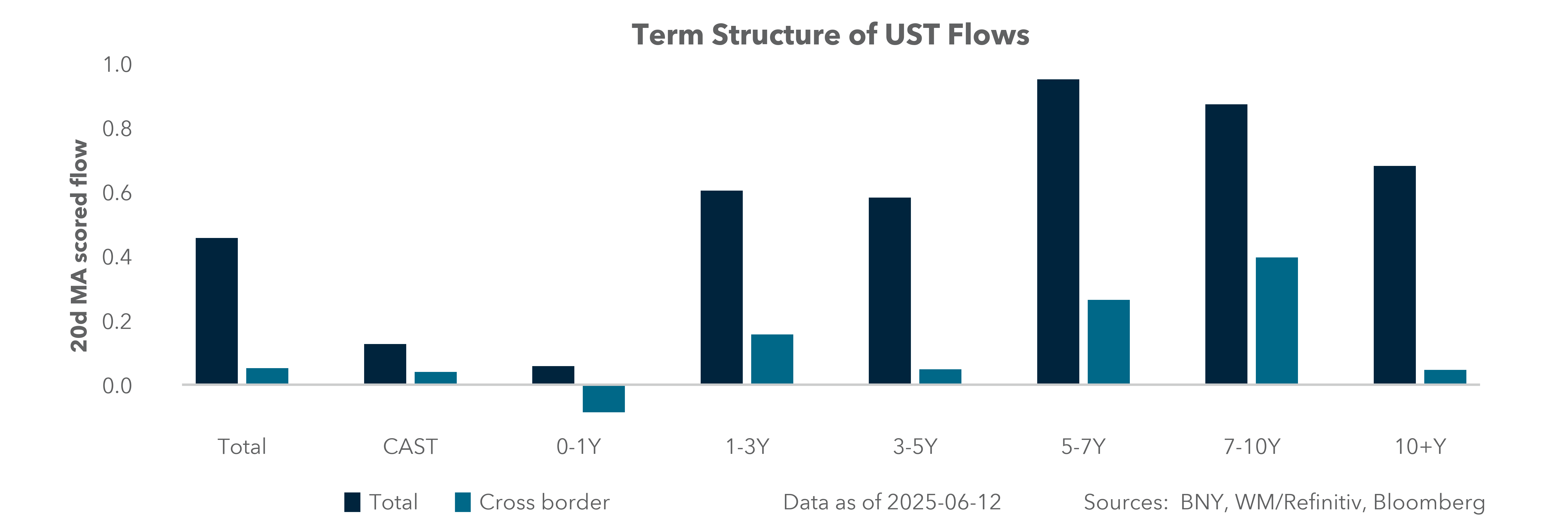

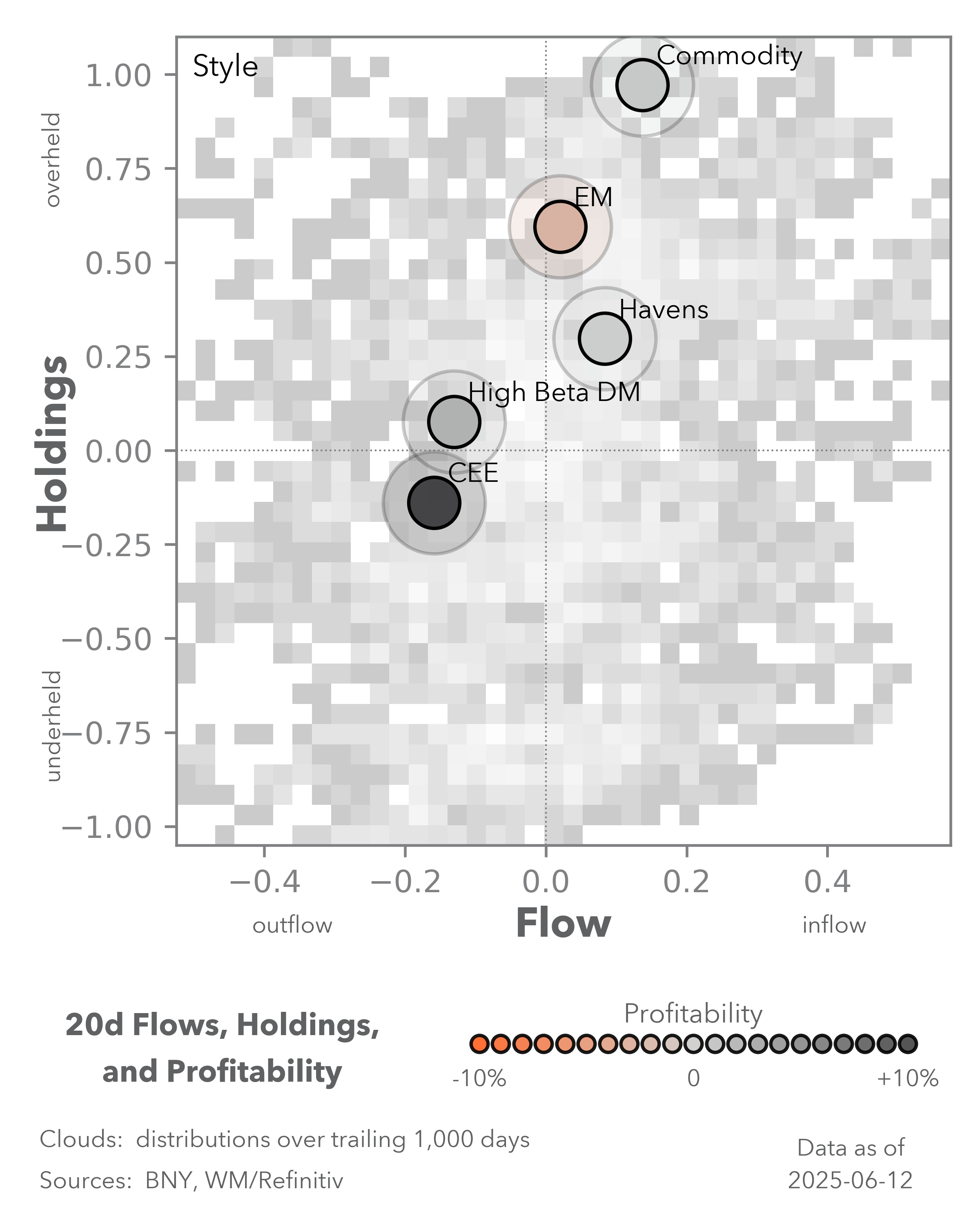

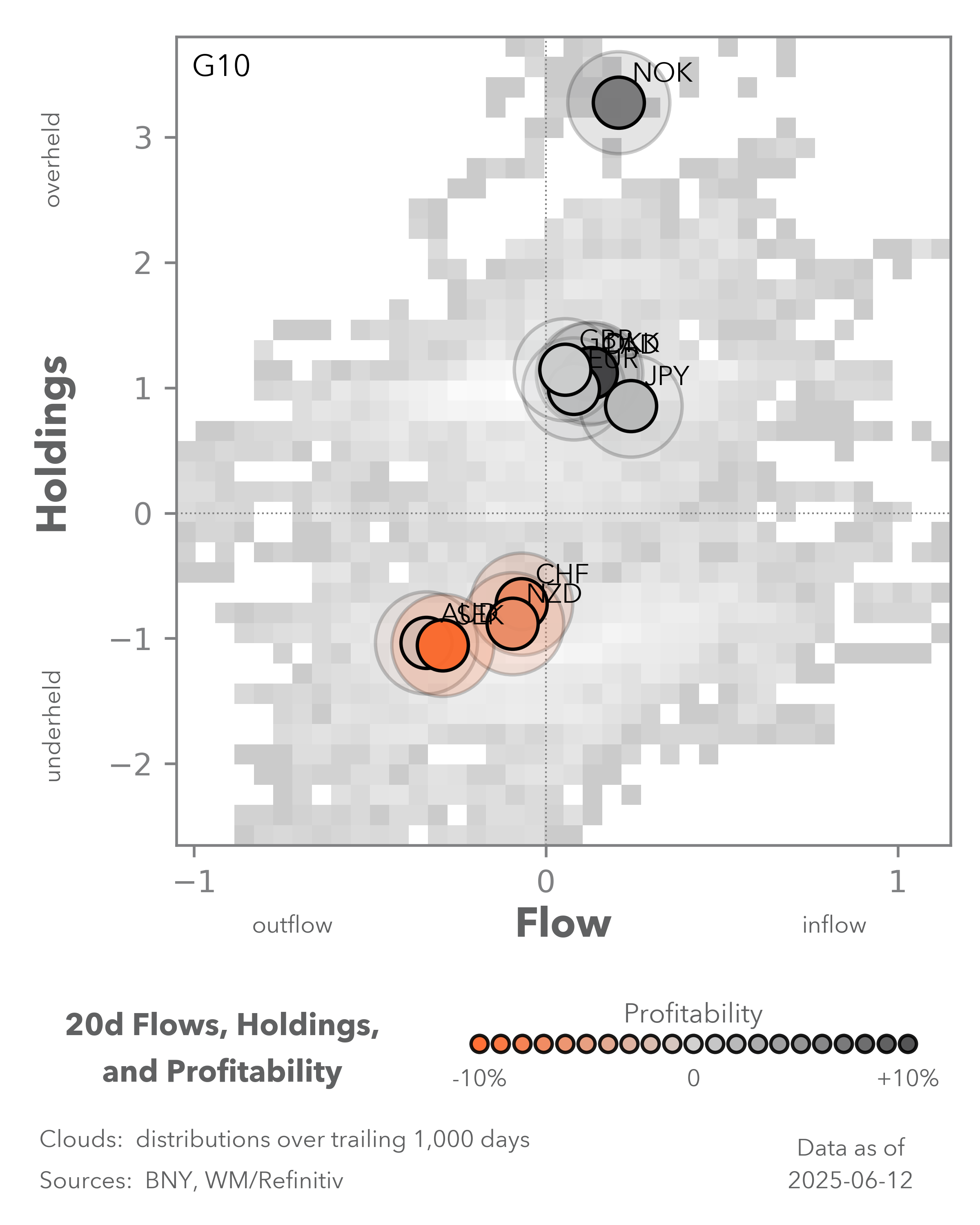

Decisions

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 14 minutes

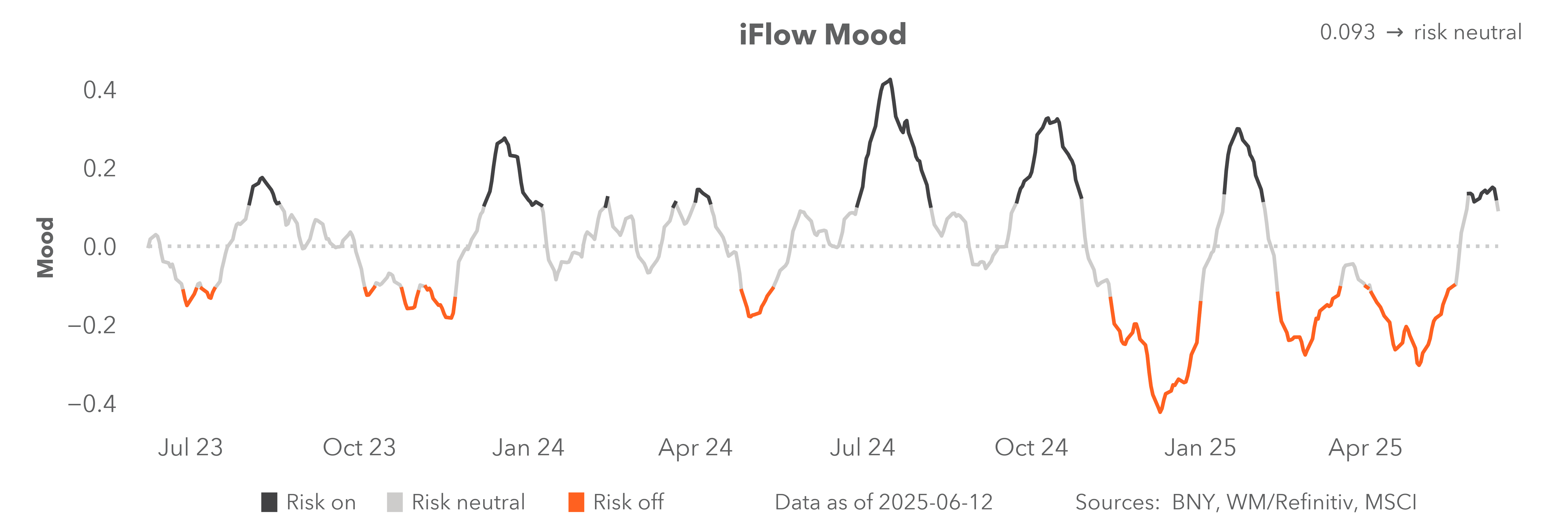

Risk sentiment is sharply lower this week on back of lagging momentum and the surprise of Israel’s action against Iranian nuclear facilities. We have moved from significantly positive mood to neutral in our iFlow index, and we see other factors like trend, carry and growth turning down. The weekend will matter to how markets open on Monday, with fears of escalation driving position clearing Friday. Before Friday, markets were content to wait and see ahead of more hard economic data. Next week will test how market thinking about growth and inflation matches the logic of central bankers. The risk of geopolitical events, combined with ongoing trade deal uncertainty, has led to modest risk adjustments, but not yet to a shift in narrative. In order for events ahead to change views, we need to see more volatility with specific asset-price levels broken. Oil significantly higher (over $80/bbl), USD significantly stronger, EURUSD below 1.10, USDJPY over 148, and U.S. rate markets pricing in more than two cuts in 2025. Whether this happens in the week ahead is likely to set the tone for how Q2 rebalancing and risk views play into the summer. Surprise market events are becoming more commonplace than calm, boring range trading.

How easy are financial conditions?

