Coin Toss

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 10 minutes

We may see a trend reversal in the week ahead, with many clients who have been waiting on the sidelines likely compelled to act. Call this the coin toss week for investors as they move away from barbell positions long in both cash and tech, motivated by FOMO and the search for value, growth and stable returns. There is a heavy mix of key economic data points this week, including jobs, inflation, U.S. bond supply of $213bn in 2y–7y notes along with the U.S. Treasury quarterly refunding plans, IG issuance, Q2 earnings reports covering 37% of the S&P 500, and important central bank decisions from the Fed, the Bank of Japan, the Bank of Canada and many emerging markets. In addition, August 1 is the deadline for trade deals, and having the actual U.S. tariff rate will provide more clarity about growth and inflation in the months ahead. The only offset for action may be the weather, with many people at the beach instead of in front of a screen. There is a coin-toss quality to the risk ahead, which could bring significant volatility with each batch of news or lead to the momentum chasing that we have seen since April.

Just how important is August 1 to markets?

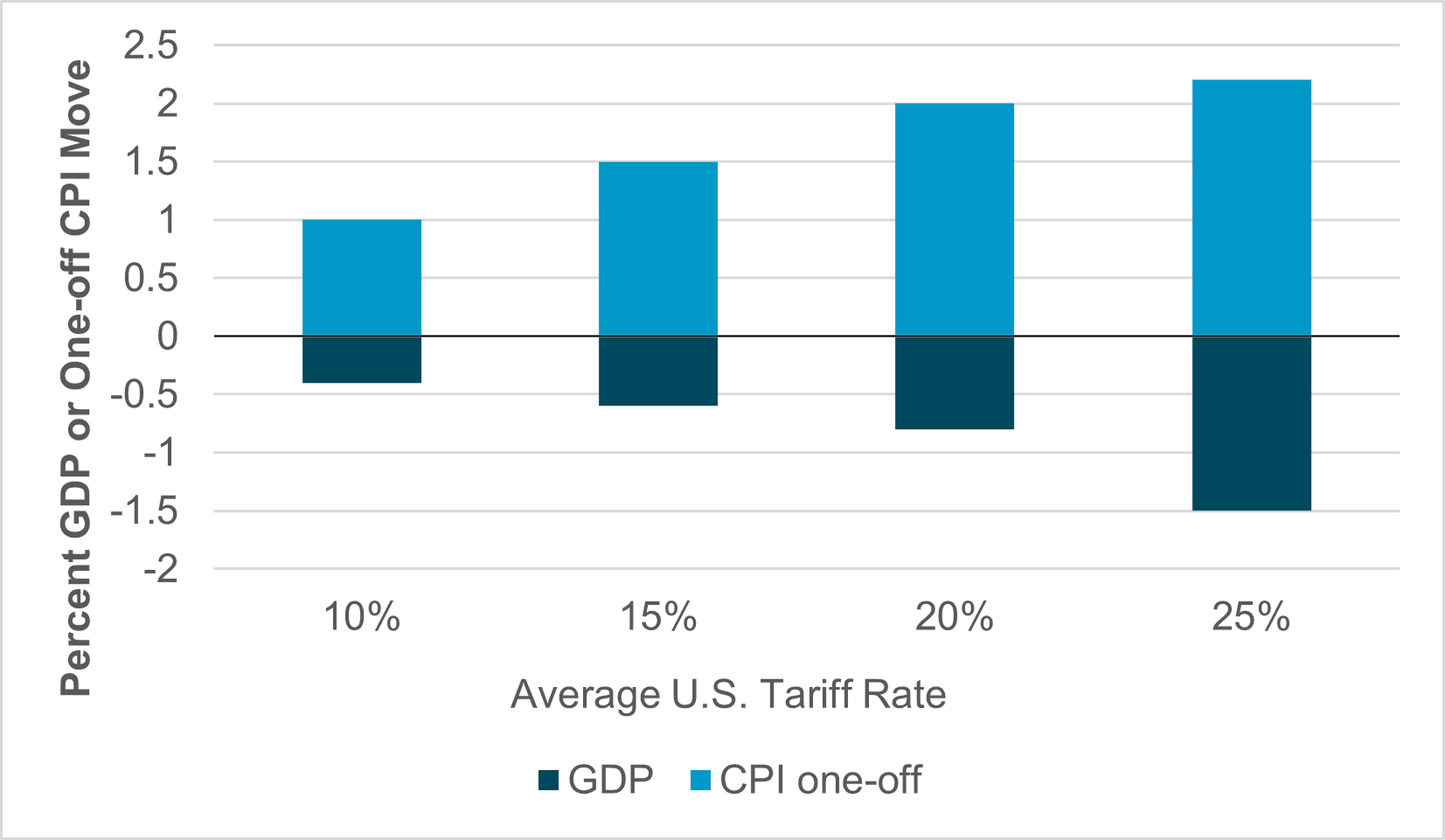

EXHIBIT #1: AVERAGE U.S. TARIFFS VS. GROWTH AND INFLATION FORECASTS

Source: BNY, Yale Budget Lab, Boston Federal Reserve

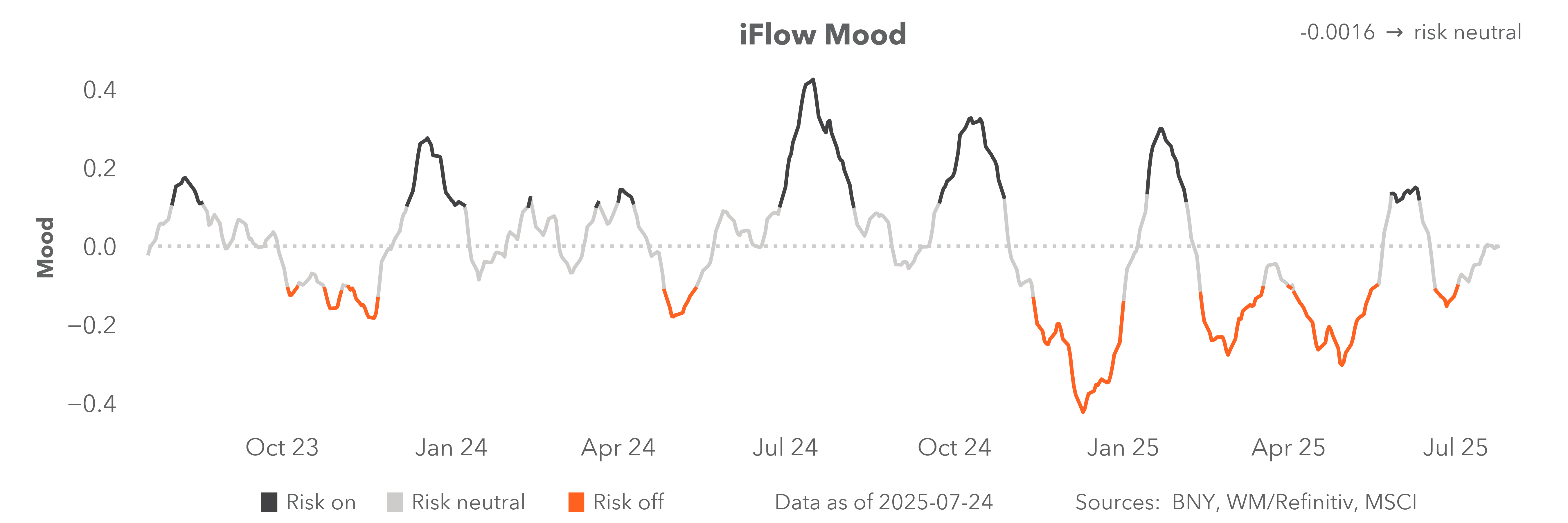

Our take: Markets have looked through the risks of tariffs, focusing on hard data and Q2 earnings in the last week. We think this will change based on the long positions for risk that show up globally. The U.S. equity market is trading at record highs, supported by Q2 earnings beats. The U.S. bond market has remained in tighter ranges, with expectations of FOMC easing in the quarter ahead. USD