Market Movers: Watching the Economy

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 11 minutes

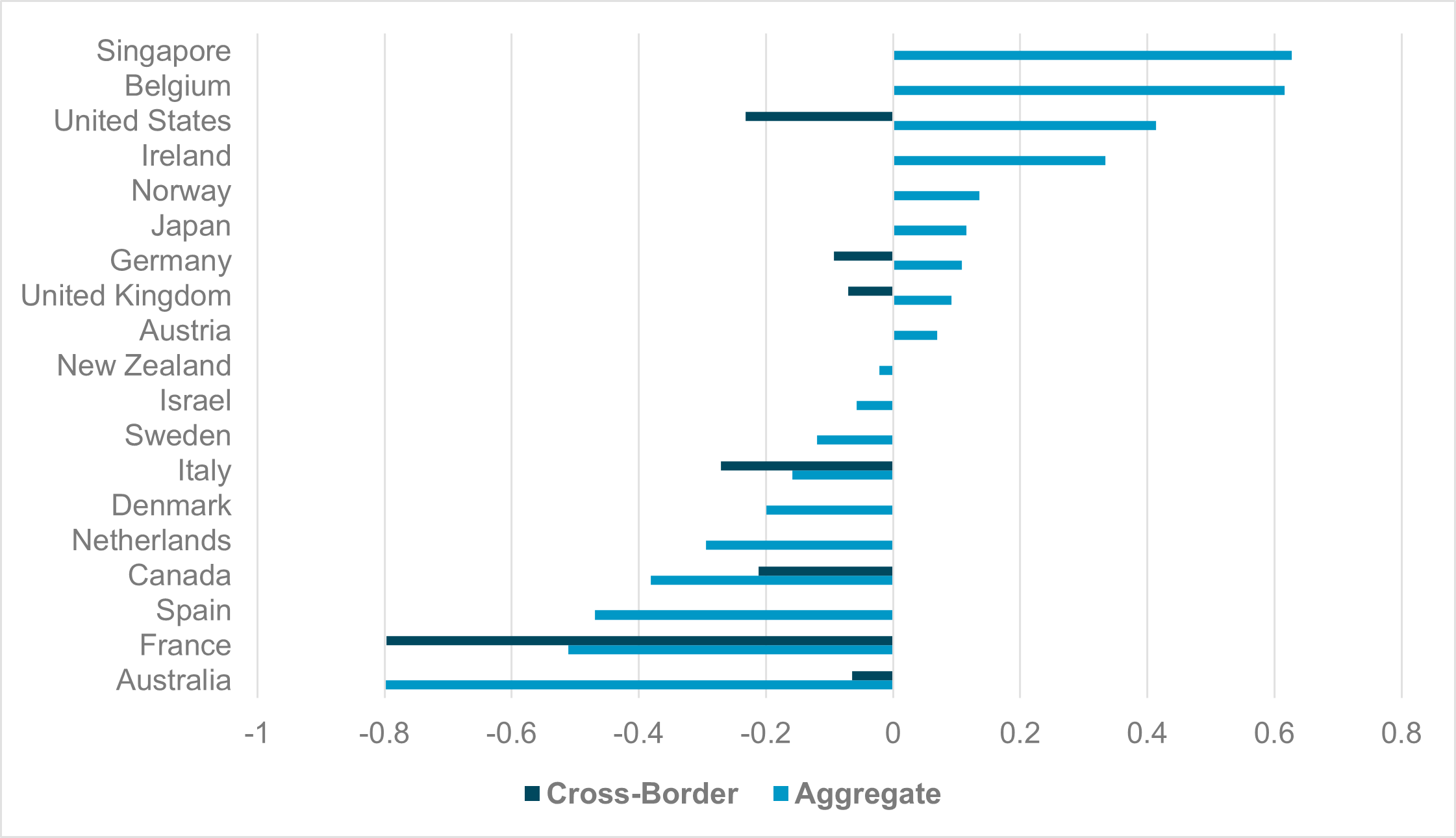

EXHIBIT #1: MIXED DEVELOPED BOND FLOWS INTO MONTH-END

Source: BNY

Month-end rebalancing provided limited support to global bond markets in May, as rising long-dated yields and structural concerns – such as weak productivity and widening deficits – persisted. While equities partially recovered, demand for higher risk premia on U.S. Treasurys and outflows in the 10+-year segment signaled ongoing pressure. Major markets like the U.S., U.K., Japan and Germany saw net buying, while high-rated markets such as Denmark, Sweden and the Netherlands experienced outflows. Australia, despite its AAA rating and strong fiscal standing, was the worst performer due to stagflation concerns and warnings from the RBA about wage growth outpacing productivity. Investors are now reassessing disinflation paths as central banks pause easing cycles and inflation premia rise. Economies with strong domestic savings continue to attract flows as markets reprice growth and debt-servicing capacity. However, the level of scrutiny of U.S. fiscal policy is rising and could weigh on broader market sentiment. Overall, the search for havens is narrowing, and sovereign bond flows remain volatile, reflecting a more cautious stance amid shifting monetary and fiscal dynamics.

Risk sentiment mixed into month-end rebalancing with focus on inflation and growth data globally. Japan CPI remains high and BoJ’s Ueda remains hawkish, leaving open the possibility of July rate hike risks. Spanish CPI was low, but regional German flash reports are higher, making the national release later today important for ECB easing and guidance next week. Growth contracted in Sweden in Q1, surprising markets. For the day ahead, U.S. PCE is expected to slow, leaving the FOMC divided on rate easing. The Trump/Powell meeting yesterday made clear political pressure isn’t as important as the economic data ahead, with jobs and ISM next week key for market expectations. The overall mood as we end May reflects less conviction and more uncertainty. The U.S. CEO Q2 2025 conference board confidence survey fell 26 points to 34 – the worst since Q2 2022, reflecting pessimism. On the other hand, global economic surprise indices