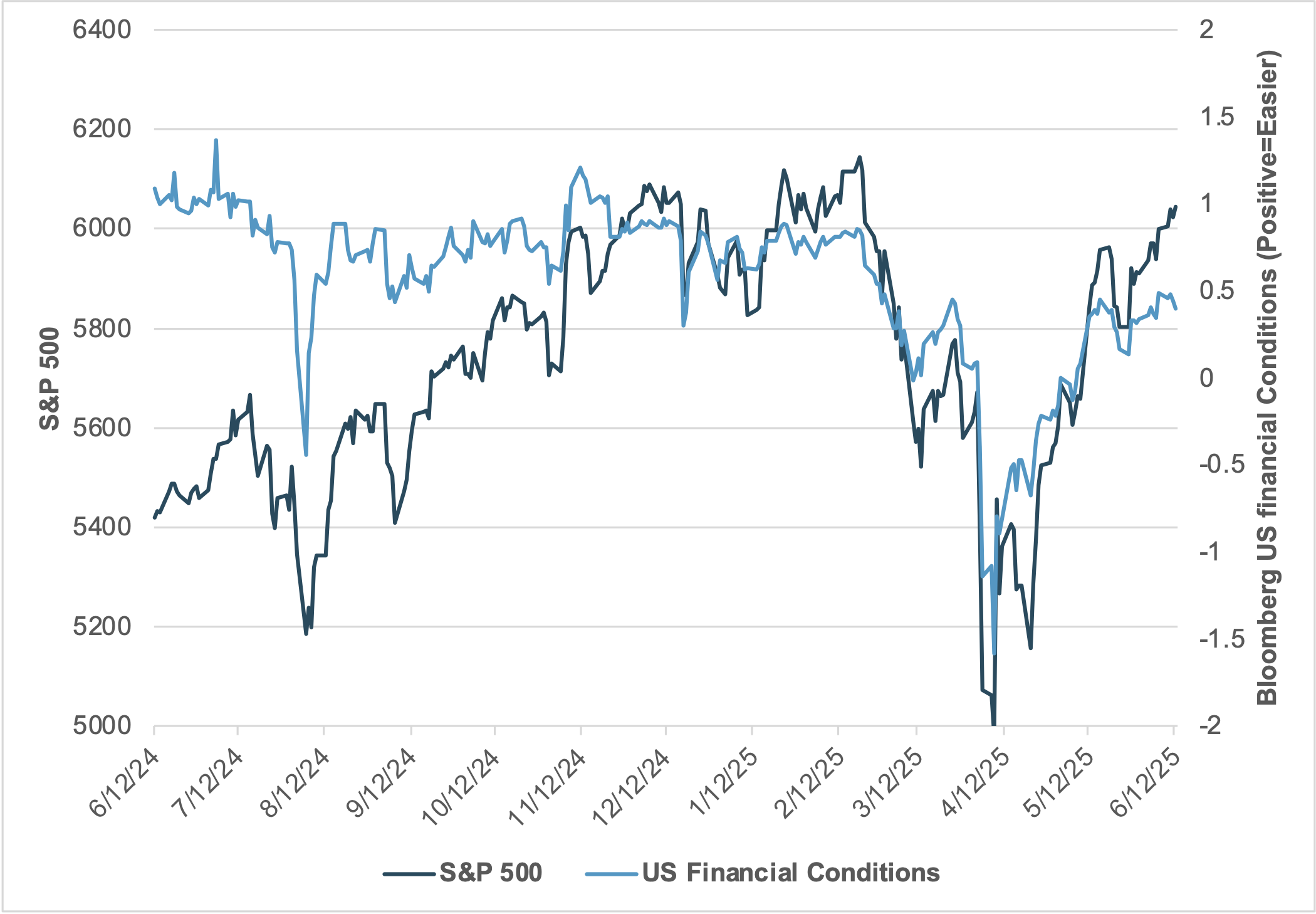

EXHIBIT #1: U.S. S&P 500 VS. U.S. FINANCIAL CONDITIONS INDEX

Source: BNY, Bloomberg

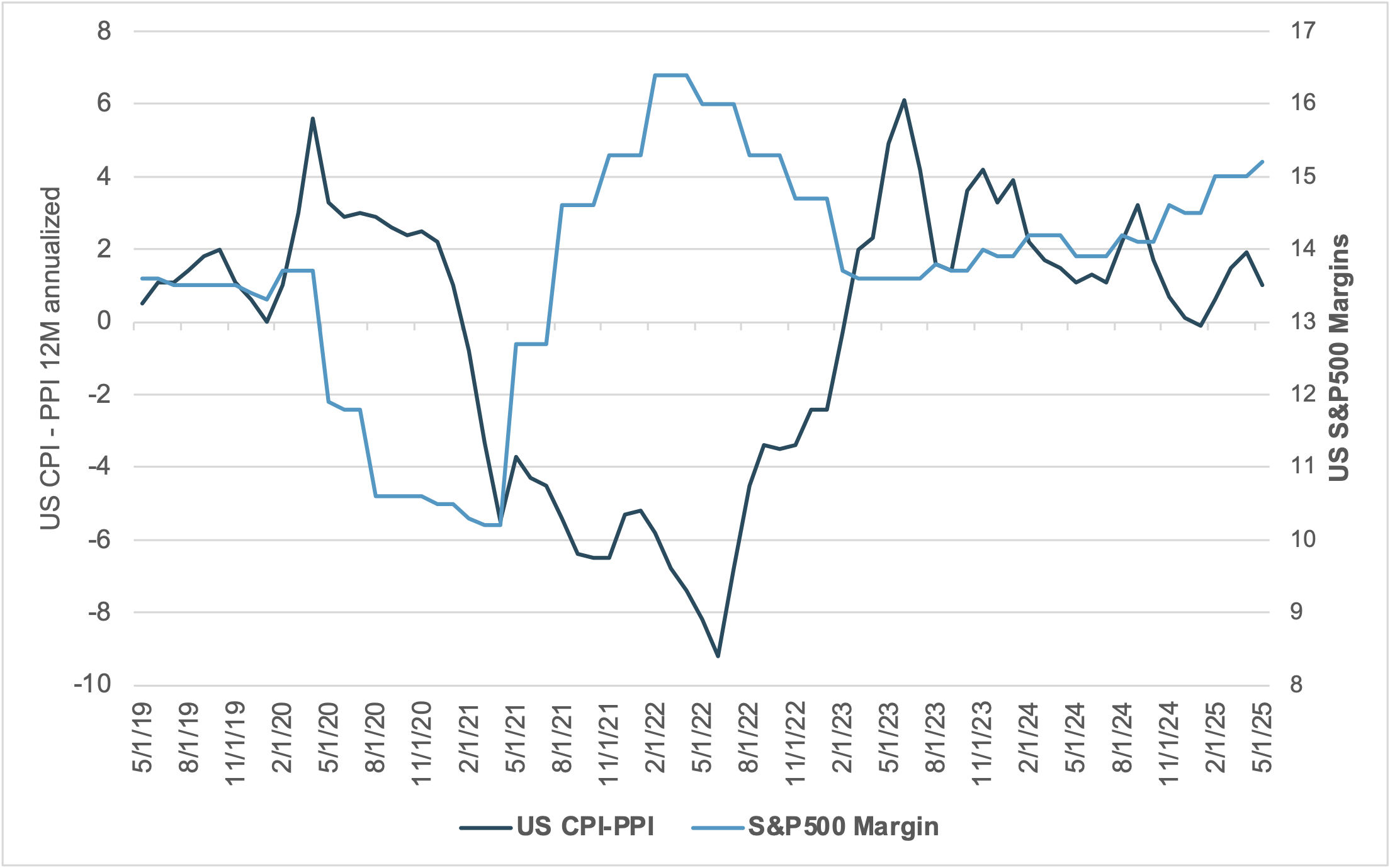

EXHIBIT 2: U.S. CPI-PPI VS. S&P 500 MARGINS

Source: BNY, Bloomberg

Our take: The U.S. stock market tested S&P 500 6000 again this week and remains up on the year. Financial conditions from April to now have reversed from –1.5 to +0.5, but the trend has stalled since May. The spread between conditions and the stock market is reaching levels that usually lead to reversals. The fear factors driving markets are shifting from tariffs to other factors, such as the Israel/Iran conflict, domestic politics or the U.S. budget debate. The surprise result of seeing CPI and PPI lower than expected matters most to how markets think about risk. The ability for companies to draw down inventories and eat price hikes linked to tariffs may have a limit, but for now, they suggest that the risk shifts from inflation to corporate returns. The week ahead will pivot on how companies guide Q2 earnings expectations and central bankers guide forward interest rates.

Forward look: The role of a weaker USD and strong U.S. stock markets in driving investor moods has been critical to how April and May trading shifted in June. While stocks are a key part of financial conditions, they are insufficient for keeping investor moods intact. Next week’s central bank decisions and the pace and scope of U.S. trade deals and geopolitical events will likely matter even more. The lack of conviction from investors, which has culminated in a wait-and-see risk positioning closer to benchmarks across assets, may be more problematic in the weeks ahead, given how margins and economic data point to slowing growth in June. Global economic hard data will affect the feedback loop for asset allocation decisions for month and quarter end.

