Market Movers: Tightropes

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 15 minutes

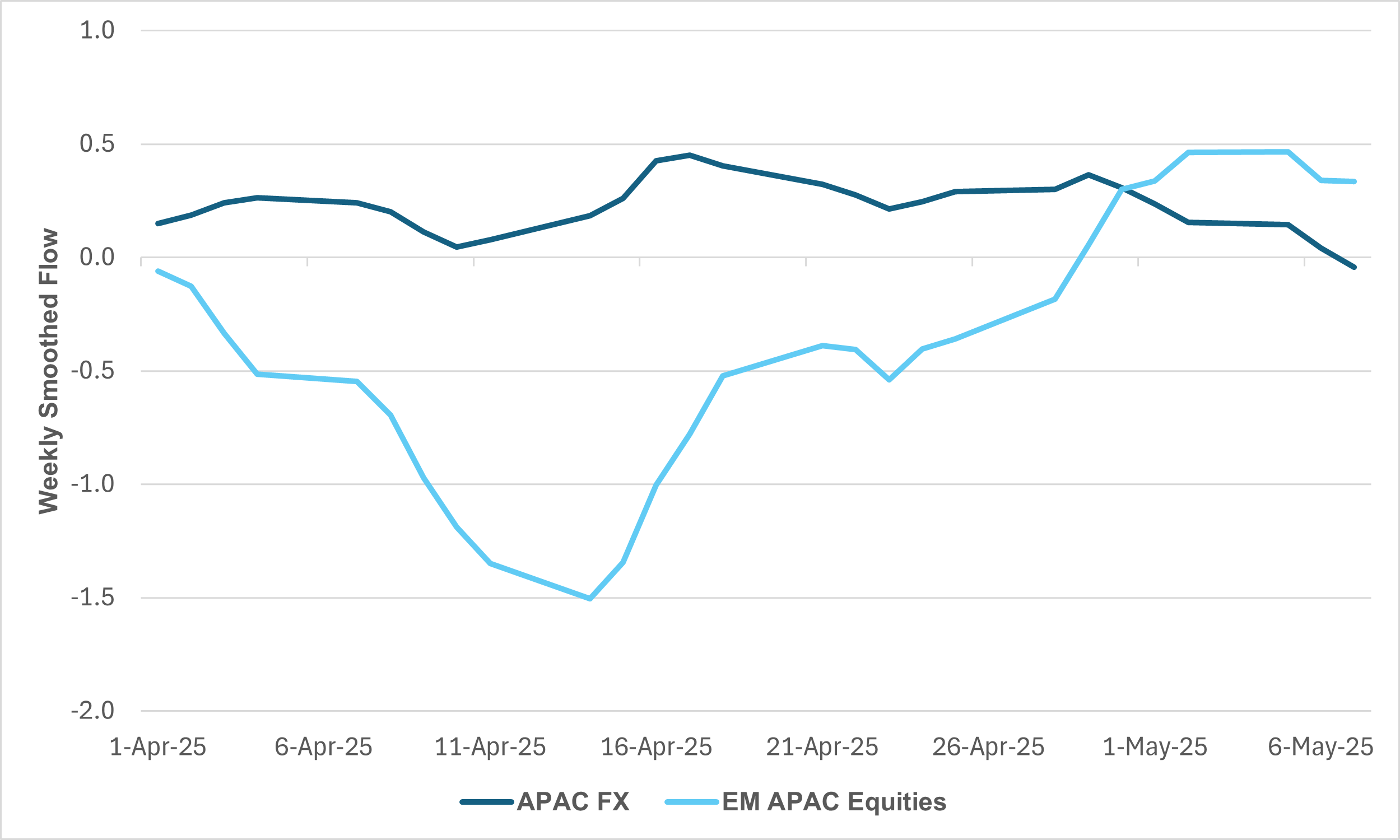

EXHIBIT #1: STRONG RECOVERY FLOW INTO EM APAC EQUITIES BUT FX TURNS TO NET SALES

Source: BNY, U.K. Government

Equity flows for APAC have clearly recovered but given the comments and actions from central banks in the region this week, tolerance for full-on FX and equity exposure is limited. After all, these economies remain export-driven, and the situation with the U.S. remains unresolved. As a result, the risks to economic growth are tilted to the downside, which also implies downside risks to inflation. While equity inflows that help loosen financial conditions are welcome, the added disinflationary — or even deflationary — pressures from a stronger currency are not. It is the latter that has triggered a strong policy response. Firm language from Taiwan and record intervention by the Hong Kong Monetary Authority were notable, but it was the mid-week easing by the People’s Bank of China that set the tone for the entire region. Even if other central banks are willing to tolerate some further currency appreciation to reflect valuation adjustments, widening policy differentials with Beijing — especially in today’s climate of persistent uncertainty — may prove a step too far. As a result, weekly smoothed FX flows have turned negative for the first time since early April. Hedging demand is rising, likely encouraged by central banks, and we expect this trend to continue. All in all, these economies will remain supportive of equity inflows, but the effects on foreign exchange will be tightly managed. This should also be a welcome asset allocation stance for cross-border investors as it limits downside risk in earnings for the companies involved, and a yield pick-up back into dollars is achievable in most cases.

Risk sentiment continues to recover with hope for more from the U.S./China icebreaker talks this weekend. The market is hoping for de-escalation, but China’s moves on rare earths overnight underscores the challenges afoot. There is a balancing act in play from the Trump Administration as U.S. Treasury Secretary Bessent pushed U.S. investment opportunities for foreigners given U.S. labor productivity and deregulation. On the other hand, U.S. Commerce Secretary Lutnick warned that the South Korea and Japan trade talks are complex — more-so than the U.K. Unlike the FOMC which this week failed to give forward guidance on inflation or growth and stayed in their wait-and-see stance on policy, the Trump team is pushing for markets to believe in forward guidance on growth and stocks. The prerequisite for any U.S. equity rally to hold remains dependent on earnings and clarity on tariffs. What we have learned this week is that the 10% reciprocal rate is the floor. This is important and has wider