trading has fallen (down 0.75% on the week) but remains well off its monthly lows. iFlow data show mood, trend and carry factors are all neutral – proving out wait-and-see behavior. This should change with the clarification of the average tariff rate for U.S. goods imports starting August 1. The market has assumed deals will be finalized either at or just after the tariff deadline.

Forward look: The key driver for looking through the bravado of “Liberation Day” tariff levels was the view that a series of bilateral agreements would drive the average down. Where the U.S. average falls matters, with 15–17% the consensus. This means the U.S. will have a 1.5–2.0% one-off inflation increase and a 0.5–0.8% hit to GDP. Markets offset some of the growth pain with fiscal and deregulation factors. The chart on tariffs looks linear until you get to over 25% tariffs, when inflation risks are about the same, but growth risks rise, and over 30% there is a topping out of expectations as the cost of tariffs becomes more like a tax on consumers. Supporting this analysis on the non-linear effect is research from the Boston Fed, the Yale Budget Lab and Victoria University's Centre of Policy Studies (CoPS). We need to see what the actual tariffs are on August 1. Estimates of U.S. government revenue range from $190bn a year with tariffs of 10% to $400bn annually with tariffs of 25%. This revenue is offset by growth drags hitting other tax revenues. Rather than the U.S. dollar, the barometer for the week ahead will be the U.S. 10-year note, with a focus on the risk of breaching 4.60%. Instead of decreasing concerns about U.S. debt, higher tariffs will likely increase concerns about a U.S. slowdown, with the FOMC expected to hold off on rate cuts and job data that is expected to disappoint.

The week ahead will not be a quiet summer period in the U.S.

