Market Movers: Tax Day

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 8 minutes

• China orders airlines not to take further deliveries of U.S. Boeing jets, expanding trade war.

• U.S. Treasury Secretary Bessent gives priority to U.K., Australia, South Korea, and Japan on trade talks as the global auto equity indices trade higher on potential tariff exemptions, with Japan’s TOPIX Transportation Index up 3.6%, South Korea’s KRX Auto Index up 3.2%, EuroStoxx Auto up 2.4%.

• IEA cuts 2025 oil demand forecast due to tariffs, sees growth slowing into 2026, with lower energy prices not changing economics.

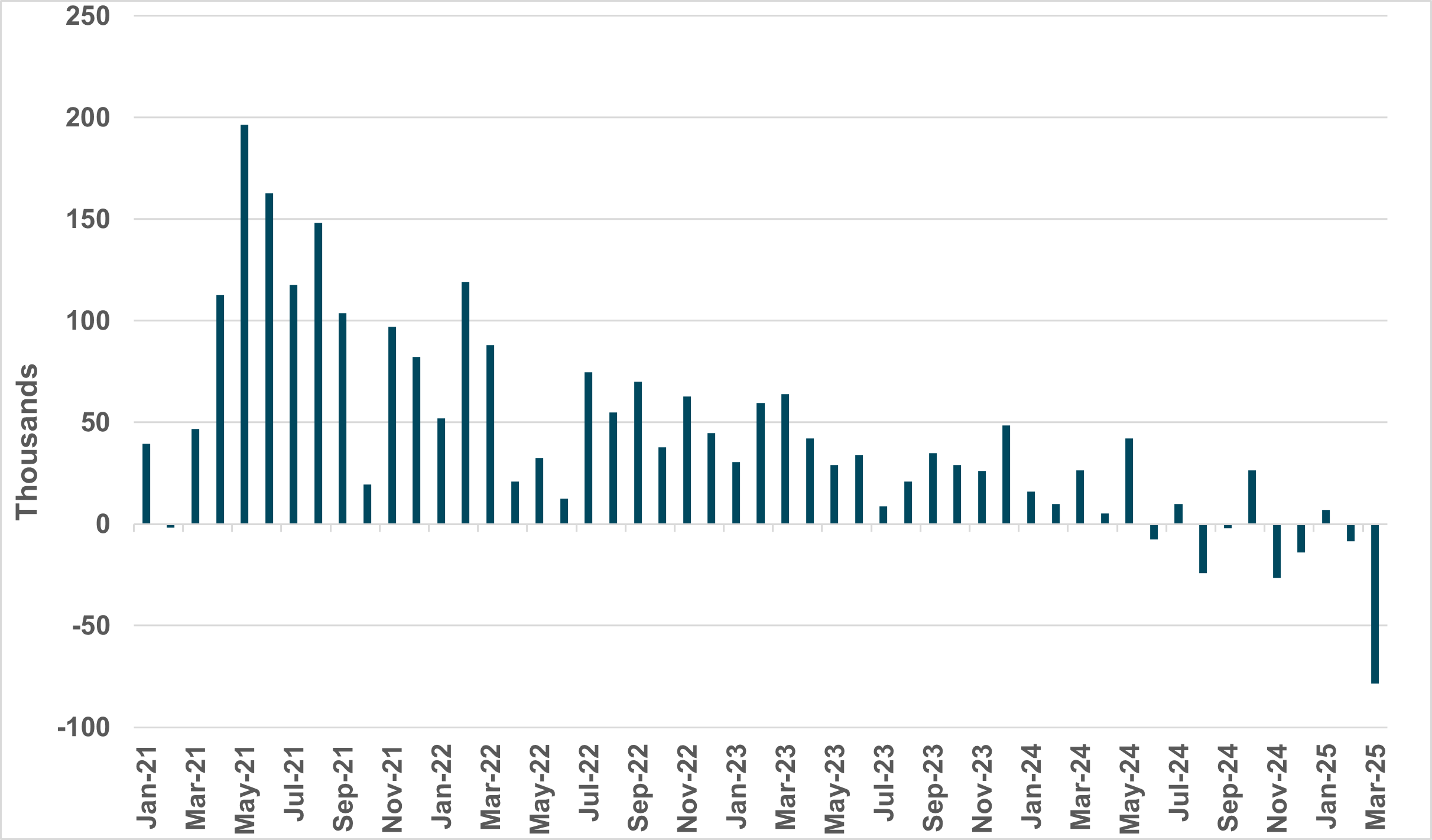

EXHIBIT #1: SHARP DROP IN U.K. PAYROLLED EMPLOYEES

Source: BNY

The sharp decline in U.K. payrolled employees in March adds to other losses. In six months, the U.K. has shed almost 100k jobs, opening the way for a material Bank of England policy change on rates.

