Market Movers: Win Win

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 9 minutes

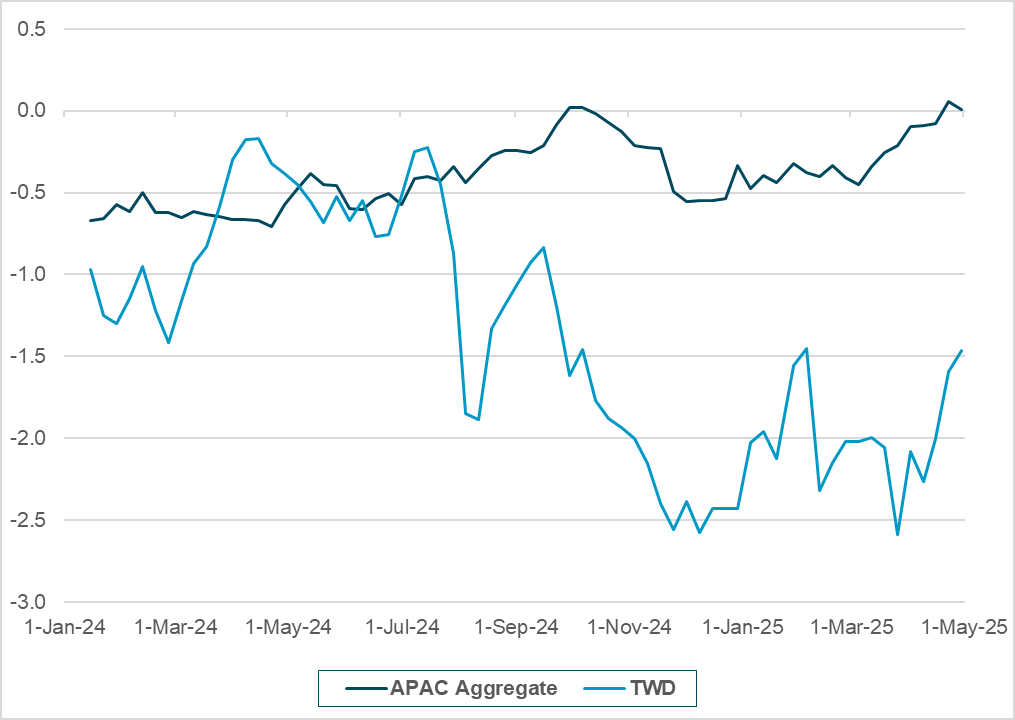

EXHIBIT #1: TWD THE LEAST HELD IN APAC, HELPING TO DRIVE TODAY’S MOVE

Source: BNY, iFlow

APAC currencies performed very strongly overnight, with TWD leading the flow surge, up over 2.5%. Based on current holdings data, we believe there is more to come in APAC, if the U.S. comes to an agreement with China and the wider region. Currently, APAC currencies are near flat in positioning, and the only strongly overweight currencies among cross-border investors are higher yielding such as the IDR, and SGD. Price action in TWD resembles what we saw with the EUR over the last few months. There are fundamental factors in favor of a recovery, including better growth, real rates and valuations. While the unwinding of extremely underheld positions amplified the process. Like the EUR, TWD holdings hit -2.5 iFlow holdings score and bounced. There is still potential for improvement as positions unwind further, though we doubt that much of APAC can move into an overheld position due to relatively low yields. The best template remains that of CHF and SEK, where funding currencies can move to flat, as the market favors surplus economies in a weak risk environment.

Risk sentiment extends its winning streak, with China confirming potential U.S. trade talks. The biggest overnight mover on the back of that story was TWD, which gained over 2.5%, sending the USD lower across APAC. The link of dollar weakness to trade is part of the narrative for deal success. The lower dollar makes U.S. asset values cheaper and along with better Q1 earnings, stabilizes the Q2 outlook somewhat. Also important overnight, U.K. local elections show the pushback against both Labour and Conservatives, something that might show up in the weekend elections in Australia and Singapore. Voters are still discontent in developed markets. There is a corollary to market optimism that is showing up in copper, which jumped 1% and correlates well to further equity gains in the U.S. However, the biggest story today is yet to be released, with U.S. non-farm payrolls looking more important than usual as the report will cover April hiring and firing. What sectors saw pain along with the wages and hours worked and the underemployed are all in play. The risk for downside jobs – i.e., NFP under 75,000 and unemployment up to 4.4% – would result in another FOMC cut being priced and further USD weakness. The question is whether that matters to stocks, which like Q1 earnings enough and see weaker U.S. data forcing more Fed easing, making equity risk a win-win regardless of the global economy. There is a tipping point between a bumpy landing and a recession which isn’t priced in this rally back in risk. Furthermore, no one looks likely to win in the political discord a weaker economy brings.

