Dynamic Tensions Across Markets

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 12 minutes

The surprise of the week was the divergence between price and ECB rate cuts, with forward expectations again dominating current market sentiment. For the week, the USD is lower against the EUR, while U.S. 10y bond yields are up 8bp and the S&P500 is 1.7% higher. Four new themes are driving this:

In the mix of event risks next week: The meeting of G7 leaders in Canada, US/Mexico/Brazil/India CPI economic releases, Fed blackout and U.S. bond supply 3Y $58bn, 10y $39bn, 30y $22bn, along with longer-dated sales from Korea 50Y and the BOJ statements on tapering. The themes and trades that fall out of these revolve around USDEUR 1.15, JGB 1.50% 10y, UST 4.60% 10y and the carry trade unwind with Brazil and Mexico in focus. China/U.S. trade talks and the way tech stocks trade with the Musk/Trump feud also in the mix for equities, with Russell 2000 vs. Nasdaq 100 in play.

Last week, Elections did and didn’t matter. Poland had a surprise outcome with Nawrocki, while Korea delivered the expected new president Lee. Korea KRW rose 1.2% on the week while PLN is up 0.2%, but Brazil leads up 1.5% as carry trades return with less fear on global trade as U.S./China trade talks restarted after a Trump/Xi call. The Musk and Trump spat became a public feud, driving worries about the technology sector along with U.S. taxes and the ongoing Senate debate over the “big, beautiful bill.” The U.S. jobs data confirm hard data is slowly catching up to soft, pushing the market to stick to near two Fed cuts in 2025 but not more, while the U.S. President would like four from Powell now. The global equity markets printed new highs, with Japan and U.S. lagging and Hong Kong and Europe leading. The bond markets were mixed, with U.S. and U.K. leading rallies and Korea and New Zealand lagging. FX continues with the USD weakness trend, as the dollar fell 0.5% on the week in G10 markets and more in EM markets.