implications for rates and the USD. The role of sectoral tariffs beyond aluminum and steel — autos, pharmaceuticals and maybe movies, all that leaves 15% or 20% average tariffs in models — which implies higher one-off inflation and lower global growth. The consensus is 2.5% CPI and a bumpy zero or slightly higher GDP in 2025. All that can change, and quickly, with this weekend like all the others filled with hopes about talks. For the day, Canadian unemployment looks important given the Carney/Trump talks and the long runway towards any deal take-off given this is about United States-Mexico-Canada Agreement and Mexico being part of the discussion. The other story is about the simmering conflict between India and Pakistan. While this isn’t new, the escalation rhymes with other larger conflicts in the past and the current policy — from Vice President J.D. Vance noting its “none of our business” is reminiscent of the U.S. isolationist stance toward WWII. The contrast to President Trump’s offer to broker a peace deal stands out and may have the makings of more, not less U.S. foreign policy initiatives.

In a surprise decision, the Central Reserve Bank of Peru (BCRP) reduced its benchmark interest rate by 25 basis points to 4.50%, bringing it closer to the estimated neutral level. The decision reflects recent inflation data, with monthly inflation at 0.32% and core inflation at 0.14% for April. Twelve-month headline inflation rose to 1.7%, while core inflation remained stable at 1.9%, near the target range. Inflation expectations held at 2.3% and projected to converge toward the 2% target in the coming months. Economic activity indicators weakened slightly but remained near potential. Global trade tensions have raised uncertainty and market volatility. The BCRP emphasized it will closely monitor inflation dynamics and adjust policy as needed. BVL PGI -0.066% to 30324.83, USDPEN +0.303% to 3.6345, 10y PGB 0bp to 6.55%.

South Korea’s current account registered a surplus of $9.14 billion in March, driven by a robust goods account surplus of $8.49 billion, as exports rose 2.2% year-on-year to $59.31 billion, and imports increased 2.3% to $50.82 billion. The services account posted a $2.21 billion deficit, mainly due to travel and other business services shortfalls. The primary income account showed a $3.23 billion surplus, driven by higher equity income, while the secondary income account posted a $0.37 billion deficit. On the financial side, net assets increased by $7.82 billion, supported by gains in direct and portfolio investments. However, reserve assets declined by $2.58 billion. The figures indicate continued strength in Korea’s external balance despite service sector weaknesses, but tariffs and global trade uncertainty will challenge these numbers. KOSPI -0.086% to 2577.27, USDKRW +0.325% to 1400.4, 10y KTB +2.3bp to 2.625%.