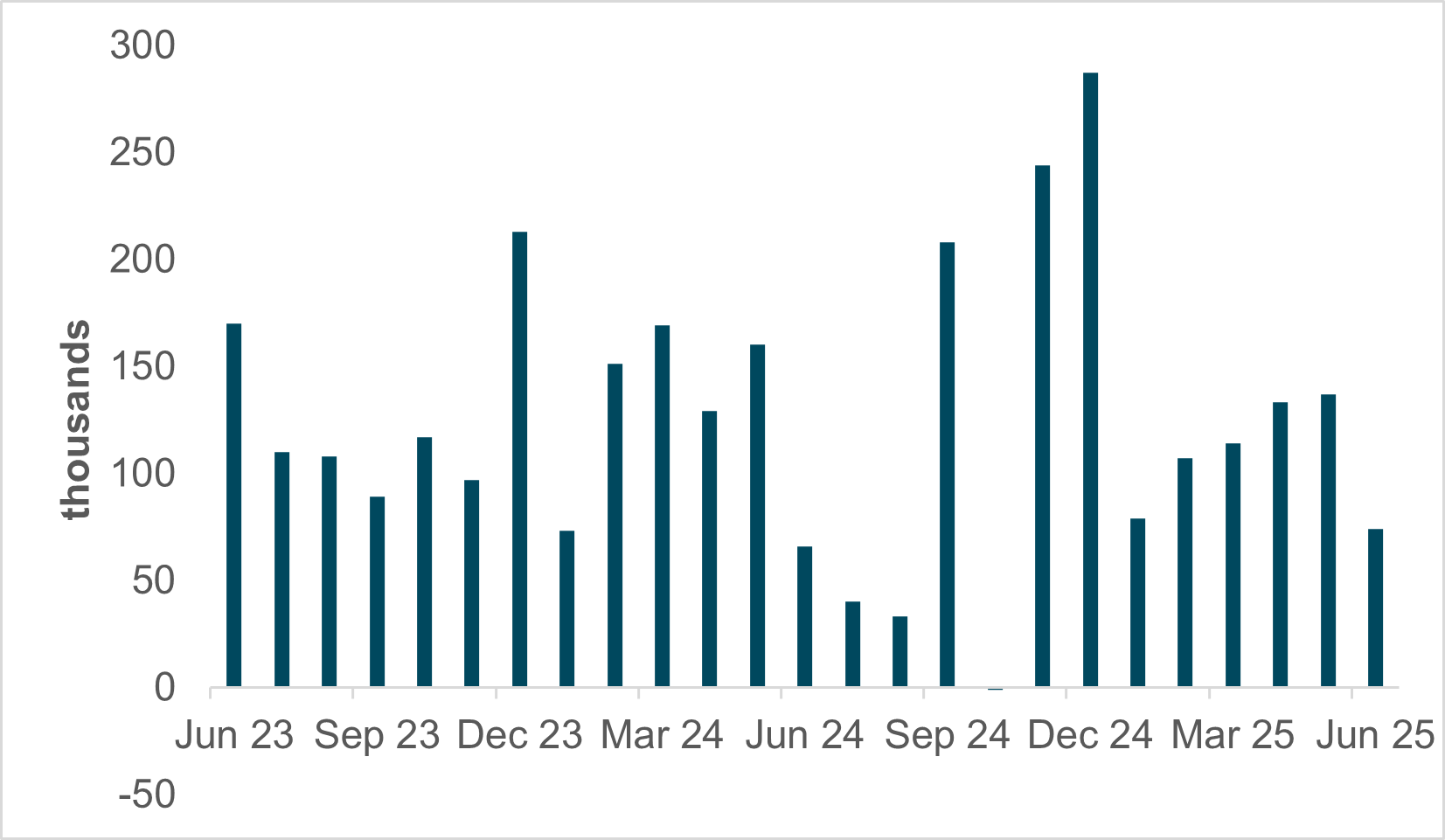

EXHIBIT #2: U.S. PRIVATE PAYROLLS

Source: BNY, BLS

Our take: Did someone mention slow weeks in the summer? There is little doubt that the upcoming week will be anything but quiet given the slew of U.S. economic data (including the July report) and an FOMC rate decision on Wednesday. Beyond the NFP data, we’ll see JOLTS, the first print of Q2 GDP, the ISM manufacturing survey, and the Employment Cost Index. This week will likely see many market participants’ eyes glued to the tape to start their days.

Our view is that the labor market is beginning to weaken, and we didn’t heavily celebrate the June release, given the fact that only 74k private sector jobs were created, and the labor force shrank. Hence, we’ll be watching all the releases – not just NFPs, but JOLTS, claims, and the ECI – to see if our concerns are justified. We are paying particularly close attention to private jobs growth and whether the retreat of foreign-born workers from the labor force continues – since March over 1.1mn have exited the jobs market. Once private sector jobs growth slows for more than a few months in a row, recessions often follow. We’re not forecasting a recession but are watchful for any new, weaker trends in the labor market.

Forward look: The FOMC meeting is almost certainly not going to yield a change in interest rates, although how the Fed (and specifically Chair Powell) characterizes the current state of inflation and economic growth will be important. We still think the inflation story is beginning to show goods price inflation, which could accelerate as tariff effects continue to work their way through the supply chain. We also expect much discussion on Fed independence, the much-criticized headquarters renovation and the meeting between Powell and the president last week. However, we don’t expect Powell to offer too much on these topics.