Technology leads U.S. risk recovery, but rate cuts are needed for new buyers

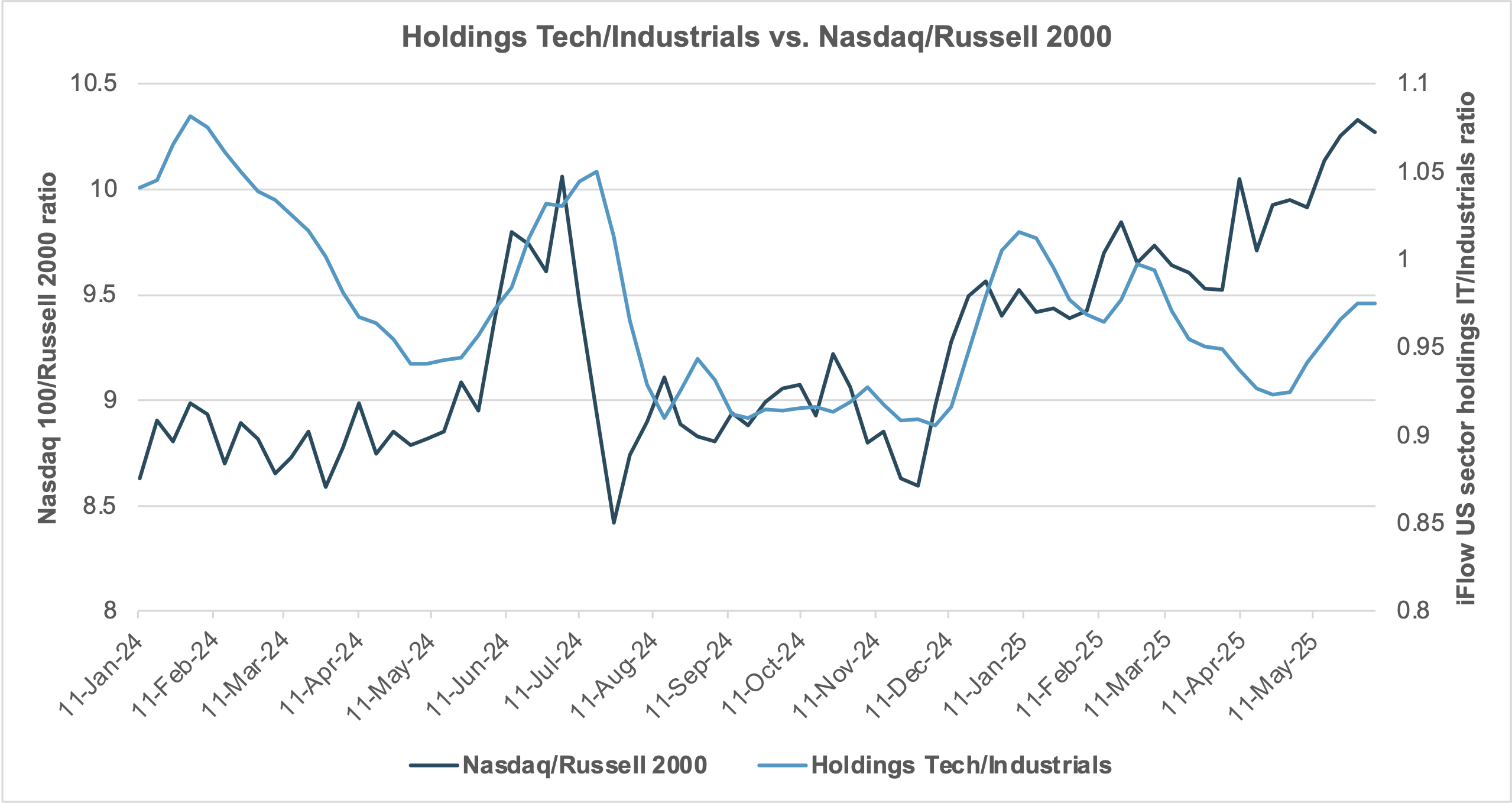

EXHIBIT #1: IFLOW U.S. SECTOR HOLDINGS RATIO OF IT/INDUSTRIALS AGAINST U.S. NASDAQ/RUSSELL 2000

Source: BNY, Bloomberg

Our take: The focus on the U.S. equity recovery since April has inspired fast money to drive back into the technology sector. We highlighted this in our report “Leadership and Melt-Ups.” Growth hopes are overshadowing recession fears in the U.S., with the Fed seen as a backstop to downside risks again. However, moves in markets have been outsized to holdings, with much focus on cross-border holdings of U.S. bonds and stocks lagging. Some of this reflects risk rewards of valuation and home bias. USD hedging has also been a key driver, with the costs leaving some U.S. assets less attractive. The push for U.S. trade policy is to increase domestic companies, particularly SMEs and those are clearly reflected in the Russell 2000, which lags the IT-heavy Nasdaq since December.

Forward look: Without new policy support, the spread of technology buying against industrials and other U.S. domestic-focused shares will revert to the mean. The best example of this shows up in the summer of 2024 when U.S. tech regulation worries first rose to the fore. Following the recent spat between U.S. President Trump and Elon Musk, many investors may be wondering about renewed risks to reigning in tech companies given their global reach. The longer-term trend for investors has been to rotate out of purely IT holdings with the hope for industrial rebounding part of the story. Whether this trend continues will matter to how risk appetites across markets play out next week into the G7, with more trade talk hopes, U.S. CPI and the ongoing rate focus from supply and tax debates.