Japan’s inflation-adjusted real wages fell by 2.1% year-on-year in March, marking the third consecutive monthly decline as inflation continued to outpace income growth. Nominal wages increased by 2.1% to an average of ¥308,572 ($2,132), a slowdown from February’s 2.7% rise. Base salaries rose by 1.3%, while overtime pay decreased by 1.1%, the sharpest drop since April 2024, indicating potential softening in business activity. Consumer inflation remained elevated at 4.2%, driven by rising food costs. Despite major companies agreeing to over 5% wage hikes during spring labor negotiations, these increases have not yet been reflected in the data. The persistent decline in real wages underscores challenges in boosting household purchasing power amid ongoing inflationary pressures. Nikkei +1.556% to 37503.33, USDJPY +0.489% to 145.2, 10y JGB +3.4bp to 1.369%.

China’s exports rose 8.1% year-on-year in April, exceeding expectations despite a sharp 21% decline in shipments to the U.S. following the imposition of 145% tariffs. Increased exports drove the overall growth to Southeast Asia and Europe, as Chinese firms redirected trade to alternative markets. Imports fell slightly by 0.2%, indicating continued softness in domestic demand. The trade surplus with the U.S. narrowed to $20.5 billion, reflecting reduced bilateral trade volumes. The data precede upcoming China-U.S. trade talks in Switzerland, where tariff relief is expected to be central to discussions. While April’s figures suggest external demand remains resilient, ongoing trade tensions and elevated shipping costs could constrain future growth without policy changes or improved bilateral relations with the U.S. CSI 300 -0.175% to 3846.16, USDCNY -0.025% to 7.2446, 10y CGB +0.2bp to 1.631%.

The People’s Bank of China issued its Q1 Monetary Policy Report. It stated that policy will remain moderately accommodative to support the ongoing economic recovery, focusing on maintaining ample liquidity and lowering financing costs. The Bank pledged to fine-tune the pace and intensity of monetary tools based on domestic and global conditions, while improving the interest rate transmission mechanism. Priorities include enhanced credit support for small businesses, green finance, tech innovation, and stabilizing consumption and trade. The PBOC will also continue to guide lending rates lower, manage expectations around the RMB, and strengthen financial system resilience. It reiterated that monetary policy will strike a balance between growth and risk prevention, with a clear emphasis on macro policy coordination and preserving overall economic stability amid rising external headwinds.

Norway’s Consumer Price Index (CPI) rose by 2.5% year-on-year, slightly down from 2.6% in March. The CPI, adjusted for tax changes and excluding energy products (CPI-ATE), increased by 3.0% over the same period. Month-on-month, the CPI rose by 0.7%, while the CPI-ATE increased by 0.5%. These figures indicate a continued moderation in headline inflation, with core inflation also showing signs of easing. The data broadly support the findings from Norges Bank’s decision yesterday, in which the policy board continued to express support for easing at some point this year, but inflation remained well above target for an earlier move. Other forms of activity data also show softening output, but the strong labour market will likely keep core inflation elevated; the current run-rate of underlying inflation remains well-above target. OSE -0.396% to 1508.12, EURNOK +0.264% to 11.682, 10y NGB +2.3bp to 3.988%.

Hungarian April CPI rose 4.2% year-on-year and 0.2% month-on-month. Food prices increased by 5.4% annually, with especially sharp rises in eggs (+26.9%), flour (+23.7%), and edible oil (+23.4%). However, some items like margarine (–29.2%) and milk products (–7.5%) declined. Service prices rose 7.0%, notably in postal services (+11.3%), rents (+11.0%), and vehicle repair (+10.5%). Electricity, gas, and fuel prices climbed 3.5%, while motor fuel prices fell 7.1%. Compared to March, food prices dropped 1.3%, but natural gas surged 8.3% and clothing rose 2.1%. Services became 0.8% more expensive month-on-month. The data reflect persistent inflation in core services, while food prices showed monthly declines due to seasonal and commodity factors. Budapest SI +1.126% to 93771.89, EURHUF +0.24% to 404.59, 10y HGB -1bp to 6.87%.