U.S. – FOMC wait-and-see vs. the dot plots

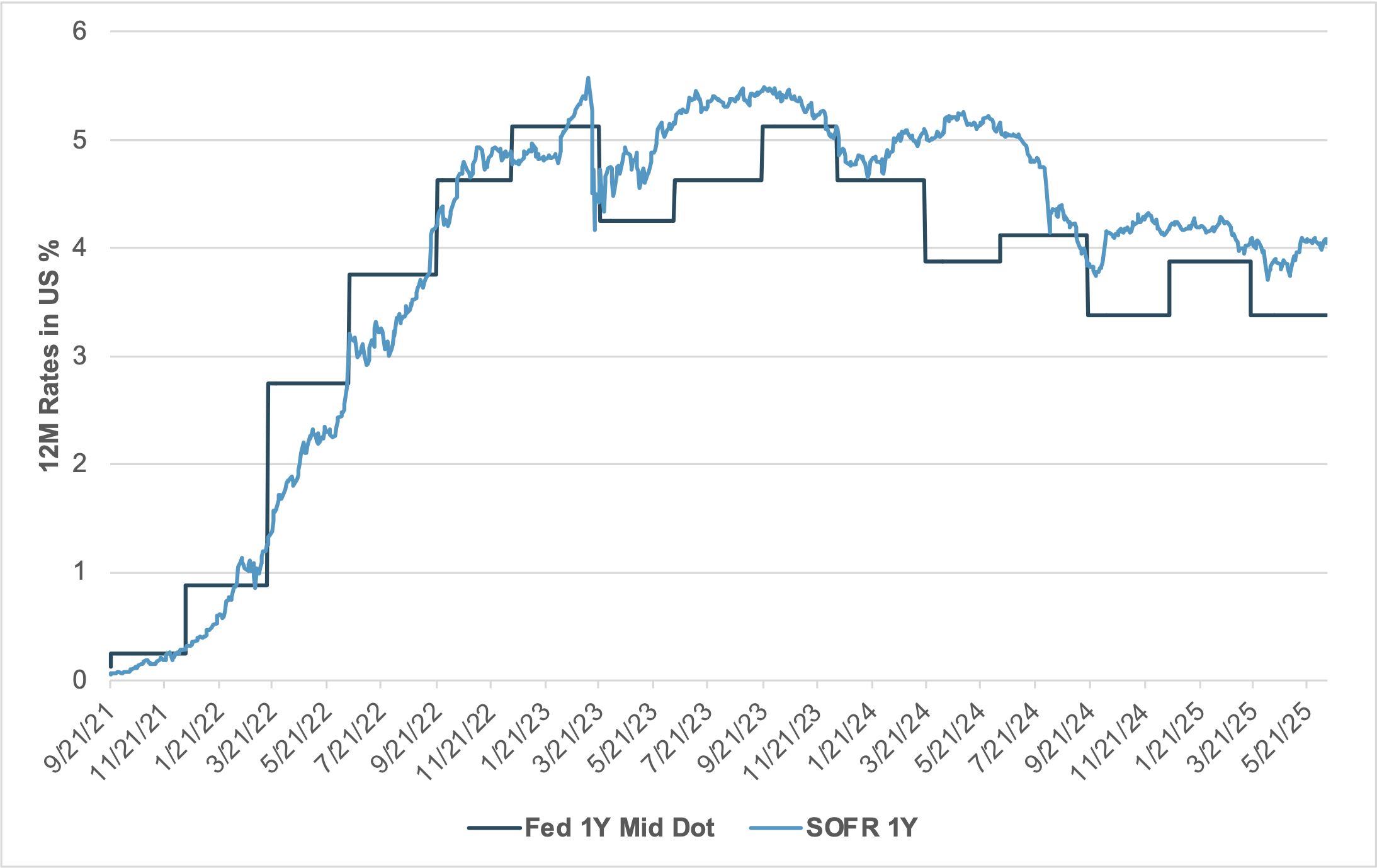

EXHIBIT 3: U.S. FED MID DOT PLOT 1Y FORWARD VS. SOFR FUTURES

Source: BNY, Bloomberg, Federal Reserve

Our take: The next week will be focused on the FOMC decision. While consensus is for no change in policy, the surprise may be in the Summary of Economic Projections. The ability for the market risk sentiment to hold positively rests on the future expectations for rate cuts. The 12-month forward view of the market is still more hawkish than the Fed. If this shifts next week, there will be knock-on effects for bonds, stocks and the dollar. In addition to the dot plot, attention has shifted to hard data with most of the Fed speakers. Among these are U.S. May retail sales on Tuesday, which are expected to hold near +0.1% m/m, and U.S. May industrial production, which is expected to rise to 0.1% from 0%. Both indicators impact the nowcasts for GDP and the Fed decision. A Q2 bounce back in growth over 1% is expected. Relatively tame inflation in the last week and the lack of pass-through of tariff-related price hikes will likely be the main focus for questions about easing bias during FOMC Chair Powell’s press conference.

Forward look: The surprise stability of U.S. inflation in both CPI and PPI has changed the equation for many Fed watchers into next week’s meeting. Our view remains biased for the FOMC to ease two times, but the hard data weakness for jobs and companies still matters to sustaining this story, along with stable financial conditions such as stock markets holding their melt-ups, dollar weakness extending, and rates remaining stable. The market isn’t yet screaming for rate cuts from the FOMC, which means they have time to wait for more clarity on the actual tariff levels and the impact on the economy for the summer ahead.

SNB leading the charge back to zero rates, but CHF can further strengthen

EXHIBIT 4: REAL EFFECTIVE EXCHANGE RATES, SEK AND CHF

Source: BNY, Bloomberg

Our take: All Western European central banks will hold their policy decisions in the week ahead. Only the Swiss National Bank (SNB) is likely to move on rates. Not for the first time, it will be leading the charge back to zero, and the market is comfortably pricing in the prospect of negative rates. SNB President Schlegel has repeatedly refused to rule this out, as the conditional inflation forecasts may even indicate a prolonged period of very low inflation without any action. Naturally, the focus will shift towards the prospect of intervention or even further unorthodox measures. We continue to hold the view that the bar to such action is very high and will be highly contingent on external circumstances. Geopolitics will play a role, but we believe the tolerance threshold for CHF strength is far larger than market expectations or previous episodes. Firstly, CHF valuations in real terms (Exhibit #4) are not extreme compared to when the floor was first established, and the pace of gains is manageable for now. Inflation differentials will not come down in the near term, providing a buffer that was not present in the past. The ECB’s ending of its cycle will serve as mitigation.

Forward look: Nothing is off the table for the entire region, but we doubt anyone will follow the SNB back into negative rates, let alone intervention.

Even the SNB can continue adding sight deposits to its balance sheet, thereby depressing funding costs further through open market operations without impacting the overall size. By contrast, the Riksbank is not even expected to cut rates, and current SEK valuations (Exhibit #4) can also help stabilize inflation expectations. The Norges Bank decision should also have limited consequences for the currency, but we stress that current holdings remain at very extreme levels within iFlow, and some positions may choose to take advantage of the bounce in oil prices to exit.

The BoE will likely remain split: the recent softening in wage and growth data, in addition to the fiscal adjustments stated in the spending review, could moderate demand expectations in the near term and justify a slight shift in the balance of risks back toward weaker growth. GBP has already reacted accordingly, but we expect the BoE to wait until wage data confirms a full loosening of the labor market before making use of its policy space.