U.S. markets watching the data and waiting for better times

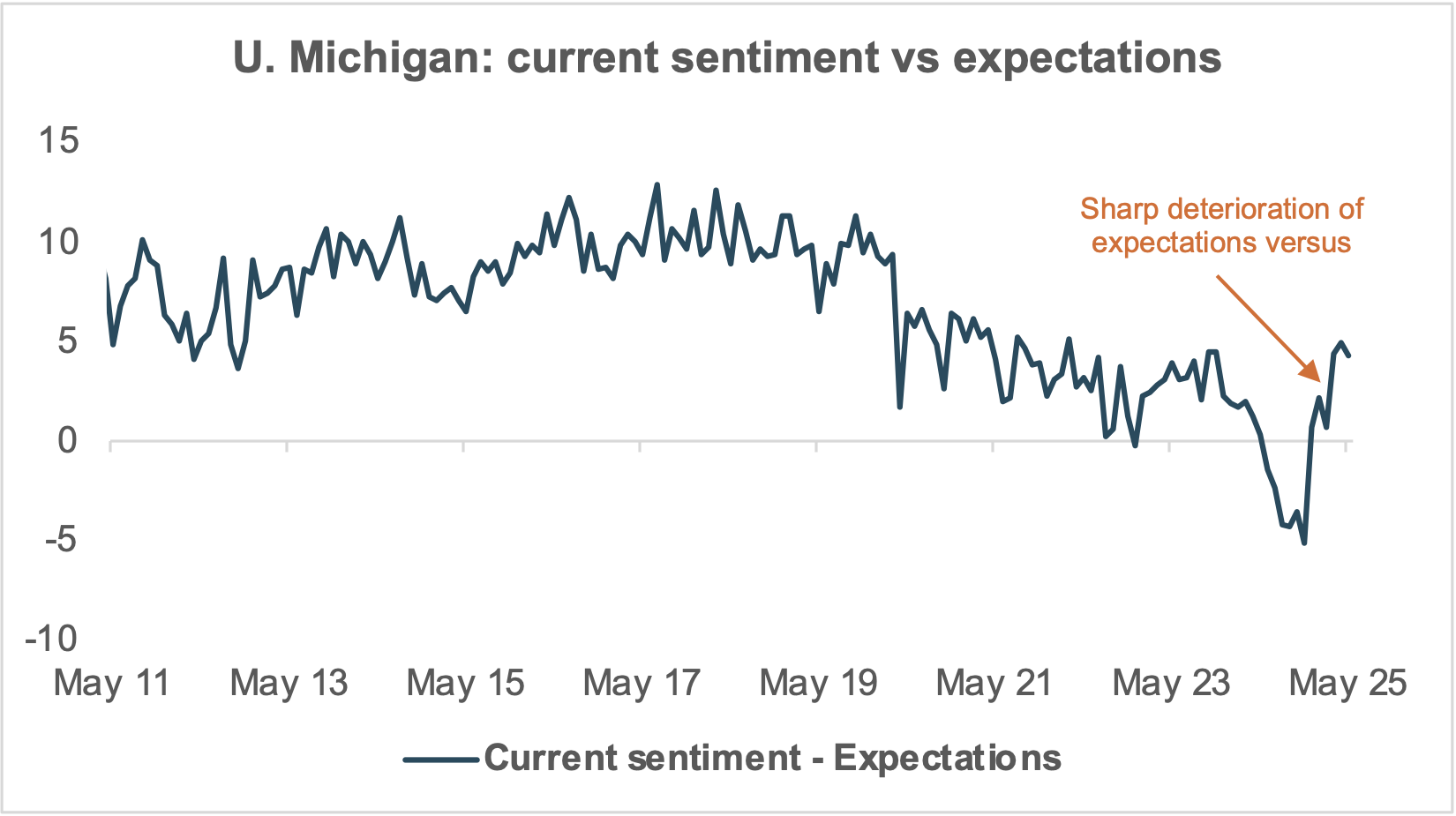

EXHIBIT #2: U.S. CONSUMER SENTIMENT VS. EXPECTATIONS

Source: Michigan Consumer Sentiment Index

Our take: Investors are watching consumers while consumers are watching investors. Better equity markets and weaker U.S. dollar and bond yields not going up further have made financial conditions easier. These have also lifted expectations for better times ahead, just as last week showed that the weaker present sentiment across businesses and consumers is beginning to converge in hard data like jobless claims, house sales, and auto sales. High real rates and ongoing uncertainty over tariff inflation effects drive much of the mood despite the better equity prices. Hopes for the future wrap around trade deals and Fed rate cuts, both of which are unlikely to become more certain in the next week.

Forward look: Although last Friday’s U.S. employment report was generally healthy, there were other initial signs of weakening data during the week, namely, Institute for Supply Management reports (ISMs) and slightly higher unemployment claims data. This coming week, we do not expect much data on output and demand, but we will receive information on consumer and producer prices and another print of the Michigan Consumer Sentiment survey. We expect a slight uptick in inflation with 0.3% m/m and 3.0% y/y reading for core inflation.