Eurozone preliminary April CPI flat at 2.2% y/y, unchanged from the previous month but higher than expectations of 2.1%. Crucially, core inflation was high at 2.7%, well above expectations of 2.5%, which is out of tune to the narrative that the European consumer is slowing down due to tariffs, as indicated by the recent downside surprise in the services PMI results. The unemployment rate ticked higher, however, to 6.2%. As the ECB is non-committal regarding rate cuts in June, this won’t change the rhetoric excessively. The Governing Council’s bias remains toward further easing, especially due to EUR strength. EuroStoxx 50 +1.161% to 5220.12, EURUSD +0.337% to 1.1328, 10y Bund +1.5bp to 2.459%.

In an interview with the Wall Street Journal, Japanese Finance Minister Kato noted the country “will act in response to any surge in Chinese imports if U.S. tariffs push unsold Chinese goods onto global markets,” underscoring concerns globally that due to high tariffs to the U.S., significant excess supply will be redirected to Japan, the European Union and other developed markets. He said that Japan will continue to ask the U.S. to “reconsider” tariffs, and that any FX rate target or new currency-related accord did not come up with his U.S. counterpart Scott Bessent. Nikkei +1.038% to 36830.69, USDJPY +0.394% to 144.82, 10y JGB +0.8bp to 1.264%.

U.S. April non-farm payrolls expected lower at 138k after the March surge to 228k. The unemployment rate is seen steady at 4.2% while average hourly earnings are expected up 0.3% m/m, 3.9% y/y from 3.8% y/y – how this number plays against FOMC easing expectations of 1% for rest of 2025 will be key.

U.S. March factory orders expected up 4.5% m/m after 0.6% m/m with the final durable goods expected up 9.2% m/m – key is cap goods orders, ex-defense and air up 0.1% m/m – the pre-tariff order surge widely priced.

Mood: Surging demand for core sovereign bonds pushed iFlow Mood deeper into risk-off zone. Equities selling momentum flattened out with higher market prices.

FX: USD outflows against broad inflows in the rest, most in AUD, ZAR and CNY. USD scored holdings back to the low of the year, below -1.

FI: Increasing demand in U.S. Treasurys, Eurozone government bonds as well as Brazilian sovereign bonds with ongoing selling pressure in Chinese and Indonesia bonds

Equities: U.S. equities stood out, with buying flows against broad selling pressure in G10. LatAm equities were sold against mixed flows in EMEA and APAC region.

“Negotiation in the classic diplomatic sense assumes parties more anxious to agree than to disagree.” – Dean Acheson

“Win-win is a belief in the Third Alternative. It’s not your way or my way; it’s a better way, a higher way.” – Stephen Covey

Japan March jobless rate ticked higher at 2.5% from 2.4% y/y with job-to-applicant ratio higher at 1.26% from 1.24% and new jobs-to-applicant ratio back at 2.32 (February: 2.30%). Labor market remains tight and supports recent upward momentum of wage hike. BoJ’s Ueda expects the recent inflation-wage cycle to be maintained at BoJ press conference at May 1, 2025. Nikkei +1.038% to 36830.69, USDJPY +0.394% to 144.82, 10y JGB +0.8bp to 1.264%.

APAC regional PMI were weak in April. Indonesia April PMI plunged the most, from 52.7 to 46.7 into contraction. South Korea, Malaysia, Thailand and Taiwan April PMI fell further into contraction at 47.5 (49.1), 48.6 (48.8), 49.5 (49.9) and 47.8 (49.8), respectively. Philippines April PMI unexpectedly surged into expansion 53.0, but the degree of confidence ahead was the second lowest in series history since 2016, the worst since March 2020. Sentiment is severely shaken in the region and does not bode well for Q1 GDP ahead. MSCI Asia -0.409% to 186.04, BBG Asia Dollar Index +0.841% to 91.4047, 12M BBG AGG APAC Government High Grade USD +0.1bp to 4.851%.

Australia Q1 PPI rose slightly from 0.8% q/q to 0.9% q/q while year-on-year stayed unchanged at 3.7%, affirming the stabilization of CPI trend. Price growth for goods and services produced by most industries was lower compared with Q4 2024 except for manufacturing products. This was driven by the depreciation of the Australian dollar affecting imported goods destined for final consumption. Elsewhere, Australia March retail sales up 0.3% m/m, 4.3% y/y from 0.2% m/m, 3.7% y/y in February 2025. Looking into the breakdown, food retailing up the most by 0.7% m/m, followed by clothing at 0.3% against a drop in sales in department stores (-0.5%) and care and restaurants (-0.5%). ASX +0.594% to 4629.66, AUDUSD +0.564% to 0.6419, 10y ACGB +3.1bp to 4.22%.