are positive reflecting the tariff pause and further front-loading of goods globally. Hard data have yet to catch up to soft and that spread reflects ongoing volatility. The division between bulls and bears across markets rests on how this plays out next week, not today, with the usual rebalancing flows likely to be less powerful a driver into the close as we are all watching the economy more than the tape. The rally up in stocks, selling of bonds and ongoing USD weakness isn’t likely to shift until we see something different.

Japan May Tokyo CPI steady at 3.4% from downwardly revised 3.4%, core inflation ex-fresh food and energy rose from 3.1% to 3.3%, the highest since January 2024. Headline and ex-fresh food and energy both up 0.3% m/m. Rice inflation continues to be elevated at 93.7% y/y. Looking into the breakdown, fresh food was down the most, declining from from 3.9% y/y to 0.3% y/y, followed by furniture & household utensils at 3.1% y/y from 4.3% y/y and small increases in transportation (2.6% y/y), education (1.9% y/y) and reading & recreation at (3.3% y/y). Elsewhere, Japan’s April unemployment rate and job-to-applicant ratio remain unchanged at 2.5% y/y and 1.26% y/y, respectively, while the new jobs-to-applicant ratio eased slightly to 2.24 from 2.32. Risks to JGB yields are likely to remain to the upside. Nikkei -1.217% to 37965.1, USDJPY -0.084% to 144.09, 10y JGB -2.8bp to 1.501%.

Sweden’s GDP declined by 0.2% in Q1 2025 compared to the previous quarter, mainly due to a 3.8% drop in gross fixed capital formation, particularly in buildings and construction. However, net exports rose significantly, with exports up 1.8% and imports up 0.3%, contributing 0.8 percentage points to GDP. Compared to Q1 2024, GDP rose by 0.9% (calendar adjusted). Household consumption fell by 0.2%, while government consumption slightly increased (0.1%). Value added dropped 0.2% overall, with goods-producing industries down 2.8% and services up 1.1%. Employment declined 0.1%, and hours worked decreased 0.2%. Household real disposable income fell 0.4%. The public sector deficit narrowed to SEK 18.8bn from SEK 26.1bn a year earlier. SEK remains challenged by funding status and we continue to see it underperforming. OMX -0.127% to 2506.966, EURSEK +0.147% to 10.8811, 10y Swedish GB -3.4bp to 2.343%.