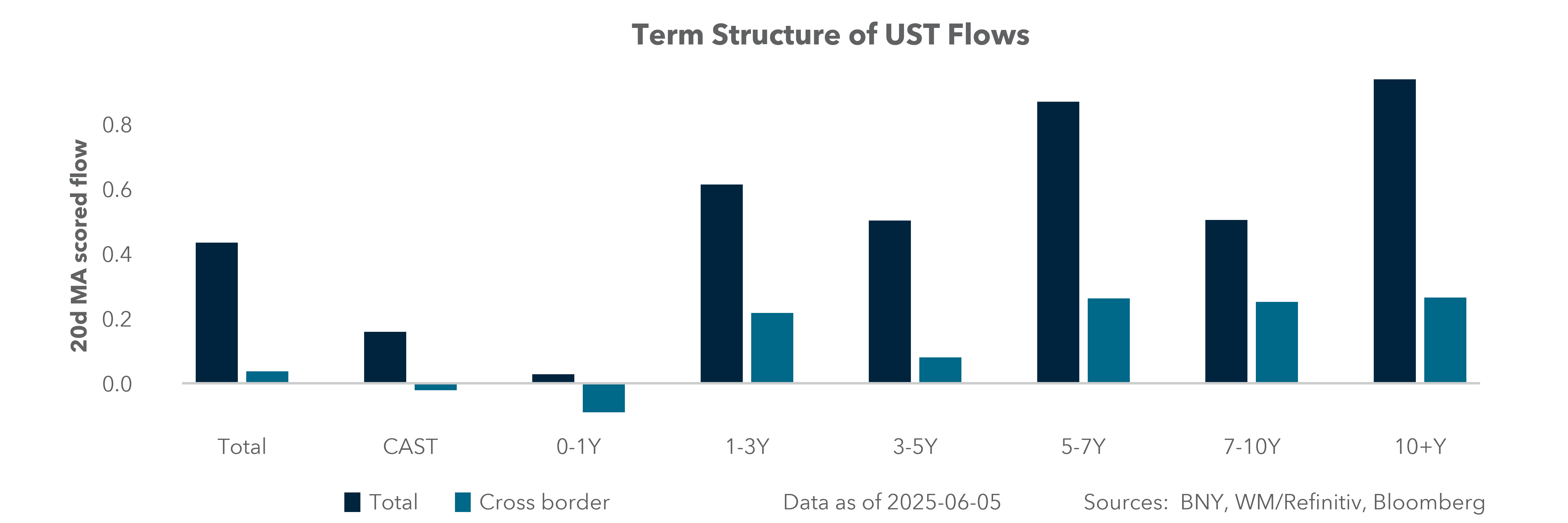

There are three coupon auctions this week, with the highlight being the 10y seeing a $39bn reopening on Wednesday. We’ll have a chance to see how demand for long-dated U.S. paper holds up, a crucial data point when thinking about the bond market and ten-year yields. Worse inflation data could complicate the offering, but there isn’t too much worry about a poor auction at the moment.