EMEA: Trade deal done, but price and labor data to test ECB

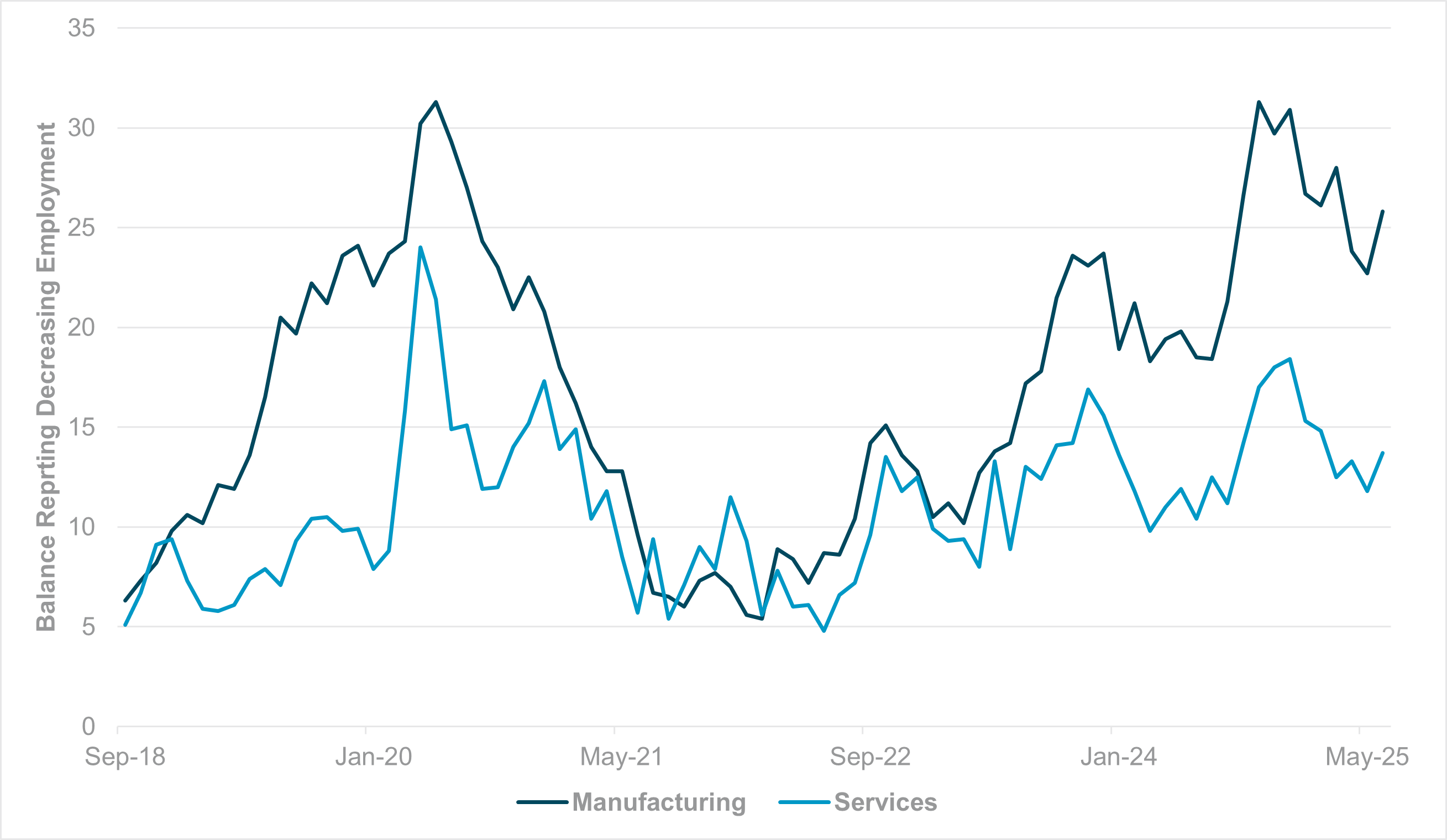

EXHIBIT #3: IFO SURVEY BALANCE OF RESPONDENTS EXPECTING DECREASE IN EMPLOYMENT, BY INDUSTRY

Source: BNY

Our take: On balance, the ECB was probably more optimistic on the economy than expected at its July meeting. President Lagarde managed to find a consensus and reports after the decision noted that the doves on the Governing Council could struggle to make the case for a cut in September due to the current run of data. However, the ECB may be “in a good place” with regard to policy as Lagarde stated, but all the risks are to the downside and in the near term, even with a framework trade deal in place for the U.S. and EU. Given the EU’s decision-making process, there will be a lag before approval as individual nation states will need to have their say as well, but an agreement has been our base case and the Eurozone can at least avoid the “severe” scenario listed in the June Staff Economic projections, which would shave potentially 40bp off growth this year alone (0.9% to 0.5%). Nonetheless, as tariffs will still be in play, albeit negotiated, the “mild scenario” detailed by the ECB will come into play, pushing inflation down to 1.7% y/y (vs. 1.6% y/y baseline), but growth will be at 1.2% y/y due to established certainty for trade over the medium term. Of course, much will depend on the details and the sectoral impact.

Forward look: With European Q2 earnings reports in full swing, we continue to see risks to profitability to the downside due to earnings translation and this will be reflected in producer and consumer prices. Lagarde may have stated that the Eurozone is at the “June baseline” in CPI, but FX assumptions are not given the central tendency was anchored at closer to 1.12. At 1.17–1.18, EURUSD is already well beyond the 75th percentile for exchange rate movements, which is only a 1.5% move. This means there is a risk that inflation will deviate from the baseline outlook for this year (current expectation is no shock) and the shock to next year will be close to 20bp, potentially to 1.5% y/y, due to FX alone. With an agreeable deal, trade won’t generate as much of an inflation shock, but the margins are very thin for the ECB to meet its mandate. Consequently, we believe that September easing should still be considered a precautionary measure even if there is a lack of data justification.