Risk sentiment is mixed as trade policy continues to drive uncertainty. The Trump administration has started trade probes into semiconductor and pharmaceutical imports as the Commerce Department investigates the impact on U.S. national security. While neither the U.S. nor China are pushing for higher tariffs, selective signs of escalation continue with news that China halted deliveries of U.S.-made jets. The risks to industrial output globally are evident, with leading industrial surveys released today, such as the German ZEW, dropping the most since Russia invaded Ukraine, - and the U.S. Empire Manufacturing Index giving a clear indication of the risks to growth ahead. With off ramps to the trade conflict elusive, recessionary risk can only rise with oil and other commodity demand a key barometer. Futures continue to indicate a better session for U.S. equities on hopes for more tariff exemptions, but we should have learned by now that any relief is temporary. The lack of additional safety valves and diversification destinations is another challenge for markets. Other bond safe havens look fully positioned. Our data shows over the past week that flows were modest in larger AAA sovereigns such as Germany and Australia, while other supposedly well-funded places, such as Sweden, have seen outright outflows. The CHF valuations are now in question given the pace of the moves with SNB intervention, and Switzerland will also face disproportionate impact from tariffs on the pharmaceutical sector. Higher discount factors for U.S. assets, for now, are not translating into a premium for supposed alternatives. In the day ahead markets will be watching for volatility in funding costs, given it is Tax Day, and the squeeze in cash for payments could matter ahead of Fed Chair Powell’s speech tomorrow and the 20-year bond sale. The market will continue to struggle with lower volume and higher volatility until there is more information to identify the new equilibrium for the global economy.

The German ZEW Index collapsed to -14 from 51.6 against expectations of a decline to 10.0. This is the biggest drop in one month since Russia invaded Ukraine. The Current Situation Index improved slightly from -87.6 to -81.2, but forward figures will likely be much weaker. This is also the lowest figure since July 2023. Expectations for the Eurozone have also fallen sharply to -18.5, while large declines were registered for the U.S. (-48.7 to -71.5) and China (8.0 to -38.1). DAX up 1.46% to 21,260.74, 10y Bund 1.4bp lower to 2.498%, EURUSD 0.03% higher to 1.1354.

U.K. labor market data for March 2025 showed significant cooling, which will be welcome news for the Bank of England. The sharp drop in payrolled employees aside, the Office for National Statistics stated that job vacancies had declined to below pre-COVID levels. However, the unemployment rate held at 4.4% and wage growth was still robust at 5.9%, driven by public sector pay increases. FTSE up 0.8% to 8196.40, 10yr Gilt 1.8bp lower at 4.642%, GBPUSD 0.23% higher at 1.3320.

South Korea proposed increasing the size of an envisioned extra budget to KRW 12tn ($8.43bn) to support key industrial sectors amid an escalating trade war and respond to a surge in natural disasters. This is KRW 2tn more than previously proposed. KOSPI up 0.9%, 10yr KTB 4bp lower at 2.67%, KRW down 0.2% at 1428.

Reserve Bank of Australia April meeting keeps near-term rate cut hope alive, saying that May would be an opportune time to revisit policy setting. Overall, RBA expressed caution, noting that it was not yet possible to determine the timing of the next move in rates. ASX200 up 0.2%, 10yr ACGB 5bp lower at 4.35%, AUD up 0.6% at 0.635.

Japan 20yr JGB auction came in soft with 2.5bp tail versus 1.6bp in March and a lower bid/cover ratio at 2.96 (March: 3.46). That said, the new 20yr JGB did acquire a good premium, with auction yield at 2.349%, nearly 10bp lower compared with adjacent JGBs. The focus on Bank of Japan policy normalization adding to steeper curves for bonds continues. The implication for U.S. 20-year is key. Nikkei 0.8% higher, 10yr JGB 3bp higher at 1.37%, JPY down 0.1% at 143.29.

Singapore has called a general election for May 3rd. This will be the first electoral battle for the ruling People's Action Party (PAP) under current Prime Minister Lawrence Wong. Markets see this as a key political test for the new leader. STI up 1.95% to 3617.97, 10y SIGB 5.3bp lower to 2.52%, USDSGD up 0.03% to 1.3159.

U.S. April NY Fed Empire Manufacturing Index expected -13.5 after falling to -20.0 in March. Still watching for a bounce back in the industrial sector against a further tariff hit, with jobs and prices key.

Canada’s March CPI expected up 0.6% m/m, 2.6% y/y after 1.1% m/m, 2.6% y/y – with core CPI expected up 0.7% m/m, 2.8% after 2.7% y/y. Outsized results could complicate BOC’s easing path.

U.S. Import Price Index expected 0% m/m, 1.4% y/y – important given the surge in goods pre-tariff and weaker USD with Export Price Index expected 0% m/m, 1.8% y/y, after 2.1% y/y with focus on oil and natural gas effects.