EMEA: Easing trajectories shallowing further as peers look to follow ECB

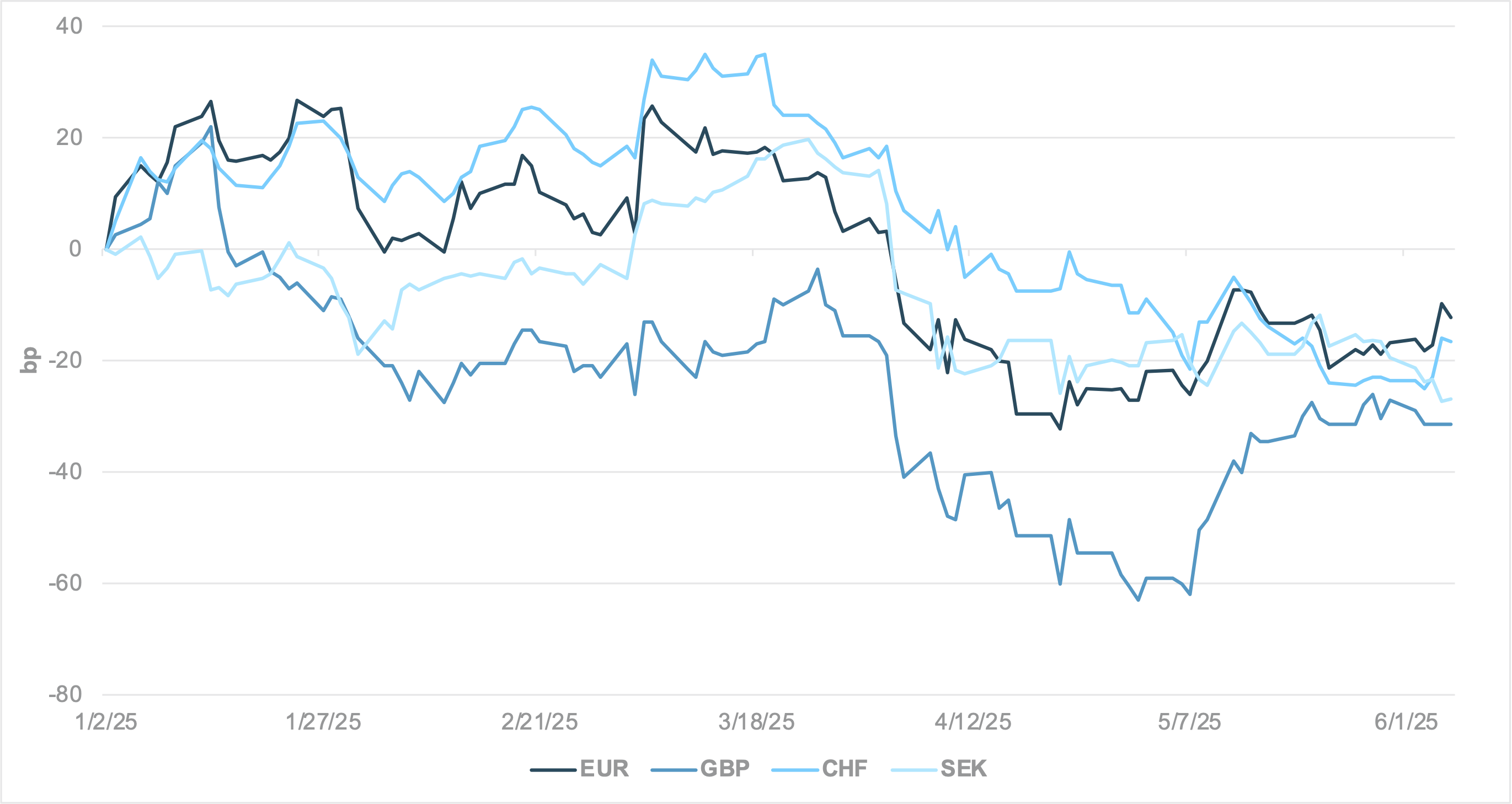

EXHIBIT #3: CHANGE IN END-YEAR RATE EXPECTATIONS YEAR TO DATE

Source: BNY, Bloomberg

Our take: The ECB’s 25bp rate cut in June was widely anticipated, but President Lagarde’s suggestion that the easing cycle is effectively complete has implications well beyond the Eurozone. Given the region’s status as the main trading partner for several key European economies, its monetary stance will likely shape the broader continental trajectory. We see limited room for significant policy divergence between the Eurozone and peers such as Switzerland, Sweden, and even the U.K. As a result, policy expectations are likely to converge, and we anticipate further removal of easing priced into current curves, contingent on upcoming data. However, this doesn’t mean further volatility compression as the lack of additional easing is far from ideal, depending on the economy. Central banks in Europe may not have a growth mandate, but this does not mean that growth is not sensitive to changes in financial conditions. The market is once again paying close attention to fiscal sustainability. This is happening at a time when Europe’s short-term economic growth relies heavily on public investment. As a result, markets are particularly sensitive to movements in the yield curve. Consequently, a shift in central bank guidance in Europe could have an adverse impact, not on growth expectations per se but on the “cost” of growth. Such tensions are playing out in the U.S., and markets should be attuned to such risks in Europe as well.