APAC to test risk on trend with central banks and key economic data

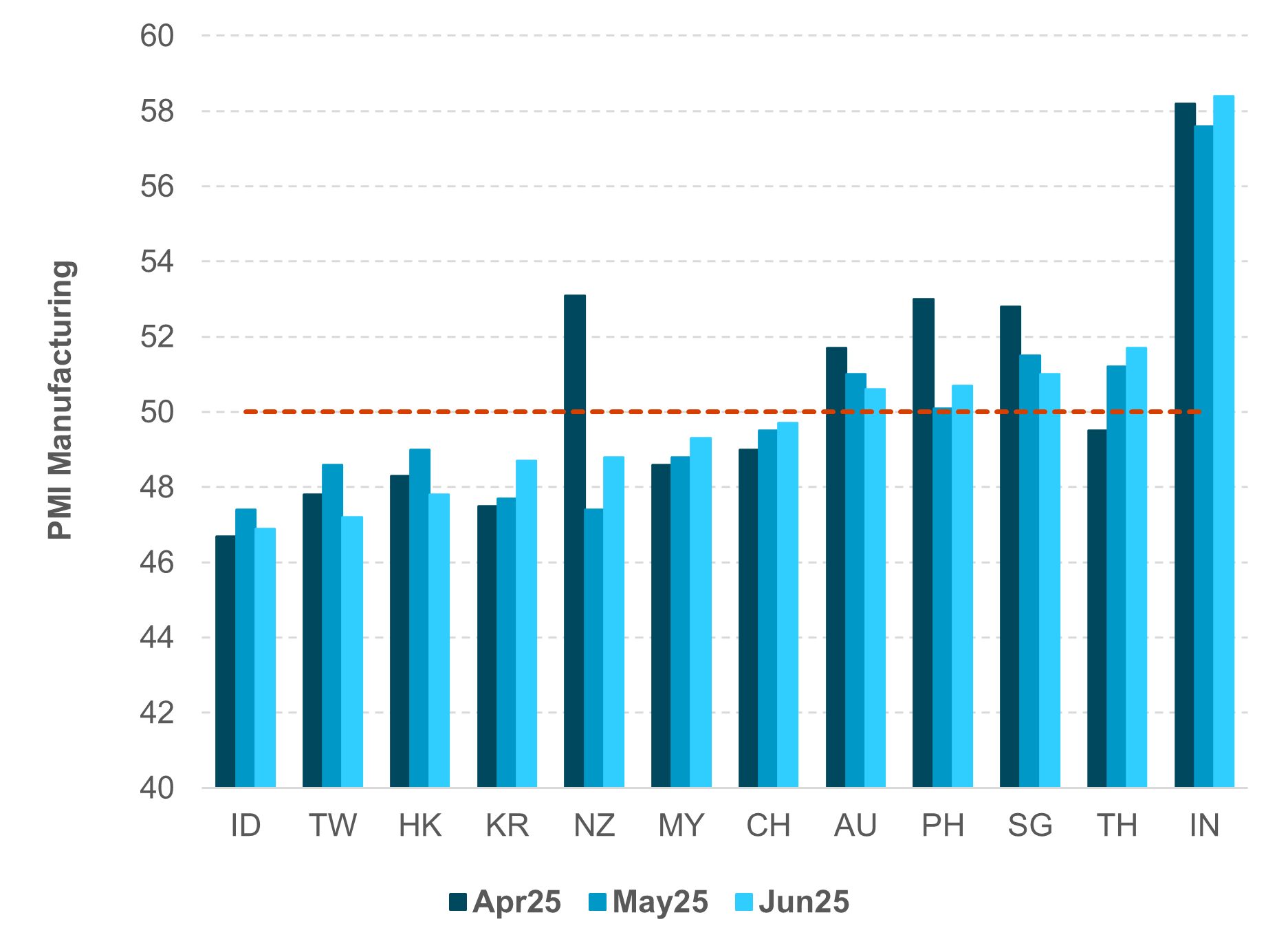

EXHIBIT #4: APAC PMI TO RISE WITH IMPROVING RISK SENTIMENT

Source: BNY, Bloomberg

Our take: In the Asia-Pacific region, the focus this week will be on the Bank of Japan’s meeting, regional July purchasing manager indexes (PMI), Indonesia and Australia inflation, as well as South Korea July trade and exports and June exports for Thailand, the Philippines and Indonesia. The U.S. and China will conduct their third round of trade talks in Stockholm from July 27–30 ahead of August 12 deadline. After an unexpectedly weaker June PMI, the expectation is for a rebound supported by strong asset price gains and positive trade negotiations over the past month. For China PMI manufacturing, we will be closely monitoring the three key subcomponents: new orders, which drifted into expansion territory in June at 50.2, new export orders and imports, which both remained in contraction at 47.7 and 47.8, respectively. For China’s PMI non-manufacturing, service business activities, which had been hovering around 50.0–50.3 since the beginning of the year, will be a key gauge of the recovery of domestic consumption. The focus will also be on Taiwan, where PMI unexpected dropped in June to 47.2, the lowest level since December 2023, despite solid export momentum, and South Korea (June: 48.7) to gauge the impact of government fiscal stimulus.