China activity, investment and housing data, BoJ, BI and CBC in Focus

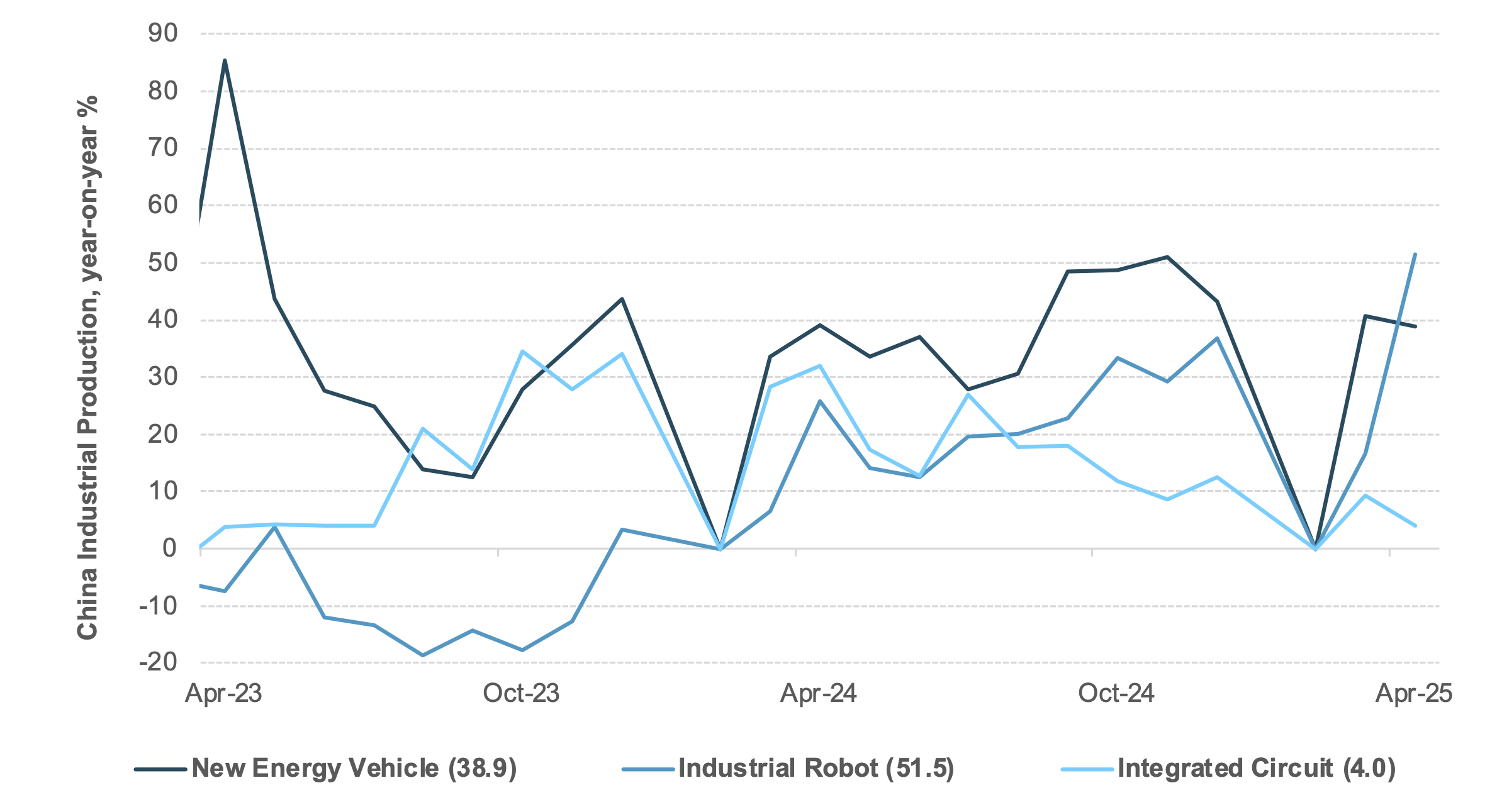

EXHIBIT 5: STRONG MOMENTUM OF CHINA HIGH-TECH RELATED PRODUCTION GROWTH

Source: BNY, Bloomberg

Our take: In the Asia-Pacific region, this week’s focus is on China May activity, investment data, and the latest housing market developments. This week will also see the 2025 Lujiazui Forum in Shanghai, where a fresh round of financial policies and supportive measures are expected. Elsewhere, there will also be May exports releases from Malaysia, India, Singapore and Japan. China May activity and investment are expected to maintain a gradual recovery supported by a pick-up in the credit growth cycle. The latest April fixed asset investment and infrastructure investment stood at 4% and 5.8% ytd y/y, respectively, from 3.2% and 4.4% in 2024, and retail sales at 4.7% ytd y/y (2024: 3.5%). We will be closely monitoring progress and investment into the high-tech sector. New energy, vehicle and industrial robot production sustained a high growth rate of 38.9% ytd y/y and 51.5% ytd y/y, respectively, while integrated circuit production eased to 4% ytd y/y after 12.5% in 2024. China will also release the latest May housing data, where our focus will be on m/m house prices in both new and used and the total volume of sales. A lower inventory trend in the housing market is as important as the evolution of home prices. Note that the inventory growth for residential housing stood steady at 6.6% y/y as of April from 16.2% at the end of 2024, while Tier-1 cities new and used home prices posted -0.20% and -0.42% m/m decline in April.

There will also be May exports data in Malaysia, India, Singapore and Japan. The early release of May exports in the APAC region indicates a potential easing of exports after a stellar front-loaded volume in April.

Forward look: Market sentiment has been solid with the comeback of foreign investors. Foreign investor inflows have supported Taiwan and South Korea equities, up over 2% on the week. At the same time, Hang Seng conditions continue to be buoyant on recent equity IPO successes, strong pipelines, and the persistent Stock Connect program southbound inflows. Note that year-to-date inflows are over HKD 680bn, nearly matching HKD 808bn for all 2024. HKD remains in focus as it approaches the top side of the 7.75–7.85 band under the Linked Exchange Rate System (LERS). Ongoing HKMA board management is likely to continue to keep HKD liquidity flush, leaving a wide interest rates gap between HKD HIBOR and USD SOFR rates, which stood at 0.598% and 4.31%, respectively.

Asia FX traded well, taking advantage of the lower USD trajectory. TWD stood out with an over 1% gain on Taiwan lifers hedging demand. Trade and tariff uncertainties continue to be the main driver for APAC FX. That said, the recent surge in crude oil prices will likely weigh on net-oil-importing countries’ currencies, especially THB, PHP, INR, KRW and JPY.

Lastly, this is a busy week for central bank meetings. Bank Indonesia (BI) and the Central Bank of the Republic of China (CBC) are expected to maintain the status quo, while the Philippines BSP is seen delivering a back-to-back rate reduction. Market consensus sees an unchanged BoJ at 0.5%, but all eyes will be on the update on its three-year JGB buying program schedule, currently targeting a JPY 400bn reduction of bond buying per quarter until March 2026.