Forward look: The upcoming week’s data focus will likely be on the U.K., where a resilient labor market continues to challenge the BoE’s scope to ease. Among European economies, the U.K. appears most vulnerable to a shift away from aggressive easing. SONIA futures still imply more cuts by the end of 2025 than at the start of the year (Exhibit #3), while equivalents in the Eurozone, Switzerland and Sweden are pricing in fewer moves. A return to equilibrium may be underway, with Swiss and Swedish policy guidance suggesting rates will not return to the deeply negative levels seen in past deflationary periods. The U.K., by contrast, retains greater policy space. Yet the BoE is particularly sensitive to the risk that labor market slack remains minimal despite tighter financial conditions. Inaction, based solely on inflation, risks broader economic damage: directly, through high variable borrowing rates, or indirectly, through fiscal channels, as gilt debt servicing costs and Asset Purchase Facility indemnification expenses can remain elevated due to persistent curve steepness. As carry trades begin to unwind, benefiting funders like SEK and CHF but pressuring low-savings, stagflation-prone economies, GBP could remain under pressure even if the BoE refrains from easing.

China inflation and trade, Japan Q2 BSI

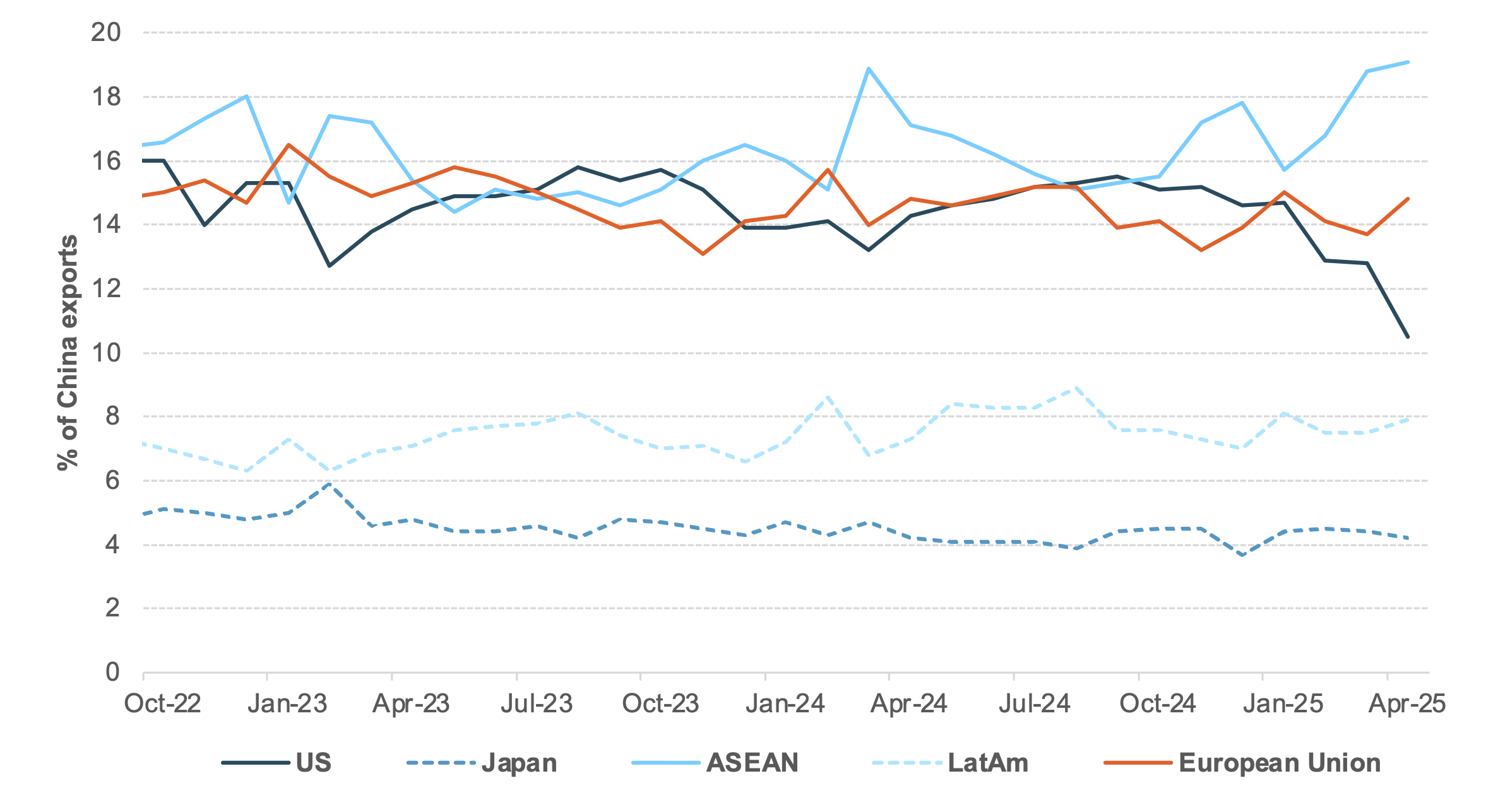

EXHIBIT #4: CHINA EXPORTS DESTINATIONS

Source: BNY, Bloomberg

Our take: In the Asia-Pacific region, the focus this week is on China May inflation and exports and trade data, South Korea first 10-days exports, and Japan Q2 Business Survey Index (BSI) data. Data will be light elsewhere, with Taiwan and India May trade data and Thailand, Indonesia and Australia consumer confidence. APAC May exports will be closely watched following the front-loading-related April data. Consensus is China May exports will ease to 6.0% after 8.1% y/y, while imports are seen to stay depressed at -0.9% y/y vs -0.2% y/y in April. Another interesting aspect to look out for is the distribution of export destinations. Export to U.S. as a percentage of total Chinese exports has dropped sharply this year to 10.5% in April compared with a monthly average of 14.7% in 2024, while ASEAN as an exports destination has picked up strongly, accounting for 19.1% of total Chinese exports from monthly averages of 16.4% in 2024. This week will also see May trade data from Taiwan and India as well as early indication of June exports data from South Korea.

China May inflation will be closely watched both as a gauge of price pressure and an indicator of domestic demand. Market expectations are for further disinflation pressure, with consensus for May CPI and PPI at -0.2% and -3.0% y/y, respectively, but the pressure is not exclusive to China. Latest regional May readings were lower in South Korea (1.9%), Taiwan (1.55%), Indonesia (1.60%) and the Philippines (1.3%), driven primarily by lower food and transportation prices. Heavy basis impact from lower crude oil will likely remain a potential drag on regional price pressure. India May CPI this week is projected to trend lower at 3.00%, the lowest since 2019, likely confirming the lower inflation trend.