Federal Reserve Governor Lisa D. Cook speaks at Cal Alumni Club in Washington D.C. with Q&A.

Mood: No signs of stabilization as the market dropped further into risk-off zone with safe haven demand for sovereign bonds and unwinding of equity risk exposure.

FX: Euro and GBP were sold amongst broad inflow pressure in G10. LatAm currencies were sold while mixed flows in EMEA and APAC. TRY posted the most outflow.

FI: EMEA and LatAm government bonds were sold against mixed flows in G10 and APAC. A notable highlight was cross-border selling of U.S. Treasuries versus buying of Eurozone government bonds.

Equities: EM APAC equities were sold most, especially in China and Hong Kong, as well as Swedish and UK equities. Within the U.S., utilities and real estate were bought against selling in the rest of the sectors, especially health care, materials and energy over the past week.

“In this world nothing can be said to be certain, except death and taxes.” – Benjamin Franklin

“It’s a privilege to pay taxes.” – Lewis Black

New Zealand March Food Price rose 0.5% m/m, and year-on-year accelerated higher to 3.5% from 2.4% y/y. Higher prices for the grocery food group and the meat, poultry, and fish group contributed most to the annual increase in food prices, up 5.1% and 5.3% y/y, respectively. Note that the upside inflation risk is within Reserve Bank of New Zealand (RBNZ) expectations and unlikely to sway RBNZ from further easing. RBNZ cut rates by 25bp to 3.5% and said that further reduction in OCR is appropriate. NZX50 down 0.8%, 10yr NZGB off 14bp to 4.59, NZD +0.6% at 0.591.

India March Wholesale Price Index dropped more than expected from 2.38% y/y to 2.05% y/y. The main drag is the lowering of primary articles prices at 0.76% y/y (Feb: 2.81%) while fuel & power is higher at 0.20% y/y (Feb: 0.71% y/y) and manufactured products at 3.07% y/y (Feb: 2.86%). Food Index, which consists of food articles from the primary articles group came in at 4.66% y/y from 5.94% in February 2025. Elsewhere, Indian March exports returned to positive growth at 0.7% y/y after 4 months of decline, while imports surged at 11.4% y/y (Feb: -16.3%). March trade deficit was $21.54bn. NIFTY up 2.1%, 10yr IGB 3bp lower at 6.41%, INR up 0.4% 85.71.

Indonesia March consumer confidence plunged to 2024 lows at 121.1. Looking into the details, income satisfaction is normal but the prospect for jobs compared to six months ago has deteriorated sharply at 100.3, the lowest since April 2022. JCI up 1.3%, 10yr INDOGB down 6bp to 6.97%, IDR down 0.2%16809.

UK March BRC Sales Like-for-Like steady at 0.9% y/y, mainly driven by pick up in non-food sales at 0.5% y/y (Feb: -0.1%). Sales gains linked to better weather while the annual rate hit by Easter timing last year.

German wholesale prices fell by 0.2%m/m, dragging annualized growth down to 1.3%. The Federal Statistical Office highlighted that the main reason for the year-on-year increase in wholesale prices (total) in March 2025 was higher prices in the wholesale of food, beverages, and tobacco, with prices up 4.4% from March 2024 on average. By contrast, the prices observed in the wholesale of computers and peripheral equipment were 5.6% lower than in March 2024. DAX up 1.46% to 21,260.74, 10y Bund 1.4bp lower to 2.498%, EURUSD +0.03% higher to 1.1354.

France March final CPI rises 0.2% m/m, 0.8% y/y after 0% m/m, 0.8% y/y – unrevised as expected. The HICP rose 0.2% m/m, 0.9% y/y after 0.1% m/m, 0.9% y/y also unrevised. Steeper declines in energy prices (-6.6% vs -5.8% in February) and manufactured goods (-0.2% after stability) were offset by rising prices in services (+2.3% vs +2.2%), particularly insurance, as well as food (+0.6% vs +0.3%), especially fresh products (+3.8% vs +1.8%). Meanwhile, tobacco prices rose at a slower pace (+4.1% vs +4.5%).

Eurozone February industrial production up 1.1% m/m, 1.2% y/y after 0.6% m/m, -0.5% y/y – better than the 0.3% m/m, -0.8% y/y expected. This is the first annualized rise in 21 months and the fastest monthly growth since August 2024, driven primarily by strong rebounds in the output of non-durable consumer goods (2.8% vs. -2.4% in January) and capital goods (0.8% vs. flat previously). Intermediate goods production also rose, though at a slower pace (0.3% vs. 1.4%). Meanwhile, output continued to decline for both energy products (-0.2% vs. -1.1%) and durable consumer goods (-0.3% vs. -1.5%), marking a second straight month of contraction.