In April 2025, German retail sales fell by 1.1% in real terms and 1.2% in nominal terms compared to March, according to Destatis. However, year-on-year sales rose 2.3% (real) and 3.4% (nominal). March figures were revised upward to show a 0.9% monthly increase in both real and nominal terms. Food retail declined 0.1% (real) from March but rose 2.3% y/y. Non-food retail dropped 1.3% (real) from March but increased 2.6% compared to April 2024. Online and mail-order sales dipped 0.2% m/m but surged 14.1% y/y in real terms, highlighting strong annual growth in e-commerce. The dip may reinforce some of the dovish arguments for the ECB decision ahead of next week’s decision. DAX +0.831% to 24132.21, EURUSD -0.352% to 1.133, 10y Bund +1.8bp to 2.526%.

Italian CPI came in at flat on a monthly basis, but the annualized figure was in line with expectations at 1.7%. HICP came in at 0.1% m/m, 1.9% y/y, both in line with consensus. Combined with Spanish figures released today, the numbers support the view that Southern European headline and core inflation are materially softening but may not be enough to offset strength in the north ahead of Germany inflation due later in the day. The figures are sufficient to support additional ECB cuts next week, but the path would be far more data-dependent thereafter. FTSEMIB +0.754% to 40284.52, EURUSD -0.352% to 1.133, 10y BTP +1.9bp to 3.508%.

Switzerland’s KOF Economic Barometer rose by 1.4 points in May to 98.5, up from 97.1 in April, signaling a modest improvement in the country’s economic outlook. The uptick is primarily driven by positive momentum in the Swiss manufacturing sector, where indicators for general business conditions, exports, production and competitiveness all improved. However, demand-side components – specifically foreign and consumer demand – remained under pressure. Within manufacturing, Swiss industries such as chemicals and pharmaceuticals, wood, glass, construction materials, food and beverages, and paper products reported more favorable prospects. Meanwhile, the textile and metal sectors showed signs of weakness. Inventory indicators for intermediate goods also declined. CHF’s safety status is still in flux due to tariff risks. SMI +0.867% to 12292.39, EURCHF -0.23% to 0.93301, 10y Swiss GB -1.9bp to 0.281%.

According to Statistics Poland’s flash estimate, consumer prices in May 2025 rose by 4.1% y/y and fell by 0.2% m/m. The price index stood at 104.1 compared to May 2024, and at 99.8 relative to April 2025. Food and non-alcoholic beverages increased by 5.5% y/y, while electricity, gas, and other fuels surged by 13.1%. In contrast, fuel prices for personal transport fell 11.4% y/y and 3.7% m/m. The inflation rate remained above the National Bank of Poland’s 2.5% target, continuing the recent trend of elevated inflation. We expect presidential elections on Sunday to play a bigger role in Polish assets for now. WIG -1.33% to 100599.4, EURPLN +0.18% to 4.2508, 10y PGB -6.8bp to 5.369%.

German CPI is expected to touch 2.1% y/y (2.0% y/y HICP), 0.1% m/m. Regional prints earlier today have erred to the upside.

U.S. April personal income and spending is seen to ease to 0.3% y/y and 0.2% y/y from 0.5%, 0.7%, respectively.

U.S. April core PCE consensus sees easing from 2.6% to 2.5% y/y.

U.S. April advance goods trade balance is projected to narrow to $-143bn from $-163bn.

U.S. April retail inventories consensus unchanged at -0.1%.

U.S. May MNI Chicago PMI consensus sees improvement to 45.1 from 44.6.

U.S. May final University of Michigan consumer sentiment is seen improving to 51.5 (flash: 50.8) while 1-year inflation expectation is projected to ease from flash estimate 7.3% to 7.1%.

Canada Q1 GDP is projected to slow to 1.7% from 2.6% in Q4 2024.

Brazil Q1 GDP is seen to pick up on the quarter at 1.5% q/q, but slowing to 3.1% y/y.

Mood: iFlow Mood retains its risk-on mode with continued elevated demand for equities, but lessened buying in sovereign government bonds.

FX: CNY, KRW and PEN posted the most significant inflows, with limited outflows across the iFlow Universe. USD, SEK and TWD were lightly sold.