Elsewhere, the Japan Q2 Business Survey Index will be interesting to watch as the latest gauge of business sentiment following the contraction in Q1 quarterly GDP. Macro focus in Australia and New Zealand will be on business and consumer confidence.

Forward look: Market sentiment has been solid despite overall neutral-to-softer-bias data releases. APAC assets continue to enjoy a solid risk-on performance with higher equities prices and stronger domestic currencies, supported by a lower U.S. dollar trend and lower global bond yields. Unless there is a major downside data surprise, the ongoing expectation for tariff relaxation supports APAC risk. Looking ahead, China is said to release a fresh round of major financial policies at next week’s 2025 Lujiazui Forum in Shanghai on June 18–19, 2025. Lastly, an interesting development is the Hong Kong dollar, which has seen a substantial influx of liquidity. This movement pushed one-month HKD HIBOR to 0.7%, a historically wide spread of nearly 350bp below USD SOFR-equivalent fixings. USDHKD is currently just shy of the weak end of the convertible trading band of 7.75–7.85 under the Linked Exchange Rate System (LERS).

The dynamic tension for the week ahead rests on how inflation and growth economic data from the U.S. and rest of world catch up to the expectations already priced into markets. The idea that developed nations have already cut rates and are nearing their end of easing vs. the FOMC, which has paused, stands out in this narrative. As we look into the risks for next week, we see three points:

Putting it all together, the events for the week ahead, from the G7 meetings to ongoing trade talks to U.S. bond auctions, will matter as much as the focus on economic data. We see the key focus on breakouts from recent ranges with EUR 1.15, JGB 10y 1.50% and S&P500 6000 all in play.

Central bank decisions

Peru, BCRP (Thursday, June 12) – The Central Reserve Bank of Peru (BCRP) is expected to maintain its benchmark rate at 4.50% at the upcoming policy meeting, following a 25bp cut in May that brought the rate closer to its estimated neutral level. May inflation edged up to 1.69% y/y from 1.65% in April, remaining comfortably within the BCRP’s 1–3% target range. Core inflation held steady at 1.9%, and one-year-ahead inflation expectations stayed at 2.3%, indicating stable price dynamics. The BCRP has signaled a data-dependent approach, with future rate adjustments contingent on added information about inflation and its determinants. Given the current inflation outlook and the central bank’s cautious stance, a pause in the easing cycle appears for now.