Australia Q2 inflation releases will serve as a key input for the Reserve Bank of Australia (RBA) policy meeting in August. The consensus is for the Q2 trimmed mean CPI to slow to 2.7% y/y from 2.9% in Q1 2025. That said, recent RBA Governor Bullock’s “measured and gradual” approach to policy easing suggests that August decision is not a done deal yet. The consensus is for RBA to cut 25bp to 3.60% at the August meeting.

South Korea’s July exports will serve as an early indicator of export growth recovery beyond the front loading-driven strength in H1 2025. The first 20-day exports were downbeat at–2.2% y/y compared with 4.3% y/y growth in June. The Philippines and Indonesia will release June export data.

Forward look: Current strong market sentiment is likely to see an asymmetric reaction to macro data, with weak domestic data likely to be brushed off while good data will further consolidate investors’ conviction. The Bank of Japan (BoJ) and Monetary Authority of Singapore (MAS) will convene this week. BoJ rhetoric will be closely watched given the recent trade deal and upper house election outcome. That said, BoJ impact on USDJPY is likely to be limited as the 10y U.S. Treasury and U.S. dollar had been the dominant driver. USDSGD will be closely watched for the MAS policy decision. APAC currencies are being driven by opposing factors in our view. External factors such as a weakening USD, the resurgence of foreign investor inflows and anticipation of a trade deal with the U.S. are supportive, but a weak domestic growth outlook, monetary policy easing and fiscal expansion argue for weaker currency evolution. For now, external factors may have the upper hand.

This week marks a pivotal juncture for global markets, as a confluence of rate decisions, risk reversals and headline events threatens to upend the cautious optimism that has defined July’s trading. With Q2 earnings covering 37% of the S&P 500, a hefty $213bn in U.S. Treasury supply and the FOMC meeting all landing alongside key labor and inflation data, investors face a classic “risk-off” setup – particularly as German CPI and jobs numbers are poised to challenge the ECB’s baseline narrative of gradual disinflation. The U.S. dollar, down 0.75% last week, remains rangebound, but the real test lies ahead: should the FOMC signal a more hawkish stance or U.S. payrolls disappoint, we could see a sharp reversal in risk appetite, with 10-year Treasury yields threatening to break above 4.60%. Meanwhile, the anticipated Stockholm meeting between U.S. and Chinese officials to finalize a trade deal adds another layer of binary risk, with the August 1 tariff deadline looming large – any hiccup could see risk assets retrace recent gains. In short, with positioning still largely neutral (as per iFlow data), the market’s next move hinges on a handful of high-impact data points and policy decisions. The probability of a risk-off move is elevated this week, as even a modest miss on jobs or an upside surprise in inflation could trigger a cascade of profit-taking and volatility, especially with so many investors on the sidelines, ready to chase momentum in either direction.

Central bank decisions

Chile, Banco Central de Chile (July 29) –The Banco Central de Chile is expected to cut its benchmark interest rate by 25bp to 4.75% at its July 28 monetary policy meeting. This follows June’s consumer price index falling by 0.4% – the steepest drop since late 2023 – and annual inflation easing to 4.1%. A further cut to 4.5% is possible by year-end. The benchmark rate has remained at 5.0% year to date amid persistent inflation pressures and global uncertainties. The bank’s July Monetary Policy Report emphasized flexibility, noting the monetary policy rate will gradually approach its neutral range and that future adjustments will depend on evolving macroeconomic conditions and disinflation progress. The government confirmed its GDP growth forecast at 2.5% for 2025 and 2.3% for 2026, underscoring a supportive backdrop for policy easing.

Singapore, Monetary Authority of Singapore (July 30) – The easing of inflationary pressure and downside growth warrant further easing by MAS. That said, conventional Singapore nominal effective exchange rate (SGDNEER) policy has been distorted by the weakening of the U.S. dollar, which has led to continued SGD strength despite two easing measures via a flattening of the SGDNEER slope in January and April this year. Consensus is for the MAS to maintain the status quo on SGDNEER policy. All eyes will be on a potential revision of the macro projection. The latest GDP projection is 0%–2%, while both headline and core inflation are seen at an average of 0.5–1.5% in 2025. We see MAS continuing to engineer lower front-end rates to cap SGD appreciation pressure.

Canada, Bank of Canada (July 30) – The Bank of Canada is expected to keep its policy rate on hold at 2.75% at its July 30 Monetary Policy Report announcement. This follows June’s consumer price index rising 1.9% y/y, up from 1.7% in May, while core measures such as CPI-trim and CPI-median remain stubbornly above 3%. Markets fully expect a hold this week, with some prospect of an adjustment now anticipated in the fourth quarter, subject to data. The BoC will use its July report to update its neutral rate estimate and economic projections, signaling how it plans to balance slowing inflation gains against lingering risks to growth amid domestic structural imbalances and external shocks. Meanwhile, trade issues continue to linger over the Canadian economy but the CAD’s recent performance and BoC pricing does not indicate strong risk of a highly adverse impact.