FI: Good demand in U.S. Treasurys, Singaporean and Chinese government bonds as well as light buying in U.K. gilts and Japanese government bonds. Australian government bonds were most sold.

Equities: Good buying in EMEA, EM APAC and LatAm against better outflows in the G10 complex, most in Japan, Sweden and Canada. Hong Kong, Indonesia and Peru were the top three recipient of flows.

“It’s not what you look at that matters, it’s what you see.” – Henry David Thoreau

“Information is the oil of the 21st century and analytics is the combustion engine.” – Peter Sondergaard

U.K. business confidence rose sharply in May, reaching 50% − an 11-point increase and the highest level since August 2024, according to the Lloyds Business Barometer. Optimism in firms’ own trading prospects rose six points to 56%, while confidence in the wider economy jumped 16 points to 44%. The East Midlands (66%) and North East (65%) were the most confident regions. Construction confidence hit a nine-month high at 56%, services reached a one-year peak at 54%, and manufacturing edged up to 40%. Retail, however, declined by five points to 40%, the lowest since January. Hiring expectations, wage outlook and trading prospects all improved, signaling resilience amid ongoing global uncertainty and strengthening financial markets. FTSE 100 +0.765% to 8783.12, GBPUSD -0.149% to 1.3472, 10y gilt +1.2bp to 4.66%.

In Q1 2025, Italy’s GDP grew by 0.3% q/q and 0.7% y/y, confirming preliminary estimates. The annual growth forecast for 2025 rose to 0.5%. Domestic demand contributed 0.4 percentage points to GDP growth, driven by a 0.1% rise in household and private non-profit consumption and a 1.6% increase in fixed investments, while public sector spending weighed negatively. Imports and exports rose by 2.6% and 2.8%, respectively, with net external demand contributing 0.1 points. Inventory changes subtracted 0.3 points. Value added increased in agriculture (+1.4%) and industry (+1.2%) but declined slightly in services (-0.1%). Hours worked rose by 1%, per capita income by 0.5%, and employment by 0.7%. FTSEMIB +0.754% to 40284.52, EURUSD -0.352% to 1.133, 10y BTP +1.9bp to 3.508%.

Spain’s estimated annual inflation rate (CPI) for May 2025 is 1.9%, down from 2.2% in April, according to the National Statistics Institute’s flash estimate. The decline is mainly attributed to lower prices in leisure and culture compared to May 2024, as well as decreased transport costs and a smaller rise in electricity prices. Underlying inflation, which excludes non-processed food and energy, also fell by 0.3 percentage points to 2.1%. The Harmonized Consumer Price Index (HCPI) shows a similar annual drop to 1.9%, with the underlying HCPI at 2.1%. The estimated monthly change in the HCPI is -0.1%. IBEX 35 +0.301% to 14187, EURUSD -0.352% to 1.133, 10y bono +1.3bp to 3.125%.

In Q1 2025, Turkey’s GDP grew by 2.0% y/y and 1.0% q/q (seasonally and calendar adjusted). At current prices, GDP reached TRY 12.13tn (USD 335.5bn), a 36.7% increase from the previous year. Sector-wise, construction saw the highest growth at 7.3%, followed by information and communication (6.1%), and other services (4.7%). Industry and agriculture declined by 1.8% and 2.0%, respectively. On the expenditure side, household consumption rose by 2.0%, government spending by 1.2%, and gross fixed capital formation by 2.1%. Exports slightly declined (-0.01%) while imports increased by 3.0%. Compensation of employees surged by 42.9%, raising their share in gross value added to 43.7%, up from 41.7% a year earlier. BI 100 -1.07% to 9072.39, USDTRY +0.345% to 39.242, 10y TGB -3bp to 33.1%.

In April 2025, Turkey’s seasonally adjusted unemployment rate rose to 8.6%, up 0.6 points from March, with male unemployment at 7.1% and female at 11.5%. The number of employed persons fell by 316,000 to 32.36 million, bringing the employment rate down to 48.8%. Labor force participation declined slightly to 53.4%. Youth unemployment increased to 15.7%, with a sharp gender gap: 11.2% for men and 23.7% for women. Average weekly working hours dropped to 42.2. The composite labor underutilization rate surged to 32.2%, reflecting rising time-related underemployment and potential labor force pressures.