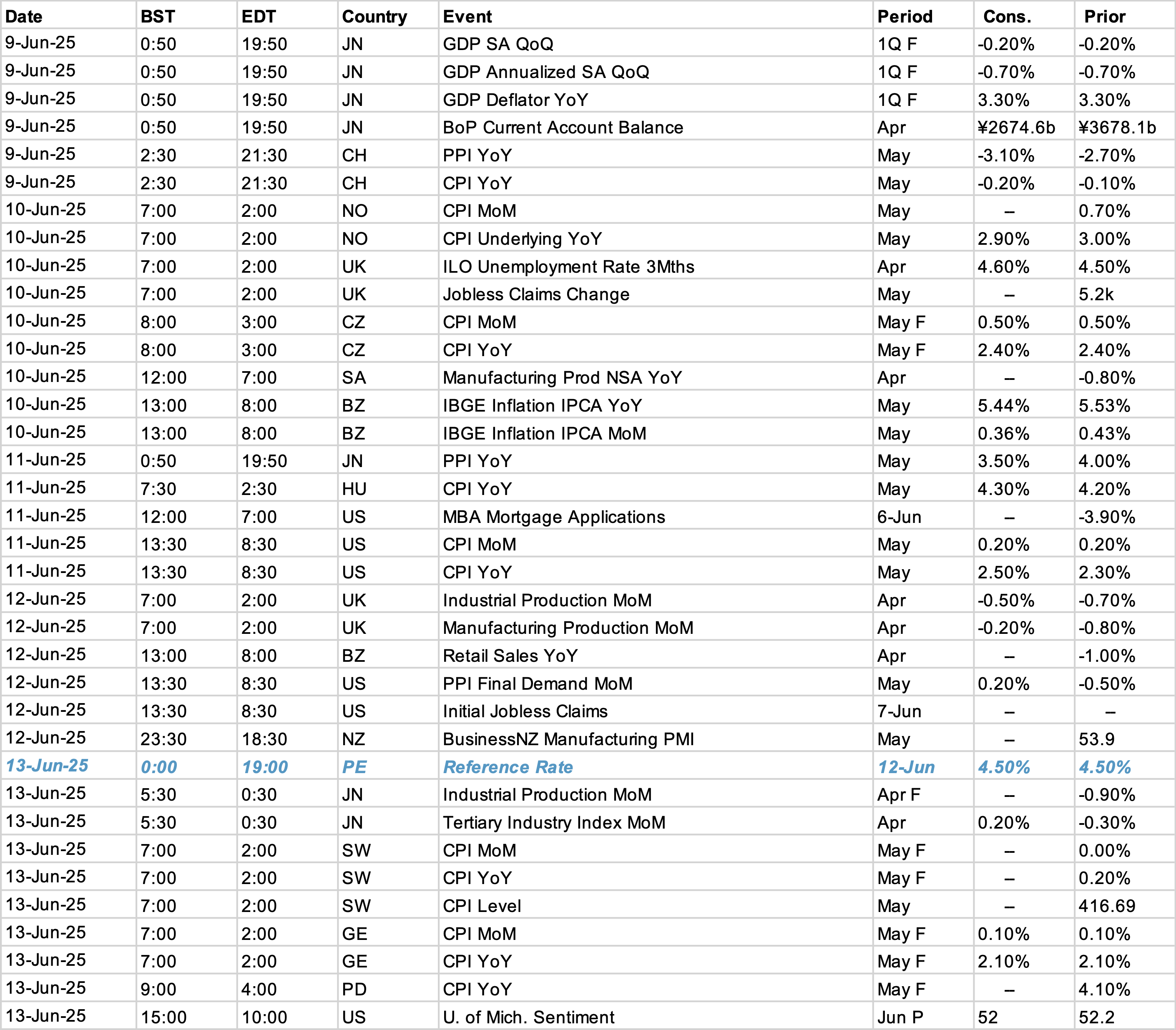

Data Calendar

Event Calendar