The FOMC decision next week will be pivotal, not in the action but in the guidance, with potential surprises in the Summary of Economic Projections affecting bonds, stocks and USD. In Europe, the SNB is poised to lead central banks back toward zero rates, though CHF valuations remain manageable compared to previous intervention periods. China’s May activity data is expected to show gradual recovery, with fixed asset investment at 4% ytd y/y, infrastructure investment at 5.8%, and retail sales at 4.7%, while high-tech sectors maintain strong momentum with new energy vehicle and industrial robot production growing at 38.9% and 51.5% ytd y/y respectively.

A busy week for other central banks includes BI and CBC maintaining their status quo, BSP potentially delivering consecutive rate cuts, and BoJ expected to hold at 0.5% with focus on its JPY 400bn quarterly JGB buying reduction program. For EMEA, holds from Norges Bank, Riksbank and BoE are expected, but like the Fed, guidance for potential easing matters. Volatility has been lower across asset classes in the last week until Friday, with prices normalizing but not panicked. The mix of central bankers watching markets for fear and investors watching central bankers for doubts sets up a more difficult trading environment as conditions clash with headlines.

Central bank decisions

Japan, BoJ (Monday, June 16) — The Bank of Japan (BoJ) is widely expected to hold its policy rate at 0.5% at the June meeting, maintaining a cautious stance amid persistent inflation and external uncertainties. Core CPI in April remained at 3.6% y/y, the lowest print since December, although food prices continued to rise 6.5%, down from 7.4% in March. Governor Ueda has reiterated that further rate hikes depend on sustained underlying inflation and wage growth, which remain below target. While the BoJ remains open to tightening if conditions warrant, general consensus now points to a delayed hike timeline, possibly into early 2026, reflecting concerns over global trade dynamics and domestic fiscal strains. The BoJ is also expected to assess its bond tapering strategy, with long-term JGB yields rising and investor demand softening.

Chile, BCC (Tuesday, June 17) — The Central Bank of Chile (BCC) is expected to keep its benchmark rate steady at 5% at its June meeting, maintaining a cautious stance amid persistent inflation and external uncertainties. May inflation eased slightly to 4.4% y/y from 4.5% in April, remaining above the BCC’s 2 – 4% target range. The central bank has indicated that, while inflation may remain elevated in the short term, it is projected to decline to 3.8% by December and approach 3% in early 2026. Given the current inflation outlook and the central bank’s cautious stance, a pause in the easing cycle appears likely for now.

Indonesia, BI (Wednesday, June 18) — We expect Bank Indonesia (BI) to maintain the status quo at 5.5% while taking a relatively dovish stance. Low inflationary pressure and high-positive real yield warrant further rate reductions, but the pace of easing ahead is likely to hinge on the development of USDIDR — an increasing pace of IDR strength might see greater room for cuts. We expect BI to maintain its current triple intervention strategy, including offshore non-deliverable forwards (NDFs).

Sweden, Riksbank (Wednesday, June 18) — The Sveriges Riksbank is expected to maintain its policy rate at 2.25% at its upcoming meeting, although a rate cut later this year remains possible. May’s preliminary CPIF inflation held steady at 2.3% y/y, while core inflation (excluding energy) eased to 2.5% from 3.1% in April, both below market expectations. Governor Thedéen noted that recent data supports the Riksbank’s forecast of easing inflation pressures throughout 2025, suggesting that slowing economic growth and diminishing inflationary pressure could warrant a rate cut later in the year. The Swedish economy contracted in Q1 amid weak investment and consumer spending, partly due to U.S. tariff uncertainties. While the central bank is likely to hold rates steady this month, the combination of subdued inflation and soft growth may prompt easing later in the year.

United States, FOMC (Wednesday, June 18) — The Federal Reserve is expected to keep the federal funds rate unchanged at the June meeting, maintaining a cautious stance amid persistent inflation and external uncertainties. May CPI rose to 2.4% y/y, up from 2.3% in April, remaining above the Fed’s 2% target. Chair Powell has indicated that, while the general direction for interest rates remains downward, the pace and extent of these changes are now significantly less predictable due to global trade policy turmoil. Geopolitics may also play a role moving forward. Given the current inflation outlook and the central bank’s cautious stance, a pause in the easing cycle appears likely for now.

Brazil, Copom (Wednesday, June 18) — The Banco Central do Brasil (BCB) is expected to maintain the Selic rate at 14.75% at its next meeting, following a 50bp hike in May that brought borrowing costs to a near two-decade high. May’s IPCA inflation slowed more than anticipated to 5.32% y/y from 5.53% in April, although it remains above the 3% ±1.5pp target range. Core services inflation also moderated, reflecting a cooling economy under tight monetary conditions. Governor Galípolo emphasized “flexibility and caution,” indicating that policy decisions will remain data-dependent amid ongoing fiscal concerns and elevated inflation expectations. With inflation still exceeding the target and economic activity showing signs of deceleration, the central bank is likely to hold rates steady while assessing the impact of previous tightening measures.

Taiwan, CBC (Thursday, June 19) — We see Taiwan’s central bank keeping rates unchanged at 2% at the June meeting. Strong GDP growth momentum and easing inflation pressure are good places to be. May CPI dropped to 1.55%, with core inflation at 1.61% y/y and Q1 GDP at 5.48% y/y. There might be a chance for CBC to shift rates lower toward the year’s end if growth were substantially lower than expected. In the meantime, there is no urgency for any preemptive move. The present and top priority for CBC is to maintain FX stability.

Philippines, BSP (Thursday, June 19) — We see the Bangko Sentral ng Pilipinas (BSP) delivering a back-to-back rate cut by 25bp to 4.75% at the June meeting, prompted by the lower inflation trajectory. We expect BSP to maintain a dovish stance and continue to take a measured approach in deciding on further monetary easing. Beyond the June meeting, we see room for another 50bp rate cut in H2 2025, depending on domestic growth recovery and continuing inflation, where a sustained backup of crude oil and food prices might reverse the current downward trend in inflation.

Switzerland, SNB (Thursday, June 19) — The Swiss National Bank (SNB) is widely expected to cut its policy rate by 25bp to 0.00% at its June meeting, responding to a return of deflation and a surging CHF. May CPI fell to -0.1% y/y, the first negative print in four years, while core inflation eased to 0.5%, both below the SNB’s 0 – 2% target range. The CHF has appreciated over 10% against the USD this year, driven by safe-haven flows amid global trade tensions, further suppressing import prices. Chairman Schlegel emphasized the SNB’s focus on medium-term price stability but noted that sustained currency strength and deflation risks may necessitate further easing. Market consensus anticipates a rate cut to zero, with a one-in-four chance of a deeper move into negative territory. The SNB is also prepared to intervene in FX markets if needed, although it faces scrutiny after being added to the U.S. Treasury’s currency monitoring list.

