic data focus in APAC this week will be on the Japan, India and Australia flash PMI reports and their growth vs. inflation balance. However, the main focus next week for the region is on South Korea. The South Korea composite business sentiment will be closely scrutinized following the uneven recovery after a martial law-induced drop in December. The manufacturing sector has improved slightly while non-manufacturing sentiment declined further, to the lowest level since September 2020. There are unsettling political uncertainties in South Korea as the market awaits the constitutional court verdict on Yoon’s impeachment. Instead, the verdict on Prime Minister Han impeachment is set to be announced on Monday. There is some expectation of a relief rally in Korea, but we see holdings of both FX and equities as back to normal levels.

China will announce its 1-year Medium Lending Facility (MLF) swap, which might see another month of net withdrawals. This should not be seen as tightening signal, but rather as a change of liquidity strategy and further winding down of total MLF outstanding after a surge in late 2023. How markets trade on current liquidity matters particularly given the Hang Seng pullback last week on IPO margin restrictions. Money is not easy in China and that increases the policy-easing risks. Precisely when matters as markets are not fully pricing the much-anticipated RRR reduction and potential interest rates reduction in the near term.

Elsewhere, Singapore and Australia will release February inflation data, which is directly relevant to forthcoming policy meetings. A further drop in inflation in Singapore, which stood at 1.2% y/y and 0.8% y/y for headline and core CPI in January, might add pressure for MAS to move again in April. Note that MAS slightly reduced the slope of the SG$ NEER policy band at the January 2025 meeting which clearly was not enough. Australia inflation is trending lower but might not be sufficient yet for RBA to pull the trigger. The market consensus is for the RBA to keep the rate unchanged at 4.0%. The RBA also will have the government’s spring budget to dissect and consider with further stimulus likely to slow faster cutting plans.

Lastly, we will be closely monitoring capital flows conditions, which broadly remain on the sell side except for ongoing optimism in Chinese equities and sign of stabilization in South Korea, which posted its first weekly inflows in 10 weeks. Special attention will be paid to Indonesia, which had suffered all-out significant outflows in Indonesia government bonds and a sharp widening of the spread vs. US Treasurys. There is no central bank meeting in APAC this week.

EXHIBIT #5: SOUTH KOREA SENTIMENT MATTERS, ELECTION RISKS ARE NEXT

Source: Bank of Korea, BNY

We expect the week ahead to be focused on month-end and quarter-end rebalancing and more wait-and-see hope for diplomacy. This will leave trading to ranges with less volatility and reactive position washouts. Risks from South Korea, China, the UK and the US are clear. However, the light economic calendar – with only global PMI flash reports – and only four rather than 12 central bank decisions add to the expectation of relative calm. For many investors this will be more of a week of fatigue rather than relief – as the April 2 tariffs remain the driver of significant uncertainty.

Central bank decisions

Hungary MNB (Tuesday, March 25) – No change is expected by the MNB, while CEE economies need to work through the impact of the German spending package, which is expected to fundamentally change the growth and inflation outlook across the continent. Hungarian assets have seen particularly strong inflows, according to our data, over the past few weeks but there are signs of re-rating running out of steam. Domestically, financial conditions are still to lose with inflation running at 0.8%m/m and 5.6%y/y, which means that at 6.5% base rates, the real rate buffer remains small.

Czech CNB (Wednesday, March 26) – The repurchase rate is expected to remain at 3.75%, but unlike its regional peers CNB’s inflation view is largely on track, with inflation running just above the 2% level based on monthly changes in January and February. However, other activity figures are mixed with downside surprise to retail sales and industrial prices. On the other hand, the country is expected to be a major beneficiary of Germany’s reinvestment drive, but it will take time for the industrial supply chain to reorient advantageously.

Norway Norges (Thursday, March 27) – Norges Bank is expected to remain on hold, keeping the deposit rate at 4.50% as Statistics Norway’s latest forecast round points to an economy facing stagflation risk. Inflation for February surprised to the upside, very strongly for both the monthly and annualized figure and with inflation likely to stay well above the 3.0% for the year, there is limited scope for easing. Should support be needed we expect fiscal levers to be pulled swiftly. The currency remains overheld on a cross-border border basis and is realistically the only carry name in G10.

Mexico Banxico (Thursday, March 27) – Another 50bp cut is expected by Banxico, bringing the overnight rate to 9.0% as inflation continues to run in a 3.5-4% range, which does allow room for further easing. However, economic activity is flat to contracting and trade issues will come to the fore soon as key deadlines for bilateral and reciprocal tariffs approach. January’s industrial production contraction of 2.9%y/y was the weakest annualized print in four years. Meanwhile, the Fed’s relatively firm policy path may also limit MXN appreciation risk, especially if USD flows begin to stabilize.

Source: BNY

Source: BNY