U.S., Federal Reserve (July 30) – The Federal Reserve is expected to keep its policy rate on hold at 4.25–4.50% at its July 29–30 FOMC meeting. This follows June’s consumer price index rising 2.7% y/y, up from 2.4% in May, as energy and goods prices eased and core services inflation moderated. Next week’s PCE data for June is expected to show similar levels of price growth. Market pricing points to a near-certain pause next week, with the first 25bp cut now pushed to September. However, a recent commentary suggests that there will be dissenting votes in favor of cuts, and the reasoning for a cut will likely need to be addressed. Policy guidance aside, however, we think much of the post-decision press conference will be dominated by questions surrounding personnel and policy independence, which have become more notable drivers of the dollar and broader risk sentiment.

Brazil, Banco Central do Brasil (July 31) – The Banco Central do Brasil is expected to keep its benchmark Selic rate on hold at 15% at its next Copom meeting, maintaining its pause in rate hikes after the June 24 decision to raise the rate by 25bp to 15%. This comes as tightening effects are still being felt and inflation remains well above the 3% target, with projections of around 5.2% for 2025 and GDP growth forecast at roughly 2.2% in 2025 and 1.7% in 2026. Markets expect the Selic rate to remain unchanged through year-end, delaying any prospect of rate cuts until 2026, reflecting the central bank’s commitment to a prolonged restrictive stance to anchor inflation expectations, and the bank reiterated it will not hesitate to resume hikes if inflationary pressures persist.

South Africa, South African Reserve Bank (July 31) – The South African Reserve Bank is expected to cut its repo rate by 25bp to 7.00% at its July 31 monetary policy meeting. This follows June’s headline inflation edging up to 3.0% y/y, still at the lower bound of its 3–6% target, driven by higher food, rental and utility costs alongside declining fuel prices. Since August 2024 the SARB has trimmed rates at four of five meetings to provide some rate relief and ahead of tariff risks – the upcoming meeting is just ahead of the potential imposition of a 30% U.S. tariff on South African exports on August 1, adding pressure to the economic outlook. Markets expect another 25bp reduction by year-end as the bank continues to emphasize flexibility, stating that future adjustments will depend on evolving macroeconomic conditions and the pace of disinflation.

Colombia, Banco de la República (July 31) – The Banco de la República is expected to cut its benchmark interest rate by 25bp to 9.00% at its upcoming Board of Directors meeting. This follows June’s annual inflation easing to 4.82% – the lowest since October 2021 – still above the bank’s 3% target as the economy faces fiscal uncertainties after suspending its fiscal rule and widening the 2025 deficit to 7.1% of GDP. Markets expect this reduction in July, driven by the disinflation trend and bond market gains bolstering calls for easier policy. After pausing cuts since December 2023, the bank surprised with a 25bp cut in April and has emphasized flexibility, noting that future adjustments will hinge on inflation momentum, fiscal developments, and exchange rate dynamics as it balances price stability with growth.

Japan, Bank of Japan (July 31) – The Bank of Japan is expected to keep its policy balance rate steady at 0.5% at its July monetary policy meeting. This follows the ruling coalition’s setback in the recent upper house elections and rising U.S. tariff pressure, even as core consumer inflation is projected at 2.6% for the fiscal year ending March 2026. Meanwhile, June’s core consumer price index slowed to 3.3% y/y from 3.7% in May, and nationwide CPI also fell to 3.3%, still above the BoJ’s 2% target. Markets expect the rate to remain on hold through September, with a minority anticipating a 25bp hike by year-end if wage growth and price momentum firm. The BoJ will publish its quarterly Outlook for Economic Activity and Prices after the meeting, providing clues on how it views U.S. tariff effects and the pace of future policy normalization.