In a speech in Reykjavik, BoE Governor Andrew Bailey stated that the U.K. has shifted from a stable monetary environment (the “NICE” era) to a volatile one (“NaSTY” – Not-As-Tranquil Years), shaped by global shocks like the pandemic, war in Ukraine, and trade fragmentation. Bailey defended the U.K.’s flexible inflation-targeting framework and stressed the value of an independent, individually accountable Monetary Policy Committee. To adapt to growing uncertainty, the Bank is shifting toward scenario-based policymaking rather than relying solely on a single forecast. He welcomed Ben Bernanke’s recommendations to enhance the BoE’s data, modelling, and risk analysis capabilities. Crucially for near-term monetary policy, he stated that there was evidence of pay inflation coming down in the U.K., which is a prerequisite for a more sustained easing cycle. FTSE 100 +0.402% to 8565.9, GBPUSD +0.189% to 1.3271, 10y Gilt +4.7bp to 4.593%.

Meeting in Moscow for Russia’s Victory Day Parade, Chinese President Xi Jinping and Russian President Vladimir Putin signed the Comprehensive Strategic Partnership for a New Era, a wide-ranging bilateral agreement to deepen cooperation across energy, military, and trade. The pact emphasizes resistance to U.S.-led “hegemonic bullying” and outlines joint opposition to Western containment strategies. Xi described the partnership as a “friendship of steel,” highlighting mutual support amid rising global tensions. The leaders pledged to significantly expand trade and investment by 2030, with China committed to bolstering Russia’s sanctions-hit economy. Their joint statement also called for a new multipolar global order. Observes noted that Xi’s presence during Russia’s Victory Day celebrations reinforced solidarity, while both leaders reiterated that resolving the Ukraine war requires addressing NATO’s role—echoing Russia’s narrative.

Canada April Labor Market Report – +5k expected change in employment, unemployment rate expected to rise to 6.8% and wage growth falling to 3.3%.

Hoover Monetary Policy Conference – Federal Reserve’s Williams and Waller on panel session “John Taylor and Taylor Rules in Policy.”

Mood: iFlow Mood continues to normalise with rising equity buying momentum with sign of easing of demand in sovereign bonds.

FX: Significant outflows in JPY, ILS while strong inflows in CAD and GBP. Elsewhere, EUR inflow continue, and EUR scored holdings recent highs. APAC currencies inflows slowed with aggregate scored holding dipped marginally below zero.

FI: Sovereign bonds flows were mixed with good demand observed in U.S. Treasurys. Elsewhere, notable flows were continued strong demand for Brazil sovereign vs selling of Chinese government bonds.

Equities: Good buying flows continued in APAC and EMEA against selling in Americas in both DM and EM space.

“A bishop must not be a little prince sitting in his kingdom” – Cardinal Robert Francis Prevost, now People Leo XIV

“Never ask the tightrope walker how he keeps his balance. If he stops to think about it, he falls off.” – Terry Pratchett, from A Hat Full of Sky

After three months of decline, Indonesia’s Consumer Confidence Index (CCI) rose to 121.7 in April, up from 121.1 in March, signalling renewed optimism. The Current Economic Condition Index (CECI) increased from 110.6 to 113.7, with sub-indices for job availability (101.6) and current income both showing gains. Confidence was strongest among consumers in their 20s (CCI: 126.4) and those spending over Rp 5 million/month (CCI: 127.9). The Consumer Expectation Index (CEI), however, fell from 131.7 to 129.8, with future job availability concerns (sub-index 123.5) weighing on sentiment. The saving-to-income ratio improved to 14.8%, while the average consumer spent 74.8% of income. This recovery in sentiment followed disappointing Q1 GDP growth of 4.87%, attributed partly to the absence of election-related stimulus. JCI +0.074% to 6832.803, USDIDR -0.122% to 16515, 10y IDGB -0.1bp to 6.859%.

Norway’s Producer Price Index (PPI) for manufactured goods rose by 3.2% year-on-year in April, down from 5.9% in March. The slowdown was driven mainly by export prices, which increased just 3.6% annually — down sharply from 10% in March — and fell by nearly 3% month-on-month. Price growth in the chemical industry dropped from over 30% in March to 4.4%, while refined petroleum products also recorded a notable deceleration. The gap between export and domestic market price growth, which had widened since late 2024, nearly vanished in April. Additionally, crude oil and gas extraction prices fell 11.5%, lowering the overall PPI growth to 2.1%. In contrast, electricity prices surged 19.4% year-on-year. The data reflect easing industrial inflation, especially in key export sectors. OSE -0.396% to 1508.12, EURNOK +0.264% to 11.682, 10y NGB +2.3bp to 3.988%.