Norway, NB (Thursday, June 19) — Norges Bank (NB) is expected to keep its policy rate unchanged at 4.5% at the June meeting, maintaining a cautious stance amid persistent inflation and external uncertainties. May’s core inflation (CPI-ATE) eased to 2.8% y/y from 3% in April, marking the lowest rate in four months. Governor Bache has emphasized that prematurely lowering the policy rate could lead to a rapid price rise. The central bank projects a policy rate reduction to 4% by the end of 2025, with a gradual further decline through the forecast horizon. Given the current inflation outlook and the central bank’s cautious stance, a pause in the easing cycle appears likely for now.

United Kingdom, BoE (Thursday, June 19) — The Bank of England (BoE) is expected to keep the bank rate unchanged at 4.25% at its June meeting, maintaining a cautious stance amid persistent inflation and external uncertainties. April CPI rose to 3.5% y/y, up from 3.2% in March, remaining above the BoE’s 2% target. Governor Bailey has indicated that, while the general direction for interest rates remains downward, the pace and extent of these changes are now significantly less predictable due to global trade policy turmoil. The U.K. economy contracted by 0.3% in April, the largest monthly decline since October 2023, driven by a £2bn plunge in U.S. exports following new tariffs and a sharp drop in legal and estate agency activities. Nonetheless, given the current inflation outlook and the central bank’s cautious stance, a pause in the easing cycle appears likely for now.

Turkey, TCMB (Thursday, June 19) — The Central Bank of the Republic of Turkey (TCMB) is widely expected to hold its policy rate at 46% at the June meeting, following a 700bp hike in April aimed at stabilizing the TRY amid political unrest. May CPI fell more than anticipated to 35.41% y/y from 37.86% in April, with monthly inflation easing to 1.53%, both below forecasts. Despite this disinflation, the TCMB has maintained its year-end inflation forecast at 24%, citing persistent uncertainties. Governor Karahan emphasized a cautious, data-dependent approach, indicating that rate cuts are not imminent. Market consensus suggests easing may begin in July, contingent on sustained disinflation and improved financial stability.

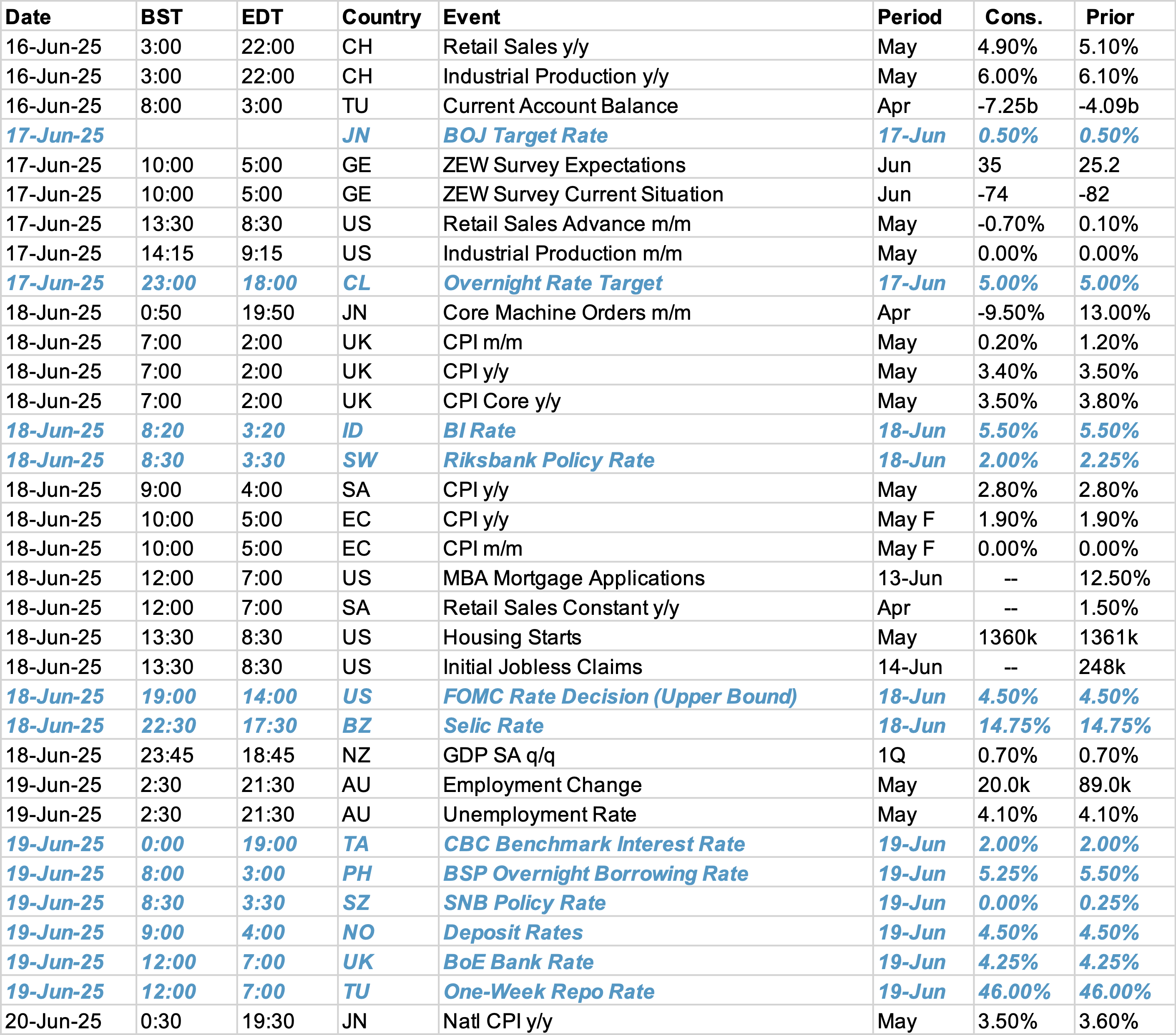

Data Calendar

Event Calendar