The Czech economy grew by 0.8% q/q and 2.2% y/y in Q1 2025. Gross value added rose 1.3% q/q, led by industry (+1.6%), construction (+3.4%), IT (+2.0%) and finance (+5.9%), while the trade and hospitality sectors declined. Household consumption and gross capital formation supported growth, though government spending fell 1.5% q/q. Year on year, household and government consumption and inventories contributed positively to GDP, while fixed capital formation and net exports weighed on it. Household spending rose 0.1% q/q and 2.5% y/y. Fixed capital formation increased 1.1% q/q but declined 0.6% y/y, due to lower investment in machinery and transport. Exports grew 2.8% q/q and 3.6% y/y; imports rose 2.1% and 4.6%, respectively. The trade surplus reached CZK 140.8bn. Prague SE -0.417% to 2149.51, EURCZK -0.004% to 24.917, 10y CZGB -4.6bp to 4.16%.

South Korea April industrial production dropped -0.9% m/m after 2.9% m/m gain in March. In year-on-year terms, IP came at 4.9% from a downwardly revised 4.4% (from 5.3% y/y). Within the manufacturing sector, the April production index is -0.9% m/m, 5.2% y/y (March: 3.1% m/m, 4.7% y/y), the shipment index at 0.9% m/m, 2.5% y/y (March: 0.9% m/m, 0.7% y/y), the inventory Index came in flat 0% m/m, -6% y/y (March: -2.4% m/m, -5.7% y/y). KOSPI -0.844% to 2697.67, USDKRW +0.668% to 1380.05, 10y KTB +5.8bp to 2.76%.

South Korea April cyclical leading economic index (LEI) gains for the third straight month at 0.3% m/m, the most since July 2023. The recovery of LEI y/y at 0.2% y/y bodes well for the stabilization of GDP in the coming quarter after a contraction in Q1 2025.

Japan April flash industrial production eases to -0.9% m/m, 0.7% y/y (March: 0.2% m/m, 1.0% y/y). Elsewhere, Japan April retail sales improve to 0.5% m/m, 3.3% y/y from March -1.2% m/m, 3.1% y/y. Looking into the breakdown, motor vehicle sales surged 7.1% m/m while general merchandise was down -5.7% m/m. Elsewhere, Japan April housing starts slowing to -26.6% y/y after a strong 39.1% y/y gain in March. Year-to-date growth rate at 1.32% ytd y/y. Nikkei -1.217% to 37965.1, USDJPY -0.084% to 144.09, 10y JGB -2.8bp to 1.501%.

Australia April total building approval falls -5.7% m/m after -7.1% m/m drop in March. Private sector homes did better, with a small rebound of 3.1% m/m, the most since March 2024, after -1.9% m/m in March. Australia April retail sales fell -0.1% m/m, 3.8% y/y from March 0.3% m/m, 4.3% y/y. The biggest drag is the large falls in clothing, footwear and personal accessory retailing (-2.5% m/m) and department stores (-2.5% m/m) against gains in cafes, restaurants (1.1% m/m) and household goods (0.6% m/m). Elsewhere, Australia April private sector credit growth had a strong monthly gain of 0.7% m/m, the most since September 2022 and up 6.7% y/y from 6.5%. Investor housing (5.93%) credit growth has surpassed owner-occupier credit growth (5.69% y/y) for the first time since late 2015. ASX +0.747% to 4767.31, AUDUSD -0.389% to 0.6417, 10y ACGB -11.4bp to 4.258%.

New Zealand April building permits fall -15.6% m/m after 10.7% m/m gain in March. In the year ended April 2025, the actual number of new dwellings consented was 33,554, down 5.2% from the year ended April 2024. The annual value of non-residential building work consented was $8.9bn, down 7.6% from the year ended April 2024. Elsewhere, New Zealand May consumer confidence dropped to 92.9, the lowest since October 2024. Two-year inflation expectations fell from 4.7% to 4.6%.NZX 50 +1.12% to 12418.89, NZDUSD -0.235% to 0.5953, 10y NZGB -6.9bp to 4.566%.