In Q1 2025, Sweden’s Services Producer Price Index (SPPI) rose by 0.6% quarter-on-quarter and 2.2% year-on-year, with positive annual rates recorded across all markets. On a quarterly basis, prices increased 0.9% on the domestic market and 0.2% on the import market, while falling 1.1% on the export market. Annual growth was 2.5% for domestic, 1.9% for imports, and just 0.4% for exports. Sectors such as consultancy, engineering, and advertising contributed positively, while warehousing and sea transport dragged on export prices. Currency appreciation also influenced price developments. The data indicate modest but broad-based price increases in the Swedish service sector, with export-related services under some pressure. OMX +0.017% to 2449.627, EURSEK +0.394% to 10.8864, 10y Swedish GB +4.3bp to 2.366%.

Swedish household consumption in March fell by 0.4% month-on-month (seasonally adjusted) but rose 1.8% year-on-year (constant prices, working day adjusted). For Q1 overall, consumption was up 1.5% from the same period in 2024 and increased 0.7% from Q4 2024. The largest sector, housing, electricity, gas and heating, declined 1.4% from February but rose 0.3% annually. Retail trade (mostly food and beverages) was flat month-on-month but rose 1.9% year-on-year. However, unadjusted year-on-year figures show a 4.7% decline due to the Easter calendar shift from March in 2024 to April in 2025.

In March 2025, Sweden’s private sector production fell by 0.5% from February (seasonally adjusted) and declined 0.2% year-on-year (calendar adjusted). Industrial production dropped 1.6% month-on-month and 3.5% year-on-year, with the chemical and pharmaceutical industry seeing a sharp 15.2% monthly fall. However, motor vehicle manufacturing rose 9.9%, though still down 13.4% annually. Services production decreased 0.9% monthly but increased 0.7% compared to March 2024. The largest negative monthly contributor was information and communication services (–8.5%), while administrative and technical support services rose 1.9%. Construction output grew 1.0% from February and 2.2% year-on-year. Overall, the data show mixed sectoral trends, with notable weakness in manufacturing offset partly by resilience in construction and selected services.

Czech retail trade sales in March (excluding motor vehicles) rose 0.6% month-on-month in real terms. Sales of non-food goods increased 1.6%, and automotive fuel sales rose 1.2%, while food sales declined 1.0%. Year-on-year, retail sales grew 3.4%, led by strong increases in automotive fuel (+10.0%) and non-food goods (+5.1%), while food sales dipped 0.6%. Online and mail-order sales surged 16.1% and were key contributors to overall growth. Notable year-on-year increases were seen in cosmetics (+8.7%), medical goods (+6.1%), recreational goods (+5.4%), and information and communication equipment (+3.7%). Sales of household equipment fell 4.8%. In food retail, specialized store sales rose 0.9%, while non-specialized store sales declined 0.7%. Motor vehicle trade and repair increased 0.5% both monthly and annually. Prague SE +1.239% to 2129.67, EURCZK -0.073% to 24.939, 10y CZGB +3bp to 4.103%.

SECO Swiss consumer sentiment index fell to -42 points. This is 4 points lower than in April 2024. The economic outlook sub-index declined compared to April 2024, but some sub-indices were still higher compared to a year ago: past financial situation, financial outlook and moment to make major purchases. The decline will add to the urgency of the Swiss government to act on trade negotiations with Swiss President Karin Keller-Sutter announcing that Switzerland is among 15 countries selected by the United States for “privileged” negotiations. The U.S. has imposed a 31% tariff on Swiss imports, which is notably higher than the tariffs on goods from comparable economies like the European Union and Japan. SMI +0.195% to 12085.23, EURCHF -0.055% to 0.93453, 10y Swiss GB +4bp to 0.327%.

Turkey’s industrial production rose 3.4% month-on-month in March. By subsector, mining and quarrying increased 8.2%, manufacturing rose 3.7%, while electricity, gas, steam, and air conditioning supply declined 3.5%. Compared to March 2024, total industrial production grew steadily, with mining and quarrying up 4.9%, manufacturing increasing 2.0%, and electricity, gas, steam, and air conditioning supply rising 6.1%. These figures suggest broad-based annual growth, supported by a strong monthly rebound in extractive and manufacturing industries, though energy-related output remained volatile. The latest data reinforce a continuing recovery trend across key industrial components. BI 100 -0.457% to 9236.8, USDTRY -0.326% to 38.7503, 10y TGB -2bp to 34.76%.