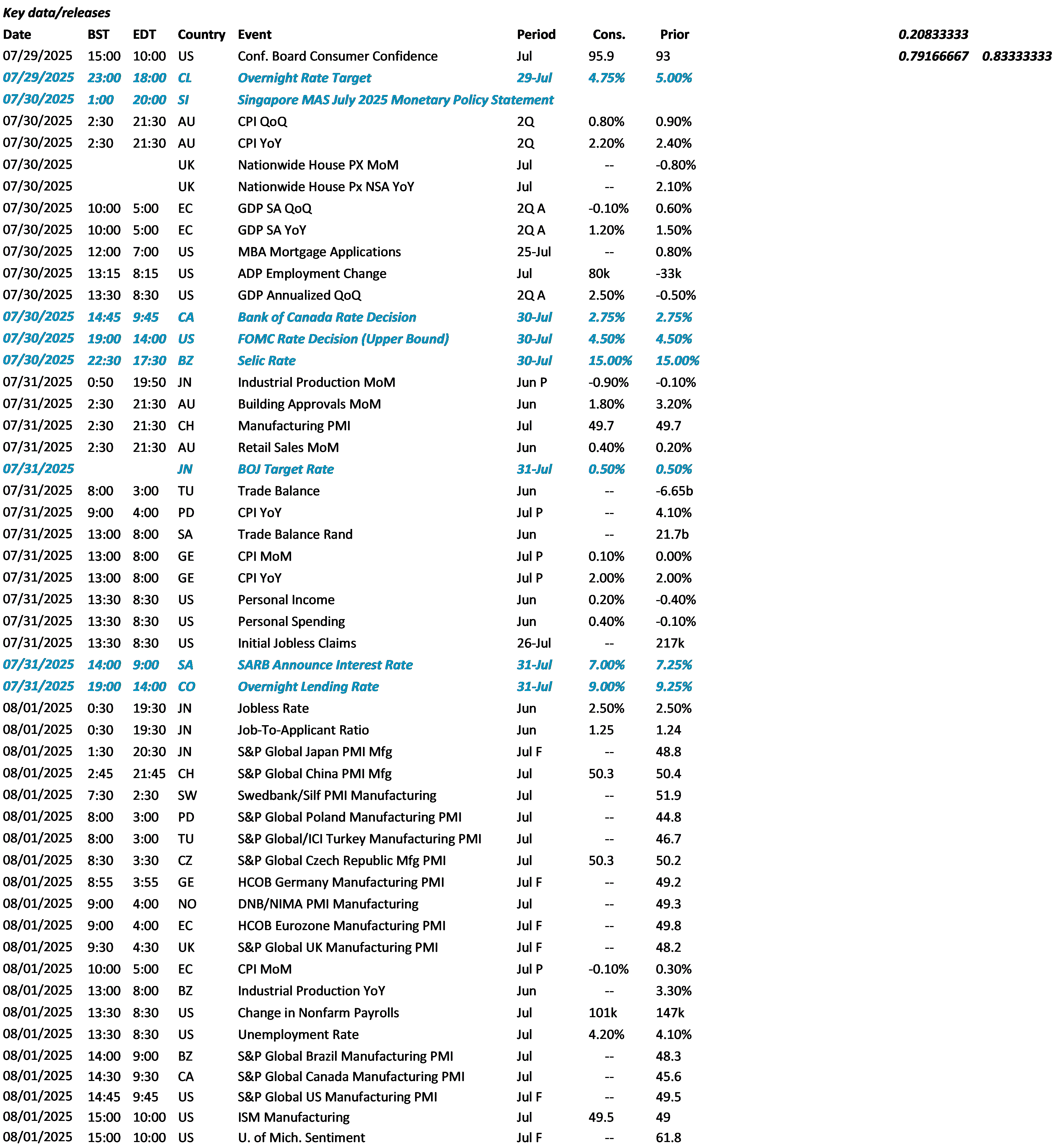

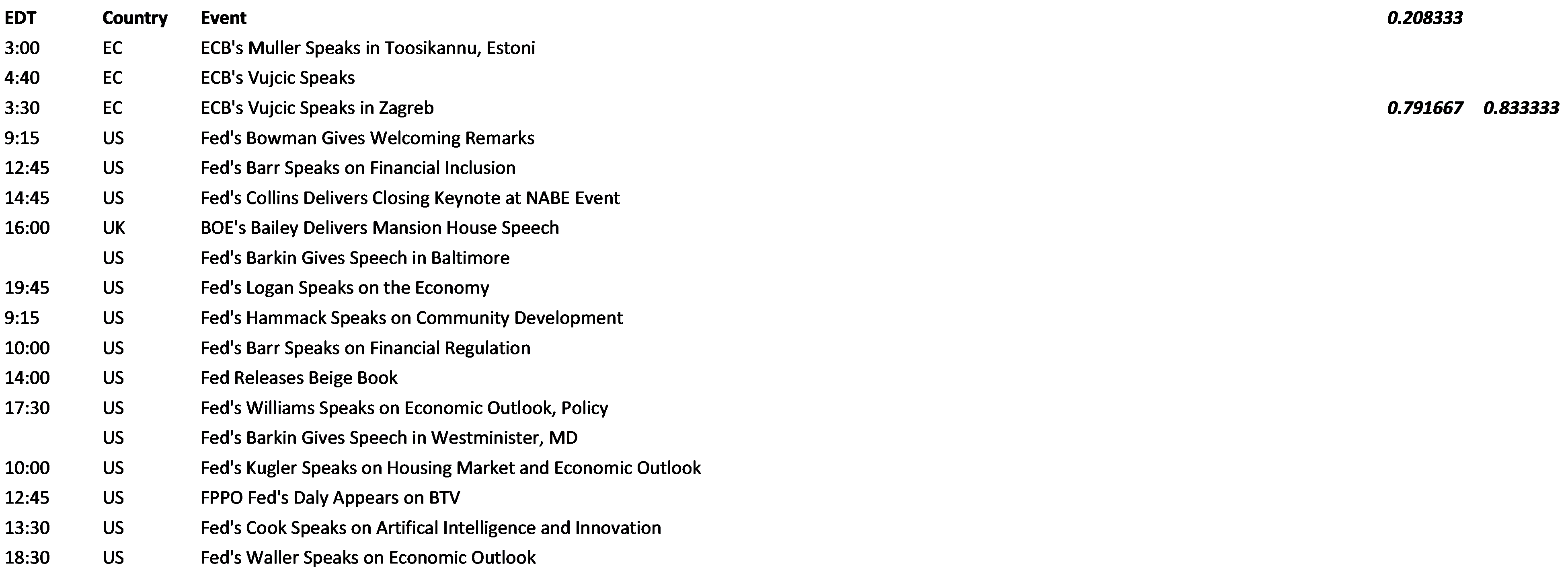

Data Calendar

Event Calendar