Indonesia April inflation surged from 1.03% to 1.95% y/y while core inflation ticked higher from 2.48% to 2.50% y/y. The surge is driven by the ending of electricity subsidies, which saw housing, water & electricity up 6.6% m/m, or 1.6% y/y (March: 8.45% m/m, -4.68% y/y) and the 2.46% m/m, 9.93% y/y rise in personal care and other services. Inflation is normalizing from the atypical collapse in Q1 2025. Inflation is higher but remains at the lower end of the range. Bank Indonesia is likely to stay dovish and looking for room to cut in the near term depending on FX development. April collapse in PMI is likely to weigh more over the uptick of inflation in determining monetary policy ahead. JCI +0.723% to 6815.73, USDIDR +1.01% to 16435, 10y IDGB +0.1bp to 6.876%.

The U.K. ONS reported that average U.K. household disposable income rose by 1.2% in the financial year ending 2024, reaching £32,300. This marks a moderate recovery from prior inflation-adjusted declines, though the income gains were unevenly distributed. Income inequality, measured by the Gini coefficient, remained unchanged at 34.5, reflecting persistent disparities in wealth and earnings. The top 20% of households earned 5.3 times more than the bottom 20%, highlighting limited progress on economic inclusion. Analysts noted that while fiscal policies such as targeted energy subsidies helped low-income groups, structural issues in wage growth and housing affordability remain. FTSE 100 +0.686% to 8555.12, GBPUSD +0.075% to 1.3288, 10y gilt – 6.7bp to 4.414%.

Czech PMI for April rose to 48.9 from 48.3 in March, marking the highest reading in nearly a year, though still below the neutral 50 threshold that separates expansion from contraction. The data signal a slower pace of decline in output and new orders, suggesting that the sector may be approaching stabilization after nearly three years of persistent downturn. Firms noted reduced cost pressures and slightly improving demand conditions, while business confidence rose modestly. Although the sector remains in contraction, the latest figures support expectations of a gradual turnaround in the second half of the year. Prague SE +0.873% to 2036.9, EURCZK +0.052% to 24.909, 10y CZGB +1bp to 4.077%.

Poland’s April manufacturing PMI eased to 50.2 from 50.7 in March, remaining above the 50 threshold for a third straight month but reflecting softer growth momentum. While output rose for a third month running and employment increased, the slowdown in new orders raised concerns over the durability of the recovery. Confidence among manufacturers deteriorated sharply, with sentiment posting its steepest monthly drop since early 2020. Firms cited weaker global trade conditions and elevated uncertainty as key headwinds. Nonetheless, the continued expansion suggests underlying resilience in the industrial base. WIG +1.502% to 100205.3, EURPLN +0.145% to 4.2735, 10y PGB +0.6bp to 5.22%.

Swedish manufacturing PMI increased to 54.2 in April from 53.8 in March, extending its expansionary streak to nine months and exceeding expectations. The rise was supported by stronger domestic orders and continued growth in output and employment. Companies also reported improved supplier delivery times, suggesting easing supply chain constraints. The data highlight Sweden’s industrial resilience in contrast to contraction seen elsewhere in Europe. Though external demand remains mixed, Swedish companies appear to be benefiting from firm internal demand and stabilizing input costs. OMX +0.304% to 2441.454, EURSEK +0.457% to 10.9533, 10y Swedish GB +2bp to 2.343%.

Turkey’s manufacturing PMI held steady at 47.3 in April, unchanged from March and marking the 13th consecutive month of contraction. Output and new orders continued to fall, with firms citing fragile domestic demand and geopolitical uncertainties. However, the pace of export order declines slowed, and input cost inflation accelerated, driven by a weaker lira and higher raw material prices. Supplier delivery times improved, and inventory levels were cut further. Despite persistent weakness, some respondents expressed cautious optimism that conditions could improve if economic stability returns. BI 100 +0.58% to 9131.13, USDTRY -0.247% to 38.5435, 10y TGB -73bp to 34.24%.

India’s final manufacturing PMI for April rose to 58.2 from 58.1 in March, marking the strongest improvement in the sector’s health in 10 months. This uptick was driven by robust growth in output, employment and purchasing activity. Production levels climbed at the fastest pace since June 2024, supported by a surge in both domestic and overseas demand. Export orders grew at the second-highest rate in over 14 years, with increased sales to clients across Africa, Asia, Europe, the Middle East and the Americas. To meet rising demand, companies expanded their workforce, with 9% of respondents indicating they had increased staff through a mix of permanent and temporary contracts. Purchasing activity also rose sharply, aided by efforts to build up inventories. Firms raised selling prices significantly, recording the sharpest uptick since October 2013, as strong demand allowed them to pass on higher input costs. Business confidence remained historically high, with over 30% of manufacturers forecasting higher output in the year ahead. SENSEX +0.267% to 80456.12, USDINR +0.208% to 84.32, 10y INGB -0.9bp to 6.347%.